A Strong Order 1/2 Method for Multidimensional SDEs with Discontinuous Drift

Abstract

In this paper we consider multidimensional stochastic differential equations (SDEs) with discontinuous drift and possibly degenerate diffusion coefficient. We prove an existence and uniqueness result for this class of SDEs and we present a numerical method that converges with strong order 1/2. Our result is the first one that shows existence and uniqueness as well as strong convergence for such a general class of SDEs.

The proof is based on a transformation technique that removes the discontinuity from the drift such that the coefficients of the transformed SDE are Lipschitz continuous. Thus the Euler-Maruyama method can be applied to this transformed SDE. The approximation can be transformed back, giving an approximation to the solution of the original SDE.

As an illustration, we apply our result to an SDE the drift of which has a discontinuity along the unit circle and we present an application from stochastic optimal control.

Keywords: stochastic differential equations, discontinuous drift, degenerate diffusion, existence and uniqueness of solutions, numerical methods for stochastic differential equations, strong convergence rate

Mathematics Subject Classification (2010): 60H10, 65C30, 65C20 (Primary), 65L20 (Secondary)

1 Introduction

We consider a -dimensional time-homogeneous stochastic differential equation (SDE)

| (1) |

where and are measurable functions and is a

-dimensional standard Brownian motion on the filtered probability space

.

If both and are Lipschitz, then existence and uniqueness is

guaranteed by Picard iteration.

Furthermore, (1) can be solved numerically with, e.g., the Euler-Maruyama method, which then converges

with strong order

1/2, see [11, Theorem 10.2.2].

However, in applications one is frequently confronted with SDEs where is non-Lipschitz, e.g., in stochastic control theory. There, whenever an optimal control of bang-bang type appears, meaning that the strategy is of the form

for some measurable set , the drift of the controlled underlying system is discontinuous. Furthermore, for example in setups with incomplete information, which are currently heavily under study, e.g., for applications in mathematical finance, the underlying systems have degenerate diffusion coefficients.

Therefore, the class of SDEs that we study in this paper appears frequently in applied mathematics and we shall elaborate our contributions to this kind of problems later in the paper.

The question of existence and uniqueness of solutions to SDEs with non-Lipschitz drift has been studied by various authors.

For the case where is only bounded and measurable and is bounded, Lipschitz, and satisfies a certain uniform ellipticity condition, Zvonkin [26] and Veretennikov [23, 24, 25] prove existence and uniqueness of a solution by removing the drift coefficient in a way such that the Lipschitz condition of the diffusion coefficient is preserved.

But uniform ellipticity is a strong assumption which is – as mentioned above – frequently violated in applications.

In Leobacher et al. [17] an existence and uniqueness result for (1) is presented for the case where the drift is potentially discontinuous at a hyperplane, or a special hypersurface, but well behaved everywhere else and where the diffusion coefficient is potentially degenerate. In that paper, not the whole drift is removed, but only the discontinuity is removed locally from the drift.

Due to the weaker requirements on the diffusion coefficient the restriction to homogeneous SDEs does not pose any loss of generality. In Shardin and Szölgyenyi [20] the authors extend the result from [17] to the time-inhomogeneous case.

In Leobacher and Szölgyenyi [15] an existence and uniqueness result, as well as a numerical

method are presented for the one-dimensional

case with piecewise Lipschitz drift coefficient. There the

coefficients are globally transformed into Lipschitz ones. Both

computation of the transformed coefficients and inversion can be done

efficiently. This leads to a numerical method for one-dimensional SDEs

through application of the Euler-Maruyama

scheme on the transformed equation and transforming the approximation back.

We present a simplified version of this result in Section 2.

However, extending the result from [15] to the -dimensional case is far from being straightforward. One problem is that there is no immediate generalization of the concept of a piecewise Lipschitz function with several variables that suits our needs. The second problem is that it is more difficult to obtain a transform that is a Lipschitz diffeomorphism . We use Hadamard’s global inverse function theorem to prove that our transform is of this kind. Moreover, we need to show that the transform and its inverse are sufficiently well-behaved for Itô’s formula to hold.

The coefficients of the SDE obtained by transforming the original one

are shown to be

Lipschitz, such that we can apply the

Euler-Maruyama method to the transformed SDE. An approximation to the original SDE is then obtained

by applying the inverse transform to the approximation of the transformed solution.

For this scheme we show

strong convergence with order .

One might ask whether the results of Zvonkin and

Veretennikov give rise to a similar method. However, in order to apply their method one

would have to solve a system of parabolic partial differential equations (in

each step). Further, for using this solution in a numerical method

like ours, one would also have to find its inverse function. Therefore such a method, if it exists at all,

would be rather costly from the computational perspective.

In the present paper we present a transform for the multidimensional case which allows to prove an existence and uniqueness result for -dimensional SDEs with discontinuous drift and degenerate diffusion coefficient under conditions significantly weaker than those in the literature. The essential geometric condition in our setup is that the diffusion must have a component orthogonal to the set of discontinuities of the drift.

Furthermore, we

present a numerical method for such SDEs based on the ideas outlined above.

Up to the authors’ knowledge there is no other numerical method that can deal

with such a general class of SDEs and gives strong convergence, much less

giving a strong convergence rate.

We are now going to review the literature on numerical methods for SDEs with non-globally Lipschitz drift coefficient. In Berkaoui [1] strong convergence of the Euler-Maruyama scheme is proven under the assumption that the drift is of class . For an SDE with continuously differentiable but non-globally Lipschitz drift Hutzenthaler et al. [8] introduce a new explicit numerical scheme – the tamed Euler scheme – and prove its strong convergence. Sabanis [19] proves strong convergence of the tamed Euler scheme for SDEs with one-sided Lipschitz drift. For the Euler-Maruyama scheme Gyöngy [6] proves almost sure convergence for the case that the drift satisfies a monotonicity condition. A different approach is introduced by Halidias and Kloeden [7], who show that the Euler-Maruyama scheme converges strongly for SDEs with a discontinuous monotone drift coefficient, especially mentioning the case in which the drift is a Heaviside function. Kohatsu-Higa et al. [12] show weak convergence of a method where they first regularize the drift and then apply the Euler-Maruyama scheme. They allow the drift to be discontinuous. Étoré and Martinez [3, 4] introduce an exact simulation algorithm for one-dimensional SDEs that have a bounded drift coefficient being discontinuous in one point, but differentiable everywhere else.

This paper is organized as follows. In Section 2 we present the one-dimensional result and algorithm in a form that can be generalized to multiple dimensions, which is subsequently done in Section 3. In Section 4 we give two numerical examples: one where the drift coefficient has discontinuities along the unit circle in and an example from stochastic optimal control.

Some of the more technical and geometrical proofs have been moved to the appendix.

2 The one-dimensional problem

Here we consider the one-dimensional version of SDE (1) and give simple conditions for existence and uniqueness of a solution and a strong order 1/2 algorithm. For this we recall the following definition.

Definition 2.1.

Let be an interval. We say a function is piecewise Lipschitz, if there are finitely many points such that is Lipschitz on each of the intervals and .

We make the following assumptions on the coefficients.

Assumption 2.1.

The drift coefficient is piecewise Lipschitz.

Assumption 2.2.

The diffusion coefficient is Lipschitz with whenever .

For simplicity we derive the result for that is

Lipschitz with the exception of only a single point where is

allowed to

jump.

We are going to construct a transform such that

the process formally defined by satisfies an SDE with

Lipschitz coefficients and therefore has a solution by Itô’s classical

theorem on existence and uniqueness of solutions, see [9].

For this define the following bump function on , which we need to localize the impact of the transform :

| (2) |

The function has the following properties:

-

1.

defines a function on all of ;

-

2.

, , ;

-

3.

for all .

We define the transform by

| (3) |

where and are some constants.

Lemma 2.2.

Let .

Then for all . Furthermore, for all . Therefore has a global inverse .

Proof.

Differentiating for yields

For positive this is positive, if . For negative it is positive, if . Altogether a sufficient condition for to be positive is . ∎

W.l.o.g. we always choose , such that has a global inverse.

Remark 2.3.

In [15] the function is constructed differently. There, is piecewise cubic, such that is piecewise radical and hence admits exact inversion, which is advantageous for the numerical treatment.

In fact, can be made piecewise cubic by still using equation (3), but with a different choice for . Actually, any function with support contained in satisfying properties 1., 2., 3. from page 3 will give rise to a transform sufficient for our purpose, with a similar condition on the constant for to be invertible. The form chosen here is simple in the one-dimensional case and has a direct multidimensional analog.

Formally define . Abbreviating , we have

| (4) |

where

We now show that, for an appropriate choice of , the transformed drift is Lipschitz. For this we need the following elementary lemma from [15].

Lemma 2.4.

Let be piecewise Lipschitz and continuous.

Then is Lipschitz on .

From Lemma 2.4 and we see that the mapping is Lipschitz. In order to make the mapping continuous, we need to choose so that

i.e.

Thus we get, for the choice

that is continuous.

Note that at this point we need non-degeneracy of in .

Since is continuous with the appropriate choice of , it is Lipschitz as well by Lemma 2.4.

One may worry about the quadratic occurrence of in the expression

for . Note, however, that vanishes outside .

To prove that is Lipschitz as well, we need the following lemma:

Lemma 2.5.

Let be Lipschitz. Then is Lipschitz.

Proof.

Let be a Lipschitz constant for . Note that is a Lipschitz constant for . If , then

where . For we have

The same estimate holds for the case . For we have . ∎

Thus, is Lipschitz by Lemma 2.5 and the fact that the

composition of Lipschitz functions is Lipschitz.

Altogether we have that the SDE (4) for has Lipschitz coefficients and .

The generalization to finitely many discontinuities of in the points is now straightforward: define

with

We are ready to prove existence and uniqueness of a solution to the one-dimensional SDE (1).

Theorem 2.6 (cf. [22, Theorem 2.2]).

Let Assumptions 2.1, and 2.2 be satisfied, i.e. is piecewise Lipschitz with finitely many jump points, is Lipschitz and .

Then the one-dimensional SDE (1) has a unique global strong solution.

Proof.

Since the SDE (4) for has Lipschitz coefficients, it follows that (4) with initial condition has a unique global strong solution. Furthermore, has a global inverse , which inherits the smoothness from . Although , Itô’s formula holds for , see [10, 5. Problem 7.3]. Applying Itô’s formula to , we obtain that satisfies

Setting yields the desired result. ∎

For approximating the solution to the one-dimensional SDE (1) we propose the following numerical method. Let be the Euler-Maruyama approximation of the solution to SDE (4) with step size smaller than .

Algorithm 2.7.

Go through the following steps:

-

1.

Set .

-

2.

Apply the Euler-Maruyama method to the SDE (4) to obtain .

-

3.

Set .

Theorem 2.8 (cf.[22, Theorem 3.1]).

Proof.

We estimate the -error of the approximation. For every there is a constant , such that

for every sufficiently small step size , where is the Lipschitz constant of and where we applied [11, Theorem 10.2.2] for the -convergence of the Euler-Maruyama scheme for SDEs with Lipschitz coefficients. ∎

3 The multidimensional problem

We now consider the multidimensional case. Like in dimension one, we will have to make assumptions on the drift so that it is Lipschitz apart from – relatively few – locations of discontinuity. That is, we need a concept similar to that of “piecewise Lipschitz” in the one-dimensional case. We will develop such a concept now.

In contrast to the one-dimensional case, we shall have to make additional assumptions on the behaviour of the drift close to its points of discontinuity, which shall all lie in a hypersurface .

Regarding the diffusion coefficient we need to find a condition corresponding to Assumption 2.2.

Note that most of these assumptions are automatically satisfied, or can at least be weakened, if is compact. We will treat the case of compact in Section 3.6.

3.1 Piecewise Lipschitz functions

For a continuous curve , let denote its length,

Definition 3.1.

Let . The intrinsic metric on is given by

where , if there is no continuous curve from to .

Definition 3.2.

Let . Let be a function. We say that is intrinsic Lipschitz, if it is Lipschitz w.r.t. the intrinsic metric on , i.e. if there exists a constant such that

Remark 3.3.

Note that for a function we have that is piecewise Lipschitz, iff is intrinsic Lipschitz on , where is a finite subset of .

This motivates the following definition:

Definition 3.4.

A function is piecewise Lipschitz, if there exists a hypersurface111By a hypersurface we mean a -dimensional submanifold of the . with finitely many components and with the property, that the restriction is intrinsic Lipschitz. We call an exceptional set for .

The definition is more general than the more obvious requirement that can be partitioned into finitely many patches in a way such that is Lipschitz on all of the patches. This is illustrated by the following example.

Example 3.5.

Consider the function , . Then is not Lipschitz, since and for .

It is readily checked, however, that is intrinsic Lipschitz on and is obviously a one-dimensional submanifold of .

Thus is piecewise Lipschitz in the sense of Definition 3.4.

The following lemma is a multidimensional generalization of Lemma 2.4.

Lemma 3.6.

Let be a function. If

-

1.

is continuous in every point ;

-

2.

is piecewise Lipschitz with exceptional set ;

-

3.

for and there exists a continuous curve from to with such that .

Then is Lipschitz on w.r.t. the Euclidean metric, and with the same Lipschitz constant.

Proof.

Let be the intrinsic Lipschitz constant of , i.e. for all , and let . If , then clearly .

If , then the line segment has non-empty intersection with .

Consider first the case where , i.e. we have finite intersection. There exist such that . Define by .

Set . W.l.o.g., . Now

where we have used the continuity of and , and that the intrinsic metric coincides with the Euclidean metric for pairs of points for which the connecting line segment has empty intersection with .

If contains infinitely many points, we can replace by , which is only slightly longer than , but has only finitely many intersections with . A slight modification of the argument above then gives that for any , and thus the desired result. ∎

Conjecture 3.7.

We will later give sufficient conditions for item 3 of the assumptions of Lemma 3.6 to hold, see Lemma 3.11. These conditions are satisfied in our applications.

It is well-known that differentiable functions with bounded derivative are Lipschitz w.r.t. the euclidean metric. The same holds true for the intrinsic metric:

Lemma 3.8.

Let be open and let be differentiable with .

Then is intrinsic Lipschitz with constant .

Proof.

Let and let be a continuous curve of finite length with and . (If no such curve exists we trivially have .) Let . Without loss of generality the can be chosen such that the line segment spanned by and is in for every . Then

∎

Furthermore, we prove that the composition of an intrinsic Lipschitz function with a Lipschitz function is intrinsic Lipschitz:

Lemma 3.9.

Let be open. Let be Lipschitz with constant . Let be intrinsic Lipschitz with constant .

Then is intrinsic Lipschitz with constant .

Proof.

Let be a continuous curve of finite length with and . (If no such curve exists we trivially have .) Let . For every there are such that . So

Since was arbitrary, we obtain the result. ∎

3.2 The form of the set of discontinuities

We are going to generalize the idea of transforming a discontinuous drift into a Lipschitz one to general dimensions.

For this we assume that the drift coefficient is piecewise Lipschitz in the sense of Definition 3.4, that is, there exists a hypersurface with finitely many components such that is intrinsic Lipschitz. The assumption on the drift that will make our method work therefore encompasses assumptions on .

Assumption 3.1.

The drift coefficient is a piecewise Lipschitz function . Its exceptional set is a hypersurface.

A consequence of Assumption 3.1 is that locally there exists a orthonormal vector, that is, for every sufficiently small open and connected there exists an orthonormal vector on , i.e. a -function such that for all the vector is orthogonal to the tangent space of in and . It is well-known, that there are in general two possible choices for and that one can take only if is orientable. But given on , the only other orthonormal vector is .

Define the distance between a point and the hypersurface in the usual way, . For every we define .

Assumption 3.2.

There exists such that has the unique closest point property, i.e. for every with there is a unique with .

A set possessing the property described in Assumption 3.2 is called a set of positive reach. The reach of a set is the supremum over all such that has the unique closest point property. This and the notion of unique closest point property can be found in [13].

Lemma 3.10.

Let be a -hypersurface.

If is of positive reach, then is bounded:

for all .

The proof of Lemma 3.10 can be found in the appendix.

Note that one can find examples of hypersurfaces

with bounded which are not of positive reach,

see Figure 1.

Due to Assumption 3.2 there exists an

for which we may define a mapping

assigning to each the point in closest to .

Lemma 3.11.

The rather technical proof of this lemma can be found in the appendix. Note that for many examples, like a (hyper-)sphere or hyperplane, item 3 of Lemma 3.6 is obviously satisfied. So in these cases there is no need to resort to Lemma 3.11. However, it is an interesting fact that this condition is automatically satisfied under our assumptions on .

3.3 Construction of the transform

As before, we construct a transform with the property that the SDE for has Lipschitz coefficients.

For this to be well-defined, we make the following assumption:

Assumption 3.3.

There is a constant such that for all .

Remark 3.12.

Assumption 3.3 is a non-parallelity condition, meaning that for all , must not be parallel to , in the sense that there exists some such that is not in the tangent space of in .

Assumption 3.3 is by far weaker than uniform

ellipticity. For the practical example we study in Section 4 it

is satisfied, whereas uniform ellipticity clearly is not.

For defining the transform, we first switch to a local setting. Suppose is close to , i.e. . Let be an open environment of in and an orthonormal vector. It follows that the set

is an open environment of , and every point can be uniquely represented in the form , , .

We are now ready to locally define the transform by

| (5) |

where , with (different than in (2)) defined by

and where

| (6) |

One important point to note is the following proposition.

Proposition 3.13.

The value of the function does not depend on the choice of the orthonormal vector.

Proof.

Both and depend on the parametrization only through the direction of the normal vector . But from the definitions of and we see that if is replaced by , then and both change sign. Therefore, does not depend on the particular choice of the orthonormal vector. ∎

The only reason why we defined locally at first was that for a non-orientable hypersurface we do not have, by definition, a global orthonormal vector. However, since the value of the locally defined function does not depend on the particular choice of the orthonormal vector, we can use the same equations (5) and (6) for defining globally on . That is, the function ,

is well-defined. Note further that, if we require , then from it follows that and therefore with a -smooth paste to in all points satisfying .

3.4 Properties of

We need to prove the following:

-

1.

can be chosen in a way such that is a diffeomorphism ;

-

2.

Itô’s formula holds for ;

-

3.

the SDE for has Lipschitz coefficients.

Assumption 3.4.

There is a constant such that every locally defined function as defined in (6) is and all derivatives up to order 3 are bounded by .

Theorem 3.14.

For proving Theorem 3.14 we first need to prove two technical lemmas. For every , denote by the tangent space of in .

Lemma 3.15.

For , is a linear mapping from into .

Proof.

is by definition a linear mapping . Furthermore, we have , so that for any curve in

If , we can find a curve in such that and . Thus, , i.e. . ∎

Remark 3.16.

If is and of positive reach then we may choose such that, whenever with , then is invertible.

Indeed, let be a bound on and let for some fixed . Then for we have , such that is invertible by the subsequent well-known Lemma 3.17.

Lemma 3.17.

Let be a linear operator on a subspace and let have (operator) norm smaller than .

Then is invertible and .

Proof.

Consider the Neumann series , which converges in operator norm and satisfies . Then

Thus, is the inverse of . ∎

Proof of Theorem 3.14.

Fix some and set , where is a bound on , which exists by Lemma 3.10.

Let .

For , differentiability of in is obvious.

For choose an open subset of (as before) and an orthonormal vector such that is an open set with and every can uniquely be written in the form with . can be parametrized locally by a one-one mapping , where is an open rectangle in , and there is a point such that . By making and/or smaller, if necessary, we may w.l.o.g. assume that .

Thus, we have a bijective mapping ,

Note that for all .

We have

where , and thus

Now note that

for all . Further,

Recall that for any , we have that and are linear mappings from the tangent space of in into the . For it then follows that

Since this equation holds for all , , it also holds for every vector in the tangent space, i.e.

For , the mapping is invertible by the argument from Remark 3.16. Denote the inverse of by .

Then for any we can write with and therefore

For a general vector we have that is orthogonal to the tangent space and is in the tangent space.

We abbreviate , , , , , . Then we have for

Therefore,

or, more explicitly,

| (7) |

In order to apply Hadamard’s global inverse function theorem [18, Theorem 2.2] and thus to show that is a diffeomorphism , we need to show that is , is invertible for all , and .

We have already proven differentiability of in . If is sufficiently small, is invertible, since and are uniformly bounded with a bound that tends to 0 for . For small enough it is therefore guaranteed that is close to the identity and therefore invertible by Lemma 3.17. We show in the separate Lemma 3.18 that can be chosen uniformly for all such that is invertible.

Since and both and are bounded by the definition of and Assumption 3.4, we also have the third requirement of Hadamard’s global inverse function theorem. is therefore a diffeomorphism. ∎

We will see that can always be chosen sufficiently small in the proof of Theorem 3.14.

Lemma 3.18.

Proof.

Note that .

Let and recall equation (3.4) from the proof of Theorem 3.14

We begin by estimating the operator norm of for given .

where we used that and for (by estimating the maxima), and that . Furthermore , since by , Lemma 3.17 and Remark 3.16. Hence

Therefore .

We want small enough to have and to that end we choose and

Hence is invertible for by Lemma 3.17. For , . ∎

W.l.o.g. we always choose like in Lemma 3.18.

We proceed with proving that, although , Itô’s formula holds for and .

Proof.

If , then since on , Itô’s formula holds for and until the first time hits . So the only interesting case is .

For this, there exists an open rectangle and a local parametrization of . Let . Moreover,

Let be defined as in the proof of Theorem 3.14. Note that , because is by Assumption 3.1, so Itô’s formula holds for . is locally invertible with , so as well. If we can show that Itô’s formula holds for , then it also holds for .

fits the assumptions of [17, Theorem 2.9]

(we get boundedness of the derivatives by localizing to a bounded domain),

so Itô’s formula holds for , and therefore also for .

is a function with continuous first and second derivatives, with the sole exception of , which is bounded, but may be discontinuous for . Since on an environment of , this property transfers to the inverse, which is . Thus, again by [17, Theorem 2.9], Itô’s formula holds for , and a fortiori for . ∎

Now we are ready to show that the coefficients of the transformed SDE for are Lipschitz.

Assumption 3.5.

We assume the following for and :

-

1.

the diffusion coefficient is Lipschitz;

-

2.

and are bounded on .

Assumption 3.6.

The exceptional set of is . Every unit normal vector of has bounded second and third derivative.

Lemma 3.26.

Then the function with is three times differentiable with bounded first, second, and third derivative.

Proof.

For we have with . By [dud, Corollary 4.5], is on .

Since maps into the tangent space of in it holds that . Thus we have . Note that is bounded by on .

By Assumptions 3.1, 3.2 and Lemma 3.10 the first derivative of every unit normal vector is bounded, and by Assumption 3.6 the second and third derivative of are bounded. Now [14, Corollary 4] implies that , , and are bounded on .

Now it follows from the chain and product rule that the function and its derivatives up to order 4 are bounded on .

Note further that

In total, by the chain and product rule, the first three derivatives of are bounded. ∎

Lemma 3.27.

Then the function is three times differentiable with bounded first, second, and third derivative.

Proof.

Lemma 3.28.

Proof.

Proof.

We first show that the drift of is continuous in . Let , , , and be defined as in the proof of Theorem 3.14. Suppose now, we have a locally defined process in . Then there exists a locally defined process in with

i.e. .

If is a locally defined solution to , then by Itô’s formula

where and denote the Jacobian and the Hessian of , and denotes the trace of a matrix. We want , or more precisely , i.e. . For brevity write . Now

We show that . It is not hard to see that the Jacobian of in a point is given by

such that

Therefore we have

on .

The drift coefficient of the SDE for has only discontinuities in the set . Further,

i.e. . The second term is continuous, so that

| (8) | ||||

Consider

and

Differentiation yields

We look at the second derivative w.r.t. :

Since for , we have that for , and thus

| (9) | ||||

Consider the drift coefficient of , which is

, thus . Further, note that is continuous for all pairs except .

Now the drift coefficient of the SDE for the process is continuous as well: and compounding with and preserves continuity of the drift since .

The -th coordinate of the transformed drift has the form

and we have just seen that it is continuous in all . It remains to show that is intrinsic Lipschitz on . For we have . is intrinsic Lipschitz on , and therefore also on .

On we have that is differentiable with bounded derivative and is therefore intrinsic Lipschitz by Lemma 3.8. is intrinsic Lipschitz on by Assumption 3.1 and is bounded on by Assumption 3.5, item 2. Moreover, is Lipschitz on and thus the mapping is intrinsic Lipschitz by Lemma 3.9.

In the same way we see that is differentiable with bounded derivative on and is therefore intrinsic Lipschitz by Lemma 3.8. is Lipschitz on and therefore intrinsic Lipschitz on . Moreover, both and are bounded on , thus is intrinsic Lipschitz by Lemma 3.9.

Now is intrinsic Lipschitz as a sum of intrinsic Lipschitz functions.

Altogether we have shown that is piecewise Lipschitz and

continuous, and hence Lipschitz by Lemma 3.6 and Lemma 3.11.

The transformed diffusion coefficient is given by

Since , and are Lipschitz, the mappings and are Lipschitz. Moreover, they are both bounded on (and thus on ), such that their product is Lipschitz. ∎

3.5 Main results

Finally, we are ready to prove the two main results of this paper.

Theorem 3.21.

Then the -dimensional SDE (1) has a unique global strong solution.

Proof.

Since by Theorem 3.20 SDE (10) has Lipschitz coefficients, it follows that it has a unique global strong solution for the initial value . Due to Theorem 3.14, the transformation has a global inverse . Itô’s formula holds for by Theorem 3.19. Applying Itô’s formula to , we obtain that satisfies

Setting closes the proof. ∎

For calculating the solution to the -dimensional SDE (1), the same algorithm as for the one-dimensional case works, if applied using the transformations from the -dimensional case. Let be the Euler-Maruyama approximation of the solution to SDE (10) with step size smaller than .

Algorithm 3.22.

Go through the following steps:

-

1.

Set .

-

2.

Apply the Euler-Maruyama method to SDE (10) to obtain .

-

3.

Set .

Theorem 3.23.

Proof.

We estimate the -error of the approximation. For every there is a constant , such that

for every sufficiently small step size , where is the Lipschitz constant of . We used [11, Theorem 10.2.2] for the -convergence of order of the Euler-Maruyama scheme for SDEs with Lipschitz coefficients. ∎

3.6 Compact set of discontinuities

To be able to prove our main results we had to make a number of assumptions on the coefficient functions and . At least one of those is indispensable for our method to work, that is, Assumption 3.1, which demands that is piecewise Lipschitz and that its set of discontinuities is a hypersurface.

There are two more assumptions on and several on the behaviour of the coefficients close to . In this subsection we shall find out which assumptions are automatically satisfied in the case where is compact.

Lemma 3.24.

Let be a compact submanifold with .

Then has a neighbourhood with the unique closest point property, and the projection map is .

Assumption 3.3 prescribes a certain geometrical relation between and directions of the diffusion coefficient. This will not be satisfied automatically only from making additional assumptions on , of course. But for the case of compact , Assumption 3.3 follows easily from weaker requirements on .

Proposition 3.25.

Let be a compact hypersurface and let be Lipschitz.

If for all , then there exists a constant such that for all .

Proof.

Let be a bounded, open, and connected subset with the property that there exists an orthonormal vector on . Since is continuous on the closure , there exists such that for all .

By compactness, can be covered by finitely many sets with lower bounds and we can take for the conclusion to hold. ∎

Note that also follows from

. So in particular, regularity of

implies Assumption 3.3 for compact .

Finally, consider Assumption 3.4 which asserts boundedness of the first three derivatives of the locally defined function on . Similar to what we have done in the proof of Proposition 3.25, we can conclude boundedness of the derivatives from their continuity.

From Assumption 3.6 one only needs the part that is . Boundedness of the second and third derivative of every unit normal vector follows from the fact that for a hypersurface a unit normal vector on any given connected open set is unique up to a factor of and from compactness.

4 Numerical Examples

In this section we present concrete examples. We compute the transform as well as the coefficients of the transformed SDE to which we apply the Euler-Maruyama scheme. Furthermore, we examine the quality of the approximation by considering the estimated -error.

Discontinuity on the unit circle

Let be the unit circle in , i.e. the drift of our SDE is discontinuous only in . We want to solve the following SDE numerically:

| (17) |

where

, and is a two-dimensional standard Brownian motion. Note that the non-parallelity condition, Assumption 3.3 is satisfied with ( is even uniformly elliptic).

We have that yielding the transform

and , if , or , where we have chosen .

Then the drift of the transformed SDE is given by

and , if , and

, if .

Furthermore, .

has to be evaluated numerically.

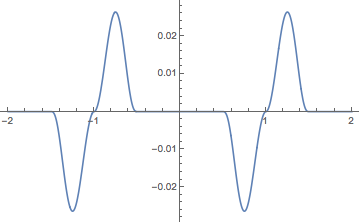

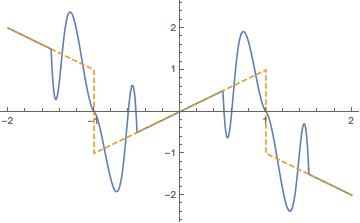

Figure 2 shows the deviation of the first component of from the identity. Figure 3 shows the first component of , and .

All other components look similar.

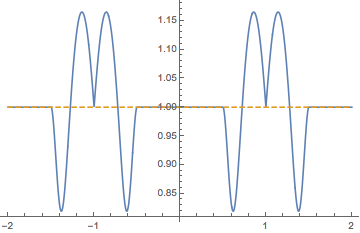

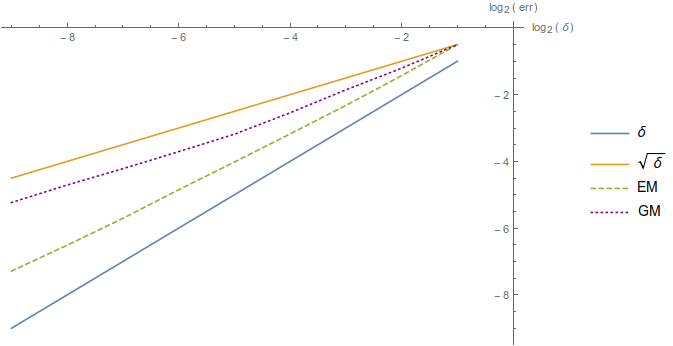

We apply Algorithm 3.22 to solve SDE (17). Figure 4 shows the estimated -error of the approximation of our -transformed Euler-Maruyama method (GM), compared to the Euler-Maruyama (EM) scheme:

plotted over ,

where is the numerical approximation with step size

, is an estimator of the mean value using 4096

paths, and is a normalizing constant so that .

We observe that our -transformed (GM) method converges roughly with order , and the crude Euler-Maruyama (EM) method seems to converge even at a higher rate. Note however that, even though the Euler-Maruyama method is extensively used in practice, it is not even known whether the method converges strongly for SDEs of the kind considered here. Especially we cannot conclude whether for even smaller step-size the error of the Euler-Maruyama method will still become smaller, will flatten out, or whether it will even explode.

Dividend maximization

In [22] the dividend maximization problem from actuarial mathematics, that is, the problem of maximizing the expected discounted future dividend payments until the time of ruin of an insurance company, is studied. In actuarial mathematics, the solution of this optimization problem serves as a risk measure. The problem is studied in a setup with incomplete information, where the drift of the underlying surplus process of the insurance company from which dividends are paid is driven by an unobservable Markov chain, the states of which represent different phases of the economy; an assumption that makes the model more realistic. In order to solve the optimization problem, the underlying surplus process has to be replaced by a multidimensional process consisting of filter probabilities of the states of the hidden Markov chain and the surplus written in terms of the filter probabilities. The resulting system is

| (18) | ||||

where and where is the dividend strategy, is the surplus process, and the , , are the conditional probabilities that the underlying hidden Markov chain is in state . is a one-dimensional Brownian motion. We assume knowledge of the following constants: are the entries of the intensity matrix of the Markov chain, is the diffusion parameter of the surplus and , , is the drift of the surplus, if the Markov chain is in state .

The application of filtering theory leads to an equivalent optimization problem:

| (19) |

with discount rate .

This is studied in [22]

and the candidate for the optimal dividend policy is of the form with threshold level , leading to a discontinuous drift of the surplus process from which the dividends are paid.

Due to the application of filtering theory, the diffusion coefficient is

not uniformly elliptic.

In order to verify the admissibility of the candidate for the optimal control policy,

existence and uniqueness of the underlying state process has to be proven.

This can be done by applying the result presented herein and we can also simulate the optimally controlled surplus (e.g., to calculate the expected time of ruin).

And our results are even further applicable: in [22] the optimization problem (19) is solved for by policy iteration in combination with solving an associated partial differential equation.

Doing the same for dimension 4 or higher would not be numerically tractable.

So in higher dimension one needs to solve the problem by combining policy iteration with simulation.

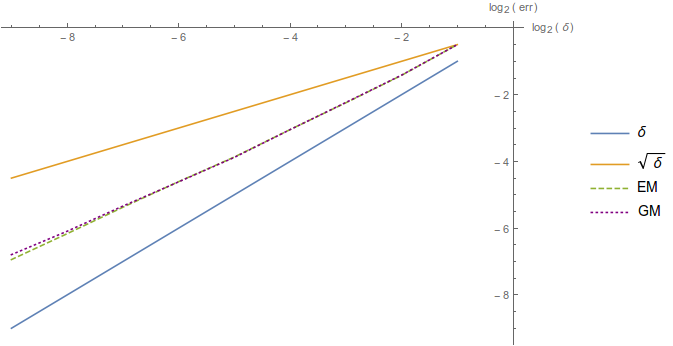

Figure 5 shows the estimated -error of the approximation of the solution of (18) in dimension 5 with a linear initial threshold level. In [22] for a threshold level which is a linear interpolation of the constant optimal threshold levels of the problem under full-information was used as an initial policy for policy iteration. However, we need not restrict ourselves to linear threshold levels.

Note that for our example checking whether the non-parallelity condition, Assumption 3.3 holds (in dependence on the parameter choice) is straight-forward.

We see that in this practical example the convergence order is again roughly .

Further examples from stochastic control theory, where SDEs with discontinuous (and unbounded) drift and degenerate diffusion coefficient appear are, e.g., [16, 20, 21]. The SDEs appearing there can now be shown to have a unique global strong solution under conditions significantly weaker than known so far, and this solution can be approximated with a numerical method that converges with strong order . As elaborated above our method can be used for approximating solutions to these optimization problems in dimensions greater than 4, where PDE methods become practically infeasible.

Concluding remarks

In this paper we have presented an existence and uniqueness result of strong solutions for a very general class of SDEs with discontinuous drift und degenerate diffusion coefficient; a class of SDEs that frequently appears in applications when studying stochastic optimal control problems. This is the most general result for such SDEs. Furthermore, we have derived a numerical algorithm that – under the same conditions as for the existence and uniqueness result – is proven to converge and we have established a strong convergence order of . We have applied our algorithm to two examples: one of theoretical interest and one coming from a concrete optimal control problem in actuarial mathematics.

Appendix A Supplementary proofs

Proof of Lemma 3.10

Let . W.l.o.g. and , where is the -th canonical basis vector of the . Thus can locally be parametrized by of the form , where is a -function with and . Hence, for all ,

with . Note that is a -function satisfying and w.l.o.g. the parametrization is chosen such that . Hence

where denotes the Hessian of in .

On the other hand

. In particular,

.

Now choose any that is smaller than the reach of . Then is the unique closest point on both to and . In other words, the open balls with centers and contain no point of . Therefore,

for all with , from which we conclude that for sufficiently small. In particular, we have for and sufficiently small that

By letting and applying de l’Hospital’s rule twice we see that

In the same way we conclude from

that Thus

i.e. is bounded by . Since this holds for all , we have .

Proof of Lemma 3.11

We prove the claim that a

hypersurface that satisfies Assumption 3.2

has the property that every line segment from to can be replaced

by a continuous curve from to with

where is a given constant.

Let from now on , where is as in Assumption 3.2, so that in particular for every with there is a unique closest point on .

Denote by the line segment from to and identify it with it’s parameter representation . Let . For any set denote by the set of accumulation points of .

Proposition A.1.

Let . Then .

Proof.

Suppose this was not the case, i.e. . W.l.o.g. . Let be a sequence in with , . W.l.o.g, for all , or for all .

By Assumption 3.2 we have , where denotes the open ball with midpoint and radius .

Suppose for all . Then

and the last expression is smaller than for large enough. Thus we have found a point on , namely , with . But this contradicts the fact that is the point on closest to .

If for all , then the same argument carries through with replaced by . ∎

Denote the tangent hyperplane on in the point by , i.e. .

Proposition A.2.

For any we can find such that for any with we have that the line segment has precisely one intersection with .

Proof.

We can locally parametrize by a function on an open environment of in the tangent hyperplane . That is, there is an open interval and a -function such that every point can be uniquely written as . Since and thus , we may assume that for some . Choose some such that and such that for all we have whenever .

Now if with , then precisely one point of lies on the line segment . But there is no point of on the line segment , since this is entirely contained in the open ball , which by the unique closest point property for does not contain any point of .

By the same reasoning . ∎

Proposition A.3.

Let . Then for any there exists a point with and .

Proof.

If , then set . Otherwise, there is a unique closest point . Set

Then is obvious, and by the unique closest point property. ∎

We can now modify the straight line from to to get a

continuous curve, which is not much longer than , but

has only finitely many intersections with .

For what follows, let and for set

.

We construct a sequence of continuous curves of finite length which becomes stationary after finitely many steps, i.e. there exists such that for all .

Furthermore, will have only finitely many intersections with and it will be only slightly longer than , see (20).

Set .

Step :

If , then set .

Otherwise proceed as follows:

According to Proposition A.3 there exists a

point with and

.

Define as the concatenation of the lines

and . We have

, and there is at most one

intersection of , the second line segment, with , due to Assumption 3.2.

Set .

After step 1 we have constructed a polygonal curve such that

. If has infinitely

many intersections with , then all but finitely many are

contained in a single

line segment, , which satisfies

.

Now we enter an iteration procedure.

Suppose that after steps we have constructed

a polygonal curve , with the properties that

, and such that

either has finitely

many intersections with , or all intersections are

contained in a single

line segment, , which satisfies

.

We construct from as follows:

Step :

If , then set .

Otherwise, is contained in the line segment . Parametrize this segment by , and let .

Set , and let .

If is isolated from the left,

or if , then set . Now consider the case where is not isolated from the left.

By Proposition A.1, lies in the tangent hyperplane

and

we can find a small ball with radius such that, for any

with , the line

segment has

at most one intersection with , by Proposition A.2.

Consider the line segment .

If the intersection of this with the plane through , which is orthogonal to the line segment, is non-empty, denote the unique intersection point by .

Then we construct as the concatenation of the following line segments:

-

•

, which by definition of and has only finitely many intersections with ;

-

•

, which has at most one intersection with by the construction of and Proposition A.2;

-

•

, which is completely contained in , which does not contain any point of by the unique closest point property for ;

-

•

, which has no intersection with , because as , there is no intersection strictly between and , and lies in the closure of (this is where we need Step 1);

-

•

.

In this case the curve has only finitely many intersections with

and .

Otherwise, set , and construct as the concatenation of the following line segments:

-

•

, which by definition of and has only finitely intersections with ;

-

•

, which has at most one intersection with by the construction of and Proposition A.2;

-

•

, which is completely contained in , which does not contain any point of by the unique closest point property for ;

-

•

, which still may have infinitely many intersections with ;

-

•

.

Again we have that . Note that

In particular, . Note that , since otherwise the line segment would intersect the hyperplane orthogonal to and passing through .

Thus .

After step we have constructed a polygonal curve

such that

. If

has infinitely

many intersections with , then all but finitely many are

contained in a single

line segment, , and .

So finally we have constructed a sequence with

-

-

;

-

-

either has only finitely many intersections with , or all but finitely many intersections are contained in a segment of length at most .

Since , we have that , such that

With this, and since , the iteration can have at most

steps before the sequence becomes stationary, and thus there exists a such that has at most finitely many intersections with .

For the length of for we have

| (20) |

This can be made as close to as we desire by making small. Thus the proof is finished.

Acknowledgements

The authors thank Bert Jüttler for valuable discussions regarding questions related to differential geometry and Thomas Müller-Gronbach for pointing out an inaccuracy in the definition of .

G. Leobacher is supported by the Austrian Science Fund (FWF): Project F5508-N26, which is part of the Special Research Program "Quasi-Monte Carlo Methods: Theory and Applications". This paper was written while G. Leobacher was member of the Department of Financial Mathematics and Applied Number Theory, Johannes Kepler University Linz, 4040 Linz, Austria.

M. Szölgyenyi is supported by the Vienna Science and Technology Fund (WWTF): Project MA14-031. A part of this paper was written while M. Szölgyenyi was member of the Department of Financial Mathematics and Applied Number Theory, Johannes Kepler University Linz, 4040 Linz, Austria. During this time, M. Szölgyenyi was supported by the Austrian Science Fund (FWF): Project F5508-N26, which is part of the Special Research Program "Quasi-Monte Carlo Methods: Theory and Applications".

References

- Berkaoui [2004] A. Berkaoui. Euler Scheme for Solutions of Stochastic Differential Equations with Non-Lipschitz Coefficients. Portugaliae Mathematica, 61(4):461–478, 2004.

- Dudek and Holly [1994] E. Dudek and K. Holly. Nonlinear orthogonal projection. Annales Polonici Mathematici, 59(1):1–31, 1994.

- Étoré and Martinez [2013] P. Étoré and M. Martinez. Exact Simulation for Solutions of One-Dimensional Stochastic Differential Equations Involving a Local Time at Zero of the Unknown Process. Monte Carlo Methods and Applications, 19(1):41–71, 2013.

- Étoré and Martinez [2014] P. Étoré and M. Martinez. Exact Simulation for Solutions of One-Dimensional Stochastic Differential Equations with Discontinuous Drift. ESAIM: Probability and Statistics, 18:686–702, 2014.

- Foote [1984] R. L. Foote. Regularity of the Distance Function. Proceedings of the American Mathematical Society, 92(1):153–155, 1984.

- Gyöngy [1998] I. Gyöngy. A Note on Euler’s Approximation. Potential Analysis, 8:205–216, 1998.

- Halidias and Kloeden [2008] N. Halidias and P. E. Kloeden. A Note on the Euler–Maruyama Scheme for Stochastic Differential Equations with a Discontinuous Monotone Drift Coefficient. BIT Numerical Mathematics, 48(1):51–59, 2008.

- Hutzenthaler et al. [2012] M. Hutzenthaler, A. Jentzen, and P. E. Kloeden. Strong Convergence of an Explicit Numerical Method for SDEs with Nonglobally Lipschitz Continuous Coefficients. The Annals of Applied Probability, 22(4):1611–1641, 2012.

- Itô [1951] K. Itô. On Stochastic Differential Equations. Memoirs of the American Mathematical Society, 4:1–57, 1951.

- Karatzas and Shreve [1991] I. Karatzas and S. E. Shreve. Brownian Motion and Stochastic Calculus. Graduate Texts in Mathematics. Springer-Verlag, New York, second edition, 1991.

- Kloeden and Platen [1992] P. E. Kloeden and E. Platen. Numerical Solutions of Stochastic Differential Equations. Stochastic Modelling and Applied Probability. Springer Verlag, Berlin-Heidelberg, 1992.

- Kohatsu-Higa et al. [2013] A. Kohatsu-Higa, A. Lejay, and K. Yasuda. Weak Approximation Errors for Stochastic Differential Equations with Non-Regular Drift. 2013. Preprint, Inria, hal-00840211.

- Krantz and Parks [1981] S. G. Krantz and H. R. Parks. Distance to Hypersurfaces. Journal of Differential Equations, 40:116–120, 1981.

- Leobacher and Steinicke [2018] G. Leobacher and A. Steinicke. Existence, uniqueness and regularity of the projection onto differentiable manifolds. 2018. arXiv:1811.10578.

- Leobacher and Szölgyenyi [2016] G. Leobacher and M. Szölgyenyi. A Numerical Method for SDEs with Discontinuous Drift. BIT Numerical Mathematics, 56(1):151–162, 2016.

- Leobacher et al. [2014] G. Leobacher, M. Szölgyenyi, and S. Thonhauser. Bayesian Dividend Optimization and Finite Time Ruin Probabilities. Stochastic Models, 30(2):216–249, 2014.

- Leobacher et al. [2015] G. Leobacher, M. Szölgyenyi, and S. Thonhauser. On the Existence of Solutions of a Class of SDEs with Discontinuous Drift and Singular Diffusion. Electronic Communications in Probability, 20(6):1–14, 2015.

- Ruzhansky and Sugimoto [2015] M. Ruzhansky and M. Sugimoto. On Global Inversion of Homogeneous Maps. Bulletin of Mathematical Sciences, 5(1):13–18, 2015.

- Sabanis [2013] S. Sabanis. A Note on Tamed Euler Approximations. Electronic Communications in Probability, 18(47):1–10, 2013.

- Shardin and Szölgyenyi [2016] A. A. Shardin and M. Szölgyenyi. Optimal Control of an Energy Storage Facility Under a Changing Economic Environment and Partial Information. International Journal of Theoretical and Applied Finance, 19(4):1–27, 2016.

- Shardin and Wunderlich [2017] A. A. Shardin and R. Wunderlich. Partially Observable Stochastic Optimal Control Problems for an Energy Storage. Stochastics, 89(1):280–310, 2017.

- Szölgyenyi [2016] M. Szölgyenyi. Dividend Maximization in a Hidden Markov Switching Model. Statistics & Risk Modeling, 32(3-4):143–158, 2016.

- Veretennikov [1981] A. YU. Veretennikov. On Strong Solutions and Explicit Formulas for Solutions of Stochastic Integral Equations. Mathematics of the USSR Sbornik, 39(3):387–403, 1981.

- Veretennikov [1982] A. YU. Veretennikov. On the Criteria for Existence of a Strong Solution of a Stochastic Equation. Theory of Probability and its Applications, 27(3), 1982.

- Veretennikov [1984] A. YU. Veretennikov. On Stochastic Equations with Degenerate Diffusion with Respect to Some of the Variables. Mathematics of the USSR Izvestiya, 22(1):173–180, 1984.

- Zvonkin [1974] A. K. Zvonkin. A Transformation of the Phase Space of a Diffusion Process that Removes the Drift. Mathematics of the USSR Sbornik, 22(129):129–149, 1974.

G. Leobacher

Institute of Mathematics and Scientific Computing, University of Graz, Heinrichstraße 36, 8010 Graz, Austria

gunther.leobacher@uni-graz.at

M. Szölgyenyi 🖂

Institute of Statistics and Mathematics, Vienna University of Economics and Business, Welthandelsplatz 1, 1020 Vienna, Austria

michaela.szoelgyenyi@wu.ac.at