Pricing Parisian down-and-in options

Abstract

In this paper, we price American-style Parisian down-and-in call options under the Black-Scholes framework. Usually, pricing an American-style option is much more difficult than pricing its European-style counterpart because of the appearance of the optimal exercise boundary in the former. Fortunately, the optimal exercise boundary associated with an American-style Parisian knock-in option only appears implicitly in its pricing partial differential equation (PDE) systems, instead of explicitly as in the case of an American-style Parisian knock-out option. We also recognize that the “moving window” technique developed for pricing European-style Parisian up-and-out options can be adopted to price American-style Parisian knock-in options as well. In particular, we obtain a simple analytical solution for American-style Parisian down-and-in call options and our new formula is written in terms of four double integrals, which can be easily computed numerically.

Keywords. Down-and-in options, American-style Parisian options, “moving window” technique, analytical solutions

1 Introduction

Barrier options are common path-dependent options traded in financial markets. One possible reason is that this kind of options provides a more flexible and cheaper way for hedging and speculating than vanilla options because the option buyers only pay a premium for scenarios they perceive as likely. The “one touch” breaching barrier, however, may have an undesirable feature of suddenly losing all proceeds (knock-out options) or suddenly receiving the embedded option (knock-in options) if the price of the underlying momentarily touches the asset barrier, no matter how briefly the breaching occurs. This opens up the possibility of market practitioners deliberately manipulating the underlying asset to force the cancelation or activation of the option. To partially remedy such a drawback, Parisian options are introduced, with a unique feature that the underlying asset has to continually stay above or below the asset barrier for a prescribed amount of time before the knock-out or knock-in feature is activated. This extended trigger clause can also be found in some derivative contracts, such as callable convertible bonds and executive warrants [5]. It is also worthwhile to note that Parisian options can be a useful tool in corporate finance [1].

Like the relationship between a vanilla American option and its European counterpart, the valuation problem of American-style Parisian options, in general, is much more difficult than that of their European-style counterparts. While a closed-form analytical solution of the latter has already been found by [15], a closed-form solution of the former only exists for the perpetual knock-in case (cf. [3]). In this paper, an explicit analytical solution for American-style Parisian knock-in call options is found after adopting the “window technique” developed in [15]. Our solution procedure can be extended to find analytical solutions of other types of Parisian knock-in options.

The paper is organized as follows. In Section 2, we introduce the PDE systems governing the price of Parisian down-and-in call options. In Section 3 the solution procedure is presented. Conclusion is given in the last section.

2 The PDE systems

One does not need to deal directly with the optimal exercise boundary in the evaluation of American-style Parisian knock-in options. This is because holders of an American-style Parisian knock-in option cannot do or decide anything until the option is activated. Moreover, once the “knock-in” feature is activated, the optimal exercise boundary of the option is the same as that of the embedded vanilla American option, the calculation of which has been thoroughly studied in the literature [10, 14, 13, 16, 4, 12, 7, 9, 6, 11]. In other words, the optimal exercise boundary does not appear explicitly before the option is knocked-in, and is already determined after the option being knocked-in. This suggests that the valuation of American-style Parisian knock-in options should be similar to that of European-style Parisian knock-in options and a simple analytical solution can be achieved.

Theoretically speaking, an American Parisian down-and-in call option will be knocked in and become the embedded American vanilla call if the underlying asset continually stays below the barrier for a prescribed time period . Otherwise, the Parisian down-and-in call option will be expired worthless.

For some extreme values of the “barrier”, one can easily observe an American Parisian down-and-in call option becomes worthless or degenerates to either a one-touch barrier option or a vanilla option. For example, if approaches zero, the option will be immediately “knocked in” once the underlying touches the barrier from the above, which is the same as the specification of a one-touch barrier call option with down-and-in feature. Similarly, it can be deduced that if is greater than the option life, , or approaches zero, the option values nothing. On the other hand, if approaches infinity and is less than T, the option price should be the same as that of the associated American call as the knock-in feature will be surely activated.

For other non-degenerate cases, the price of an American Parisian down-and-in call option is, however, not trivial. It depends on the underlying price , the current time and the barrier time , in addition to other parameters such as the volatility rate , risk-free interest rate and the expiry time . We now assume that the underlying asset with a continuous dividend yield follows a lognormal Brownian motion given by

| (2.1) |

where is a standard Brownian motion.

Based on the same financial arguments in [15], the pricing domains of those non-degenerated cases can be elegantly reduced as

Let and denote the option prices in the region and , respectively. Based on the definition of the option, the continuity condition of the option price and the “option Delta”, it can be shown that the option price should satisfy (cf.[15, 8])

| (2.2) |

where is defined on , and is defined on , operator , with being the identity operator.

One can observe that the above PDE systems are quite similar to those governing a European-style Parisian up-and-out call option. However, there are still several key differences. Firstly, it is obvious that the pricing domain of a Parisian down-and-in option is reversed from that of its up-and-out counterpart. Secondly, the knock-in feature makes the “terminal condition”, with respect to , become non-homogeneous in . This is because the option price is equal to that of the associated American call option, denoted by , at the time it is “knocked in”. Finally, we have the homogeneous boundary condition in when S becomes very large because in this case the option is never “knocked in”.

Albeit different, the above coupled PDE systems can be solved by adopting the “moving window” technique developed in [15]. In the next section, we shall briefly discuss the solution procedure.

3 Solution of the coupled PDE systems

We first replace the sum of the two partial derivatives appearing in , i.e., , by the directional derivative . As a result, the governing equation in the new coordinate system can be written as

| (3.3) |

where serves as a parameter, identifying the slide passing through the point . Furthermore, the constant can be absorbed by rescaling , i.e., , and (3.3) becomes

| (3.4) |

which is nothing but the BS equation!

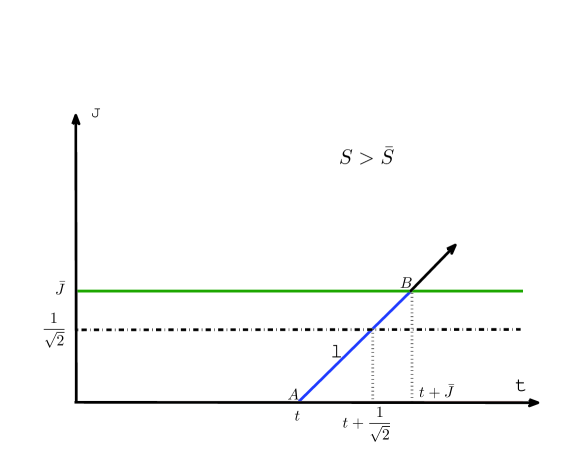

A 2-D diagram demonstrating the above coordinate transformation is shown in Fig 1, where the line denotes the projection on the plane of the slide passing through the point . From this figure, one can also observe that the solution in the new coordinate system is equal to in the original pricing domain . Particularly, let , we have .

Once all the boundary conditions in the new coordinate system are worked out accordingly, the 2-D PDE systems governing the price of an American-style Parisian down-and-in call option can be summarized as

| (3.5) |

where denotes the time-dependent function as . This unknown function that provides the coupling between the two PDE systems also needs to be solved as part of the solution. Here, is defined on , and is defined on .

To solve the newly established pricing system (3.5) effectively, we shall first non-dimensionalize all variables. In addition to the dimensionless variables introduced in [15], we further introduce:

With all primes and tildes dropped from now on, the dimensionless PDE system reads:

| (3.6) |

| (3.7) |

where is defined on , and is defined on , operator with being equal to .

By applying the Laplace transform technique as well as the Green function method, we obtain

| (3.8) |

where

Similarly, can be solved as

| (3.9) |

where and

Now, applying the connectivity condition (3.7) to (3.8) and (3.9), we obtain the integral equation governing as

| (3.10) |

which can be written as below after a new variable transform is introduced

| (3.11) |

It can be observed that the left hand side of (3.11) contains the information of from the expiry () to the current time to expiry, , while its right hand side involves the value of , with varying within , which coincides with the projection of the “slide” (a plane is of angle to both of the plane , and ) passing through on the plane . As in [15], we also name such a projection as a “window”. On the initial window, with varying within , the option price is the same as that of the standard American call and the value of is defined by .

By solving the integral equation (3.11) with varying within , we obtain the value of W in the first window, denoted by , as

It is quite interesting to observe that the last three terms in the above formula are identical to those in the corresponding formula for the European-style Parisian up-and-out call [15]. The differences are only in the first term, especially with the price of the standard American call appearing in the integrand.

Similar to the case in [15], for a state point , one can evaluate forwards, window by window, until the value at the required time is found. However, the determination of , assuming that the option price on the th window is known, is slightly different from that of . In fact, in the new coordinate system , solving with the known option price on the th window is equivalent to determining from the following PDE system:

| (3.13) |

| (3.14) |

Here , , with being equal to . Moreover, is defined on , and is defined on .

The non-homogeneous initial condition of the system makes its solution procedure more complicated than that of . However, using the Laplace transform technique and the Green function method, we have managed to derive its solution as

| (3.15) |

where

The corresponding integral equation governing is

| (3.16) |

which can be solved as

where .

Consequently, the analytical formula for is

There are several points that we should remark here. First, once is found, the price of an American-style Parisian down-and-in call option can then be calculated straightforwardly by means of (3.8) and (3.9). The calculation procedure for an American-style Parisian down-and-in call option is very similar to that for a European Parisian up-and-out call as presented in [15], except that we replace the value of the European vanilla option by the numerical value of its American counterpart, which is well documented in the literature. For simplicity, we do not present the calculation procedure in this paper. Second, from the above solution for an American-style Parisian down-and-in call option, we can immediately derive a closed-form solution for European-style Parisian down-and-in call option by replacing the value of the American vanilla call option in the above formulae of by the value of an European call. Third, using American-style Parisian put-call symmetry as in [3], the solution for an Parisian knock-in put option can be derived from the call counterpart.

4 Conclusion

In this paper, a simple analytical solution for American-style Parisian down-and-in call options is derived. This analytical solution can also be considered in a closed form if we suppose the value of embedded American vanilla call is known in advance. A key step of our approach is to apply the “moving window” technique developed in [15] to simplify the pricing domain, and consequently reduce a 3-D problem to two coupled 2-D systems. Our solution procedure can be easily extended to other types of American-style Parisian knock-in options.

References

- [1] C. Bernard, and O. L. Courtois, and F. Quittard-Pinon (2005) A new procedure for pricing Parisian options. The Journal of Derivatives 12, 45–53; doi: 10.3905/jod.2005.517185

- [2] F. Black and M. Scholes, “The Pricing of Options and Corporate Liabilities”, Journal of Political Economy 81 (1973) 637-654; doi: 10.1086/260062.

- [3] M. Chesney and L. Gauthier, “American Parisian options”, Finance and Stochastics 4 (2006) 475–506; doi: 10.1007/s00780-006-0015-3.

- [4] J. C. Cox and S. A. Ross and M. Rubinstein, “Option pricing: A simplified approach”, Journal of Financial Economics 7 (1979) 229 - 263; doi:10.1016/0304-405X(79)90015-1.

- [5] M. Dai and Y. K. Kwok, “Knock-in American options”, Journal of Futures Markets 24 (2004) 179–192; doi:10.1002/fut.10101.

- [6] B. Gao and J. Z. Huang and M. Subrahmanyam, “The valuation of American barrier options using the decomposition technique”, Journal of Economic Dynamics and Control 24 (2000) 1783 - 1827; doi: 10.1016/S0165-1889(99)00093-7.

- [7] D. Garcia, “Convergence and Biases of Monte Carlo estimates of American option prices using a parametric exercise rule”, Journal of Economic Dynamics and Control 27 (2003) 1855 - 1879; doi:10.1016/S0165-1889(02)00086-6.

- [8] R. J. Haber, P. J. Sch nbucher, and P. Wilmott, “Pricing Parisan Options”, The Journal of Derivatives 6 (1999) 71–79; doi:10.3905/jod.1999.319120.

- [9] S. D. Jacka, “Optimal Stopping and the American Put”, Mathematical Finance 1 (1991) 1–14; doi:10.1111/j.1467-9965.1991.tb00007.x.

- [10] I. J. Kim, “The analytic valuation of American options”, Review of Financial studies 3 (1990) 547–572; doi: 10.1093/rfs/3.4.547.

- [11] F. A. Longstaff and E. S. Schwartz, “Valuing American Options by Simulation: A Simple Least-Squares Approach”, Review of Financial Studies 14 (2001) 113-147; doi: 10.1093/rfs/14.1.113 .

- [12] K. Muthuraman, “A moving boundary approach to American option pricing”, Journal of Economic Dynamics and Control 32 (2008) 3520 - 3537; doi:10.1016/j.jedc.2007.12.007.

- [13] S. P. Zhu, “A new analytical approximation formula for the optimal exercise boundary of American put options”, International Journal of Theoretical and Applied Finance 09 (2006) 1141-1177; doi:10.1142/S0219024906003962.

- [14] S. P. Zhu, “An exact and explicit solution for the valuation of American put options”, Quantitative Finance 6 (2006) 229-242; doi:10.1080/14697680600699811.

- [15] S. P. Zhu and W. T. Chen, “Pricing Parisian and Parasian options analytically”, Journal of Economic Dynamics and Control 37 (2013) 875–896; doi: 10.1016/j.jedc.2012.12.005 .

- [16] S. P. Zhu and Z. W. He, “Calculating the early exercise boundary of American put options with an approximation formula”, International Journal of Theoretical and Applied Finance 10 (2007) 1203-1227; doi:10.1142/S0219024907004615.

- [17] S. P. Zhu and N. T. Le and W. T. Chen and X. P. Lu, “Pricing Parisian down-and-in options”, Applied Mathematics Letters 43 (2015) 19 - 24; doi: 10.1016/j.aml.2014.10.019.