Uniform bounds for Black–Scholes implied volatility

Abstract.

In this note, Black–Scholes implied volatility is expressed in terms of various optimisation problems. From these representations, upper and lower bounds are derived which hold uniformly across moneyness and call price. Various symmetries of the Black–Scholes formula are exploited to derive new bounds from old. These bounds are used to reprove asymptotic formulae for implied volatility at extreme strikes and/or maturities.

1. Introduction

We define the Black–Scholes call price function by the formula

where is the standard normal density and is its distribution function. As is well known, the financial significance of the function is that, within the context of the Black–Scholes model [4], the minimal replication cost of a European call option with strike and maturity written on a stock with initial price is given by

where is the dividend rate, is the interest rate and is the volatility of the stock. Therefore, in the definition of , the first argument plays the role of log-moneyness of the option and the second argument is the total standard deviation of the terminal log stock price.

Of the six parameters appearing in the Black–Scholes formula for the replication cost, five are readily observed in the market. Indeed, the strike and maturity date are specified by the option contract, and the initial stock price is quoted. The interest rate is the yield of a zero-coupon bond with maturity and unit face value, and can be computed from the initial bond price . Similarly, the dividend rate can computed from the stock’s initial time- forward price .

As suggested by Latané & Rendleman [17] in 1976, the remaining parameter, the volatility , can also be inferred from the market, assuming that the call has a quoted price . Indeed, note that for fixed , the map is strictly increasing and continuous, so we can define the inverse function

by

The implied volatility of the call option is then defined to be

Because of its financial significance, the function has been the subject of much interest. For instance, approximations for can be found in several papers [5, 7, 19, 22]. Unfortunately, there seems to be only one case where the function can be expressed explicitly in terms of elementary functions: when we have

and hence

The main contribution of this article is to provide bounds on the quantity in terms of elementary functions of . As an example, in Proposition 4.3 below we will see that

| (1) |

for every such that .

We list here two possible applications of such bounds. When , the function can be evaluated numerically. A simple way to do so is to implement the bisection method for finding the root of the map . That is to say, for fixed pick two points such that and . By the intermediate value theorem, we know that the root is in the the interval . We then let be the midpoint. If we know that the root is in the the interval , in which case we relabel as . Similarly, if we relabel as . This process is repeated until , where is a given tolerance level whereupon we declare . (We note here that a more sophisticated idea is apply the Newton–Raphson method as suggested by Manaster & Koehler [21] in 1982. We will return to this idea in Section 3.)

In order to implement the bisection method, we need a lower bound and upper bound to initialise the algorithm. However, aside from the obvious lower bound , there do not seem to be many well-known explicit upper and lower bounds on the quantity which hold uniformly in . This note provides such bounds, and indeed, equation (1) is an example.

We now consider another application of our bounds. Consider a market model with a zero-coupon bond with maturity date whose time- price is and a stock with time -price . Suppose the initial price of a call option with strike and maturity is given by

where the expectation is under a fixed -forward measure. Further, suppose the stock’s initial time- forward price is given by

(If the stock pays no dividend, static arbitrage considerations would imply . We do not need this formula here so the stock is allowed to pay dividends in the present discussion; however, we will return to this point in Remark 4.13 below.) Now, equation (1) implies that the implied volatility is bounded by

| (2) | ||||

Note that the above bound is the composition of two ingredients: the model-dependent formulae for the quantities and , and a uniform and model-independent bound on the function .

There has been much recent interest in implied volatility asymptotics. See for instance the papers [2, 3, 6, 9, 12, 13, 14, 15, 18, 23, 26] for asymptotic formulae which depend on minimal model data, such as the distribution function or the moment generating function of the returns of the underlying stock. Paralleling the discussion above, such asymptotic formulae can be seen as compositions of two limits: first, the asymptotic shape of the call surface as predicted by the model at, for instance, extreme strikes and/or maturities; and second, asymptotics of the model-independent function . The uniform bounds on that are presented in this note are used to provide short, new proofs of these second model-independent asymptotic formulae.

In their long survey article, Andersen & Lipton [1] warn that many of the asymptotic implied volatility formulae that have appeared in recent years may not be applicable in practice, since typical market parameters are usually not in the range of validity of any of the proposed asymptotic regimes. Our new bounds on the function are uniform, and hence side-step the critique of Andersen & Lipton.

The rest of the note is organised as follows. In Section 2 we discuss various symmetries of the Black–Scholes pricing function . These symmetries will be used repeatedly throughout the remainder of the note. In Section 3 the Black–Scholes implied total standard deviation function is represented as the value function of several optimisation problems. These results constitute the main contribution of this note since they allow to be bounded arbitrarily well from above and below by choosing suitable controls to insert into the respective objective functions. In Section 4 these bounds are used to reprove some known asymptotic formulae. As a by-product, we derive formulae which have the same asymptotic behaviour as the known formulae, but are guaranteed to bound either from above or below.

2. Put-call and close-far symmetries

The Black–Scholes call price function contains a certain amount of symmetry. In order to streamline the presentation of our bounds, we begin with an exploration of two of these symmetries.

To treat the two cases and as efficiently as possible, we begin with an observation. Suppose is the normalised price of a call option with log-moneyness . Then by the usual put-call parity formula, the corresponding normalised price of a put option with the same log-moneyness is

Now if is for some , then we have

The above calculation is the well-known Black–Scholes put-call symmetry formula. We have just proven the following result:

Proposition 2.1.

For any and we have

One conclusion of proposition 2.1 is that it is sufficient to study the function only in the case . Indeed, to study the case one simply applies the above put-call symmetry formula.

We now come to another, less well-known, symmetry of the Black–Scholes formula. While put-call symmetry involves replacing the log-moneyness with , the symmetry discussed here involves replacing the total standard deviation with . By put-call symmetry, we can confine our discussion to the case .

Proposition 2.2.

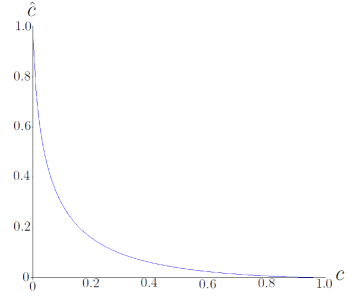

For all and , let

Then and we have

Figure 1 is shows the graph of when .

Proof.

We must prove that

or equivalently

The above identity can be verified by differentiating both sides with respect to , and using the Black–Scholes vega formula: for , we have

∎

Remark 2.3.

Fix and , and let . Note that when is very small, and indeed it is a straightforward exercise to verify (see Section 4) that

On the other hand, we have when is very large, and furthermore

In the context of the Black–Scholes model, the quantity has the interpretation as the total standard deviation , where is the volatility and is the maturity date of the option. Proposition 2.2 then is a symmetry relation between the prices of short-dated and long-dated options.

We conclude this section with some easy observations which we will use later.

Proposition 2.4.

For all , the function is convex and satisfies the functional equation

holds for all .

Proof.

It is easy to see that is strictly increasing. That is convex follows from the fact that its gradient is increasing.

That the functional equation is proven by noting

and using the fact that that is strictly increasing. ∎

Proposition 2.5.

For , let

Then

where .

Proof.

By setting and hence , the identity can be proven by computing the derivative with respect to of the left-hand side, and note that it is vanishes identically. ∎

Remark 2.6.

3. Various optimisation problems

This section contains one of the main results of this note, formulae for the function in terms of various optimisation problems. The first result is that can be calculated by solving a minimisation problem. In particular, we can use this formula to find an upper bound simply by evaluating the objective function at a feasible control.

Theorem 3.1.

For all and we have

Furthermore, if , then the two infima are attained at

where .

Remark 3.2.

We are using the convention that for and for .

The following proof is due to Pieter-Jan De Smet [25], simplifying the proof in an early version of this paper. The idea is essentially that the inequality

holds for all with equality if and only if .

Proof.

Fix and and let be such that . Note that for any we have

There is equality from the first to second line only if , and there is equality from the second to the third line only if . Rearranging then yields

Let in the above inequality to obtain the first expression. ∎

Let

| (3) |

and

| (4) |

and note that

in line with put-call symmetry. We use this notation to compute in terms of a maximisation problem. This representation can be used, in principle, to find lower bounds.

Theorem 3.3.

Let be the space of continuous functions on . For and , we have

for any .

Proof.

In light of Proposition 2.2 we now give a representation of in terms of a minimisation problem. We restrict attention to with no real loss thanks to put-call symmetry.

Proposition 3.4.

For and we have

Proof.

Of course, there are other representations of in terms of an optimisation problems. For instance, we have

Indeed, this simple observation underlies the bisection method discussed in the introduction.

We conclude this section with a slightly more interesting representation. It be can used to find upper and lower bounds of , at least in principle. However, in practice it is not clear how to choose candidate controls, so we do not explore this idea in the sequel. This result is due to Manaster & Koehler [21], and is motivated by the Newton–Raphson method for computing implied volatility numerically.

Proposition 3.5 (Manaster & Koehler).

Fix and . If then

Otherwise, if then

Proof.

The restriction of to is convex, as can be confirmed by differentiation. Hence, by the Black–Scholes vega formula, we have

for any . Fixing and letting we have proven

as desired. Similarly, since the restriction of to is concave the second conclusion follows. ∎

4. Uniform bounds and asymptotics

In this section, we will offer quick proofs of some asymptotic formulae for the function . These formulae already appear in the literature, but the important novelty here is that we will derive bounds on the function which hold uniformly, not just asymptotically. To obtain upper bounds in most cases, we simply choose a convenient or to plug into Theorem 3.1. Note that the proposed upper bound is close to the true value of when, for instance, the proposed value of is close to the minimiser . In principle, lower bounds could be found by choosing convenient controls into Theorem 3.3. However, in practice, we have found other arguments, while lacking the same unifying principle, which do have the advantage of being simple. In the proofs that follow, we usually only consider the case, as the case follows directly from Proposition 2.1.

Before we begin, we need a lemma regarding the asymptotic behaviour of the standard normal quantile function .

Lemma 4.1.

As we have

In particular, we have

Proof.

Let for large and let

In this notation we have the identity

Since it is well known that as we have

or equivalently

Plugging in this limit into the identity yields the first conclusion, and Taylor’s theorem yields the second. ∎

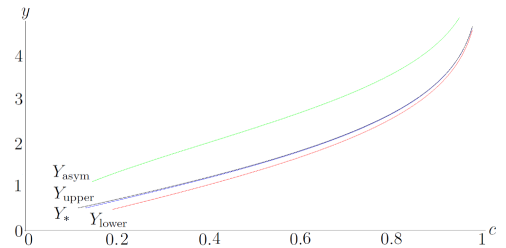

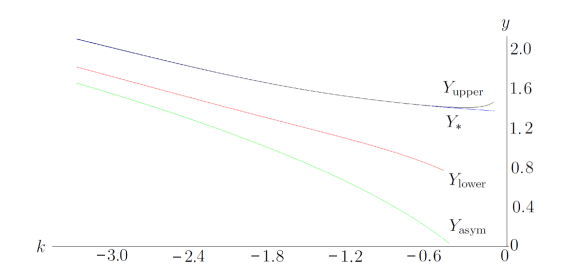

The first example comes from [26]. This asymptotic formula considers the behaviour of when is close to its upper bound of . This result is useful in studying implied volatility at very long maturities, when the strike is fixed.

Theorem 4.2.

For fixed , we have

as .

The proof of the above theorem relies the following simple bounds which hold uniformly in .

Proposition 4.3.

Fix and . For we have

and for we have

Proof.

For the upper bound, let in Theorem 3.1.

For the lower bound, let . Note that is decreasing and hence

when . In the case when , note that

and that

Now appeal to the put-call parity formula of Proposition 2.1. ∎

Proof of Theorem 4.2.

Figure 2 illustrates the behaviour of as , compared with the uniform upper and lower bounds of Proposition 4.3 and the asymptotic formula in Theorem 4.2. We fixed the log-moneyness and plotted four functions:

-

(1)

is the upper bound from Proposition 4.3;

-

(2)

is the true function of our interest;

-

(3)

is the lower bound from Proposition 4.3;

-

(4)

is the asymptotic shape from Theorem 4.2.

Note that as predicted. Also, it is interesting to see that is remarkably good approximation over large range of . Finally, note that for this range of . Indeed, is a rather poor approximation of for realistic values of the normalised call price due to the fact that the error term is actually increasing for !

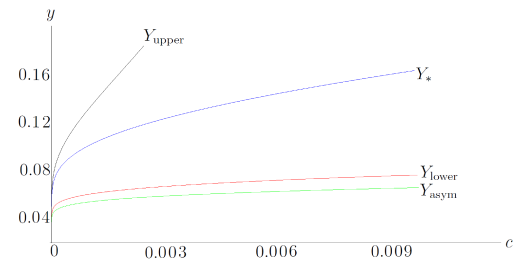

The next example we consider in this section is due to Roper & Rutkowski [23] and deals with the case where is close to its lower bound . In particular, this regime is useful for studying the implied volatility smile of options very near maturity.

Theorem 4.4 (Roper & Rutkowski).

If then

as . If then

as , where .

As always, we will prove the asymptotic result by finding uniform bounds. As discussed in Section 2, we can reuse of the bounds which are tight when is close to 1 by first bounding the function .

Proposition 4.5.

For and , we have

where

| (5) |

Proof.

For the upper bound, simply note that

Now, we appeal to the upper bound in Proposition 4.3 to conclude that

To complete the proof, note that the bound

which holds for all . ∎

We now prove an inequality which provides an easy way to convert bounds which are good when into bounds which are good when .

Proposition 4.6.

Proof.

Remark 4.7.

The inequality

which holds for all and , has an appealing symmetry!

Proof of Theorem 4.4.

First fix . Using the second lower bound from Proposition 4.6, together with Lemma 4.1, we have that

Similarly, since Lemma 4.1 implies that the quantity from Proposition 4.5 is of asymptotic order

as thanks to Proposition 4.1, the upper bound follows.

The case follows from the put-call symmetry of Proposition 2.1. ∎

Figure 3 illustrates the behaviour of as , compared with the uniform upper and lower bounds of Proposition 4.6 and the asymptotic formula in Theorem 4.4. We fixed the log-moneyness and plotted four functions:

-

(1)

is the upper bound from Proposition 4.6;

-

(2)

is the true function of our interest;

-

(3)

is the lower bound from Proposition 4.6;

-

(4)

is the asymptotic shape from Theorem 4.4.

Note again that as predicted. Finally, note that for this range of .

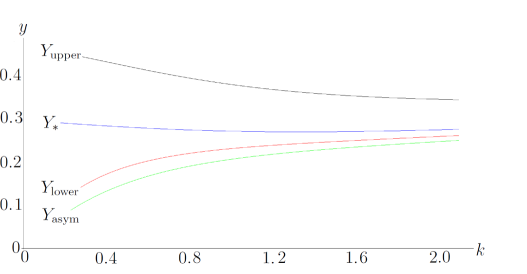

The next example is due to Gulisashvili [13]. This result is useful in studying the wings of the implied volatility surface for extreme strikes but fixed maturity date.

Theorem 4.8 (Gulisashvili).

If as then

If as then

where .

As before, the proof will rely on appropriate uniform bounds:

Proposition 4.9.

Fix and . If we have

and for we have

where .

Proof.

Consider the case . For the upper bound, let in Theorem 3.1.

For the lower bound, let . Observe that

The conclusion follows from noting that the strictly increasing map

from to is the inverse of the map

from to .

The case where is handled by put-call symmetry as always. ∎

Remark 4.10.

The idea behind the lower bound is the simple inequality

which holds for all .

Proof of Theorem 4.8.

For , we apply Proposition 4.9 and Lemma 4.1 to get

where we have used as to control the error from the first term, and the bound to control the error from the second term. Similarly, for the upper bound Proposition 4.9 and Lemma 4.1 yield

The case is similar. ∎

Figure 4 illustrates the behaviour of when as , compared with the uniform upper and lower bounds of Proposition 4.9 and the asymptotic formula in Theorem 4.8. We have chosen the function according to the variance gamma model. That is, we fix a time horizon and let

where

and and are real constants, and the process is a Brownian motion subordinated to the gamma process , which is an independent Lévy process with jump measure for some constant . The constant is chosen so that

It is well known that has the gamma distribution with mean and variance . By a routine calculation involving the moment generating functions of the normal and gamma distribution, we find the moment generating function of to be

Therefore, we must set

Note that we must assume the parameters are such that

to ensure that is real. Recall that the random variable has the interpretation of the ratio of the time- price of some asset to its initial time- forward price. The expected value is computed under a fixed time- forward measure. Hence models initial normalised price of a call option with log-moneyness and maturity . We use the parameters , and as suggested by the calibration of Madan, Carr and Chang [20] and set .

As before, we plotted four functions:

-

(1)

is the upper bound from Proposition 4.9;

-

(2)

is the true function of our interest;

-

(3)

is the lower bound from Proposition 4.9;

-

(4)

is the asymptotic shape from Theorem 4.8.

As always, note that as predicted. Finally, note that for this example. It is worth remarking that for the points on the extreme right side of the graph of the moneyness and normalised call price are outside the range of typical liquid market prices.

The recent paper [9] of De Marco, Hillairet & Jacquier studies a similar asymptotic regime as the case of Theorem 4.8, except now the assumption is that . See also the paper of Gulisashvili [15] for further refinements. The motivation is to study the left-wing behaviour of the implied volatility smile in the case where the price of the underlying stock may hit zero. The first two terms in the following expansion have been known for a few years; see for instance [27].

Even more recently, Jacquier & Keller-Ressel [16] have interpreted the corresponding (via Proposition 2.1) right-wing formula in terms of a market model with a price bubble. We will comment on this interpretation below.

Theorem 4.11 (De Marco, Hillairet & Jacquier).

Suppose as where . Then letting we have

as , where

(Jacquier & Keller-Ressel). Furthermore, suppose as where . Then

where

Our proof of Theorem 4.11 reuses the uniform lower bound from Proposition 4.9. However, another upper bound is needed in this situation:

Proposition 4.12.

Fix and . If , we have

and if we have

where .

Proof.

In the statement of Theorem 3.1, let if , or let if . ∎

Proof of Theorem 4.11.

Figure 5 illustrates the behaviour of when as , where , compared with the uniform upper of Proposition 4.12, lower bounds of Proposition 4.9 and the asymptotic formula in Theorem 4.11. We have chosen the function according to the Black–Scholes model with a jump to default. That is, we fix a horizon and let

where

and and are positive constants, the process is a Brownian motion and the random variable is independent of and exponentially distributed with rate , so that

Note that

On the other hand, it is straightforward to calculate

We use the parameters and with time horizon .

As before, we plotted four functions:

-

(1)

the upper bound from Proposition 4.12;

-

(2)

is the true function of our interest;

-

(3)

is the lower bound from Proposition 4.9;

-

(4)

is the asymptotic shape from Theorem 4.11.

As always, note that as predicted, that is a surprisingly good approximation for , and that for this example. For the left-hand points of the graph, the moneyness is somewhat outside the range of typical liquid market prices.

Remark 4.13.

To compute the implied volatility for a given model, one generally needs three ingredients: the bond price , the forward price and the call price . Consider the case where the interest rate is zero and the underlying stock pays no dividends. In particular, for this discussion .

In the discrete time case, one typically models the stock price as a martingale so that there is no arbitrage. The call price is then calculated as

with the justification that the above price is consistent with no-arbitrage in general, and in the case of a complete market, the expected payout under the unique risk-neutral measure is the replication cost of the option and hence the unique no-arbitrage price. Similarly, we have for the forward price the following formula

In the continuous time setting, things are more subtle because of the existence of doubling strategies. If one assumes the NFLVR notion of no-arbitrage, then by Delbaen & Schachermayer’s fundamental theorem of asset pricing [10] the asset prices are sigma-martingales, but not necessarily true martingales. In particular, given a dynamic model of the underlying process , this no-arbitrage condition alone does not uniquely specify the call and forward prices, even in a complete market. See, for instance, the paper of Ruf [24] for a discussion of this issue. When the market is complete, a candidate call price is the minimal replication cost

Another sensible way to price the call is to assume that the put price is its minimal replication cost and the call is priced by put-call parity:

Similarly, the forward price can be either given by static replication

or by dynamic replication

Of course, if is a true martingale the corresponding candidate prices agree; however, there has been recent interest in models where, for instance, the process is a non-negative strict local martingale, and hence a strict supermartingale. (Such price processes are often described as bubbles; see, for instance, the paper of Cox & Hobson [8].)

The result of Jacquier & Keller-Ressel quoted here as the second half of Theorem 4.11 corresponds to choosing and so that the implied volatility is

We note here that this convention for defining implied volatility was also adopted in [26]. On the other hand, note that the convention and is used in equation (2) of the introduction.

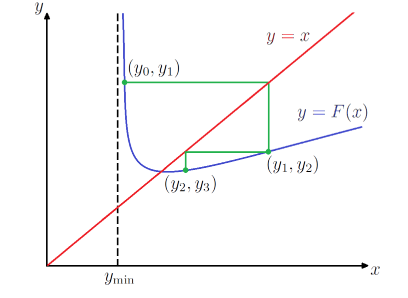

We conclude with some remarks on the bounds and asymptotic formulae in this section. The numerical results suggest that for at least some situations, one of the upper or lower bounds is a better approximation to the implied total standard deviation than the corresponding lowest order asymptotic formula. One could argue that with more terms in the asymptotic series, better accuracy could be attained with the asymptotics. Although such a claim is indeed plausible, there are a few reasons why it is beside the point.

First, the numerical results presented here should only be considered a proof of concept, rather than a head-to-head competition between state-of-the-art approximations. Nevertheless, it is worth noting both the given bounds and the asymptotic formulae are only approximations, and therefore have an error term. But unlike the error terms of an asymptotic formula, the error term for our bounds have a known sign.

Second, given one bound, the theorems of Section 3 give a systematic way of finding a better bound. Indeed, fix with , and let . Suppose it known that

where is some given approximation. Define by

where

and is the functions defined by equation (3) of Section 3. Letting

we have by Theorem 3.1 that

However, more is true. Note that the map has a unique fixed point . Since

we conclude by the continuity of that for , and more importantly, that for . In particular,

That is, is a better approximation of and the error term has the same sign as the original approximation. Of course, this process can iterated. Letting we see that the sequence is decreasing and .

Notice that this sequence converges very rapidly. Indeed, by Taylor’s theorem

for some . Since minimises we have

and hence, by the continuity of , we have

as .

Furthermore, we can find our initial upper bound by choosing any and letting . This procedure is illustrated by the cobweb diagram of Figure 6. Of course, the convergence can be helped along by an inspired choice of as discussed at the beginning of this section.

The above discussion of a rapidly converging sequence should be contrasted with the approach taken, for instance, in the paper of Gao & Lee [12]. There a systematic method of computing terms in the asymptotic series for implied volatility is obtained. However, unlike the procedure discussed above, an asymptotic series may diverge as more terms are added.

A third and final point is that the approximations for the implied total standard deviation are not particularly interesting on their own. Indeed, to use the formulae in Proposition 4.9 one must already know the normalised bond price . If this quantity is to be calculated numerically from a certain model, one might as well compute the numerically also. The point of these bounds is to be used in conjunction with other, model dependent bounds on to obtain useful bounds on the quantities of interest.

5. Acknowledgement

This work was presented at the Conference on Stochastic Analysis for Risk Modeling in Luminy and the Tenth Cambridge–Princeton Conference in Cambridge. I would like to thank the participants for their comments. I would also like to thank the anonymous referees whose comments on earlier drafts of this paper greatly improved the present presentation. Finally I would like to thank the Cambridge Endowment for Research in Finance for their support.

References

- [1] L. Andersen and A. Lipton. Asymptotics for exponential Lévy processes and their volatility smile: survey and new results. International Journal of Theoretical and Applied Finance 16(01): 1350001. (2013)

- [2] S. Benaim and P. Friz. Regular variation and smile asymptotics. Mathematical Finance 19(1): 1–12. (2009)

- [3] S. Benaim and P. Friz. Smile asymptotics. II. Models with known moment generating functions. Journal of Applied Probability 45(1) 16–23. (2008)

- [4] F. Black and M. Scholes. The pricing of options and corporate liabilities. Journal of Political Economy 81:637–654. (1973)

- [5] M. Brenner and M.G. Subrahmanyam. A simple formula to compute the implied standard deviation. Financial Analysts Journal 44(5): 80–83. (1988)

- [6] F. Caravenna and J. Corbetta. General smile asymptotics with bounded maturity. arXiv:1411.1624 [q-fin.PR]. (2015)

- [7] C.J. Corrado and Th.W. Miller, Jr. A note on a simple, accurate formula to compute implied standard deviations. Journal of Banking & Finance 20: 595–603. (1996)

- [8] A. Cox and D. Hobson. Local martingales, bubbles and option prices. Finance and Stochastics 9(4): 477–492. (2005)

- [9] S. De Marco, C. Hillairet and A. Jacquier. Shapes of implied volatility with positive mass at zero. arXiv:1310.1020 [q-fin.PR]. (2013)

- [10] F. Delbaen and W. Schachermayer. The fundamental theorem of asset pricing for unbounded stochastic processes. Mathematische Annalen 312: 215–250. (1998)

- [11] A. Dieckmann. Table of Integrals. Physikalisches Institut der Uni Bonn. http://www-elsa.physik.uni-bonn.de/dieckman/IntegralsDefinite/DefInt.html (2015)

- [12] K. Gao and R. Lee. Asymptotics of implied volatility to arbitrary order. Finance Stochastics 18(2): 349–392. (2014)

- [13] A. Gulisashvili. Asymptotic formulas with error estimates for call pricing functions and the implied volatility at extreme strikes. SIAM Journal on Financial Mathematics 1: 609–641. (2010)

- [14] A. Gulisashvili. Analytically Tractable Stochastic Stock Price Models. Springer Finance. (2012)

- [15] A. Gulisashvili. Left-wing asymptotics of the implied volatility in the presence of atoms. International Journal of Theoretical and Applied Finance 18(02). (2015)

- [16] A. Jacquier and M. Keller-Ressel. Implied volatility in strict local martingale models. arXiv:1508.04351 [q-fin.MF]. (2015)

- [17] H.A. Latané and R.J. Rendleman, Jr. Standard deviations of stock price ratios implied in option prices Journal of Finance 31(2): 369–381. (1976)

- [18] R. Lee. The moment formula for implied volatility at extreme strikes. Mathematical Finance 14(3): 469–480. (2004)

- [19] S. Li. A new formula for computing implied volatility. Applied Mathematics and Computation 170: 611–625. (2005)

- [20] D.B. Madan, P.P. Carr and E.C. Chang. The variance gamma process and option pricing. European Finance Review 2: 79–105. (1998)

- [21] S. Manaster and G. Koehler. The calculation of implied variances from the Black-Scholes model: A note. Journal of Finance 37(1): 227–230. (1982)

- [22] P. Pianca. Simple formulas to option pricing and hedging in the Black–Scholes model. Rendiconti per gli Studi Economici Quantitativi: 223–231. (2005)

- [23] M. Roper and M. Rutkowski. On the relationship between the call price surface and the implied volatility surface close to expiry. International Journal of Theoretical and Applied Finance 12(4): 427-–441 (2009)

- [24] J. Ruf. Negative call prices. Annals of Finance 9(4). (2013)

- [25] P.-J. De Smet. Private communication. (2014)

- [26] M. Tehranchi. Asymptotics of implied volatility far from maturity. Journal of Applied Probability 46(3): 629–650. (2009)

- [27] M. Tehranchi. No-arbitrage implied volatility dynamics. Presentation for the PDE & Finance Conference, Stockholm. http://www.math.kth.se/pde_finance07/ (2007)