Estimation of the Pointwise Hölder Exponent of Hidden Multifractional Brownian Motion Using Wavelet Coefficients

Abstract

We propose a wavelet-based approach to construct consistent estimators of the pointwise Hölder exponent of a multifractional Brownian motion, in the case where this underlying process is not directly observed. The relative merits of our estimator are discussed, and we introduce an application to the problem of estimating the functional parameter of a nonlinear model.

keywords: Pointwise Hölder exponent; multifractional process; wavelet coefficients; parametric estimation

1 Introduction

Multifractional Brownian motion (mBm) is considered as one of the most natural extensions of fractional Brownian motion (fBm). Nowadays applications of mBm are numerous and growing. Similar to fBm, mBm has been used in such diverse areas as geology, image analysis, signal processing, traffic networks and mathematical finance. For instance, we refer to Lévy-Véhel (1995), Bertrand et al. (2012) and Bianchi et al. (2013). In this brief introduction, we focus on applications to mathematical finance, which we know best. Since generally neither fBm nor mBm are semi-martingales, Rogers (1997) pointed out that there would be arbitrage in a market where stocks are modelled by fBm. However, Cheridito (2003) showed that, if one relaxes the definition of arbitrage, fBm is an excellent candidate to model long-term memory in stock markets. Bayraktar et al. (2006) obtained fBm as the limit of the stock price in an agent-based model where investors display inertia. Moreover, unlike stock prices, several processes, like stochastic volatility, exchange rates, or short interest rates do not need to be semi-martingales for a mathematical model to be arbitrage-free in a strict sense. For each of these processes, there is empirical evidence of long-term memory. We refer to Corlay et al. (2014) for stochastic volatility, Xiao et al. (2010) for exchange rates, and Ohashi (2009) for interest rates. Making the Hurst parameter time-dependent allows to model different regimes of the stochastic process of interest. For example, in times of financial crisis, asset volatility rises significantly. Likewise, empirical evidence shows that there has been periods of different volatility in either exchange rates or interest rates. This phenomena motivates one to introduce mBm into finance, since unlike fBm, the local regularity of volatilities driven by mBm allows to change via different periods. Let denote an mBm with Hurst function . We consider a general model with , . In this paper we are interested in estimating , starting from the observations of . An advantage of our model and methodology is that the functions and do not need to be known a priori. This is for instance the case of stochastic volatility, where the volatility is an unknown class function of .

We define the mBm through its harmonizable representation (see Benassi et al. 1997): for ,

| (1.1) |

where:

-

The Hurst functional parameter is a -Hölderian function with some ;

-

The complex-valued stochastic measure is defined as the Fourier transform of the real-valued Brownian measure . More precisely, for all ,

where denotes the Fourier transform of :

Statistically, the most significant feature of mBm, its local Hölder regularity, can be measured by its pointwise Hölder exponent. Recall that for a continuous nowhere differentiable process , its pointwise Hölder exponent is a stochastic process defined by: for each ,

Ayache and Lévy-Véhel (2004) show that for each , the pointwise Hölder exponent of at each point , , is with probability equal to its Hurst functional parameter :

Since generating the scenarios of fBm and mBm relies only on their Hurst parameters (see Ayache and Lévy-Véhel 2004), the problem of estimation of the Hurst parameter has significant interests. Several results have already been obtained recently on the estimation of the mBm’s Hurst functional parameter. We refer to Rosenbaum (2008), Coeurjolly (2005, 2006), Bardet (2002), Bardet and Surgailis (2013) and Bertrand et al. (2013).

Rosenbaum (2008) and Bardet (2002) used wavelet-based methods to study inference problem on fBm, i.e., the Hurst parameter is constant; Coeurjolly (2005, 2006) and Bertrand et al. (2013) studied the estimation of by using respectively generalized variations (see also Chan et al. 1995) and increment ratio statistic method, where a discretized sample path of the mBm is assumed to be observed. Bardet and Surgailis (2013) developed a nonparametric estimation method (based on the increment ratio) for evaluating the local Hurst function of a multifractional Gaussian process (whose increments are asymptotically a multiple of an fBm) which extends mBm, starting from a discrete sample path of this process. In this work we consider a model more general than mBm but slightly less general than the one considered in Bardet and Surgailis (2013). We study a different statistical setting (either the wavelet coefficients of or a discrete path of points is observed), by applying a wavelet-based approach. Note that the main advantage of this statistical setting is that, it could be applied to inferential problems when only a set of wavelet coefficients are available (we refer to Delbeke and Van (1995), Abry et al. (2002), Abry and Conçalvès (1997) and the references therein). By a study on the fine regularity property, our central limit theorem provides an explicit form for the limit covariance matrix. It is worth noting that, the construction of our estimator relies on a sharp estimation of the covariance structure of the mBm’s wavelet coefficients. The main technical difficulty arises due to the fact that the covariance structure of mBm is much more complicated than that of fBm. The techniques used to identify such covariance structure is not obvious and thus has its specific interests in statistical inferences on multifractional processes as well as on stochastic analysis.

1.1 Statistical setting

Consider the following system: for ,

| (1.2) |

where

-

is an mBm defined in (1.1). Assume that its Hurst functional parameter belongs to and

-

The closed forms of the deterministic functions and are unknown. However we assume that

-

, almost everywhere and there exist two constants such that for all .

-

and almost everywhere.

-

Suppose that a discrete trajectory of : is observed for some large enough.

Our major goal is to evaluate the functional parameter . As in Coeurjolly (2005, 2006), we introduce a pointwise estimation method, namely, the function is estimated pointwisely for any . Once the time is fixed, the problem becomes a parametric estimation problem. Peng (2011a) studied this problem when is some stationary increment process (with ), where the optimal convergence rate is obtained by using the observations . However, when varies via time, the estimation of only relies on the sample size of the observed data in the neighborhood of and this neighborhood’s radius’ convergence speed. Hence the convergence speed of the corresponding estimator would be reasonably slower than (see e.g. Coeurjolly (2005, 2006) for a particular case when is mBm). In this work, heuristically speaking, since the sample size of the neighborhood data of for estimating each is about , it is then believed that a good estimator should have its convergence rate near . Subject to this statistical setting, we try to get the “optimal” rate of convergence estimator of by using wavelet basis.

1.2 Methodology and technical assumptions

Let the integer and let us pick any mother wavelet whose first moments are vanishing:

and

| (1.3) |

is called the cancellation order of . Fix an integer , with being a subsequence of . The wavelet coefficients of are given by: for ,

| (1.4) |

We introduce a set of indices corresponding to a neighborhood of each :

where the radius of this neighborhood satisfies and as . Then the quadratic form estimator of is given as:

For showing the consistency of our estimator and existence of central limit results, we need to impose the following technical assumptions to , and :

- (A0):

-

. This condition leads to . We remark that the latter inequality still holds when and , as a consequence our results are still valid. However, we won’t consider the latter assumptions, because practitioners in data analysis wouldn’t expect the unknown functional parameter should be valued less than .

- (A1):

-

A lower bound of the convergence rate of toward 0 is given as:

- (A2):

-

An upper bound of the convergence rate of toward 0 is described as: for any arbitrarily small,

- (A3):

-

There exists a constant such that .

- (A4):

-

This condition is stronger than (A1):

Through this paper we assume that (A0) is always satisfied. We will successively show that our estimator of is weakly consistent under assumption (A1); it is strongly consistent under assumptions (A1)-(A2); and it has an asymptotic Gaussian behavior subject to assumptions (A2)-(A4). Before stating these main results, we make some notation conventions:

Definition 1.1

- (a)

-

A sequence of real-valued random variables is said to be bounded almost surely if and only if

it is said to be bounded in probability if and only if

Let be a sequence of strictly positive real numbers and let be a sequence of positive random variables. The notations

mean respectively that the sequence is bounded almost surely and in probability.

- (b)

-

We say two sequences of strict positive values and are equivalent as tends to infinity if and only if there exist two constants such that

We denote the relation of equivalence by .

- (c)

-

We use the notations “”, “” and “” to respectively denote convergence -almost surely, convergence in probability and convergence in law.

It is also useful to briefly introduce the steps which lead to the construction of the estimators:

- Step 1:

-

Identification of starting from the observations . In order to estimate , it suffices to make an identification of given in (1.4). Such an identification can be naturally obtained by discretization of integrals to the sum as

(1.5) By Lévy’s modulus of continuity theorem for mBm (see e.g. Theorem 1.7 in Benassi et al. 1997), , (6.2) and the fact that

there exists a positive-valued random variable all of whose moments are finite, such that for all with ,

(1.6) Then, the following important relations hold (the proofs are given in the appendix):

(1.7) (1.8) which show that is a good estimator of . Next we set

(1.9) and show that satisfies

(1.10) Please see the appendix for the proof of (1.10).

- Step 2:

-

Identification of starting from . We use similar computations appeared in Peng (2011a). The main result is the following (see Proposition 2.2 for a more explicit formula):

where is a constant which does not depend on ; denotes the cardinal of . It is observed that

Therefore subject to feasible choices of the sequence , the following convergence can accordingly take place in probability or almost surely:

(1.11) where is some constant not depending on .

- Step 3:

-

Identification of starting from .

Under assumption (A1) (resp. (A1)-(A2)), one has the following relation of equivalence (see (1.11), (3.2), (3.16) and (3.18)): for ,

in probability (resp. almost surely). As a consequence,

is a consistent estimator of . We remark that the speed of convergence relies on the choice of . More details on the choice of will be discussed in Theorem 3.2.

2 Some preliminary results

2.1 Identification of the covariance structure of the wavelet coefficients of

In this part we provide a sharp estimation of the covariance structure of wavelet coefficients of . For , define the wavelet coefficient of by

| (2.1) |

for all with being the integer part function.

The following proposition provides a fine identification of ’s covariance structure .

Proposition 2.1

Let satisfy that, there exist two constants such that 444We will denote this relation by .. Let , .

If and , then we have

| (2.2) |

where the closed form of is given in and the remaining terms verify

If , we have

| (2.3) |

where the explicit form of is given in .

The proof of Proposition 2.1 is given in the appendix. The following lemma is a straightforward consequence of Proposition 2.1 (it suffices to take in Proposition 2.1.) that we will rely on heavily through the remaining context.

Lemma 2.1

2.2 Identification of when are observed

In this section we first construct a consistent estimator of , when the wavelet coefficients of : can be straightforwardly observed (i.e. ). To this end we let

| (2.7) |

The following proposition provides sharp identifications of ’s first order and second order moments.

Proposition 2.2

The proof of Proposition 2.2 is given in the appendix.

We remark that, since a sequence of random variables bounded almost surely is also bounded in probability, therefore the following identification of holds, thanks to Proposition 2.2, Chebyshev’s inequality and Borel-Cantelli’s lemma.

Lemma 2.2

If , we have

| (2.11) | |||||

As a consequence,

- (a)

-

if , then

(2.12) - (b)

-

if and for arbitrarily small , then

(2.13) for arbitrarily small .

Proof. By using Chebyshev’s inequality, (2.2) and the condition that , we get for any ,

| (2.14) |

where is some constant which does not depend on . This implies

| (2.15) |

Then it follows from (2.8), (2.15) and the fact that that

(2.11) has been proven. Note that (2.12) follows straightforwardly from (2.11). Now we only need to show (2.13) holds. From (2.15) and Chebyshev’s inequality, we observe that there exists a constant which does not depend on nor on such that for any ,

| (2.16) |

Since , then applying Borel-Cantelli’s lemma leads to

Further observe that

Now we are ready to state the main results of this section. The following theorem constructs a consistent estimator of starting from the wavelet coefficients .

Theorem 2.1

For , denote by

- (a)

-

If , then

(2.17) - (b)

-

if and for any arbitrarily small, then

(2.18)

Proof. This theorem is a straightforward consequence of Lemma 2.2, as we observe that, by construction, verifies

Then, by Lemma 2.2, the fact that the logarithm function belongs to , continuous mapping theorem and the mean value theorem, we get Theorem 2.1.

In Theorem 2.1, if we assume with some and , then by elementary computation we obtain the following corollary, which leads to choose to obtain the best rate of convergence of the estimator . This result is similar to the choice of in Bardet (2002) in the setting of fBm.

Corollary 2.1

Under assumption with and ,

- (a)

-

Taking and , we have

- (b)

-

For small , taking and , we obtain

The second main result of this part describes an asymptotic Gaussian behavior of the estimator of , where the limit covariance matrix is precisely given, which depends on .

Theorem 2.2

For , if and assumptions (A2)-(A3) are verified, then

| (2.19) |

where the constant

with given in (A3) and given in (2.10).

In order to prove Theorem 2.2, we rely heavily on the following proposition.

Proposition 2.3

For any and any integer , denote by

Then

where with and

Proof. Following the similar method as in Bardet (2000), we show that for the empirical average of , a multivariate central limit theorem holds thanks to a Lindeberg’s condition. More precisely, for big enough and for , , denote by

a Lindeberg’s condition thus can be deduced from the following relations:

-

•

For ,

(2.21) -

•

For ,

(2.22) -

•

For ,

(2.23)

To show (2.21)-(2.23) hold, we first observe, from (6.40), that

| (2.24) |

Therefore (2.21) results from (2.24), (2.3) and (2.6). In order to obtain (2.22), it suffices to take for , then belong to and they satisfy . This entails that (2.1) can be applied on by setting and . As a consequence (2.22) follows from (2.24), (2.1) and (2.6). For proving (2.23), we just plug , into (2.1) and then use (2.24) and (2.6). Using this identification of ’s, we show the Lindeberg’s condition (the same as in Bardet 2000) is verified and the central limit theorem holds. Now it remains to show

| (2.25) | |||

| (2.26) |

We only prove (2.25) holds since (2.26) can be followed by quite a similar way. Remark that ; and for large enough,

and for a function continuous on ,

Considering all the above facts and (2.21)-(2.23), (6.49)-(6.4), and assumption (A3), we obtain

Finally, we have proved Proposition 2.3.

Next we present the following classical result (see e.g. Oehlert 1992).

Proposition 2.4 (Multivariate delta rule)

Let the estimators (valued in ) of satisfy the following central limit theorem:

where denotes the covariance matrix of the limit distribution and is a sequence of positive numbers tending to infinity. Let ( or ) belong to , then the following convergence in law holds:

where denotes the transpose of the gradient of on .

Note that if in Proposition 2.4, the gradient of becomes a Jacobian matrix.

Proof of Theorem 2.2. For simplifying notation we denote by

Therefore the following decomposition holds:

| (2.27) |

Since the fact that implies

| (2.28) |

And also by taking in (6.15), we have

| (2.29) |

By (2.6) (2.2), (6.8), (2.28) and (2.29), we then obtain

It follows from Markov’s inequality that there exists such that

The assumption (A2) then allows us to apply Borel-Cantelli’s lemma to obtain

Therefore, it follows from Proposition 2.3 and continuous mapping theorem that

Since , using Slutsky’s theorem, we get

This is in fact equivalent to

| (2.30) |

with . Then by applying Proposition 2.4 to (2.30) with , , and , we get

| (2.31) |

because the Jacobian matrix .

3 Identification of when are observed

3.1 Estimators starting from

Since in practice, it is more realistic to assume that a discretized trajectory of is observed, therefore in this section, we obtain a consistent estimator of starting from the high frequency is still available. Recall that the assumptions on are given in Section 1.1., then the key point leading to these results is to take a second order Taylor expansion with integral remainder, to obtain for ,

This together with (1.6) and the fact that for all yields

| (3.2) |

Note that (1.6) can lead to

| (3.3) |

It follows from (3.2), the definition of and (3.3) that

| (3.4) |

Hence similar to Lemma 2.2, we have

Lemma 3.1

If , then

As a consequence,

- (a)

-

Under assumption (A1),

(3.6) - (b)

-

Under assumptions (A1)-(A2),

(3.7) for arbitrarily small.

Here we note that, to show ((a)) and ((b)) hold, we must observe that under assumption (A1),

Lemma 3.1 further implies the following:

Theorem 3.1

For , denote by

- (a)

-

Under assumption (A1),

(3.8) - (b)

-

Under assumptions (A1)-(A2),

(3.9) for arbitrarily small.

- (c)

Proof. (3.8) and (3.9) are obvious by using Lemma 3.1 and the fact that convergences in probability and almost surely are preserved under continuous transformations. In order to show (3.10), we only need to verify

| (3.11) |

Equivalently, it suffices to show

| (3.12) |

We have, by using the mean value theorem on ,

where is some random variable valued in the open interval with ending points and . Since tends to a.s. as , then according to (3.4) and (A1), the right-hand side of the above equation can be bounded by

which converges to as , thanks to assumption (A4).

The following results are of the most interests in this section. We construct consistent estimators of starting from the observations .

Theorem 3.2

For , denote by

- (a)

-

Set , with . We let satisfy assumption (A1), then

(3.13) - (b)

-

Let satisfy assumptions (A1)-(A2), then

(3.14) for any arbitrarily small.

- (c)

-

Under assumptions (A2)-(A4) and ,

(3.15)

Proof. In order to prove ((a)) and ((b)), we rely on the following relation: under assumptions (A1)-(A2),

| (3.16) |

This is because, by using Markov’s inequality, Cauchy-Schwarz inequality, (1.10), ((b)) and the dominated convergence theorem,

| (3.17) |

Similarly to (3.1), we also obtain for any arbitrarily small,

The fact that implies , then by Borel-Cantelli’s lemma,

| (3.18) |

Therefore, ((a)) (resp. ((b))) follows from the following 2 decompositions:

For showing (3.15), we only need to show

| (3.19) |

By using the same idea we took to prove (3.11), we just need to verify

This is true since, according to (3.1) and the fact that (by assumption (A4)) , the left-hand side of the above term can be bounded in probability by

The fact that entails . Consequently,

hence (3.15) holds.

3.2 Selection of the parameters and from practical point of view

In Theorem 3.2, the choices of and depend on the target parameter . This is unacceptable from practical point of view. To overcome this inconvenience, we make assumptions (A1), (A4) stronger so that the values of and don’t rely on : suppose the lower bound and the upper bound are known.

- (A1)´

-

with ;

- (A4)´

-

with and .

Without great effort we could see (A1)´ implies (A1) and (A4)´ implies (A4) for all . Then from Theorem 3.1 and Theorem 3.2, we easily derive the following results:

Corollary 3.1

- (a)

-

Let satisfy assumption (A1)´, then

- (b)

-

If satisfies assumption (A1)´, then it also satisfies (A2). As a result,

for arbitrarily small.

- (c)

-

Under assumptions (A2), (A3), (A4)´,

Corollary 3.2

- (a)

-

Set , with . If satisfies assumption (A1)´, then

- (b)

-

If satisfies assumption (A1)´, then

for any arbitrarily small.

- (c)

-

Under assumptions (A2), (A3), (A4)´,

We conclude that the selection of can be made for each setting as follows:

-

•

In Corollary 3.1 (a), for any , taking , we obtain the best rate of convergence in this setting:

-

•

In Corollary 3.1 (b), similarly, taking obtains

-

•

In Corollary 3.2 (a), the best choices of , are the ones such that and . Consequently,

-

•

In Corollary 3.2 (b) we select and to obtain

From the above discussion we conclude that our estimator has its best convergence rate approximately when the wavelet coefficients of are observed, and when a discrete sample path of is observed. This convergence rate is poorer than the case when is straightforwardly available.

4 An application to statistical inferences: estimation of

The estimation of the hidden pointwise Hölder exponent also allows to solve stochastic volatility model’s nonparametric estimation problem. For example, suppose some underlying mBm satisfies the following nonlinear model: for ,

| (4.1) |

where

-

•

is an mBm with unknown ;

-

•

, almost everywhere is an unknown real-valued deterministic function;

-

•

only a discrete trajectory is available.

From the statistical setting, the information of the hidden mBm remains unknown. However, the following result shows it is still possible to evaluate the parameter . The strategy is: first estimate the pointwise Hölder exponent by given in Theorem 3.2, then the following result holds:

Proposition 4.1

Fix and with . Let

Then,

- (a)

-

Under assumption (A1)´,

(4.2) - (b)

-

Under assumptions (A1)´ and (A2),

(4.3)

Proof of Proposition 4.1. We only show (4.3) holds, since the way to obtain (4.2) is similar. Under assumptions (A1)´ and (A2), on one hand, it follows from (3.18) and ((b)) that

| (4.4) |

On the other hand, by using (6.35) and the fact that , we see

| (4.5) |

Since the functions and are both continuous over , therefore by combining (4.4), (4.5) and ((b)), we obtain Proposition 4.1.

5 Comparison to Bardet and Surgailis (2013) and a simulation study

Bardet and Surgailis (2013) established a pseudo-generalized least squares version of the localized increment ratio estimator and quadratic estimator of , denoted by and respectively. This work is so far the most achieved one on estimation of the mBm’s pointwise Hölder exponent. In this section we compare our model and approach to Bardet and Surgailis (2013)’s and illustrate some simulation results. The main differences between our statistical setting and Bardet and Surgailis (2013)’s are:

-

1.

Bardet and Surgailis (2013) considers observation of a multifractional Gaussian process which has asymptotic self-similarity and “tangent to” an fBm with Hurst parameter and scaled by at each time . This setting covers ours when . However, our model is different when is some other function.

-

2.

The estimators and are obtained in terms of observations of discrete sample path of the process. We have established estimators based on observations of discrete sample path of and wavelet coefficients of the process (see in Theorem 3.1), respectively. The latter result is the main contribution of this paper. For more details on wavelet-based statistics we refer to Delbeke and Van (1995), Abry et al. (2002), Abry and Conçalvès (1997).

-

3.

The estimators and apply to all with , however our estimators only work for .

-

4.

In both and , the length of the local window plays the role as in our setting, which partially explains the estimator’s asymptotic behavior. For building up the convergence, both Bardet and Surgailis (2013)’s and our model are subject to some technical assumptions. Here we consider a particular case to compare the estimators’ rate of convergence. Let , where has pointwise Hölder exponent . From Proposition 3 (iii) and (iv) in Bardet and Surgailis (2013) we see for and arbitrarily small , the estimators and have the best rate of convergence in probability and a.s. respectively:

and

where IR2 or QV2. We set in Corollary 2.1. Then according to Corollary 2.1, has a better rate of convergence in probability than , while outperforms by having a better rate of a.s. convergence.

Now we deliver algorithms to generate our estimators and . From Theorem 3.1, an algorithm to generate can be given as follows:

Algorithm I: estimation of starting from wavelet coefficients

: INPUT: a sample , and

: Initialize all the parameters:

: ; ;

: Establish a set of indices corresponding to the neighbors of :

: ;

: Compute “partial” sum of squares of the wavelet coefficients:

: ;

: Compute estimate of :

: ;

: OUTPUT:

In Algorithm I, Line 3 proposes a data-driven procedure to set the parameters and . From Line 7 we see that this algorithm requires at least operations. By this result and Corollary 3.1 it appears a trade-off between computational cost and precision of estimation: less value of reduces computational cost but leads to less precision of estimation.

Next we numerically study the estimator and compare the results with Bardet and Surgailis (2013)’s. In view of Corollary 3.2, we choose the parameters , with and . We also choose to be Haar wavelet’s mother wavelet function: . Below is an algorithm to simulate , according to Theorem 3.2.

Algorithm II: estimation of starting from discretized trajectory

: INPUT: a sample , and

: Initialize all the parameters:

: ; ; ; ;

: Establish a set of indices corresponding to the neighbors of :

: ;

: Estimate the wavelet coefficients:

: for in , do:

: ;

: end for

: Estimate “partial” sum of squares of the wavelet coefficients:

: ;

: Compute estimate of :

: ;

: OUTPUT:

Line 3 shows the procedure to set the parameters , , and . In Line 8, each item can be approximated by , when is large. Hence from Lines 7-9 of the algorithm we see that the algorithm requires at least operations. This fact together with the discussion on Corollary 3.2 reveals that the choice of has no impact on the computational cost, but only on the precision of the estimation.

Next we provide the empirical mean, the standard deviation and the quantile-quantile plots (QQ plots) through a simulation study, where all the codes in MATLAB are available from authors upon request.

We let , then choose 4 different types of and different Hurst functional parameters , as follows:

Since for the above three , we then choose , , . We assume a single discrete trajectory: is available, and denote to be the estimate of : () for short. By generating each estimator times, we present the corresponding empirical mean () and standard deviation () in the following table.

| 0.0636 | 0.0851 | 0.0874 | ||||

| 0.0612 | 0.0487 | 0.0618 | ||||

| 0.0775 | 0.0699 | 0.0676 | ||||

| 0.0787 | 0.0696 | 0.0491 | ||||

| 0.0939 | 0.0609 | 0.0605 | ||||

| 0.0769 | 0.0780 | 0.0779 | ||||

| 0.0683 | 0.0568 | 0.0845 | ||||

| 0.0711 | 0.0897 | 0.0805 | ||||

| 0.0823 | 0.0874 | 0.0767 | ||||

| 0.0609 | 0.0666 | 0.0774 | ||||

| 0.0695 | 0.1647 | 0.1185 | ||||

| 0.0835 | 0.1043 | 0.0580 | ||||

| 0.1150 | 0.1064 | 0.1075 | ||||

| 0.1200 | 0.0971 | 0.0681 | ||||

| 0.1092 | 0.0563 | 0.0628 | ||||

| 0.0713 | 0.0852 | 0.1196 | ||||

| 0.0790 | 0.0564 | 0.0686 | ||||

| 0.0988 | 0.1072 | 0.1267 | ||||

| 0.0938 | 0.0908 | 0.0579 | ||||

| 0.1145 | 0.0610 | 0.0619 | ||||

From Table 1 we see that our estimator has a consistent performance on evaluating the true pointwise Hölder exponent with respect to different and . Now we consider comparing the IR2 estimators in Bardet and Surgailis (2013) with ours. To this end we take to let be an mBm. By using the MATLAB functions VariaIRMBM(eta,,tot) and HestIR(,) obtained from http://samm.univ-paris1.fr/-Jean-Marc-Bardet, we also provide the empirical mean and standard deviation (based on independent scenarios of mBm and ) of IR2 estimators as follows:

| mBm | ||||||

|---|---|---|---|---|---|---|

| 0.0513 | 0.0801 | 0.0636 | ||||

| 0.0557 | 0.0838 | 0.0450 | ||||

| 0.0652 | 0.0810 | 0.0759 | ||||

| 0.0664 | 0.0606 | 0.0603 | ||||

| 0.0794 | 0.0435 | 0.0509 | ||||

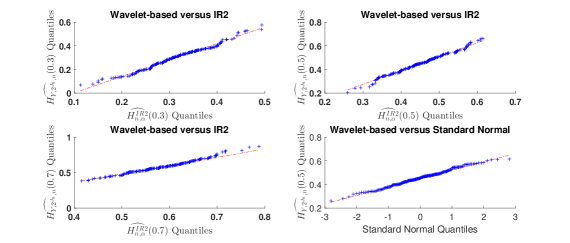

Note that in the function VariaIRMBM(eta,n,tot), the mBm was previously generated using the Choleski decomposition of the covariance matrix, so that the sample size is limited to . However here we have generated the mBm using Wood Chan circulant matrix, some krigging and a prequantification (see Chan and Wood 1998; Barrière 2007), the sample size can be thus taken as . The empirical comparison shows no significant difference between the performances of and , except that estimator has less variance. Below we compare the probability distributions of versus , by displaying QQ plots (see Fig. 1). The first QQ plots show whether and come from the same distribution for , , and ; the last one illustrates the asymptotically normal behavior of our estimator for and .

The QQ plots show that the probability distribution of our estimator for each are close to that of IR2 estimator when the observed signal process is mBm and it is asymptotically normally distributed.

Through the above simulation study we conclude that there is no significant difference among IR2 estimator provided in Bardet and Surgailis (2013) and our wavelet-based estimator. And no significant difference is observed among wavelet-based estimators corresponding to different . We also state that the bias and variance of are generally greater than IR2 estimator when the sample size is relatively small. This is because, the wavelet-based method generally provides estimators of slower convergence rate than IR2 estimator.

6 Appendix

6.1 Proofs of (1.7) and (1.8).

First by using triangle inequality, we get

| (6.1) |

Recall that for . Define the random variable to be

| (6.2) |

Since is continuous and not equal to almost everywhere, then is a Gaussian process with continuous trajectories, by applying Dudley’s theorem and Borell’s inequality (more precisely, with the same arguments for the proof of on Page 1445-1446 in Rosenbaum (2008). See also Ledoux and Talagrand (2010)), we can show that This means all of ’s moments are finite. Hence, using the mean value theorem, we get

| (6.3) |

where is a random variable. It follows from (6.1) and (6.3) that

| (6.4) |

In order to get (1.7), we need (1.6), from which we see there exists a positive random variable with all finite moments such that

| (6.5) |

Observe that for ,

and

| (6.6) |

This together with the fact that for yields there exists a positive random variable with all finite moments such that,

| (6.7) |

Now we are going to prove (1.8). For , we consider the -order moment of in (6.1). By applying the following two versions of Jensen’s inequalities:

| (6.8) |

and Cauchy-Schwarz inequality, we obtain

| (6.9) |

Note that by Lemma 2.12 (i) in Ayache et al. (2011), there exists a constant which does not depend on and such that

Therefore by using again (6.6) and the fact that , there exists some constant such that

| (6.10) |

Using (6.10) and similar computations as in (6.1), we obtain there exists such that

| (6.11) |

By using the fact that all the moments of Gaussian variable are equivalent, we get there exists some constant (only depending on ) such that

| (6.12) |

Finally it results from (6.1) and (6.12) that

where . Therefore (1.8) has been proven.

6.2 Proof of (1.10)

First notice that, by the definition of , we have

| (6.13) |

as , because .

It follows from (6.8), Cauchy-Schwarz inequality, (6.13) and the fact that that

| (6.14) |

Roughly speaking (and it can be proven without efforts), since the trajectory is at least as smooth as , then for , there exists a constant (only depending on ) such that,

| (6.15) | |||||

Then it results from (6.2), (6.15), (1.8) and (6.13) that

| (6.16) |

In view of the equivalence relation between and as and , (1.10) finally results from (6.16).

6.3 Proof of Proposition 2.1

6.3.1 Proof of (2.1)

By using the fact that , are zero-mean Gaussian random variables, Fubini’s theorem, the isometry property of mBm’s harmonizable presentation and a change of variables, we get

| (6.17) |

Since the pointwise Hölder exponent of in the neighborhood of behave locally asymptotically like those of fractional Brownian motions with Hurst parameters : on and on , we can thus consider a Taylor expansion of respectively on and . To be more explicit, let’s fix and define , since belongs to , we take the second order Taylor expansion for respectively on and There exist and such that

| (6.18) | |||||

| (6.19) |

where we denote, for , ,

and

Thus we rewrite (6.3.1) as

where

We note here ’s and ’s are notations in short for (6.18) and (6.19). By using (6.3.1), it suffices to make an identification of all the terms in order to estimate the covariance structure of the wavelet coefficients. We consider different cases according to the values of . The key to these identifications is to observe the following:

-

•

First, observe that for , , we have

where for , , with being the binomial coefficient.

-

•

Secondly, for , , , and , a order Taylor expansion of on yields:

(6.21) where the integral remainder of ’s -th order Taylor expansion (see e.g. Apostol 1967) is given as: for ,

(6.22) for ,

and the function

Here we note that for and ,

- Case (i)

-

.

- Case (ii)

-

- Case (iii)

-

Observe that can be expressed as

- Case (iv)

-

By using the fact that , can be expressed asLet respectively, and in (• ‣ 6.3.1) and notice that depends on , we get

Then similarly to (• ‣ 6.3.1), using a order Taylor expansion of respectively on and on , and also use the fact that for , (since ), we obtain

By using symmetric property,

- Case (v)

-

.

Since the computations are quite similar as in the previous cases, we present the results without proof.(6.30) (6.31) (6.32)

Now denote by

| (6.33) |

It remains to show that for and ,

According to (6.33), it suffices to prove for any ,

| (6.34) |

To prove (6.34) holds we only take as an example, since the computations of the other items are similar. Recall that

Remember that, the fact that yields , and . These facts together with imply

6.3.2 Proof of (2.3)

When , we still make a Taylor expansion as in the proof of (2.1). For the first term , since (some constant), then using the same formula in (6.25), we get

where

| (6.35) |

The remaining items of ’s are of higher order so we only give a bound of them. By means of a Taylor expansion of on , then similar discussion shows that, for ,

6.4 Proof of Proposition 2.2

Fix . It follows from the definition of , (2.7), (2.6) and the fact that that

| (6.36) |

It remains to show, for ,

For this purpose, for fixed we define as for ,

Then by using the Taylor expansion of around and the facts that , , , we obtain

| (6.37) |

where is some value in .

Therefore, by using (6.4), (6.4) and the fact that

| (6.38) |

we get

| (6.39) |

Thus (2.8) follows. Now we are going to show (2.2). First observe

Then we recall the fact that if is a centered Gaussian random vector, then (see e.g. Lemma 5.3.4 in Peng 2011b)

| (6.40) |

It yields

| (6.41) |

(6.4) together with Lemma 2.1 implies

| (6.42) |

Now we study the second line of (6.4). By the facts that , , , we obtain

| (6.43) |

For the fourth line of (6.4), by using Cauchy-Schwarz inequality and Proposition 2.1, we get

| (6.44) | |||

| (6.45) |

Therefore (6.4) is equivalent to

| (6.46) |

In order to make an identification of the dominating part of (6.4), for fixed we define as, for ,

Then it follows from the Taylor expansion and the fact that that

| (6.47) |

where is some value in and

| (6.48) |

where are some values satisfying and . Observe that, by a change of variable,

| (6.49) |

Then (6.49) together with (6.4), (6.47), (6.4) entails that

| (6.50) |

Observe that, since ,

On one hand, we recall that if is a monotonic decreasing function and the series is convergent, then for ,

It yields

| (6.52) | |||||

On the other hand, since , then it is easy to see

Finally,

| (6.53) |

It follows by (6.4) and (6.53) that

| (6.54) |

We thus can conclude

where is a constant only depending on . Proposition 2.2 has been proven.

References

- [1] Apostol T (1967) Calculus. Jon Wiley Sons, Inc.

- [2] Abry P, Flandrin P, Taqqu M S, Veitch D (2002) Self-similarity and long-range dependence through the wavelet lens. In: Theory and Applications of Long-range Dependence: 527-556

- [3] Abry P, Gonçalvès P (1997) Multiple-window wavelet transform and local scaling exponent estimation. In Proc. IEEE-ICASSP-97: 3433-3436

- [4] Ayache A (2001) Du mouvement Brownien fractionnaire au mouvement Brownien multifractionnaire. Technique et Science Informatiques 20 (9): 1133-1152

- [5] Ayache A, Lévy-Véhel J (2004) On the identification of the pointwise Hölder exponent of the generalized multifractional Brownian motion. Stoch. Proc. Appl. 111: 119-156

- [6] Ayache A, Shieh N R, Xiao Y (2011) Multiparameter multifractional Brownian motion: local nondeterminism and joint continuity of the local times. Ann. Inst. H. Poincaré Probab. Statist. 47 (4): 1029-1054

- [7] Bardet J M (2000) Testing for the presence of self-similarity of Gaussian time series having stationary increments. J. Time Series Anal. 21 (5): 497-515

- [8] Bardet J M (2002) Statistical study of the wavelet analysis of fractional Brownian motion. IEEE Trans. Inform. Theory 48 (4): 991-999

- [9] Bardet J M, Surgailis D (2013) Nonparametric estimation of the local Hurst function of multifractional Gaussian processes. Stoch. Proc. Appl 123 (3): 1004-1045

- [10] Barrière O (2007) Synthèse et estimation de mouvements Browniens multifractionnaires et autres processus à régularité prescrite: définition du processus autorégulé multifractionnaire et applications. Ph.D. Dissertation, Ecole Centrale de Nantes

- [11] Bayraktar E, Horst U, Sircar R (2006) A limit theorem for financial markets with inert investors. Math. Oper. Res. 31 (4): 789-810

- [12] Benassi A, Jaffard S, Roux D (1997) Elliptic Gaussian random processes. Rev. Mat. Iberoam. 13: 19-90

- [13] Bertrand P R, Fhima M, Guillin A (2013) Local estimation of the Hurst index of multifractional Brownian motion by increment ratio statistic method. ESAIM: PS. 17: 307-327

- [14] Bertrand P R, Hamdouni A, Khadhraoui S (2012) Modelling NASDAQ series by sparse multifractional Brownian motion. Methodol. Comput. Appl. Probab. 14 (1): 107-124

- [15] Bianchi S, Pantanella A, Pianese A (2013) Modeling stock prices by multifractional Brownian motion: an improved estimation of the pointwise regularity. Quant. Finance. 13 (8): 1317-1330

- [16] Chan G, Hall P, Poskitt D S (1995) Periodogram-based estimators of fractal properties. Ann. Statist. 23 (5): 1684-1711

- [17] Chan G, Wood A T A (1998) Simulation of Multifractional Brownian Motion. In Proce. COMPSTAT 13th Symposium, Bristol, Great Britain: 233-238

- [18] Cheridito P (2003) Arbitrage in fractional Brownian motion models. Finance Stoch. 7: 533-553

- [19] Corlay S, Lebovits J, Lévy-Véhel J (2014) Multifractional stochastic volatility models. Math. Finance 24 (2): 364-402

- [20] Coeurjolly J F (2005) Identfication of multifractional Brownian motion. Bernoulli 11 (6): 987-1008

- [21] Coeurjolly J F (2006) Erratum: identfication of multifractional Brownian motion. Bernoulli 12 (2): 381-382

- [22] Delbeke L, Van A W (1995) A wavelet based estimator for the parameter of self-similarity of fractional Brownian motion. Proceedings of the 3rd International Conference on Approximation and Optimization in the Caribbean, 14 pp. (electronic), Benemérita Univ. Autón.

- [23] Ledoux M, Talagrand M (2010) Probability in Banach spaces. Springer, Berlin Heidelberg

- [24] Lévy-Véhel J (1995) Fractal approaches in signal processing. Fractals 3: 755-775

- [25] Oehlert G W (1992) A note on the delta method. Amer. Statist. 46 (1): 27-29

- [26] Ohashi A (2009) Fractional term structure models: no-arbitrage and consistency. Ann. Appl. Probab. 19 (4): 1553-1580

- [27] Peng Q (2011a) Uniform Hölder exponent of a stationary increments Gaussian process: estimation starting from average values. Statist. Probab. Lett. 81: 1326-1335

- [28] Peng Q (2011b) Statistical inference for hidden multifractional processes in a setting of stochastic volatility models. Dissertation, University Lille 1

- [29] Rogers L C G (1997) Arbitrage with fractional Brownian motion. Math. Finance 7: 95-105

- [30] Rosenbaum M (2008) Estimation of the volatility persistence in a discretely observed diffusion model. Stoch. Proc. Appl. 118: 1434-1462

- [31] Xiao W, Zhang W, Zhang Z, Wang Y (2010) Pricing currency options in a fractional Brownian motion with jumps. Econom. Mod. 27: 935-942