Second Order Calibration: A Simple Way to Get Approximate Posteriors

Abstract.

Many large-scale machine learning problems involve estimating an unknown parameter for each of many items. For example, a key problem in sponsored search is to estimate the click through rate (CTR) of each of billions of query-ad pairs. Most common methods, though, only give a point estimate of each . A posterior distribution for each is usually more useful but harder to get.

We present a simple post-processing technique that takes point estimates or scores (from any method) and estimates an approximate posterior for each . We build on the idea of calibration, a common post-processing technique that estimates . Our method, second order calibration, uses empirical Bayes methods to estimate the distribution of and uses the estimated distribution as an approximation to the posterior distribution of . We show that this can yield improved point estimates and useful accuracy estimates. The method scales to large problems - our motivating example is a CTR estimation problem involving tens of billions of query-ad pairs.

1. Introduction

Suppose we have a regression problem: we have responses and covariates for items , and we want to estimate a parameter for each item using our responses and covariates. We often want a posterior distribution for each , but common regression methods, like neural networks, boosted trees and penalized GLMs, only give us point estimates . In this paper, we show how to post-process any regression method’s point estimates to get an approximate posterior.

Our motivating problem is click through rate (CTR) estimation for sponsored search (Richardson et al., 2007). Here, our items are query-ad pairs, and for each pair, we know the number of times it was shown (the number of “impressions”, ), the number of times it was clicked (), and covariates that describe the query, ad and match between them, (). We assume the clicks for each query-ad pair follow a Poisson distribution:

and want to estimate , the CTR for the query-ad pair. A complex machine learning system gives us point estimates . We want a posterior distribution for each . Among other things, we could use these posteriors to make fine-grained accuracy estimates and explore-exploit tradeoffs.

Any method to get posteriors for the CTR problem has to have three important features. First, it has to scale. Search engines have billions of query-ad pairs. Second, it cannot depend on the underlying machine learning system that gives . CTR estimation systems are complex - not least because of their scale - and are constantly being improved (Graepel et al., 2010). If a method used detailed knowledge of the system to get posteriors, it would have to account for all the complexity and be updated constantly as the system changed; we also wouldn’t be able to use its posteriors to compare the system to a very different competitor. Third, the method must share information across query-ad pairs. Because of the long-tail nature of search queries, most query-ad pairs are shown a small number of times. This, combined with CTRs that are generally low, means that taken individually, most query-ad pairs have little information.

We get approximate posteriors by extending the idea of calibration, a common post-processing technique that removes bias from regression estimates. There are a few different methods for calibration, but all are based the same idea: instead of using , estimate and use (we’ll drop the subscripts from now on, when the meaning is clear). In the CTR estimation problem, for example, we can estimate using the average CTR of query-ad pairs with close to . Calibration can improve any regression method’s estimates by removing any aggregate bias. This lets us use methods that, because of regularization, other bias-variance tradeoffs, or model mis-specification, are efficient but biased. We can also use calibration to turn scores, that are not estimates of but have information about , into estimates of without aggregate bias. Finally, calibration satisfies the three requirements for the CTR estimation problem - it scales easily, it doesn’t depend on the underlying system, and it shares information by using all the items with a similar to estimate the correction at that .

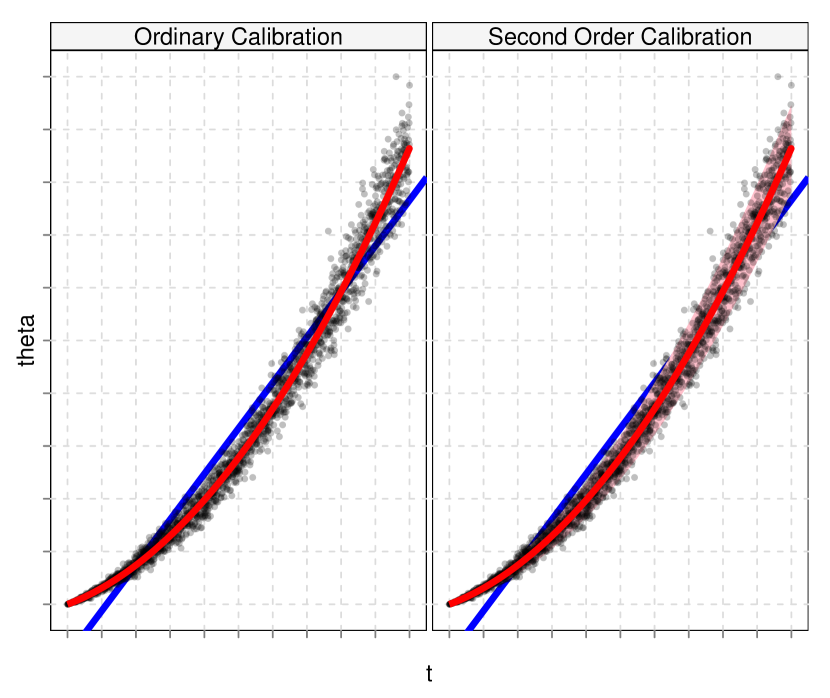

Calibration estimates . We propose estimating the distribution of , and using this to approximate the distribution of . Figure 1 illustrates the idea by plotting vs . Calibration adjusts our estimate, as a function of , by moving from the line to the conditional mean curve . The proposed method, which we call second order calibration, goes further and estimates the distribution of around that curve. We don’t observe the true , so we can’t estimate the distribution of directly. But if many items have an estimate close to , we can estimate the distribution by using the observed s for those nearby items and employing standard empirical Bayes techniques. Like ordinary calibration, our method can also be used when is a score that has information about , rather than itself an estimate of , though for this paper, we assume is an estimate of .

How is this useful? Although we think approximate posteriors will be useful in many ways, we focus on three applications: overall accuracy estimation, improved point estimates, and fine-grained accuracy estimation.

Overall Accuracy Estimation

Second order calibration estimates , which measures the accuracy of the estimation system (if is a score, this measures the accuracy of the calibrated score). This lets us separate errors due to noise, which would happen even with perfect parameter estimates, from errors in estimation. Separating these errors can be valuable. For example, consider the CTR estimation problem. Because of the Poisson noise, we cannot make perfect predictions even if we estimate perfectly for each query-ad pair. If we have an estimation system that predicts badly, second order calibration can tell us whether this is because the system is inaccurate and can be improved, or whether it is predicting as well as the noise will allow.

Improved Point Estimates

Second order calibration can improve point estimates through better shrinkage. Suppose that for each item , is trained on data independent of ; we can do this by dividing our data into multiple folds, like in cross-validation, and would need to do this anyway for ordinary calibration. Ordinary calibration improves on by using instead. We can do even better by using . This estimator essentially decomposes memorization and generalization. The underlying regression method handles generalization: the distribution of reflects what we know about based on , the underlying regression method’s summary of the information in and the other items. Second order calibration then handles memorization by combining with the item-specific information in . By estimating the distribution of , we can often combine the two sources of information close to optimally. Requiring not be trained on makes sure we don’t double count the information in . In practice, this condition can be relaxed: can be trained on as long as does not influence too much.

Decomposing memorization and generalization can be much better than letting the underlying estimation system train on all the data and handle both memorization and generalization. More interestingly, we could design our estimation system to work with this decomposition. For example, we could use a relatively coarse generalization model to generate and memorize item-specific information using .

Fine-Grained Accuracy Estimation

Second order calibration can estimate our accuracy for each item. Again, suppose is trained on data independent of for each (or, in practice, that does not influence too much). We can use to measure the accuracy of , and as a general measure of how much we know about each item. Second order calibration gives us estimates of , which we can use to make risk-adjusted decisions and explore-exploit tradeoffs, or to find where the underlying regression method is particularly good or bad.

Worries and Limitations

We might worry that there just isn’t enough information in the s to get a useful estimate of the distribution of . If this were true, second order calibration could never be useful. Fortunately, this is not the case for each of the three applications above. We prove as long as our estimate of the distribution of fits well, second order calibration will correctly estimate the true , and . We discuss a simple diagnostic to check the fit.

Like ordinary calibration, second order calibration is intended to be easy and useful, not comprehensive or optimal, and it shares some of ordinary calibration’s limitations. Both ordinary calibration and second order calibration require that each be trained on data independent of . This is easy to achieve in principle with folds, but can be inconvenient; in practice, both methods work well if does not influence too much. Both methods can also be wrong for slices of the data while being correct on average, since they only use through . This is especially important for second order calibration, since we always approximate using . We can guard against this by calibrating separately for important classes of items (for example, we can calibrate CTR estimates separately for each country), but that cannot solve the problem completely.

Second order calibration also has another important limitation, not shared with ordinary calibration: we must have a known parametric model for the distribution of . In our CTR example, for instance, is assumed to be , with known. We need to know the noise mechanism to work backward from the observed distribution of the s to the distribution. It can be hard to check whether our noise model is accurate - in our CTR example, we use predictive distributions to check the Poisson model indirectly. Also, although we expect second order calibration to work well for fairly general known noise, our theory only applies when the noise is Poisson or a continuous natural exponential family (e.g. normal with known variance).

The rest of this paper is organized as follows. We discuss related work in Section 2. We then present our method for second order calibration in Section 3, using CTR estimation to illustrate. In Section 4, we state a theoretical result justifying the three applications of second order calibration mentioned above. Finally, in Section 5, we present our results on the CTR estimation problem and on simulations. Proofs are in Appendix A.

2. Related work

Second order calibration is closely related to existing calibration and empirical Bayes methods.

2.1. Calibration

Calibration is usually used to post-process the output of good classifiers that produce bad class probability estimates (Niculescu-Mizil and Caruana, 2005). Cohen and Goldszmidt (2004) show that, in general, calibration does not reduce classification accuracy, and makes it easier to find the right threshold to minimize classification error. Calibration can be very effective: Caruana and Niculescu-Mizil (2006) show that it turns boosted trees into excellent probability estimators. The two most common methods for calibration are Platt scaling (Platt, 1999), which is equivalent to logistic regression, and isotonic regression (Zadrozny and Elkan, 2002).

Most of the literature on calibration discusses classifiers, but regression methods are commonly calibrated as well. Both isotonic regression and Platt scaling generalize straightforwardly to calibrating regression methods. Amini and Johnson (2009) use random effect methods to calibrate and estimate the accuracy of regression methods.

2.2. Empirical Bayes

Empirical Bayes methods use Bayesian inference to solve problems, but estimate priors instead of using subjective or reference priors. The key idea is that if we have many independent draws from a model with unknown prior, we can use the data to estimate the prior, or a quantity of interest that depends on the prior.

For example, suppose that comes from an unknown prior , our data is , and we observe many s from this model. We want to say something about the unobserved corresponding to each . As Robbins (1954) showed, we can use the s to estimate the prior, then estimate using , where is the expectation in our model under the estimated prior . This estimate of combines global information from all the s (via ) with the specific information in .

Emprical Bayes methods work when the quantity we’re interested in can be expressed in terms of the marginal density of the data. Such an expression tells us we can estimate the quantity, since we can estimate the marginal density using our data. In our normal example, Tweedie’s formula (Robbins, 1954) shows that if is the marginal density of the s,

for any prior (Robbins actually estimated this quantity directly instead of using an estimate of the prior). Since we observe many s, we can estimate the marginal and thus estimate without knowing the prior in advance.

Empirical Bayes methods need a large amount of data to shine. Big data sets have made them increasingly useful; Efron (2010) gives an introduction and review. They have enjoyed particular success recently in signal processing (e.g. (Johnstone and Silverman, 2004)) and multiple testing (though false discovery rates, e.g. (Efron et al., 2001)).

2.3. Why not bootstrap?

At first glance, the bootstrap seems like a natural way to get approximate posteriors for any regression method. Before we present second order calibration, it is worth understanding why the bootstrap doesn’t work for this problem. The bootstrap is often too slow for large data sets, since it requires training the regression method many times. In the CTR estimation problem, for example, bootstrapping would require training a massive, resource-intensive machine learning system tens or even hundreds of times. This is impractical and expensive. Post-processing methods like ordinary and second order calibration are much easier to use.

More importantly, though, the bootstrap estimates the distribution of , not of , and these distributions can be very different, particularly for the biased estimators often used on large data sets. Consider the trivial estimator . The bootstrap would correctly find that is always , but this tells us nothing about the distribution of .

3. The Proposed Method

We now state the second order calibration problem more precisely. We are given responses for items . Each item has a parameter that controls the response in a known way: , where is a given parametric family. The family can depend on known offsets that are different for each ; we suppress this dependence in our notation. We assume that is either Poisson () or a continuous exponential family with natural parameter (for example, with known ). For each item , a machine learning system gives us an estimate that is not trained on . Our goal is to estimate the posterior distribution , which we denote by , for each .

We will use to approximate the full posterior distribution . The quality of this approximation will depend on the underlying machine learning method and the data set. In this paper, we will not try to quantify the approximation error. Our goal is to estimate functionals of the true , which average the true distributions, in the same way that ordinary calibration estimates , not , and is content to be correct on average.

3.1. In a Nutshell

The proposed method has five steps:

-

(1)

Bin the items by , so that is approximately constant in each bin.

-

(2)

Estimate separately for each bin. Assume is constant in the bin, so the observations in the bins are drawn from the model

(1) where is the common value of for items in the bin. Choose a parametrization for , and estimate by maximum marginal likelihood. Do this in parallel for all the bins to get an estimate for each bin.

-

(3)

Collect the . If necessary, adjust them so that and are smooth functions of . Here, and denote the expectation and variance in Model 1, above, with prior .

-

(4)

Check the fit. When plugged into Model 1, the adjusted should lead to marginal distributions of that fit the data.

-

(5)

Calculate the overall calibration curve , overall accuracy curve , updated estimates and fine-grained accuracy estimates .

If the items naturally fall into coarse categories, we can follow these steps separately for each category. For example, in the CTR estimation problem, we can treat the query-ad pairs for each country separately.

In the rest of this section, we discuss each step in more detail, illustrating with the CTR estimation problem.

3.2. Step 1: Binning by

Binning the items by is straightforward - simply divide the range of into bins. The only questions are how to choose , and how to set the bin boundaries. Using quantiles of the distribution of for the bin boundaries seems to work well. This gives bins with the same number of items.

Choosing is a bias-variance tradeoff: each bin has to be small enough so that is approximately constant in each bin, but big enough so that we have enough data in each bin to estimate . Because we later smooth our estimates of across bins, the choice of bin width is not crucial, as long as it is in a reasonable range. For CTR estimation, we tried different choices of and judged them by how wide the bins were and how stable the fitted were. In the end, we found that a range of s all gave reasonably well-behaved , and, for maximum parallelism, chose the largest reasonable .

3.3. Step 2: Fitting for each bin

We now work within a single bin. Within this bin, is approximately constant, so all the are all approximately the same distribution, . This means that the data in the bin approximately come from the model

We estimate by giving it a convenient parametrization and estimating the parameters by maximum marginal likelihood. That is, we maximize the marginal log-likelihood

where the sum is taken over the items in the bin, and

is the marginal density of that corresponds to . The distribution depends on (through the bin) and on any known offsets in , but our notation suppresses this.

In the CTR estimation problem, for example, we model using a Gamma distribution. This makes negative binomial, with mean and dispersion that depend on and the shape and scale of . We fit ’s shape and scale by finding the values that maximize the negative binomial likelihood.

How should we model ? The theoretical results in Section 4 show that the details of the choice aren’t too important, at least for the applications in this paper. What matters is that leads to a marginal distribution that fits the observed data; that guarantees the final results will be correct on average. This means we should choose the simplest, most convenient model for that fits the data.

We recommend first trying to model as a conjugate prior. If that proves too restrictive, we recommend modeling as a mixture of conjugate priors, using the simplest model necessary to fit the data (use the fewest or otherwise most constrained mixture components). Conjugate prior mixtures and similar nonparametric maximum likelihood methods often perform well in empirical Bayes problems (Kiefer and Wolfowitz, 1956; Muralidharan, 2010; Jiang and Zhang, 2009). They are flexible enough to fit any distribution, with enough components, but can still be manipulated using conjugacy formulas. For the CTR estimation problem, we tried two models for - a simple Gamma distribution, and a mixture of Gammas. For the latter, we fixed the mixture components and fit the weights using the standard EM algorithm for mixtures. We found that a single Gamma distribution fit our data well (Subsection 5.1 examines the fit).

Our method scales to large data sets easily because we find separately for each bin, with no communication between bins. This lets us find for all the bins in parallel. Since we only need (and for CTR estimation) for items in a bin to find , each bin can usually be handled by one machine and that makes parallelization especially easy.

3.4. Step 3: Adjusting if necessary

The disadvantage of fitting in each bin separately is that may not vary nicely with . For example, and may not be smooth functions of . We may also want to be a monotone function of . Sometimes this isn’t a problem - if we have enough data in each bin, the can vary nicely enough with even though we haven’t constrained them to do so.

If not, though, we can fix the problem by smoothing or monotone regression. For CTR estimation, we used smoothing splines to get smoothed versions of and , as functions of , then adjusted the so their means and variances matched the smoothed and . To make sure stayed positive, we shifted and scaled the distributions of instead of .

3.5. Step 4: Checking the fit

Our theoretical results show that we must fit the marginal distribution of the data well to get good results. This means we need to check the marginal fit before we use the . Let be the marginal distribution of in the within-bin model (, ). The distribution depends on any known offsets in , but our notation suppresses this. We need to check that the s fit the observed s.

There are many ways to assess the fit of a collection of distributions (see (Gneiting et al., 2007) for a discussion of different criteria, in the context of predictive distributions). We suggest using the standard probability integral transform, randomized to account for the discreteness of . Let

where is independent of , and is probability under . Each is if and only if is the true distribution of , and the more non-uniform is, the more differs from the true distribution of (Muralidharan et al., 2012).

We check the fit of the by looking at the observed distribution of the s in each bin. If the s are non-uniform in a bin, then does not fit the data in that bin well. When this happens, the shape of the histogram often suggests a solution. For example, a U-shaped histogram says that is too light-tailed, since we see more large and small s than predicts. If the s are uniform in each bin, our fits are at least correct on average, so the theory says we can expect reasonable results.

3.6. Step 5: Calculating useful quantities

Armed with , we can now compute the overall calibration curve , overall accuracy curve , updated estimates and fine-grained accuracy estimates . These can all be computed quickly in closed form if is a conjugate prior or conjugate mixture. Each quantity only involves , and a known offset like for one item, so we can treat the items in parallel.

4. Theoretical Support

We now present a simple theoretical result that says second order calibration will give us good estimates of , , and as long as we fit the marginal distribution of .

The result tries to address two worries. First, we might worry that the s just don’t have enough information to estimate the quantities we are interested in. For example, suppose , and we tried to use the s to estimate . This is essentially impossible: we will never have enough data to choose between the two distributions and for small enough , since they produce very similar marginal distributions of , but the two distributions lead to very different estimates of . We need to show that second order calibration does not fall into the same trap.

Second, we might worry that the exact model we use for will strongly influence our results. If so, this would be a serious problem, since we have no principled way to choose between two models that fit the data equally well.

It turns out that neither of these worries is a problem, at least when is Poisson or a continuous natural exponential family. The ’s have enough information to estimate , , and , and any model for that fits the data well will give similar estimates for these four quantities.

This happens because each quantity can be written in terms of the marginal distribution of . We can learn the marginal using data, and models with the same marginal give the same estimates. For example, Robbins (1954) shows that if ,

where , and is the marginal distribution of in Model 1 (for simplicity, we drop the in the subscript instead of writing ). We can express and in terms of the marginal by taking the expectations of and over and using the conditional variance identity. Similar formulas for continuous natural exponential families are in the Appendix.

There is one caveat that is theoretically important, though not practically. The formulas all involve dividing by , so they can behave badly if is close to zero. If our estimated gives a marginal with light tails, our estimates can behave badly. To guard against this problem, we can regularize our estimates by dividing by instead of by , where is a tuning parameter (Zhang, 1997). This is slightly unnatural, but the resulting regularized estimators actually have some nice properties that we discuss in the Appendix. We find regularization unnecessary in practice - the that fit our data usually aren’t light-tailed. Should we need to regularize, we can choose to maximize the predictive accuracy of the regularized estimator on a test set.

Theorem 1 makes this marginal distribution argument more precise. Building on regret bounds in the empirical Bayes literature (Jiang and Zhang, 2009; Muralidharan, 2011), it bounds the error in our estimates of and in terms of our error in estimating the marginal density and its derivatives, plus a regularization term that vanishes as . Because we can use these to get and , the theorem implies that the error in our estimates of the latter two can also be bounded in terms of our error in estimating the marginal.

Bounds like the ones in the theorem can be used to find rates of convergence for empirical Bayes estimators, but we think it serves better as motivation and a sanity check for second order calibration than as a technical tool. Its bounds are for the regularized estimates; the regularized and unregularized estimates are usually very close, but for completeness, we give bounds for the unregularized estimates in the Appendix. The Appendix also has error bounds for estimates of higher cumulants, like the skewness and kurtosis.

We measure error using the norm, weighted by : . For the Poisson, the theorem gives bounds for and , which is clearly equivalent to bounding the errors for and .

Theorem 1.

If is , the regularized posterior moment estimators have error at most

where , are constants that only depend on , (not the same from line to line), and .

If is a continuous natural exponential family, the regularized posterior moment estimators have error at most

where , , are constants that depend on , (not the same from line to line) and . also depends on through .

5. Results on Real Data and Simulations

We now show that second order calibration performs well on real and simulated CTR data, and on a simulated normal data set. For each data set, we show the fitted and the histogram that checks for model fit. We then show that second order calibration can estimate , , and well, and that the second order calibrated estimates often significantly improve on the original estimates and the first order calibrated estimates . Note that because the bootstrap was computationally impractical and doesn’t estimate what we are interested in, we did not include it as a baseline.

5.1. Real CTR data

We first illustrate our method with real CTR data, with clicks and impressions for more than 20 billion query-ad pairs. For each query ad-pair, we also have , an estimate of the CTR generated by a black-box regression method. The CTR estimates are actually generated for each impression, and we sum them to get an overall for each query-ad pair. This induces a slight dependence between and - although the predictions and response are independent at the impression level, the prediction for an impression may depend on previous responses, and this creates dependence at the query-ad level. This dependence is small for most query-ad pairs, so we ignore it.

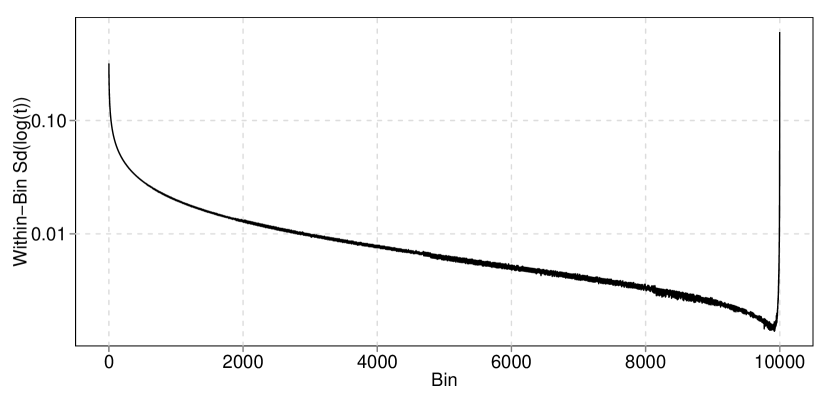

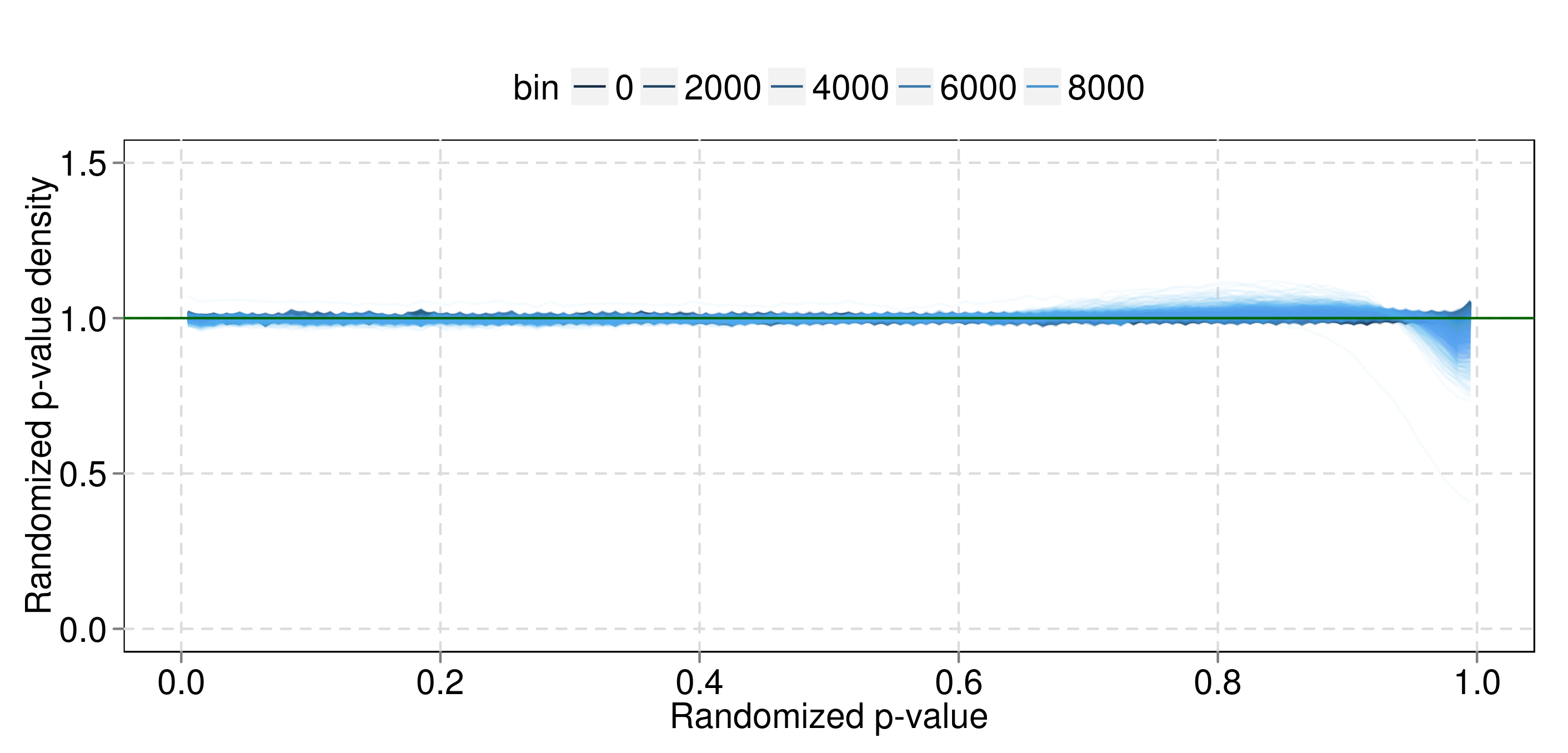

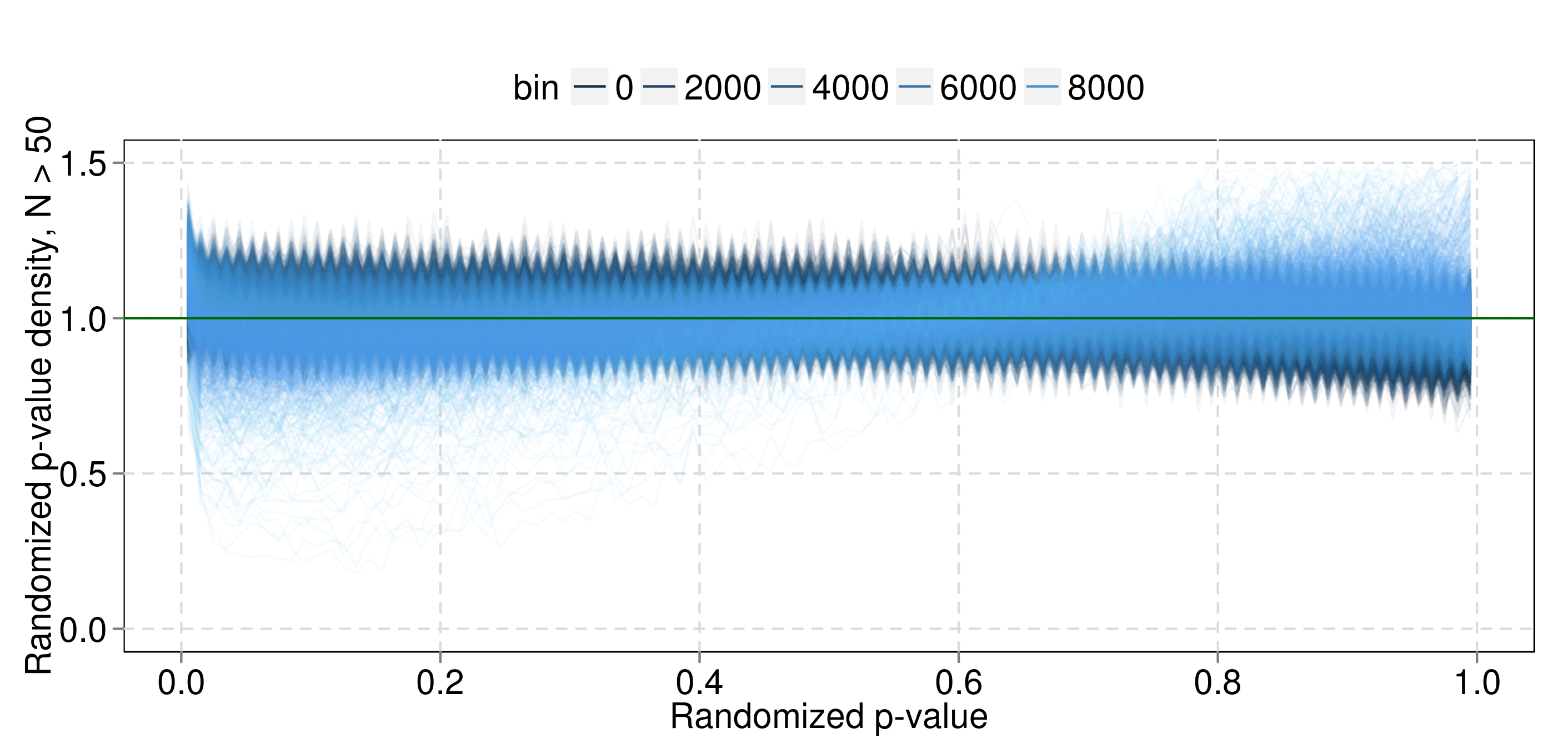

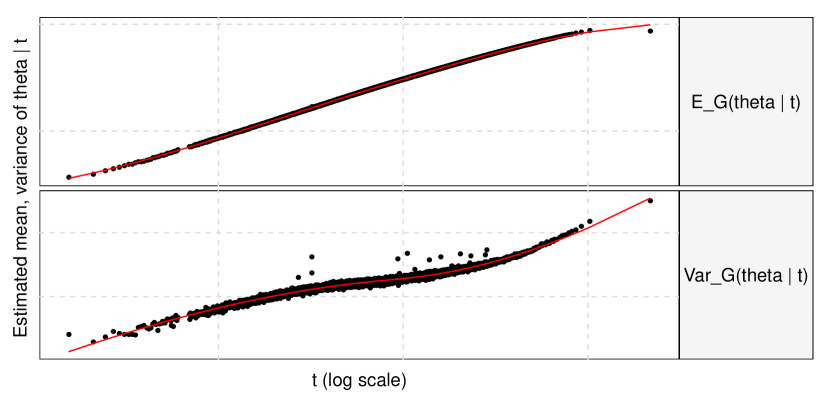

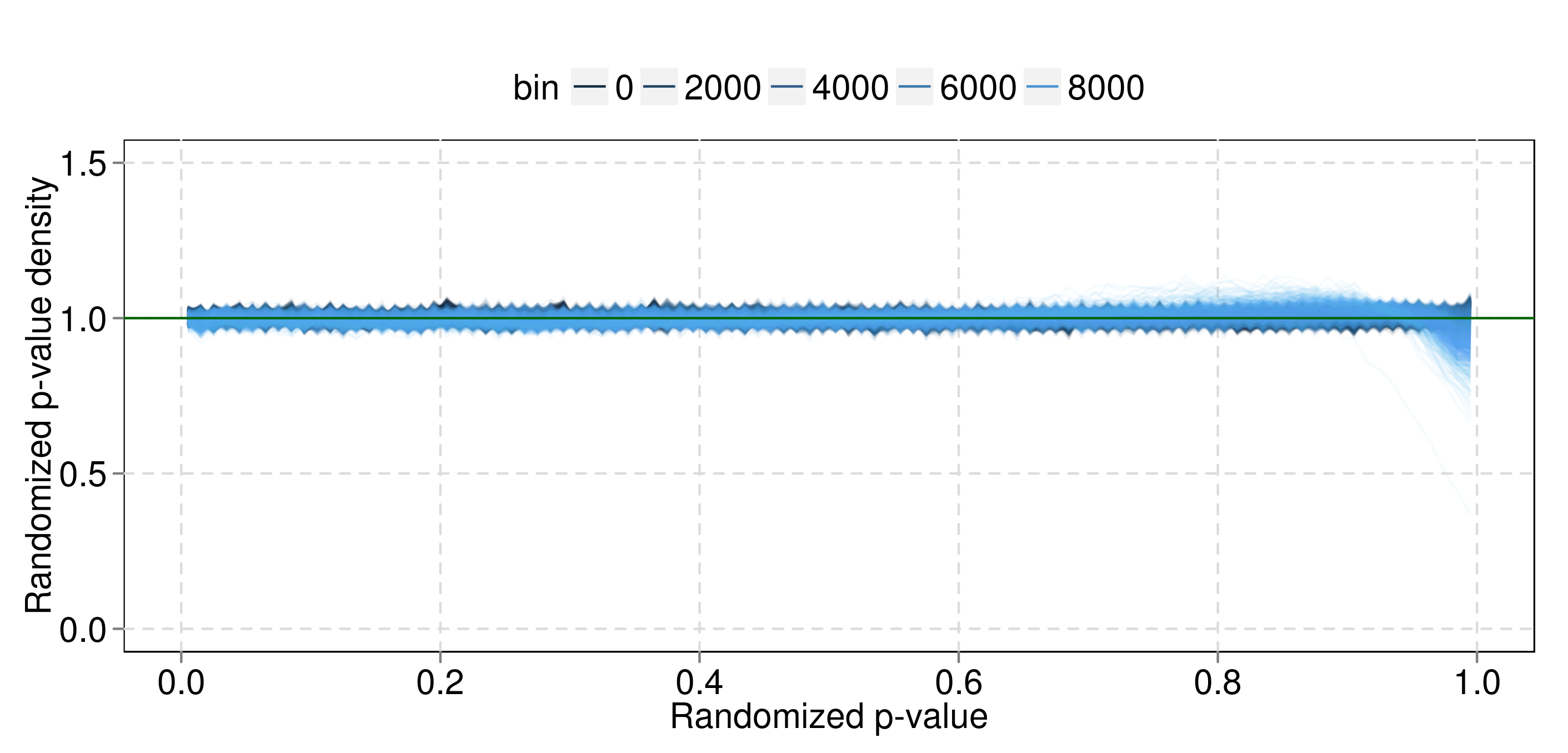

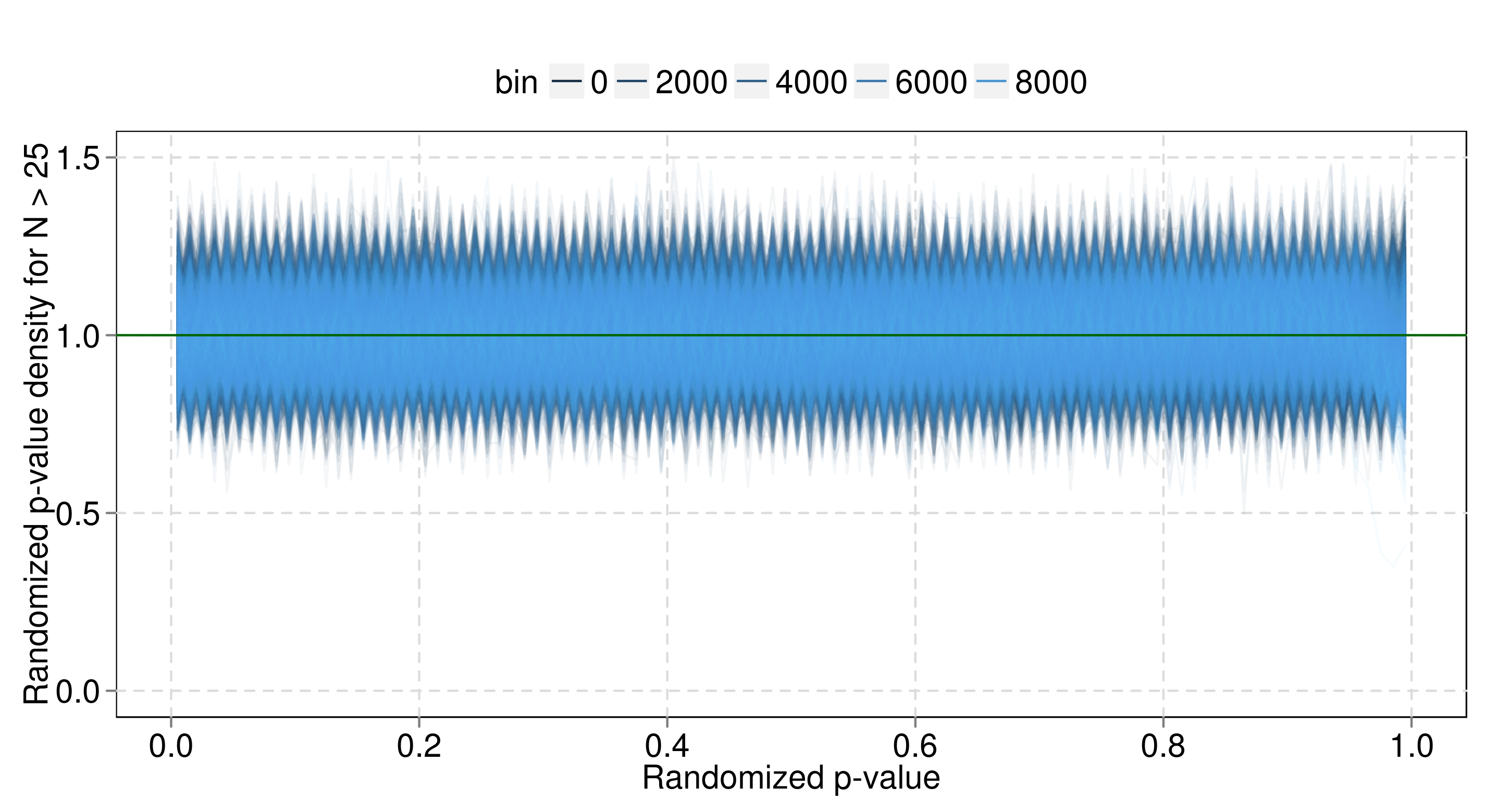

We divided the query-ad pairs into 10,000 bins, each with an equal number of clicks. Within each bin, was approximately constant: usually had a standard deviation of less than , but the left and rightmost bins are much wider (Figure 2). We tried two models for - a Gamma distribution, and a mixture of Gamma distributions with fixed gamma parameters (chosen to have equispaced mean and equal variance on the log scale). Figure 3 shows the histograms for the single Gamma model. The s are mostly uniform, indicating that the model fits well; the densities are slightly skewed right, indicating that our don’t have quite enough mass on the right tail. The fit is also poor in the very rightmost bins. The histograms have little power when is small, since any sensible will give a marginal density of concentrated at . To make sure we aren’t just seeing this zero-effect, we also looked at the histogram for query-ad pairs with , where we have more power to detect if our model fits badly (Figure 4). These looked similar, indicating that our model actually fits the data well for most bins. Based on this, we used a single Gamma model for the rest of our analysis.

Figure 5 shows the fitted , as functions of . The , curves are nicely behaved, but the variance is noisy. We smoothed the curves and adjusted the accordingly (we actually smoothed , to make sure the stayed positive). Figure 6 shows the adjusted . We used the adjusted to get , , and , where

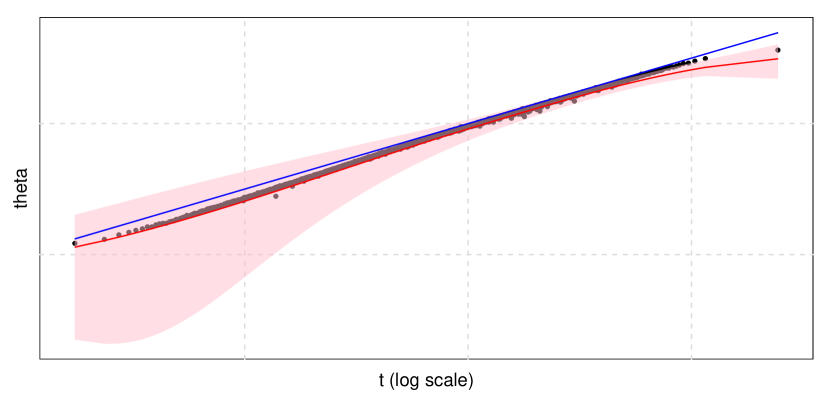

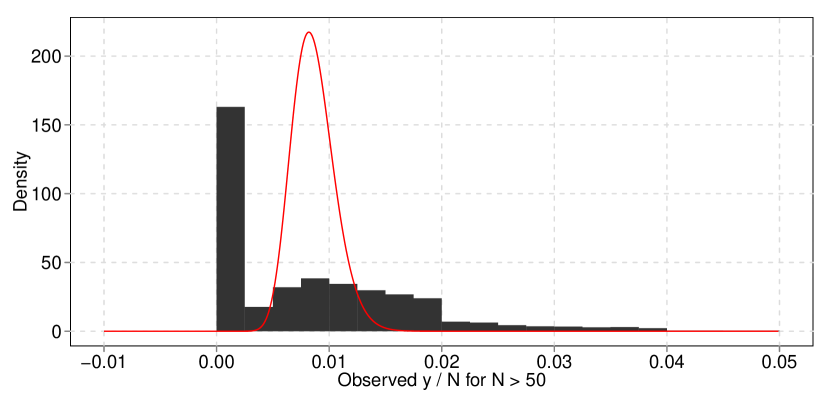

and are the adjusted (the other expectations and variances are defined similarly). Figure 7 shows for the middle bin, along with for the query-ad pairs with . is centered at about the center of the histogram, but is narrower and smoother. The histogram also has a big spike at . The marginal -histograms fit well, indicating that while does not have any mass at , it captures this spike when we add Poisson noise to get the distribution of .

Evaluating these estimates is tricky since we do not know the true CTRs. We cannot directly measure how well the point estimates match , or check that accurately estimates the distance between and Instead, we evaluate our estimates by using them to make predictions and predictive intervals. We randomly divided the impressions for each query-ad pair into training () and test () sets, and tried to predict the test data using the training data.

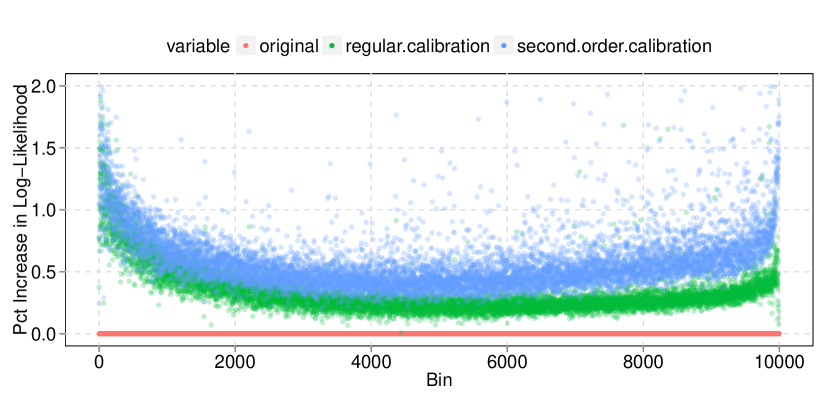

Second order calibration significantly improves our point estimates. We judged the point estimates , and by their test set likelihood (under the assumed Poisson noise). Figure 8 shows the improvement in test set likelihood for each bin. Both ordinary and second order calibration increase test set likelihood in each bin, and help more as we move away from the center. Overall, using , the ordinary calibration estimate, instead of increases the test set likelihood by , and using the second order calibration estimate increases the test set likelihood by . This is a substantial increase, given the difficulty of CTR estimation and the degree to which has been optimized. For comparison, using a constant, naive estimate for all items (the average CTR in the middle bin) gives a a test set likelihood lower than .

We used the fit of the predictive distributions to judge the accuracy of . The predictive distributions are wider when is large and shorter when is small, so if the predictive distributions match the data, is probably measuring uncertainty well. We assessed the fit of the predictive distributions with -histograms like the one we used to check the fit of the marginal distribution. Figures 9 and 10 show that the predictive distributions fit well, both on the all the query-ad pairs, and those with in the test set. The fit suggests that our estimates are accurate enough to be useful.

The fit of our point estimates and predictive distributions also suggests that our Poisson model is approximately correct. To get the predictive distributions right, we need to divide the variance of into signal () and noise (). If we underestimate the noise, for example, our estimate for will be too high. This means we will undershrink - our point estimates and will be too close to , and our predictive distributions will be mis-centered. The fit of our predictive distributions indicates that our model is putting about the right weight on signal and noise.

Second order calibration gives us some interesting model-dependent estimates of performance. For example, we can use the model to estimate the fraction of the variance of explained by :

where

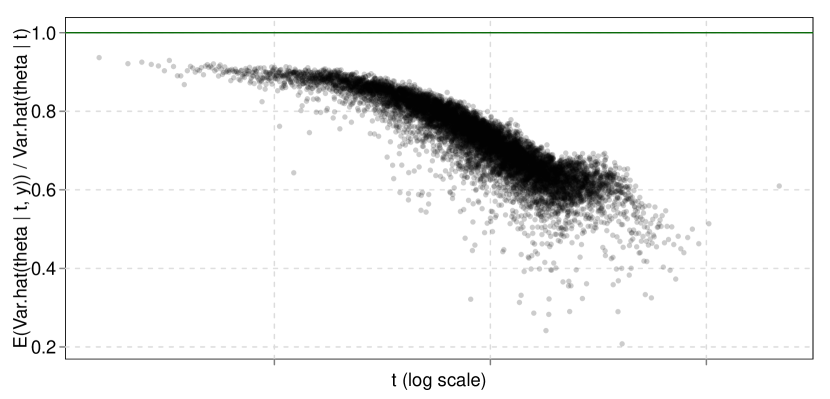

is the overall variance of , estimated using the conditional variance formula and the fitted mean and variance of in each bin. For the CTR data, was around , indicating that is a strong predictor of . We could use to compare different candidates for (Amini and Johnson (2009) use a similar metric based on a random effects model). We can also use the model to estimate how much second order calibration lowers the variance in our estimate of . Figure 11 plots for each bin, where the expectation is weighted by in the test set. Averaged over bins, this ratio was about , which says that second order calibration gives us a mean squared error about less than ordinary calibration. The figure shows that the variance reduction is biggest in the high- bins; this makes sense, since query-ad pairs in those bins have more clicks, and thus more information about . Although these performance estimates are model-dependent, and could be wrong because of model misspecification, the fit and predictive distribution checks above mean that the estimates are trustworthy enough to be interesting.

5.2. Simulated CTR data

Next, we tested our method on simulated CTR data that was based on our real data set. We used the same and , generated true lognormally around with some bias and variance, and generated new clicks:

We used the same fitting method as for real data (so we had around 2-3 billion query-ad pairs), and looked at the results for different values of and . To make computation easier, we used every tenth bin instead of every bin.

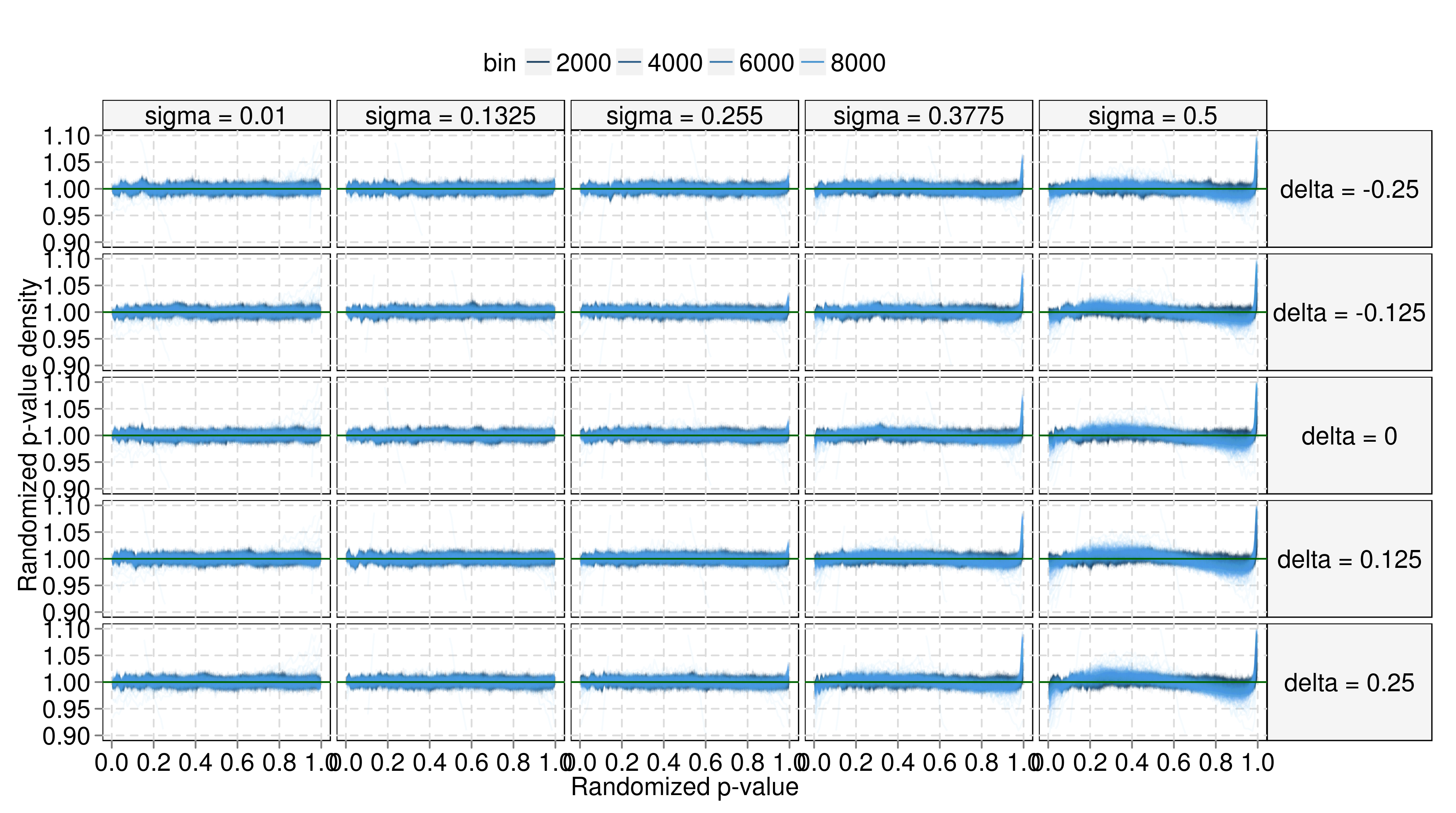

Figure 12 shows that a Gamma model for fit the simulated data reasonably well - not surprising, since the Gamma distribution approximates the lognormal distribution well when is small. The Gamma model doesn’t quite fit the data when is large. We smoothed as before and calculated , , and .

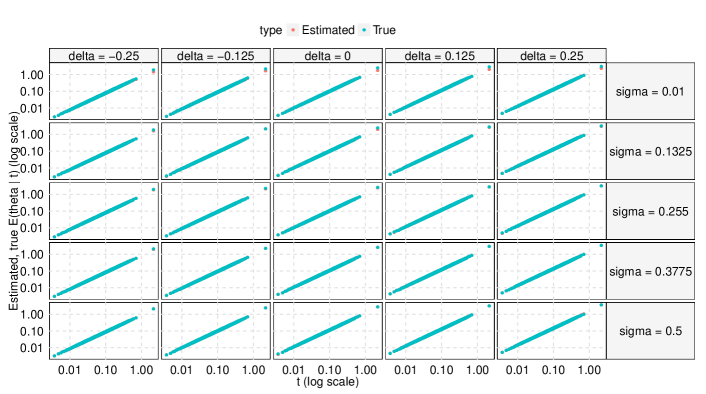

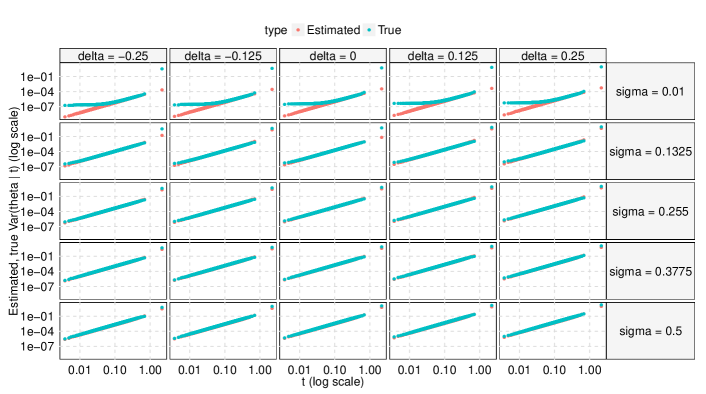

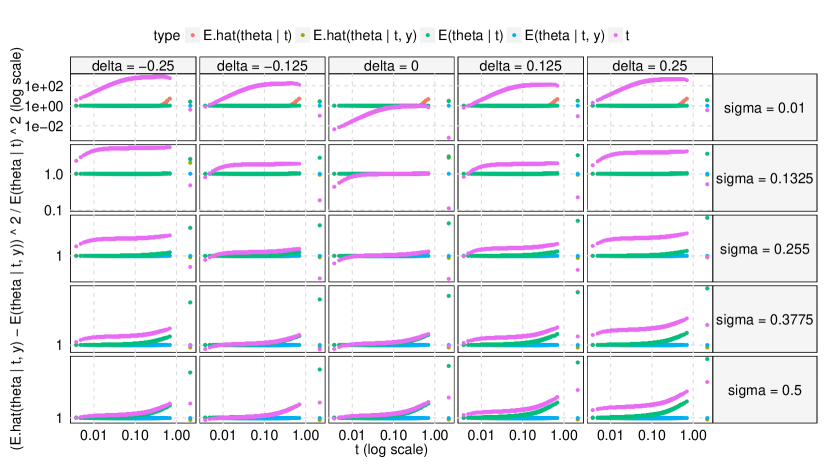

Our estimates are accurate for all the values of and that we tried. We measured their accuracy directly, since we knew the true distributions. Figure 13 shows that our estimates of , , and were close to the corresponding true quantities. Calculating posterior quantities in the true lognormal-Poisson model is computationally expensive, so we found and by approximating the lognormal with a Gamma distribution. This worked better than approximation with a grid of point masses, and yielded an accurate approximation for , but cannot capture the heavy tails of the lognormal distribution and slightly underestimated .

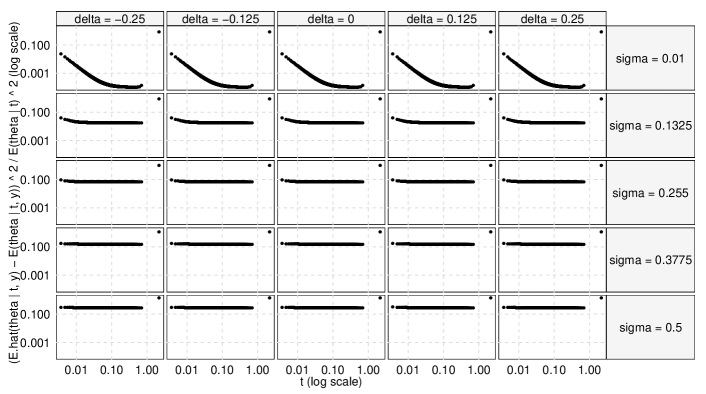

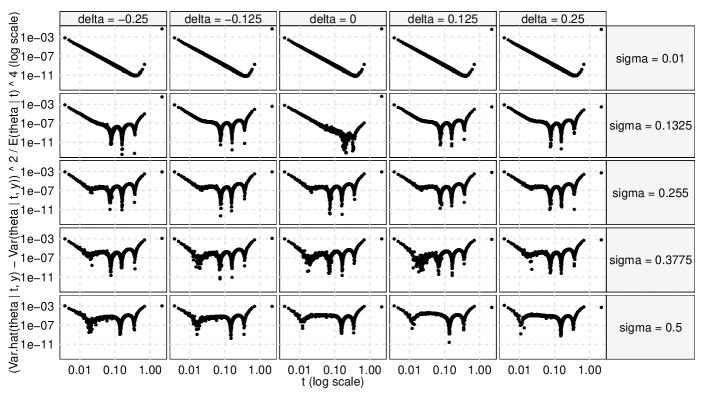

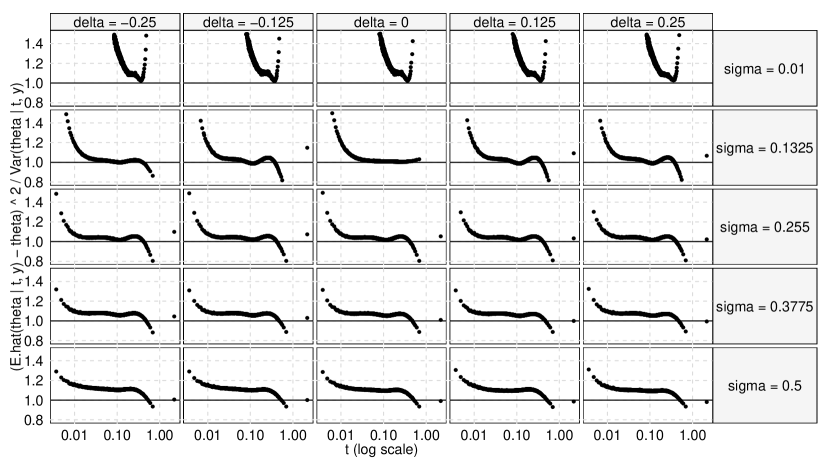

Figure 14 shows if this were a real problem, second order calibration would not be perfect, but would be good enough to be useful. It gives better point estimates - substantially improves on , , and , and estimates almost as well as our approximate . The improvement is especially large when is big, since the bigger is, the more information is item-specific, and the more we can gain by using it. Our variance estimates are also reasonably accurate. On average, is usually close to , but is about too small (Figure 15). This is because the true distribution of is lognormal, and our Gamma model cannot capture its heavy tails. Our -histograms detect this misfit when is large, but are not sensitive enough to detect the misfit when is small.

5.3. Simulated Normal data

As a final illustration of our method, we consider a smaller simulated normal data set with million items. Each item had a covariate with iid entries, and a response . was a quadratic function of , plus noise:

where were drawn iid from a Laplace distribution with variance . The coefficient vectors and each had entries that were with probability and ( for ) with probability . To get , we divided the data into five folds and regressed onto (with no interactions or quadratic terms). Finally, we fit using a seven-component normal mixture (using the R package “mixfdr” (Muralidharan, 2010)), and smoothed and .

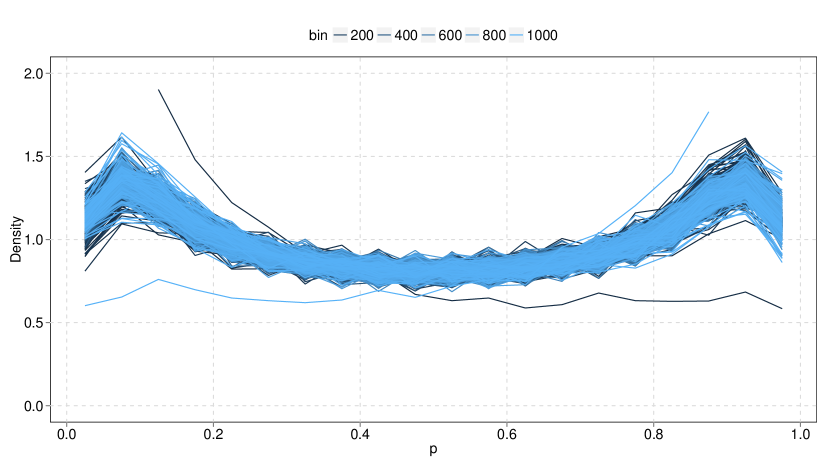

Figure 16 shows the -histograms for our fitted model. Although the fit is decent in the center of the distribution, we see many more low and high s than our fitted densities predict. Our normal mixture model does not capture the heavy tails of the distribution of . If this were a real data set, the -histograms would tell us our model for doesn’t fit, and we would refine it.

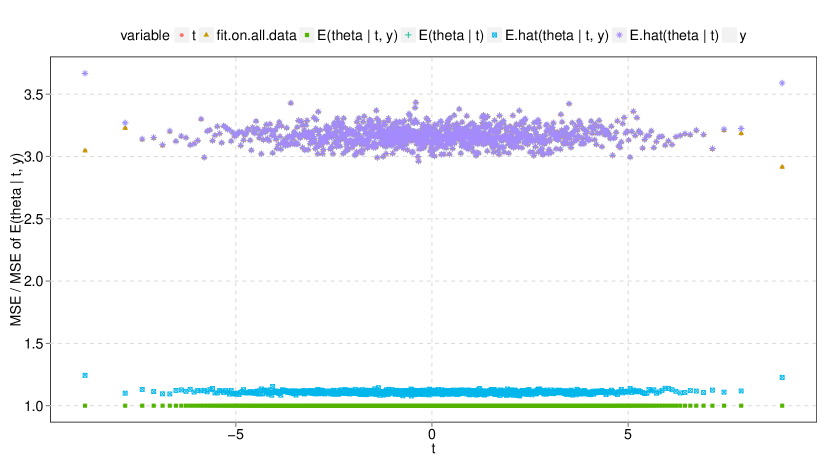

It is interesting, though, to see how our flawed model performs. Figure 17 shows that is a good, but not perfect point estimate. It estimates much more accurately than or , and is about worse than (calculated using a fine grid approximation). Figure 18 shows that our light-tailed fit makes our variance estimates too small - is, on average, about further from than indicates. Theorem 1 says that a better-fitting model should perform better.

6. Summary

This paper considers second order calibration, a simple way to get approximate posteriors from the output of an arbitrary black box estimation method. The idea, which extends the usual idea of calibrating the mean, is to approximate the distribution of with the distribution , and estimate the latter distribution using the data. We give a five step procedure to estimate these quantities: bin by , estimate the distribution of in each bin, collect and if necessary smooth the estimates across bins, check the fit, and use the estimates to calculate , , and . This is a reasonable thing to do: if the distribution of is Poisson or a continuous natural exponential family, the data has enough information to estimate , , and effectively. When applied to real and simulated data, second order calibration improves point estimates and gives useful accuracy estimates.

6.1. Acknowledgements

We thank many colleagues for helpful comments, suggestions and discussion: Sugato Basu, Nick Chamandy, Brad Efron, Brendan McMahan, Donal McMahon, Deirdre O’Brien, Daryl Pregibon and Tom Zhang.

Appendix A Proofs

From now on, we work within a bin. We always condition on (assumed constant in the bin), so we drop it to simplify notation.

A.1. Posterior Cumulant Formulas

In Section 4, we stated Robbins’ formulas for the posterior mean and variance of when is . Similar formulas exist for higher moments. Using Robbins’ argument, it is easy to show that

| (2) |

where , and . The two terms in the formula have a natural interpretation. The uniformly minimum variance unbiased (UMVU) estimate of is , so the first term in the formula is the UMVU estimate of . The second term is a correction that depends on the prior.

When is a continuous natural exponential family, it is easier to work with cumulants than with moments. Let be the th cumulant of a distribution and let be the polynomial that expresses the th cumulant of a distribution in terms of the first moments, so that for any distribution,

where is the th moments. Let be the th posterior cumulant of the distribution (it depends on , but we suppress this). Simple algebra shows that if is a continuous natural exponential family with base density , then

| (3) |

The two terms in this formula have the same interpretation as the two terms in equation 2. The UMVU estimator of is (Sharma, 1973), so the first term plugs UMVU estimates of into to estimate . The second term is a correction that depends on the prior.

A.2. Regularized Cumulant Estimators

Equations 2 and 3 divide by . If our estimate gives a light-tailed , this division can make our posterior moment and cumulant estimates behave badly. To avoid this, we follow the approach of Zhang (1997) and regularize our estimates: instead of divding by , we divide by , where is a tuning parameter. This gives regularized estimators

instead of our original, unregularized estimators , .

These regularized estimators guard against overshrinking. In the far tail, the second term in each formula tends to zero, since becomes and the numerator of each ratio tends to zero. That means that the correction term that depends on the prior disappears, and our estimates reduce to frequentist estimators. This makes sense: we don’t know much about the prior in the far tail, so we shouldn’t deviate too much from the safe frequentist estimator. The regularized estimators are similar in this respect to the limited translation estimators introduced by Efron and Morris (1971).

A.3. Proof of Theorem 1

We prove Theorem 1 by bounding the error in estimating the posterior cumulants and moments in terms of the error in estimating the marginal density. We first bound the error of the regularized estimates, then use those bounds that to bound the error of the unregularized estimates.

Lemma 1.

The regularized Poisson moment estimator has error at most

where , only depend on and : and .

Proof.

We first bound :

The second term is . We bound the first term using Cauchy-Schwartz and the triangle inequality:

∎

Lemma 2.

The regularized posterior cumulant estimator for continuous natural exponential families has error at most

Proof.

We have

To bound the first term, we write where is a polynomial of degree ; we can do this since every term in has degree . Let be the box , and let be the maximum of the norm of the gradient over . only depends on , through and . Then the first term is bounded by

∎

Lemma 3.

The unregularized Poisson moment estimator has error at most

Proof.

For any ,

The first term is , and we can bound the second term using Lemma 1. Taking the minimum over finishes the proof.∎

Lemma 4.

The unregularized posterior cumulant estimator for continuous natural exponential families has error at most

Proof.

References

- Amini and Johnson [2009] Ali Amini and Nicholas Johnson. Random effects / error measurement (in preparation). 2009.

- Caruana and Niculescu-Mizil [2006] Rich Caruana and Alexandru Niculescu-Mizil. An empirical comparison of supervised learning algorithms. In Proceedings of the 23rd international conference on Machine learning, ICML ’06, pages 161–168, New York, NY, USA, 2006. ACM. ISBN 1-59593-383-2. doi: 10.1145/1143844.1143865. URL http://doi.acm.org/10.1145/1143844.1143865.

- Cohen and Goldszmidt [2004] Ira Cohen and Moises Goldszmidt. Properties and benefits of calibrated classifiers. In 8th European Conference on Principles and Practice of Knowledge Discovery in Databases (PKDD), pages 125–136. Springer, 2004.

- Efron [2010] Bradley Efron. Large-Scale Inference: Empirical Bayes Methods for Estimation, Testing, and Prediction. Cambridge University Press, 2010.

- Efron and Morris [1971] Bradley Efron and Carl Morris. Limiting the risk of bayes and empirical bayes estimators–part i: The bayes case. Journal of the American Statistical Association, 66(336):807–815, 1971. ISSN 01621459. URL http://www.jstor.org/stable/2284231.

- Efron et al. [2001] Bradley Efron, Robert Tibshirani, John D. Storey, and Virginia Tusher. Empirical bayes analysis of a microarray experiment. Journal of the American Statistical Association, 96(456):1151–1160, 2001.

- Gneiting et al. [2007] Tilmann Gneiting, Fadoua Balabdaoui, and Adrian E. Raftery. Probabilistic forecasts, calibration and sharpness. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 69(2):243–268, 2007. ISSN 1467-9868. doi: 10.1111/j.1467-9868.2007.00587.x. URL http://dx.doi.org/10.1111/j.1467-9868.2007.00587.x.

- Graepel et al. [2010] Thore Graepel, Joaquin Quinonero Candela, Thomas Borchert, and Ralf Herbrich. Web-scale bayesian click-through rate prediction for sponsored search advertising in microsoft’s bing search engine. 2010. URL http://citeseerx.ist.psu.edu/viewdoc/summary?doi=10.1.1.165.5644.

- Jiang and Zhang [2009] Wenhua Jiang and Cun-Hui Zhang. General maximum likelihood empirical bayes estimation of normal means. The Annals of Statistics, 37:1647–1684, 2009.

- Johnstone and Silverman [2004] Iain M. Johnstone and Bernard W. Silverman. Needles and straw in haystacks: Empirical bayes estimates of possibly sparse sequences. Annals of Statistics, 4(4):1594–1649, 2004.

- Kiefer and Wolfowitz [1956] J. Kiefer and J. Wolfowitz. Consistency of the maximum likelihood estimator in the presence of infinitely many incidental parameters. The Annals of Mathematical Statistics, 27(4):887–906, 1956. ISSN 00034851. URL http://www.jstor.org/stable/2237188.

- Muralidharan [2010] Omkar Muralidharan. An empirical bayes mixture method for effect size and false discovery rate estimation. Annals of Applied Statistics, 4(1):422–438, 2010.

- Muralidharan [2011] Omkar Muralidharan. High dimensional exponential family estimation via empirical bayes. Statistica Sinica, 2011.

- Muralidharan et al. [2012] Omkar Muralidharan, Georges Natsoulis, John Bell, Hanlee Ji, and Nancy R. Zhang. Detecting mutations in mixed sample sequencing data using empirical bayes. Annals of Applied Statistics, 2012.

- Niculescu-Mizil and Caruana [2005] Alexandru Niculescu-Mizil and Rich Caruana. Predicting good probabilities with supervised learning. In Proceedings of the 22nd international conference on Machine learning, ICML ’05, pages 625–632, New York, NY, USA, 2005. ACM. ISBN 1-59593-180-5. doi: http://doi.acm.org/10.1145/1102351.1102430. URL http://doi.acm.org/10.1145/1102351.1102430.

- Platt [1999] John C. Platt. Probabilistic outputs for support vector machines and comparisons to regularized likelihood methods. In ADVANCES IN LARGE MARGIN CLASSIFIERS, pages 61–74. MIT Press, 1999.

- Richardson et al. [2007] Matthew Richardson, Ewa Dominowska, and Robert Ragno. Predicting clicks: estimating the click-through rate for new ads. In Proceedings of the 16th international conference on World Wide Web, WWW ’07, pages 521–530, New York, NY, USA, 2007. ACM. ISBN 978-1-59593-654-7. doi: 10.1145/1242572.1242643. URL http://doi.acm.org/10.1145/1242572.1242643.

- Robbins [1954] Herbert Robbins. An empirical bayes approach to statistics. Proceedings of the Third Berkeley Symposium on Mathematical Statistics and Probability, 1:157–163, 1954.

- Sharma [1973] Divakar Sharma. Asymptotic equivalence of two estimators for an exponential family. The Annals of Statistics, 1:973–960, 1973.

- Zadrozny and Elkan [2002] Bianca Zadrozny and Charles Elkan. Transforming classifier scores into accurate multiclass probability estimates. In Proceedings of the eighth ACM SIGKDD international conference on Knowledge discovery and data mining, KDD ’02, pages 694–699, New York, NY, USA, 2002. ACM. ISBN 1-58113-567-X. doi: 10.1145/775047.775151. URL http://doi.acm.org/10.1145/775047.775151.

- Zhang [1997] Cun-Hui Zhang. Empirical bayes and compound estimation of normal means. Statistica Sinica, 7:181–193, 1997.