modeling extreme values by the residual coefficient of variation

Abstract.

The possibilities of the use of the coefficient of variation over a high threshold in tail modelling are discussed. The paper also considers multiple threshold tests for a generalized Pareto distribution, together with a threshold selection algorithm. One of the main contributions is to extend the methodology based on moments to all distributions, even without finite moments. These techniques are applied to Danish fire insurance losses.

Key words and phrases:

Statistics of extremes; heavy tails; high quantile estimation; value at risk.1. Introduction

Fisher & Tippett [7] and Gnedenko [9] show that, under regularity conditions, the limit distribution for the normalized maximum of a sequence of independent and identically distributed (iid) random variable (r.v.) is a member of the generalized extreme value (GEV) distribution with a cumulative distribution function

where is called extreme value index. This family of continuous distributions contains the Fréchet distribution (), the Weibull distribution (), and the Gumbell distribution ( as a limit case), see [12].

The Pickands–Balkema–DeHaan Theorem, see [6] and [12], initiated a new way of studying extreme value theory via distributions above a threshold, which use more information than the maximum data grouped into blocks. This Theorem is a very widely applicable result that essentially says that the generalized Pareto distribution () is the canonical distribution for modelling excess losses over high thresholds. The cumulative distribution function of is

| (1) |

where and are scale and shape parameters. For the range of is , in this case the is simply the usual Pareto distribution. The limit case corresponds to the exponential distribution. For the range of is and has bounded support. The shape parameter in GPD corresponds to the extreme value index in GEV. The has mean and variance provided .

Let be a continuous non-negative r.v. with distribution function . For any threshold, , the r.v. of the conditional distribution of threshold excesses given , denoted , is called the residual distribution of over . The cumulative distribution function of , is given by

| (2) |

The quantity is called the residual mean and the residual variance. The residual coefficient of variation () is given by

| (3) |

like the usual , the function is independent of scale, that is, if is multiplied by a positive constant, is invariant.

The residual distribution of a is again and for any threshold , the shape parameter is invariant, in fact

| (4) |

Note that the residual is independent of the threshold and the scale parameter, since it is given by

| (5) |

Gupta and Kirmani [10] show that the residual characterizes the distribution in the univariate as well as the bivariate case, provided there is a finite second moment. In the case of , the residual is constant and is a one to one transformation of the extreme value index suggesting its use to estimate this index.

Castillo et al. [2] suggest a new tool to identify the tail of a distribution based on the residual , henceforth called CV-plot, as an alternative to the mean excess plot (ME-plot) that is a commonly used diagnostic tool in risk analysis to justify fitting a , see [8], [6] and [5]. Given a sample of size of positive numbers, we denote the ordered sample , so that . The CV-plot is the of the residual samples, that is, the function, of the of the threshold excesses for the exceedances , over the order statistics, , given by

| (6) |

where, is the size of the sub-sample removed. This tool has been applied to financial and environmental datasets, see [3].

The -plot has some advantages over ME-plot: first, it does not depend on the scale parameter; second, detecting constant functions is easier than linear functions, since linear functions are defined by two parameters and the constants by only one. The uncertainty is essentially reduced from three to one single parameter.

A unconscientious use of some measures of variation can lead to wrong conclusion, see [1]. A serious problem with the residual coefficient of variation is the fact that the proposed method only works when the extreme value index is smaller than 0.25. To fix this, some transformations that relate light-heavy tails are introduced in Section 2.

Section 3 extends some results of Castillo et al. [2] from the exponential distribution to all GPD when the extreme value index is below 0.25. Moreover, multiple threshold tests together with a threshold selection algorithm, designed in a way that avoids subjectivity, are also achieved. In Section 4, the approach developed in the previous sections is illustrated using the Danish fire insurance dataset, a highly heavy-tailed, infinite-variance model.

2. Transformations of heavy-light tails

The transformations introduced to this section make it possible to estimate the extreme value index using methods based on moments in situations where moments are not finite.

A distribution function is said to be in the maximum domain of attraction of , written , if under appropriate normalization the block maxima of a iid sequence of r.v. with distribution converge to . For a r.v. with distribution function is also written . A positive function on slowly varies at if

Regularly varying functions can be represented by power functions multiplied by slowly varying functions, i.e. if and only if .

Gnedenko proved, see [12, Theorems 7.8 and 7.10], that the maximum domain of attraction of a Fréchet distribution, with shape parameter , is characterized in terms of the tail function, , by

Similarly the maximum domain of attraction of a Weibull distribution, with shape parameter , is characterized by

where .

The following result of practical importance is embedded in the previous characterizations, and which to our knowledge has not been used.

Corollary 1.

Let be a r.v. with cumulative distribution function .

-

(1)

If with , then .

-

(2)

If with , then , where .

Proof.

(1) The cumulative distribution function of is and . By assumption with slowly varying at , hence and .

(2) The tail function of is now . Hence, and . ∎

Corollary 1 provides an asymptotic method and is related to an exact result in the GEV model: has Fréchet distribution if and only if has Weibull distribution with the same extreme value index, but with the sign changed. However, the corresponding result is not true in , as we discuss below.

For a r.v. , the Pickands–Balkema–DeHaan Theorem shows that if and only if the limiting behavior of the residual distribution of over , , is like a with the same parameter , see [12, Theorem 7.20]. Hence, Corollary 1 can be used in applied methods of threshold exceedances.

Corollary 2.

Let be a r.v. such that the limiting behavior of the residual distribution of over a threshold is with parameter , then the limiting behaviour of the residual distribution of over a threshold is with parameter .

Corollary 2 enables use of methods to determine the extreme value index for light tails in heavy tailed distributions and vice versa. For instance ME-plot and -plot can be used to determine the extreme value index in really heavy tailed distributions, see Example 4 below. These asymptotic results can be improved on GPD for practical aplications.

The distributions are standardized so that all their observations take positive values. The supports of the distributions are , where for and for . The distributions can be expanded to include a location parameter by . The behavior of near is the same as that of near . The transformation is also associated with the origin at zero, but can be generalized to , provided , or , in order for the transformations to remain monotonous increasing on . The following result examines these transformations on .

Theorem 3.

Let be a r.v. with distribution in and or , then has distribution with location parameter if and only if . Then has distribution.

Proof.

Corollary 4.

Let , and , then a r.v. has distribution if and only if has distribution with , and the support .

Proof.

In the direct sense, this is proved by the Theorem 3, because and .

In practical applications of the previous results, a first estimate of the shape and the scale parameters is required in order to define the transformation to a lighter tail, after which the residual empirical CV plot is constructed.

3. Multiple threshold test

Some results of Castillo et al. [2] on the residual CV extend directly from the exponential distribution to all GPD, provided there is a finite fourth moment. Therefore, the proof of the following theorem is omitted. The asymptotic distribution of the residual CV as a random process indexed by the threshold provides pointwise error limits for -plot in (6) and a multiple thresholds test for GPD that really does reduce the multiple testing problem. The multiple thresholds test provides a clear sense of significance levels and p-values.

Theorem 5.

Pointwise error limits of the -plot under GPD follow from the next result.

Corollary 6.

Given a sample of a distribution and a threshold , the asymptotic distribution of the residual is

| (8) |

where is in (5), and

Proof.

From the last result the asymptotic confidence intervals of the -plot for exponential distribution are obtained with and and for uniform distribution with and .

3.1. Simple null hypothesis

Corollary 6 makes it possible to test whether the empirical of a sample, or of threshold excesses, fit the of a with fixed values and . However, from [10], in order to have a consistent test in GPD, must be checked for all threshold . From Theorem 5, a multiple threshold test for a number of thresholds as large as necessary for practical applications can also be constructed using the building blocks , regardless of the scale parameter, with asymptotic distribution under the null hypothesis of .

The choice of thresholds could be arbitrary, but the multiple thresholds test, , is designed to avoid subjectivity as much as possible, to the limit of the number of thresholds . If the thresholds are selected as empirical quantiles or order statistics, then is invariant when the sample is multiplied by a positive number while maintaining the set of probabilities, since CV is invariant. This first condition ensures that the test results do not depend on units used for the observations.

Given a sample of size of non-negative numbers, denotes the inverse of the empirical distribution function,

| (9) |

From a set of probabilities let be the corresponding empirical quantiles of the sample, , then a multiple thresholds statistic can be constructed as

The asymptotic expectation is , hence is an estimator of the asymptotic variance , when is known or estimated. Note that the distribution of is independent of the scale parameter . makes it possible to test the null hypothesis that the sample comes from a distribution with the residual corresponding to previous quantiles all equal to .

Hence, if is accepted and is large enough, say or , it will be reasonable to assume that the sample comes from a distribution . The previous test is a global test in the sense that some may be significant and others not but with one test alone the equality of all for all quantiles is checked.

A second desirable condition is to select the set of probabilities that determine the statistic so that the corresponding thresholds are approximately equally spaced. This can be achieved for the exponential distribution by taking , , and the corresponding quantiles, since for a random variable, , with exponential distribution , where is the expected value. Then the condition holds for and is fairly approximate for . Selecting the probabilities this way, , and becomes

| (10) |

In applications, given the number of single tests that will be included in the multivariant test, , we choose the value of , which determines the distance between the quantiles, such that , where is the sample size such that irrelevant information comes from smaller sub-samples. Hence, given , is suggested. In this paper is used in numerical algorithms. Note that this way depends only on and and the researcher chose only the number of thresholds used in the analysis, essentially eliminating subjectivity. These multiple thresholds tests generalize those developed by Castillo et al. [2] for and .

The asymptotic distribution of is easily calculated from Theorem 5, following the steps suggested by Castillo et al. [2], whenever . However, taking into account the different values of the extreme value index and the diverse small sample sizes, it is easier in practice to calculate the -value for using simulation methods, which are especially simple in this case. Assuming for simulations, only the sample size, the number of thresholds, , and are needed. Since the distribution does not depend on scale, parameter will be used.

3.2. Composite null hypothesis

In most cases the parameter is unknown and its estimate should be incorporated in the statistic (see the R code below). The method for estimating leads to slight variations in the statistic, but it leads to essentially equivalent inference whenever we use the same estimation method in simulations to obtain the -value. The null hypothesis is now that the sample comes from a distribution in which all residual are equal.

The alternative hypothesis is that the residual are equal from a threshold to the threshold .

The most recommended estimation method is maximum likelihood estimation (MLE), although in it is only asymptotically efficient provided , see [5]. For this distribution, the is a one-to-one transformation of , see (5), and the empirical of the residual sample, , provides an alternative method of estimation. It is asymptotically normal whenever , see Corollary 6. The multiple thresholds tests (10) suggest estimating as the value such that achieves the minimum , namely

| (11) |

From Corollary 6 the estimator is also asymptotically normal. The main advantage of this method is that under the alternative hypothesis it is a better estimator than or MLE, since the sample is only over a threshold . Since the main interest is in samples that are not , but in the tail, and results are often used in small samples with , the estimation method (11) is included in the statistic . The following R code for is used in the algorithms, see [13].

#Statistic Tm of a sample given the number of thresholds m.

Tm<-function(m,sample){sam<-sample-min(sample);

n<-length(sam);ns<-8;

p<-round(exp(log(ns/n)/m),digits=2);

Ws<-Ps<-Qs<-Cs<-numeric(m+1);

for(k in 1:(m+1)){Ws[k]<-p^(k-1)};

Ps<-1-Ws;Qs<-as.vector(quantile(sam,Ps));

for(k in 1:(m+1))

{Cs[k]<-sd(sam[sam>=Qs[k]]-Qs[k])/mean(sam[sam>=Qs[k]]-Qs[k])};

cx<-(1-p)*sum(Ws*Cs)/(1-p^(m+1));xi<-(cx^2-1)/(2*cx^2);

tm<-n*sum(Ws*(Cs-cx)^2);list(CV=cx,Tm=tm,Xi=xi)}

3.3. Threshold Selection Algorithms

To select the number of extremes used in applying the peaks over a high threshold method, threshold selection algorithms are developed in this section to estimate the point above which the distribution can be used to estimate the extreme value index for a set of extreme events, , of size . For this purpose the previous statistical tests will be adapted.

Note that in the calculation the number of thresholds is the only parameter that must be fixed by the researcher. This determines the thresholds (quantiles) where the is calculated, , which are fixed throughout the procedure. Then, by simulation of , the associated -value is calculated (running samples). After that, we accept or reject the null hypothesis with the estimated shape parameter using all the thresholds.

If the hypothesis is rejected, the threshold excesses are calculated for the sub-sample . The previous steps are repeated, but removing one threshold, to accept or reject the null hypothesis that the sample is from a . At every stage only statistics associated to thresholds , where , are calculated:

| (12) |

In summary, the steps of the general algorithm are

-

(1)

Given find such that , where is the smaller sample size used to calculate (here is used, but it can be modified).

-

(2)

Calculate , where , and , where , .

-

(3)

Estimate minimizing the value of with the specific values in the previous steps.

-

(4)

Calculate by simulation of the -value associated to the mini-mum and accept or reject the null hypothesis with the estimated shape parameter using all the thresholds (starting with ).

-

(5)

If the hypothesis is rejected, compute the threshold excesses for the sub-sample and repeat the previous steps with and , to accept or reject the null hypothesis that the sample is from a , but removing a threshold.

-

(6)

Continue the process for the next value in the index of thresholds while the hypothesis is rejected.

Several authors recommend giving a prominent role to the exponential distribution in the model , see [3]. The usual method for doing this is to consider the exponential models as the null hypothesis testing against , see [11]. Alternatively, one can consider the Akaike or Bayesian information criteria for model selection, see [4]. The previous algorithm can be adapted to the case when (or simply known) skipping step-3.

4. Danish fire insurance data

An interesting aspect of this article is the combination of the results of sections 2 and 3 when applying the peaks over threshold technique for tails in any maximum domain of attraction. This approach is illustrated here using a popular dataset.

The Danish fire insurance data are a well-studied set of losses to illustrate the basic ideas of extreme value theory. The dataset consists of fire insurance losses over one million Danish kroner from 1980 to 1990 inclusive, see [6, Example 6.2.9], [14] and [12, Example 7.23].

In this example the authors agree to assume iid observations and a heavy tailed model. They also agree to set the threshold at million Danish kroner, the exceedances over the threshold, denoted , are .

Fitting a to by MLE, the parameter estimates in [12] are and with standard errors and , respectively. Thus the fitted model is a very heavy-tailed, infinite-variance model and the method in Section 3 cannot be applied directly. However, they can be used through the results shown in Section 2.

First of all, let us suppose we want to use to check whether the above data correspond to a distribution with the estimated extreme value index. Applying Theorem 3 with , let be, then the set has light tails and the same extreme value index with the sign changed, provided that the estimated parameters are the true parameters. The of is which provides a new estimation of , solving (5) by then, according to Theorem 3, , not far from , since the standard error is . Alternatively, the multiple thresholds statistic , from (12), can be used to check . The corresponding under is . Taking , we get with a -value (by simulation with samples), accepting the null hypothesis.

Now consider the problem of choosing the threshold to estimate the extreme value index. In this example, most researchers use a visual observation of the ME-plot on the full Danish dataset. The algorithm in Section 3.3 with the transformations from Section 2, comes to similar solutions automatically and opens up new perspectives.

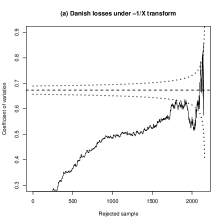

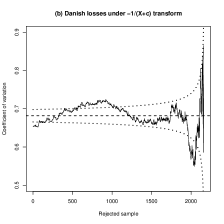

Figure 1 shows the -plots of the full Danish dataset, transformed according to the Corollary 2, plot (a), and Theorem 3, plot (b). The first, corresponding to the transformation , shows an increasing and the second, corresponding to , shows a stabilized close to a constant, indicating that the original dataset is close to a , which is also shown by ME-plot.

Applying the algorithm of Section 3.3 with after transformation , constant residual is rejected in the first 11 steps (each one reduces the sample size by ). Step 12, for the last 106 observations, accepts constant residual (-value ) with estimates and . The estimated threshold is approximately the same ( instead of ), while the extreme value index is different but within the confidence interval.

The algorithm in Section 3.3, with after transformation with , rejects constant residual in the first three steps. Step 4, for the last 951 observations, accepts constant residual (-value ) with estimates and . The number of observations is much higher, the extreme value index being very close to that obtained with the transformation and within the confidence interval. The -value remains similar in the following steps up until the 12th, where it jumps up to . The number of observations is again and the estimation , nearer to .

The conclusions from using the new methodology to analyze this dataset are the following. First, the results obtained by previous investigators are validated, in particular can be accepted with parameter , for the larger observations see [12]. This also shows the consistency of the presented methodology with other common techniques.

Moreover, from examining the extreme value index it is now known that for the larger observations can also be accepted, where the MLE parameter estimate is , with standard error ( obtained by is within the confidence interval). The estimated extreme value index is now much more accurate because the sample size is much larger. We also note that the tails are heavier than was assumed, which means that higher risks should be considered.

|

|

Acknowledgement

This work was supported by the Spanish Ministry of Economy and Competitiveness under Grant: Applied Stochastic Processes, MTM 2012-31118.

References

- [1] Albrecher, H., Ladoucette, S. Teugels, J. Asymptotics of the Sample Coefficient of Variation and the Sample Dispersion, Journal of Statistical Planning and Inference, 140, 358-368 (2010).

- [2] Castillo, J. D., Daoudi, J. and Lockhart, R., Methods to Distinguish Between Polynomial and Exponential Tails, Scandinavian Journal of Statistics, 41, 382–393 (2014).

- [3] Castillo, J. D. and Serra, I., Likelihood inference for Generalized Pareto Distribution, Computational Statistics and Data Analysis, 83, 116–128 (2015).

- [4] Clauset A., Shalizi C. and Newman, M., Power-law distributions in empirical data, SIAM Review, 51, 661–703 (2009).

- [5] Davison, A. C. and Smith, R. L., Models for exceedances over high thresholds, Journal of the Royal Statistical Society. Series B, 393–442 (1990).

- [6] Embrechts, P., Klüppelberg, C. and Mikosch, T., Modeling Extremal Events for Insurance and Finance, Springer, Berlin (1997).

- [7] Fisher, R. A. and Tippett, L. H. C., Limiting forms of the frequency distribution of the largest or smallest member of a sample, In: Mathematical Proceedings of the Cambridge Philosophical Society, 24, 180–190, Cambridge University Press (1928).

- [8] Ghosh, S. and Resnick, S., A discussion on mean excess plot, Stochastic Processes and their Applications, 120, 1492–1517 (2010).

- [9] Gnedenko, B., Sur la distribution limite du terme maximum d’une serie aleatoire, The Annals of Mathematics, 44, 423–453 (1943).

- [10] Gupta, R. C. and Kirmani, S. N. U. A., Residual coefficient of variation and some characterization results, Journal of Statistical Planning and Inference, 91, 23–31 (2000).

- [11] Kozubowski, T. J., Panorska, A. K., Qeadan, F., Gershunov, A. and Rominger, D., Testing exponentiality versus Pareto distribution via likelihood ratio, Comm. Statist. Simulation Comput., 38, 118–139 (2009).

- [12] McNeil, A. J., Frey, R. and Embrechts, P., Quantitative Risk Management: Concepts, Techniques, and Tools, Princeton Series in Finance, New Jersey (2005).

- [13] R Development Core Team, R: A Language and Environment for Statistical Computing, R Foundation for Statistical Computing, Vienna, Austria (2010).

- [14] Resnick, S. I., Discussion of the Danish data on large fire insurance losses, Astin Bull, 27, 139–151 (1997).