Unbiased Monte Carlo estimate of stochastic differential equations expectations

Abstract

We propose an unbiased Monte Carlo method to compute where is a Lipschitz function and an Ito process. This approach extends the method proposed in [16] to the case where is solution of a multidimensional stochastic differential equation with varying drift and diffusion coefficients. A variance reduction method relying on interacting particle systems is also developed.

Key words: unbiased estimate, linear parabolic PDEs, interacting particle systems

MSC2010: Primary 65C05, 60J60; secondary 60J85, 35K10

1 Introduction

Let and be a dimensional Brownian motion. We introduce the process defined as the unique strong solution of the multi-dimensional Stochastic differential Equation (SDE) with coefficients satisfying the usual Lipschitz conditions :

| (1.1) |

where is the drift and is the diffusion of the process, being the set of dimensional matrices.

In this paper, we are interested in a Monte Carlo approach to compute an expectation of the form

| (1.2) |

When no explicit solution is available, the classical method to solve equation (1.2) consists in using a discretization scheme of (1.1) (for example the Euler scheme [18], the Milstein scheme [19], or the Burrage scheme [5]) and the error can be decomposed as a sum of an error due to the discretization time step and a statistical error of order due to the Monte Carlo method for a number of simulations.

In principle, this bias/variance tradeoff should carefully be adjusted in order to optimize the rate of convergence. This type of analysis has been conducted in [9] showing that, for instance with the the simple Euler Monte Carlo method, (using the Euler scheme to discretize the time), the best choice of time step as a function of the sample size would lead to a rate of order , where measures the computing time. Hence the combination of the bias and variance error deteriorates the standard rate , due to the statistical error, when is easily simulatable and . Moreover, in practice it is difficult to evaluate properly the bias error so that the optimal tradeoff is rarely practicable.

The Multilevel Monte Carlo (MLMC) method introduced in [12] is a way to improve the bias/variance tradeoff and to reduce the variance by combining several Euler-Monte Carlo estimates, associated with different time discretization steps. The idea is then to adjust judiciously the size of the sample simulated for each discretization level, in order to achieve a better rate of convergence.

This approach has been extended in [20] allowing for an infinite number of levels so that the bias vanishes. The estimate is then expressed as an infinite sum (over the levels), which is randomized by introducing a probability distribution driving the levels.

However, when the order of the time discretization scheme is not sufficiently high, this method results in an infinite variance estimate. More precisely, as soon as the time discretization scheme implies a strong error greater than or equal to the order , either the variance or the computing time blows up. Unfortunately this situation includes the case of the Euler scheme, which is so far the most widely usable discretization scheme in multidimensional cases.

This approach has been improved in [1], where the authors rely on the parametrix expansion presented in [2] to propose a finite variance estimate. More specifically, the parametrix method provides a precise expansion of the expected difference considered at two successive levels in terms of a difference between the infinitesimal generator, , associated with (1.1) and the one associated with the same SDE with frozen coefficients at a given point, as defined hereafter by (2.3). Finally, importance sampling is used to change the levels distribution in order to control the variance.

These developments lead to the backward simulation method or the forward simulation method, depending on whether or its adjoint is used to represent the expectation.

The backward method consists in generating some independent and identically distributed (i.i.d.) Euler type discretizations of a process, at random discrete times, from time to time . The payoff function, is used as initial distribution at time and the estimator results from a weighted average over the trials that hit the initial point, , at time . Therefore, this approach requires the payoff to be integrable and is limited to small dimensions (for which the probability of reaching a given point can efficiently be computed).

The forward method consists in generating some i.i.d. Euler type discretizations of (1.1) at random discrete times from time to and then computing a weighted average of the payoff function evaluated at the final points. In both methods the weights depend on the drift and diffusion coefficients and evaluated along the simulated path. However, the forward approach relies on a stronger regularity assumption on the SDE coefficients. In particular, the related weights involve the first derivatives of the drift and the first and second derivatives of the volatility function.

Another approach called Exact simulation was initialized in [3]. The idea relies on Lamperti transform to come down to a unit diffusion process. It has been extended to more general SDEs in for instance [6, 17]. However, the Lamperti transform is limited to the one dimensional case and extensions to the multidimensional are still limited to some specific cases.

In this paper, we propose to extend a method originally developed in [16]. The main idea developed in this seminal paper is to start by simulating exactly a SDE :

where the coefficients and are updated at independent exponential switching times.

Then the change in coefficients in SDE (1.1) is taken into account in an expectation representation via weights derived from the automatic differentiation technique developed in [11].

By carefully choosing the coefficients , , the authors were able to provide a finite variance method in the case where the diffusion coefficient is constant or with a general diffusion term but without drift and in dimension one.

However, the variance of the resulting estimator is proved to be infinite in the most general case.

One interest of this approach which is very similar to the forward parametrix representation [2, 1] is that the weights do not involve any derivatives of the coefficients or so that no differentiability assumptions on those coefficients is required.

Besides, one major motivation of this type of approach goes beyond the scope of the present paper. The idea is to generalize the branching diffusion representation of nonlinear Partial Differential Equations (PDEs) considered in [13, 15] to a more general class of nonlineariries. One step in that direction has already been done in [14] with an extension of the branching diffusion representation to a class of semilinear PDEs.

To bypass the infinite variance obstacle faced in [16], the idea developed in the present paper consists in extending the original framework to more general switching times and exploit the switching time distribution to control the estimator variance. Notice that the same idea has been independently investigated in [1] to control the variance of the parametrix representation proposed in [2].

We prove that under suitable assumptions on the switching times distribution, we can provide a finite variance estimate of the solution of (1.2) in the most general case with drift and diffusion coefficients both varying. For instance, the gamma distribution is proved to verify those assumptions as soon as the shape parameter satisfies , when the coefficients and are supposed to be uniformly -Hölder continuous w.r.t the time variable.

Another contribution consists in proposing an original interacting particle scheme that helps to stabilize even more the estimator. This approach results in a new estimator combining both branching and interacting particle techniques. The new estimator is proved to be unbiased with finite variance. Finally, numerical tests confirm the interest of our new algorithm showing significant variance reduction in various examples.

2 Notations

Let denote the set of continuously differentiable bounded functions with bounded derivatives of order for the time variable and bounded derivatives up to order for the space variable. Let denote the infinitesimal generator associated with (1.1) such that for any sufficiently regular function in the domain of , is given as the real valued function such that

| (2.1) |

where , and (resp. ) denotes the differential operator of order (resp. of order 2) w.r.t. the space variable . Let us consider a real valued Lipschitz continuous function defined on . By the Feynman-Kac formula it is well-known that if there exists solution of the linear Partial Differential Equation (PDE)

| (2.2) |

then this PDE has a unique classical solution .

In the sequel stands for the norm of a vector or a matrix .

First we introduce an intermediary assumption that will be relaxed for our main results:

Assumption 1.

The linear PDE (2.2) admits a unique classical solution .

All along this paper, the following assumption will be in force.

Assumption 2.

-

1.

The diffusion is non-degenerated such that for some constant :

-

2.

and are uniformly Lipschitz w.r.t. the space variable i.e. there exists a finite constant such that for any

-

3.

There exists such that and are uniformly -Hölder continuous w.r.t. variable i.e. there exists a finite constant such that for any

For a fixed point , we introduce some operators and processes that will be useful in the sequel

-

•

the differential operator similar to with the drift and diffusion frozen at such that for any regular function in the domain of

(2.3) -

•

the Gaussian process with infinitesimal operator defined by

(2.4) for a given initial condition .

-

•

involving the unique solution of (2.2) is defined by

(2.5) Notice that is a well defined continuous function since and in particular

(2.6)

3 Probabilistic representation using a regime switching process

Recalling [16], the following representation holds

Lemma 3.1.

Suppose that Assumptions 1 and 2 hold and is the Gaussian process defined in (2.4), then defined by (1.2) and its (bounded and continuous) derivatives and are solutions of the system

| (3.1) |

where for any the function is such that

| (3.2) |

and are respectively the first and second order Malliavin weights associated with the process that is using

| (3.3) |

Proof.

The proof relies on the uniqueness property of classical solutions of PDEs satisfying the Feynman-Kac representation. Notice that under Assumptions 1 2, is the unique classical solution of (2.2). Of course, thanks to equation (2.6), for any is also a solution of the following linear PDE

Then one can use again Feynman-Kac formula to represent the unique solution of the above PDE as

| (3.4) |

Finally observe that

| (3.5) |

The equations relative to and are obtained by applying Elworthy’s formula [10] (which simply results here in the Likelihood ratio of Broadie and Glasserman [4]) in (3.4) and by using some technical estimates placed in the Appendix 8 to be able to differentiate under the time integral.

∎

Let be a random time independent of the Brownian following the density supposed to be strictly positive on and . One can rewrite representation (3.1) by using a change of measure to replace the time integral by an expectation according to the random time .

where is the cumulative distribution of . We will now apply recursively this representation (3) by considering a sequence of i.i.d. random times .

Let us introduce a non regular (stochastic) mesh of the interval ,

| (3.7) |

characterized by the Markov chain defined by

| (3.8) |

where is an i.i.d. sequence of random times distributed according the common probability density .

Notice that defines a Markov chain with an absorbing state, . will define the so-called switching time.

The random integer is defined as the following stopping time

| (3.9) |

Now notice by the law of large numbers that so almost surely so is almost surely finite. In the sequel, we will consider an i.i.d. sequence of gamma variables with parameters recalling that the gamma density with parameter is given by

| (3.10) |

where is the gamma Euler function.

For a given mesh (defined as in (3.7) (3.8)), we consider the following sequence (defining a Markov chain conditionally to the mesh )

| (3.11) |

where . For the sake of simplicity, we will often note or instead of or .

Using representation (3) with and , conditioning with respect to one gets for any integer

| (3.12) |

with for and

The derivatives and in are given by applying the representation (3) with and , conditioning with respect to one gets for any integer

Let us introduce the sequence of weights such that for

| (3.13) |

Following the same lines as the proof of Theorem 2.2 in [16], one can derive by recurrence a representation formula for as the expectation of an exactly simulatable variable. Before one has to introduce some new assumptions.

Assumption 3.

The coefficients and are uniformly bounded i.e. there exists a finite constant such that for any

Assumption 4.

The function is Lipschitz.

Proposition 3.2.

Remark 3.1.

- 1.

-

2.

Using an exponential distribution for , one recovers the representation given in [16].

- 3.

Proof.

We will only give the sketch of the proof since it mimics step by step the proof of Theorem 2.2 in [16], which proceeds into two steps.

- 1.

-

2.

For the clarity of the paper we recall here the arguments developed in [16] to extend, by smooth approximations, the representation proved at item 1. outside of Assumption 1. Since according to assumptions 2 and 4, are Lipschtiz we can find a sequence of bounded smooth functions converging locally uniformly to as such that Assumption 1 is verified when replacing by (the infinitesimal generator associated to ) in the PDE (2.2). Let denote the solution of

and set . By item 1. The following representation holds

where (and respectively the weights ) are given by (3.11) (resp. the recursion (3.13)), where is replaced by . By stability of SDEs, and dominated convergence theorem, Similarly one can prove that which ends the proof.

∎

We next define a second representation that will be interesting in order to get some finite variance estimator for some given switching distribution, . Following [16], one can introduce antithetic variables to control the variance induced by the last time step. Let . Observe that

Hence replacing by in (3.14) does not change the expectation since due to the tower property:

Notice that the following decomposition holds whenever

Then using antithetic variables for the second term in the r.h.s. of the above equality yields the following estimator.

4 Variance Analysis in the case of Gamma distribution

The previous representation given by Proposition 3.3 is general but the variance associated to the estimator is generally infinite as it is the case when is an exponential density.

From now on, we will suppose that the density is the Gamma density (3.10) with parameters with cumulative distribution .

First, we will introduce the following assumptions.

Assumption 5.

The following assertions hold

-

1.

is Lipschitz and .

-

2.

.

Now, we can state the following proposition.

Proposition 4.1.

Proof.

Let denote the sigma-field generated by the Brownian up to the random time and the random times up to the random time i.e. .

Let us consider the second term on the r.h.s of (3.15). Notice that can easily be bounded by the boundness assumptions on and and the Lipschitz property of .

Let us consider the first term on the r.h.s. of (3.15).

The proof will be decomposed into several steps. We will first try to bound the general term of the above series , then we will consider the sum.

-

1.

Bounding

First considering and one easily obtains(4.2) Notice that in the sequel, will denote finite constants that may change from line to line that do not depend on or but only on the characteristics of the problem (, the bounds or Lipschitz constants related to , , , ). Then consider the general term of the sum (4).

We get

(4.3) Consider the first term on the r.h.s. of inequality (1), by the Lipschitz property of , the boundness of , and using the fact that is uniformly bounded away from zero, we obtain

(4.4) Consider the second term of (1). By Assumption 5.2 () one can apply Ito and obtain

This implies still using the boundness of , and using the fact that is uniformly bounded away from zero :

(4.5) Injecting (1) and (1) into (1) finally yields

(4.6) -

2.

Bounding , where the r. v. is defined by

(4.7) Consider the term ,

using the fact that is Lipschitz w.r.t. the space variable and -Hölder continuous w.r.t. the time variable. With the same development on one finally gets

(4.8) -

3.

Bounding

Using (1), we obtain(4.9) observing that and recalling that is defined by (4.7). Using the tower property of expectation and bound (4.6) yields

By Cauchy-Schwarz, for any and using (4.8), we have

(4.10) Hence, we obtain by recursion

(4.11) observing that .

Then recalling that implies finally yields

(4.12) -

4.

Convergence of the sum . Let us introduce notice that with cumulative distribution

Hence one can bound as follows

This implies that

with . Using the generalization of the Stirling formula one proves that which is the general term of a convergent sum.

∎

Remark 4.1.

The convergence of the series (4) relies on two facts :

-

•

The general term of the series (4) has to be finite: for any fixed number of switching times . However, one can observe that our bound on the r.h.s. of (4.11) can possibly blow up to infinity when . In particular, in the case of an exponential density, corresponding to , it is well-known that the conditional distribution, , is the uniform distribution on , hence the expectation on the r.h.s. of (4.11) is infinite. When , we observe that our bound is finite whatever the conditional distribution, . Notice that using gamma switching times increases the occurrence of small jumps w.r.t. the exponential case and hence the occurence of high numbers of time steps is also increased. To better adjust the complexity and variance tradeoff, one could consider other switching times densities with a smaller intensity of small jumps and rely on the conditional law to ensure that the expectation on the r.h.s. of (4.11) is bounded.

-

•

The sum has to converge. By increasing the intensity of small jumps as explained at point 1., we expect that will decrease more slowly with . This results in a tradeoff one has to achieve: increasing small jumps intensity to be able to bound each term of the series but not too strongly to ensure the convergence of .

Consequently, the representation (3.15) provides a Monte Carlo approach to compute , by simulating the regime switching process (3.11) instead of the SDE (1.1) which would potentially require to implement a stochastic Euler discretization scheme. However, even though our estimator is proved to have finite variance, one can observe in practice huge variances due to the product of a random number of terms that could potentially take values greater that one. This expectation of products is by nature not a good candidate for Monte Carlo estimation. Hence, we propose to use a resampling procedure to change this expectation of products in a product of expectations which is known to be much more stable for estimation.

5 Resampling method for regime switching processes

In this section, we propose to introduce an interacting particle system (in the same vein as those thoroughly discussed in the reference books [7] and [8]) to approximate . We will prove that the resulting estimator has finite variance under the same assumptions required to bound the variance of estimator (3.15). However, in practice, the new estimator relying on interacting particle systems will show better performances providing smaller variances in many examples, as illustrated in Section 6.

5.1 A Feynman-Kac measure representation

First we have to express as an integral according to a Feynman-Kac measure. Let us consider the Markov chain consisting of the sequence of random variables , where and are given respectively by the dynamics (3.8) and (3.11). In the sequel, we note the path valued Markov chain. Let us introduce, for any integer , the real valued function depending on the path with the notations and such that

| (5.1) |

with and where the real valued functions and are such that for any

| (5.4) | |||||

| (5.7) |

with

Observe that does not really depend on the whole path , but only on , for . Recalling (3.13), notice that the following identity holds

In the sequel, it will appear to be crucial to consider positive potential functions with uniformly bounded conditional variances, more specifically such that , thus we define the potential functions (depending implicitly on ) such that for any and for any ,

| (5.8) |

where the real valued function is defined on , for , by

| (5.9) |

Notice that this definition of is such that where was defined in (4.7), hence

Then observe that one can prove an inequality similar as (3) with replaced by

| (5.10) |

which yields as announced, that for any and

| (5.11) |

Notice that where for any and for any ,

| (5.12) |

and

| (5.13) |

Let us introduce defined on such that and for any

| (5.14) |

with .

Recalling (3.15), observe that

| (5.15) | |||||

where to simplify the notation (resp. ) denotes the product (resp. ), with in particular when , where denotes the function which takes the unique value . Now, we can define the sequence of non negative measures such that for any real valued bounded test function defined on , we have

| (5.16) |

We set by convention where denotes the probability distribution, , of the initial condition i.e. . Gathering (5.15) together with the above definition one readily obtains the following proposition expressing as an integral w.r.t. the non-negative measures .

Remark 5.1.

The weights used in equation (5.8) can be generalized with as

| (5.17) |

Proposition 5.1.

Remark 5.2.

Observe that for a given , is defined by (5.19) as a conditional expectation of a terminal payoff delivered at a future random time , knowing the state of the Markov chain from time to . Hence, evaluating is not trivial, for a given , since it requires to compute a conditional expectation. However whenever is such that , then the knowledge of determines completely both and , which implies

Now, let us introduce the sequence of probability measures defined by normalization of

| (5.20) |

where denotes the function which takes the unique value . Observing that for , , we obtain by recurrence

| (5.21) | |||||

As announced, we have replaced the expectation of a product of functions by the product of expectations of functions, since for any

Our objective is now to approximate the sequence of probability measures by a sequence of empirical measures based on a system of particles to finally end up with an approximation of the type

5.2 The particle approximation scheme

The sequence of approximating measures will be defined by mimicking the dynamics of . Hence, we begin by describing this recursive dynamics.

First let denote the transition kernel of the path valued Markov chain from to for any integer . Recall that can be considered both as an integral operator on the space of measurable functions defined on and on the space of finite measures, , such that

-

•

for any measurable test function defined on , is a measurable function defined on such that for any

-

•

for any finite measure on , is a finite measure on such that for any

In particular, let denote the probability law underlying the random variable (we will often write ), for any . Then observe that the probability law of . Besides, notice that if denotes the transition kernel of the Markov chain from to , then the transition kernel is obtained as the following cartesian product, for any

Now we can describe the dynamics of with . For any real valued test function defined on , the following identities holds

where the sign denotes the projective product between a non-negative function defined on and a non-negative measure returning the probability measure such that

| (5.22) |

Hence, one can describe the evolution from to into two steps

| (5.23) |

In other words, the sequence of probability measures satisfies the following recursion

| (5.24) |

An Interacting Particle System will be used to approximate the sequence of probability measures by a sequence of empirical probability measures , such that for all , is associated with an -samples approximately distributed according to . To simplify the notation, we will often drop the exponent and write instead of . The recursive evolution described by (5.24) is approximated by the following dynamics:

| (5.25) |

where denotes the empirical measure associated to an -sample i.i.d. according to , that is

Hence, the algorithm proceeds as follows. Recalling that , we initiate the algorithm by generating i.i.d. random variables according to , then we set

| (5.26) |

The evolution of the discrete measures, , (where denotes the size of the particle system) between two iterations and , consists into three steps:

-

1.

Weighting: each particle is weighted according to the value of the current potential function . For all , we compute and we set .

-

2.

Selection: i.i.d. random variables are generated according to the weighted discrete probability distribution . More specifically, for all , an index is generated independently with probability and we set .

-

3.

Mutation: Each selected particle evolves independently according to the dynamics . This produces a new particle system . More specifically, for all , we generate independently according to the conditional distribution , then we set

(5.27)

For all , let us introduce , the particle approximation of based on defined by recursion (5.25) and such that for any real valued measurable test function defined on ,

| (5.28) |

We begin by stating a Lemma that will be crucial to prove the convergence of our new estimator.

Lemma 5.2.

Let be a Markov chain (with initial distribution and transition kernel ) defined on a sequence of measurable spaces and be a sequence of positive measurable functions defined on such that there exists a finite constant such that

| (5.29) |

We consider the sequence of Feynman-Kac measures such that for any measurable real valued function defined on ,

| (5.30) |

Let be a sequence of particle approximation measures of defined similarly as in (5.28), with defined by (5.25). For a given , let us consider a real valued measurable function defined on such that there exists a finite positive constant such that

| (5.31) |

Then the particle approximation is unbiased with finite variance, more precisely

| (5.32) |

The proof of this Lemma relies on the formalism developed in the reference books [7, 8]. However, we had to carry out an original proof to take into account our specific framework where the potential functions are unbounded which is not considered to our knowledge in the existing literature. The proof is placed in the Appendix 7.

We are now in a position to state the main result of this section.

Theorem 5.3.

Suppose that Assumptions 2, 3 and 5 are satisfied. For any , the resampling estimator defined by (5.28) is unbiased with finite variance. More precisely,

| (5.33) |

where is a sequence of real valued functions defined on by (5.19) and is a constant depending only on the characteristics of the problem (, the bounds or Lipschitz constants related to , , , ).

Remark 5.3.

-

1.

Computing reduces to compute the following product of empirical means

where is the particle system at the th iteration of the algorithm as stated by (5.27). This in particular requires to compute for each particle of the final particle system . Recalling Remark 5.2, this may require to compute a conditional expectation. In practice, one chooses large enough such that most of particles have already reached time after iterations implying that for most particles can be computed explicitly. In the rare cases of particles that have not reached yet time , the computation of that should normally require to compute a conditional expectation is approximated by one simulation according to

Notice that it would be interesting to consider the estimator

This will be left for future work.

-

2.

Another approach to avoid this problem would consists in doing the resampling procedure only on the space variables. First simulate a sequence of random switching times and conditionally to this time mesh run an interacting particle system on the Markov chain (3.11). The estimator would then be given as an empirical mean of the resampling estimates over i.i.d. time meshes.

Proof.

Theorem 5.3 is a direct consequence of Proposition 5.1 stating that and of Lemma 5.2 after having verified that there exists a finite positive constant for which the bounds (5.29) and (5.31) are verified. Observe that (5.29) is automatically implied by (5.11). Let us consider (5.31), similarly to the proof of Proposition 4.1 one obtains

| (5.34) |

Now considering the general term of this sum for

where is a constant that may change from line to line. Recalling (5.1) finally gives

We proceed similarly when . We conclude by observing that the sum (5.34) is finite by the same argument as in the proof of Proposition 4.1. ∎

6 Numerical simulations

In this section, we begin by an empirical analysis of complexity then we analyse and compare the performances of the three approaches described previously

-

1.

Switching Monte Carlo method with exponential switching times;

-

2.

Switching Monte Carlo method with gamma switching times (with parameter );

-

3.

Resampling and Switching Monte Carlo method with gamma switching times (with parameter ).

On one test case, we compare numerically the Switching Monte Carlo method with gamma switching times with the Euler Monte Carlo method.

First, we consider a simple example for which all assumptions of Proposition 4.1 are satisfied.

Then we consider simulations involving a more standard payoff function occuring in finance (corresponding to the call option) that does not fulfill Assumption 4.1. However, this offers the opportunity to check the robustness of our approach out of theoritical assumptions.

In all cases, we consider

-

•

a drift coefficient ,

-

•

an initial condition ,

-

•

a terminal time .

The parameters of the switching time distributions is for the exponential distribution. Even if the exponential distribution gives a theoretical infinite variance (in cases we consider here), the numerical variance observed is finite so

it is interesting to compare the results obtained by the gamma distribution and the exponential distributions.

To implement efficiently the different methods on a computer using many cores (96 on our computer), we allocate particles to each core such that the total number of particles used is . When resampling is used, a resampling estimator is simulated independently on each core and we return the average estimator : .

Then the procedure is repeated independently for estimations, so as to approximate empirically the expectation and the variance of each estimator by the empirical average and variance computed on the estimates.

The whole procedure is then repeated for different values of from to , with .

We reported on the graphs the evolution of the estimator expectation as a function of and the related standard deviation is represented on - graphs. On each figure devoted to the standard deviation, the theoretical decrease at a rate is represented by the plot of a line with slope .

6.1 Complexity analysis

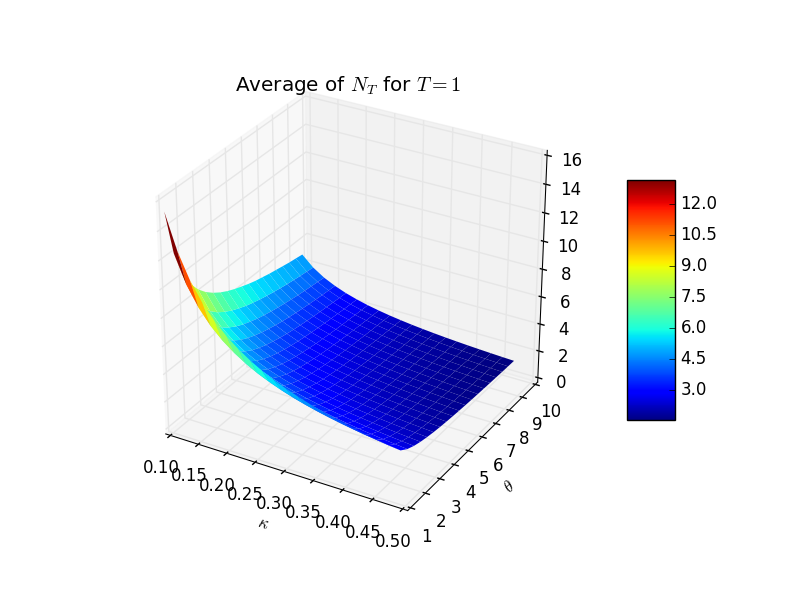

The Switching Monte Carlo method requires to simulate, for each trial, a random number of time steps, , before reaching . In order to analyze the impact of the parameters and on the complexity of the algorithm, we consider as a function of . As we couldn’t derive any analytical approximation, we have computed a numerical estimate which is reported on Figure 1 for different values of and .

One can observe that the expected number of time steps increases as or decreases. More precisely, can be accurately estimated by the following polynomial approximation:

for and , recalling that we are only interested by values of . Besides, at each switching time of each trial the computational complexity is given by

where are given constants, is the complexity of generating the switching time (according to an exponential or a gamma law depending on the approach), is the complexity for generating a Gaussian r.v.,

and the term in is the theoretical optimal cost for inversion by a method.

The global complexity of the algorithm without resampling for simulations is in high dimension:

Remark 6.1.

Notice that, based on our numerical tests, the cost, (in the gamma case), of generating a gamma r.v. with a rejection method is on average between and floating operations, whereas the cost, , of generating a Gaussian random variable requires around floating operations. Hence, for low dimension, the leading term corresponds to .

With resampling, we have to add some operations independent of the dimension of the problem: using the order statistics of the exponential law, we are able to generate some sorted uniformly distributed random variables that are used to select the particles during the selection step with a cost linear with .

Remark 6.2.

The resampling method, by imposing to store the states of all simulations simultaneously, gives a computational cost (including the memory access time) increasing slightly more than linearly with (see Figure 4 below). The advantage of the method without resampling comes from the fact that the memory access time is weaker so that the computational cost is strictly linear with the number of particles.

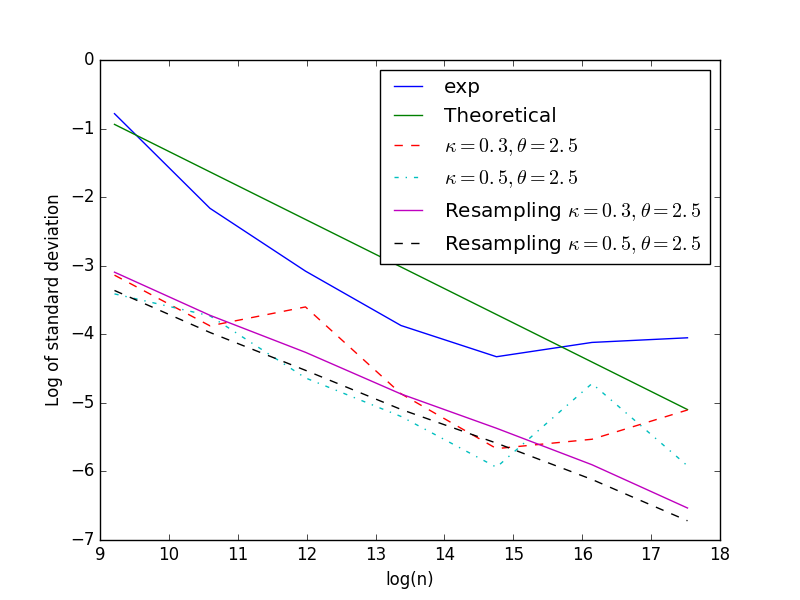

6.2 An example with , .

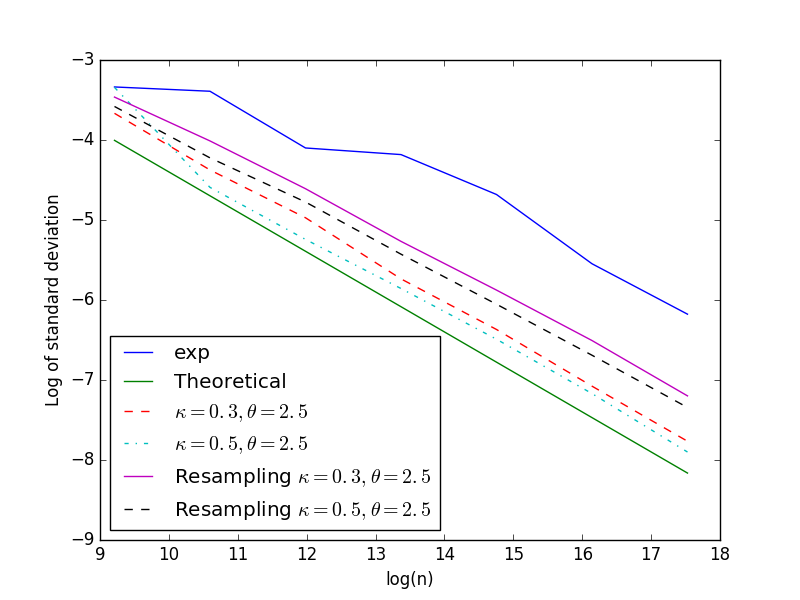

In dimension 1, we give on Figure 2 the convergence observed with the exponential law and the gamma law with and without resampling.

The method converges easily with the gamma laws.

Using the exponential distribution, the empirical standard deviation seems to decrease to zero but the rate cannot be diagnoseds: this is the consequence of an infinite theoretical variance.

On this case, the resampling doesn’t improve much the results because of the small variation of the function.

With the gamma laws, the linear decay of the log of the standard deviation follows the theory with a slope equal to with respect to .

6.3 One dimensional tests with .

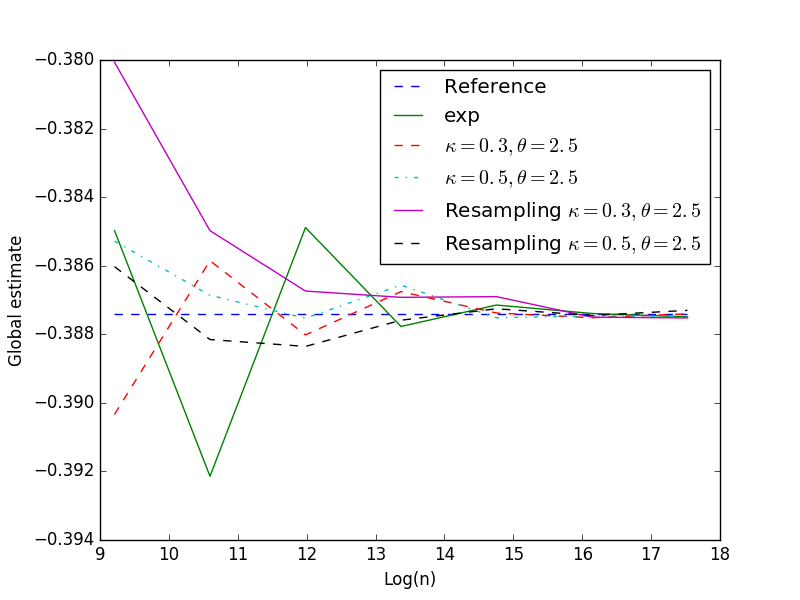

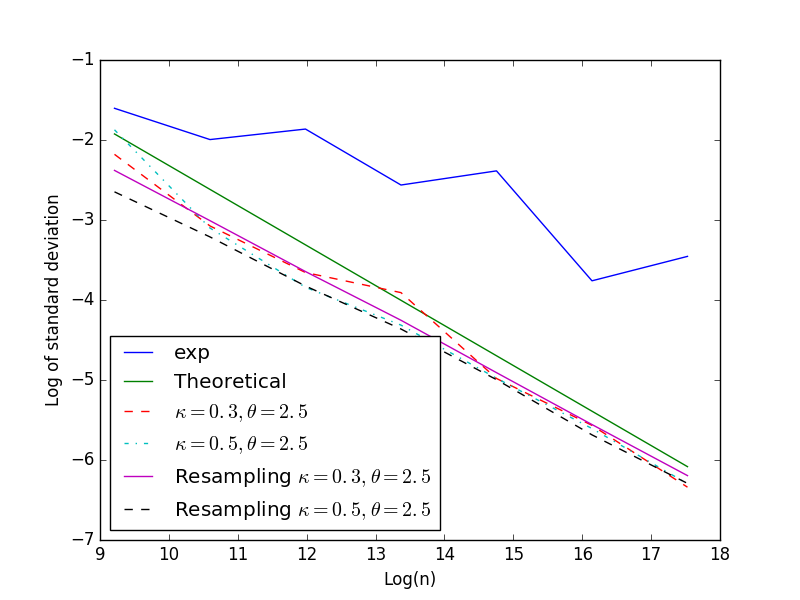

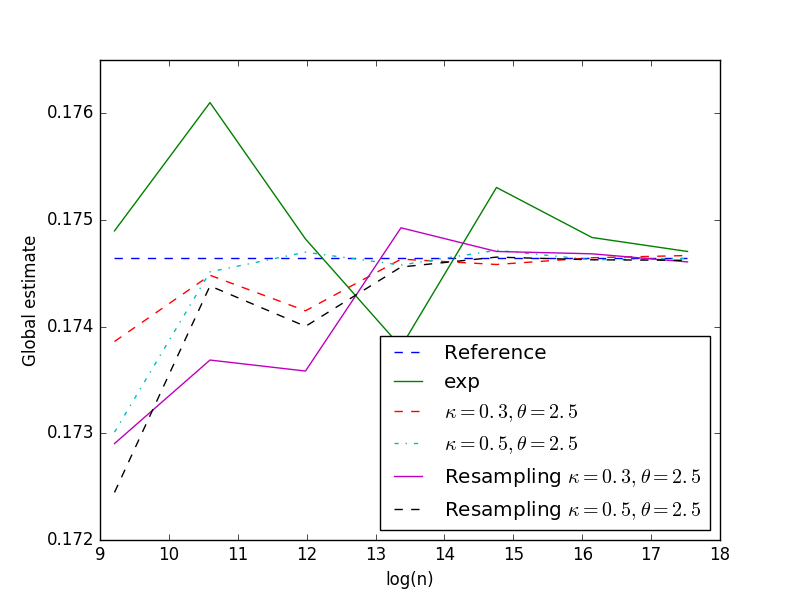

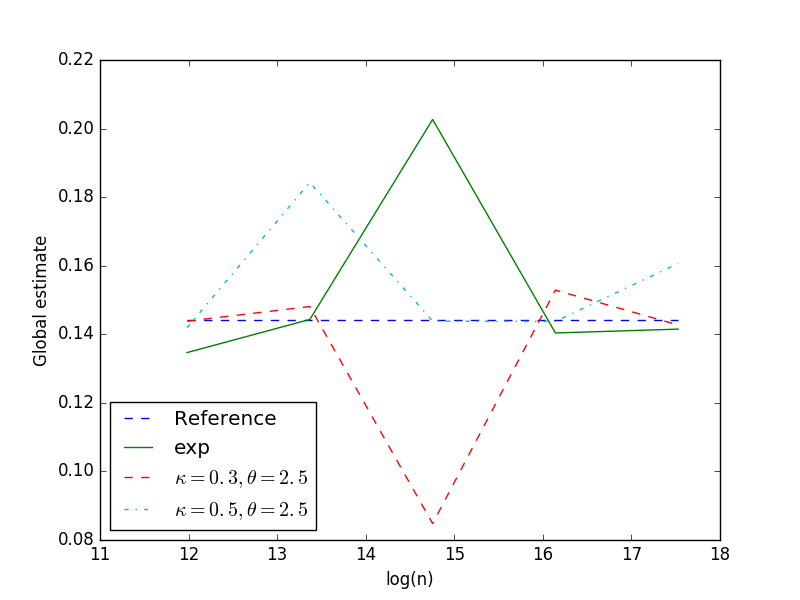

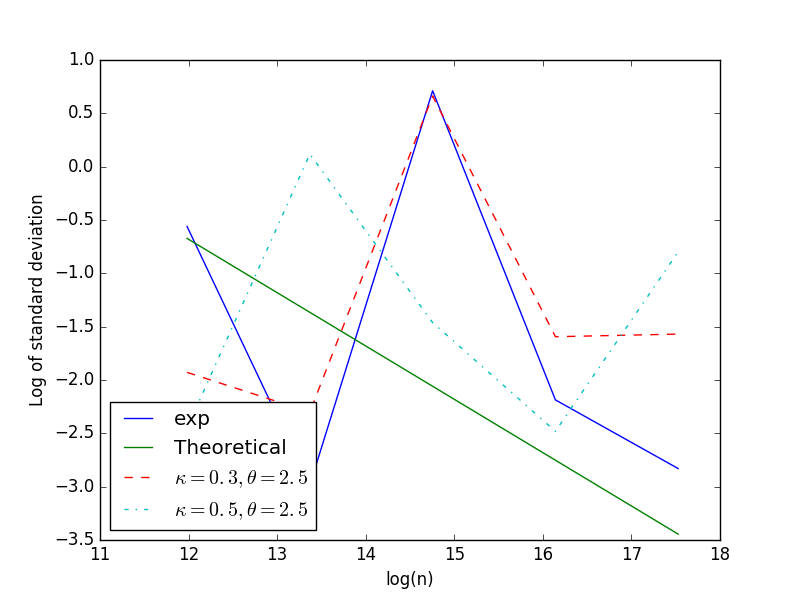

With this kind of function assumptions of Proposition 4.1 are not satisfied. We will show nevertheless that the method gives good results. Because the variance of the results is closely related to the diffusion coefficient variation, we will consider various examples with getting more and more space dependent.

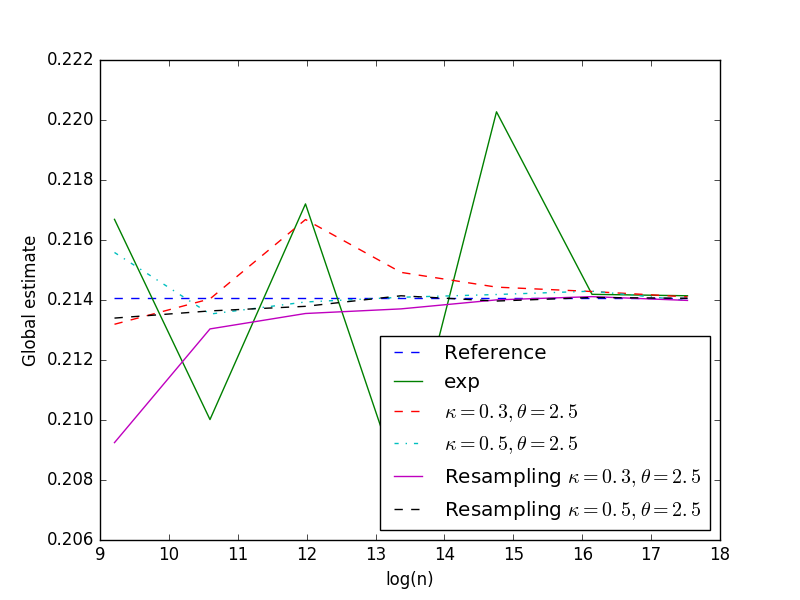

6.3.1

This second case shows some quite small variations of . The reference value is . Evolution of the global estimate and the standard deviation are given on Figure 3 for gamma and exponential laws.

In this simple case easily converging as in the first case, resampling doesn’t improve the standard deviation.

We are interested in comparing numerically the Switching Monte Carlo method (SMC) with the Euler Monte Carlo method (EMC). It is well known [21] that the error due the EMC method with a time discretization step, , and a number of particles, , can be decomposed into a bias term, , and a standard deviation term, . To achieve a fixed level of accuracy, by balancing the two types of errors we quasi-optimally chose and , where and respectively have been estimated using a reference calculation with particles and time steps and respectively using time steps. Using the empirical variance computed on SMC estimators, we have estimated the error, , of the SMC method for different numbers of particles . For each, error , we have used an Euler Monte Carlo (EMC) with a time step and simulations to achieve the same error . On Table 1, we have reported for each error, , and for each approach, SMC or EMC, the associated computing time (Time), mean estimate (Mean), number of particles (, ), and for the EMC approach, we have further reported the number of time steps.

| 8e-4 | 0.000398 | 0.000219 | 1.02 e-4 | 5.42e-5 | 2.67e-5 | 1.34e-5 | |

| SMC Time | 0.65 | 2.11 | 8.88 | 34.76 | 125.85 | 502.49 | 1991.43 |

| SMC Mean | 0.173861 | 0.174482 | 0.17415 | 0.174633 | 0.174583 | 0.174646 | 0.17466 |

| SMC | 10000 | 40000 | 160000 | 640000 | 2560000 | 1024e4 | 4096e4 |

| EMC Time | 0.11 | 0.93 | 5.62 | 55.5 | 369.67 | 3096.63 | 24429 |

| EMC Mean | 0.175225 | 0.174888 | 0.174615 | 0.174613 | 0.174674 | 0.174667 | 0.17465 |

| EMC | 432025 | 1779528 | 5879543 | 27e6 | 96e6 | 396e6 | 1.579e9 |

| EMC | 145 | 295 | 536 | 1151 | 2167 | 4402 | 8763 |

One can observe on Table 1 that for errors up to the SMC method appears to be slower than the Euler scheme by a factor between and whereas for very high precisions it begins to be more effective in the considered case.

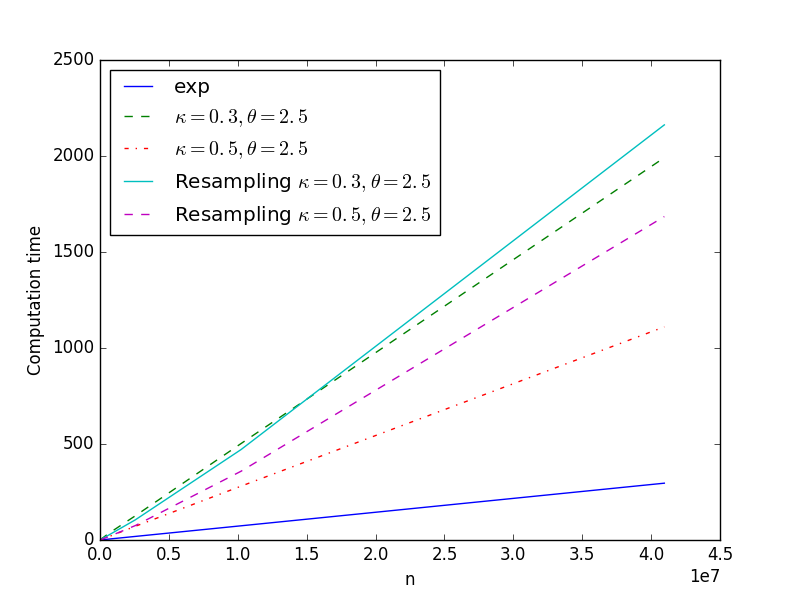

On Figure 4, we give the computional time of each method depending on the switching laws and their parameters.

One can observe on Figure 4 that indeed the computational time of the Switching Monte Carlo method is proportional to the number of particles. Of course, using a gamma distribution instead of an exponential one increases the number of switching times and hence the computational time.

One can observe that with resampling, the computational time increases slightly more than linearly with the number of particles.

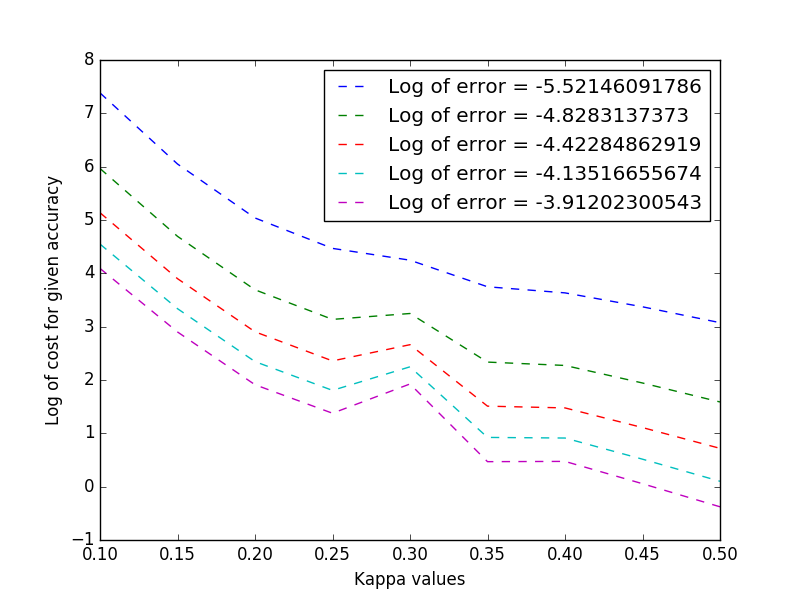

On Figure 5, for different levels of accuracy, we compute the computational time needed for the SMC method with gamma switching times to reach a given accuracy, depending on the parameter ( being fixed to ).

Clearly the optimal parameter is . In fact using a parameter doesn’t improve much the accuracy of the result but the computional time required is smaller.

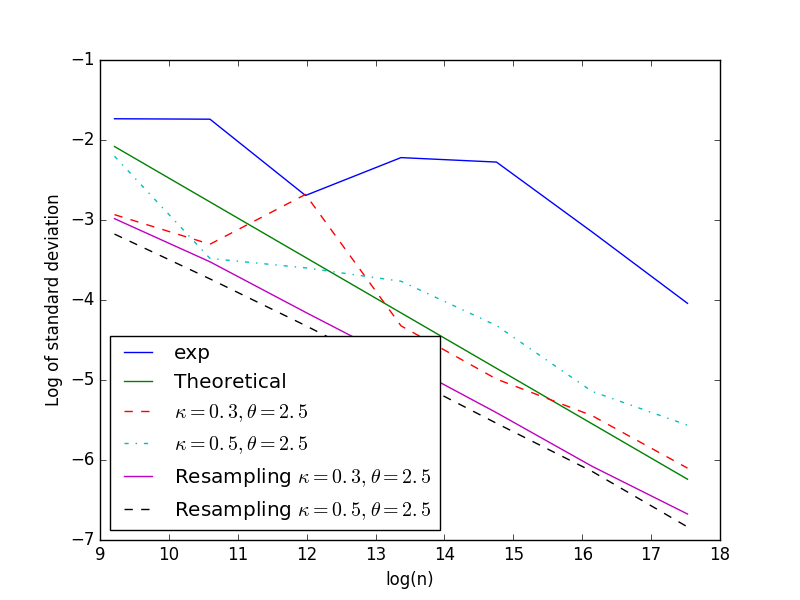

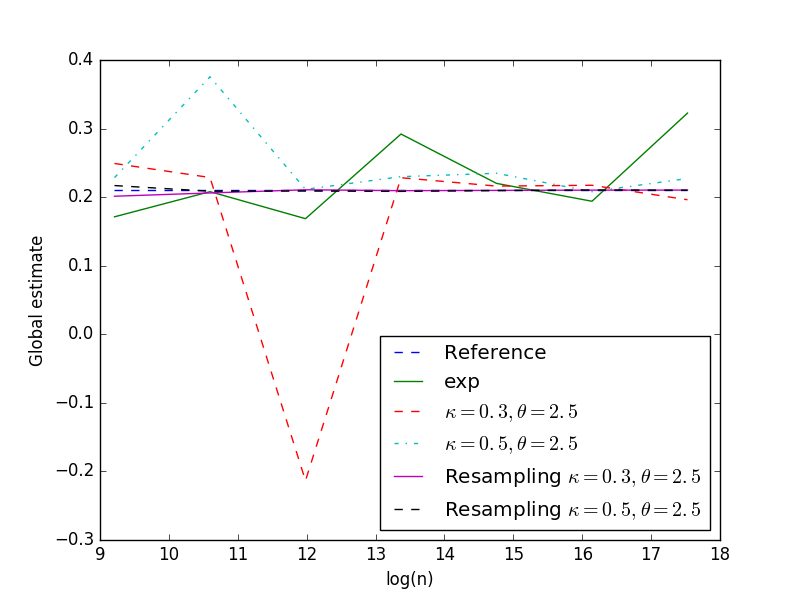

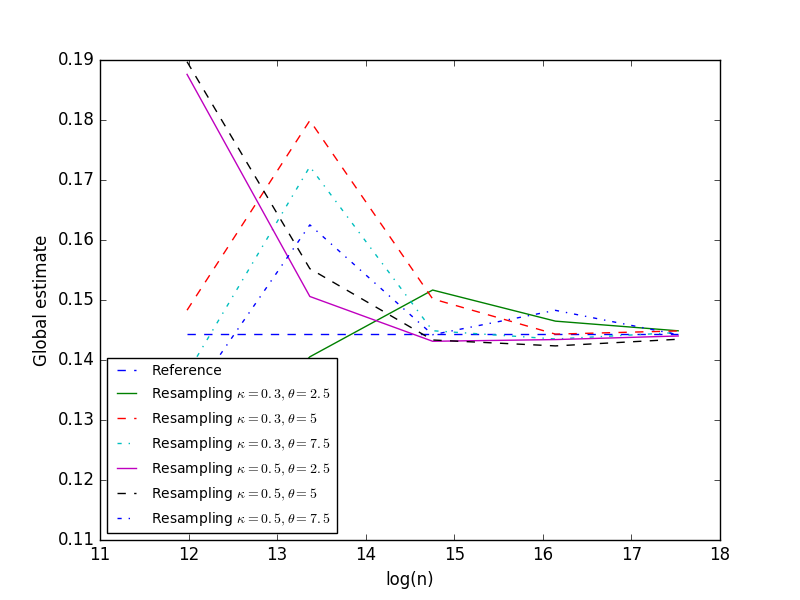

6.3.2 .

With this more difficult case, we report results obtained with , , with and without resampling for the gamma distribution and for the exponential distribution. The reference value is . Evolution of the mean estimate and the standard deviation are given on Figure 6.

With or without resampling, the standard deviation is decreasing steadily while using gamma distributions. As we quadruple the number of simulations, the standard deviation is roughly divided by two which is coherent with the theory. The convergence with the exponential law is erratic once more.

In the case of gamma distribution, the standard deviation with resampling is nearly half of the one without resampling clearly showing the interest in this method. Results with and are very similar especially with resampling, but the number of jumps increases as decreases and the computational time is nearly doubled with indicating that the optimal choice is to take .

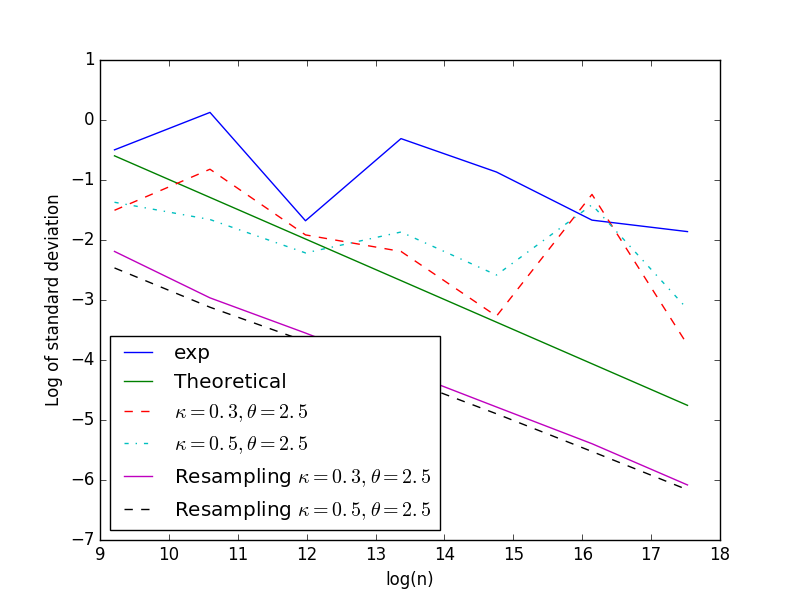

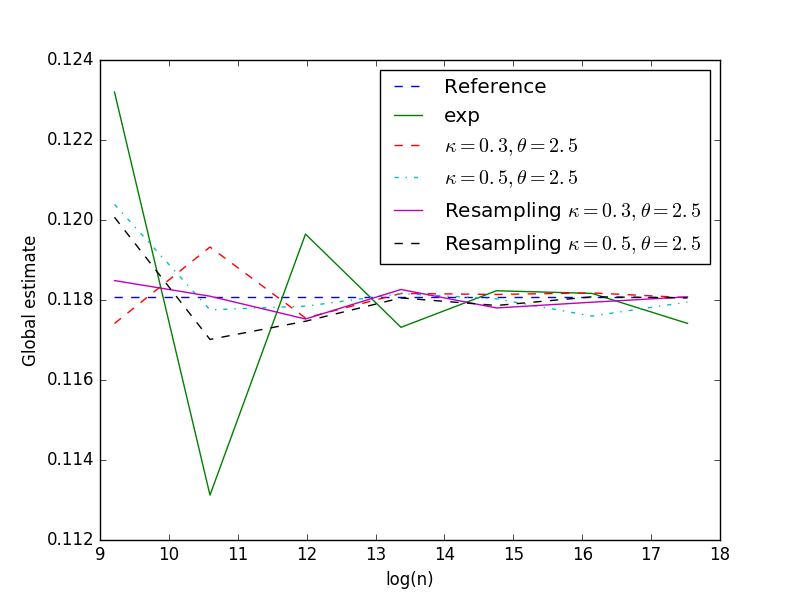

6.3.3 .

This case is more difficult than the two first ones. The reference value is . We keep and we use and . Figure 7, reveals that without resampling the SMC method shows difficulties to converge, while the resampling SMC method is always converging with a standard deviation decreasing at the rate . Besides the exponential case doesn’t seem to converge at all.

6.4 Some four dimensional cases with .

The diffusion coefficient is such that for any and for a given positive real, .

6.4.1

The reference solution is . We keep for the gamma distribution. For this first case, we plot on Figure 8 the results obtained with the exponential distribution and the gamma distribution with and without resampling.

On Figure 8, one can observe that for the resampling SMC method with gamma switching times, the log of the standard deviation decreases linearly, whereas without resampling, the decrease of standard deviation is not regular either with gamma or exponential switching times. On this test case, resampling is effective by reducing the standard deviation by a factor rougly equal to 2 and by stabilizing the results.

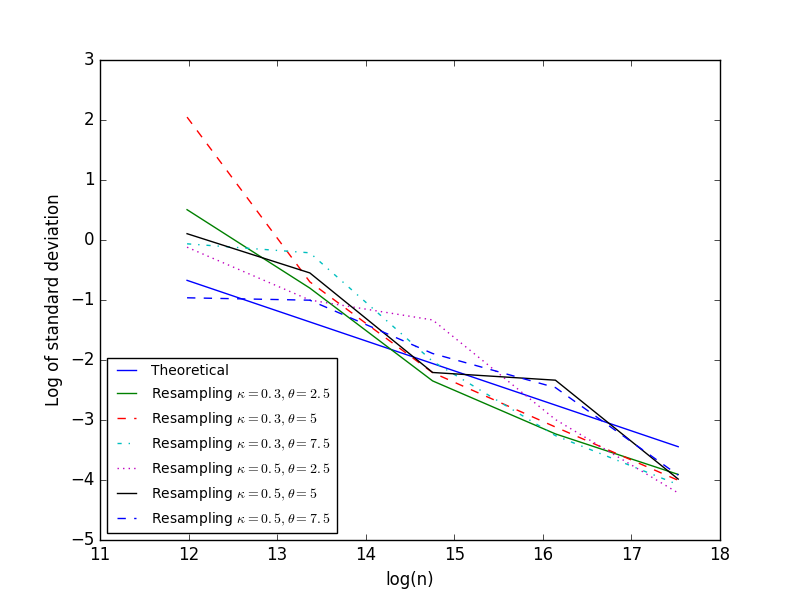

6.4.2

We give the results obtained without resampling on Figure 9. The method doesn’t seem to converge when a gamma distribution is used without resampling or when an exponential distribution is used.

On Figure 10, we only give the results obtained with resampling and the gamma distribution taking different parameters for and . We notice that the standard deviation calculated are far higher than in the previous case. We have difficulties to get the theoretical linear reduction in the standard deviation. The influence of parameter is not clear on the curves, but because higher gives higher jumps, it gives smaller computational times.

7 Appendix: Usefull notations and proof of Lemma 5.2

7.1 Classical notations and results

Let us recall somme classical notations and results stated in [7, 8]. We consider a Markov chain (with initial probability and transition kernel ) taking values on a sequence of measurable spaces and a sequence of positive potential functions defined on .

-

•

For all , we define the sigma-finite measure such that for any real valued bounded test function defined on ,

-

•

For all , let us define the probability measure obtained by normalization of and such that for any real valued bounded test function defined on ,

Notice that can be written as the following product involving the probability measures ,

-

•

For all , let us introduce the nonlinear operator, defined on the space of sigma-finite and non-negative measures and taking values in such that

(7.1) Then the nonlinear evolution of can be summarized by

(7.2) -

•

For all , let us define the Feynman-Kac semi-group associated to the distribution flow such that for all and any real valued bounded test function defined on ,

(7.3) Notice that for all , can be written as the transformation of via ,

(7.4) Moreover, for any sigma-finite non-negative measure ,

(7.5) - •

- •

-

•

Let us introduce the following notations

(7.8) -

•

For any , let us introduce the -algebra generated by the particle system until the -th generation, observe that since

where are i.i.d. according to conditionally to . Thus

(7.9) -

•

Moreover one can bound the conditional variance of as follows

(7.10)

We are now in a position to prove Lemma 5.2.

7.2 Proof of Lemma 5.2

Let us introduce the notation for any . Recalling (7.7) and notations (7.8) gives

Using (7.9) stating that gives

Recalling assumption (5.29), observe that for any

Then using the bound (7.10), with and as a test function implies

Using the above inequality and recalling that yields

Again recall that by assumption (5.29)

which finally yields

Adding the above inequality from to gives for any

We obtain by recursion

| (7.11) |

Now let us consider a test function verifying assumption (5.31). Using again (7.9) stating that gives

By (7.10) and Assumption (5.31), we obtain which yields

By (7.11) we finally get

as soon as and .

8 Appendix: Technicalities related to the proof of Lemma 3.1

This section provides technical arguments allowing for differentiating under the integral sign that are necessary to prove the second and third identity of (3.1).

8.1 Concerning the second identity of (3.1)

Assume the first identity of (3.1) is verified. Let us introduce the real valued function such that for any

| (8.1) |

where is the Gaussian process defined by (2.4) and is the real valued function defined on by (2.5). Recalling identity (3.4) and using Fubini’s lemma gives

| (8.2) |

Notice that by a simple application of Elworthy’s formula [10] (which simply results here in the Likelihood ratio of Broadie and Glasserman [4]), we get

| (8.3) | |||||

where denotes the centered and standard Gaussian density on and is the Malliavin weight defined at (3.3). Recall that and are Lipschitz w.r.t. the space variable and -Hölder continuous w.r.t. the time variable as stated at item 2. and 3. of Assumption 2 and that and are bounded as stated in Assumption 1. Thus there exists a finite constant depending on and that may change from line to line such that

Thus for any such that .

| (8.4) |

Since the term on the r.h.s of the above inequality is integrable w.r.t on one can differentiate under the integral sign in (8.2) which ends the proof of the second identity of (3.1).

8.2 Concerning the third identity of (3.1)

Let us introduce the valued function such that for any

| (8.5) |

where with

| (8.6) |

Observe that is differentiable w.r.t. the variable and for any and

where

| (8.7) |

Notice that does not depend on the pair , hence one can fix . Let us consider a fixed point , two indexes , and a point such that each coordinate for any and is fixed at a given value. We want to prove that exists and is continuous (which implies the differentiability of ) and to give an explicit expression for it. By the mean value theorem, there exists a real (to simplify the notations we will forget the dependence on ) such that for any

| (8.8) |

where denotes the vector of with zeros coordinates except for the coordinate that equals . Observe that in full generality the real resulting from the mean value theorem depends on and not only on . However, since we consider the specific situation where for all one can express this real as a function of . Consider the following equation w.r.t. the variable

One can check that there exists a solution to this equation. Indeed, taking and and recalling that , we obtain

which, by continuity of , implies the existence of a solution. Now we choose to take in equation (8.2), as the vector having the same coordinates as except that , this vector will be denoted by . Observe that by construction choosing implies

We are now interested in the limit of (8.2) as . The technical point will consist in applying Lebesgue theorem to permute the limit with the integral sign. First, by Lebesgue theorem, and observing that when , we have

Considering the integral term involving , using the Lipschitz and -Hölder properties of and , we get

so

where is locally bounded due to the non degeneracy hypothesis and the Lipschitz properties in assumption 2. The rhs of the previous equation is integrable so that we can use the Lebesgues Theorem,

We finally obtain

which ends the proof.

AKNOWLEDGMENTS

The authors are very grateful to the anonymous Referees for their careful reading of the paper and the suggestions which have largely contributed to improve the first submitted version.

References

- [1] P. Andersson and A. Kohatsu-Higa. Unbiased simulation of stochastic differntial equations using parametrix expansions. to appear in Bernoulli [Online] Available: http://www.bernoulli-society.org/index.php/publications/bernoulli-journal-papers, 2016.

- [2] V. Bally and A. Kohatsu-Higa. A probabilistic interpretation of the parametrix mehod. The Annals of applied Probability, 25(6):3095–3138, 2015.

- [3] A. Beskos and G. Roberts. Exact simulation of diffusions. Annals of applied Probability, 15(4):2422–2444, 2005.

- [4] M. Broadie and P. Glasserman. Estimating security prices using simulation. Manag. Sc., 42:269–285, 1996.

- [5] K. Burrage, P. M. Burrage, and P. Tian. Numerical methods for strong solutions of stochastic differential equations: an overview. Proceedings of the Royal Society of London, Series 1 460:373–402, 2004.

- [6] N. Chen and Z. Huang. Localization and exact simulation of brownian motion-driven stochastic differential equations. Mathematics of Operations Research, 38(3):591–616, 2013.

- [7] P. Del Moral. Feynman-Kac formulae. Probability and its Applications (New York). Springer-Verlag, New York, 2004. Genealogical and interacting particle systems with applications.

- [8] P. Del Moral. Mean field simulation for Monte Carlo integration. Monographs on Statistics and applied Probability. Chapman and Hall, 2013.

- [9] D. Duffie and P. W. Glynn. Efficient Monte Carlo simulation of security prices. Annals of applied Probability, 5(4):897–905, 1995.

- [10] E. Fournié, J.M. Lasry, J. Lebuchoux, P.L. Lions, and N. Touzi. Applications of Malliavin calculus to Monte Carlo methods in finance. Finance Stoch., 3(4):391–412, 1999.

- [11] E. Fournié, J.M. Lasry, J. Lebuchoux, and N. Touzi. Some applications of malliavin calculus to Monte Carlo methods in finance. Finance and Stochastics, 3:391–412, 1999.

- [12] M. B. Giles. Multilevel Monte Carlo path simulation. Operations Research, 56(3):607–617, 2008.

- [13] P. Henry-Labordère. Countreparty risk valuation : A marked branching diffusion approach. Available at SSRN: http://ssrn.com/abstract=1995503 or http://dx.doi.org/10.2139/ssrn.1995503, 2012.

- [14] P. Henry-Labordère, N. Oudjane, X. Tan, N. Touzi, and X. Warin. Branching diffusion representation of semilinear pdes and Monte Carlo approximations. 2016.

- [15] P. Henry-Labordère, X. Tan, and N. Touzi. A numerical algorithm for a class of bsde via branching process. Stochastic Processes and their Applications, (124):1112–1140, 2014.

- [16] P. Henry-Labordère, X. Tan, and N. Touzi. Unbiased simulation of stochastic differential equations. 2016.

- [17] B. Jourdain and M. Sbai. Exact retrospective Monte Carlo computation of arithmetic average asian options. Monte Carlo Methods and Applications, 13(2):135–171, 2007.

- [18] P. E. Kloeden and E. Platen. Numerical solution of stochastic differential equations, volume 23 of Applications of Mathematics (New York). Springer-Verlag, Berlin, 1992.

- [19] G. N. Milstein. Approximate integration of stochastic differential equations. Theory of Probability & Its Applications, 19(3):557–600, 1975.

- [20] C. H. Rhee and P. W. Glynn. Unbiased estimation with square root convergence for sde models. Operations Research, 63(5):1026–1043, 2015.

- [21] D. Talay and L. Tubaro. Expansion of the global error for numerical schemes solving stochastic differential equations. Stochastic Analysis And Applications, 8(4):483–509, 1990.