A continuous updating weighted least squares estimator of tail dependence in high dimensions

Abstract

Likelihood-based procedures are a common way to estimate tail dependence parameters. They are not applicable, however, in non-differentiable models such as those arising from recent max-linear structural equation models. Moreover, they can be hard to compute in higher dimensions. An adaptive weighted least-squares procedure matching nonparametric estimates of the stable tail dependence function with the corresponding values of a parametrically specified proposal yields a novel minimum-distance estimator. The estimator is easy to calculate and applies to a wide range of sampling schemes and tail dependence models. In large samples, it is asymptotically normal with an explicit and estimable covariance matrix. The minimum distance obtained forms the basis of a goodness-of-fit statistic whose asymptotic distribution is chi-square. Extensive Monte Carlo simulations confirm the excellent finite-sample performance of the estimator and demonstrate that it is a strong competitor to currently available methods. The estimator is then applied to disentangle sources of tail dependence in European stock markets.

Keywords: Brown–Resnick process; extremal coefficient; max-linear model; multivariate extremes; stable tail dependence function.

1 Introduction

Extreme value analysis has been applied to measure and manage financial and actuarial risks, assess natural hazards stemming from heavy rainfall, wind storms, and earthquakes, and control processes in the food industry, internet traffic, aviation, and other branches of human activity. The extension from univariate to multivariate data gives rise to the concept of tail dependence. The latter can and will be represented here by the stable tail dependence function, denoted by (Huang, 1992; Drees and Huang, 1998), or tail dependence function for short. Estimating this tail dependence function is the subject of this paper. Fitting tail dependence models for spatial phenomena observed at finitely many sites constitutes an interesting special case.

In high(er) dimensions, the class of tail dependence functions becomes rather unwieldy, and therefore we follow the common route of modelling it parametrically. Note that this is far from imposing a fully parametric model on the data generating process. In particular, we only assume a domain-of-attraction condition at the copula level. Parametric models for tail dependence have their origins in Gumbel (1960), and many models have since then been proposed, see, e.g., Coles and Tawn (1991), and more recently, Kabluchko et al. (2009).

Likelihood-based procedures are perhaps the most common way to estimate tail dependence parameters (Davison et al., 2012; Wadsworth and Tawn, 2014; Huser et al., 2015). Likelihood methods, however, are not applicable to models involving non-differentiable tail dependence functions. Such functions arise in max-linear models (Wang and Stoev, 2011), in particular factor models (Einmahl et al., 2012) or structural equation models based on directed acyclic graphs (Gissibl and Klüppelberg, 2015). Moreover, likelihoods can be hard to compute, especially in higher dimensions. This is why current likelihood methods are usually based on composite likelihoods, relying on pairs or triples of variables only, not exploiting information from higher-dimensional tuples.

It is the goal of this paper to estimate the true parameter vector of the tail dependence function and to assess the goodness-of-fit of the parametric model. The parameter estimator is obtained by comparing, at finitely many points in the domain of , some initial, typically nonparametric, estimator of the latter with the corresponding values of the parametrically specified proposals, and retaining the parameter value yielding the best match. The method is generic in the sense that it applies to many parametric models, differentiable or not, and to many initial estimators, not only the usual empirical tail dependence function but also, for instance, bias-corrected versions thereof (Fougères et al., 2015; Beirlant et al., 2015). Further, the method avoids integration or differentiation of functions of many variables and can therefore handle joint dependence between many variables simultaneously, more easily than the likelihood methods mentioned earlier and the M-estimator approach in Einmahl et al. (2016). This feature is particularly interesting for inferring on higher-order interactions, going beyond mere distance-based dependence models such as those frequently employed for spatial extremes. Finally, in those situations where likelihood methods are applicable, the new estimator is a strong competitor.

The distance between the initial estimator and the parametric candidates is measured through weighted least squares. The weight matrix may depend on the unknown parameter and is hence estimated simultaneously. The construction of the estimator bears some similarity with the continuous updating generalized method of moments (Hansen et al., 1996); the present estimator, however, is substantially different and does not use moments. Our flexible estimation procedure is related to that in Einmahl et al. (2016), but the continuous updating procedure is new in multivariate extreme value statistics.

We show that the weighted least squares estimator for the tail dependence function is consistent and asymptotically normal, provided that the initial estimator enjoys these properties too, as is the case for the empirical tail dependence function and its recently proposed bias-corrected variations. The asymptotic covariance matrix is a function of the unknown parameter and can thus be estimated by a plug-in technique. We also provide novel goodness-of-fit tests for the parametric tail dependence model based on a comparison between the nonparametric and the parametric estimators. Under the null hypothesis that the tail dependence model is correctly specified, the test statistics are asymptotically chi-square distributed.

The paper is organized as follows. In Section 2 we present the estimator, the goodness-of-fit statistic, and their asymptotic distributions. Section 3 reports on a Monte Carlo simulation study involving a variety of models, as well as a finite-sample comparison of our estimator with estimators based on composite likelihoods. An application to European stock market data is presented in Section 4, where we try to disentangle sources of tail dependence stemming from the country of origin (Germany versus France) and the economic sector (chemicals versus insurance), fitting a structural equation model. All proofs are deferred to the appendix.

2 Inference on tail dependence parameters

2.1 Setup

Let , , be random vectors in with a common cumulative distribution function and marginal cumulative distribution functions . The (stable) tail dependence function is defined as

| (2.1) |

for , provided the limit exists, as we will assume throughout. Existence of the limit is a necessary, but not sufficient, condition for to be in the max-domain of attraction of a -variate Generalized Extreme Value distribution. Closely related to is the exponent measure function , for . For more background on multivariate extreme value theory, see for instance Beirlant et al. (2004) or de Haan and Ferreira (2006).

The function is convex, homogeneous of order one, and satisfies for all . If , these properties characterize the class of all -variate tail dependence functions, but not if (Ressel, 2013). For any dimension , the collection of -variate tail dependence functions is infinite-dimensional. This poses challenges to inference on tail dependence, especially in higher dimensions.

The usual way of dealing with this problem consists of considering parametric models for , a number of which are presented in Section 3. Henceforth we assume that belongs to a parametric family with . Let denote the true parameter vector, that is, let denote the unique point in such that for all . Our aim is to estimate the parameter and to test the goodness-of-fit of the model.

Extremal coefficients are popular summary measures of tail dependence (de Haan, 1984; Smith, 1990; Schlather and Tawn, 2003). For non-empty , let be defined by

| (2.2) |

The extremal coefficients are defined by

| (2.3) |

The extremal coefficients can be interpreted as assigning to each subset the effective number of tail independent variables among .

2.2 Continuous updating weighted least squares estimator

Let denote an initial estimator of based on ; some possibilities will be described in Subsection 2.5. The estimators that we will consider depend on an intermediate sequence , that is,

| (2.4) |

The sequence will determine the tail fraction of the data that we will use for inference, see for instance Subsection 2.5.

Let , with for , be points in which we will evaluate and . Consider the column vectors

| (2.5) | ||||

| (2.6) |

where . The points need to be chosen in such a way that the map is one-to-one, i.e., is identifiable from the values of . In particular, we will assume that , where is the dimension of the parameter space . Since for any tail dependence function , any and any , we will choose the points in such a way that each point has at least two positive coordinates.

For , let be a symmetric, positive definite matrix with ordered eigenvalues and define

| (2.7) |

Our continuous updating weighted least squares estimator for is defined as

| (2.8) |

The set of minimizers could be empty or could have more than one element. The present notation, suggesting that there exists a unique minimizer, will be justified in Theorem 2.1. If all points are chosen as in (2.2) for some collection of different subsets of , each subset having at least two elements, then we will refer to our estimator as an extremal coefficients estimator.

We will address the optimal choice of below. The simplest choice for is the identity matrix , yielding an ordinary least-squares estimator

| (2.9) |

This special case of our estimator is similar to the estimator proposed in Nolan et al. (2015) in the more specific context of fitting max-stable distributions to a random sample from such a distribution.

2.3 Consistency and asymptotic normality

If is differentiable at an interior point , its total derivative will be denoted by . Differentiability of the map is a basic smoothness condition on the model; we do not assume differentiability of the map .

Theorem 2.1 (Existence, uniqueness and consistency).

Let , with , be a parametric family of -variate stable tail dependence functions. Let be points such that the map is a homeomorphism from to . Let the true -variate distribution function have stable tail dependence function for some interior point . Assume that is twice continuously differentiable on a neighbourhood of and that is of full rank; also assume that is twice continuously differentiable on a neighbourhood of . Assume . Finally assume, for , and for a positive sequence satisfying (2.4),

| (2.10) |

Then with probability tending to one, the minimizer in (2.8) exists and is unique. Moreover,

Theorem 2.2 (Asymptotic normality).

If in addition to the assumptions of Theorem 2.1, the estimator satisfies

| (2.11) |

for some covariance matrix , then, as ,

| (2.12) |

where the covariance matrix is defined by

and the matrices and are evaluated at .

Provided is invertible, we can choose in such a way that the asymptotic covariance matrix is minimal, say , i.e., the difference is positive semi-definite. The minimum is attained at and the matrix becomes simply

| (2.13) |

see for instance Abadir and Magnus (2005, page 339). Now extend the covariance matrix to the whole parameter space by letting the map be such that is an invertible covariance matrix and satisfies the assumptions on .

Corollary 2.3 (Optimal weight matrix).

The asymptotic covariance matrices and in (2.12) and (2.14), respectively, depend on the unknown parameter vector through the matrices , and evaluated at . If these matrices vary continuously with , then it is a standard procedure to construct confidence regions and hypothesis tests, cf. Einmahl et al. (2012, Corollaries 4.3 and 4.4).

2.4 Goodness-of-fit testing

It is of obvious importance to be able to test the goodness-of-fit of the parametric family of tail dependence functions that we intend to use. The basis for such a test is , the difference vector between the initial and parametric estimators of at the estimated value of the parameter.

Corollary 2.4.

The easiest case in which (2.15) can be exploited is when is invertible and . Then it suffices to consider the minimum attained by the criterion function in (2.7), i.e., the test statistic is just . Observe that it is important here that we allow to depend on .

Corollary 2.5.

Let . If the assumptions of Corollary 2.3 are satisfied, in particular if , then

If is different from , for instance when is not invertible, a goodness-of-fit test can still be based upon (2.15) by considering the spectral decomposition of the limiting covariance matrix. For convenience, we suppress the dependence on . Let

where is an orthogonal matrix, , the columns of which are orthonormal eigenvectors, and is diagonal, , with the corresponding eigenvalues, at least of which are zero, the rank of being . Let be such that and consider the matrix

where is an diagonal matrix and where is a matrix having the first eigenvectors as its columns.

Corollary 2.6.

If the assumptions of Theorem 2.2 hold and if is such that, in a neighbourhood of , and the matrix depends continuously on , then

2.5 Choice of the initial estimator

Our estimator in (2.8) is flexible enough to allow for various initial estimators, perhaps based on exceedances over high thresholds or rather on vectors of componentwise block maxima extracted from a multivariate time series (Bücher and Segers, 2014). Here we will focus on the former case, and more specifically on the empirical tail dependence function and a variant thereof.

For simplicity, we assume that the random vectors , are not only identically distributed but also independent, so that they are a random sample from . Let denote the rank of among for . For convenience, assume that is continuous.

Empirical stable tail dependence function

A natural estimator of is obtained by replacing and in (2.1) by their empirical counterparts and replacing by , yielding

| (2.16) |

This estimator, the empirical stable tail dependence function, was introduced for in Huang (1992) and studied further in Drees and Huang (1998). A slight modification of it allows for better finite-sample properties,

| (2.17) |

By Einmahl et al. (2012, Theorem 4.6), this estimator satisfies (2.11) under conditions controlling the rate of convergence in (2.1) and the growth rate of the intermediate sequence . The first-order partial derivatives of are assumed to exist and to be continuous in neighbourhoods of the points for which .

In this case, the entries of the matrix in (2.11), for in the interior of , are, for , given by

| (2.18) |

with and with a zero-mean Gaussian process with covariance function , the maximum being taken componentwise. For points of the form in (2.2), the expectation in (2.18) can be calculated as follows: for non-empty subsets and of ,

where and .

Bias-corrected estimator

A drawback of in (2.17) is its possibly quickly growing bias as increases. Recently, two bias-corrected estimators have been proposed. We consider here the kernel-type estimator of Beirlant et al. (2015), which is partly based on (the one in) Fougères et al. (2015).

Consider first a rescaled version of in (2.16), defined as for . Then define the weighted average

| (2.19) |

where is a kernel function, i.e., a positive function on such that .

In addition to (2.1), we assume there exist a positive function on tending to as and a non-zero function on such that for all ,

| (2.20) |

Moreover, we assume a third-order condition on (Beirlant et al., 2015, equation (3)). In Beirlant et al. (2015, Theorem 1) the asymptotic distribution of in (2.19) is derived under these three assumptions and for intermediate sequences growing faster than the ones considered above. A non-zero asymptotic bias term arises and the idea is to estimate and remove it, thereby obtaining a possibly more accurate estimator.

In order to achieve this bias reduction, the rate function, , and its index of regular variation, , need to be estimated. Consider another intermediate sequence such that . The bias-corrected estimator is then defined as

where and are the estimators of and defined in Beirlant et al. (2015). Under the mentioned conditions, asymptotic normality as in (2.11) holds, where the limiting random vector is equal in distribution to times the one corresponding to . Here, the growth rate of here can be taken faster than when using .

A simple choice for is a power kernel, i.e, for and . Then . Note that this factor tends to 1 if . In practice, we take as recommended in Beirlant et al. (2015).

3 Simulation studies

We conduct simulation studies for data in the max-domain of attraction of the logistic model, the Brown–Resnick process and the max-linear model. For each model, we report the empirical bias, standard deviation, and root mean squared error (RMSE) of our estimators. We also study the finite-sample performance of the goodness-of-fit statistic of Corollary 2.5. All simulations were done in the R statistical software environment (R Core Team, 2015).

3.1 Logistic model: comparison with likelihood methods

The -dimensional logistic model has stable tail dependence function

The domain-of-attraction condition (2.1) holds for instance if has continuous margins and its copula is Archimedean with generator , also known as the outer power Clayton copula (Hofert et al., 2015).

In Huser et al. (2015), a comprehensive comparison of likelihood estimators for has been performed based on random samples from this copula. We compare those results to our extremal coefficients estimator, i.e., the weighted least squares estimator based on points of the form , with ranging in the collection

| (3.1) |

for . Moreover, we let be the identity matrix, since by exchangeability of the model, a weighting procedure can bring no improvements.

Following Huser et al. (2015, Section 4.2), we simulated random samples of size from the outer power Clayton copula. For the likelihood-based estimators, the margins are standardized to the unit Pareto scale via the rank transformation

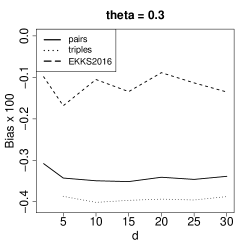

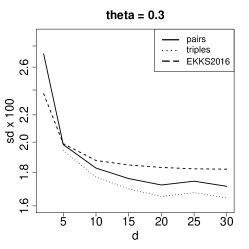

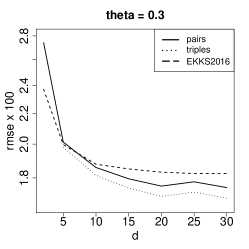

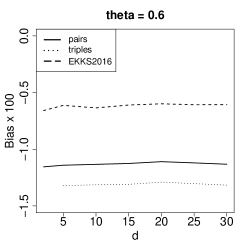

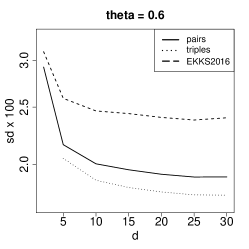

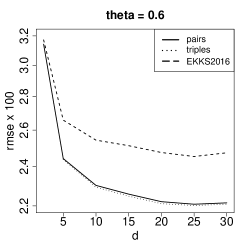

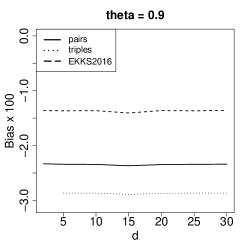

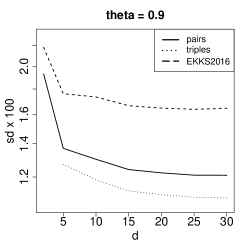

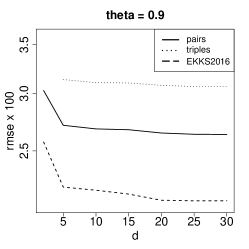

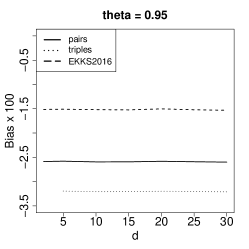

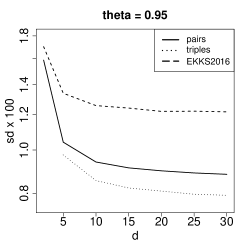

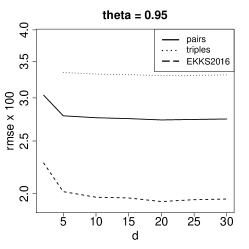

Again as in Huser et al. (2015, Section 4.2), we take dimension and parameter . Note that in the likelihood setting, this is a very demanding experiment, and three of the ten likelihood-based estimators considered in Huser et al. (2015) are only computed for . In Huser et al. (2015), threshold probabilities are set to , corresponding to in our setup.

Figure 1 shows the bias, standard deviation and RMSE of three estimators based on the empirical tail dependence function: the two extremal coefficient estimators mentioned above and the pairwise M-estimator of Einmahl et al. (2016) as implemented in the R package spatialTailDep (Kiriliouk and Segers, 2014). As the tuple size changes from pairs to triples, the absolute bias increases but the standard deviation decreases. When dependence is strong, , the gains in variance offset the losses in bias and the estimator based on performs best. Note also that when the dependence is not too weak, the estimators based on extremal coefficients perform better than the pairwise M-estimator of Einmahl et al. (2016). Finally, our estimation procedures have almost constant RMSE as the dimension increases, in line with the pairwise composite likelihood methods studied in Huser et al. (2015).

Comparing these results to the ten likelihood-based estimators in Huser et al. (2015, Figure 4), we see that our estimators are strong competitors in the sense that they rank highly when comparing RMSEs, and are not dominated by one of the likelihood-based estimators. More precisely, for , only the likelihood estimators based on the Poisson process representation (Coles and Tawn, 1991) and the multivariate Generalized Pareto distribution outperform our estimators; for , the same two likelihood estimators outperform ours, but only for ; finally, for and only the pairwise censored likelihood estimator (Huser and Davison, 2014) has a smaller RMSE than our estimators.

3.2 Brown–Resnick process

The Brown–Resnick process on a planar set is given by

| (3.2) |

where is a Poisson process on with intensity measure and are independent copies of a Gaussian process with stationary increments such that and with variance and semi-variogram . In Kabluchko et al. (2009) it is shown that the Brown–Resnick process with is the only possible limit of (rescaled) maxima of stationary and isotropic Gaussian random fields; here and .

For locations , the distribution of the random vector is max-stable with tail dependence function depending on . From Huser and Davison (2013), we obtain the following representation for the extremal coefficients in (2.3). Let denote the cumulative distribution function of the distribution. Then we have

where with , and where is a correlation matrix with entries given by

We simulate 300 random samples of size from the Brown–Resnick process on a unit distance grid using the R package SpatialExtremes (Ribatet, 2015). To arrive at a more realistic estimation problem, we perturb the samples thus obtained with additive noise, i.e., if is an observation from the Brown–Resnick process, then we set for and , where are independent random variables.

We estimate the parameters using the extremal coefficient estimator based on the subset of in (3.1) consisting of pairs of neighbouring locations, i.e., locations that are at most a distance apart. This leads to pairs. Including pairs of locations that are further away tends to drastically increase the bias (Einmahl et al., 2016).

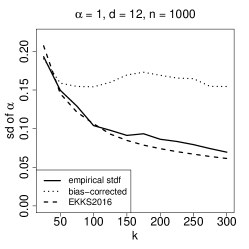

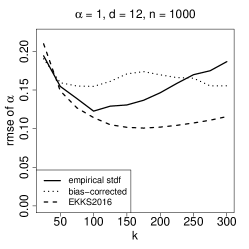

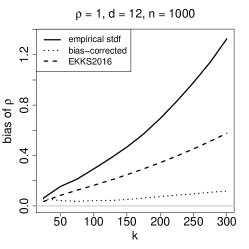

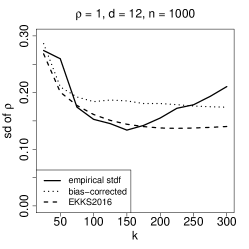

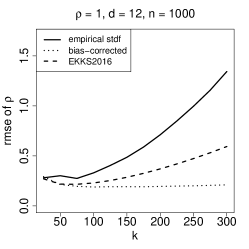

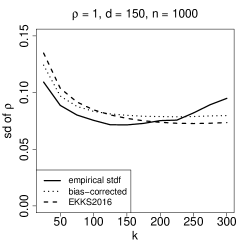

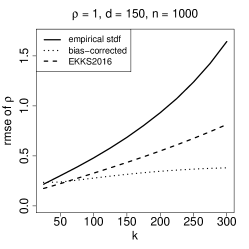

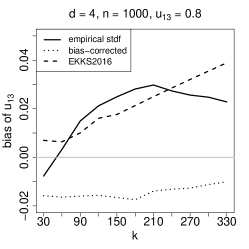

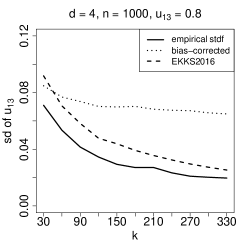

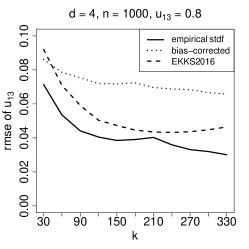

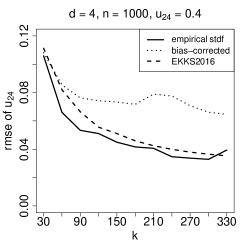

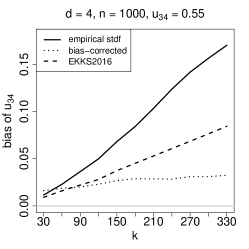

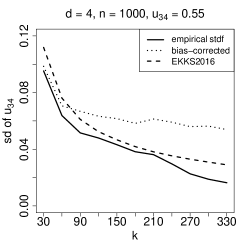

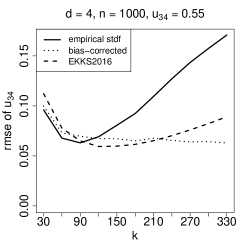

The upper panels of Figure 2 show the bias, standard deviation and RMSE for three estimators: the estimator based on the empirical tail dependence function with (solid lines), the estimator based on the bias-corrected tail dependence function with (dotted lines), and the pairwise M-estimator from Einmahl et al. (2016) (dashed lines). We see that for the estimation of the shape parameter it is better to use one of the estimators based on the empirical stable tail dependence function, whereas for the scale parameter the bias-corrected estimator performs better.

To show the feasibility of the estimation procedure in high dimensions, we simulate samples of size from the perturbed Brown–Resnick process on a unit-distance grid (), using again and selecting pairs of neighbouring locations only, yielding pairs in total. The bottom panels of Figure 2 show the bias, standard deviation and RMSE for the estimator based on the empirical tail dependence function with (solid lines), the estimator based on the bias-corrected tail dependence function with (dotted lines), and the pairwise M-estimator from Einmahl et al. (2016) (dashed lines). Compared to above, the estimation of has improved whereas the estimation quality of stays roughly the same.

3.3 Max-linear models on directed acyclic graphs

A max-linear or max-factor model has stable tail dependence function

| (3.3) |

where the factor loadings are non-negative constants such that for every and all column sums of the matrix are positive (Einmahl et al., 2012). An example of a random vector that has tail dependence function (3.3) is for , where are independent unit Fréchet variables. The random variables are then unit Fréchet as well.

Since the rows of sum up to one, it has only free elements. Further structure may be added to the coefficient matrix , leading to parametric models whose parameter dimension is lower than ; see below. Even then, the map in (2.5) induced by restricting the points to be of the form in (2.2) is typically not one-to-one. Therefore, we need more general choices of the points in the definition of the estimator.

In Gissibl and Klüppelberg (2015), a link is established between max-linear models and structural equation models, from which graphical models based on directed acyclic graphs (DAGs) can be constructed. A max-linear structural equation model is defined via

where denotes the set of parents of node in the graph, for all and for all . We let be independent unit Fréchet random variables. A max-linear structural equation model can then be written as a max-linear model with parameters determined by the paths of the corresponding graph.

We focus on the four-dimensional model corresponding to the following directed acyclic graph (Gissibl and Klüppelberg, 2015, Example 2.1):

![[Uncaptioned image]](/html/1601.04826/assets/x25.png)

If we require to be unit Fréchet, the matrix of factor loadings becomes

where the diagonal elements for are such that the row sums are equal to one. The parameter vector is then given by .

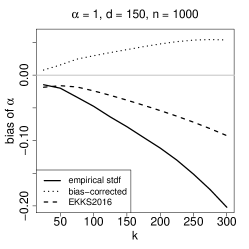

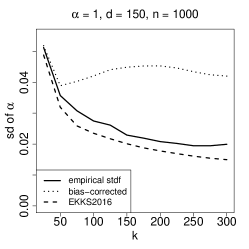

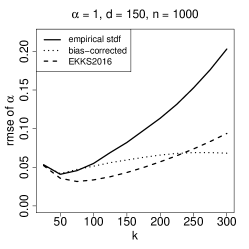

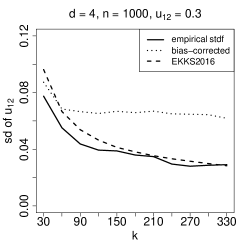

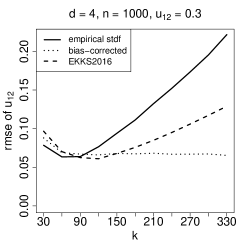

We conduct a simulation study based on samples of size from the four-dimensional model with tail dependence function (3.3) and as above, with parameter vector . As before, we put , with as above and independent random variables. The estimators are based on the points on the grid having at least two positive coordinates.

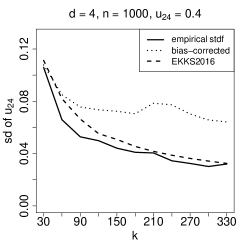

Figure 3 shows the bias, standard deviation and RMSE for the estimator based on the empirical tail dependence function with (solid lines), the estimator based on the bias-corrected tail dependence function with (dotted lines) and the pairwise M-estimator from Einmahl et al. (2016) (dashed lines). The difference between the pairwise M-estimator and our estimators based on the empirical tail dependence function is negligible. The estimators based on the empirical tail dependence function perform better than the ones based on the bias-corrected version, especially for the parameters and .

Remark 3.1.

For the weight matrix, we actually defined as for some small . The reason for applying such a Tikhonov correction is that some eigenvalues of are (near) zero, which can in turn be due to the fact that for max-linear models such as here, may hit its lower bound for some .

3.4 Goodness-of-fit test

We compare the performance of the goodness-of-fit test presented in Corollary 2.5 to the three goodness-of-fit test statistics , , and proposed in Can et al. (2015, page 18). In the simulation study there, the observed rejection frequencies are reported at the significance level under null and alternative hypotheses for two bivariate models for ; a bivariate logistic model with and

i.e., a mixture between the logistic model and tail independence. For both models, they generate 300 samples of size from a “null hypothesis” distribution function, for which the model is correct, and 100 samples of from an “alternative hypothesis” distribution function, for which the model is incorrect. These distribution functions are described in equations (32), (33), (35), and (36) of Can et al. (2015). We take , , and .

Table 1 shows the observed fractions of Type I errors under the null hypotheses and the observed fraction of rejections under the alternative hypotheses. The results for , , and are taken from Can et al. (2015, Table 1). We see that our goodness-of-fit test performs comparably to the test statistics in Can et al. (2015).

| Null | Alternative | |||

|---|---|---|---|---|

| logistic | mixture | logistic | mixture | |

| 19/300 | 9/300 | 92/100 | 97/100 | |

| 11/300 | 13/300 | 90/100 | 97/100 | |

| 17/300 | 18/300 | 95/100 | 100/100 | |

| 16/300 | 14/300 | 100/100 | 82/100 | |

It should be noted that the tests are of very different nature. The three test statistics in Can et al. (2015) are functionals of a transformed empirical process and are therefore of omnibus-type. The results in there are based on the full max-domain of attraction condition on and the procedure is computationally complicated and therefore difficult to apply in dimensions (much) higher than two. The present test only performs comparisons at points and avoids integration. Therefore it is computationally much easier to apply in dimension .

4 Tail dependence in European stock markets

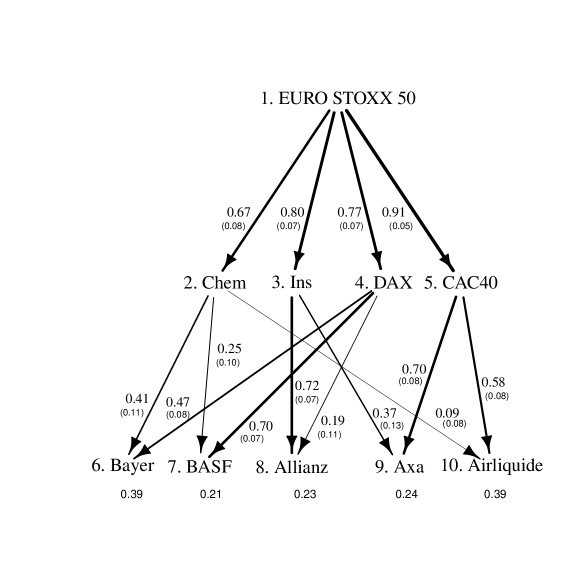

We analyze data from the EURO STOXX 50 Index, which represents the performance of the largest 50 companies among 19 different “supersectors” within the 12 main Eurozone countries. Since Germany (DE) and France (FR) together form of the index, we will focus on these two countries only. Every company belongs to a supersector, of which there are 19 in total. We select two of them as an illustration: chemicals and insurance. We study the following five stocks: Bayer (DE, chemicals), BASF (DE, chemicals), Allianz (DE, insurance), Airliquide (FR, chemicals), and Axa (FR, insurance), and we take the weekly negative log-returns of the stock prices of these companies from Yahoo Finance111http://finance.yahoo.com/ for the period January 2002 to November 2015, leading to a sample of size .

We fit a structural equation model based on the directed acyclic graph given in Figure 4. The nodes DE and FR are represented by their national stock market indices, the DAX and the CAC40, respectively, and the nodes chemicals and insurance are represented by corresponding sub-indices of the EURO STOXX 50 Index. Note that this is a model for the tail dependence function only, i.e., we only assume that the joint distribution of the negative log-returns has tail dependence function as in (3.3) with coefficient matrix given in Table 2. We have and the parameter vector is given by .

We perform the goodness-of-fit test described in Corollary 2.6, based on the points in the grid having either two or three non-zero coordinates. We take , , and we choose such that , leading in this case to . The value of the test statistic is ; the quantile of a distribution is , so that the tail dependence model is not rejected.

The resulting parameter estimates are pictured at the edges of Figure 4, where the relative width of each edge is proportional to its parameter value. The standard errors are given in parentheses. We note that, except for Allianz, the influence of the stock market indices DAX and CAC40 is (much) stronger than the influence of the sector indices chemicals and insurance.

Appendix A Proofs

Proof of Theorem 2.1.

This proof follows the same lines as the one of Einmahl et al. (2016, Proof of Theorem 1). Let be such that the closed ball is a subset of ; such an exists since is an interior point of . Fix such that . Let, more precisely than in (2.8), be the set of minimizers of the right-hand side of (2.8). We show first that

| (A.1) |

Because is a homeomorphism, there exists such that for , implies . Equivalently, for every such that we have . Define the event

If is such that , then on the event , we have

It follows that on ,

The infimum on the right-hand side is actually a minimum since is continuous and is compact. Hence on the set is non-empty and . To show (A.1), it remains to prove that as , but this follows from (2.10).

Next we will prove that, with probability tending to one, has exactly one element, i.e., the function has a unique minimizer. To do so, we will show that there exists such that, with probability tending to one, the Hessian of is positive definite on and thus is strictly convex on . In combination with (A.1) for , this will yield the desired conclusion.

For , define the symmetric matrix by

for . The map is continuous and

| (A.2) |

is a positive definite matrix. This matrix is non-singular, since the matrix is non-singular and the matrix has rank (recall ). Let denote the spectral norm of a matrix. From Weyl’s perturbation theorem (Jiang, 2010, page 145), there exists an such that every symmetric matrix with has positive eigenvalues and is therefore positive definite. Let be sufficiently small such that the second-order partial derivatives of and are continuous on and such that for all .

Let denote the Hessian matrix of . Its -th element is

Since and since converges in probability to , we obtain

| (A.3) |

By the triangle inequality, it follows that

| (A.4) |

In view of our choice for , this implies that, with probability tending to one, is positive definite for all , as required. ∎

Proof of Theorem 2.2.

Let , a vector, be the gradient of at . By (2.11), we have

| (A.5) |

Since is a minimizer of , we have . An application of the mean value theorem to the function at and yields

| (A.6) |

where is a random vector on the segment connecting and and is the Hessian matrix of as in the proof of Theorem 2.1. Since , we have as too. By (A.3) and (A.2) and continuity of , it then follows that

| (A.7) |

Since is non-singular, the matrix is non-singular with probability tending to one as well. Combine equations (A.5), (A.6) and (A.7) to see that

Convergence in distribution to the stated normal distribution follows from (2.11) and Slutsky’s lemma. ∎

Proof of Corollary 2.4.

Since , we have

By (2.12) and the delta method, we have

where and are evaluated at . Combination of the two previous displays yields

By (2.11) and Slutsky’s lemma, we arrive at (2.15), as required.

The matrix has rank since the matrix has rank and the matrix is non-singular. Since , it follows that rank rankrank ∎

Proof of Corollary 2.5.

Equation (2.11) can be written as

In view of (2.15) and , we find, by Slutsky’s lemma and the continuous mapping theorem,

here , with and evaluated at .

It remains to identify the distribution of the limit random variable. The random vector is equal in distribution to , where and where is a symmetric square root of . Straightforward calculation yields

where It is easily checked that is a projection matrix (). Moreover, has rank . It follows that is a projection matrix too and that it has rank . The distribution of the limit random variable now follows by standard properties of quadratic forms of normal random vectors. ∎

Proof of Corollary 2.6.

Let , which by (2.11) is the limit in distribution of . By (2.15) and the continuous mapping theorem, we have, as ,

| (A.8) |

We can represent as , with . The limiting random variable in (A.8) is then given by

Since is an orthogonal matrix, this expression simplifies to , which has the stated distribution. ∎

Proof of Remark 2.1.

Inspection of the proofs of Corollaries 2.5 and 2.6 shows that the difference between the two test statistics converges in distribution to the random variable , where is a certain -variate normal random vector and where

The matrix can be shown to be equal to zero, proving the claim of the remark. To see why is zero, note first that, suppressing and writing , we have and . Recall the eigenvalue equation for . Note that if and if . The eigenvalue equation implies that for while for . Since the vectors are orthogonal, we find that the vectors are linearly independent. It then suffices to show that for all and for all . The first property follows from the fact that and for (use the eigenvalue equation again), while the second property follows from for . ∎

References

- Abadir and Magnus (2005) Abadir, K. M. and J. R. Magnus (2005). Matrix Algebra, Volume 1. Cambridge University Press.

- Beirlant et al. (2015) Beirlant, J., M. Escobar-Bach, Y. Goegebeur, and A. Guillou (2015). Bias-corrected estimation of the stable tail dependence function. Available at https://hal.archives-ouvertes.fr/hal-01115538/.

- Beirlant et al. (2004) Beirlant, J., Y. Goegebeur, J. Segers, and J. Teugels (2004). Statistics of Extremes: Theory and Applications. Wiley.

- Bücher and Segers (2014) Bücher, A. and J. Segers (2014). Extreme value copula estimation based on block maxima of a multivariate stationary time series. Extremes 17(3), 495–528.

- Can et al. (2015) Can, S. U., J. H. J. Einmahl, E. V. Khmaladze, R. J. A. Laeven, et al. (2015). Asymptotically distribution-free goodness-of-fit testing for tail copulas. The Annals of Statistics 43(2), 878–902.

- Coles and Tawn (1991) Coles, S. G. and J. A. Tawn (1991). Modelling extreme multivariate events. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 53(2), 377–392.

- Davison et al. (2012) Davison, A. C., S. A. Padoan, and M. Ribatet (2012). Statistical modeling of spatial extremes. Statistical Science 27(2), 161–186.

- de Haan (1984) de Haan, L. (1984). A spectral representation for max-stable processes. The Annals of Probability 12(4), 1194–1204.

- de Haan and Ferreira (2006) de Haan, L. and A. Ferreira (2006). Extreme Value Theory: an Introduction. Springer-Verlag Inc.

- de Haan and Pereira (2006) de Haan, L. and T. T. Pereira (2006). Spatial extremes: Models for the stationary case. The Annals of Statistics 34(1), 146–168.

- Drees and Huang (1998) Drees, H. and X. Huang (1998). Best attainable rates of convergence for estimators of the stable tail dependence function. Journal of Multivariate Analysis 64(1), 25–47.

- Einmahl et al. (2016) Einmahl, J. H. J., A. Kiriliouk, A. Krajina, and J. Segers (2016). An M-estimator of spatial tail dependence. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 78(1), 275–298.

- Einmahl et al. (2012) Einmahl, J. H. J., A. Krajina, and J. Segers (2012). An M-estimator for tail dependence in arbitrary dimensions. The Annals of Statistics 40(3), 1764–1793.

- Fougères et al. (2015) Fougères, A.-L., L. de Haan, and C. Mercadier (2015). Bias correction in multivariate extremes. The Annals of Statistics 43(2), 903–934.

- Gissibl and Klüppelberg (2015) Gissibl, N. and C. Klüppelberg (2015). Max-linear models on directed acyclic graphs. Available at http://arxiv.org/abs/1512.07522.

- Gumbel (1960) Gumbel, E. J. (1960). Bivariate exponential distributions. Journal of the American Statistical Association 55(292), 698–707.

- Hansen et al. (1996) Hansen, L. P., J. Heaton, and A. Yaron (1996). Finite-sample properties of some alternative GMM estimators. Journal of Business & Economic Statistics 14(3), 262–280.

- Hofert et al. (2015) Hofert, M., I. Kojadinovic, M. Maechler, and J. Yan (2015). copula: multivariate dependence with copulas. R package version 0.999-13.

- Huang (1992) Huang, X. (1992). Statistics of bivariate extreme values. Ph. D. thesis, Tinbergen Institute Research Series.

- Huser and Davison (2013) Huser, R. and A. Davison (2013). Composite likelihood estimation for the Brown-Resnick process. Biometrika 100(2), 511–518.

- Huser and Davison (2014) Huser, R. and A. Davison (2014). Space–time modelling of extreme events. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 76(2), 439–461.

- Huser et al. (2015) Huser, R., A. C. Davison, and M. G. Genton (2015). Likelihood estimators for multivariate extremes. Extremes, 1–25.

- Jiang (2010) Jiang, J. (2010). Large sample techniques for statistics. Springer.

- Kabluchko et al. (2009) Kabluchko, Z., M. Schlather, and L. de Haan (2009). Stationary max-stable fields associated to negative definite functions. Annals of Probability 37(5), 2042–2065.

- Kiriliouk and Segers (2014) Kiriliouk, A. and J. Segers (2014). spatialTailDep: Estimation of spatial tail dependence models. R package version 1.0.2.

- Nolan et al. (2015) Nolan, J., A.-L. Fougères, and C. Mercadier (2015). Estimation for multivariate extreme value distributions using max projections. Presentation available at http://sites.lsa.umich.edu/eva2015/program/.

- Oesting et al. (2015) Oesting, M., M. Schlather, and P. Friedrichs (2015). Statistical post-processing of forecasts for extremes using bivariate Brown-Resnick processes with an application to wind gusts. Available at http://arxiv.org/abs/1312.4584.

- R Core Team (2015) R Core Team (2015). R: A Language and Environment for Statistical Computing. Vienna, Austria: R Foundation for Statistical Computing.

- Ressel (2013) Ressel, P. (2013). Homogeneous distributions–and a spectral representation of classical mean values and stable tail dependence functions. Journal of Multivariate Analysis 117, 246–256.

- Ribatet (2015) Ribatet, M. (2015). SpatialExtremes: Modelling Spatial Extremes. R package version 2.0-2.

- Schlather and Tawn (2003) Schlather, M. and J. Tawn (2003). A dependence measure for multivariate and spatial extreme values: Properties and inference. Biometrika 90(1), 139–156.

- Smith (1990) Smith, R. L. (1990). Max-stable processes and spatial extremes. Unpublished manuscript.

- Wadsworth and Tawn (2014) Wadsworth, J. L. and J. A. Tawn (2014). Efficient inference for spatial extreme-value processes associated to log-gaussian random functions. Biometrika 101(1), 1–15.

- Wang and Stoev (2011) Wang, Y. and S. A. Stoev (2011). Conditional sampling for spectrally discrete max-stable random fields. Advances in Applied Probability 43(2), 461–483.