Backtesting Lambda Value at Risk

Abstract

A new risk measure, Lambda value at risk (), has been recently proposed as a generalization of Value at risk (). appears attractive for its potential ability to solve several problems of . This paper provides the first study on the backtesting of .

We propose three nonparametric tests which exploit different features. Two tests are based on simple results of probability theory. One test is unilateral and is more suitable for small samples of observations. A second test is bilateral and provides an asymptotic result. A third test is based on simulations and allows for a more accurate comparison among computed with different assumptions on the asset return distribution.

Finally, we perform a backtesting exercise that confirms a higher performance of in respect to especially when it is estimated with distributions that better capture tail behaviour.

Keywords: backtesting, hypothesis testing, model validation, risk management.

JEL Codes: C12, C52, G32

1 Introduction

Risk measurement and its backtesting are matter of primary concern to financial industry. Value at risk () has become the most widely used risk measure. Despite its popularity, after the recent financial crisis, has been extensively criticized by academics and risk managers. Among these critics, we recall the inability to capture the tail risk and the lack of reactivity to market fluctuations. Thus, the suggestion of the Basel Committee, in the consultative document Fundamental review of the trading book (2013), is to consider alternative risk measures that are able to overcome the ’s weaknesses.

A new risk measure, Lambda Value at Risk (), has been introduced by a theoretical point of view by Frittelli, Maggis, and Peri (2014). is a generalization of the at confidence level . Specifically, considers a function instead of a constant confidence level , where is a function of the losses. Formally, given a monotone and right continuous function , the of the asset return is a map that associates to its cumulative distribution function the number:

| (1) |

This new risk measure appears to be attractive for its potential ability to solve several problems of . First of all, it seems to be flexible enough to discriminate the risk among return distributions with different tail behavior, by assigning more risk to heavy-tailed return distributions and less in the opposite case. In addition, may allow for a rapid changing of the interval of confidence when the market conditions change.

Recently, Hitaj, Mateus, and Peri (2015) proposed a methodology for computing and a first attempt of backtesting based on the hypothesis testing framework by Kupiec (1995). In this study, the accuracy of the model is evaluated by considering the maximum of the function as confidence level. However, the level of coverage provided by the model may not be constant at any time; hence, this method misses to assess the actual performance.

The objective of this paper is to propose the first theoretical framework for the backtesting of . We present three backtesting methodologies which exploit different features and may be used with different aims. Our tests evaluate if provides an accurate level of coverage, this means that the probability of a violation occurring ex-post actually coincides with the one predicted by the model. In respect to the hypothesis test proposed in Hitaj, Mateus, and Peri (2015), we consider a null hypothesis which better evaluates the benefits introduced by the flexibility. Our tests can be easily extended to allowing for a proper comparison among the two risk measures.

Two of these tests are based on simple test statistics whose distribution is obtained by applying results of probability theory. The first test is unilateral and provides more precise results for shorter backtesting time windows (e.g. 250 observations). The second test is bilateral and provides an asymptotic result that makes it more suitable for larger samples of observations.

We propose a third test that is inspired to the approach used by Acerbi and Szekely (2014) for the Expected Shortfall backtesting. Here, the distribution of the test statistic is obtained by Monte Carlo simulations. This test allows to better evaluate the impact of the assumption on the model generating data and compare different choices on the asset return distribution.

Finally, we conduct an empirical analysis where we experiment and compare the results of our backtesting proposals for , computed using the same dynamic benchmark approach proposed by Hitaj, Mateus, and Peri (2015). The backtesting exercise has been performed along six different time windows throughout all the global financial crisis (2006-2011).

2 and models

Let us consider a probability space , where the sigma algebra represents the information at time . We assume that is the random variable of the returns of an asset distributed along a real (unknown) distribution , i.e. , and it is forecasted by a model predictive distribution conditional to previous information, i.e. .

We can measure the risk of the asset return using the classical , by attributing to at time the following value:

| (2) |

The objective of this study is the alternative risk measure proposed by Frittelli, Maggis, and Peri (2014), , that attributes to at time the following value:

| (3) |

where is a monotone function that maps in with and . When is constant and equal to for any , coincides with at confidence level . The interesting feature of is the sensitivity to tail risk, in particular, it is able to discriminate the risk of assets having the same at some level but different tail behavior. Thus, may allow to enhance the capital requirement in case of expected greater losses.

Hitaj, Mateus, and Peri (2015) proposed a method to compute the function that is called dynamic benchmark approach. Here, the function is taken as proxy of the tails of the market return distribution. This feature allows to assess the different asset reactions in respect to the market by detecting different confidence levels. This approach is also dynamic since is re-estimated at each time according the information in . In this way, incorporates the recent market fluctuations and adjusts the confidence level according the different asset reactions.

The authors proposed different models to compute . One proposal is to obtain by linear interpolation of points for any and fix constantly equal to the lower (upper) bound for any and to the upper (lower) bound for any in the increasing (decreasing) case. In their empirical analysis, the authors chose 4 points (). In particular, on the probability axis, they set the lower bound , the upper bound and the others values, with , by an equipartition of the interval . On the losses axis, they fix points equal to order statistics of the return distribution of some selected market benchmarks. Specifically, is equal to the minimum of all benchmark returns: where is the realized return of the -th benchmark, for and is the time horizon (i.e. number of days in the rolling window), and for and is the number of benchmarks; , , and are equal to the maximum, mean, and minimum of the benchmarks’ -, respectively.

In the next section, we will recall the first attempt of backtesting for , explain its limit and introduce our hypothesis test proposals.

3 and backtesting models

The Basel Committee on Banking Supervision (1996) refers to backtesting as the process of ”comparing daily profits and losses with model-generated risk measures to gauge the quality and accuracy of risk measurement systems”. A violation occurs when the risk measure estimate is not able to cover the realized return (profit and loss, PL). In the same Basel 2 Accord, the Commitee has also set up the first regulatory backtesting framework for the measure, known as traffic light approach. This procedure monitors the 1 violations over the last 250 days. Afterwards, many alternative proposals have been introduced in the literature for ; we refer to Campbell (2005), Christoffersen (2010), and Berkowitz et al. (2011) for a detailed review.

Let us denote with the realization of the asset return at time . In order to perform the backtesting of a risk measure, we need to construct the sequence of random variables representing the violations, , across days, as follows:

| (4) |

where is the return forecasted by the risk measure. The hit sequence is equal to 1 on day if the realized returns on that day, , is smaller than the value predicted by the risk measure at time for the day , i.e. or . If is not exceeded (or violated), then the hit sequence returns a 0. We observe that is a random variable that follows a Bernoulli distribution, that is:

| (5) |

where is the probability of having an exception at time .

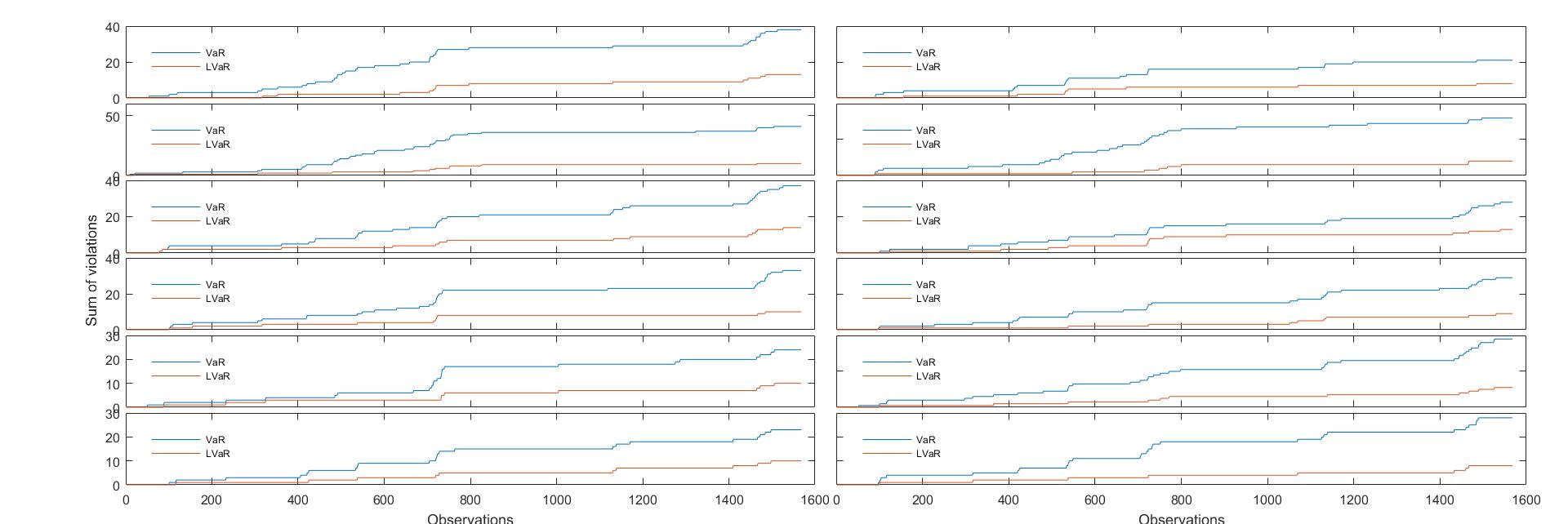

In the following, we focus on testing the unconditional coverage property of the risk measures that assumes the independence of the violations . A common practice in the industry is testing the independence by visual inspection of the cluster of the exceptions (see Acerbi and Szekely (2014), section 1). We conduct an empirical analysis with the available data which shows that clusters the exceptions considerably less than and suggests a higher level of independence of the exceptions (as shown in Figure (1)). The reason behind might be that is recalculated at each time incorporating the recent market movements and, in this way, it may avoid sequential violations. However, in order to have a complete assessment of the accuracy of a risk measure, a specific test of independence is required. In the case of , one cannot rely on the immediate extension of the framework since the exceptions are not identically distributed. This requires a more complex analysis that we leave for a future study.

The first theoretical proposal for the backtesting of is given by Kupiec (1995), where the author considers the following null and alternative hypothesis:

| (6) |

where is the confidence level. The at level is accepted if the frequency of the exceptions does not exceed the confidence level for any .

Recently, Hitaj, Mateus, and Peri (2015) have proposed a backtesting method for by adapting the classical Kupiec test for . They consider the following null and alternative hypothesis:

| (7) |

Substantially, is accepted if the frequency of violations is less than . This is an unilateral hypothesis test that can be conducted by using the same log-likelihood ratio and critical value of the test. This approach permits to verify if the coverage objective given by the maximum has been reached, however, it does not allow to evaluate the accuracy of at any time .

Indeed, if the model is correct, at time we should be expecting that the hit sequence assumes value 1 with probability

| (8) |

and 0 with probability . This intuition is correct if both and are continuous. In case this does not occur, we have .

As a consequence, the random variables of the violations for are not identically distributed, which implies that usual likelihood backtesting framework (POF by Kupiec 1995 , TUFF by Christoffersen 2010 etc.) cannot be directly applied.

Hence, if is correct, the null hypothesis should be:

| (9) |

while the alternative hypothesis, either:

| (10) |

in case of a bilateral test, or:

| (11) |

in case of an unilateral test where we reject in presence of risk under-estimation.

The null hypothesis in (9) allows to evaluate if guarantees the level of coverage predicted by the parameter. In this way, we are able to assess the correctness of more precisely than Hitaj, Mateus, and Peri (2015). Notice that a rejection of in (7) implies a rejection of in (9). Observe also that these hypothesis tests are also valid for at confidence level by fixing for any .

In order to test the accuracy of the model, we propose three test statistics. The distribution of the first two test statistics is obtained by exploiting simple results of probability theory. In particular, the second test provides an asymptotic result, hence it is more suitable for larger samples of observations (i.e. time horizon larger than 500).

We propose also a third test that is more useful to check if has been estimated with the correct distribution function, . Here, the correctness of the null hypothesis is evaluated by a simulation exercise.

We suggest that the first two tests are used for an initial validation of the model, while the third test is used as second step for selecting the best choice of estimation for the asset return distribution.

3.1 Test 1

We set the null and the alternative hypothesis as in (9) and (11), respectively. We construct this first test by defining the test statistic equal to the number of violations over the time horizon , as follows:

| (12) |

The distribution of is obtained by applying classical results of probability theory. If the violations independently occurs, the sum of independent Bernoulli with different mean follows a Poisson Binomial distribution , thus we have that under :

| (13) |

This test is in principle a bilateral test, with critical region: , where denotes the significance level of the test (i.e. 1 type error) and is the quantile of the distribution under , i.e. . However, in the backtesting practice, this test can be treated as unilateral, where the critical region is given by:

| (14) |

Indeed, the probability that falls in the left side of the critical region is null, since is zero any time the following relation is satisfied: . This is typical for usual test significance levels ( or lower), usual time horizon and - or - (since ).

This test represents an extension of the traffic light approach by Basel Committee on Banking Supervision (1996) to with two bands instead of three. In particular, for at confidence level , under we have:

that is follows a Binomial distribution. In the empirical analysis we fix and we compare the results with .

3.2 Test 2

We propose a second test statistic that is founded on a result of probability theory known as Lyapunov theorem. We set the null and the alternative hypothesis as in (9) and (10), respectively. We propose another test statistic defined as follows:

| (15) |

Under , is asymptotically distributed as a Standard Normal, formally:

| (16) |

This result follows from the application of Lemma 2 and the Lyapunov’s theorem (see Appendix for details).

We remark that this is a bilateral test. Thus, we reject the null hypothesis if the realization of the test statistic stays in the following critical region:

| (17) |

where is the significance level of the test, and is the quantile function of the Standard Normal distribution .

Also for this test, in the empirical analysis, we fix and we compare the results with .

3.3 Test 3

The third test is inspired by Acerbi and Szekely (2014) and focused on another aspect. The aim of this test is to directly verify if has been estimated under the correct assumption on the distribution of the returns. To this purpose we build a test statistic, , and we proceed by simulating its distribution using the same assumption as for the asset return distribution in the risk measure computation.

We set the null and the alternative hypothesis as in (9) and (11), respectively, and we define as follows:

| (18) |

We observe that under , we have , while under , for (see Proposition (3) in Appendix). So, if the model is correct the realized value is expected to be zero. On the other hand, a negative is a signal that the model estimation does not allow for covering the risk.

Under the distribution of depends on the assumption for the distribution of the asset returns. Hence, we perform the test by simulating scenarios of the distribution of the returns at each time , with . In this way, we obtain at time the distribution of the test statistic under . In order to construct the critical region we need to study the behavior of when the distribution of the returns changes from to . Let us compute :

where is distributed as a Binomial Poisson of parameter . We observe that is an increasing function of (i.e. shifts to left when increases). As a consequence, given a significance level , we reject the null hypothesis when the p-value is smaller than .

In the empirical analysis we conduct simulations using the same assumptions on the asset return distribution as for the risk measures computation. We set the test significance level at .

This test allows to verify how the choice of the asset return distribution influences the risk coverage capacity of , that, instead, is not directly assessed by Test 1 and Test 2. Hence, the best use of Test 3 is comparing the results between the same kind of models, but estimated with different assumptions on the PL distribution (i.e. Historical, Montecarlo Normal and GARCH, etc.).

The limit of this test is that requires a massive storage of information, since at time we need all the predictive distributions of the returns for .

4 Empirical analysis

In this section, we provide an empirical analysis of the backtesting methods of that we have defined in Section (3). We applied the tests to a slightly different version of the models proposed in Hitaj, Mateus, and Peri (2015) and to the model. We compare the backtesting results with the Kupiec-type test proposed in Hitaj, Mateus, and Peri (2015) for and with the classical Kupiec’s test for .

We refer to the same dataset as in Hitaj, Mateus, and Peri (2015), consisting in daily data of 12 stocks quoted in different countries along different time windows throughout the global financial crisis (specifically, from January 2005 to December 2011). These comprise the stocks of Citigroup Inc. (C UN Equity) and Microsoft Corporation (MSFT UW Equity) for the United States, Royal Bank of Scotland Group PLC (RBS LN Equity) and Unilever PLC (ULVR LN Equity) for the United Kingdom, Volkswagen AG (VOW3 GY Equity) and Deutsche Bank AG (DBK GY Equity) for Germany, Total SA (FP FP Equity) and BNP Paribas SA (BNP FP Equity) for France, Banco Santander SA (SAN SQ Equity) and Telefonica SA (TEF SQ Equity) for Spain, and Intesa Sanpaolo SPA (ISP IM Equity) and Enel SPA (ENEL IM Equity) for Italy. The market benchmarks for the computation have been chosen among the market indexes with the highest volume of exchanges; these are SP500, FTSE 100, and EURO STOXX 50.

The computation of the risk measures is based on different assumptions on the distribution of the asset returns. We consider the classical Historical and Normal simulation approach and we add robustness to the analysis by implementing GARCH models with t-student increments and the Extreme Value Theory (EVT) method based on the generalised Pareto distribution (we remand to McNeil (1999) for a review on this method). The estimation of the parameters is based on 250 days of observations for the Historical and Normal assumption, while 500 days are considered for the GARCH model. For the Extreme Value Theory method, we implement an automatic routine to identify the threshold in the different time windows.

The backtesting exercise is conducted comparing the realized ex-post daily returns with the daily and estimates of the 12 stocks over the time period of 1 year. In particular, we split the analysis into six different 2-year time windows (250 days for the risk measure computation and 1 year for the backtesting).

4.1 Results

4.1.1 Violations and Kupiec test

We first report the results of the violations and the Kupiec test for the model and the Kupiec-type test adapted by Hitaj, Mateus, and Peri (2015) for the model. We compute the average number of violations and acceptance rate over all the assets and different time horizon . The results presented, hereafter, in Table (1) are under the assumption of Historical distribution of the asset returns.

| Average number of violations | Kupiec-Test | |||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | |||

| VaR | 1% | 3.42 | 5.33 | 11.58 | 0.75 | 3.08 | 6.83 | 100 % | 83 % | 0 % | 100 % | 92 % | 50 % | |

|

|

3.42 | 5.33 | 11.58 | 0.75 | 3.08 | 6.83 |

|

100% | 83% | 0% | 100% | 92% | 50% | |

| (decr) | (VaR 5%) | 2.25 | 3.67 | 7.00 | 0.67 | 2.00 | 4.25 | 100 % | 83 % | 42 % | 100 % | 100 % | 83 % | |

| (VaR 1%) | 2.17 | 2.33 | 5.75 | 0.67 | 1.58 | 4.00 | 100 % | 83 % | 67 % | 100 % | 100 % | 83 % | ||

|

|

2.21 | 3.00 | 6.38 | 0.67 | 1.79 | 4.13 |

|

100 % | 83 % | 54 % | 100 % | 100 % | 83 % | |

| (incr) | (VaR 5%) | 1.17 | 1.00 | 3.92 | 0.42 | 0.92 | 2.75 | 100 % | 100 % | 100 % | 100 % | 100 % | 100 % | |

| (VaR 1%) | 1.17 | 1.08 | 3.92 | 0.42 | 1.00 | 2.75 | 100 % | 100 % | 100 % | 100 % | 100 % | 100 % | ||

|

|

1.17 | 1.04 | 3.92 | 0.42 | 0.96 | 2.75 |

|

100 % | 100 % | 100 % | 100 % | 100 % | 100 % | |

As expected and already pointed out in Hitaj, Mateus, and Peri (2015) the average number of violations of is bigger than the one of , in particular if compared with the increasing models. In fact shows a drastic increase in the average number of violations, moving from 3.42 in 2006 to 11.58 in 2008. On the other hand, the increasing models register an average number of violations of around 1.17 during 2006 and retain the number at around 3.92 in the 2008 crisis.

This result was expected since the function has been built with , which implies that is always greater or equal than , so that, losses not covered by the first are also not covered by the latter. This implies that performs always better than by using an unilateral Kupiec-type test, since this kind of test does not capture the variability of the function that is the essential feature of .

The violations trend is the same also under the other distribution’s assumptions taken in exam as shown in Table (2).

| Normal | GARCH | EVT | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | ||

| VaR | 1% | 4.58 | 7.08 | 14.92 | 1.75 | 4.17 | 9.42 | 3.17 | 6.83 | 8.25 | 0.33 | 0.75 | 4.33 | 3.42 | 5.33 | 11.58 | 0.83 | 3.08 | 6.92 |

| 4.58 | 7.08 | 14.92 | 1.75 | 4.17 | 9.42 | 3.17 | 6.83 | 8.25 | 0.33 | 0.75 | 4.33 | 3.42 | 5.33 | 11.58 | 0.83 | 3.08 | 6.92 | ||

| (decr) | (VaR 5%) | 4.42 | 6.75 | 14.25 | 1.58 | 3.75 | 9.17 | 3.08 | 5.83 | 7.33 | 0.33 | 0.42 | 4.25 | 2.33 | 2.33 | 7.25 | 0.75 | 1.75 | 4.25 |

| (VaR 1%) | 4.25 | 5.83 | 13.08 | 1.42 | 3.42 | 8.58 | 2.75 | 4.75 | 6.42 | 0.25 | 0.33 | 3.92 | 2.08 | 2.08 | 6.92 | 0.75 | 1.67 | 4.08 | |

| 4.33 | 6.29 | 13.67 | 1.50 | 3.58 | 8.88 | 2.92 | 5.29 | 6.88 | 0.29 | 0.38 | 4.08 | 2.21 | 2.21 | 7.08 | 0.75 | 1.71 | 4.17 | ||

| (incr) | (VaR 5%) | 3.33 | 4.75 | 10.83 | 0.92 | 2.75 | 6.67 | 1.25 | 2.67 | 3.58 | 0.00 | 0.17 | 1.42 | 1.25 | 1.00 | 4.25 | 0.42 | 0.92 | 2.75 |

| (VaR 1%) | 3.33 | 5.08 | 11.67 | 1.17 | 3.00 | 7.00 | 1.25 | 2.83 | 3.50 | 0.00 | 0.33 | 1.42 | 1.25 | 1.25 | 4.33 | 0.42 | 1.00 | 2.75 | |

| 3.33 | 4.92 | 11.25 | 1.04 | 2.88 | 6.83 | 1.25 | 2.75 | 3.54 | 0.00 | 0.25 | 1.42 | 1.25 | 1.13 | 4.29 | 0.42 | 0.96 | 2.75 | ||

4.1.2 Test 1 and Test 2: comparison of and risk coverage

In Table (3) and (4) we show the results of Test 1 and 2 proposed in Section (3) for . The results here presented are under different assumptions of the distribution of the assets return, specifically, Historical, Normal, GARCH and EVT method.

| Historical | Normal | ||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | ||

| VaR | 1% | 100% | 58% | 0% | 100% | 75% | 25% | 58% | 33% | 0% | 92% | 50% | 8% |

| 100% | 58% | 0% | 100% | 75% | 25% | 58% | 33% | 0% | 92% | 50% | 8% | ||

| (decr) | (VaR 5%) | 100 % | 75 % | 17 % | 100 % | 92 % | 67 % | 42% | 8% | 0% | 83% | 50% | 8% |

| (VaR 1%) | 92 % | 83 % | 25 % | 100 % | 100 % | 75 % | 33% | 25% | 0% | 92% | 42% | 8% | |

| 96% | 79% | 21% | 100% | 96% | 71% | 38% | 17% | 0% | 88% | 46% | 8% | ||

| (incr) | (VaR 5%) | 75 % | 83 % | 0 % | 100 % | 83 % | 25 % | 0 % | 0 % | 0 % | 42 % | 33 % | 8 % |

| (VaR 1%) | 75 % | 83 % | 0 % | 100 % | 75 % | 17 % | 8 % | 8 % | 0 % | 42 % | 42 % | 8 % | |

| 75% | 83% | 0% | 100% | 79% | 21% | 4% | 4% | 0% | 42% | 38% | 8% | ||

| GARCH | EVT | ||||||||||||

| VaR | 1% | 75% | 50% | 33% | 100% | 100% | 67% | 100% | 58% | 0% | 100% | 75% | 25% |

| 75% | 50% | 33% | 100% | 100% | 67% | 100% | 58% | 0% | 100% | 75% | 25% | ||

| (decr) | (VaR 5%) | 75% | 50% | 33% | 100% | 100% | 67% | 100 % | 92 % | 8 % | 100 % | 92 % | 50 % |

| (VaR 1%) | 67% | 67% | 33% | 100% | 100% | 67% | 100 % | 92% | 8 % | 100 % | 100 % | 58 % | |

| 71% | 58% | 33% | 100% | 100% | 67% | 100% | 92% | 8% | 100% | 96% | 54% | ||

| (incr) | (VaR 5%) | 67% | 58% | 25% | 100% | 92% | 58% | 67 % | 83 % | 0 % | 100 % | 83 % | 17 % |

| (VaR 1%) | 75% | 50% | 25% | 100% | 92% | 58% | 67 % | 67 % | 0 % | 100 % | 75 % | 25 % | |

| 71% | 54% | 25% | 100% | 92% | 58% | 67% | 75% | 0% | 100% | 79% | 21% | ||

| Historical | Normal | ||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | ||

| VaR | 1% | 100 % | 75 % | 0 % | 100 % | 92 % | 42 % | 58% | 42% | 0% | 100% | 67% | 25% |

| 100% | 75% | 0% | 100% | 92% | 42% | 58% | 42% | 0% | 100% | 67% | 25% | ||

| (decr) | (VaR 5%) | 100% | 83% | 17% | 100% | 100% | 75% | 58% | 42% | 0% | 100% | 67% | 17% |

| (VaR 1%) | 100% | 83% | 42% | 100% | 100% | 83% | 50% | 50% | 0% | 100% | 67% | 17% | |

| 100% | 83% | 29% | 100% | 100% | 79% | 54% | 46% | 0% | 100% | 67% | 17% | ||

| (incr) | (VaR 5%) | 100% | 100% | 17% | 100% | 92% | 42% | 17% | 25% | 0% | 92% | 50% | 8% |

| (VaR 1%) | 100% | 100% | 17% | 100% | 92% | 42% | 25% | 33% | 0% | 83% | 58% | 25% | |

| 100% | 100% | 17% | 100% | 92% | 42% | 21% | 29% | 0% | 88% | 54% | 17% | ||

| GARCH | EVT | ||||||||||||

| VaR | 1% | 83% | 58% | 42% | 100% | 100% | 67% | 100 % | 75 % | 0 % | 100 % | 92 % | 33 % |

| 83% | 58% | 42% | 100% | 100% | 67% | 100% | 75% | 0% | 100% | 92% | 33% | ||

| (decr) | (VaR 5%) | 83% | 58% | 33% | 100% | 100% | 67% | 100 % | 92 % | 8 % | 100 % | 100 % | 67 % |

| (VaR 1%) | 92% | 75% | 42% | 100% | 100% | 75% | 100 % | 92 % | 17 % | 100 % | 100 % | 67 % | |

| 88% | 67% | 38% | 100% | 100% | 71% | 100% | 92% | 13% | 100% | 100% | 67% | ||

| (incr) | (VaR 5%) | 92% | 75% | 67% | 100% | 100% | 83% | 100 % | 100 % | 17 % | 100 % | 92 % | 42 % |

| (VaR 1%) | 92% | 67% | 67% | 100% | 92% | 83% | 100 % | 92 % | 17 % | 100 % | 92 % | 42 % | |

| 92% | 71% | 67% | 100% | 96% | 83% | 100% | 96% | 17% | 100% | 92% | 42% | ||

We first notice that the acceptance rate of these tests is lower than the unilateral Kupiec test in Hitaj, Mateus, and Peri (2015). This is due to the particular construction of the Kupiec test. Indeed, this test is useful to assess if the model guarantees an acceptable coverage given by , but cannot capture the daily variations of the confidence level of . Thus, it cannot be used to evaluate the real coverage offered by at time . On the other hand, the coverage tests that we have proposed are able to better evaluate if the flexibility introduced by the function helps to detect adverse scenario and put aside a more adequate amount of capital.

If we compare the tests results, we observe that for all the models Test 2 provides higher acceptance rates in respect to Test 1. This may be due to the fact that Test 1 returns more precise results with smaller number of observations and also to its unilateral nature that attributes the highest weight to the violations.

With the exception of the normal estimator, the models result often more accurate than , confirming the outcomes in Hitaj, Mateus, and Peri (2015). This means that the highest flexibility of contributes to the highest coverage, especially when it is computed with distributions that better capture the tail behaviour. In our tests, the decreasing models seem to be more accurate, in contrast with the results of the Kupiec test. We think this is a consequence of a lower power of these tests for the decreasing models. We remand the analysis of the test power for further research since it would complicate this study without adding significant value.

4.1.3 The choice of the minimum

During the analysis of the results, Test 1 and Test 2 have pointed out an issue of estimation in the models proposed by Hitaj, Mateus, and Peri (2015). In particular, the authors do not discuss in details the choice of the minimum, , that seems to be set equal to after empirical experimentations. In addition, the extended Kupiec test proposed by the authors could not identify the impact of this choice.

When we have run for the first time Test 1 and 2 using the choice of Hitaj, Mateus, and Peri (2015), , we have noticed that the increasing models presented the highest rejection rate, even if they had the smallest number of infractions, as shown by Table (5).

| Test 1 | Test 2 | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | |||

| (decr) | (VaR 5%) | 100 % | 75 % | 8 % | 100 % | 92 % | 67 % | 100 % | 83 % | 17 % | 100 % | 100 % | 75 % | |

| (VaR 1%) | 92 % | 83 % | 25 % | 100 % | 100 % | 67 % | 100 % | 83 % | 42 % | 100 % | 100 % | 83 % | ||

|

|

96 % | 79 % | 17 % | 100 % | 96 % | 67 % |

|

100 % | 83 % | 29 % | 100 % | 100 % | 79 % | |

| (incr) | (VaR 5%) | 8 % | 17 % | 0 % | 58 % | 42 % | 8 % | 75 % | 83 % | 0 % | 100 % | 75 % | 17 % | |

| (VaR 1%) | 8 % | 17 % | 0 % | 58 % | 42 % | 8 % | 75 % | 83 % | 0 % | 100 % | 83 % | 25 % | ||

|

|

8 % | 17 % | 0 % | 58 % | 42 % | 8 % |

|

75 % | 83 % | 0 % | 100 % | 79 % | 21 % | |

Thus, we have studied how the probability of infraction evolves in the different models and we have observed that in most of the cases it obtains the minimal value. This happens especially during crisis periods, when the cumulative distribution function of the assets shifts on the left and intersects the function at the minimum level. In such a case, the choice of the minimum is relevant and also a critical issue.

From our point of view, the minimum should provide the probability to lose more than the worst case event (i.e. benchmarks’ minimum, ) over the time window observations (i.e. 250 in our case). If we consider all the events equally probable, the selection of the minimum should be greater than over observations. Thus, we propose to compute the models by fixing the minimum equal to , i.e. , since the probability of an event over 250 past realizations is .

The results of the estimations with minimum have been shown before in Table (3) and (4). The number of infractions does not change in any period under consideration, while the acceptance rate of the increasing models drastically increases, validating our choice. Clearly, this new setting does not affect the decreasing models. Anyway, the choice of the minimum can be refined considering more precise evaluation of the probability of the worst case event, but this is beyond the objective of this paper.

4.1.4 Test 3: comparison of with different distribution estimations

As anticipated in Section (3), the best use of Test 3 is the comparison of the accuracy of the risk measures computed with different estimations of asset return distribution. We compute the time evolution of the acceptance rate aggregated at the level of the increasing and decreasing models. We repeat the analysis changing the assumption on the asset return distribution: specifically, Historical, Monte Carlo Normal, GARCH and EVT method. The results are presented in Table (6)

| Historical | Normal | ||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | ||

| VaR | 1% | 50% | 33% | 0% | 100% | 58% | 25% | 58% | 33% | 0% | 92% | 50% | 8% |

| 50% | 33% | 0% | 100% | 58% | 25% | 58% | 33% | 0% | 92% | 50% | 8% | ||

| (decr) | (VaR 5%) | 50% | 33% | 0% | 100% | 67% | 17% | 58% | 42% | 0% | 92% | 58% | 17% |

| (VaR 1%) | 58% | 50% | 8% | 100% | 67% | 8% | 50% | 33% | 0% | 92% | 58% | 25% | |

| 54% | 42% | 4% | 100% | 67% | 13% | 54% | 38% | 0% | 92% | 58% | 21% | ||

| (incr) | (VaR 5%) | 8% | 17% | 0% | 58% | 42% | 0% | 17% | 17% | 0% | 92% | 50% | 8% |

| (VaR 1%) | 8% | 17% | 0% | 58% | 42% | 8% | 33% | 8% | 0% | 83% | 50% | 17% | |

| 8% | 17% | 0% | 58% | 42% | 4% | 25% | 13% | 0% | 88% | 50% | 13% | ||

| GARCH | EVT | ||||||||||||

| VaR | 1% | 75% | 58% | 33% | 100% | 100% | 67% | 50 % | 33 % | 0 % | 100 % | 58 % | 25 % |

| 75% | 58% | 33% | 100% | 100% | 67% | 50% | 33% | 0% | 100% | 58% | 25% | ||

| (decr) | (VaR 5%) | 75% | 58% | 33% | 100% | 100% | 67% | 67 % | 58 % | 0 % | 92 % | 58 % | 42 % |

| (VaR 1%) | 92% | 67% | 33% | 100% | 100% | 75% | 67 % | 58 % | 0 % | 92 % | 58 % | 33 % | |

| 83% | 63% | 33% | 100% | 100% | 71% | 67% | 58% | 0% | 92% | 58% | 38% | ||

| (incr) | (VaR 5%) | 83% | 67% | 67% | 100% | 100% | 83% | 17 % | 25 % | 8 % | 58 % | 42 % | 0 % |

| (VaR 1%) | 83% | 58% | 67% | 100% | 92% | 83% | 17 % | 33 % | 0 % | 58 % | 42 % | 8 % | |

| 83% | 63% | 67% | 100% | 96% | 83% | 17% | 29% | 4% | 58% | 42% | 4% | ||

The results show that the GARCH assumption on the returns guarantees the highest accuracy in terms of average acceptance rate. Moreover, we notice here that the Historical and the EVT estimators of the increasing often underperform the Normal one, in contrast with the previous tests. These outcomes are quite reasonable since this third test is based on simulations and points out the issue of estimating risk measures with distributions having cut-off tails (as the Historical) or based on a small range of values (as the EVT). However, such a preference for the Normal distribution is completely reversed by the other tests which privilege the assumption of distributions which rely more on tail events and not on the full shape of the distribution.

5 Conclusions

A new risk measure sensitive to tail risk, , has been recently introduced. However, an ad hoc study on its backtesting has not been conducted in literature so far. The main issue for the backtesting is that the probability of a violation is not constant, but may change at any time and for any asset. This consideration implies that the Kupiec-type backtesting framework, proposed by Hitaj, Mateus, and Peri (2015), fails to keep into account the effective predictive capacity of as introduced by the function.

We propose three backtesting methodologies for and we asses the accuracy of the new risk measure from different points of view. Test 1 and Test 2 are based on results of probability theory and allow for a straightforward application. Test 3 is performed by simulations and allows for more accurate comparison of models estimated under different assumptions on the PL distribution.

The validity of our backtesting proposals is confirmed by the results of the empirical analysis. In fact, this study shows that models perform better than , confirming the findings in Hitaj, Mateus, and Peri (2015). In addition, computed with the GARCH model of returns has the highest level of coverage. This outcome substantiates what is well known in literature that fat-tailed asset return distributions explain better the real asset return behavior and allow for a more accurate risk coverage.

Moreover, our backtesting methods denote higher precision than the Kupiec-type test proposed by Hitaj, Mateus, and Peri (2015) since they have been able to detect an estimation issue of computed with a lower bound of as in the former study.

Suggestions for future research include the study of the test power that would permit a more accurate comparison among these backtesting proposals.

Appendix

We recall hereafter the Lyapunov Theorem that is a result of probability theory based on the application of the central limit theorem to random variables that are independent but not identically distributed (see Lyapunov 1954).

Theorem 1 (Lyapunov)

Suppose is a sequence of independent random variables, each with finite expected value and variance . Define

If for some , the “Lyapunov’s condition”

is satisfied, then the following convergence in distribution holds as goes to infinity:

In the following lemma we show that the “Lyapunov’s condition” is satisfied when and .

Lemma 2

If is a sequence of independent random variables distributed as a Bernoulli with parameters and , then

with .

Proof. We observe that:

On the other hand we have

We can thus conclude that

as .

The following proposition shows theoretical implications on the test statistic in (18) under the null and alternative hypothesis.

Proof. It is enough to notice that under , so that , which implies

In a similar way, under , since with , we obtain that .

References

- Acerbi and Szekely (2014) Acerbi, C., and B. Szekely. 2014. ”Back-testing Expected Shortfall.” Risk 27 (11).

- Berkowitz et al. (2011) Berkowitz, J., P. Christoffersen, and D. Pelletier. 2011. ”Evaluating Value-at-Risk Models with Desk-Level Data.” Management Science 57: 2213-2227.

- Basel Committee on Banking Supervision (1996) Basel Committee on Banking Supervision. 1996. ”Supervisory Framework for the Use of Backtesting in Conjunction with the Internal Models Approach to Market Risk Capital Requirements.” Bank for International Settlements.

- Fundamental review of the trading book (2013) Basel Committee on Banking Supervision. 2013. ”Fundamental Review of the Trading Book.” 2nd consultative document. Bank for International Settlements.

- Campbell (2005) Campbell, S. 2005. ”A Review of Backtesting and Backtesting Procedures.” Finance and Economics Discussion Series. Divisions of Research Statistics and Monetary Affairs, Federal Reserve Board, Washington D.C.

- Christoffersen (2010) Christoffersen, P. 2010. ”Encyclopedia of Quantitative Finance - Backtesting.” John Wiley and Sons.

- Frittelli, Maggis, and Peri (2014) Frittelli, M., M. Maggis, and I. Peri. 2014. ”Risk Measures on and Value at Risk with Probability/Loss Function.” Mathematical Finance 24 (3): 442-463.

- Hitaj, Mateus, and Peri (2015) Hitaj, A., C. Mateus, and I. Peri. 2015. ”Lambda Value at Risk and Regulatory Capital: a Dynamic Approach to Tail Risk.” Working paper available at http://ssrn.com/abstract=2932475.

- Kerkhof and Melenberg (2004) Kerkhof, J., and B. Melenberg. 2004. ”Backtesting for Risk-Based Regulatory Capital.” Journal of Banking Finance 28 (8): 1845-1865.

- Kupiec (1995) Kupiec, P. 1995. ”Techniques for Verifying the Accuracy of Risk Measurement Models.” Journal of Derivatives 3 (2): 73-84.

- Lyapunov (1954) Lyapunov, A. M. 1954. Collected Works 1.

- McNeil (1999) McNeil, A.J. 1999. ”Extreme Value Theory for Risk Managers.” Internal Modeling and CAD II. London: Risk Books, 93-113.