Multiple–Instance Learning: Radon–Nikodym Approach to Distribution Regression Problem.

Abstract

$Id: DistReg1Step.tex,v 1.41 2015/12/02 11:00:50 mal Exp $

For distribution regression problem, where a bag of –observations is mapped to a single value, a one–step solution is proposed. The problem of random distribution to random value is transformed to random vector to random value by taking distribution moments of observations in a bag as random vector. Then Radon–Nikodym or least squares theory can be applied, what give estimator. The probability distribution of is also obtained, what requires solving generalized eigenvalues problem, matrix spectrum (not depending on ) give possible outcomes and depending on probabilities of outcomes can be obtained by projecting the distribution with fixed value (delta–function) to corresponding eigenvector. A library providing numerically stable polynomial basis for these calculations is available, what make the proposed approach practical.

Dedicated to Ira Kudryashova

I Introduction

Multiple instance learningDietterich et al. (1997) is an important Machine Learning (ML) concept having numerous applicationsYang (2005). In multiple instance learning class label is associated not with a single observation, but with a “bag” of observations. A very close problem is distribution regression problem, where a sample distribution of is mapped to a single value. There are numerous heuristics methods developed from both: ML and distribution regression sides, see Zhou (2004); Szabó et al. (2014) for review.

As in any ML problem the most important part is not so much the learning algorithm, but the way how the learned knowledge is represented. Learned knowledge is often represented as a set of propositional rules, regression function, Neural Network weights, etc. In this paper we consider the case where knowledge is represented as a function of distribution moments. Recent progress in numerical stability of high order moments calculationMalyshkin and Bakhramov (2015) allow the moments of very high order to be calculated, e.g. in Ref. Malyshkin (2015a) up to hundreds, thus make this approach practical.

Most of distribution regression algorithms deploy a two–step type of algorithmSzabó et al. (2014) to solve the problem. In our previous work Malyshkin (2015b) a two–step solution with knowledge representation in a form of Christoffel function was developed. However, there is exist a one–step solution to distribution regression problem, a random distribution to random value, that converts each bag’s observations to moments of it, then solving the problem random vector (the moments of random distribution) to random value. Once this transition is made an answer of least squares or Radon–Nikodym type from Ref. Malyshkin and Bakhramov (2015) can be applied and close form result obtained. The distribution of outcomes, if required, can be obtained by solving generalized eigenvalues problem, then matrix spectrum give possible outcomes, and the square of projection of localized at given bag distribution to eigenvector give each outcome probability. This matrix spectrum ideology is similar to the one we used in Malyshkin (2015b), but is more generic and not reducible to Gauss quadrature.

The paper is organized as following: In Section II a general theory of distribution regression is discussed and close form result or least squares and Radon–Nikodym type are presented. Then in Section III an algorithm is described and numerical example of calculations is presented. In Section IV possible further development is discussed.

II One–Step Solution

Consider distribution regression problem where a bag of observations of is mapped to a single outcome observation for .

| (1) |

A distribution regression problem can have a goal to estimate , average of , distribution of , etc. given specific value of

For further development we need basis and some and measure. For simplicity, not reducing the generality of the approach, we are going to assume that measure is a sum over index , measure is a , the basis functions are polynomials , where is the number of elements in basis, typical value for is below 10–15.

Let us convert the problem “random distribution” to “random variable” to the problem “vector of random variables” to “random variable”. The simplest way to obtain “vector of random variables” from distributions is to take the moments of it. Now the would be this random vector:

| (2) | |||

| (3) |

Then the (3) becomes vector to value problem. Introduce

| (4) | |||||

| (5) | |||||

| (6) |

The problem now is to estimate (or distribution of ) given distribution, now mapped to a vector of moments calculated on this distribution. Let us denote these input moments as to avoid confusion with measures on and . For the case we study the value is given, and for a state with exact the values are:

| (7) |

what means that all observations in a bag give exactly the same value. The problem now becomes a standard: random vector to random variable. We have solutions of two types for this problem, see Malyshkin and Bakhramov (2015) Appendix D, Least Squares and Radon–Nikodym . The answers would be:

| (8) | |||||

| (9) |

The (8) is least squares answer to estimation given . The (9) is Radon–Nikodym answer to estimation given . These are the two estimators at given for distribution regression problem 1. These answers can be considered as an extension of least squares and Radon–Nikodym type of interpolation from value to value problem to random distribution to random variable problem. In case the and are reduced exactly to value to value problem considered in Ref. Malyshkin and Bakhramov (2015). Note, that the answer not necessary preserve sign, but always preserve sign, same as in value to value problem.

If distribution at given need to be estimated this problem can also be solved. With one–step approach of this paper we do not need basis used in two–step approach of Ref. Malyshkin (2015b) and outcomes of are estimated from moments only. Generalized eigenvalues problemMalyshkin and Bakhramov (2015) give the answer:

| (10) |

The result of (10) is eigenvalues (possible outcomes) and eigenvectors (can be used to compute the probabilities of outcomes). The problem now becomes: given value estimate possible –outcomes and their probabilities. The moments of states with given value are from (7), so the distribution with (7) moments should be projected to distributions corresponding to states, the square of this projection give the weight and normalized weight give the probability. This is actually very similar to ideology we used in Malyshkin (2015b), but the eigenvalues from (10) no longer have a meaning of Gauss quadrature nodes. The eigenvectors correspond to distribution with moments , and the distribution with such moments correspond to value. These distributions can be considered as “natural distribution basis”. This is an important generalizatioh of Refs. Malyshkin and Bakhramov (2015); Malyshkin (2015a) approach to random distribution, where natural basis for random value, not random distribution, was considered.

The projection of two distributions with moments and on each other is

| (11) |

then the required probabilities, calculated by projecting the (7) distribution to natural basis states, are:

| (12) | |||||

| (13) |

The (10) and (13) is one–step answer to distribution regression problem: find the outcomes and their probabilities . Note, that in this setup possible outcomes do not depend on , and only probabilities of outcomes depend on . This is different from a two–step solution of Malyshkin (2015b) where outcomes and their probabilities both depend on . Also note that .

One of the major difference between the probabilities (13) and probabilities from Christoffel function approach Malyshkin (2015b) is that the (13) has a meaning of “true” probability while in two–step solution Malyshkin (2015b) Christoffel function value is used as a proxy to probability on first step. It is important to note how the knowledge is represented in these models. The model (8) has learned knowledge represented in by matrix (5) and size vector (4). The model (9) as well as distribution answer (13) has learned knowledge represented in two by matrices (5) and (6).

III Numerical estimation of One–Step Solution

Numerical instability similar to the one of two–stage Christoffel function approach Malyshkin (2015b) also arise for approach in study, but now the situation is much less problematic, because we do not have –basis , and all the dependence on enter the answer through matrix (6). In this case the only stable basis is required.

The algorithm for estimators of (8) or (9) is this: Calculate moments from (2, then calculate matrices (5) and (6), if least squares approximation is required also calculate moments (4). In contrast with Christoffel function approach where matrix can be obtained from moments by application of polynomials multiplication operator, here the (5) and (6) can be hardly obtained this way for and should be calculated directly from sample. This is not a big issue, because is typically not large. Then inverse matrix from (5), this matrix is some kind similar to Gramm matrix, but uses distribution moments, not basis functions. Finally put all these to (8) for least squares estimation or to (9) for Radon–Nikodym estimation.

If – distribution is required then solve generalized eigenvalues problem (10), obtain as possible –outcomes (they do not depend on ), and calculate –dependent probabilities (13), these are squared projection coefficient of a state with specific value, point–distribution (7), or some other distribution of general form, to eigenvector.

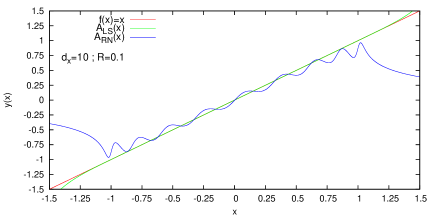

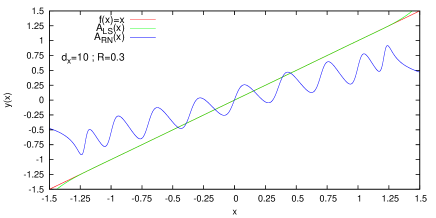

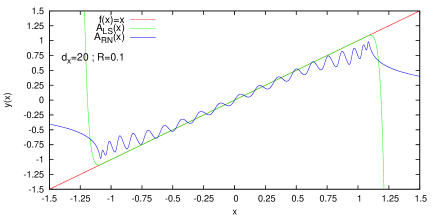

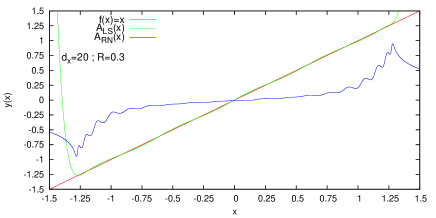

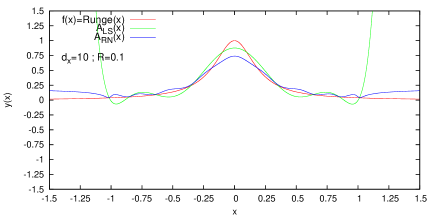

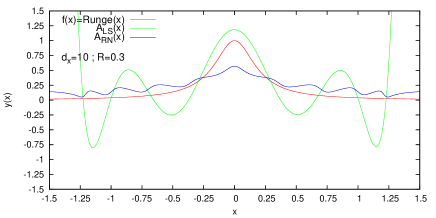

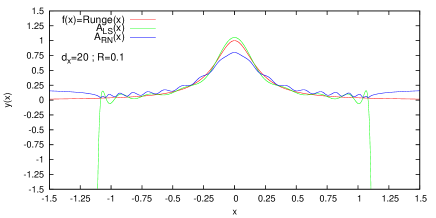

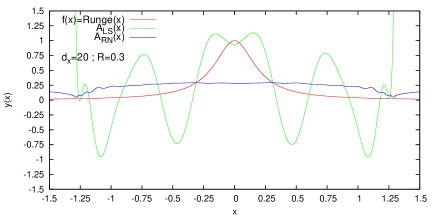

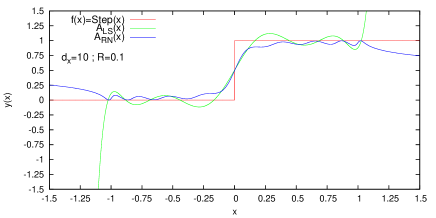

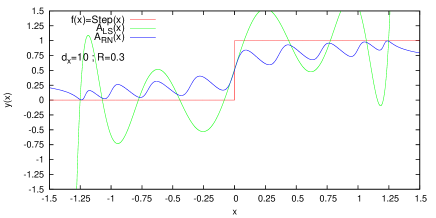

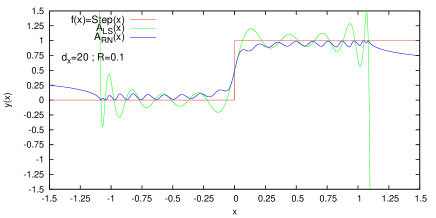

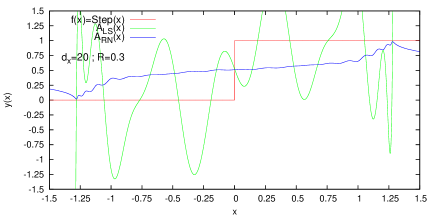

To show an application of this approach let us take several simple distribution to apply the theory. Let be a uniformly distributed random variable and take and . Then consider sample distributions build as following 1) For take random out of interval. 2) Calculate , take this as . 3) Build a bag of observations as , where is a parameter. The following three functions for building sample distribution are used:

| (14) | |||||

| (15) | |||||

| (18) |

In Figs. 1, 2, 3, the (8) and (9) answers are presented for from (14), (15) and (18) respectively for and . The range is specially taken slightly wider that interval to see possible divergence outside of measure support. In most cases Radon–Nikodym answer is superior, and in addition to that it preserves the sign of . Least squares approximation is good for special case and typically diverges at outside of measure support.

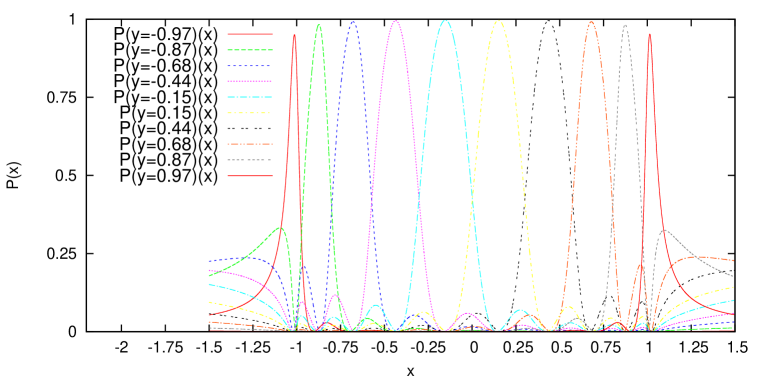

The numerical estimation of probability function (the and ) were also calculated and eigenvalue index , corresponding to maximal typically correspond to , for which is most close. For simplistic case (14) see Fig. 4. See the Ref. Malyshkin (2014), file com/polytechnik/ algorithms/ ExampleDistribution1Stage.scala for algorithm implementation.

IV Discussion

In this work a one–stage approach is applied to distribution regression problem. The bag’s observations are initially converted to moments, then least squares or Radon–Nikodym theory can be applied and closed form answer to be received. These (8) and (9) estimate value given . This answer can be generalized to “what is estimate given distribution of ”. For this problem obtain moments , corresponding to given distribution of , first, then use them in (8) or (9) instead of , corresponding to localized at state. Similary, if probabilities of outcomes are required for given distribution of , the should be used in weights expression (12) instead of (this is a special case of two distribution projection on each other (11)). Computer code implementing the algorithms is availableMalyshkin (2014).

And in conclusion we want to discuss possible directions of future development.

-

•

In this work a closed form solution for random distribution to random value problem (1) is found. The question arise about problem order increase, replace “random distribution” by “random distribution of random distribution” (or even further “random distribution of random distribution of random distribution”, etc.). In this case each in (1) should be treated as a sample distribution itself, and index then can be treated as 2D index . Working with 2D indexes is actually very similar to working with images, see Ref. Malyshkin (2015a) where the 2D index was used for image reconstruction by applying Radon–Nikodym or least squares approximation. Similarly, the results of this paper, can be generalized to higher order problems, by considering all indexes as 2D.

-

•

Obtaining possible outcomes as matrix spectrum (10) and then calculating their probabilities by projection (11) of given distribution (point distribution (7) is a simplest example of such) to eigenvectors (13) is a powerful approach to estimation of distribution under given condition. We can expect this approach to show good performance for data drawn from a wide range of probability distributions, especially for distributions that are not normal. The reason is because the (10) is expressed in terms of probability states, what make the role of outliers much less important, compared to methods based on norm, particulary least squares. For example, this approach can be applied to distribtions where only first moment of is finite, while the norm approaches require second moment of to be finite, what make them inapplicable to distributions with infinite standard deviation. We expect the (10) approach can be a good foundation for construction of Robust StatisticsHuber (2011).

References

- Dietterich et al. (1997) Thomas G Dietterich, Richard H Lathrop, and Tomás Lozano-Pérez, “Solving the multiple instance problem with axis-parallel rectangles,” Artificial intelligence 89, 31–71 (1997).

- Yang (2005) Jun Yang, Review of multi-instance learning and its applications, Tech. Rep. (Tech. Rep, 2005).

- Zhou (2004) Zhi-Hua Zhou, “Multi-Instance Learning: A Survey,” Department of Computer Science & Technology, Nanjing University, Tech. Rep (2004).

- Szabó et al. (2014) Zoltán Szabó, Arthur Gretton, Barnabás Póczos, and Bharath Sriperumbudur, “Learning theory for distribution regression,” arXiv preprint arXiv:1411.2066 (2014).

- Malyshkin and Bakhramov (2015) Vladislav Gennadievich Malyshkin and Ray Bakhramov, “Mathematical Foundations of Realtime Equity Trading. Liquidity Deficit and Market Dynamics. Automated Trading Machines. http://arxiv.org/abs/1510.05510,” ArXiv e-prints (2015), arXiv:1510.05510 [q-fin.CP] .

- Malyshkin (2015a) Vladislav Gennadievich Malyshkin, “Radon–Nikodym approximation in application to image analysis. http://arxiv.org/abs/1511.01887,” ArXiv e-prints (2015a), arXiv:1511.01887 [cs.CV] .

- Malyshkin (2015b) Vladislav Gennadievich Malyshkin, “Multiple–Instance Learning: Christoffel Function Approach to Distribution Regression Problem,” ArXiv e-prints (2015b), arXiv:1511.07085 [cs.LG] .

- Malyshkin (2014) Vladislav Gennadievich Malyshkin, (2014), the code for polynomials calculation, http://www.ioffe.ru/LNEPS/malyshkin/code.html.

- Huber (2011) Peter J Huber, Robust statistics (Springer, 2011).