A Transformation Approach that Makes SPAI, PSAI and RSAI Procedures Efficient for Large Double Irregular Nonsymmetric Sparse Linear Systems††thanks: Supported in part by National Science Foundation of China (No. 11371219).

Abstract

A sparse matrix is called double irregular sparse if it has at least one relatively dense column and row, and it is double regular sparse if all the columns and rows of it are sparse. The sparse approximate inverse preconditioning procedures SPAI, PSAI() and RSAI() are costly and even impractical to construct preconditioners for a large sparse nonsymmetric linear system with the coefficient matrix being double irregular sparse, but they are efficient for double regular sparse problems. Double irregular sparse linear systems have a wide range of applications, and 24.4% of the nonsymmetric matrices in the Florida University collection are double irregular sparse. For this class of problems, we propose a transformation approach, which consists of four steps: (i) transform a given double irregular sparse problem into a small number of double regular sparse ones with the same coefficient matrix , (ii) use SPAI, PSAI() and RSAI() to construct sparse approximate inverses of , (iii) solve the preconditioned double regular sparse linear systems by Krylov solvers, and (iv) recover an approximate solution of the original problem with a prescribed accuracy from those of the double regular sparse ones. A number of theoretical and practical issues are considered on the transformation approach. Numerical experiments on a number of real-world problems confirm the very sharp superiority of the transformation approach to the standard approach that preconditions the original double irregular sparse problem by SPAI, PSAI() or RSAI() and solves the resulting preconditioned system by Krylov solvers.

keywords:

Linear system, preconditioning, sparse approximate inverse, double irregular sparse, double regular sparse, transformation approach, F-norm minimization, Krylov solverAMS:

65F10simaxxxxxxxxx–x

1 Introduction

In scientific and engineering computing, a core task is to solve the large sparse linear system

| (1) |

where is an real nonsymmetric and nonsingular matrix, and is a given -dimensional vector. Krylov iterative solvers, such as the generalized minimal residual method (GMRES) and the biconjugate gradient stabilized method (BiCGStab) [30], have been commonly used for solving (1) in nowdays. However, the convergence of Krylov solvers is generally extremely slow when is ill conditioned or has bad spectral property [30]. So it is necessary to use preconditioning techniques to accelerate the convergence of Krylov solvers. Sparse approximate inverse preconditioning procedures have been one class of the most important general-purpose preconditioning procedures over the past two decades [5, 16, 30]. Their goal is to construct a sparse approximate inverse or a factorized directly. The preconditioned linear system is with , or with , which corresponds to the right, left or factorized preconditioning, respectively.

There are mainly two kinds of constructing a sparse approximate inverse . Typical algorithms of constructing a factorized sparse approximate inverse are approximate inverse (AINV) type algorithms [6, 8] and the balanced incomplete factorization (BIF) algorithm [10, 11]. Stabilized and block versions of the AINV factorized approximate inverse preconditioner are proposed in [7]. Kolotilina and Yeremin [29] have proposed a factorized sparse approximate inverse (FSAI) preconditioning procedure with a prescribed sparsity pattern of . FSAI has been generalized to block form, called BFSAI, in [23]. An adaptive algorithm which gets the sparsity pattern of the BFSAI preconditioner can be found in [21, 22, 24].

The other kind of approach is based on F-norm minimization, which is inherently parallelizable and computes a right preconditioner by minimizing with certain sparsity constraints on , where denotes the Frobenius norm of a matrix and is the identity matrix of order . Applying this kind of approach to , one can compute a left preconditioner . A key of this kind of approach is the efficient determination of an effective sparsity pattern of . If the sparsity pattern of is prescribed, the resulting procedure is called a static one; if the sparsity pattern of is adaptively determined during the computational process, the procedure is called adaptive. For a-priori effective sparsity patterns of , we refer the reader to [3, 4, 13, 17, 20]. The SPAI algorithm proposed by Grote and Huckle [19] has been a popular adaptive F-norm minimization based sparse approximate inverse preconditioning procedure. It has been generalized to block form, called BSPAI, in [2]. Jia and Zhu [28] have proposed an adaptive Power sparse approximate inverse (PSAI) preconditioning procedure and developed a practical PSAI() algorithm that, during the loops, drops the nonzero entries in whose sizes are below some tolerance . PSAI() has been shown to be at least competitive with and can be substantially more effective than SPAI [27, 28]. Jia and Zhang [26] have recently established a mathematical theory on dropping tolerances for all static F-norm minimization based sparse approximate inverse procedures and PSAI(). Very recently, the authors of this paper have proposed a Residual based Sparse Approximate Inverse (RSAI) preconditioning procedure [25], which is different from the way used in SPAI and is based on only the partial but dominant other than all indices of nonzero entries in the current residual. They have developed a practical RSAI() algorithm with dropping strategies exploited. RSAI() improves the computational efficiency of SPAI substantially and meanwhile constructs effective preconditioners . For more on sparse approximate inverse preconditioning procedures, we refer the reader to [5, 9, 12, 16, 30].

For SPAI and PSAI(), Jia and Zhang [27] have investigated the efficiency of constructing and the preconditioning effectiveness of . They introduce the term of ’irregular sparse matrix’, where an irregular sparse means that it has at least one relatively dense column, whose number of nonzero entries is substantially more than the average number of nonzero entries per column of . In implementations, we call column irregular sparse if it has one column whose number of nonzero entries is at least , where is the average number of nonzero entries per column of [27]. Following this standard, it is reported in [27] that column irregular linear problems have a wide range of applications and 34% of the square matrices in the University of Florida sparse matrix collection [14] are column irregular sparse; see [27] for further information on where column irregular sparse matrices come from and how dense irregular columns are, etc. For a column irregular sparse , Jia and Zhang [27] have shown that SPAI and PSAI() are costly and may be impractical; they have given theoretical arguments and numerical evidence that obtained by SPAI may be ineffective for preconditioning (1), but by PSAI() is effective though its construction is costly. Their analysis has also revealed that SPAI and PSAI() are costly when applied to for computing left preconditioners for column irregular sparse, that is, we compute by minimizing with certain sparsity constraints on .

In the same way, we call row irregular sparse if it has at least one relatively dense row. If is both column and row irregular sparse, it is called double irregular sparse. In contrast, if all the columns and rows of are sparse, is called double regular sparse. Using the same standard as that of an irregular column, we define an irregular row. By this definition, a column irregular symmetric matrix is double irregular sparse. We have investigated all the real nonsymmetric square matrices in the collection [14], which contains 775 matrices. We have found that 189 of them are double irregular sparse, that is, 24.4% of the nonsymmetric matrices in the collection are double irregular. This indicates that double irregular sparse linear systems have a wide range of practical applications. Numerical experiments have illustrated that RSAI() improves the computational efficiency of SPAI substantially for column irregular sparse problems [25]. However, we will see that RSAI() is expensive and may be impractical for row irregular sparse problems. This is also the case for PSAI(); see [27].

Summarizing the above, we come to the conclusion that SPAI, PSAI() and RSAI() are costly and even impractical for double irregular sparse problems. Therefore, how to efficiently use the three preconditioning procedures to solve double irregular sparse linear systems is of great importance. We will focus this topic in the current paper.

As is known from [25, 27, 28], a common and attractive feature of the aforementioned three procedures is that they can construct preconditioners efficiently for double regular sparse, among of which PSAI() is most effective and SPAI and RSAI() are comparably effective for preconditioning double regular sparse linear systems. For the column irregular sparse (1), making use of the Sherman-Morrison-Woodbury formula, Jia and Zhang [27] have proposed an approach that transforms (1) into a small number of column regular sparse ones with the same coefficient matrix and multiple right-hand sides, so that SPAI and PSAI() can construct preconditioners for the regular sparse problems much more efficiently than they do for (1) directly. An approximate solution of the original system with a prescribed accuracy is then recovered from those of the regular sparse ones with the accuracy determined by . The numerical experiments in [27] have indicated that such transformation approach speeds up the computational efficiency of SPAI and PSAI() very substantially, compared to them applied to the original problem. However, the transformation approach does not suit for row irregular sparse problems, for which SPAI, PSAI() and RSAI() are still costly, as has been pointed out above.

In this paper, we show that a double irregular sparse matrix can be expressed as the sum of a double regular sparse and two certain low rank matrices. Motivated by the work [27], by exploiting the Sherman-Morrison-Woodbury formula [18] twice, we propose an approach that transforms the irregular sparse into a regular sparse and (1) into linear systems with the same coefficient matrix and right-hand sides, where and are the numbers of relatively dense columns and rows, respectively. The transformation consists of two steps: first transform with dense columns into a column regular sparse matrix , then transform with dense rows into a double regular sparse matrix . Since is supposed to be sparse, and must be very small. As it will turn out, the double regular sparse equals minus two matrices of low ranks and , respectively. Then we use SPAI, PSAI() and RSAI() to construct preconditioners for these double regular sparse systems and solve the resulting preconditioned linear systems by Krylov solvers. Finally, we recover the solution of (1) from those of the double regular sparse ones. The above whole process is called the transformation approach. We consider a number of theoretical and practical issues, including the non-singularity of and its conditioning. Particularly, we prove how to design stopping criteria for the double regular linear systems in order to ultimately obtain an approximate solution of (1) with a prescribed accuracy from those of the double regular ones. Numerical experiments will exhibit the very sharp efficiency of our transformation approach to the standard approach that first preconditions (1) by SPAI, PSAI() or RSAI() and then solves the preconditioned linear system by Krylov solvers. We will demonstrate that, due to the memory storage and huge computational cost, SPAI, PSAI() and RSAI() are either out of memory or cannot generate preconditioners within 100 hours when directly applied to six of the ten real-world double irregular sparse problems, but our transformation approach works very efficiently for all the test problems and consumes only a few seconds to no more than half an hour for the six hard problems that the standard approach fails to solve.

The paper is organized as follows. In Section 2, we briefly review SPAI, PSAI() and RSAI() procedures. In Section 3, we propose our transformation approach for solving the double irregular sparse problem (1). In Section 4, we consider some theoretical and practical issues. In Section 5, we report on numerical experiments, confirming the very sharp superiority of our transformation approach to the standard approach that preconditions (1) by SPAI, PSAI() or RSAI() directly and solves it by Krylov solvers. Finally, we conclude the paper in Section 6.

2 The SPAI, PSAI() and RSAI() procedures

For an F-norm minimization based sparse approximate inverse preconditioning procedure, we need to solve the constrained minimization problem

| (2) |

where is the set of matrices with a given sparsity pattern . Define as the set of -dimensional vectors whose sparsity pattern is , and let . Then (2) is recast as the independent constrained least squares (LS) problems

| (3) |

where is the th column of . Here and hereafter, denotes the 2-norm of a matrix or vector. For each , denote by the set of indices of nonzero rows of . Then (3) amounts to solving the smaller unconstrained LS problems

| (4) |

which can be solved by QR decompositions in parallel.

If is not yet good enough, that is, (3) does not drop below a prescribed tolerance for at least one , one can use some adaptive sparse approximate inverse preconditioning procedure, e.g., SPAI, PSAI() or RSAI() to improve it by augmenting or adjusting the sparsity pattern dynamically. We highlight that, mathematically, the unique fundamental distinction of all the adaptive F-norm minimization based sparse approximate inverse preconditioning procedures is the way that augments or adjusts the sparsity pattern of . It has been shown in [27, 28] that PSAI() captures the sparsity pattern of more effectively than SPAI; moreover, the effectiveness of PSAI() is independent of whether is (column or row) regular sparse or not, while SPAI is more effective for regular sparse matrices than for irregular sparse ones. In [25], the authors have shown that RSAI() and SPAI compute comparably effective preconditioners but the former is more efficient than the latter. In what follows we briefly review SPAI, PSAI() and RSAI().

2.1 The SPAI procedure

Denote by the sparsity pattern of after loops starting with an initial pattern , and define to be the set of all nonzero row indices of . Denote the residual of (3) by

| (5) |

If , denote by the set of indices for which and the set of indices of nonzero columns of . Then

| (6) |

forms the new candidates for augmenting in the next loop of SPAI, in which is updated as follows [19]: For each , consider the one-dimensional minimization problem

| (7) |

whose solution is

| (8) |

and the 2-norm of the new residual satisfies

| (9) |

SPAI selects a few, say , most profitable indices from with the smallest and adds them to to obtain . Define to be the set of indices of new nonzero rows corresponding to the most profitable indices added, and let . Then we solve the new LS problem

| (10) |

whose solution can be updated from the previous efficiently. Proceed in such a way until or reaches the prescribed maximum , where is a mildly small tolerance, usually, ; see [19, 27, 28]. Obviously, if the cardinality of is very big, SPAI is costly, which corresponds to the case that the th column of is dense [27, 28]. Precisely, suppose that the th column of is almost fully dense. SPAI has to compute almost numbers by (9), then sort almost indices in by comparing the sizes of and finally pick up a few most profitable indices among them. This is very time consuming and can make SPAI fatally slow. Similarly, it is easy to justify that SPAI is costly when an index in corresponds to a relatively dense row of , which results in a very big cardinality of . Therefore, SPAI is costly and even impractical for double irregular sparse.

2.2 The PSAI() procedure

We first review the basic PSAI (BPSAI) procedure proposed in [28], which is motivated by the Cayley–Hamilton theorem: can be expressed as

| (11) |

where and the are certain constants for . Denote by the sparsity pattern of a matrix or vector, and define the matrix . We see from (11) that . So the pattern of a good sparse approximate inverse can be taken as for a given small in BPSAI. As a result, the sparsity pattern of the th column of is a subset of since .

For , BPSAI updates the sparsity pattern adaptively in the following way: For , denote by the sparsity pattern of at loop and by the set of nonzero row indices of . Define with . Then the sparsity pattern . Denote by the set of new nonzero row indices of , and let . Then the new LS problem (4) can be solved by updating instead of resolving it. Proceed in such a way until or .

In order to develop a practical algorithm, we must control the sparsity of . Jia and Zhu [28] have proposed the PSAI() algorithm, which, during the loops, drops those nonzero entries whose magnitudes are below a prescribed threshold and retains only those large ones. It has turned out that the choice of has strong effects on the preconditioning effectiveness and sparsity of . Jia and Zhang [26] have established a mathematical theory on robust dropping tolerances for PSAI() and all the static F-norm minimization based sparse approximate inverse preconditioning procedures. According to the theory, they have designed an adaptive and robust dropping criterion: At loop , a nonzero entry is dropped if

| (12) |

where is the number of nonzero entries in and is the 1-norm of a matrix. From the theory in [26], PSAI() with the above dropping criterion will compute a preconditioner that is as sparse as possible and meanwhile has comparable preconditioning quality to the one generated by BPSAI without dropping any nonzero entries. However, PSAI() involves large sized LS problems for column irregular sparse matrices and is thus costly or simply faces out of memory, though obtained by it is an effective preconditioner [27]. As a whole, if is double irregular sparse, PSAI() is costly and may be impractical.

2.3 The RSAI() procedure

We first review the basic RSAI (BRSAI) procedure [25]. Suppose that is the sparsity pattern of generated by BRSAI after loops starting with the initial sparsity pattern . If does not yet satisfy the prescribed accuracy , BRSAI improves by augmenting its sparsity pattern as follows.

Denote by the set of indices for which the -th entry of . BRSAI takes precedence to reduce a few largest entries in since they make the most contributions to the size of . The indices corresponding to the largest entries of are called the dominant indices. Denote by the set of the dominant indices with the largest entries , and define to be the set of all new column indices of that correspond to but do not appear in . Then we set

When choosing from in the above way, it may happen that . If so, set

and choose from the set whose elements are in but not in . In this way, is always non-empty unless is exactly the th column of [25]. Denote by the set of indices of new nonzero rows corresponding to the added column indices . Then we update and solve the new LS problem (10), which generates a better approximation to the th column of . Repeat this process for until or exceeds .

Similar to the PSAI() algorithm, in order to control the sparsity of , a practical RSAI() algorithm has been developed in [25] that introduces the dropping criterion (12) into BRSAI. It has been shown in [25] that RSAI() is as equally effective as SPAI, but it is more efficient than SPAI because we uses only a few other than all indices of the nonzero and do not compute possibly a great many numbers in SPAI, avoiding sorting them and picking up the most profitable indices. However, RSAI() may be costly or out of memory for is row irregular sparse: Suppose that the th row of is relatively dense. Then once , the resulting is also relatively dense, leading to a relatively large sized (4). Therefore, if is double irregular sparse, RSAI() may be very costly and impractical.

3 Transformation of double irregular sparse linear systems into double regular sparse ones

The previous discussion has indicated that SPAI, PSAI() and RSAI() is costly and even impractical when is double irregular sparse. In order to improve their efficiency, we will propose a transformation approach, which consists four steps: (i) transform a double irregular sparse (1) into a small number of double regular sparse ones with the same coefficient matrix , (ii) use SPAI, PSAI() and RSAI() efficiently construct possibly effective sparse approximate inverses of , (iii) solve the preconditioned double regular sparse linear systems by Krylov solvers, and (iv) recover an approximate solution of (1) with a prescribed accuracy from those of the double regular sparse ones. One of the key ingredients of the transformation approach is the following well-known Sherman-Morrison-Woodbury formula [18, p. 50]).

Lemma 1.

Let with . If is nonsingular, then is nonsingular if and only if is nonsingular. Furthermore,

| (13) |

In practical applications, one is typically interested in the formula for , which reduces to the Sherman-Morrison formula when .

In what follows, for the given double irregular sparse we assume that the th columns and the th rows of are relatively dense, respectively. Let , where is the th column of and is the sparsification of , each column of which is sparse and retains nonzero entries of , where is the average number of nonzero entries per column of with the number of nonzero entries of . Let . Obviously, the nonzero entries of are just those dropped ones of . Define to be the matrix that replaces the dense columns of by the sparse vectors , . Then is column regular sparse and satisfies

| (14) |

where with the th column of . Obviously, is of rank . Assume that and are nonsingular. By (13), we have

| (15) |

Clearly, the th rows of are still dense. Next, we further transform into double regular sparse. Let , where is the th dense row of , . Define to be the sparsification of , where each row is sparse and retains only nonzero entries of , where is the average number of nonzero entries per row of . Let . Then the nonzero entries of are just those dropped ones of . Let be the matrix that replaces the dense rows of by the sparse vectors , . Then is double regular sparse and is related to by

| (16) |

where with the th column of and is of rank .

The combination of (14) and (16) gives

| (17) |

As a result, we have transformed the double irregular sparse into the double regular sparse , which modifies with two low rank and matrices and , respectively.

Assume that and are nonsingular. By (13), we have

| (18) |

From (15), the solution of (1) is

| (19) |

which requires to compute and . Substituting (18) into (19), we obtain

| (20) |

and

| (21) |

which require to compute , and . It is now clear that from (18)–(21) that the ultimate computation of needs , and as well as the inversions of the small matrix and matrix , whose costs are negligible relative to the computation of , and .

Keep in mind and . Then the computation of , and amounts to solving the following double regular sparse linear systems:

| (22) | |||||

| (23) | |||||

| (24) |

With the above derivation, we can now summarize our transformation approach to solving as Algorithm 1. In our context, its implementation consists of four steps: Firstly, we construct the double regular sparse ; secondly, we compute a sparse approximate inverse of by SPAI, PSAI() or RSAI() and use it as a preconditioner for the double regular sparse linear systems; thirdly, we solve the preconditioned systems approximately by Krylov solvers; finally, we recover the solution of (1) from the solutions of the double regular sparse linear systems. The three procedures SPAI, PSAI() and RSAI() are expected to be much more efficient than them applied to directly. On the other hand, as shown in [27, 28], as preconditioners, the constructed by the three procedures applied to are at least as effective as the corresponding ones applied to .

Finally, it is particularly worthwhile to stress that, as is known from [5, 9, 16], that the CPU time of constructing overwhelms that of Kryolv solvers for the preconditioned systems even in a parallel computing environment, provided that is an effective preconditioner. This is a typical feature of F-norm minimization based and factorized sparse approximate inverse preconditioning procedures. Nonetheless, as is pointed out in [5, 9, 16], although -norm minimization sparse approximate inverse preconditioning procedures are more costly than incomplete LU (ILU) type preconditioning procedures, they are more robust, stable and general than the latter ones are. Also importantly, the action of is to only form matrix-vector products, which is substantially advantageous to ILU’s where at each iteration of Krylov solvers one must solve an auxiliary linear system with the given preconditioner as the coefficient matrix. Lastly, -norm minimization based sparse approximate inverse preconditioning procedures are naturally parallelizable and suit better for the linear systems with the same coefficient matrix but multiple right-hand sides, whereas ILU preconditioning is inherently sequential and has very limited parallelization. In view of these, the overall performance of Algorithm 1 is expected to very greatly outperform the standard approach that first preconditions (1) by SPAI, PSAI() or RSAI() directly and then solves it by Krylov solvers.

4 Theoretical analysis and practical considerations

In this section, we will give some theoretical analysis and practical considerations on the proposed transformation approach. Within the framework of Algorithm 1, we then develop a practical iterative solver for (1). To this end, we need to consider several issues.

First of all, we adapt the definition of column irregular sparse in [27] to double irregular sparse: A column or row is claimed to be dense if the number of nonzero entries in it exceeds or , where and are the average numbers of nonzero entries per column of and that per row of , respectively. The second issue is which nonzero entries in and should be dropped to generate and . We deal with this issue as follows: Suppose that all the diagonals of are nonzero. We then adopt the same strategy as that in [27] and retain the diagonal and the or nonzero entries nearest to the diagonal in each column of or each row of .

As we have seen, when transforming the double irregular sparse (1) into the double regular sparse ones, we always assume that the column regular sparse and the double regular sparse are nonsingular. Our third issue arise naturally: for which classes of matrices , one can ensure the nonsingularity of ? Jia and Zhang [27] have investigated this problem in some detail for the column regular sparse and established a number of results, which are directly adapted to our current double regular sparse , as Theorem 2 and Corollary 3 states.

Theorem 2.

obtained by the above transformation approach is nonsingular for

the following classes of matrices:

(i) is strictly row or column diagonally dominant.

(ii) is irreducibly row or column diagonally dominant.

(iii) is an -matrix.

(iv) is an –matrix.

The above four classes of matrices have wide applications. Similar to [27], we can extend the first two classes of matrices in Theorem 2 to more general forms.

Corollary 3.

obtained by the above transformation approach is nonsingular for

the following classes of matrices:

(i) or is strictly row or column diagonally dominant

where is an arbitrary nonsingular diagonal matrix.

(ii) is strictly row or column diagonally dominant

where and are permutation matrices.

(iii) or is strictly row or column diagonally dominant

where is an arbitrary nonsingular diagonal matrix and are

permutation matrices.

(iv) is an irreducible analogue of the matrices in

(i)–(iii).

There should exist more classes of matrices for which the resulting are nonsingular. We do not pursue this topic further. Strikingly, we will numerically find that for a general nonsingular that does not belong to the aforementioned classes of matrices, the resulting is indeed nonsingular. This fact has been extensively verified for column irregular sparse matrices and column regular sparse [27].

The fourth issue is the conditioning of . Theoretically, for a general nonsingular , the conditioning of may become better or worse. However, when is a strictly row or column diagonally dominant matrix or a -matrix, Jia and Zhang [27] have given mathematical justifications on why the resulting column regular sparse is generally better conditioned than . The same arguments works for these classes of matrices in our current context, and can be shown to be generally better conditioned than . Remarkably, later numerical experiments will indicate that the resulting is always and often considerably better conditioned than a general double irregular sparse which does not fall into the matrices in Theorem 2 and Corollary 3.

The above considerations on the third and fourth issues indicates that our transformation approach is of generality in practical applications.

Our final issue is the selection of stopping criteria for Krylov solvers applied to the double regular sparse linear systems for a given the prescribed accuracy for (1). This selection is crucial for reliably recovering an approximate solution of (1) with the prescribed accuracy . In order to solve this problem, we present the following theorem, based on which we can design reliable stopping criteria for the double regular sparse linear systems.

Theorem 4.

For and defined in Algorithm 1, let , , and , , be the approximate solutions of (22), (23) and (24), respectively. Define , and the residuals , , , assume that is nonsingular, and define and , and take

| (28) |

and

| (29) |

to be the approximations of and defined by (20) and (21), respectively. Assume that is nonsingular, and define and

| (30) |

to be an approximate solution of . Then if

| (31) |

| (32) |

and

| (33) |

we have

| (34) |

Proof.

Define and . From (14), we obtain

| (35) |

Though Theorem 4 gives the stopping criteria for the double regular sparse problems, they are not directly applicable for the prescribed accuracy of (1). The reason is that , and can be computed only until iterations for (22), (23) and (24) terminate, but the stopping criteria (32) and (33) for (23) and (24) depend on , and . As a result, the computation of , and and the termination of iterative solvers interact, and cannot be done in advance. Fortunately, it appears that the accurate estimates of , and are unnecessary and quite rough ones are enough. It is seen that is moderate if is not ill conditioned. Suppose that and are not very ill conditioned. We observe that and rely on the norm of and depends on the norm of . In implementations, we simply take and . In numerical experiments, we will find that such choices of , and work reliably and makes (34) hold for all the test problems.

Having done the above, we have finally developed Algorithm 1 into a truly working algorithm, called Algorithm 2 hereafter.

5 Numerical experiments

In this section, we test Algorithm 2 on ten real-world double irregular sparse nonsymmetric problems listed in Table 1, which are from [14]. We first construct sparse approximate inverses of double regular sparse matrices by SPAI, PSAI() or RSAI() and then solve the resulting preconditioned double regular sparse linear systems by the Krylov solver BiCGStab, whose code bicgstab.m is from Matlab 7.8.0. We will compare Algorithm 2 with the standard approach that preconditions (1) by SPAI, PSAI() or RSAI() directly and solves the preconditioned double irregular sparse system by BiCGStab. Depending on which of SPAI, PSAI() and RSAI() is used, Algorithm 2 gives rise to three algorithms, named New-SPAI, New-PSAI() and New-RSAI(), abbreviated as N-SPAI, N-PSAI() and N-RSAI(), respectively. Similarly, we denote by S-SPAI, S-PSAI(), and S-RSAI() the algorithms that directly precondition (1) by SPAI, PSAI() and RSAI(), respectively.

We will make numerous comparisons. Most importantly, in terms of the CPU time, we shall demonstrate that N-SPAI, N-PSAI() and N-RSAI() outperform S-SPAI, S-PSAI() and S-PSAI() very greatly, respectively. Particularly, we will show that S-SPAI, S-PSAI() and S-PSAI() fail to compute preconditioners for the last six larger ones of the ten test problems because of huge computational cost or memory storage, but N-SPAI, N-PSAI() and N-RSAI() work very well.

| matrices | Description | ||

|---|---|---|---|

| rajat04 | 1,041 | 8,725 | circuit simulation problem |

| rajat12 | 1,879 | 12,818 | circuit simulation problem |

| rajat13 | 7,598 | 48,762 | circuit simulation problem |

| memplus | 17,758 | 99,147 | computer component design memory circuit |

| ASIC_100k | 9,9340 | 940,621 | Sandia, Xyce circuit simulation matrix |

| dc1 | 116,835 | 766,396 | circuit simulation problem |

| dc2 | 116,835 | 766,396 | circuit simulation problem |

| dc3 | 116,835 | 766,396 | circuit simulation problem |

| trans4 | 116,835 | 749,800 | circuit simulation problem |

| trans5 | 116,835 | 749,800 | circuit simulation problem |

We perform numerical experiments on an Intel Core 2 Quad CPU E8400@ 3.00GHz with 2GB RAM using Matlab 7.8.0 with the machine precision under the Linux operating system. We use the SPAI 3.2 package [1] for the SPAI algorithm, which is written in C/MPI and is an optimized code in some sense. PSAI() and RSAI() are experimental Matlab codes in the sequential environment. We take the initial sparsity pattern as that of for SPAI and RSAI(). We apply row Dulmage-Mendelsohn permutations to the matrices having zero diagonals so as to make their diagonals nonzero [15]. The related Matlab command is , which is applied to rajat04, rajat12, rajat13 and ASIC_100k. We take , and as the values defined in the end of Section 4, and stop BiCGStab when (31), (32) and (33) are satisfied with or 1,000 iterations are used. The initial guess of the solution to each problem is always and the right-hand side is formed by choosing the solution . We have found that BiCGStab without preconditioning does not converge for all the test problems in Table 1 within 1,000 iterations except for rajat04, rajat12 and rajat13. With defined by (30), we compute the actual relative residual norm

| (39) |

and compare it with the required accuracy .

In Table 2, we give some information on and constructed by Algorithm 2. It is observed that all the test matrices have some almost fully dense columns and rows except rajat04, rajat12, rajat13 and memplus. It is also seen from the table that and are very small relative to , as they must be. Having sparsified those dense columns and rows, we find that the number of nonzero entries in are considerably smaller than those in . We remark that all the test matrices do not belong to the classes of matrices in Theorem 2, but the table shows that all the are always better and can be better conditioned than the corresponding by one to nearly three orders, as the condition numbers and indicate clearly. This demonstrates that our transformation of into is of practical generality that ensures not only the non-singularity of but also improves the conditioning of the double regular sparse linear systems.

| matrices | |||||||||

| rajat04 | 5 | 6 | 8 | 642 | 659 | 5702 | |||

| rajat12 | 9 | 9 | 6 | 1,195 | 1,190 | 6,803 | |||

| rajat13 | 29 | 29 | 6 | 5,412 | 5,383 | 27,232 | |||

| memplus | 144 | 124 | 6 | 353 | 319 | 67,649 | |||

| ASIC_100k | 132 | 129 | 9 | 92,258 | 92,165 | 543,876 | |||

| dc1 | 55 | 54 | 6 | 114,174 | 114,184 | 425,819 | |||

| dc2 | 55 | 54 | 6 | 114,174 | 114,184 | 425,819 | |||

| dc3 | 55 | 54 | 6 | 114,174 | 114,184 | 425,819 | |||

| trans4 | 55 | 54 | 6 | 114,174 | 114,184 | 425,819 | |||

| trans5 | 55 | 54 | 6 | 114,174 | 114,184 | 425,819 |

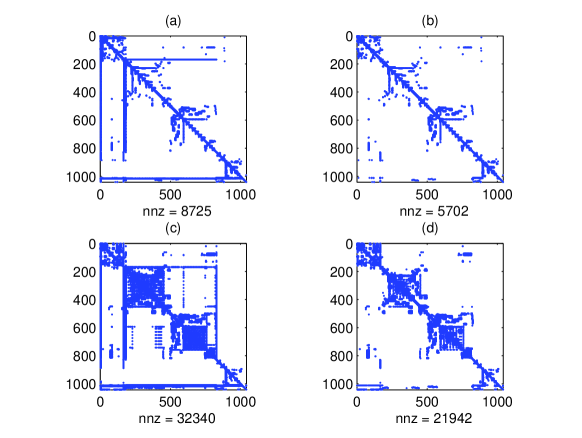

Now we look into the effective approximate sparsity pattern of and that of obtained by our transformation approach. We aim to show that effective sparse approximate inverses of double irregular and regular sparse matrices are structure preserving, though theoretically good approximate inverses of a double regular sparse matrix may be irregular sparse [27]. We take rajat04 as an example. Performing a row Dulmage-Mendelsohn permutation on it, we depict the sparsity patterns of and . We first use the Matlab function inv to compute and accurately and then drop their nonzero entries whose magnitudes fall below so as to obtain good sparse approximate inverses of and . Figure 1 depicts the patterns of , , and the sparsified and . Clearly, the generated good approximate inverse of is sparse, but it is double irregular sparse, whose numbers of irregular columns and rows are no less than those of . In contrast, for the double regular sparse , the generated good sparse approximate inverse of it is not only double regular sparse but also considerably sparser than that of . These observations imply that SPAI is not only costly but also cannot construct effective preconditioners of (1) since the by SPAI are column regular sparse unless the loops are allowed to be very big, which is prohibited for SPAI. PSAI() and RSAI() are also costly. In contrast, since good sparse approximate inverses of are generally double regular sparse, it is expected that SPAI, PSAI() and RSAI() construct good approximate inverses of much more efficiently than they do for .

In the later tables, we denote by or the sparsity of relative to or , by the number of columns of whose residual norms do not drop below the prescribed accuracy , by and the CPU time (in seconds) of constructing and that of solving the preconditioned linear systems by BiCGStab, respectively. The notation means that we do not count CPU time when BiCGStab fails to converge within 1000 iterations. Let the actual relative residual norm . Then means that our choices of and work reliably and relative residual norm (39) satisfies the prescribed accuracy .

5.1 S-SPAI and N-SPAI

We will show that N-SPAI is much more efficient than S-SPAI with the same parameters used in SPAI, in which the initial pattern of is that of , and we take , and add five most profitable indices to the pattern of at each loop for . The number of nonzero entries in is therefore no more than for the given parameters. Consequently, if good preconditioners have at least one column whose number of nonzero entries is bigger than 101, SPAI may be ineffective for preconditioning (1). Table 3 shows the results, where the notation indicates that S-SPAI could not construct when 100 hours are consumed, and the notation stands for the numbers of iterations and maximum iterations that BiCGStab uses for (1) and the systems (22), (23) and (24), respectively.

| S-SPAI | N-SPAI | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| matrices | ||||||||||||

| rajat04 | 0.37 | 1.18 | 6 | 0.33 | 30 | 0.14 | 0.39 | 0.05 | 2 | 0.27 | 15 | 0.07 |

| rajat12 | 0.89 | 3.19 | 3 | 0.58 | 46 | 0.04 | 0.81 | 0.03 | 0 | 0.35 | 38 | 0.25 |

| rajat13 | 0.92 | 271.2 | 6 | 0.91 | 73 | 0.19 | 1.16 | 0.27 | 2 | 0.12 | 8 | 0.35 |

| memplus | 1.05 | 13.6 | 0 | 0.70 | 92 | 0.40 | 1.35 | 0.48 | 0 | 0.50 | 23 | 4.06 |

| ASIC_100k | 0.55 | 4.36 | 12 | 0.35 | 9 | 27.0 | ||||||

| dc1 | 1.10 | 8.80 | 6 | 0.31 | 314 | 95.8 | ||||||

| dc2 | 1.04 | 7.70 | 0 | 0.40 | 107 | 51.6 | ||||||

| dc3 | 1.06 | 8.01 | 6 | 0.28 | 81 | 55.8 | ||||||

| trans4 | 1.14 | 8.05 | 0 | 0.26 | 37 | 10.0 | ||||||

| trans5 | 1.13 | 9.00 | 0 | 0.47 | 79 | 20.1 | ||||||

From Table 3, we find that all the for all the test problems. This indicates that our choices of and are reliable in practice. For the last six larger problems S-SPAI could not construct within 100 hours but N-SPAI does the job in no more than nine seconds, and Algorithm 2 solves all the preconditioned double regular sparse linear systems with the total CPU time () between seconds, very dramatic improvements over the standard approach! The reason is that each of these matrices contains some fully dense columns and rows, so that SPAI spends unaffordable time in finding most profitable indices because of the large cardinalities of and for at each loop. Precisely, for a double irregular sparse matrix whose irregular column and row are fully dense, at each loop , SPAI has to compute almost numbers by (9), then sort almost indices in by comparing the sizes of and finally pick up a few most profitable indices among them. This is a huge computational task and makes SPAI fatally slow. In contrast, N-SPAI overcomes this drawback very well since there are only a very small number of elements in and N-SPAI only needs to compute the same number of and select the most profitable indices. This is why N-SPAI outperforms S-SPAI so dramatically. For each of the smaller rajat04, rajat12, rajat13 and the relatively large memplus whose irregular rows and columns are, though relatively dense, far from fully dense, we observe that the by N-SPAI is still much smaller than the corresponding one by S-SPAI and the CPU time is reduced by tens to one thousand of times. So, even for that does not have very dense irregular columns and rows, N-SPAI exhibits its much higher efficiency than S-SPAI does.

We next look at the preconditioning effectiveness of . We observe that the in S-SPAI are bigger than those counterparts in N-SPAI for rajat04, rajat12, rajat13 and memplus. This demonstrates that SPAI is difficult to capture a good approximate sparsity pattern of when is double irregular sparse. This is also confirmed by the numbers ’s, which show that BiCGStab converges much faster for the the double regular sparse problems than for (1), that is, SPAI is considerably less effective for preconditioning double irregular sparse linear systems than it is for double regular sparse ones.

Finally, we compare our transformation approach with that in [27], where double irregular sparse matrices are only transformed into column regular sparse ones, which are still row irregular sparse for our test matrices. Therefore, SPAI is still time consuming, though its efficiency is improved greatly relative to its application to directly. We mention that for numerical experiments we use the same computer as that in [27]. Precisely, for the last six larger matrices, the approach used in [27] takes about half an hour to two hours to construct the , while our approach here only costs about eight seconds, improvements of hundreds of times!

5.2 S-PSAI() and N-PSAI()

We will illustrate that N-PSAI() is much more efficient than S-PSAI(), where we take and . Table 4 shows the results, where the notation indicates that our computer is out of memory when constructing due to the appearance of large sized LS problems.

| S-PSAI() | N-PSAI() | |||||||||||

| matrices | ||||||||||||

| rajat04 | 0.72 | 1.40 | 0 | 0.79 | 11 | 0.01 | 0.39 | 0.18 | 0 | 0.15 | 13 | 0.08 |

| rajat12 | 2.22 | 3.48 | 0 | 0.74 | 32 | 0.03 | 2.11 | 0.80 | 0 | 0.28 | 37 | 0.19 |

| rajat13 | 1.36 | 204 | 0 | 0.19 | 4 | 0.07 | 0.91 | 0.17 | 0 | 0.29 | 6 | 0.27 |

| memplus | 6.25 | 624 | 0 | 0.98 | 215 | 1.30 | 1.78 | 48.6 | 0 | 0.35 | 27 | 4.08 |

| ASIC_100k | 0.43 | 582 | 0 | 0.34 | 8 | 27.7 | ||||||

| dc1 | 1.67 | 1340 | 0 | 0.26 | 379 | 101 | ||||||

| dc2 | 1.71 | 1295 | 0 | 0.36 | 58 | 48.3 | ||||||

| dc3 | 1.73 | 1299 | 0 | 0.47 | 54 | 44.0 | ||||||

| trans4 | 1.80 | 1679 | 0 | 0.26 | 28 | 10.9 | ||||||

| trans5 | 1.62 | 1475 | 0 | 0.73 | 60 | 17.8 | ||||||

From the table, we observe that all the for all the test problems. This indicates that our choices of and are reliable. Clearly, the table tells us that for the last six larger problems S-PSAI() could not construct . This is because that each of these has fully dense columns, which lead to some large LS problems (4) with dimensions and generate some fully dense before dropping small nonzero entries in them; see [27, 28] for details. So, for large, PSAI() faces a severe difficulty when applied to column irregular sparse matrices. In contrast, with the same parameters, N-PSAI() overcomes this difficulty very well and computes effective preconditioners efficiently for the last six larger problems. By comparison, for rajat04, rajat12, rajat13 and memplus, N-PSAI() can construct the several or many times faster than S-PSAI(). However, unlike SPAI, we observe all , indicating that both S-PSAI() and N-PSAI() succeed in finding effective sparse approximate inverses, which confirms the theory that PSAI() can capture effective approximate sparsity patterns of the inverse of a sparse matrix, independent of whether the matrix is regular or irregular sparse [27, 28].

Next, we compare our transformation approach with that used in [27], which only transforms double irregular sparse into column regular sparse ones. We point out that good sparse approximate inverses of a row irregular sparse matrix may have some relative dense columns; see Figure 5.2 of [27] for rajat04. In this case, PSAI() needs to solve some LS problems whose sizes are not as small as those for double regular sparse matrices, which causes PSAI() to be considerably more costly for only column regular sparse matrices than for double regular sparse ones. Indeed, in comparison with the results obtained by the approach in [27], we find that for the last six larger matrices our approach saves about half the CPU time .

Finally, we make some comments on N-SPAI and N-PSAI(). From Tables 3–4, we find that the by N-SPAI and N-PSAI() are correspondingly comparable but N-PSAI() is at least competitive with N-SPAI and the former is considerably more effective than the latter for preconditioning half of the test problems, as indicated by the corresponding and . This justifies that PSAI() is more effective than SPAI to capture good sparsity patterns of approximate inverses even for double regular sparse matrices. In addition, we have noticed that N-PSAI() is more costly than N-SPAI. This is simply due to our non-optimized code of PSAI() in the Matlab language, whose efficiency is inferior to the optimized SPAI code written in C/MPI.

5.3 S-RSAI() and N-RSAI()

We will demonstrate that N-RSAI() is much more efficient than S-RSAI(). We take and , and use three dominant indices with the largest at each loop for . Table 5 lists the results, where the notation indicates that S-RSAI() could not construct within 25 hours and indicates that our computer is out of memory when constructing due to the appearance of large sized LS problems resulting from the relatively dense rows of .

| S-RSAI() | N-RSAI() | |||||||||||

| matrices | ||||||||||||

| rajat04 | 7.26 | 9.05 | 3 | 0.34 | 17 | 0.05 | 0.52 | 0.31 | 3 | 0.31 | 19 | 0.09 |

| rajat12 | 129 | 110 | 3 | 0.37 | 11 | 0.16 | 2.06 | 1.05 | 0 | 0.18 | 8 | 0.09 |

| rajat13 | 3.85 | 13.6 | 2 | 0.12 | 8 | 0.39 | ||||||

| memplus | 8.81 | 675 | 0 | 0.63 | 16 | 0.18 | 1.73 | 39.0 | 0 | 0.53 | 16 | 3.09 |

| ASIC_100k | 1.54 | 1292 | 0 | 0.27 | 8 | 35.4 | ||||||

| dc1 | 1.19 | 1234 | 2 | 0.29 | 303 | 80.6 | ||||||

| dc2 | 1.20 | 1206 | 2 | 0.51 | 66 | 54.9 | ||||||

| dc3 | 1.22 | 1311 | 6 | 0.33 | 72 | 49.1 | ||||||

| trans4 | 2.30 | 1984 | 0 | 0.23 | 13 | 8.51 | ||||||

| trans5 | 2.14 | 1681 | 0 | 0.22 | 11 | 11.2 | ||||||

We see that all the for all the test problems. This again confirms the reliability of our choices of , and . We observe from the table that S-RSAI() fails to compute for the last six larger problems. This is because each has some fully dense rows so that RSAI() involves solutions of some large LS problems (4) with dimensions at each loop, which exceeds the RAM of our computer. However, with the same parameters, N-RSAI() computes the for all the double regular sparse matrices very efficiently and costs comparable CPU time to N-PSAI() except rajat13. Meanwhile, these are effective for preconditioning and have similar effects to those obtained by N-PSAI(), as shown by the corresponding and . For rajat04, rajat12 and memplus, the constructed by S-RSAI() are much denser than those by N-RSAI(), meaning that S-RSAI() costs much more CPU time than N-RSAI() does, but the by S-RSAI() have comparable preconditioning quality to those by N-RSAI(). For rajat13, we see that S-RSAI() fails to construct within 25 hours. This is because has one dominant index that corresponds to a dense row of at some loop when computing for , causing totally large LS problems to emerge, which is a huge computational task. Actually, we have found that S-RSAI() costs about 81 hours to solve this problem. In contrast, N-RSAI() is very efficient and uses only 13.6 seconds to construct , and Algorithm 2 costs only 14 seconds to solve the problem, a very striking improvement over the standard approach!

Finally, we summarize the six algorithms S-SPAI, S-PSAI(), and S-RSAI() and N-SPAI, N-PSAI(), and N-RSAI(). As can be observed from the numerical experiments, for the standard approach the CPU time of constructing dominates the overall efficiency and it overwhelms the CPU time of solving the preconditioned linear systems by BiCGstab. This is in accordance with the remark paragraph in the end of Section 3. As a matter of fact, the numerical experiments have indicated that, due to the memory storage and huge computational cost, SPAI, PSAI() and RSAI() cannot generate preconditioners when directly applied to six of the ten test irregular sparse problems. By contrast, the transformation approach is very successful and solves all the ten test double irregular sparse problems very efficiently.

6 Conclusions

We have considered SPAI, PSAI() and RSAI() for double irregular sparse linear systems, which are common in practical applications. We have shown that they are costly and even impractical for this class of problems, but much cheaper to construct effective preconditioners for double regular sparse ones. To fully exploit these three preconditioning procedures, by making use of the Sherman-Morrison-Woodbury formula, we have proposed an approach that transforms a double irregular sparse problem into a small number of double irregular sparse ones with the same coefficient matrix , for which we can use the three procedures to efficiently construct good preconditioners for the resulting double regular sparse problems and solve the preconditioned linear systems by Krylov solvers. We have considered the non-singularity and conditioning of . To develop the transformation approach into a practical and reliable algorithm, we have given a number of theoretical and practical considerations.

The numerical experiments have demonstrated that the proposed transformation approach has the very sharp superiority to the standard approach that first preconditions the original double irregular sparse problem (1) by SPAI, PSAI() or RSAI() and then solves the preconditioned linear system by Krylov solvers. The experiments have also illustrated that the transformation approach greatly improves the efficiency of the algorithm proposed in [27] that only transforms a double irregular sparse problem into column regular sparse ones with the same coefficient matrix. We have seen that, due to the memory storage and huge computational cost, SPAI, PSAI() and RSAI() cannot generate preconditioners when directly applied to six of the ten real-world double irregular sparse problems.

References

- [1] S. T. Barnard, O. Bröker, M. J. Grote and M. Hagemann, SPAI 3.2, http://www.computational.unibas.ch/software/spai (2006).

- [2] S. T. Barnard and M. J. Grote, A block version of the SPAI preconditioner, in Proceedings of the 9th SIAM conference on Parallel Processing for Scientific Computing, Hendrickson BA et al. (eds.), SIAM, Philadelphia, PA, 1999.

- [3] M. W. Benson and P. O. Frederickson, Iterative solution of large sparse linear systems in certain multidimensional approximation problems, Util. Math., 22 (1982), pp. 127–140.

- [4] M. W. Benson, J. Krettmann and M. Wright, Parallel algorithms for the solution of certain large sparse linear systems, Int. J. Comput. Math., 16 (1984), pp. 245–260.

- [5] M. Benzi, Preconditioning techniques for large linear systems: a survey, J. Comput. Phys., 182 (2002), pp. 418–477.

- [6] M. Benzi, C. Meyer and M. Tůma, A sparse approximate inverse preconditioner for the conjugate gradient method, SIAM J. Sci. Comput., 17 (1996), pp. 1135–1149.

- [7] M. Benzi, R. Kouhia and M. Tůma, Stabilized and block approximate inverse preconditioners for problems in solid and structural mechanics, Comput. Methods Appl. Mech. Engrg., 190 (2001), pp. 6533–6554.

- [8] M. Benzi and M. Tůma, A sparse approximate inverse preconditioner for nonsymmetric linear systems, SIAM J. Sci. Comput., 19 (1998), pp. 968–994.

- [9] M. Benzi and M. Tůma, A comparative study of sparse approximate inverse preconditioners, Appl. Numer. Math., 30 (1999), pp. 305–340.

- [10] R. Bru, J. Marín, J. Mas and M. Tůma, Balanced incomplete factorization, SIAM J. Sci. Comput., 30 (2008), pp. 2302–2318.

- [11] R. Bru, J. Marín, J. Mas and M. Tůma, Improved balanced incomplete factorization, SIAM J. Matrix Anal. Appl., 31 (2010), pp. 2431–2452.

- [12] K. Chen, Matrix Preconditioning Techniques and Applications, Cambrige Unversity Press, 2005.

- [13] E. Chow, A priori sparsity pattern for parallel sparse approximate inverse preconditoners, SIAM J. Sci. Comput., 21 (2000), pp. 1804–1822.

- [14] T. A. Davis and Y. Hu, The University of Florida sparse matrix collection, ACM Trans. Math. Soft., 38 (2011), pp. 1–25.

- [15] I. S. Duff, On algorithms for obtaining a maximum transversal, ACM Trans. Math. Softw., 7 (1981), pp. 315–330.

- [16] M. Ferronato, Preconditioning for sparse linear systems at the dawn of the 21st century: history, current developments, and future perspectives, ISRN Appl. Math., Vol. 2012, Article ID 127647, 49 pages, doi:10.5402/2012/127647.

- [17] J. R. Gilbert, Predicting structure in sparse matrix computations, SIAM J. Matrix Anal. Appl., 15 (1994), pp. 62–79.

- [18] G. H. Golub and C. F. Van Loan, Matrix Computations, 3rd ed., John Hopkins University Press, Baltimore, MD, 1996.

- [19] M. J. Grote and T. Huckle, Parallel preconditioning with sparse approximate inverses, SIAM J. Sci. Comput., 18 (1997), pp. 838–853.

- [20] T. Huckle, Approximate sparsity pattern for the inverse of a matrix and preconditioning, Appl. Numer. Math., 30 (1999), pp. 291–303.

- [21] C. Janna, N. Castelletto and M. Ferronato, The effect of graph partitioning techniques on parallel block FSAI preconditioning: a computational study, Numer. Algor., 68 (2015), pp. 813–836.

- [22] C. Janna and M. Ferronato, Adaptive pattern research for block FSAI preconditioning, SIAM J. Sci. Comput., 33 (2011), pp. 3357–3380.

- [23] C. Janna, M. Ferronato and G. Gambolati, A block FSAI-IlU parallel preconditioner for symmetric positive definite linear systems, SIAM J. Sci. Comput., 32 (2010), pp. 2468–2484.

- [24] C. Janna, M. Ferronato and G. Gambolati, Enhanced block FSAI preconditioning using domain decomposition techniques, SIAM J. Sci. Comput., 35 (2013), pp. 229–249.

- [25] Z. Jia and W. Kang, A residual based sparse approximate inverse preconditioning procedure for large sparse linear systems, 24 (2) (2017), Article Number: UNSP e2080.

- [26] Z. Jia and Q. Zhang, Robust dropping criteria for F-norm minimization based sparse approximate inverse preconditioning, BIT Numer. Math., 53 (2013), pp. 959–985.

- [27] Z. Jia and Q. Zhang, An approach to making SPAI and PSAI preconditiong effective for large irregular sparse linear systems, SIAM J. Sci. Comput., 35 (2013), pp. A1903–A1927.

- [28] Z. Jia and B. Zhu, A power sparse approximate inverse preconditioning procedure for large sparse linear systems, Numer. Linear Algebra Appl., 16 (2009), pp. 259–299.

- [29] L. Yu. Kolotilian and A. Yu. Yeremin, Factorized sparse approximate inverse preconditionings I. theory, SIAM J. Matrix Anal. Appl., 14 (1993), pp. 45–58.

- [30] Y. Saad, Iterative Methods for Sparse Linear Systems, 2nd ed., SIAM, Philadelphia, PA, 2003.