Discretization of Continuous Time Discrete Scale Invariant Processes: Estimation and Spectra

Abstract

Imposing some flexible sampling scheme we provide some discretization of continuous time discrete scale invariant (DSI) processes which is a subsidiary discrete time DSI process.

Then by introducing some simple random measure we provide a second continuous time DSI process which provides a proper approximation of the first one. This enables us to

provide a bilateral relation between covariance functions of the subsidiary process and the new continuous time processes.

The time varying spectral representation of such continuous time DSI process is characterized, and its spectrum is estimated. Also, a new method for estimation time dependent Hurst parameter of such processes is provided which gives a more accurate estimation. The performance of this estimation method is studied via simulation. Finally this method is applied to the real data of SP500 and Dow Jones indices for some special periods.

Keywords:Discretization of continuous time DSI processes, Time dependent Hurst parameter estimation, Spectral representation.

2010 MSC: 60G18, 60G99

1 Introduction

Scale invariance (or self-similarity), as an important feature, often are used as a fundamental property to interpret many natural and man-made phenomena like turbulence of fluids, textures in geophysics, telecommunications of network traffic, image processing, finance, [2]. Scale invariance is often described as a symmetry of the system relatively to a transformation of a scale, that is mainly a dilation or a contraction (up to some re-normalization) of the system parameters [2]. Discrete scale invariance (DSI) is a property which requires invariance by dilation for certain preferred scaling factors [18]. Burnecki et al. [4] and Borgnat et. al. [3] have studied the property of DSI and its relation to PC by means of the Lamperti transformation [16].

Even though that the re-normalization factor for scale invariant processes has some fixed exponent called Hurst parameter, but for many real world data we are dealt with situations in which th Hurst parameter , changes in time. As part of the literatures in studying scale invariant processes with time dependent Hurst parameter , we refer the reader to the works of Flandrin and Goncalves [7], [8], Cavanaugh et al [5], Courjouly [6], Goncalves and Abry [9], Kent and Wood [11], Stoev et al [21] and Wang et al [22] s. We present a new method for estimating time dependent Hurst parameter and implement it for simulated data and also SP500 and Dow Jones indices for some periods.

In this paper we are to extend the work of Modarresi and Rezakhah [14] that they provided covariance structure and time varying spectral representation of certain periodically correlated processes. Even though one could provide the results expressed here in this paper by applying some quasi Lamperti transform, but we are to study this by an alternative way. Modarresi and Rezakhah [15] considered a flexible sampling scheme for continuous time DSI process and provide a discretization of this process as a discrete time DSI process. We follow their method to introduce simple random measures on subintervals between sampling points of such discrete time process, which amounts to the size of the process at the end point of each subinterval. So following their method we provide a second continuous time DSI process which is a proper approximation of the first one, which enables us to obtain the spectral representation and spectrum of this new continuous time DSI process. The covariance structure and the spectral representation of such a continuous time DSI process are specified.

Let to be a continuous time DSI process with scale , which can be considered as the accumulated of flow in time. We assume that X(t) in turn can be approximated via a DSI sequence , which represents the increment of the flow on some proper partition of time. Following the flexible sampling scheme, we consider a partition of the positive real line as for and , so . Then we consider sampling of at arbitrary points inside the first scale interval , and follow sampling at corresponding points in the successive scale intervals [16]. This provides a partition for each scale interval and divide the scale interval to subintervals . Here we introduce some certain continuous time DSI processes and provide corresponding spectral representation, which can be applied to approximate many continuous time DSI processes. In this order we extend the method of Modarresi and Rezakhah [14], which presented to provide spectral representation of certain continuous time periodically correlated processes.

1.1 Continuous time DSI process.

Let , for and , where is some continuous time DSI process. Then , for is a subsidiary discrete time (H-)-DSI process. Now let be a sequence of random measures defined on , where , and for . The covariance structure of such random measures is assigned through the covariance structure of the discrete time DSI process . In addition, as the amount of the process on a set A, say the ruin due to an earthquake or a tsunami, we define simple random measure , where .

Then we study , where is a linear combination of and , for which describes elimination of the effect of the process from the previous subinterval,say , and aggregate the amount of the process on the current subinterval , say , as approaches to the right end point of ; say surges in a tsunami. We also study the spectral representation of this process.

The paper is organized as follows. In Section 2, we give some background on DSI and PC processes and the Lamperti transformation. In Section 3, the main results as the covariance structure and the spectral representation of such continuous certain DSI processes are presented. In Section 4, a new method for the estimation of in the DSI processes is presented and the performance and accuracy of the method is studied via simulation. The proposed estimation method is also compared with the method introduced by Modarresi and Rezakhah [16]. Finally, the estimation method is applied on SP500 and Dow Jones indices for some special periods.

2 Preliminaries

In this section, we review the spectral representation of PC processes based on unitary operators, and also the quasi Lamperti transform which connects PC and DSI processes.

2.1 DSI and PC processes and Lamperti transformation

A unitary operator on a Hilbert space , is a linear operator from to which preserve inner product as for every , [10].

Theorem 1

For any unitary operator on a Hilbert space , there exist a unique spectral measure on the Borel subsets of such that , and for any integer , [10].

Proposition 1

Definition 2

A random process is called discrete time DSI in wide sense with index and scale with parameter space , where is any subset of distinct points of positive real numbers, if for all and , where :

See [13].

Definition 3

Let be a random process. The quasi Lamperti transform with positive parameter H and , denoted by , is defined as , and the inverse quasi Lamperti transform for any random process is , [17].

Proposition 2

If is a DSI process with parameter and scale , then for , is PC with period . Conversely if is PC with period T, then for , is a DSI process with parameter and scale , [17].

3 Main results

Here, we study a new class of continuous time DSI processes , and investigate its special structure in subsection 3.1. Further, the covariance structure and the spectral representation of the process are studied in subsections 3.2 and 3.3, respectively.

3.1 Continuous DSI process

We consider a second order discrete time DSI process with scale , in the sense that , and a random measure on Borel field of subsets of , where . For , , we define

| (1) |

and covariance functions

| (2) |

where

and . Also, for ,

Let , where , . Thus, by Eq (1),

| (3) |

where . Moreover, for , and , by (2),

| (4) |

| (5) |

where , for , and . Consequently, if , , , such that , then

| (6) |

Further, by (1), (3) and the DSI property of , we have that

| (7) |

Therefore, by defining

| (8) |

where , we find that is a discrete time DSI process with scale with respect to , , for fixed .

Moreover, for we define

| (9) |

where . Thus, for ,

| (10) |

where . In the next subsection, we study about the covariance structure of the certain continuous time DSI process .

3.2 Covariance function of the certain DSI precess

Now, we present a lemma which provides the covariance function of the certain continuous time DSI process .

Lemma 4

Let , be a partition of the positive real line, and . The covariance function of for and , is

| (11) |

where for , and , and for , , ; also .

3.3 Spectral representation

In this section we study the spectral representation structure of the continuous time DSI process .

Let be a subsidiary DSI process with scale in for fixed , in the sense that . Modarresi and Rezakhah [15] provided the spectral representation and spectral density matrix of the corresponding subsidiary multi-dimensional self-similar corresponding to such subsidiary DSI process which can be applied to obtain the spectral representation and spectral density function of such continuous time DSI process. Also Modarresi and Rezakhah [13] provided the spectral representation of the corresponding discrete time DSI process when and which can be applied to obtain spectral representation of the process in such a case.

4 Simulation

This section, we present a new method for the estimation of Hurst parameter of DSI processes which is more compatible for real world data. This motivation comes from the fact that in many DSI processes we have different behavior for the fluctuation of the process in different parts of scale intervals which are followed in corresponding parts of successive scale intervals. So assuming the Hurst parameter to be some fixed number for the whole process, in many real data is not realistic. The other behavior of the DSI process is some self-similar behavior inside the scale intervals. Therefore, it would be useful to consider some partition of scale intervals, say , that the ratio of the length of each subinterval to the length of the corresponding scale intervals are fixed through out the process. Then we evaluate the estimation of the Hurst parameter corresponding to the growth of the process in corresponding subintervals. By assuming such partition for each scale interval, we have a Hurst estimation vector of size to be estimated.

Extending the method proposed by Modarresi and Rezakhah [16] for scale intervals, we evaluate the ratios of quadratic variations of corresponding subintervals in consecutive scale intervals by the following and estimate the Hurst vector. Thus we calculate the quadratic variations corresponding to the th subinterval in the th scale interval as

| (12) |

for , ; where is the number of observations in th subinterval, and , . Then, we use

| (13) |

Finally, the Hurst estimation for th subinterval is obtained as .

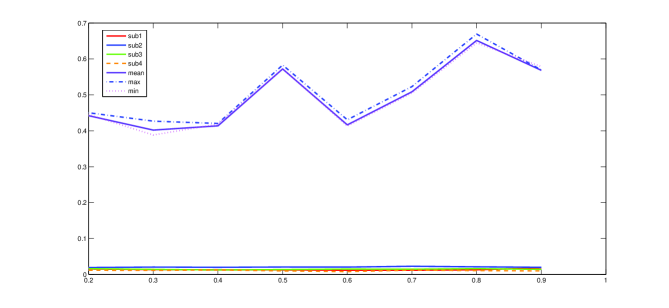

The superiority of the method is investigated for simulated and empirical data. In the simulation case, MSEs of the proposed method and the method presented in [16] are computed for different Hurst indices. To this end, we consider DSI processes in which the Hurst parameter changes slowly in time, such that we can assume some subintervals in each scale interval where the Hurst parameter is approximately constant for the entire subinterval, but it changes from one subinterval to another. As an example, we consider a DSI process which contains 4 scale intervals, 4 subintervals and 80 equally spaced samples points in each scale interval. Hence, the estimator would be a vector of size 4, as . The MSEs of are computed and depicted in Figure 1, with different colors for subintervals 1, 2, 3, 4, and for different values of . Also, the MSEs of the estimator proposed by Modarresi and Rezakhah [16] are indicated for the mean, maximum and minimum of , for different values of . As can be seen in the Figure 1, considering subintervals in each scale interval gives a more accurate estimation than the method presented in [16].

4.1 Empirical Data

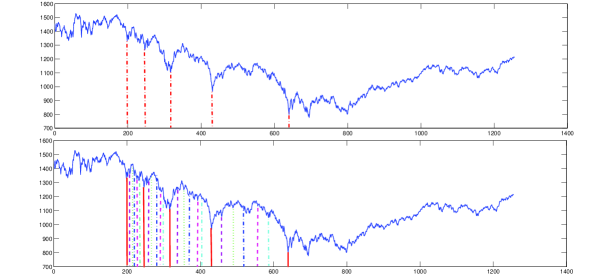

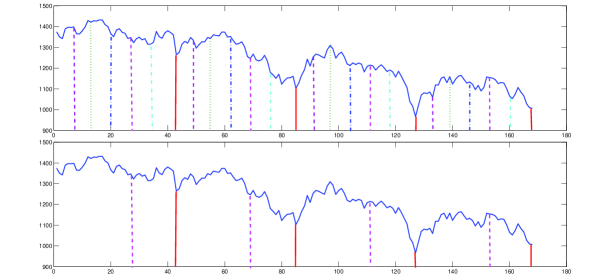

The superiority of the method is also investigated for empirical data. To this end, we study the daily indices of two stock markets: SP500 and Dow Jones. First, we consider daily indices of SP500 from the first January 2000 till the end of 2004. As there is not any index on Saturdays, Sundays and holidays, the available data for the selected period are 1256 days. The time series of these indices is shown in Figure 2. These data are also studied by Bartolozzi et al. [1], where the existence of a DSI behavior, with scale 2, in some periods of data has been justified. We only consider the indices from 16th October 2000 until 23th July 2002 which the DSI behavior can be seen in four scale intervals and is shown in Figure 2 by red lines. The preferred scaling factor of the process for the periods is evaluated approximately with 1.66. Therefore, the end points of the scale intervals would be , , , and . To study these four scale intervals accurately, subintervals should be determined such that the process behaves the same in all consecutive subintervals. For the SP500 process, the subintervals of the first scale interval are indicated with the end points: , , , , , and , which are shown in Figure 2 with different colors. The corresponding subintervals of the th scale interval, j = 2, 3, 4, are determined as , where , and is the starting point of the th scale interval, also, is the bracket. Following the sampling method, we consider 42 arbitrary sample points in the first scale interval as 200, 201, 202, , 241, and corresponding sample points in the th scale interval, can also be determined as , j = 2, 3, 4. So, we would have 6, 6, 7, 7, 7, 9 data in subintervals 1, 2, , 6 of the first scale interval, respectively. The sampled SP500 process, obtained by the sampling method, is depicted in Figure 3.

By computing ratios of sample variances of subintervals, Eq (12), (13), the Hurst estimation comes out as . Since, the first four Hurst estimations, and the last two ones are approximately the same; so, we combine the first four subintervals as one subinterval, and the last two ones as the second subinterval. Hence, there would be 26 and 16 observations in the first and second subintervals, respectively. Such partitions are shown in Figure 3 (Bottom). Thus, the Hurst estimations would be: . The Hurst parameter also estimated based on the method presented in [16] as .

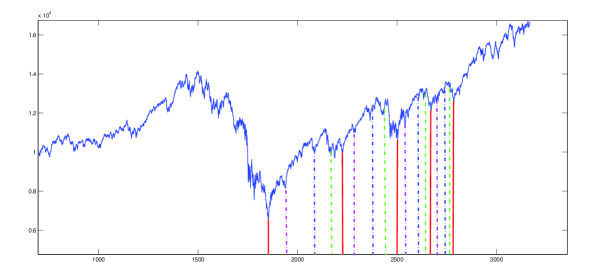

As an another example, we consider daily indices of Dow Jones from 25th October 2001 till 28th May 2014. As there is not any index on Saturdays, Sundays and holidays, the available data for the selected period are 3168 days. These indices are plotted in Figure 4, where the existence of a DSI behavior in a period from 6th March 2009 until 14th November 2012 has been justified in four scale intervals. Also, the scale has been evaluated approximately with 1.493. The red lines in Figure 4 reveals the scale intervals with the end points , , , and . To estimate the Hurst parameter accurately, 4 subintervals are determined in each scale interval. Since the last scale interval, is the shortest one, so we determine subintervals in it with the end points , , , , and . The subintervals of the rest scale intervals could be found from the relation , where , and is the starting point of the th scale interval. Partitioning of scale intervals are shown in Figure 4 with different colors. Also, 113 arbitrary sample points are considered in the last scale interval as 2671, 2672, 2673, , 2783. The corresponding sample points in the th scale interval, j = 1, 2, 3, can be determined as , where for the indices in the mentioned period, we would have 27, 43, 25, 18 data in subintervals 1, 2, 3, 4, respectively. Using (12) and (13), the Hurst estimation comes out as: , which shows the Hurst indices of subintervals 1-4. Also, based on the method provided by Modarresi and Rezakhah [16], the Hurt estimation for the whole process is computed as .

5 Conclusion

A certain continuous time DSI process is defined, where its covariance function is generated by the covariance function of a discrete time DSI process through defining some simple random measure on the positive real line. The time varying spectral representation of such a process is characterized, and its spectrum is estimated. Moreover, a new method for Hurst estimation of DSI processes is proposed. The estimation method is based on determining some subintervals in each scale interval and evaluating ratios of quadratic variations corresponding to consecutive subintervals. Numerical results were presented to show that the proposed method provided an accurate estimation than the method provided in [16], in the sense of MSE. Finally, the estimation method is applied to the SP500 and Dow Jones indices for some special periods.

References

- [1] Bartolozzi M., Drozdz S., Leieber D. B., Speth J., Thomas A.W.: Self-similar log-periodic structures in Western stock markets from 2000. Int. J. Mod. Phys. C. vol. 16, no. 9, 1347-1361, (2005)

- [2] Borgnat P., Amblard P. O., Flandrin P.: Scale invariances and Lamperti transformations for stochastic processes. J. Phys. A, Math. Gen. vol. 38, no. 10, 2081-2101, (2005)

- [3] Borgnat P., Flandrin P., Amblard P. O.: Stochastic discrete scale invariance. IEEE Signal Proc let. vol. 9, no. 6, 182-184, (2002)

- [4] Burnecki K., Maejima M., Weron A.: The Lamperti transformation for self-similar processes. Yokohama Math. J. vol. 44, 25-42, (1997)

- [5] Cavanaugh J. E., Wang Y., Davis J. W.: Locally self-similar processes and their Wavelet analysis. Stochastic processes: modelling and simulation. 93-135, Handbook of Statist. 21, North-Holland, Amsterdam. (2003)

- [6] Coeurjolly J. F.: Estimating the parameters of a fractional Brownian motion by discrete variations of its sample paths. Stat. Inference Stoch. Process. vol. 4, no. 2, 199-227, (2001)

- [7] Flandrin P., Gonalvs P.: From Wavelets to time-scale energy distributions. Recent advances in wavelet analysis, Wavelet Anal. Appl, Academic Press, Boston, MA. vol. 3, 309-334, (1994)

- [8] Goncalves P., Flandrin P.: Bilinear time scale analysis applied to local scaling exponent estimation. In Progress in Wavelet Analysis and Applications (Y. Meyer and S. Roques, eds.) Toulouse (France). 271-276, (1992)

- [9] Goncalves P., Abry P.: Multiple-window wavelet transform and local scaling exponent estimation. IEEE Int. Conf. on Acoust. Speech and Sig. Proc. Munich (Germany). (1997)

- [10] Hurd H. L., Miamee A. G.: Periodically Correlated Random Sequences: Spectral Theory and Practice. John Wiley. (2007)

- [11] Kent J. T., Wood A. T. A.: Estimating the fractal dimension of a locally self-similar Gaussian process by using increments. J. Roy. Statist. Soc. Ser. B. vol. 59, no. 3, 579-599, (1997)

- [12] Kwapień J., Drożdż S.: Physical approach to complex systems. Physics Reports. no. 515, 115-226, (2012)

- [13] Modarresi N., Rezakhah S.: Spectral Analysis of Multi-dimensional Self-similar Markov Processes. J. Phys. A-Math. Theor. vol. 43, no. 12, 125004, (2009)

- [14] Modarresi N., Rezakhah S.: Certain Periodically correlated multi-component Locally Stationary processe . Theory Probab. Appl. vol. 59, no. 2, 1-30 (2015)

- [15] Modarresi N., Rezakhah S.: A New Structure for Analyzing Discrete Scale Invariant Processes: Covariance and Spectra. J. Stat. Phys. vol. 153, no. 1, 162-176, (2013)

- [16] Modarresi N., Rezakhah S.: Characterization of discrete time scale invariant Markov process. Communnications in Statistics: Theory and Methods, http://dx.doi.org/10.1080/03610926.2014.942427

- [17] Modarresi N., Rezakhah S.: Discrete Time Scale Invariant Markov Processes. arxiv.org/pdf/0905.3959v3. (2009)

- [18] Sornette D.: Discrete scale invariance and complex dimensions. Phys. Rept. vol. 297, no. 5, 239-270, (1998)

- [19] Johansen A., Sornette D., Ledoit O.: Predicting Financial Crashes using discrete scale invariance. J. Risk, vol. 1, no. 4, 5-32, (1999)

- [20] Johansen A., Sornette D., Ledoit O.: Empirical and Theoretical Status of Discrete Scale Invariance in Financial Crashes. J. Risk, vol. 1, no. 4, 5-32, (1999)

- [21] Stoev S., Taqqu M. S., Park C., Michailidis G., Marron J. S.: LASS: a tool for the local analysis of self-similarity. Comput. Statist. Data Anal. vol. 50, no. 9, 2447-2471, (2006)

- [22] Wang Y., Cavanaugh J. E., Song C.: Self-similarity index estimation via wavelets for locally self-similar processes. J. Stat. Plan. Infer. vol. 99, no. 1, 91-110, (2001)