Central-limit approach to risk-aware Markov decision processes

Abstract

Whereas classical Markov decision processes maximize the expected reward, we consider minimizing the risk. We propose to evaluate the risk associated to a given policy over a long-enough time horizon with the help of a central limit theorem. The proposed approach works whether the transition probabilities are known or not. We also provide a gradient-based policy improvement algorithm that converges to a local optimum of the risk objective.

1 Introduction

Markov Decision Processes (MDPs) are essential models for stochastic sequential decision-making problems (e.g., Puterman, 2014; Bertsekas, 1995; Sutton and Barto, 1998). Classical MDPs are concerned with the expected performance criteria. However, in many practical problems, risk-neutral objectives may not be appropriate (cf. Ruszczyński, 2010, Example 1).

Risk-aware decision-making is prevalent in the financial mathematics and optimization literature (e.g., Artzner et al., 2002; Rockafellar, 2007; Markowitz et al., 2000; Von Neumann and Morgenstern, 2007), but limited to single-stage decisions. Risk-awareness has been adopted in multi-stage or sequential decision problems more recently. A chance-constrained formulation for MDPs with uncertain parameters has been discussed in (Delage and Mannor, 2010). A criteria of maximizing the probability of achieving a pre-determined target performance has been analyzed in (Xu and Mannor, 2011). In (Ruszczyński, 2010), Markov risk measure is introduced and a corresponding risk-averse policy iteration method is developed. A mean-variance optimization problem for MDPs is addressed in (Mannor and Tsitsiklis, 2013). A generalization of percentile optimization with objectives defined by a measure over percentiles instead of a single percentile is introduced in (Chen and Bowling, 2012). In terms of computational convenience, actor-critic algorithms for optimizing variance-related risk measures in both discounted and average reward MDPs have been proposed in (Prashanth and Ghavamzadeh, 2013). Mean and conditional value-at-risk optimization problem in MDPs is solved by policy gradient and actor-critic algorithms in (Chow and Ghavamzadeh, 2014). A unified policy gradient approach is proposed in (Tamar et al., 2015) to seek optimal strategy in MDPs with the whole class of coherent risk measures. Risk-aversion in multiarmed bandit problems is studied in (Yu and Nikolova, 2013), where algorithms are proposed with PAC guarantees for best arm identification. Robust MDPs (e.g., Nilim and El Ghaoui, 2005; Iyengar, 2005) mitigate the sensitivity of optimal policy to ambiguity in the underlying transition probabilities, and are closely related to the risk-sensitive MDPs. Such relations are uncovered by Osogami (2012).

In this work, we study the value-at-risk in finite-horizon MDPs. Computing this risk associated with a sequence of decision using the defintion and first principles is intractable. However, we show that this computation is made tractable by using a central limit theorem for Markov chains (Jones et al., 2004; Kontoyiannis and Meyn, 2003; Glynn and Meyn, 1996). For a long-enough horizon and a fixed policy , we are thus able to evaluate the risk associated with following policy over time steps. Specifically, our first contributions are policy evaluation algorithms whether the transition probability matrix induced by is known or not. Under mild conditions, we provide high-probability error bounds for the evaluation.

For a fixed risk measure , and a space of policies that is parametrized by , our second contribution is a policy improvement algorithm that converges in finite iterations, under certain assumptions, to a locally optimal policy. This approach updates the parameter in the direction of gradient of the risk measure. Compared to the previous work, our proposed method does not explicitly approximate the value function. Therefore, it does not have approximation error due to the selection of value function approximator.

Even though we deal mainly with the static value-at-risk risk measure (defined by the cumulative reward), our results can be easily extended to deal with the conditional- or average-value-at-risk by using its definition Schied (2004).

1.1 Distinction from related works

It is important to note that our risk measure is very different from the dynamic risk measure analyzed in (Ruszczyński, 2010), which has the following recursive structure: for -length horizon MDP and policy , the dynamic risk measure is defined as

where is a state dependent reward function, is a constant and is a Markov risk measure, i.e., the evaluation of each static coherent risk measure is not allowed to depend on the whole past. In contrast, our risk measure emphasizes the statistical properties of the reward accumulated over multiple time steps: it is similar to that used in (Yu and Nikolova, 2013) in the context of bandit problems.

From the computational and algorithmic perspective, we evaluate the policy and obtain the risk value directly. Different from the work (Prashanth and Ghavamzadeh, 2013; Chow and Ghavamzadeh, 2014; Tamar et al., 2015), which indirectly evaluated the risk value by using function approximation, our proposed method has an explicit policy evaluation step and does not require value function approximation. Therefore, it does not have approximation error due to the selection of value function approximator and the richness of the features. Moreover, for risk-aware MDPs that are known to be NP-hard (e.g., Delage and Mannor, 2010; Xu and Mannor, 2011), our method can find approximated solutions to those problems.

From the conceptual perspective, our work is the first attempt to consider general risk measures with a central-limit approach. Compared with (Tamar et al., 2015), our approach is not limited to so-called “coherent” risk measures (both static and dynamic), whose defining properties are not satisfied by the value-at-risk. The methods proposed in (Tamar et al., 2015) thus cannot be applied. Moreover, the time horizon in our setup is allowed to be infinite. Other previous work (Delage and Mannor, 2010; Xu and Mannor, 2011; Mannor and Tsitsiklis, 2013) restrict themselves to specific risk criteria: Delage and Mannor (2010) considered a set of percentile criteria; Xu and Mannor (2011) seek to find the policy that maximizes the probability of achieving a pre-determined target performance, and Mannor and Tsitsiklis (2013) discussed a mean-variance optimization problem.

This paper is organized as follows: In Section 2 we provide background and problem statement. For a fixed policy, we then evaluate its risk value in Section 3. In specific, we discuss the policy evaluation algorithms in Section 3.1 and 3.2 when the transition kernel is either known or unknown. The main result is Theorem 2, which bounds the error of true and estimated asymptotic variances. In Section 4, we provide policy gradient algorithm to improve the fixed policy. A conclusion is offered in Section 5.

2 Problem formulation

MDP is a tuple , where is a finite set of states, is a finite set of actions, is the transition kernel, is the (possibly infinite) moderate time horizon, and is the bounded and measurable reward function. A function is called lattice if there are and , such that is an integer for . The minimal for such condition holds is called the span of . If the function can be written as a sum , where is lattice with span and has zero asymptotic variance (which will be defined later), then is called almost-lattice. Otherwise, is called strongly nonlattice. We assume the functional is strongly nonlattice. A policy is the rule according to which actions are selected at each state. We parameterize the stochastic policies by , and denote the set of policies by . Since in this setting a policy is represented by its -dimensional parameter vector , policy dependent functions can be written as a function of in place of . So, we use and interchangeably in the paper.

Given a policy , a Markov reward process is induced by . We write the transition kernel of the induced Markov process and dependent rewards as and for all , respectively. We denote as the -step Markov transition kernel corresponding to . We are interested in the long-term behavior of the sum

If the Markov chain is positive recurrent with invariant probability measure , we define the mean of reward function as

| (1) |

where is the initial condition and is the expectation over the Markov process . Equivalently, the mean can be expressed as

| (2) |

Often we can quantify the rate of convergence of (1) by showing that the limit

exists where, in fact, the function solves the Poisson equation

| (3) |

Here operates on functions via , is the vector form of and is the vector with all elements being .

Let denote the set of bounded random variables, and let denote a risk measure. Our risk-aware objective is

| (4) |

We discuss specific types of risk measures in the coming sections. All proofs are deferred in the supplementary material due to space constraints.

3 Policy evaluation

In this section, we develop methods to evaluate the risk value for a fixed policy . In specific, we consider the Markov chain induced by policy , which is assumed to be geometrically ergodic. We then apply limit theorems for geometrically ergodic Markov chain in (Kontoyiannis and Meyn, 2003) to obtain the distribution function of cumulative reward when transition kernel is either known or unknown. Finally, we provide algorithms for computing some examples of risk measures.

Similar to Kontoyiannis and Meyn (2003), we make the following two standard assumptions for the Markov process .

Assumption 1.

The Markov process is geometrically ergodic with Lyapunov function (i.e., irreducible, aperiodic and satisfying Condition (V4) of Kontoyiannis and Meyn (2003)) where satisfies .

The detailed definition of geometric ergodicity can be found in (Kontoyiannis and Meyn, 2003, Section 2).

Assumption 2.

The (measurable) reward function has nontrivial asymptotic variance .

Theorem 1 (Theorem 5.1, Kontoyiannis and Meyn (2003)).

Suppose that and the strongly nonlattice functional satisfy Assumption 1 and 2, and let denote the distribution function of the normalized partial sums :

Then, for all and as ,

uniformly in , where denotes the standard normal density and is the corresponding distribution function. Here is a constant related to the third moment of . The definitions of and term can be found in the supplementary material.

Unlike (Heyman and Sobel, 2003), which considered finite Markov chains and obtained the moments of the cumulative reward, we further impose geometric ergodicity assumption on the Markov process . By doing this, we are able to utilize the explicit form of distribution function given by (Kontoyiannis and Meyn, 2003, Theorem 5.1) with the time error term . In addition, the geometric ergodicity property enables us to bound the approximation error in Theorem 2.

Similar to Glynn and Meyn (1996), we define the fundamental kernel associated with fixed as

where the kernel is defined as , and . If the inverse of is well defined, Glynn and Meyn (1996) stated that the solution to Poisson equation (3) has the form

| (5) |

When and , Meyn and Tweedie (2012, Equation 17.44) showed that the asymptotic variance can be obtained by

| (6) |

We remark that the asymptotic variance can also be calculated without the knowledge of by Theorem 17.5.3 of Meyn and Tweedie (2012):

where and denotes the -step transition probability to state conditioned on the initial state . It is clear that solving (6) requires the knowledge of transition kernel . In the following subsections, we study the policy evaluation with and without knowing , respectively.

3.1 Transition probability kernel is known

In this subsection, we propose an algorithm to obtain the distribution function in Theorem 1, using which we can evaluate the risk value.

Since transition kernel is known, we first calculate the stationary distribution . Note that the stationary distribution satisfies

Thus, the stationary distribution is the eigenvector of matrix with eigenvalue (recall that is always an eigenvalues for matrix ), which is unique up to constant multiples under Assumption 1.

After we compute the stationary distribution , it is straightforward to calculate the mean (2), solve Poisson equation (3) and get the asymptotic variance (6). Therefore, we are able to obtain the distribution function defined in Theorem 1 at this stage. Finally, the risk measures that can be expressed as a function of can be evaluated. We provide two examples below.

Example 3.1 (-step value-at-risk).

Let be given and fixed. The -step value-at-risk is defined by

where is the right-continuous quantile function111Formally, , where is the distribution function of . of .

When is moderate, vanishes, the distribution function defined in Theorem 1 has the form

| (7) |

This allows us to compute the -step value-at-risk. The procedure is summarized in Algorithm 1. The next example considers the mean-variance risk measure.

Example 3.2 (Mean-variance risk).

Given , the mean-variance risk measure is given by

where is the mean of , and is the variance of .

The corollary below gives formula to obtain the mean-variance risk. An algorithm can be obtained similarly for the mean-variance risk simply by replacing line in Algorithm 1 by the corresponding risk measure. The same procedure can easily be generalized to other risk measures.

Corollary 1.

3.2 Transition probability kernel needs to be estimated

In practice, knowing transition kernel is generally hard. In this subsection, we present a policy evaluation algorithm when transition kernel needs to be estimated, and provide the corresponding approximation error.

Intuitively, if the estimated transition kernel is accurate enough, the gap between solutions to estimated and true Poisson equations is small (as shown in Lemma 5), which implies the difference between estimated and true asymptotic variances is also small (as shown in Theorem 2).

A way of estimating transition kernel is to use the empirical distribution. Denoting the required number of samples by and the estimated transition kernel by , we make the following assumption.

Assumption 3.

There exist and such that and as . Moreover, we have the following bound for the error222We use and to show the dependence of the error on .:

Here the supreme norm of a matrix is defined as the maximum absolute row sum of the matrix:

We remark Assumption 3 can be easily satisfied if a large collection of observed data is provided. This could be achievable if one is allowed to simulate the system arbitrarily many times.

Next, we perturb the true transition kernel , define the resulting perturbed transition kernel as and denote the stationary distribution associated with as . Given , we let be an estimator of . Under Assumption 1, we make the following assumption which establishes the convergence of , where is the total variation norm defined as following: If is a signed measure on , then the total variation norm is defined as

Assumption 4.

Given and perturbed transition kernel . If then for every , the geometrically ergodic Markov chain has a form of convergence

where , and is a nonnegative function.

This assumption essentially guarantees the geometric ergodicity property remains if the original Markov chain is slightly perturbed.

Assumption 3 and 4 immediately imply that

| (8) |

where is the stationary distribution associated with . Let be the ergodicity coefficient of transition kernel (Seneta, 1988), which is defined by

| (9) |

If the ergodicity coefficient satisfies , Cho and Meyer (2001, Equation 3.4) shows

Therefore, under Assumption 3, we have

| (10) |

The ergodicity coefficient for the estimated transition kernel is defined in a same manner.

Matrix plays an important role in defining solution to Poisson equation. We impose a requirement on the smallest singular value of .

Assumption 5.

There exists a constant such that the smallest singular value of matrix satisfies . Here333The parameter is dependent on the initial state through nonnegative function . In the following, we omit for convenience and emphasize when such dependence is required to show.

| (11) |

Similar to (3), we define the estimated Poisson equation as

| (12) |

where is the estimated mean

| (13) |

with being the estimation of stationary distribution

| (14) |

We then define the perturbed fundamental kernel as

where with . The following lemma shows is well defined under Assumption 5.

Lemma 1.

Under Assumption 5, is well defined.

The solution to estimated Poisson equation (12) can be expressed as

| (15) |

We define the asymptotic variance associated with as , which can be obtained by the equation below:

| (16) |

The theorem below provides the condition for such that the difference between estimated and true asymptotic variances and defined in (6) and (16) is small. We provide an outline of the proof below and a complete version can be found in the supplementary material.

Theorem 2.

Proof.

By equations (6) and (16), we have

where

Equality holds due to subtracting and then adding a same term . Inequality holds by triangle inequality. In order to bound the terms and , we need following lemmas.

First, we derive a bound for by the lemma below.

Lemma 2.

Under Assumption 3, the ergodicity coefficient for the estimated transition kernel satisfies

Denoting as the Euclidean norm of vector , we present a lemma showing that the solution (5) of Poisson equation (3) is bounded.

Analogously to Lemma 3, we have the following result.

Lemma 4.

The lemma below shows that solutions to the true and estimated Poisson equations are close to each other with high probability.

Lemma 5.

Recall that for two random variables and , and with , by union bound and monotonicity property of probability, we have

Finally, by bounding terms and , we prove the theorem. ∎

Now we are able to compute the -step value-at-risk, which is summarized as a procedure in the Algorithm 2. Note that given the asymptotic variance and solution to estimated Poisson equation , when is moderate, vanishes, defined in Theorem 1 becomes

| (17) |

where is defined in a same manner as by replacing and by and , respectively.

In the following, we analysis the mean-variance risk defined in Example 3.2. Corollary 2 gives formula to obtain the mean-variance risk and provides high-probability bound for the risk measure. An algorithm can be developed for the mean-variance risk simply by replacing line in Algorithm 2 by the corresponding risk measure.

Corollary 2.

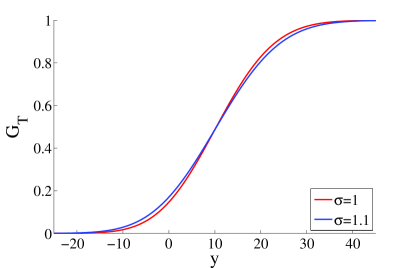

A similar argument can be developed for -step value-at-risk defined in Example 3.1. When , , , , we plot the distribution functions for and below.

Figure 1 shows the distribution functions are close, which implies the corresponding -step value-at-risks are also close to each other (When , the -step value-at-risks are and , respectively).

4 Policy Improvement

In this section, we propose policy gradient methods to improve policy and solve the optimization problem (4). Specifically, we compute the gradient of the performance (i.e., the risk) w.r.t. the policy parameters from the evaluated policies, and improve by adjusting its parameters in the direction of the gradient.

In the following, we make a standard assumption in gradient-based MDPs literature (e.g., Sutton et al., 1999; Konda and Tsitsiklis, 1999; Bhatnagar et al., 2009; Prashanth and Ghavamzadeh, 2013).

Assumption 6.

For any state-action pair , is continuously differentiable in the parameter .

In a recent work, Prashanth and Ghavamzadeh (2013, Section 4) presented actor-critic algorithms for optimizing the risk-sensitive measure that are based on two simultaneous perturbation methods: simultaneous perturbation stochastic approximation (SPSA) (Spall, 1992) and smoothed functional (SF) (Bhatnagar et al., 2012). We use similar arguments here and further apply those methods to estimate the gradient of the risk measure with respect to the policy parameter , i.e., .

The idea in these methods is to estimate the gradient using two simulated trajectories of the system corresponding to policies with parameters and . Here is a positive constant and is a perturbation random variable, i.e., a -vector of independent Rademacher (for SPSA) and Gaussian (for SF) random variables.

SPSA-based estimate for is given by

| (18) |

where is a vector of independent Rademacher random variables and is its -th entry. The advantage of this estimator is that it perturbs all directions at the same time (the numerator is identical in all components). So, the number of function measurements needed for this estimator is always two, independent of the dimension .

SF-based estimate for is given by

| (19) |

where is a vector of independent Gaussian random variables.

The step size of the gradient descent satisfies the following condition.

Assumption 7.

The step size schedule satisfies

At each time step , we update the policy parameter as follows: for ,

| (20) |

Note that ’s are independent Rademacher and Gaussian random variables in SPSA and SF updates, respectively. is an operator that projects a vector to the closest point in a compact and convex set . The projection operator is necessary to ensure the convergence of the algorithms. Specifically, we consider the differential equation

| (21) |

where is defined as follows: for any bounded continuous function ,

The projection operator ensures that the evolution of via the differential equation (21) stays within the bounded set . Let denote the set of asymptotically stable equilibrium points of the differential equation (21) and denote the set of points in the -neighborhood of .

The following is our main result, which bounds the error of our policy improvement algorithm.

Theorem 3.

The above theorem guarantees the convergence of the SPSA and SF updates to a local optimum of the risk objective function . Finally, we provide the policy improvement method in Algorithm 3.

5 Conclusion

In the context of risk-aware Markov decision processes, we use a central limit theorem efficiently evaluate the risk associated to a given policy. We also provide a policy improvement algorithm, which works on a parametrized policy-space in a gradient-descent way. Under mild conditions, it is guaranteed that the policy evaluation is approximately correct and that the policy improvement converges to a local optimum of the risk measure. We believe that many important problems that are usually addressed using standard MDP models should be revisited using our proposed approach to risk management (e.g., machine replacement, inventory management, portfolio optimization, etc.).

Appendix A Appendix

A.1 Defintion of in Theorem 1

where

and

Here denotes the -step transition probability to state conditioned on the initial state .

A.2 Definition of in Theorem 1

Kontoyiannis and Meyn (2003) showed that the term can be represented as

where

with , and . The characteristic function is defined as

is chosen large enough so that for all , and arbitrary . Here,

A.3 Proof of Lemma 1

Proof.

Let and

and be the spectral norm of matrix , which is the largest singular value of matrix :

Due to Assumption 3, (8) and (10), we have

Define , we have

| (22) |

where444The parameter is dependent on the initial state through nonnegative function . In the following, we omit for convenience and emphasize when such dependence is required to show. Same argument goes for .

We perform the singular value decomposition for the matrix and have

where and are unitary matrix with dimension , and is a diagonal matrix with non-negative real numbers on the diagonal. Next, by the definition of and , we obtain

where . In addition, we have

Since , under Assumption 5, we obtain

| (23) |

Since , is well defined, which implies is well defined.

∎

A.4 Proof of Lemma 2

Proof.

From the definition of and , we have

Here recall that if are bounded functions, then . For and , since and , thus inequality holds. Inequality holds due to reverse triangle property, while Hölder’s inequality is applied to .

A.5 Proof of Lemma 3

Proof.

Recall the solution can be bounded above by

Here is due to and Assumption 5. Since for ,

we have which implies . It is straightforward to show is also bounded.

∎

A.6 Proof of Lemma 4

Proof.

Recall the solution to estimated Poisson equation can be expressed as

First, note that From (22) in the proof of Lemma 1, we have

By Weyl’s inequality, we have

which implies

Moreover, for ,

we have Thus . Therefore, we obtain

By Lemma 2, we have

| (24) |

Applying (24), we have

It is straightforward to show is bounded because

Thus, we have

∎

A.7 Proof of Lemma 5

A.8 Proof of Theorem 2

Proof.

Recall that the element of vector is denoted by . Define the vectors and with their elements being and , respectively. Similarly for the vectors and . Lemma 3 implies

and from Lemma 4 we get

| (25) | ||||

First, by equations (6) and (16), we have

where

Equality holds due to subtracting and then adding a same term . Inequality holds by triangle inequality. In the following, we bound the terms and individually. Term can be further expressed as

Inequalities and hold due to triangle property, while is true because of Hölder’s inequality. From (8) and (10), we have

| (26) |

where . In addition, under Lemma 2 we obtain

where . Combining (25) and (26), by the union bound of probability and definition of , we have

Next, we bound the term .

Inequality holds due to triangle property, and is due to Hölder’s inequality, while is true since . Note that

Furthermore, from Lemma 3, 4 and 5, we have

| (27) |

where

In addition, we have

where

Inequalities and are due to triangle property, and is because of Hölder’s inequality.

Since , Assumption 3 implies

Since , from Lemma 4 and 5, we have

where

Moreover, from Lemma 3 and 4, we obtain

where . Note is dependent on the initial state and denote

we conclude

| (28) |

At last, by the union bound of probability, (27) and (28) yield

where

Recall that for two random variables and , and with , by union bound and monotonicity property of probability, we have

Therefore, if for

and for

We can conclude that

which further implies

by the monotonicity property and union bound of probability. ∎

A.9 Proof of Corollary 2

Proof.

From the definitions of and , we get

Here inequalities and are due to triangle property. Inequality is because Hölder’s inequality and . Moreover, since is the -perturbed transition kernel under Assumption 4, by (8) and (14), we have

| (29) |

In addition, from (10) and Lemma 2, we get

| (30) |

Applying the union bound of probability to (29), (30) and Theorem 2, we have

where . ∎

A.10 Proof of Theorem 3

Proof.

Note that, for fixed , we are able to evaluate the policy . Moreover, (20) can be considered as a discretization of the differential equation (21).

For SPSA update, is an asymptotically stable attractor for the differential equation (21), with itself serving as a strict Lyapunov function. This can be inferred as follows

The claim for SPSA update now follows from (Kushner and Clark, 2012, Theorem 5.3.1).

The convergence analysis for SF update follows in a similar manner as SPSA update. ∎

References

- Artzner et al. (2002) Philippe Artzner, Freddy Delbaen, Jean-Marc Eber, and David Heath. Coherent measures of risk. Risk management: value at risk and beyond, page 145, 2002.

- Bertsekas (1995) Dimitri P Bertsekas. Dynamic programming and optimal control, volume 1. Athena Scientific Belmont, MA, 1995.

- Bhatnagar et al. (2009) Shalabh Bhatnagar, Richard S Sutton, Mohammad Ghavamzadeh, and Mark Lee. Natural actor–critic algorithms. Automatica, 45(11):2471–2482, 2009.

- Bhatnagar et al. (2012) Shalabh Bhatnagar, HL Prasad, and LA Prashanth. Stochastic recursive algorithms for optimization: simultaneous perturbation methods, volume 434. Springer, 2012.

- Chen and Bowling (2012) Katherine Chen and Michael Bowling. Tractable objectives for robust policy optimization. In Advances in Neural Information Processing Systems, pages 2069–2077, 2012.

- Cho and Meyer (2001) Grace E Cho and Carl D Meyer. Comparison of perturbation bounds for the stationary distribution of a Markov chain. Linear Algebra and its Applications, 335(1):137–150, 2001.

- Chow and Ghavamzadeh (2014) Yinlam Chow and Mohammad Ghavamzadeh. Algorithms for CVaR optimization in MDPs. In Advances in Neural Information Processing Systems, pages 3509–3517, 2014.

- Delage and Mannor (2010) Erick Delage and Shie Mannor. Percentile optimization for Markov decision processes with parameter uncertainty. Operations research, 58(1):203–213, 2010.

- Glynn and Meyn (1996) Peter W Glynn and Sean P Meyn. A Liapounov bound for solutions of the Poisson equation. The Annals of Probability, pages 916–931, 1996.

- Heyman and Sobel (2003) Daniel P Heyman and Matthew J Sobel. Stochastic Models in Operations Research: Stochastic Optimization, volume 2. Courier Corporation, 2003.

- Iyengar (2005) Garud N Iyengar. Robust dynamic programming. Mathematics of Operations Research, 30(2):257–280, 2005.

- Jones et al. (2004) Galin L Jones et al. On the Markov chain central limit theorem. Probability surveys, 1(299-320):5–1, 2004.

- Konda and Tsitsiklis (1999) Vijay R Konda and John N Tsitsiklis. Actor-critic algorithms. In Advances in Neural Information Processing Systems, volume 13, pages 1008–1014, 1999.

- Kontoyiannis and Meyn (2003) Ioannis Kontoyiannis and Sean P Meyn. Spectral theory and limit theorems for geometrically ergodic Markov processes. Annals of Applied Probability, pages 304–362, 2003.

- Kushner and Clark (2012) Harold Joseph Kushner and Dean S Clark. Stochastic approximation methods for constrained and unconstrained systems, volume 26. Springer Science & Business Media, 2012.

- Mannor and Tsitsiklis (2013) Shie Mannor and John N Tsitsiklis. Algorithmic aspects of mean–variance optimization in Markov decision processes. European Journal of Operational Research, 231(3):645–653, 2013.

- Markowitz et al. (2000) Harry M Markowitz, G Peter Todd, and William F Sharpe. Mean-variance analysis in portfolio choice and capital markets, volume 66. John Wiley & Sons, 2000.

- Meyn and Tweedie (2012) Sean P Meyn and Richard L Tweedie. Markov chains and stochastic stability. Springer Science & Business Media, 2012.

- Nilim and El Ghaoui (2005) Arnab Nilim and Laurent El Ghaoui. Robust control of Markov decision processes with uncertain transition matrices. Operations Research, 53(5):780–798, 2005.

- Osogami (2012) Takayuki Osogami. Robustness and risk-sensitivity in Markov decision processes. In Advances in Neural Information Processing Systems, pages 233–241, 2012.

- Prashanth and Ghavamzadeh (2013) LA Prashanth and Mohammad Ghavamzadeh. Actor-critic algorithms for risk-sensitive MDPs. In Advances in Neural Information Processing Systems, pages 252–260, 2013.

- Puterman (2014) Martin L Puterman. Markov decision processes: discrete stochastic dynamic programming. John Wiley & Sons, 2014.

- Rockafellar (2007) R Tyrrell Rockafellar. Coherent approaches to risk in optimization under uncertainty. Tutorials in operations research, 3:38–61, 2007.

- Ruszczyński (2010) Andrzej Ruszczyński. Risk-averse dynamic programming for Markov decision processes. Mathematical programming, 125(2):235–261, 2010.

- Schied (2004) A. Schied. Risk measures and robust optimization problems, 2004. Lecture notes.

- Seneta (1988) E Seneta. Perturbation of the stationary distribution measured by ergodicity coefficients. Advances in Applied Probability, pages 228–230, 1988.

- Spall (1992) James C Spall. Multivariate stochastic approximation using a simultaneous perturbation gradient approximation. Automatic Control, IEEE Transactions on, 37(3):332–341, 1992.

- Sutton and Barto (1998) Richard S Sutton and Andrew G Barto. Reinforcement learning: An introduction, volume 1. MIT press Cambridge, 1998.

- Sutton et al. (1999) Richard S Sutton, David A McAllester, Satinder P Singh, Yishay Mansour, et al. Policy gradient methods for reinforcement learning with function approximation. In Advances in Neural Information Processing Systems, volume 99, pages 1057–1063. Citeseer, 1999.

- Tamar et al. (2015) Aviv Tamar, Yinlam Chow, Mohammad Ghavamzadeh, and Shie Mannor. Policy gradient for coherent risk measures. arXiv preprint arXiv:1502.03919, 2015.

- Von Neumann and Morgenstern (2007) John Von Neumann and Oskar Morgenstern. Theory of games and economic behavior. Princeton university press, 2007.

- Xu and Mannor (2011) Huan Xu and Shie Mannor. Probabilistic goal Markov decision processes. In Proceedings of the Twenty-Second international joint conference on Artificial Intelligence-Volume Volume Three, pages 2046–2052. AAAI Press, 2011.

- Yu and Nikolova (2013) Jia Yuan Yu and Evdokia Nikolova. Sample complexity of risk-averse bandit-arm selection. In Proceedings of the Twenty-Third international joint conference on Artificial Intelligence, pages 2576–2582. AAAI Press, 2013.