A New Class of Combinatorial Markets with Covering Constraints: Algorithms and Applications

Abstract

We introduce a new class of combinatorial markets in which agents have covering constraints over resources required and are interested in delay minimization. Our market model is applicable to several settings including scheduling, cloud computing, and communicating over a network. This model is quite different from the traditional models, to the extent that neither do the classical equilibrium existence results seem to apply to it nor do any of the efficient algorithmic techniques developed to compute equilibria seem to apply directly. We give a proof of existence of equilibrium and a polynomial time algorithm for finding one, drawing heavily on techniques from LP duality and submodular minimization. We observe that in our market model, the set of equilibrium prices could be a connected, non-convex set (see figure below). To the best of our knowledge, this is the first natural example of the phenomenon where the set of solutions could have such complicated structure, yet there is a combinatorial polynomial time algorithm to find one. Finally, we show that our model inherits many of the fairness properties of traditional equilibrium models.

1 Introduction

In a free market economy, prices naturally tend to find an “equilibrium” under which there is parity between supply and demand. The power of this pricing mechanism is well explored and understood in economics: It allocates resources efficiently since prices send strong signals about what is wanted and what is not, and it prevents artificial scarcity of goods while at the same time ensuring that goods that are truly scarce are conserved [38]. In addition, it ensures that the allocation of goods is Pareto optimal. Hence it is beneficial to both consumers and producers. Furthermore, equilibrium-based mechanisms have been designed even for certain applications which do not involve any exchange of money but require fairness properties such as envy-freeness and the sharing incentive property; a popular one being CEEI111Competitive Equilibrium with Equal Incomes [41]. Today, with the surge of markets on the Internet, in which pricing and allocation are done in a centralized manner via computation, an obvious question arises: can we apply insights gained from traditional markets to these new markets to accrue similar benefits? This (in addition to other motivations) has led to a long line of work in the TCS community on the computation of economic equilibria; see Appendix A for more details.

In this paper, we define a broad class of market models that are appropriate for modeling several new markets, including scheduling, cloud computing, and bandwidth allocation in networks. A common feature of our markets is that these are resource allocation markets in which each agent desires a specific amount of resources to complete a task, i.e., each agent has a covering constraint. If the agent does not get all the resources requested, then she will not be able to complete the task and hence has no value for this partial allocation. With several agents vying for the same set of resources, a new parameter that becomes crucially important is the delay experienced by agents. This naturally leads to a definition of supply and demand, as well as pricing and allocation, based on temporal considerations.

We define an equilibrium-based model for pricing and allocation in these markets. Our model is fundamentally different from traditional market models: Each agent needs only a bounded amount of resources to finish her tasks and has no use for more, and her utility, which corresponds to the delay she experiences, also has a finite maximum value, i.e., her “utility function” satiates. On the other hand, traditional models satisfy non-satiation, i.e., no matter what bundle of goods an agent gets, there is a way of giving her additional goods so her utility strictly increases. Non-satiation turns out to be a key assumption in the Arrow-Debreu Theorem, which established existence of equilibrium in traditional markets. Despite this, we manage to give an existence proof for our model. Additionally, we prove that all the above-stated benefits of equilibria, including the fairness properties of CEEI, continue to hold for our model.

We next address the issue of computing equilibria in our model. Rubinstein [47] recently showed that computing an equilibrium in our general model is PPAD-hard. For this reason, we defined a sub-model for which we seek an efficient algorithm. This sub-model is of interest in applications, including the three mentioned above. However, it turns out that equilibria of this sub-model have a different structure than those of models for which polynomial time algorithms have been designed. For instance, we give examples in which the set of equilibrium prices is non-convex. Hence techniques used for designing polynomial time algorithms for traditional models, such as the primal-dual method and convex programming, are not applicable. Our algorithms are based on new ideas: we make heavy use of LP duality and the way optimal solutions to LPs change with changes in certain parameters. Submodular minimization, combined with binary search, is used as a subroutine in this process.

In summary, for the main applications stated above, our market-based model admits equilibrium prices, which can moreover be computed in polynomial time and we show that our algorithm is incentive compatible. In addition, the equilibrium allocations satisfy a range of fairness properties. Considering the many favorable properties of market-based models and the availability of massive computing power for computing equilibria, we believe they will play an important role in markets on the Internet.

Organization.

We define the market model and state our main results in Section 2. In this section, we define the notions of strong feasibility, under which we establish existence of equilibrium, and extensibility, which gives the sub-model for which we give a polynomial time algorithm. We also discuss properties of fairness and incentive compatibility of our solution. In Section 3 we describe the algorithm for a special case in a scheduling setting, in order to convey the main ideas. The algorithm in its full generality, and an overview of the analysis are in Section 4. Section 5 contains all the different examples referred to, and also a description of a run of the algorithm for some examples. The appendices contain more details on related work (A), special cases of our model (D), existence of equilibria (C), connection of our algorithm to Myerson’s ironing in the scheduling case (B), equilibrium characterization for the general model (E), proofs missing from the main paper (F), and fairness and incentive compatibility properties (G).

2 Model and Main Results

We introduce a combinatorial version of the well studied Fisher market model [19, 6]. In market , let be a set of agents, indexed by , and be a set of divisible goods, indexed by . We represent an allocation of goods to agents using the variables . Each agent wants to procure goods that satisfy a set of covering constraints, , where is a set indexing the constraints ( is the same for all agents for ease of notation).

| (CC) |

The objective of each agent is to minimize the “delay” she experiences, while meeting these constraints. We refer to the term as the delay faced by agent on using good , and the terms s as the “requirements”; s and s are assumed to be non-negative. Agent wants an allocation that optimizes the following LP.

| (Delay LP) |

We use the notation , , , and . Although our results hold for any LP, the most interesting cases are when the constraints are covering constraints, i.e., the matrix has only non-negative entries.

We will use a market mechanism to allocate resources. Let denote the price per unit amount of good , and assume agent has a total budget of . Then, as is standard in Fisher markets, the bundle that the agent may purchase is restricted by,

| (Budget constraint) |

Allocation is an optimal allocation (bundle) of agent relative to prices , if it optimizes LP (Delay LP) with an additional budget constraint (Budget constraint). Each good has a given supply which, after normalization, may be assumed to be equal to . The allocation needs to be supply respecting, that is, it has to satisfy the supply constraints:

| (Supply constraints) |

Finally, a supply respecting allocation and prices are a market equilibrium of iff

-

1.

Each agent gets an optimal allocation relative to prices .

-

2.

If some good is not fully allocated, i.e., , then .

The equilibrium condition requires that each agent does the best for herself, regardless of what the other agents do or even what the supply constraints are. From the perspective of the goods, the aim is market clearing (rather than, say, profit maximization)222However, our algorithm will find an equilibrium where every agent spends all of her budget, and thereby it maximizes the profit automatically.. Some goods may not have sufficient demand and therefore we may not be able to clear them. This is handled by requiring these goods to be priced at zero.

In Theorem 3 we obtain characterization of equilibrium in this general model in terms of solutions of a parameterized linear program that has one parameter per agent.

2.1 Existence of equilibria.

We show how the above model is a special case of the classic Arrow-Debreu market model with quasi-concave utility functions in Appendix C.1. Unfortunately, these utility functions do not satisfy the “non-satiation” condition required by the Arrow-Debreu theorem for the existence of an equilibrium: utility does not increase beyond a point even if additional goods are allocated. In fact, equilibrium doesn’t always exist for all covering LPs, as shown via a simple example in Section 5, Figure 3. And therefore next we identify conditions under which it does exist; the example in Figure 3 shows how this condition is necessary.

The equilibrium condition requires at a minimum that there exists a supply respecting allocation that also satisfies CC of all the agents. In fact, it is easy to see that a somewhat stronger feasibility condition is necessary: suppose that a subset of agents all have high budgets while the remaining agents have budgets that are close to 0. Then at an equilibrium, agents in the former set get their “best” goods, which means that whatever supply remains must be sufficient to allocate a feasible bundle for the remaining agents.

We require a similar condition for all minimally feasible allocations, i.e., an allocation such that reducing amount of any good would make CC infeasible. We call this condition strong feasibility.

Definition 1 (Strong feasibility).

Market satisfies strong feasibility if any minimally feasible and supply respecting solution to a subset of agents can be extended to a feasible and supply respecting allocation to the entire set. Formally, , and that are minimally feasible for and are supply respecting (with ), solutions that are feasible for and is supply respecting.

Theorem 1.

[Strong feasibility implies existence of an equilibrium] If (CC)i∈A of market satisfies strong feasibility, then an allocation and prices that constitute a market equilibrium of .

The proof of this theorem is in Appendix C. Strong feasibility is quite general in the following sense: it is satisfied if there is a “default” good that has a large enough capacity and may have a large delay but occurs in every constraint with a positive coefficient. In other words, any agent’s covering constraints may all be met by allocating sufficient quantity of the default good.

2.2 Efficient computation.

Ideally we would want to design an efficient algorithm for markets with Strong feasibility condition, however this problem turns out to be PPAD-hard [47]. In order to circumvent this hardness, we define a stronger condition called extensibility, and design a polynomial time algorithm to compute a market equilibrium under it. Extensibility requires that any “optimal allocation” to a subset of agents can be “extended” to an “optimal allocation” for a set that includes one extra agent. Hence this is a matroid like condition. For this we first formally define “optimal allocation” for a subset of agents.

Definition 2.

For any subset of agents , we say that an allocation is jointly optimal for if (i) it satisfies , (ii) it is supply respecting, and (iii) it minimizes . (Observe that may not be optimal for individual agents in .)

Definition 3 (Extensibility).

Market satisfies extensibility if , given an allocation that is jointly optimal for , the following holds: for any , an allocation that is jointly optimal for , while not changing the delay of the agents in , i.e., . In other words, total delay cost of agents in can be minimized without changing the delay cost of agents in .

Extensibility seems somewhat stronger than strong feasibility, but the two conditions are formally incomparable; see example in Section 5, Figure 3. In Section 2.3 we show that extensibility condition captures many interesting problems as special cases. Another mild condition we need is that there is enough demand for goods from each agent, otherwise an agent with very little requirement but huge amount of money may drive everyone else out of the market.

Definition 4 (Sufficient Demand).

Market satisfies sufficient demand if under zero prices, the optimal bundle of each agent contains some good that is demanded more than its supply, i.e., for an optimal solution to (Delay LP), there exists a good such that .

Even for very simple markets, e.g., Tables 1 and 2 in Section 5, the set of equilibria may turn out to be highly non-convex. Therefore techniques used to obtain polynomial time algorithms for traditional models are not applicable. In Section 4 we design a polynomial time algorithm by making a heavy use of parameterized LP, duality and submodular minimization, and obtain the following result.

Theorem 2.

[Extensibility and sufficient demand implies polynomial time algorithm] There is a polynomial time algorithm that computes a market equilibrium allocation and prices for any market that satisfies extensibility and sufficient demand.

2.3 Applications

As a consequence of the above theorem we get polynomial time algorithms for the following special cases. (The proofs that these satisfy extensibility are in Appendix D.)

Scheduling.

The agents are jobs that require different types of machines, and the set of machines of type is ; the machines are the goods in the market. Each agent needs units of machines in all of type , which is captured by the covering constraint . All agents experience the same delay from machine in type . Assume that the number of machines in each type is greater than the total requirements of the agents, . In reality different machines in this model may represent actually different machines, or the same machine at different times. The main motivation for this problem is scheduling in the cloud computing context, but it also captures other client-server scenarios such as crowdsourcing. An earlier version of this paper designed an algorithm only for this case [20].

Restricted assignment with laminar families – Different arrival times.

The above basic scheduling setting can be generalized to the following restricted assignment case, where job is allowed to be processed only on a subset of all the machines for type . We need the s to form a laminar333A family of subsets is said to be laminar if any two sets and in the family are either disjoint, , or contained in one another, or . family within each type, and in addition, we require that the machines in a larger subset have lower delays. That is, if for some two agents , then for each type . This helps to model the important condition in the cloud computing context that jobs may arrive at different times.

Network Flows.

The goods are edges in a network, where each edge has a certain (fixed) delay . Each agent wants to send units of flow from a source to a sink , and minimize her own delay (which is a min-cost flow problem). We show that if the network is series-parallel and the source-sink pair is common to all agents, then the instance satisfies extensibility. This is similar to the basic scheduling example in that there is a sequence of paths of increasing delay, but the difference here is that we need to price edges and not paths. The difficulty is that paths share edges and hence the edge prices should be co-ordinated in such a way that the path prices are as desired. There are networks that are not series-parallel but still the instance satisfies extensibility. We show one such network (and also how our algorithm runs on it) in Figure 5 on page 5. For a general network, an equilibrium may not exist; we give such an example in Figure 3.

A generalization of all these special cases that still satisfies extensibility is as follows: take any number of independent copies of any of these special cases above. E.g., each agent might want some machines for job processing, as well as send some flows through a network or a set of networks, but have a common budget for both together. Our algorithm works for all such cases.

2.4 Properties of equilibria

Fairness:

We first discuss an application of our market model to fair division of goods, where there are no monetary transfers involved. This captures scenarios where the goods to be shared are commonly owned, such as the computing infrastructure of a large company to be shared among its users. A standard fair division mechanism is competitive equilibrium from equal incomes (CEEI) [41]. This mechanism uses an equilibrium allocation corresponding to an instance of the market where all the agents have the same budget. This can be generalized to a weighted version, where different agents are assigned different budgets based on their importance.

The fairness of such an allocation mechanism follows from the following properties of equilibria shown in Appendix G.1 for the general model. 1. The equilibrium allocation is Pareto optimal; this an analog of the first welfare theorem for our model. 2. The allocation is envy-free; since each agent gets the optimal bundle given the prices and the budget, he doesn’t envy the allocation of any other agent. 3. Each agent gets a “fair share”: the equilibrium allocation Pareto-dominates an “equal share” allocation, where each agent gets an equal amount of each resource. This property is also known as sharing incentive in the scheduling literature [29]. 4. Incentive compatibility (IC): the equilibrium allocation is incentive compatible “in the large”, where no single agent is large enough to significantly affect the equilibrium prices. In this case, the agents are essentially price takers, and hence the allocation is IC. We also show a version of IC when the market is not large. We discuss this in more detail below.

Incentive Compatibility:

In the quasi-linear utility model, an agent maximizes the valuation of the goods she gets minus the payment. In the presence of budget constraints, Dobzinski et al. [21] show that no anonymous444Anonymity is a very mild restriction, which disallows favoring any agent based on the identity. IC mechanism can also be Pareto optimal, even when there are just two different goods. In the context of our model, a quasi-linear utility function specifies an “exchange rate” between delay and payments, and wants to minimize a linear combination of the two. We show in Appendix G.3 that the impossibility extends to our model via an easy reduction to the case of Dobzinski et al. [21].

In the face of this impossibility, we show the following second best guarantee in Appendix G.2. For the scheduling application mentioned above, we show that our algorithm as a market based mechanism is IC in the following sense: non-truthful reporting of and s can never result in an allocation with a lower delay. A small modification to the payments, keeping the allocation the same, makes the entire mechanism incentive compatible for the model in which agents want to first minimize their delay and subject to that, minimize their payments.

The first incentive compatibility assumes that utility of the agents is only the delay, and does not depend on the money spent (or saved). Such utility functions have been considered in the context of online advertising [5, 23, 42]. It is a reflection of the fact that companies often have a given budget for procuring compute resources, and the agents acting on their behalf really have no incentive to save any part of this budget. In the fair allocation context (CEEI), this gives a truly IC mechanism, since the s are determined exogenously, and hence are not private information.

The second incentive compatibility does take payments into account, but gives a strict preference to delay over payments. Such preferences are also seen in the online advertising world, where advertisers want as many clicks as possible, and only then want to minimize payments. The modifications required for this are minimal, and essentially change the payment from a “first price” to a “second price” wherever required.

3 Scheduling on a single machine

Our algorithm for the general setting is quite involved, therefore we first present it for a very special case in a scheduling setting mentioned in Section 2.3. The basic building blocks and the structure of the algorithm and the analysis are reflected in this case. In Section 5, we describe the run of this algorithm on the example in Table 1. We note that the formal proofs are given only for the general case and not for this section.

Suppose that there is just one machine and a good is this machine at a certain time , which we refer to as slot . The set of goods is therefore and we index the goods by instead of as before. Further, assume that the delay of slot is just , i.e., . Each agent requires a certain number of slots to be allocated to her, as captured by the covering constraint , for some . We denote the sum of the requirements over a subset of agents as . Recall that the budget of agent is , and similarly . We will show that equilibrium prices are characterized by the following conditions.555For how this equilibrium characterization leads to an analogy with Myerson’s ironing for a special case of this setting, with for all , see Appendix B.

-

1.

The prices form a piecewise linear convex decreasing curve. Let the linear pieces (segments) of this curve be numbered , from right to left.

-

2.

There is a partitioning of the agents into sets where the number of slots in th segment is . Note that since s are integers so are the s.

-

3.

The sum of the prices of slots in th segment equals .

-

4.

For any , the total price of the first slots of the segment , since otherwise these slots would be over demanded. This is equivalent to saying that the total price of the last slots in this segment .

The above only characterizes equilibrium prices. We will show that Conditions 3 and 4 imply that there exists an allocation of the slots in segment to the agents in such that both their requirements and budget constraints are satisfied. Such allocations can then be found by solving the following feasibility LP (1). In this LP, segment corresponds to the interval .

| (1) | ||||

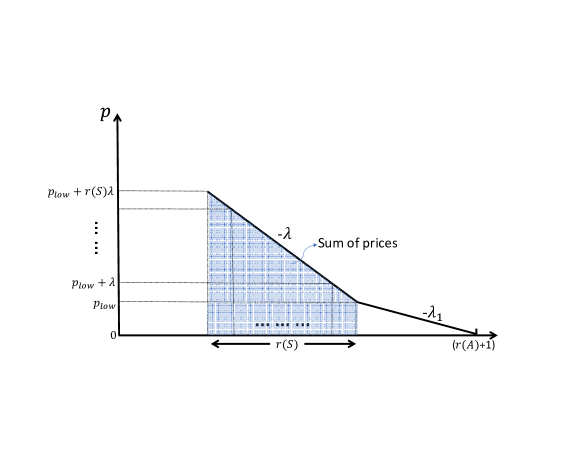

We now describe the algorithm, which is formally defined in Algorithm 1. It iteratively computes , starting from : the last segment that corresponds to the latest slots is computed first, and then the segment to its left, and so on. Inductively, suppose we have computed segments numbered 1 up to . Let be the price of the earliest slot in segment , and let . For any , consider the sum of the prices of consecutive slots to the left of this slot, forming a line segment with slope (see Figure 2); this sum is

Then for any , one can solve for the where this would be equal to ; we define this as a function of .

The next segment is defined to be the one with the smallest slope:

With this definition of the next segment, and with prices for the corresponding slots set to be linear with slope , it follows that Conditions 3 and 4 are satisfied.

It is not immediately clear how to minimize ; the function need not be submodular, for instance. The main idea here is to do a binary search over , as defined in Algorithm 2. Consider the function as defined in line 2 of this algorithm, and notice that is decreasing in . From the preceding discussion, it follows that the segment we seek is such that and . This implies that must minimize over all subsets of . Thus, given any and a minimizer of , we can tell whether the desired is above or below this , and a binary search gives us the desired segment. A minimizer of can be found efficiently since this is (as we will show) a submodular function.

In addition to the feasibility of LP (1), the main technical aspect of proving the correctness of the algorithm is to show that each agent gets an optimal allocation. This follows essentially from showing Condition 1, that the prices indeed form a piecewise linear convex curve, or equivalently, that the s form an increasing sequence. It is fairly straightforward to see that the running time of the algorithm is polynomial.

4 Algorithm under Extensibility

In this section we present the algorithm that proves Theorem 2; we will parallel the presentation in Section 3. We first present equilibrium characterization for the general model in Theorem 3 (complete proof is in Appendix E), and then describe the key ideas in designing the algorithm (the missing proofs and other details of this part are in Appendix F). We show run of our algorithm on a network example in Section 5, Figure 5.

Recall that in our general model, each agent has a delay function and a set of constraints on the bundle of goods she gets. Unlike in Section 3, there is no simple ordering among the goods that enables a geometric description of an equilibrium, therefore some parts that are immediate in that setting may require a proof here. Recall that the first step in Section 3 was to find an equilibrium characterization only in terms of prices. This used the geometry of the instance in order to partition the time slots into segments. More generally, it will be more convenient to consider a partition of agents rather than a partition of goods. By abuse of terminology, in this section, by “segment” we refer to a subset of agents. Each agent in has a parameter , that previously corresponded to the slope of the segment they were in. Similarly, now too, all agents in a segment have the same . This will also correspond to the optimal dual variable for Budget constraint in the agent’s optimization problem at the equilibrium.

Given a vector of s, denoted by , next we define a parameterized linear program and its dual. Intuition for this definition comes from the optimal bundle LP of each agent at given prices. In the following, has allocation variables s, the constraint CC for each agent , and the supply respecting constraint for each good . The corresponding dual variables are respectively s and s, where can be thought of as the price for good .

| (2) |

Remarkably, the next theorem shows that the problem of computing an equilibrium reduces to solving the above LP and its dual for a right parameter vector .

Theorem 3.

For a given if an optimal solution of and an optimal solution of satisfy Budget constraint for all agents with equality, then they constitute an equilibrium of market .

We note that the proof of Theorem 3 uses only complementary slackness conditions of optimal bundle LP of each buyer, and therefore the theorem holds for the most general model, i.e., without any of the extensibility, enough demand, or strong feasibility assumptions. Theorem 3 gives us the “geometry” of an equilibrium outcome, and is roughly equivalent to Condition 1 from Section 3. It reduces the problem to one of finding a right parameter vector ; however there is still the entire to search from. As was done in Section 3, our main goal is to further reduce this task to a sequence of single parameter searches, each involving submodular minimization and binary search.

Theorem 3 is applicable when all agents spend exactly their money at a primal-dual pair of optimal solutions for a given vector . Now the question is to characterize such parameter vectors . Note that, there really is no equivalent of Condition 2 from Section 3, since some goods may be allocated across agents in different segments. This is the source of many of the difficulties we face. Next, in Lemma 2, we derive an (approximate) equivalent of Conditions 3 and 4 from Section 3. This guarantees the existence of (allocation, prices) that satisfy the budget constraints of agents. One difference here is that this is going to be a global condition that involves the entire vector , rather than a local condition that we could apply to a single segment like in Section 3. For this we need a number of properties of optimal solutions of and that we show in Lemma 1 next.

Let us define and . Similarly, for a subset of agents , and . Let denote the set of indices. By abuse of notation, let us define

Using extensibility, in the next lemma we show that optimal solutions of and satisfy some invariants regarding delays and payments of agents, e.g., we will show that higher the the better the delay at primal optimal. For a fixed dual optimal the total payment of a segment remains fixed at all optimal allocations, and as the delay of a subset decreases, its payment increases. Recall Definition 2 for “jointly optimal for”.

Lemma 1.

Given , partition agents by equality of into sets such that .

-

1.

At any optimal solution of delay is minimized first for set , then for , and so on, finally for . This is equivalent to being jointly optimal for each where , and for any other optimal solution we have .

-

2.

Given two dual optimal solutions and , if the first part of dual objective is same at both for some , i.e., , then for any optimal solution of , .

-

3.

Given two optimal solutions and of , and an optimal solution of , if for any subset for , , then . The former is strict iff the latter is strict too.

In the above lemma, the first claim follows from extensibility. The second and third claim follow from the first claim together with the fact that any pair of primal and dual optimal satisfies complementary slackness.

Recall Conditions 3 and 4 of Section 3 requiring respectively budget balanceness, and that when a subset of agents in a segment are given the “best” allocation, their total payment should be at least their total budget (or else they will over demand some good). Using the first and last part of Lemma 1 the latter can be roughly translated to saying that when the rest of the agents are given the “worst” allocation, the rest underpay in total. Based on this intuition next we define conditions budget balance (BB) and subset condition (SC) in the following.

Definition 5.

Given , and a set , we say that condition

-

•

BB is satisfied: If at any optimal solution of , we have .

-

•

SC is satisfied: let to be an optimal solution of where is maximized. Then, .

We will show that if BB and SC are satisfied for each “segment” at any given then is the right parameter vector. We will call such a proper , formally defined next.

Definition 6.

We say that pair is proper if such that is an optimal solution of , and pair satisfies BB and SC for subsets , where is the partition of by equality of .

The next lemma shows that the parameter vector corresponding to a proper pair would ensure existence of allocation where each agent spends exactly her budget, and thereby will give an equilibrium using Theorem 3.

Lemma 2.

If pair is proper for then there exists an optimal solution of the primal such that .

Given such a and solution of that satisfy conditions of Lemma 2, the above lemma ensures existence of allocation that satisfies Budget constraint, . We derive following feasibility LP in variables to compute such an allocation.

| (3) |

Now our goal has reduced to finding a proper pair. That is, if we think of partition of agents by equality of as “segments”, then we wish to find a vector such that BB and SC are satisfied for each “segment”. Our algorithm, defined in Algorithm 3, tries to fulfill exactly this goal. At a high level, like in Section 3, our algorithm will build the segments bottom up, i.e., lowest to highest segments. We will start by setting all the s to same value, and find lowest value where BB and SC are satisfied for a subset. Once found we freeze this subset as a segment and start increasing for the rest to find the next segment, and repeat.

In this process of finding the next segment we need to make sure that BB and SC conditions are maintained for the previous segments. In Section 3 we were able to do this by simply fixing the prices of the goods in earlier segments, because goods were not shared across segments. Here, some of the goods allocated to agents in the earlier segments may also be allocated to agents in the later segments, and additionally these allocations are not fixed and may keep changing during the algorithm. (We fix the allocation only at the end.) Furthermore, the prices are required to be dual optimal w.r.t. the vector that we eventually find. On the other hand in order to maintain BB and SC conditions for the previous segments we need to ensure that the total payment of previous segments do not change.

The next lemma shows that this is indeed possible by proving that prices of goods bought by agents from previous segments can be held fixed. In fact, we will be able to fix s as well, for agents in the previous segments. The proof involves an application of Farkas’ lemma, leveraging extensibility. During computation of next segment, we will hold fix the s of agents in segments found so far, and increase the s of the remaining agents. To facilitate this we define as the indicator vector of , i.e., if , and is otherwise.

Lemma 3.

Given a , partition agents into by equality of , where . For consider primal optimal that is jointly optimal for , and let be a dual optimal. Consider for some , the vector . Then is optimal in and there exists an optimal solution of such that,

As discussed above our algorithm will build segments inductively from the lowest to highest value, by increasing of only the “remaining” agents. Suppose, we have built segments through , and let be the remaining agents. Let be the current vector where . Let be the corresponding dual price vector which is optimal for . For ease of notations we define the following.

| (4) |

Fix an allocation of . We call an optimal solution of valid if prices are monotone w.r.t. and , in the sense as guaranteed by Lemma 3 (where prices of goods allocated to previous segments are held fixed and prices of the rest of the goods are not decreased), and s are fixed for agents outside . We will call the corresponding prices valid prices. For simplicity we will assume uniqueness of valid prices.666This is without loss of generality since perturbing the parameters of the market ensures this. A typical way to simulate perturbation is by lexicographic ordering [50].

| (5) |

Since the correctness is proved by induction, the inductive hypothesis is that w.r.t. , both SC and BB are satisfied for , and SC is satisfied for the remaining agents . The base case is easy with the s all set to . Our next goal is to find the next segment , a new vector and a new price vector such that the following properties hold.

-

1.

Parameter vector is obtained from by fixing s of agents outside , increase s of agents in by the same amount, and those of agents by some more. The latter increase is to separate from . That is for some and .

-

2.

Price vector is valid and optimal for .

-

3.

W.r.t. , satisfy both BB and SC, and satisfies SC.

The computation of the next segment satisfying the above conditions is done by the subroutine NextSeg, which we describe next, and which is formally defined in Algorithm 4. As in Section 3, the basic idea is to reduce this problem to a single parameter binary search. Since Condition SC is satisfied for the remaining agents at while BB is not, total payment of is less than their total budget . In order to keep track of this surplus budget, consider the following function on .

| (6) |

We translate Condition 3 above in terms of this function, in the following lemma, which essentially reduces the problem to a single parameter search.

Lemma 4.

Suppose that for some ,

Further, suppose that , and be a maximal such set. Then there exists a rational number of polynomial-size such that, w.r.t. as defined above, satisfy both BB and SC, and satisfy SC.

The above lemma reduces the task of finding next segment to finding an appropriate such that the minimum value of is zero under the valid price . This requires two things: first we need to find a minimizer of for a given , and second we need to find the right value of . The next lemma shows that the first can be done using an algorithm for submodular minimization, and therefore in a polynomial time [51]. For convenience of notation, we define the following functions.

| (7) |

Lemma 5.

Given , function is submodular over set .

Now the question remains, how does one find an such that the minimum value is , i.e., . We will do binary search for the same. In the next lemma we derive a number of properties of that facilitates binary search, under sufficient demand assumption (Definition 4), while crucially using Lemmas 1 and 3.

Lemma 6.

Function satisfies the following: . is continuous and monotonically decreasing in , , therefore is continuous and monotonically decreasing. a rational number of polynomial size such that , and has a zero of polynomial-size. Given a set , if and for , then such that and such an can be computed by solving a feasibility linear program of polynomial-size.

The first part follows essentially from the fact that satisfies SC condition w.r.t. equivalently . For the second part, we show that for any , function is monotonically decreasing and continuous in . Since of continuous and decreasing functions is also continuous and decreasing, we get the same property for . It turns out that whatever be the current value of , there is another where is strictly smaller (using sufficient demand assumption). This strict decrease property ensures existence of where is zero. Setting to higher than any such would give since for all are monotonically decreasing in , thereby we get the third part. Finally for the fourth part, existence of follows from monotonicity and continuity of in , and using the fact that complementary slackness ensures optimality we construct a feasibility linear program to compute , given , such that .

We initialize our binary search with a lower pivot and a higher pivot to a value that is guaranteed to be higher than where some set goes tight (third part of Lemma 6). Finally, since submodular minimization, binary search over a polynomial-sized range, and solving linear program all can be done in polynomial-time, we get our main result, Theorem 2, using Lemmas 2, 4 and 6, and Theorem 3.

5 Examples

In this section we show several interesting examples that illustrate important properties of our market and of equilibria. In addition we demonstrate a run of our algorithm on a routing example.

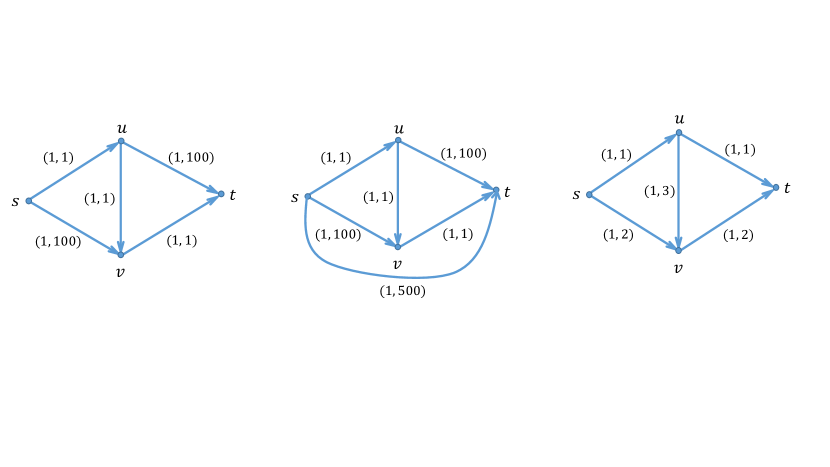

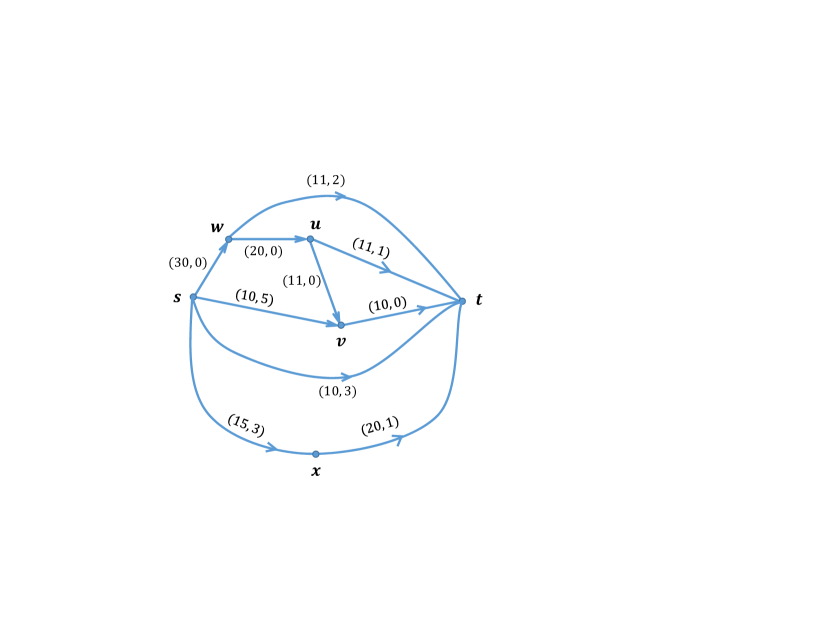

Non-existence of equilibria.

Consider the networks (typically used to show Braess’ paradox) in Figure 3, where the label on each edge specifies its (capacity, delay cost). There are two agents, each with a requirement of 1 from to . Their s are and respectively. The network on the left has enough capacity to route two units of flow, but does not satisfy strong feasibility condition and does not have an equilibrium. This demonstrates importance of strong feasibility condition, without which even a simple market may not have an equilibrium.

The network in the middle does satisfy strong feasibility but not extensibility and has an equilibrium. The network on the right satisfies extensibility but not strong feasibility and has an equilibrium. This demonstrates that conditions of strong feasibility and extensibility are incomparable.

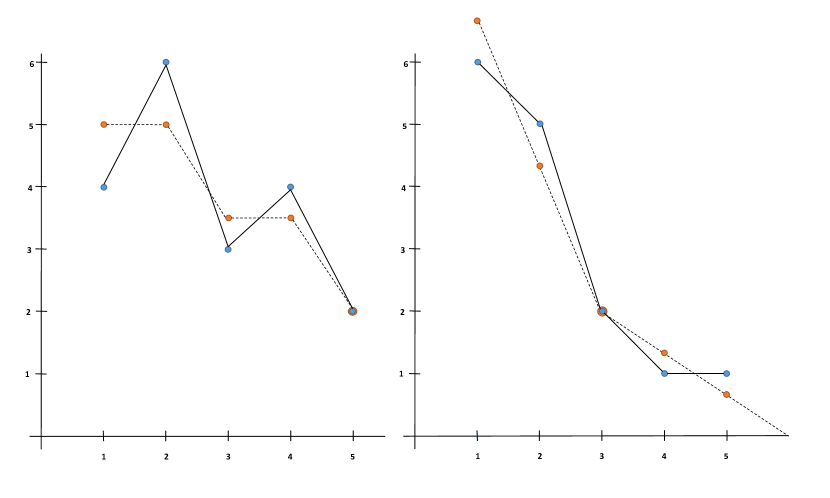

Non-convexity of equilibria.

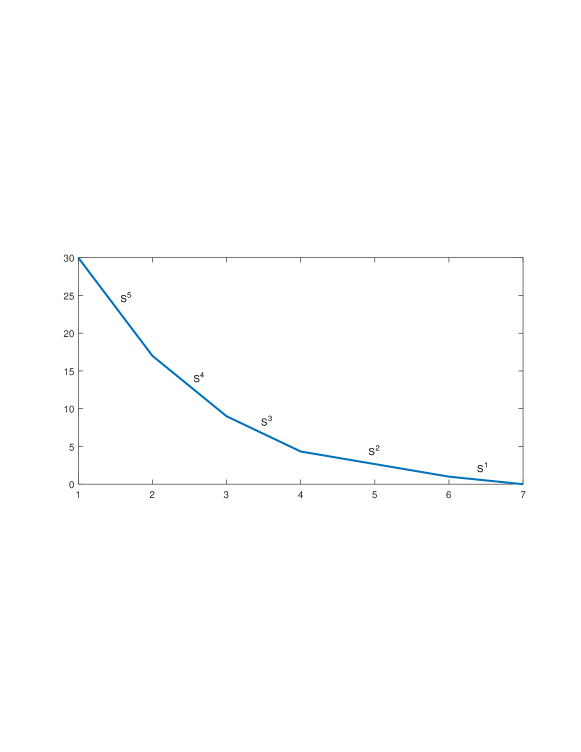

Consider a market in the scheduling setting of Section 3, with 6 agents, each with a requirement of 1. Their s are . Table 1 depicts some of the equilibrium prices for this instance. A bigger example with 9 agents is in Table 2. These examples show that the equilibrium set is not convex, but forms a connected set. Since these are in high dimension, it is not easy to determine the exact shape of the entire equilibrium set, but one can see that it is quite complicated.

![[Uncaptioned image]](/html/1511.08748/assets/x4.png)

![[Uncaptioned image]](/html/1511.08748/assets/x5.png)

A run of the algorithm.

We describe the run of our algorithms on simple examples here. The run of Algorithm 1 on the example in Table 1 is as follows. Each row below depicts one iteration, where we find a new segment. We first give the set of agents in this new segment, then the corresponding , and then the prices of the slots determined in this iteration. The last column shows the sets which give the second and third lowest s in that iteration, and hence were not selected.

| , | , | () | |

| , | , | () | |

| , | , | () | |

| , | , | () | |

| , | , |

The equilibrium price found in this run is the point in Table 1. This price curve is shown in Figure 4. The allocation obtained by solving the feasibility LP (3) is as follows: .

We next describe the run of the algorithm on a network flow example, described in Figure 5. The figure shows the network structure and the edge labels specify (capacity, delay cost). There are five agents with requirements from to respectively. Their s are . This network is not series-parallel, yet it satisfies the extensibility condition, so our algorithm finds an equilibrium.

The run of Algorithm 3 on this example (in Figure 5) is as follows. Once again, each row below depicts one iteration, where we find a new segment. We first give the set of agents in the new segment, then the corresponding , and then the prices of the edges that are fixed in this iteration. The last column shows the second and third lowest s in that iteration.

| , | , | ( | |

| ) | |||

| , | , | () |

The allocation from the feasibility LP (3):

-

•

Agent sends units of flow on path and units of flow on path .

-

•

Agent sends units of flow on path and units of flow on path .

-

•

Agent sends units of flow on path , units of flow on path and units of flow on path .

-

•

Agent sends units of flow on path , units of flow on path and units of flow on path .

-

•

Agent sends units of flow on path , units of flow on path and units of flow on path .

References

- Babaioff et al. [2014] Moshe Babaioff, Brendan Lucier, Noam Nisan, and Renato Paes Leme. On the efficiency of the Walrasian mechanism. In ACM Conference on Economics and Computation, EC, pages 783–800, 2014.

- Badanidiyuru et al. [2012] Ashwinkumar Badanidiyuru, Robert Kleinberg, and Yaron Singer. Learning on a budget: posted price mechanisms for online procurement. In Proceedings of the 13th ACM Conference on Electronic Commerce, pages 128–145. ACM, 2012.

- Bein and Brucker [1985] Wolfgang W. Bein and Peter Brucker. Minimum cost flow algorithms for series-parallel networks. Discrete Applied Mathematics, 10(2):117 – 124, 1985.

- Bhattacharya et al. [2010] Sayan Bhattacharya, Vincent Conitzer, Kamesh Munagala, and Lirong Xia. Incentive compatible budget elicitation in multi-unit auctions. In Proceedings of the twenty-first annual ACM-SIAM symposium on Discrete Algorithms, pages 554–572. SIAM, 2010.

- Borgs et al. [2007] Christian Borgs, Jennifer Chayes, Nicole Immorlica, Kamal Jain, Omid Etesami, and Mohammad Mahdian. Dynamics of bid optimization in online advertisement auctions. In Proceedings of the 16th international conference on World Wide Web, pages 531–540. ACM, 2007.

- Brainard and Scarf [2000] W. C. Brainard and H. E. Scarf. How to compute equilibrium prices in 1891. Cowles Foundation Discussion Paper, 1270, 2000.

- Budish [2011] Eric Budish. The combinatorial assignment problem: Approximate competitive equilibrium from equal incomes. Journal of Political Economy, 119(6):1061 – 1103, 2011.

- Budish and Kessler [2014] Eric B Budish and Judd B Kessler. Changing the course allocation mechanism at wharton. Chicago Booth Research Paper, (15-08), 2014.

- Che and Gale [2000] Yeon-Koo Che and Ian Gale. The optimal mechanism for selling to a budget-constrained buyer. Journal of Economic theory, 92(2):198–233, 2000.

- Chen et al. [2009] X. Chen, D. Dai, Y. Du, and S.-H. Teng. Settling the complexity of Arrow-Debreu equilibria in markets with additively separable utilities. In FOCS, 2009.

- Cheung et al. [2013] Yun Kuen Cheung, Richard Cole, and Nikhil Devanur. Tatonnement beyond gross substitutes?: gradient descent to the rescue. In Proceedings of the forty-fifth annual ACM symposium on Theory of computing, pages 191–200. ACM, 2013.

- Codenotti et al. [2006] B. Codenotti, A. Saberi, K. Varadarajan, and Y. Ye. Leontief economies encode two-player zero-sum games. In SODA, 2006.

- Codenotti et al. [2005] Bruno Codenotti, Benton McCune, and Kasturi Varadarajan. Market equilibrium via the excess demand function. In ACM Symposium on the Theory of Computing, 2005.

- Cole and Fleischer [2008] Richard Cole and Lisa Fleischer. Fast-converging tatonnement algorithms for one-time and ongoing market problems. In Proceedings of the fortieth annual ACM symposium on Theory of computing, pages 315–324, 2008.

- Cole et al. [2013] Richard Cole, Vasilis Gkatzelis, and Gagan Goel. Mechanism design for fair division: allocating divisible items without payments. In ACM Conference on Electronic Commerce, EC ’13, pages 251–268, 2013.

- Deng et al. [2002] Xiaotie Deng, Christos Papadimitriou, and Shmuel Safra. On the complexity of equilibria. In Proceedings of ACM Symposium on Theory of Computing, 2002.

- Devanur and Kannan [2008] N. Devanur and R. Kannan. Market equilibria in polynomial time for fixed number of goods or agents. In FOCS, pages 45–53, 2008.

- Devanur and Vazirani [2004] N. Devanur and V. V. Vazirani. The spending constraint model for market equilibrium: Algorithmic, existence and uniqueness results. In Proceedings of 36th STOC, 2004.

- Devanur et al. [2008] N. Devanur, C. H. Papadimitriou, A. Saberi, and V. V. Vazirani. Market equilibrium via a primal-dual algorithm for a convex program. JACM, 55(5), 2008.

- Devanur et al. [2015] Nikhil Devanur, Jugal Garg, Ruta Mehta, Vijay V Vazirani, and Sadra Yazdanbod. A market for scheduling, with applications to cloud computing. arXiv preprint arXiv:1511.08748, 2015.

- Dobzinski et al. [2012] Shahar Dobzinski, Ron Lavi, and Noam Nisan. Multi-unit auctions with budget limits. Games and Economic Behavior, 74(2):486–503, 2012.

- Etessami and Yannakakis [2010] K. Etessami and M. Yannakakis. On the complexity of Nash equilibria and other fixed points. SIAM Journal on Computing, 39(6):2531–2597, 2010.

- Feldman et al. [2007] Jon Feldman, S Muthukrishnan, Martin Pal, and Cliff Stein. Budget optimization in search-based advertising auctions. In Proceedings of the 8th ACM conference on Electronic commerce, pages 40–49. ACM, 2007.

- Fiat et al. [2011] Amos Fiat, Stefano Leonardi, Jared Saia, and Piotr Sankowski. Single valued combinatorial auctions with budgets. In Proceedings of the 12th ACM conference on Electronic commerce, pages 223–232. ACM, 2011.

- Garg et al. [2012] Jugal Garg, Ruta Mehta, Milind Sohoni, and Vijay V. Vazirani. A complementary pivot algorithm for market equilibrium under separable piecewise-linear concave utilities. In ACM Symposium on the Theory of Computing, 2012.

- Garg et al. [2014] Jugal Garg, Ruta Mehta, and Vijay V. Vazirani. Dichotomies in equilibrium computation, and complementary pivot algorithms for a new class of non-separable utility functions. In STOC, 2014.

- Garg et al. [2017] Jugal Garg, Ruta Mehta, Vijay V. Vazirani, and Sadra Yazdabod. Settling the complexity of Leontief and PLC exchange markets under exact and approximate equilibria. In ACM Symposium on the Theory of Computing, 2017. To appear.

- Garg and Kapoor [2004] R. Garg and S. Kapoor. Auction algorithms for market equilibrium. In Proceedings of 36th STOC, 2004.

- Ghodsi et al. [2011] Ali Ghodsi, Matei Zaharia, Benjamin Hindman, Andy Konwinski, Scott Shenker, and Ion Stoica. Dominant resource fairness: Fair allocation of multiple resource types. In Proceedings of the 8th USENIX Conference on Networked Systems Design and Implementation, NSDI’11, pages 323–336, 2011.

- Goel et al. [2015] Gagan Goel, Vahab Mirrokni, and Renato Paes Leme. Polyhedral clinching auctions and the adwords polytope. Journal of the ACM (JACM), 62(3):18, 2015.

- Hurwicz [1972] Leonid Hurwicz. On informationally decentralized systems. In C. B. McGuire and Roy Radner, editors, Decision and Organization: A Volume in Honor of Jacob Marschak. North-Holland, Amsterdam, 1972.

- Jain [2007] K. Jain. A polynomial time algorithm for computing the Arrow-Debreu market equilibrium for linear utilities. SIAM Journal on Computing, 37(1):306–318, 2007.

- Jain and Vazirani [2010] Kamal Jain and Vijay V Vazirani. Eisenberg–Gale markets: Algorithms and game-theoretic properties. Games and Economic Behavior, 70(1):84–106, 2010.

- Kakutani [1941] Shizuo Kakutani. A generalization of Brouwer’s fixed point theorem. Duke Mathematical Journal, 8(3):457–459, 1941.

- Kelly and Vazirani [2002] F. P. Kelly and V. V. Vazirani. Rate control as a market equilibrium. Unpublished manuscript., 2002. URL http://www.cc.gatech.edu/~vazirani/KV.pdf.

- Laffont and Robert [1996] Jean-Jacques Laffont and Jacques Robert. Optimal auction with financially constrained buyers. Economics Letters, 52(2):181–186, 1996.

- Lavi and Swamy [2009] Ron Lavi and Chaitanya Swamy. Truthful mechanism design for multidimensional scheduling via cycle monotonicity. Games and Economic Behavior, 67(1), 2009.

- Mas-Colell et al. [1995] Andreu Mas-Colell, Michael Dennis Whinston, and Jerry R Green. Microeconomic theory, volume 1. Oxford university press New York, 1995.

- Megiddo and Papadimitriou [1991] Nimrod Megiddo and Christos H Papadimitriou. On total functions, existence theorems and computational complexity. Theoretical Computer Science, 81(2):317–324, 1991.

- Mehta et al. [2005] A. Mehta, A. Saberi, U. Vazirani, and V. Vazirani. Adwords and generalized on-line matching. In FOCS, 2005.

- Moulin [2004] Hervé Moulin. Fair division and collective welfare. MIT press, 2004.

- Muthukrishnan et al. [2010] S Muthukrishnan, Martin Pál, and Zoya Svitkina. Stochastic models for budget optimization in search-based advertising. Algorithmica, 58(4):1022–1044, 2010.

- Myerson [1981] Roger B. Myerson. Optimal auction design. Mathematics of Operations Research, 6(1):58–73, 1981.

- Nisan and Ronen [2001] N. Nisan and A. Ronen. Algorithmic mechanism design. Games and Economic Behavior, 35(1–2):166–196, 2001.

- Nisan et al. [2009] Noam Nisan, Jason Bayer, Deepak Chandra, Tal Franji, Robert Gardner, Yossi Matias, Neil Rhodes, Misha Seltzer, Danny Tom, Hal Varian, and Dan Zigmond. Google’s auction for TV ads. Automata, Languages and Programming, pages 309–327, 2009.

- Orlin [2010] James B Orlin. Improved algorithms for computing Fisher’s market clearing prices: computing Fisher’s market clearing prices. In Proceedings of the forty-second ACM symposium on Theory of computing, pages 291–300. ACM, 2010.

- Rubinstein [2016] A. Rubinstein. Personal communication, 2016.

- Rustichini et al. [1994] Aldo Rustichini, Mark A Satterthwaite, and Steven R Williams. Convergence to efficiency in a simple market with incomplete information. Econometrica: Journal of the Econometric Society, pages 1041–1063, 1994.

- Scarf [1973] H. Scarf. The Computation of Economic Equilibria. Yale University Press, 1973.

- Schrijver [1986] A. Schrijver. Theory of Linear and Integer Programming. John Wiley & Sons, New York, NY, 1986.

- Schrijver [2003] A. Schrijver. Combinatorial Optimization. Springer-Verlag, 2003.

- Shoven and Whalley [1992] J. B. Shoven and J. Whalley. Applying general equilibrium. Cambridge University Press, 1992.

- Singer [2010] Yaron Singer. Budget feasible mechanisms. In Foundations of Computer Science (FOCS), 2010 51st Annual IEEE Symposium on, pages 765–774. IEEE, 2010.

- Smale [1976] S. Smale. A convergent process of price adjustment and global Newton methods. Journal of Mathematical Economics, 3(2):107–120, 1976.

- Vazirani and Yannakakis [2011] Vijay V. Vazirani and Mihalis Yannakakis. Market equilibrium under separable, piecewise-linear, concave utilities. Journal of ACM, 58(3):10:1–10:25, 2011.

- Végh [2012a] László A Végh. Concave generalized flows with applications to market equilibria. In Foundations of Computer Science (FOCS), 2012 IEEE 53rd Annual Symposium on, pages 150–159. IEEE, 2012a.

- Végh [2012b] László A Végh. Strongly polynomial algorithm for a class of minimum-cost flow problems with separable convex objectives. In Proceedings of the forty-fourth annual ACM symposium on Theory of computing, pages 27–40. ACM, 2012b.

- Wu and Zhang [2007] Fang Wu and Li Zhang. Proportional response dynamics leads to market equilibrium. In Proceedings of the thirty-ninth annual ACM symposium on Theory of computing, pages 354–363. ACM, 2007.

Appendix A Related work on computation and applications of market equilibrium

Computation and Complexity:

The computational complexity of market equilibrium has been extensively studied for the tradition models in the past decade and a half. This investigation has involved many algorithmic techniques, such as primal-dual and flow based methods [19, 18, 46, 56, 57], auction algorithms [28], ellipsoid [32] and other convex programming based techniques [13], cell-decomposition [16, 17, 55], distributed price update rules [14, 58, 11], and complementary pivoting algorithms [25, 26], to name some of the most prominent. The algorithms have been complemented by hardness results, either for PPAD [12, 10] or for FIXP [22, 27], pretty much closing the gap between the two. Most of these papers focus on traditional utility functions used in the economics literature. A notable exception that considers combinatorial utility functions is [33], that study a market where agents want to send flow in a network, motivated by rate control algorithms governing the traffic in the Internet.

Beyond being an important component in the complexity theory of total functions [39], the computation of market equilibria has been studied by economists for much longer [6, 49, 54]. The classic case for the use of equilibrium computation is counter-factual evaluation of policy or design changes [52], based on the assumption that markets left to themselves operate at an equilibrium.

Fair allocation:

Recently, market equilibrium outcomes have been used for fair allocation. Market equilibrium conditions are often considered inherently fair, therefore equilibrium outcomes have been used to allocate resources by a central planner seeking a fair allocation even when there is no actual market or monetary transfers. E.g., the proportional fair allocation, which is well known to be equivalent to the equilibrium allocation in a Fisher market [35], is widely used in the design of computer networks. Exchange of bandwidth in a bittorrent network is modeled as a process that converges to a market equilibrium by Wu and Zhang [58]. Budish [7] proposes “competitive outcome from equal incomes” (CEEI) as a way to allocate courses to students: the allocation is an equilibrium in a market for courses in which the students participate with equal budgets (with random perturbations to break ties). This scheme has been successfully used at the Wharton business school [8]. Cole et al. [15] show that a suitable modification of the Fisher market equilibrium allocation can be used as a solution to a problem of fair resource allocation, without money. The mechanism is truthful, and satisfies an approximate per-agent welfare guarantee. Truthful mechanisms have also been designed for scheduling, where it is the auctioneer who has jobs to be scheduled and the agents are the one providing the required resources e.g., see [44, 37]. This is in contrast to our setting where the agents have scheduling requirements.

Market based mechanisms:

There is also a long history of “market based mechanisms”, where a mechanism (with monetary transfers) implements an equilibrium outcome. The New York Stock Exchange uses such a mechanism to determine the opening prices, and copper and gold prices in London are fixed using a similar procedure [48]. There are different ways to do this: use a sample (either historic or random) or a probabilistic model of the population to compute the equilibrium price, and offer these prices to new agents. This is preferable to asking the bidders to report their preferences, computing the equilibrium on reported preferences and offering the equilibrium prices back. The latter leads to obvious strategic issues; Hurwicz [31] shows that strategic behavior by agents participating in such a mechanism can lead to inefficiencies. Babaioff et al. [1] show price of anarchy bounds on such mechanisms. In any case, such mechanisms are “incentive compatible in the large”, meaning that as the market size grows and each agent becomes insignificant enough to affect prices on his own, his best strategy is to accept the equilibrium outcome. Nonetheless such mechanisms have been proposed and used in practice, e.g., for selling TV ads [45].

Budget constraints:

Appendix B Relation to Myerson’s ironing

For a special case of the scheduling setting, when , we show that equilibrium conditions are equivalent to a set of conditions that are reminiscent of the ironing procedure used in the characterization of optimal auctions by Myerson [43]. It is in fact “one higher derivative” analog of Myerson’s ironing. Let’s first restate Myerson’s ironing procedure for the case of a uniform distribution over a discrete support. Suppose that we plot on the -axis the quantiles, in the decreasing order of value, and on the -axis the corresponding virtual values. This is possibly a non-monotone function, and Myerson’s ironing asks for an ironed function that is monotone non-increasing, and is such that the area under the curve (starting at 0) of the ironed function is always higher than that for the given function. Further, the ironed function given by this procedure is the minimal among all such functions. This means that wherever the area under the curve differs for the two functions, the ironed function is constant. (See Figure 6 on page 6.)

In the special case of our model with a single good and when requirements are all one, the equilibrium price of the good as a function of time is obtained as an ironed analog of the money function: the function , where we assume the s are sorted in the decreasing order. This money function is monotone non-increasing by definition but it need not be a convex function. The price as a function of time must be a monotone non-increasing and convex function. The area under the curve of the price function must always be higher than that of the money function; further, wherever the two areas are different, the price function must be linear. One can see that the conditions are the same as that of Myerson’s ironing, except each condition is replaced by a higher derivative analog. Unlike Myerson’s, the solution to our problem is no longer unique and the solution set may be non-convex!

Appendix C Existence of Equilibrium under Strong Feasibility

In this section we show existence of equilibrium for market instances satisfying strong feasibility (Definition 1 in Section 2). Given such an instance with set of agents and set of goods, let us create another instance by adding an extra good with “large quantity” and very high delay cost. Recall that the number of goods and agents in market be and respectively.

Set of agents and goods in market are respectively and . After normalizing to get quantity for good , we set coefficient of variable in all the constraints of CC to for each agent, and set the delay cost for good and for every agent to , where and . Thus, given prices of goods in , the optimal bundle of agent at these prices can be found by solving the following linear program.

| (8) |

The next lemma follows from the construction of market .

Lemma 7.

If satisfies strong feasibility then so does .

Price vector is said to be at equilibrium, if when every agent is given its optimal bundle, there is no excess demand of any good, and goods with excess supply have price zero. That is, such that,

| (9) |

Lemma 8.

If at prices for , then . That is at equilibrium.

Proof.

It is easy to see that , and hence the proof follows. ∎

Next we show that equilibria of and are related.

Lemma 9.

If satisfies strong feasibility, then every equilibrium of gives an equilibrium of .

Proof.

Let respectively be an equilibrium allocation and prices of . From Lemma 8, we know that . It suffices to show that , for the lemma to follow.

To the contrary suppose for some agent , . We will construct another bundle that is affordable to agent at prices , satisfies CC, and has a lower delay than , contradicting optimal bundle condition at equilibrium.

Due to strong feasibility, after all is given their bundle , there will be a bundle left for to buy among goods in such that constraints are satisfied. Clearly, one way to construct such is that the agent keeps buying all goods as in , and starts decreasing and increasing allocation for some other available good. Note that all such available goods are under-sold at equilibrium and therefore has zero price in . Thus payment for and are the same at prices . In other words is affordable at prices .

If good is increased by as we go from to , then we claim that , where . This is because, in a constraint even if coefficient of variable is minimum possible, and it needs to compensate for increase in other goods due to their negative coefficients, this cascade could at most harm by a factor of . Difference in delay is

∎

Due to Lemma 9, to show existence of equilibrium for market it suffices to show one for . Next to show existence of equilibrium for market it suffices to consider price vectors where due to Lemma 8, and therefore we consider the following set of possible price vectors.

Let us first handle trivial instances. It is easy to see that the feasible set of s in LP (8) at is a superset of the feasible set at any other prices . Therefore, for agent if , then she will not buy anything at any prices. In that case, it is safe to discard her from the market. Further, if there is an allocation satisfying Supply constraints for market such that , then we get a trivial equilibrium of where all the prices are set to zero; note that in this case zero prices also constitute an equilibrium of market by Lemma 9. To show existence for non-trivial instances, w.l.o.g. now on we assume the following for market .

Weak Sufficient Demand (WSD): If is such that , then , and there exists a good such that . Clearly, due to Lemma 8.

Lemma 10.

For any , is non-empty, and assuming WSD, .

Proof.

The first part of the proof is easy to see due to the extra good whose price is zero in . For the second part, to the contrary suppose for we have . By WSD assumption we know that for any , we have . Further, feasible set of LP (8) is at prices is a subset of the feasible set of this LP at zero prices. Hence we know that .

It must be the case that is not affordable at prices , i.e., . For , set . Since and both satisfy CC, so does . And since bundle is affordable at prices , thereby is feasible in . The delay at is , a contradiction to being optimal bundle at prices . ∎

Next we will construct a correspondence whose fixed points are exactly the market equilibria of . Let be the maximum possible demand of good ; we can compute by maximizing over the CC constraints of all agents . Define domain

Let . Define correspondence as follows where for a given , we have ,

| (10) |

The correspondence is well defined due to Lemma 10. If is a convex set, and graph of is closed, then Kakutani’s Theorem [34] implies that F has a fixed point, i.e., such that . Next we show the same.

Lemma 11.

Correspondence has a fixed point.

Proof.

Clearly, is a convex set since it is a cross product of solution sets of LPs. The lemma follows using Kakutani’s fixed-point Theorem [34] if graph of is closed.

Let for be a sequence of points in , and let be another sequence such that . Then essentially, and are solutions of LPs that are continuously changing with . Therefore, if and , then by continuity of parameterized LP solutions, we get that , implying graph of is closed. ∎

Lemma 12.

If is a fixed-point of then .

Proof.

Since , follows using Lemma 8. Among the rest of the goods, suppose, for we have . Let . Then the optimization problem of (10) is

The above quantity can be made more than by setting , and therefore optimal value is strictly more than . However, due to the fixed-point condition is a solution of the above, which implies , a contradiction. ∎

Lemma 13.

Assuming weak sufficient demand (WSD), if is a fixed-point of then and .

Proof.

For the first part, to the contrary suppose . Then since , and therefore by WSD condition . However . Therefore,

This contradicts the fact that is a maximizer of the above.

For the second part, to the contrary suppose , then . Further, due to Lemma 10 (together with the WSD assumption) we have , and therefore at maximum . Since is a maximizer of the above, .

However since , we get where is feasible in LP (8) at prices . Let be a demand vector when all the prices are zero. Due to Lemma 12 and WSD assumption we get that for some agent , . Let be this agent. This implies . Despite lower cost at she demands at prices , hence it should be the case that she can not afford at those prices. However, since is also not spending all the money at prices , there exists some such that she can afford at . Since both and satisfy the constraints of LP (8) for agent , so does . Thus, is a feasible point in LP, and , a contradiction to . ∎

Theorem 4.

If satisfies strong feasibility then it has an equilibrium.

Proof.

Due to Lemma 11, we know that there exists a fixed-point of correspondence . Let this be . We will show that it is a market equilibrium of . Clearly, optimal allocation condition is satisfied because . Market clearing remains to be shown, which requires: , and .

Clearly, at optimal solution of the above is non-zero only where is maximum. Since is a solution, if , then follows.

On the other hand suppose for all we have , then clearly the optimal value of the above is strictly less than . However since is a maximizer it implies that , a contradiction to Lemma 13. ∎

See 1

Remark 1.

C.1 Quasi-concave utility functions

In this section, we show that the preferences of agents in our model can be captured by quasi-concave utility functions. Notation: the symbol when used for vectors represents a co-ordinate wise relation, and represents that at least one of the inequalities is strict. Define the utility of an agent for an allocation to be the smallest delay of a feasible allocation dominated by , times :

If there is no that is feasible for Delay LP then the utility is . It is easy to check that this utility function is quasi-concave, and induces the same preferences as in our model.

Appendix D Special Cases

In this section, we show how several natural problems satisfy the extensibility condition (Definition 3) in Section 2.

Scheduling.

Recall the scheduling problem from Section 2.3. The agents are jobs that require different types of machines, and the set of machines of type is ; the machines are the goods in the market. Each agent needs units of machines in all of type , which is captured by the covering constraint . All agents experience the same delay from machine in type .

Lemma 14.

Scheduling problem satisfies the extensibility condition.

Proof.

Consider an arbitrary set of agents and an agent outside of this set. Let to be a feasible allocation that minimizes the total delay, i.e., . Since the delays are the same for each agent the total delay minimizes when the agents in gets units of machines of type with the smallest delay. Therefore, if we assign the next units of machines of type with the smallest delay to agent then would be the feasible allocation that minimizes the total delay. Therefore, this problem satisfies the extensibility condition. ∎

Restricted assignment with laminar families.

Lemma 15.

Restricted assignment with laminar families satisfies the extensibility condition if the following assumption holds for the instance

-

•

(Monotonicity) , such that then for each type .

Proof.

Since the requirement and variables for set of machines of each type is separate, it is enough to show this for .

Consider an arbitrary set of agents and an agent outside of this set .

Let .

Let to be a feasible allocation that minimizes total delay, i.e., .

For simplicity let such that .

Consider two agent and . Note that if and then such that we have and vice versa because s form a laminar family and the monotonicity condition.

Therefore, an optimal allocation allocates only a prefix of machines in .

Let’s assign to the next machines with smallest delay in subset .

We claim the new allocation is minimizing the total delay, i.e., .

Let’s prove the claim by contradiction.

Suppose the allocation is not optimal. Therefore there exists an optimal allocation with less total delay.

Suppose allocation has allocated machines 1 through in set and allocation has allocated machines 1 through in set .

Note that in allocation we can assume agent is getting the last machines in among the machines that has been allocated

in because if there exists agent that has allocation on the right side of the first machine that is allocated to then we can swap the allocations so the total delay wouldn’t change.

If then the delay of agent is the same in and . This is a contradiction because then it would conclude the total delay allocation

of is less than total delay of but we assumed is an optimal allocation for .

There are two cases.

Case1. . Consider allocation after removing agent . Since is getting the last machines it is easy to see the remaining allocation is optimal for . Since there are agents that have less allocation in in compare to .

Because of monotonicity assumption they have been allocated to machines with highest delay instead of available machines in . This is a contradiction with the fact is a optimal allocation for .

Case2. . This case is very similar to the last case. With the same argument we can argue that this case has contradiction with the fact is an optimal allocation.

∎

Network Flows.

Recall that in this setting agent wants to sent units of flow from to in a directed (graph) network where each edge has a capacity and cost per unit flow specified. Here edges are goods, and the covering constraints of agent has variable for each edge representing her flow on edge . The constraints impose flow conservation at all nodes except and , and that net outgoing and incoming flow at and respectively is .

Lemma 16.

A series-parallel network satisfies the extensibility condition.

Proof.

Consider an arbitrary set of agents and an agent outside of this set . Let to be a feasible min cost flow. Let’s remove the allocated capacities from the graph and allocate min cost flow of size to agent in the remaining graph. It is known that this greedy algorithm gives a min cost flow of size [3]. ∎

We can consider independent copies of any of these special cases above. E.g., each agent might want some machines for job processing, as well as send some flows through a network, but have a common budget for both together. Note that it would remain extensible because each copy is independent and extensible itself.

Appendix E Equilibrium Characterization

In this section we characterize equilibria of most general market instances. Recall that allocation of agent has to satisfy its covering constraints CC. Next we derive sufficient conditions for prices and allocation to be an equilibrium. As we discussed in Section 2, given prices the optimal bundle of each agent is captured by

It is well know that solutions of a linear program are exactly the ones that satisfy its complementary slackness conditions [50]. Let and be the dual variables of first and second of constraints in OB-LP(). Then, corresponding complementary slackness conditions are,

| (10) |

Here symbol between two inequalities means that both inequalities should be satisfied, and at least one of them has to hold with equality. Next, under a mild condition of sufficient demand (see Definition 4), we show that w.r.t. equilibrium prices . This would also imply that each agent spends all of its budget at equilibrium (thereby maximizing profit of the seller). We note that the following lemma is not needed for Theorem 3, but will be used to show the reverse result in Lemma 19, namely equilibrium prices and allocation gives solutions of the and for appropriately chosen parameter vector .

Lemma 17.

Let be an equilibrium of market satisfying sufficient demand, and for all let be the corresponding dual variables of OB-LP at . Then . In other words, every agent spends all her money at any equilibrium.

Proof.

Since is an equilibrium allocation, no good is over demanded. Therefore, we know that . Let be all zero price vector. By sufficient demand condition cannot be an optimal allocation of agent at prices . We will derive a contradiction to this if for some agent .

To the contrary suppose for agent , we have . Since , and satisfy complementary slackness conditions (11) of OB-LP() at prices , it is easy to see that they also satisfy these conditions at prices . This would imply that is an optimal allocation of agent at prices , a contradiction. ∎

Note that due to Lemma 17, it is no loss of generality to assume . We simplify the conditions with change of variables and , and write conditions for all the agents together.

| (11) |

At market equilibrium prices, every agent should get an optimal bundle, and market should clear, i.e., Supply constraints are satisfied and every good with positive price should be fully sold (see Section 2 for the formal definition of market equilibrium). Since optimal allocations at given prices are solutions of OB-LP() for each , they must satisfy (11). This follows from the fact that primal-dual feasibility and complementary slackness conditions are necessary and sufficient for solutions of a linear program. We get the following characterization.

Lemma 18.

If satisfies (11), and , then constitutes an equilibrium allocation and prices.

Motivated from Lemma 18 we next define parameterized LP that captures complementary slackness conditions of OB-LP for all the agents together. Suppose we are given ’s, let us define the following linear program parameterized by the vector, that we call , and its dual (same as (2) defined in Section 4):

Using the equilibrium characterization of Lemma 18 together with complementary slackness conditions between constraints of and , next we show that solutions of and exactly capture the equilibria if given appropriate value of parameter vector .

See 3

Proof.

Next we show converse of the above theorem under sufficient demand condition.

Lemma 19.

If market satisfies sufficient demand and is its equilibrium, then and gives solution of and respectively for some and .

Proof.

Due to optimal bundle condition of equilibrium we know that is an optimal solution of OB-LP() at prices . Let and be the value of corresponding dual variable in (10). Using Lemma 17 we have . Then it is easy to see using (11) that for and , satisfy complementary slackness conditions of and . Therefore the proof follows. ∎

Appendix F Missing Proofs and Details of Section 4

The proof of first theorem of Section 4, namely Theorem 3 is in Appendix E where we characterize market equilibria. Next we give proof of Lemma 1. For this we basically use the fact that any pair of primal, dual solutions of a linear program has to satisfy complementary slackness [50]. Recall the and of (2).

| (15) |

For any given , the optimal solutions of the , namely , and , namely has to satisfy the following complementary slackness conditions.

| (16) |

Recall that the symbol between two inequalities means that both inequalities should be satisfied, and at least one of them has to hold with equality. Also recall that for subset , we defined and , and for ease of notation we use when and similarly . Using this we first show a relation between and next.

Lemma 20.

For a given if and are optimal solutions of and respectively, while and are feasible in and then, such that,

Proof.

For feasible solutions we have and . Multiplying the two and summing over for each gives, . Another pair of constraints are and . Multiplying the two gives,

This gives the second part. Since optimal solutions satisfy complementary slackness, all inequalities satisfy with equality in the above for and we get the first part. ∎

Recall notation for any positive integer , and Definition 2 of an allocation being a subset of agents .

See 1

Proof.