Estimating standard errors for importance sampling estimators with multiple Markov chains

Abstract

The naive importance sampling estimator, based on samples from a single importance density, can be numerically unstable. Instead, we consider generalized importance sampling estimators where samples from more than one probability distribution are combined. We study this problem in the Markov chain Monte Carlo context, where independent samples are replaced with Markov chain samples. If the chains converge to their respective target distributions at a polynomial rate, then under two finite moment conditions, we show a central limit theorem holds for the generalized estimators. Further, we develop an easy to implement method to calculate valid asymptotic standard errors based on batch means. We also provide a batch means estimator for calculating asymptotically valid standard errors of Geyer’s (1994) reverse logistic estimator. We illustrate the method via three examples. In particular, the generalized importance sampling estimator is used for Bayesian spatial modeling of binary data and to perform empirical Bayes variable selection where the batch means estimator enables standard error calculations in high-dimensional settings.

Key words and phrases: Bayes factors, Markov chain Monte Carlo, polynomial ergodicity, ratios of normalizing constants, reverse logistic estimator.

1 Introduction

Let be a probability density function (pdf) on X with respect to a measure . Suppose is a integrable function and we want to estimate . Let be another pdf on X such that . The importance sampling (IS) estimator of based on independent and identically distributed (iid) samples from the importance density is

| (1.1) |

as . This estimator can also be used in the Markov chain Monte Carlo (MCMC) context when are realizations from a suitably irreducible Markov chain with stationary density (Hastings (1970)). Note that (1.1) requires the functions and to be known. On the other hand, it does not depend on normalizing constants and , which are generally unknown.

In this article, we consider situations where one wants to estimate for all belonging to a large collection, say . This situation arises in both frequentist and Bayesian statistics. Although (1.1) provides consistent estimators of for all based on a single Markov chain with stationary density , it does not work well when differs greatly from . In that case the ratios can be arbitrarily large for some sample values making the estimator at (1.1) unstable. In general, there is not a single good importance density which is close to all (see e.g. Geyer (1994)). Hence a natural modification is to replace in (1.1) with a mixture of densities where each density in is close to a subset of the reference densities. To this end, denote , where are positive constants, , and for are densities known up to their normalizing constants. Suppose further that are positive integers and for with . Then define the dimensional vector

| (1.2) |

Finally for , let be an iid sample from or realizations from a positive Harris Markov chain with invariant density (for definitions see Meyn and Tweedie (1993)). Then as for all , we have

| (1.3) | ||||

The generalized IS estimator (1.3) has been discussed widely in the literature, e.g. applications include Monte Carlo maximum likelihood estimation and Bayesian sensitivity analysis. Gill et al. (1988), Kong et al. (2003), Meng and Wong (1996), Tan (2004), and Vardi (1985) consider estimation using (1.3) based on iid samples. The estimator is applicable to a much larger class of problems if Markov chain samples are allowed, see e.g. Buta and Doss (2011), Geyer (1994), and Tan et al. (2015), which is the setting of this paper.

Alternative importance weights have also been proposed. In the case when the normalizing constants ’s are known, the estimator (1.3) resembles the balance heuristic estimator of Veach and Guibas (1995), which is revisited in Owen and Zhou (2000) as the deterministic mixture. The standard population Monte Carlo algorithm of Cappe et al. (2004) uses a weighted ratio of the target and the proposal it was drawn from (evaluated at the sample itself). However, when iid samples are available from , Elvira et al. (2015) have shown that the normalized estimator (’s known) version of (1.3) always has a smaller variance than that of the population Monte Carlo algorithm. Further, it may be difficult in practice to find fully known importance densities that approximate the target densities. Indeed, applications such as in empirical Bayes analysis and Bayesian sensitivity analysis routinely select representatives from the large number of target posterior densities to serve as proposal densities, and they are known only up to normalizing constants. See Buta and Doss (2011), Doss (2010), as well as section 5 for examples. Although there is no known proof for the self normalized estimator (Elvira et al., 2015, p. 16), it is reasonable to assume the superiority of (1.3) over estimators corresponding to other weighting schemes.

As noted in (1.3), the estimator converges to as the sample sizes increase to infinity, for iid samples as well as Markov chain samples satisfying the usual regularity conditions. Now given samples of finite size in practice, it is of fundamental importance to provide some measure of uncertainty, such as the standard errors (SEs) associated with this consistent estimator. Take estimators that are sample averages based on iid Monte Carlo samples for example, it is a basic requirement to report their SEs. But the very same issue is often overlooked in practice when the estimators have more complicated structure, and when they are based on MCMC samples, largely due to the difficulty of doing so. See, for e.g. Flegal et al. (2008) on the issue concerning MCMC experiments and Koehler et al. (2009) for more general simulation studies. For calculating SEs of based on MCMC samples, Tan et al. (2015) provide a solution using the method of regenerative simulation (RS). However, this method crucially depends on the construction of a practical minorization condition, i.e. one where sufficient regenerations are observed in finite simulations (for definitions and a description of RS see Mykland et al. (1995)). Further, the usual method of identifying regeneration times by splitting becomes impractical for high-dimensional problems (Gilks et al., 1998). Hence, successful applications of RS involve significant trial and error and are usually limited to low-dimensional Gibbs samplers (see e.g. Tan and Hobert (2009); Roy and Hobert (2007)). In this paper we avoid RS and provide SE estimators of using the batch means (BM) method, which is straightforward to implement and can be routinely applied in practice. In obtaining this estimator, we also establish a central limit theorem (CLT) for that generalizes some results in Buta and Doss (2011).

The estimator in (1.3) depends on the ratios of normalizing constants, , which are unknown in practical applications. We consider the two-stage scheme studied in Buta and Doss (2011) where first an estimate is obtained using Geyer’s (1994) “reverse logistic regression” method based on samples from , and then independently, new samples are used to estimate for using the estimator in (1.3). Buta and Doss (2011) showed that the asymptotic variance of depends on the asymptotic variance of . Thus we study the CLT of and provide a BM estimator of the asymptotic covariance matrix of . Since involves multiple Markov chain samples, we utilize a multivariate BM estimator. Although, the form of the asymptotic covariance matrix of is complicated, our consistent BM estimator is straightforward to code.

The problem of estimating , the ratios of normalizing constants of unnormalized densities is important in its own right and has many applications in frequentist and Bayesian inference. For example, when the samples are iid sequences this is the biased sampling problem studied in Vardi (1985). In addition, the problem arises naturally in the calculations of likelihood ratios in missing data (or latent variable) models, mixture densities for use in IS, and Bayes factors.

Our work considers the problem of estimating using Geyer’s (1994) reverse logistic regression method. Specifically, we study the general quasi-likelihood function proposed in Doss and Tan (2014). Unlike Geyer’s (1994) method, this extended quasi-likelihood function has the advantage of using user defined weights which are appropriate in situations where the multiple Markov chains have different mixing rates. We establish the CLT for the resulting estimators of and develop the BM estimators of their asymptotic covariance matrix.

Thus we consider two related problems in this paper–firstly, estimating (ratios of) normalizing constants given samples from densities, and secondly, estimating expectations with respect to a large number of (other) target distributions using these samples. In both cases, we establish CLTs for our estimators and provide easy to calculate SEs using BM methods.

Prior results of Buta and Doss (2011), Doss and Tan (2014), Geyer (1994), and Tan et al. (2015) all assume that the underlying Markov chains are geometrically ergodic. We weaken this condition substantially in that we only require the chains to be polynomial ergodic. To this end, let be the Markov transition function for the Markov chain , so that for any measurable set , and we have . Let denote the total variation norm and be the probability measure corresponding to the density . The Markov chain is polynomially ergodic of order where if there exists with such that

There is substantial MCMC literature establishing that Markov chains are at least polynomially ergodic (see Vats et al. (2015b) and the references therein).

We illustrate the generalized IS method and importance of obtaining SEs through three examples. First, we consider a toy example to demonstrate that BM and RS estimators are consistent and investigate the benefit of allowing general weights to be used in generalized IS. Second, we consider a Bayesian spatial model for a root rot disease dataset where we illustrate the importance of calculating SEs by considering different designs and performing samples size calculations. Finally, we consider a standard linear regression model with a large number of variables and use the BM estimator developed here for empirical Bayes variable selection.

The rest of the paper is organized as follows. Section 2 is devoted to the important problem of estimating the ratios of normalizing constants of unnormalized densities, that is estimating . Section 3 contains the construction of a CLT for and describes how valid SEs of can be obtained using BM. Sections 4 and Appendix E contain toy examples illustrating the benefits of different weight functions. Section 5 considers a Bayesian spatial models for binary responses. The empirical Bayes variable selection example is contained in Appendix F. We conclude with a discussion in Section 6. All proofs are relegated to the appendices.

2 Estimating ratios of normalizing constants

Consider densities with respect to the measure , where the ’s are known functions and the ’s are unknown constants. For each we have a positive Harris Markov chain with invariant density . Our objective is to estimate all possible ratios or, equivalently, the vector defined in (1.2).

Geyer’s (1994) reverse logistic regression is described as follows. Let and set for now. For define the vector by

and let

| (2.1) |

Given the value belongs to the pooled sample , is the probability that came from the distribution. Of course, we know which distribution the sample came from, but here we pretend that the only thing we know about is its value and estimate by maximizing the log quasi-likelihood function

| (2.2) |

with respect to . Since has a one-to-one correspondence with , by estimating we can estimate .

As Geyer (1994) mentioned, there is a non-identifiability issue regarding : for any constant , is same as where is the vector of ’s. So we can estimate the true only up to an additive constant. Thus, we can estimate only up to an overall multiplicative constant, that is, we can estimate only . Let be defined by , the true normalized to add to zero. Geyer (1994) proposed to estimate by , the maximizer of subject to the linear constraint , and thus obtain an estimate of . The estimator (written explicitly in Section 2.1), was introduced by Vardi (1985), and studied further by Gill et al. (1988), who proved that in the iid setting, is consistent and asymptotically normal, and established its efficiency. Geyer (1994) proved the consistency and asymptotic normality of when are Markov chains satisfying certain mixing conditions. In the iid setting, Meng and Wong (1996), Kong et al. (2003), and Tan (2004) rederived the estimate under different computational schemes.

However, none of these articles discuss how to consistently estimate the covariance matrix of , even in the iid setting. Recently Doss and Tan (2014) address this important issue and obtain a RS estimator of the covariance matrix of in the Markov chain setting. Doss and Tan (2014) also mention the optimality results of Gill et al. (1988) do not hold in the Markov chain case. In particular, when using Markov chain samples, the choice of the weights to the probability density in the denominator of (2.1) is no more optimal and should instead incorporate the effective sample size of different chains as they might have quite different rates of mixing. They introduce the following more general log quasi-likelihood function

| (2.3) |

where the vector is defined by for for an arbitrary probability vector . (Note the change of notation from to .) Clearly if , then and (2.3) becomes (2.2).

When RS can be used, Doss and Tan (2014) proved the consistency (to the true value ) and asymptotic normality of the constrained maximizer (subject to the constraint ) of (2.3) under geometric ergodicity. They also obtain a RS estimator of the asymptotic covariance matrix and describe an empirical method for choosing the optimal based on minimizing the trace of the estimated covariance matrix of . However, their procedure requires a practical minorization condition for each of the Markov chains, which can be extremely difficult. Without a minorization condition, we show is a consistent estimator of , show satisfies a CLT under significantly weaker mixing conditions, and provide a strongly consistent BM estimator of the covariance matrix of .

2.1 Central limit theorem and asymptotic covariance estimator

Within each Markov chain , assume in such a way that . In order to obtain the CLT result for , we first establish a CLT for . Note that the function that maps into is given by

| (2.4) |

and its gradient at (in terms of ) is

| (2.5) |

Since , and by definition , we can use the CLT result of to get a CLT for .

First, we introduce the following notations. For , let

| (2.6) |

The asymptotic covariance matrix in the CLT of , involves two matrices and , which we now define. The matrix is given by

| (2.7) |

Let be the matrix defined (for ) by

| (2.8) |

Remark 1.

The right hand side of (2.8) involves terms of the form and . For any fixed and , the two expectations are the same if and are exchangeable, e.g. if the chain is reversible. In general, the two expectations are not equal.

The matrix will be estimated by its natural estimate defined by

| (2.9) |

To obtain a BM estimate , suppose we simulate the Markov chain for iterations (hence and are functions of ) and define for

Now set for . For , denote where . Let

| (2.10) |

Let

| (2.11) |

and define the following matrix

| (2.12) |

where denotes the identity matrix. Finally, define

| (2.13) |

We are now ready to describe conditions that ensure strong consistency and asymptotic normality of . The following theorem also provides consistent estimate of the asymptotic covariance matrix of using BM method. Consistency of holds under minimal assumptions, i.e. if are positive Harris chains. On the other hand, CLTs and consistency of BM estimator of asymptotic covariance require some mixing conditions on the Markov chains. For a square matrix , let denote the Moore-Penrose inverse of .

Theorem 1

Suppose that for each , the Markov chain has invariant distribution .

-

1.

If the Markov chains are positive Harris, the log quasi-likelihood function (2.3) has a unique maximizer subject to the constraint . Let denote this maximizer, and let . Then as .

-

2.

If the Markov chains are polynomially ergodic of order , as , where .

- 3.

3 IS with multiple Markov chains

This section considers a CLT and SEs for the generalized IS estimator . From (1.3) we see that , where

| (3.1) |

with

| (3.2) |

Note that converges almost surely to

| (3.3) |

as . Thus itself is a useful quantity as it consistently estimates the ratios of normalizing constants . Unlike the estimator in Section 2, does not require a sample from each density . Thus is well suited for situations where one wants to estimate the ratios for a very large number of ’s based on samples from a small number of skeleton densities, say . Thus this method is particularly efficient when obtaining samples from the target distributions is computationally demanding and the distributions within are similar.

In the context of Bayesian analysis, let be the posterior density corresponding to the likelihood function and prior with normalizing constant . In this case, is the so-called Bayes factor between the two models, which is commonly used in model selection.

The estimators and in (3.1) depend on , which is generally unknown in practice. Here we consider a two-stage procedure for evaluating . In the 1st stage, is estimated by its reverse logistic regression estimator described in Section 2 using Markov chains with stationary densities , for . Note the change of notation from Section 2 where we used ’s to denote the length of the Markov chains. In order to avoid more notations, we use ’s and ’s to denote the stage 1 chains and their length respectively. Once is formed, new MCMC samples are obtained and is estimated using () based on these 2nd stage samples. Buta and Doss (2011) propose this two-stage method and quantify its benefits over the method where the same MCMC samples are used to estimate both and .

3.1 Estimating ratios of normalizing constants

Before we state a CLT for , we require some notation. Let

| (3.4) |

and . Further, define as a vector of length with th coordinate as

| (3.5) |

and as a vector of length with th coordinate as

| (3.6) |

Assuming , then let

| (3.7) |

where is the average of the st block , and is the overall average of . Here, and are the block sizes and the number of blocks respectively. Finally let .

Theorem 2

Suppose that for the stage 1 chains, conditions of Theorem 1 holds such that as . Suppose there exists such that where is the total sample size for stage 2. In addition, let for .

-

1.

Assume that the stage 2 Markov chains are polynomially ergodic of order , and for some for each where . Then as ,

(3.8) - 2.

Note that the asymptotic variance in (3.8) has two components. The second term is the variance of when is known. The first term is the increase in the variance of resulting from using instead of . Since we are interested in estimating for a large number of ’s and for every the computational time needed to calculate in (3.1) is linear in the total sample size , this can not be very large. If generating MCMC samples is not computationally demanding, then long chains can be used in the 1st stage (that is, large ’s can be used) to obtain a precise estimate of , and thus greatly reducing the first term in the variance expression (3.8).

3.2 Estimation of expectations using generalized IS

This section discusses estimating SEs of the generalized IS estimator given in (1.3). In order to state a CLT for we define the following notations:

(note is the same as defined in (3.4)) and

| (3.9) |

Since has the form of a ratio, to establish a CLT for it, we apply the Delta method on the function . Let

| (3.10) |

is a vector of length with th coordinate as

| (3.11) |

and is a vector of length with th coordinate as

| (3.12) |

where is defined in (3.6). Assuming , let

where is the average of the st block , is the overall average of and defined in Section 3.1. Finally let , and

Theorem 3

Suppose that for the stage 1 chains, conditions of Theorem 1 hold such that as . Suppose there exists such that where is the total sample size for stage 2. In addition, let for .

-

1.

Assume that the stage 2 Markov chains are polynomially ergodic of order , and for some and , for each where . Then as ,

(3.13) - 2.

Remark 2.

Part (1) of Theorems 2 and 3 extend Buta and Doss’s (2011) Theorems 1 and 3, respectively. Specifically, they require which is a non-optimal choice for (Tan et al., 2015). Our results also substantially weaken the Markov chain mixing conditions.

Remark 3.

Theorems 2 and 3 prove consistency of the BM estimators of the variances of and for a general . This extends results in Tan et al. (2015), which provides RS based estimators of the asymptotic variance of and in the special case when . With this particular choice, and in (3.2) become free of leading to independence among certain quantities. However, one can set for any user specified fixed vector , which allows the expression in (2.18) of Tan et al. (2015) to be free of and thus the necessary independence. Hence, their RS estimator can also be applied to an arbitrary vector (details are given in Appendix D).

Remark 4.

A sufficient condition for the moment assumptions for in Theorems 2 and 3 is that, for any , . That is, in any given direction, the tail of at least one of is heavier than that of . This is not hard to achieve in practice by properly choosing with regard to (see e.g. Roy, 2014). Further, if then the moment assumptions for are satisfied.

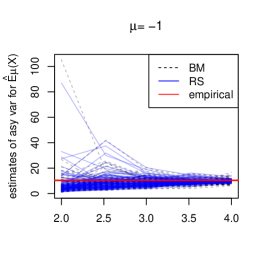

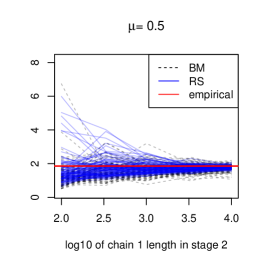

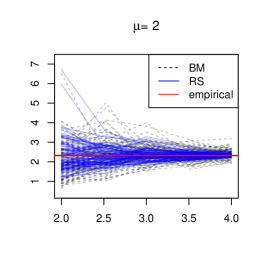

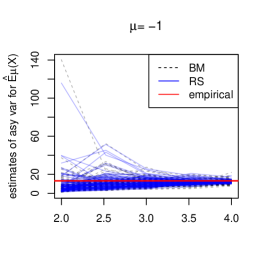

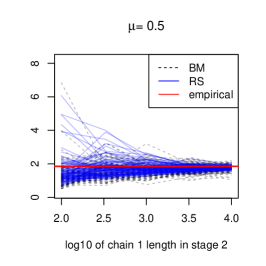

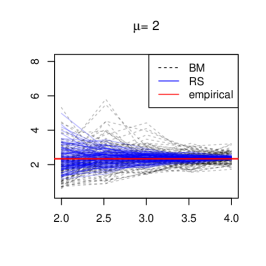

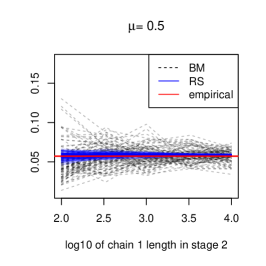

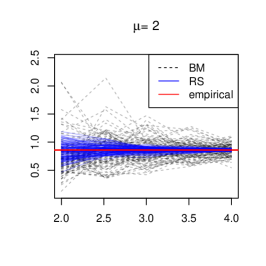

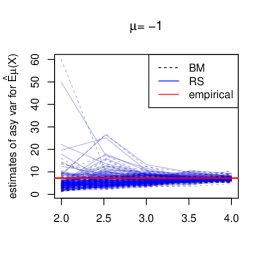

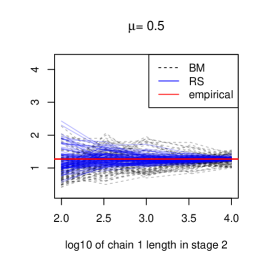

4 Toy example

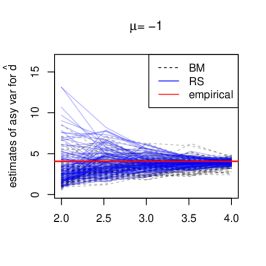

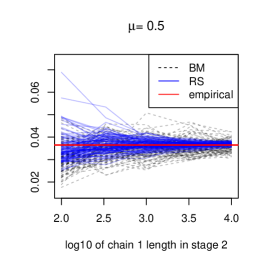

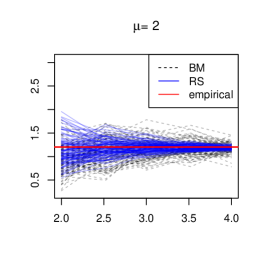

In this section, we employee a toy example to confirm that both the BM and the RS estimators are consistent, as well as demonstrate the benefit of allowing general weights to be used in the generalized IS estimator. Let denote the t-distribution with degree of freedom and central parameter . We set and , which are the density functions for a and , respectively. Pretending that we do not know the value of the ratio between the two normalizing constants, , we estimate it by the stage 1 estimator from section 2, and compare the BM and the RS method in estimating the asymptotic variance. As for the stage 2 estimators from section 3, the choice of weight and performance of the BM and the RS methods in assessing estimators’ uncertainty are studied in Appendix E.

We draw iid samples from and Markov chain samples from using the independent Metropolis Hastings algorithm with proposal density . It is simple to show , which implies the algorithm is uniformly ergodic (Mengersen and Tweedie (1996) Theorem 2.1) and hence polynomially ergodic and geometrically ergodic. For RS, our carefully tuned minorization condition enables the Markov chain for to regenerate about every 3 iterations. In contrast, the BM method proposed here requires no such theoretical development.

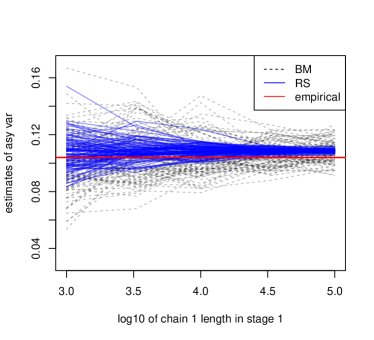

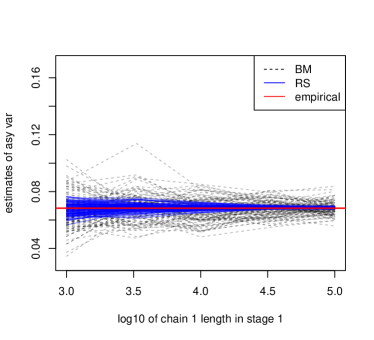

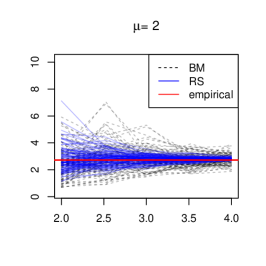

We evaluated the variance estimators at various sample sizes with different choices of weight. Figure 1 displays traces of the BM and the RS estimates of the asymptotic variance of , in dashed and solid lines, respectively. Overall, the BM and the RS estimates approach the empirical asymptotic variance as the sample size increases, suggesting their consistency. Due to the frequency of regenerations, BM estimates are generally more variable than RS estimates. Further, the left panel of Figure 1 is for estimators based on the naive weight, , that is proportional to the sample sizes; and the right panel is for estimators based on , that emphasizes the iid sample more than the Markov chain sample. Indeed, the latter weight is a close-to-optimal weight obtained with a small pilot study (see Appendix E for details). Using such a method to choose weight can lead to big improvement in the efficiency of if the mixing rate of the multiple samples differ a lot.

5 Bayesian spatial models for binary responses

In this section, we analyze a root rot disease dataset collected from a 90-acre farm in the state of Washington (Zhang, 2002). All computations are done in R, using the package geoBayes (Evangelou and Roy, 2015). Recorded at chosen sites are the longitude and the latitude , the root counts , and the number of infected roots . Of interest is a map of the disease rate over the entire area for precision farming. We consider the following spatial generalized linear mixed model (SGLMM), similar to that used by Zhang (2002) and Roy et al. (2016). Taking and as fixed, let

Here is a vector of latent variables, which is assumed to be a subvector of a Gaussian random field (GRF) , that has a constant mean , and a covariance function

Here, is the partial sill, denotes the Euclidean distance, and is a correlation function from the spherical family with range parameter . That is, for . Next, is an indicator that equals if , and equals otherwise. Finally, is the nugget effect, accounting for any remaining variability at site such as measurement error, while is the relative size of the nugget to the partial sill. Following Roy et al. (2016) we assign a non-informative Normal-inverse-Gamma prior to which is (conditionally) conjugate for the model. Specifically,

Assigning priors for in the correlation function of the Gaussian random field is usually difficult, and the choice of prior may influence the inference (Christensen, 2004). Hence we perform a sensitivity analysis focusing on obtaining the Bayes factor (BF) of the model at relative to a baseline for a range of values . Note that for a fixed , the Bayesian model described above has parameters . Conditioning on the observed data , inference is based on the posterior density

| (5.1) |

where is the likelihood, is the prior on , and is the normalizing constant, also called the marginal likelihood. The Bayes factor between any two models indexed by and is , and the empirical Bayes choice of is . Our plan is to get MCMC samples for a small reference set of , to estimate the BF among them using the reverse logistic estimator, and then get new samples to estimate using the generalized IS method. Below, we describe the MCMC algorithms and the practical concern of how long to run them, which illustrates the importance of calculating a SE.

The two high-dimensional integrals lend the posterior density in (5.1) intractable. But there exist MCMC algorithms to sample from the augmented posterior distribution, that is

| (5.2) |

Note that . Hence, a two-component Gibbs sampler that updates and in turn from their respective conditional distributions based on (5.2) yields a Markov chain with stationary distribution . As a result, the marginal is also a Markov chain with stationary distribution (Tanner and Wong, 1987).

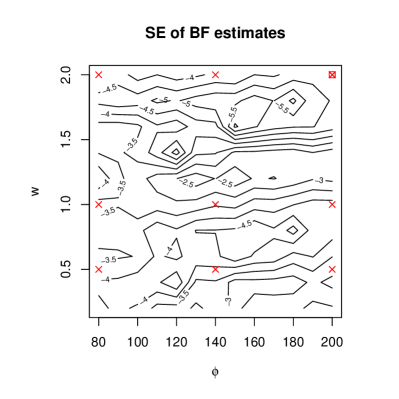

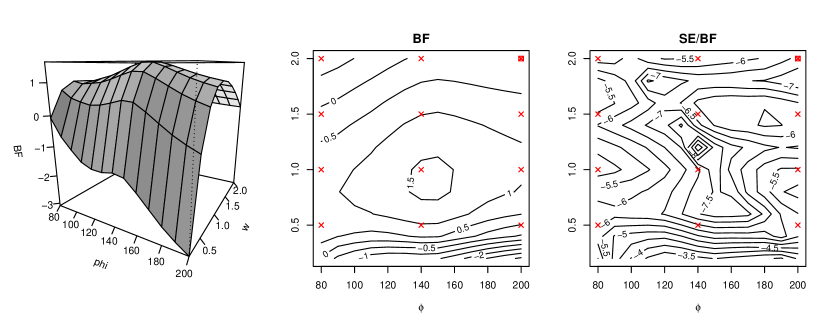

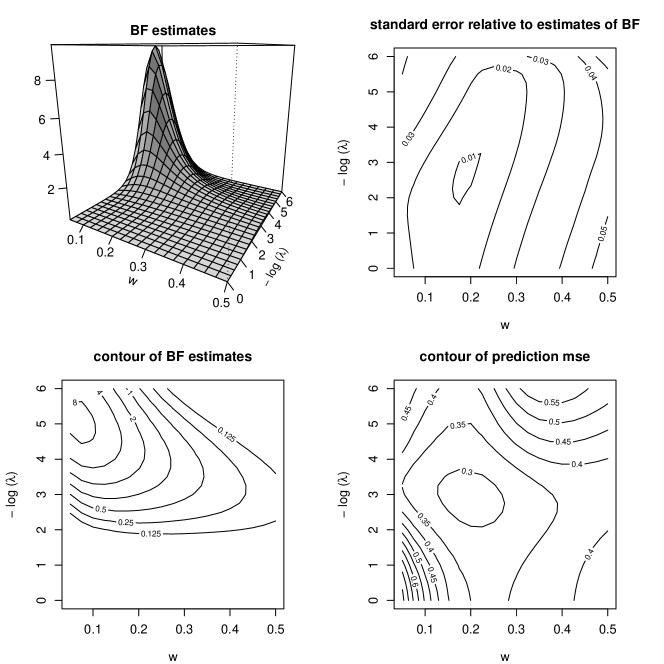

As a starting point, we use a small pilot study to identify a range for that corresponds to reasonably large BF values. This step is carried out by obtaining the reverse logistic estimator of BF at a coarse grid of values over a wide area, based on short runs of Markov chains. Specifically, and within this range the minimum BF is about 1% the size of the maximum. To more carefully estimate BF over this range, we examine a fine grid that consists of different values, with increments of size for the component, and that of for the component.

A natural choice for the set of skeleton points is , with an arbitrarily chosen baseline at . We first experiment with samples of sizes at the skeleton points (after a burn-in period of iterations and a thinning procedure that keeps one sample every iterations), of which the first are used in stage 1, and the remaining in stage 2 of the generalized IS procedure. BF estimates at all are obtained, though not shown. Given the current Monte Carlo sample sizes, it is natural to consider how trustworthy these BF estimates are. To this end, Figure 2 shows the point-wise SEs over the entire plot obtained via the BM method. In this setting for some , the magnitude of the SE is over of the corresponding BF estimate. Hence, inference based on these BF estimates could be questioned because of the high computational uncertainty.

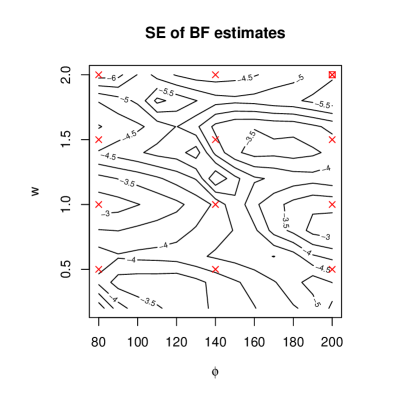

Suppose we wish to reduce the relative SE to or less for all , then roughly times as many samples would be required under the current design. Instead, we consider an alternative design using a bigger set of skeleton points, keeping the baseline unchanged at . In this alternative design, with sample sizes , the largest relative SE is . This is almost one fourth that of the previous design, but the computing time only increased by . Accordingly, running the alternative design would achieve the computing goal much faster. In this case, we increase the sample sizes to , which is approximately times . Overall, the new process takes minutes to run on a 3.4GHz Intel Core i7 running linux. The resulting BF estimates are shown in Figure 3, with maximum relative SE reduced to . For the sake of comparison, running the original design for the same amount of time allows a common sample size of resulting in a maximum relative SE of . In short, easily obtainable SE estimates allows us to experiment, choose among different designs, and perform samples size calculations.

The simplicity of the method matters when it comes to estimating SEs in practice. Using the BM method to obtain SE requires no extra input beyond what is needed for obtaining the generalized IS estimates. Indeed, as long as one can run existing software to obtain the Markov chain samples, there is no need to know the Markov transition kernels utilized in the background. Unlike the BM method, the RS method depends on identifying regeneration times, typically through constructing minorization conditions for the Markov transition kernels (see Mykland et al. (1995) for details). Despite the fact that minorization conditions can be established for any Markov transition kernel, we demonstrate for the current example the amount of effort needed to obtain a regeneration can be prohibitively high. Recall the MCMC scheme involves sampling from and in turn. The former is a standard distribution hence easy to sample from. The latter is not, and we followed Diggle et al. (1998) that updates in turn, each using a one-dimensional Metropolis-Hastings step that keeps invariant the conditional posterior distribution of given all other components. Denote the transition density of these MH steps as , and suppressing the notations of their dependence on , the transition kernel of the Markov chain can be represented as

According to a common method described in Jones and Hobert (2004), one can build a minorization condition by finding , , and such that,

Further, the above condition can be established if

where the common term on both sides of the inequality will cancel, and hence the work is in finding and . It’s easy to see that the smaller the set , the larger can possibly be, where can be interpreted as the conditional regeneration rate given is visited. Suppose we take to be small enough such that takes on a very large value of for each , then the probability of getting a regeneration given a visit to is . Being overoptimistic that the Markov chain visits with probability close to , it would still take 100 billon iterations for the chain to regenerate about twenty times, barely enough for the RS method to be effective.

Using the EB estimate of , estimation of the remaining parameters and prediction of the spatial random field can be done in the standard method using MCMC samples from (see e.g. Roy et al., 2016, section 3.2). Thus we can produce the root rot disease prediction map similar to that in Roy et al. (2016, Web Fig. 10).

6 Discussion

In this paper we consider two separate but related problems. The first problem is estimating the ratios of unknown normalizing constants given Markov chain samples from each of the probability densities. The second problem is estimating expectations of a function with respect to a large number of probability distributions. These problems are related in the sense that generalized IS estimators used for the latter utilize estimates derived when solving the first problem. The first situation also arises in a variety of contexts other than the generalized IS estimators.

For both problems, we derive estimators with flexible weights and thus these estimators are appropriate for Markov chains with different mixing behaviors. We establish CLTs for these estimators and develop BM methods for consistently estimating their SEs. These easy to calculate SEs are important for at least three reasons. First, SEs are needed to assess the quality of the estimates. Second, our ability to calculate SEs allows us to search for optimal weights for both stage 1 and 2. And last but not least, SEs form the basis for comparison of generalized IS with other available methods for estimating large number of (ratios of) normalizing constants.

Although we compare BM and RS in this paper, spectral estimators can also be derived for variance estimation using the results in Vats et al. (2015b). However, estimation by spectral methods is generally more expensive computationally. Further, Flegal and Jones (2010) compare the performance of confidence intervals produced by BM, RS and spectral methods for the time average estimator, and they conclude that if tuning parameters are chosen appropriately, all these three methods perform equally well. Control variates can be used to further improve the accuracy of our generalized IS estimators (Owen and Zhou, 2000; Doss, 2010). A direction of future research would be to establish a BM estimator of the SEs for control variate based methods.

Appendix A Proof of Theorem 1

In the appendices, we denote Doss and Tan (2014) by D&T. The proof of the consistency of follows from D&T section A.1 and is omitted. Establishing a CLT for is analogous to section A.2 of D&T, but there are significant differences. Below we establish the CLT for and finally show that is a consistent estimator of .

We begin by considering . As before, let represents the gradient operator. We expand at around , and using the appropriate scaling factor, we get

| (A.1) |

where is between and . Consider the left side of (A.1), which is just , since . There are several nontrivial components to the proof, so we first give an outline.

-

1.

Following D&T we show that each element of the vector can be represented as a linear combination of mean averages of functions of the chains.

-

2.

Based on Step , applying CLT for each of the Markov chain averages, we obtain a CLT for the scaled score vector. In particular, we show that , where defined in (2.8) involves infinite sums of auto-covariances of each chain.

- 3.

-

4.

We conclude that .

-

5.

Since and , where is defined in (2.4), by the Delta method it follows that where

We now provide the details.

-

1.

Start by considering . For , from D&T we have

(A.2) That is, (A.2) can be used to view as a linear combination of mean averages of functions of the chains.

-

2.

Next, we need a CLT for the vector , that is, to show that as . Note that,

where and is as defined in (2.6). Since for all , and , we have for any . Then since is polynomially ergodic of order , we have asymptotic normality for the univariate quantities (see e.g. Corollary 2 of Jones, (2004)). Since for and ’s are known, by independence of the chains, we conclude that

where is defined in (2.8). Next, we extend the component-wise CLT to a joint CLT. Consider any , we have

Hence, the Cramér-Wold device implies the joint CLT,

(A.3)

Steps 3-5 are omitted since the derivations are basically the same as in D&T.

Next we provide a proof of the consistency of the estimate of the asymptotic covariance matrix , that is, we show that as . Since and , it implies that . From D&T, we know that and using the spectral representation of and of , it follows that .

To complete the proof, we now show that where the BM estimator is defined in (2.13). This will be proved in couple of steps. First, we consider a single chain used to calculate quantities and establish a multivariate CLT. We use the results in Vats et al. (2015a) who obtain conditions for the nonoverlapping BM estimator to be strongly consistent in multivariate settings. Second, we combine results from the independent chains. Finally, we show that is a strongly consistent estimator of .

Denote . Similar to deriving (A.3) via the Cramér-Wold device, we have the following joint CLT for :, as , where is a covariance matrix with

| (A.4) |

The nonoverlapping BM estimator of is given in (2.10). We now prove the strong consistency of . Note that is defined using the terms ’s which involve the random quantity . We define to be with substituted for , that is,

where with . We prove in two steps: (1) and (2) . Strong consistency of the multivariate BM estimator requires both and . Since for all , for any , is polynomially ergodic of order , and where , it follows from Vats et al. (2015a) that as . We show where and are the th elements of the matrices and respectively. By the mean value theorem (in multiple variables), there exists for some , such that

| (A.5) |

where represents the dot product. Note that

where and . Some calculations show that for

and

We denote , , and similarly the centered versions of and by and respectively. Since is uniformly bounded by 1 and is polynomially ergodic of order , there exist such that , , and . We have

It is easy to see that the negative term in the above expression goes to zero as . Further, since

we have

where the last step above is due to strong consistency of the BM estimators for the asymptotic variances of the sequences and respectively. Similarly, we have

Note that the terms , etc, above actually depends on , and we are indeed concerned with the case where takes on the value , lying between and . Since, , as . Let denotes the norm of a vector . So from (A.5), and the fact that is bounded with probability one, we have

Appendix B Proof of Theorem 2

As in Buta and Doss (2011) we write

| (B.1) |

First, consider the 2nd term, which involves randomness only from the 2nd stage. From (3.3) note that . Then from (3.1) we have

Since is polynomially ergodic of order and is finite where , it follows that where is defined in (3.4). As and the Markov chains ’s are independent, it follows that .

Now we consider the 1st term in the right hand side of (B.1). Letting , by Taylor series expansion of about we have

| (B.2) |

where is between and . Simple calculations show that

| (B.3) |

where is defined in (3.5). We know that . Using similar arguments as in Buta and Doss (2011), it follows that is bounded in probability. Thus from (B.2) we have

Then Theorem 2 (1) follow from (B.1) and the independence of the two stages of Markov chain sampling.

Next to prove Theorem 2 (2), note that, we already have a consistent BM estimator of . From (B.3), we have . Applying mean value theorem on and the fact that is bounded in probability, it follows that . Writing as , it then follows that .

We now show is a consistent estimator of where and are defined in (3.4) and (3.7), respectively. Since the Markov chains are independent, it then follows that is consistently estimated by completing the proof of Theorem 2 (2).

If is known from the assumptions of Theorem 2 (2) and the results in Vats et al. (2015a), we know that is consistently estimated by its BM estimator . Note that, is defined in terms of the quantities ’s. We now show that

Denoting by , by the mean value theorem (in multiple variables), there exists for some , such that . For any , and ,

| (B.4) |

Let and . Note that, there exists, such that , and . Simple calculations show that

Hence, letting , we write

where and is similarly defined. Note that, there exists , such that , and . From (B.4) we have

Then using similar arguments as in the proof of Theorem 1, it can be shown that is bounded with probability one. Then it follows that

Appendix C Proof of Theorem 3

As in the proof of Theorem 2 we write

| (C.1) |

First, consider the 2nd term, which involves randomness only from the 2nd stage. Since

we have . Then from (3.1) we have

| (C.2) |

From the conditions of Theorem 3 and the fact that the Markov chains are independent, it follows that the above vector (C.2) converges in distribution to the bivariate normal distribution with mean and covariance matrix defined in (3.9). Then applying the Delta method to the function we have a CLT for the ratio estimator , that is, we have where is defined in (3.10).

Next letting , by Taylor series expansion of about we have

| (C.3) |

where is between and . Simple calculations show that

| (C.4) |

where and are defined in (3.11) and (3.12) respectively. It can be shown that is bounded in probability. Thus from (C.3) we have . Then Theorem 3 (1) follow from (C.1) and the independence of the two stages of Markov chain sampling.

Next to prove Theorem 3 (2), note that, we already know that is a consistent BM estimator of . From (C.4), we have . Applying mean value theorem on and the fact that is bounded in probability, it follows that .

From (3.8) we know that . From (3.13) we know . Since , it follows that . Thus . Thus to prove Theorem 3 (2), we only need to show that .

If is known from the assumptions of Theorem 3 (2) and the results in Vats et al. (2015a), we know that is consistently estimated by its BM estimator . We now show that

From Theorem 2 (2), we know that . We now show . Letting by , by the mean value theorem, there exists for some , such that . For any , and ,

Let and . Note that, there exists, such that , and . Simple calculations show that

Hence, letting , we write

where and is similarly defined. Note that, there exists , such that , and . The rest of the proof is analogous to Theorem 2, in that we have

Then it can be shown and finally .

Appendix D Regeneration with general weights

Tan et al. (2015) provide a regeneration based central limit theorem (CLT) for the estimators and defined in 1.3 and 3.1 respectively in the main text. In the case when is unknown, they allow only a special choice for the weight vector, namely for their results to hold, where is the estimator of based on the Stage 1 chains discussed in Section 2 of the main text. In this section, we establish a regeneration based CLT for and with any choice of the weight vector .

We will refer to the following conditions.

-

A1

For each , the Markov chain is geometrically ergodic and has as its invariant density.

-

A2

Let be the Markov transition density for , so that for any measurable set we have . Suppose that for each , satisfies the following minorization condition:

(D.1) where the function with , and is a probability density function on X.

-

A3

Recall the functions and defined in (3.2) of our paper. There exists such that and are finite.

-

A4

Suppose is simulated for regenerative tours for . Assume as .

Following Tan et al. (2015), let the regeneration times for the Markov chain be . Accordingly, the chain is broken up into “tours” that are independent stochastic replicas of each other. Suppose we simulate tours of the Markov chain for , so the length of the chain is . Also as in Tan et al. (2015), for define

| (D.2) |

where the sums range over the values of that constitute the tour.

Recall from Remark 4 in Section 3 of our paper, when is unknown, we set where denotes component-wise multiplication. That is, for any pre-determined weight . With this choice, the expressions for and in (3.2) become

| (D.3) |

The above quantities do not involve , and consequently for each , the triples defined in (D.2) are iid, and we have independence across ’s. The estimator for reduces to

| (D.4) | ||||

where

be the average tour length and, analogously, and . Similarly, the estimator for reduces to

| (D.5) |

Theorem 4 below gives the asymptotic distributions of and . It extends Tan et al.’s (2015) Theorem 2 to the general choice of weight vector . To state the theorem, we first need to define some notation. Let and be the vectors of length for which the coordinates are, for ,

| (D.6) |

As in Tan et al. (2015), assume that in Stage , for , the chain has been run for regenerations. So the length of the chain, , is random. We assume that in such a way that , for .

Theorem 4 Suppose that for the Stage chains, conditions A1 and A2 hold, and that for the Stage chains, conditions A1–A4 hold. If and in such a way that , then

and

where , are given in equations (D.6), , and are given in equations (2.15), (2.8), and (2.10) of Tan et al. (2015), respectively. In their (2.8) and (2.10), is taken to be . Furthermore, we can form strongly consistent estimates of the asymptotic variances if we use , , and defined in (2.16) and (2.11) of Tan et al. (2015), respectively, and use the standard empirical estimates of and .

D.1 Proof of Theorem 4

We first prove the CLT for . Note that

| (D.7) |

The second term on the right side of (D.7) involves randomness coming only from Stage sampling, and its distribution is given by Theorem 1 of Tan et al. (2015): it is asymptotically normal with mean and variance . The first term involves randomness from both Stage and Stage sampling. However, as in the proofs of Theorem 2 and 3, we can show that for this term, the randomness from Stage is asymptotically negligible, so that only Stage sampling contributes to its asymptotic distribution. Finally, the asymptotic normality of the left side of (D.7) follows since the two stages of sampling are independent. We now provide the details of the proof.

Consider the first term on the right side of (D.7). Recall that if , then

With (D.4) and (D.5) in mind, define the function

for , with for , and . Note that setting gives , and setting gives .

By a Taylor series expansion of about we get

where is between and . As , for each . We first show that the gradient converges almost surely to a finite constant vector by proving that each one of its components, , converges almost surely as . As for , for , we have

The expression above corresponds to , which is defined in (D.6), and it is finite by assumption . Next, we show that the random Hessian matrix is bounded in probability, i.e., each element of this matrix is . As for , for any , we have

where the limits are also finite.

Now, we can rewrite (D.7) as

Since from Tan et al. (2015) we have and the two sampling stages are assumed to be independent, we conclude that

The proof of the CLT for is similar. As in (D.7), we have

| (D.8) |

The asymptotic distribution of the second term in (D.8) is given in Tan et al.’s (2015) Theorem 1. The first term is linear in :

| (D.9) |

For , the coefficient of in (D.9) converges almost surely to , which is the term defined in (D.6).

Finally, from the independence of the two terms in (D.8) we conclude that

Appendix E Toy example

In this section, we follow up on the simulation studies that involve t distributions from Section 4 of the main text to verify Theorems 1-3. We also discuss different weights in forming generalized IS estimators and their effects on estimates of expectations and ratios of normalizing constants.

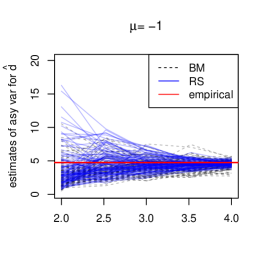

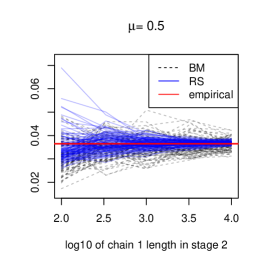

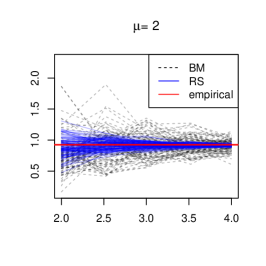

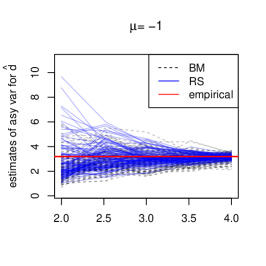

Let denote the t-distribution with degree of freedom and central parameter . We consider and as the density functions for a and , respectively. For simplicity, let for . Our plan is to first estimate the ratio between the two normalizing constants, . Then we will study a sea of -distributions where is a fine grid over , say . For each , we assume that and we estimate the ratio between its normalizing constant and , denoted by . We also estimate the expectation of each distribution in , denoted or for short. Clearly, the exact answers are and for any . Nevertheless, we follow the two-stage procedure from Sections 2 and 3 to generate Markov chains from and and build MCMC estimators from Theorems 1-3. The primary goal is to compare the performance of BM and RS estimators.

We draw iid samples from and Markov chain samples from using the so called independent Metropolis Hastings algorithm with proposal density . For RS, we follow the idea of Mykland et al. (1995, Section 4.1) on constructing minorization conditions to identify regeneration times. Based on a carefully tuned minoration condition, the Markov chain for regenerates about every 3 iterations on average. In contrast, for users of the BM method proposed in this paper, no such theoretical development is needed. For we draw observations from in stage 1 and observations from in stage 2. We set and . Recall the reason for smaller stage 2 sample sizes is due to computing cost. For completeness, note generating Markov chain samples using RS results in a random chain length so these chains were run in such a way that and .

For estimators based on stage 1 samples, Theorem 1 allows any choice of weight, . For estimators based on stage 2 samples, Theorem 2 and 3 allow any choice of weight, , in constructing consistent BM estimators of the asymptotic variances. RS based estimators in stage 2 are calculated using Theorems stated in Doss and Tan (2014) and Tan et al. (2015) with a general weight choice noted in Remark 4. This is an important generalization in that now any non-negative numerical weight vector can be used. We discuss the choice of weights and their impact on the estimators later in this section.

The following details the simulation study presented in the main text. We consider increasing sample sizes from to in order to examine trace plots for BM and RS estimates. The two stage procedure is repeated 1000 times independently. The unknown true value of the asymptotic variance of is estimated by its empirical asymptotic variance over the replications at . We consider the naive weight, , that is proportional to the sample sizes, and an alternative that weighs the iid sample more than the Markov chain sample. As illustrated in Figure 1 of the main text, both the BM and the RS estimates approach the empirical asymptotic variance as the sample size increases suggesting consistency. Similarly for stage 2, Figure 4 shows convergence of the BM and the RS estimates to the corresponding empirical asymptotic variances of and . Plots for other show similar results, but are not included here.

Overall, the simulation study suggests BM and RS methods provide consistent estimators for the true asymptotic variance. RS estimators enjoy smaller mean squared error in most cases. Nevertheless, when the number of regenerations is not great, BM estimators could be the more stable estimator. For example, in the top left panel of Figure 4, at stage 2 sample size , or about regenerations for chain 2, the RS method substantially over-estimated the target in about of the replications. Further, in the cases where regeneration is unavailable or the number of regenerations is extremely small, then BM would be the more viable estimator.

E.1 Choice of stage 1 weights

For stage 1, we recommend obtaining a close-to-optimal weight using a pilot study described in Doss and Tan (2014). In short, one can generate samples of small size from and , estimate and its asymptotic variance based on Theorem 1 for a grid of weights, and then identify the weight that minimizes the estimated variance. With a small pilot study based on samples of size from both distributions, we obtained . As depicted by the horizontal lines accross the pictures in Figure 1 of the main text, the asymptotic variance of the estimator based on is approximately , which is more than smaller than of the estimator based on the naive choice . Note that the naive weight is proportional to the sample sizes from and , which is asymptotically optimal if both samples were independent. However, since sample 2 is from a Markov chain sample, using a weight that appropriately favors the independent sample has lead to smaller error in the estimator. The gain in efficiency using a close-to-optimal weight will be more pronounced if the difference in the mixing rates of the two samples is larger.

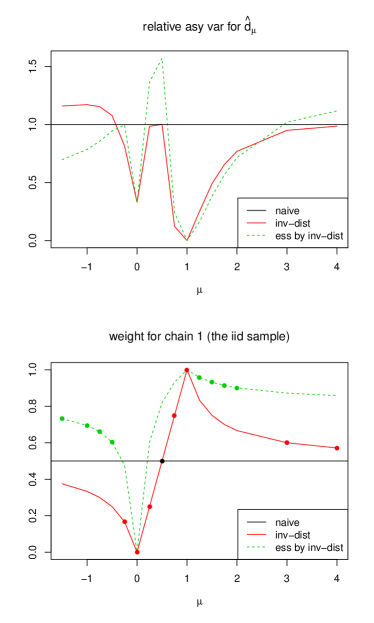

E.2 Choice of stage 2 weights

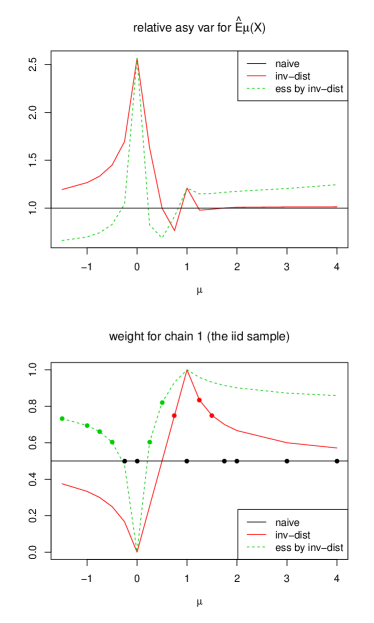

In stage 2, for each , the asymptotic variance of and are minimized at different weights. Instead of searching for each of the optimal weights in a pilot study, it is more practical to set sub-optimal weights using less costly strategies. Below, we perform a simulation study to examine three simple weighting strategies:

-

1.

naive: ,

-

2.

inverse distance (inv-dist): ,

-

3.

effective sample size (ess) by inverse distance (inv-dist): .

Using each of the three strategies, we construct generalized IS estimators for and for a grid of values between and . Note that samples are drawn from two reference distributions indexed by and respectively. Hence our simulation study concerns both interpolation and extrapolation. A summary of their performance is provided in Figure 5, and detailed results for selected simulation setups are shown in Figures 4, 6, and 7 for strategies 1, 2, and 3, respectively. Figure 5 suggests that none of the three strategies is uniformly better than the others. In particular, we observe the following.

-

1.

For estimating

-

(a)

For , strategy 2 works the best.

-

(b)

For , strategies 2 and 3 work better than strategy 1. Indeed, both of them simply set their stage 2 estimates to be the stage 1 estimate, . This would be a better choice than strategy 1 because in a two-step procedure, stage 1 chains are often much longer than stage 2 chains, and hence is already a very accurate estimate for .

-

(c)

For , strategies 2 and 3 generally lead to more stable estimates of . However, all strategies lead to very large asymptotic variances for . Hence, one needs to be mindful when doing extrapolation with IS estimators — always obtain an estimate of the standard error, or reconsider the placement of the reference points.

-

(a)

-

2.

For estimating

-

(a)

For , strategy 2 works the best in general, while strategy 3 is very unstable.

-

(b)

For either or , strategy 2 and 3 are the same, and they only utilize the reference chain from . This was a wise choice for estimating as explained before, but not so for other quantities of interest.

-

(c)

For , all strategies lead to fairly large asymptotic variances, especially for .

-

(a)

Overall in stage 2, strategy 2 has an advantage when the estimands are ratios between normalizing constants. However, when estimating , the situation is more complicated. Our impression is that assigning any extreme weight will lead to high variability in the estimator. So it is reasonable to simply use the naive weight, or other strategies that bound the weights away from and .

Appendix F Bayesian variable selection models

Here, we consider a class of Bayesian variable selection (BVS) models for linear regression with independent normal priors on the regression coefficients. This model involves a 2-dimensional prior hyperparameter that influences inference, yet no default choice guarantees good performance in practice. Hence, displaying the effect of different hyperparameter values on the posterior distribution would greatly benefit users of the model. When the number of predictors, , is large, the computing is challenging. Our solution is to obtain MCMC samples for a small number of models with different hyperparameter values, based on which generalized IS estimates can be obtained for BFs and other posterior expectations for a large number of models. Again, an important problem in practice is how long the Markov chains need to be run? In this context, the only affordable method that we are aware of is to estimate the SE of these IS estimators using the proposed BM method.

As introduced by Mitchell and Beauchamp (1988), let denote the vector of responses and denote potential predictors, each a vector of length . The predictors are standardized, so that for , and , where is the vector of ’s. The BVS model is given by:

| (F.1a) | ||||||

| (F.1b) | ||||||

| (F.1c) | ||||||

| (F.1d) | ||||||

The binary vector identifies a subset of predictors, such that is included in the model if and only if , and denotes the number of predictors included. So (F.1a) says that each corresponds to a model given by where is an sub-matrix of that consists of predictors included by , is the vector that contains corresponding coefficients, and . It is sometimes more convenient to use the notation, , where has one more column of ’s than and . Unknown parameters are for which we set a hierarchical prior in (F.1b) to (F.1d). In (F.1d), an independent Bernoulli prior is set for , where is a hyperparameter that reflects the prior inclusion probability of each predictor. In (F.1c), a non-informative prior is set for . In (F.1b), an independent normal prior is assigned to , where is a second hyperparameter, that controls the precision of the prior. Overall, is given an improper prior due to (F.1c) but the posterior of is indeed proper.

One can actually integrate out and arrive at the following model with parameter only:

| (F.2) |

Here, is a constant depending only on the sample size . Further, , where is a diagonal matrix, the main diagonal of which is the -dimensional vector . Finally, .

Using the model at (F.2) requires specification of the hyperparameter . Smaller values assign high prior probabilities to models with fewer predictors, and priors with smaller values allow selected predictors to have large coefficients. It is common to set (a uniform prior on the model space) and (a unit information prior for uncorrelated predictors, see e.g. Kass and Raftery (1995)). One can also choose adaptively, say according to the marginal likelihood . A small value of indicates that the prior is not compatible with the observed data, while is defined to be the empirical Bayesian choice of . The empirical Bayes idea has been successfully applied to various models with variable selection components (see e.g. George and Foster (2000); Yuan and Lin (2005)). However, we have not seen this idea being carried out for the model in (F.1), except where and the design matrices are orthogonal (Johnstone and Silverman (2005); Clyde and George (2000)). Due to the improper prior in (F.1d), is not uniquely defined. Nevertheless, the Bayes factor among any two models, say , is well-defined because the same improper prior is assigned to the shared parameters of the two models (see e.g. Kass and Raftery (1995, sec.5) and Liang et al. (2008, sec.2)).

Here, we concentrate on two goals. The first is to evaluate , the marginal likelihood of model relative to a reference model , which allows us to identify the empirical Bayesian choice of . The second is to evaluate the posterior mean of the vector of coefficients for each , which we denote by . Predictions can then be made for new observations using .

For model (F.2) with a fixed , a Metropolis Hastings random-swap algorithm (Clyde et al. (2011)) can be used to generate Markov chains of from its posterior distribution. In each iteration, with probability , we propose flipping a random pair of and in , and with probability , we propose changing to for a random while leaving other coordinates untouched. We set when corresponds to the null model or the full model, and otherwise. Finally, the proposal is accepted with an appropriate probability. Since this Markov chain lies on a finite state space, it is uniformly ergodic and hence polynomially ergodic as well. Further, moment conditions in Theorems 2 and 3 are satisfied because they reduce to summations of terms, a large but finite number. To achieve the goal, we generate Markov chains of with respect to model (F.2) at several values that scatters in , from which we build generalized IS estimators, and estimate their standard errors.

F.1 Cookie dough data

We demonstrate the aforementioned sensitivity analysis using the biscuit dough dataset (Osborne et al. (1984); Brown et al. (2001)). The dataset, available in the R package ppls (Kraemer and Boulesteix (2012)), contains a training set of observations and a test set of observations. These data were obtained from a near-infrared spectroscopy experiment that study the composition of biscuit dough pieces. For each biscuit, the reflectance spectrum is measured at evenly spaced wavelengths. We use these measurements as covariates to predict the response variable, the percentage of water in each dough. We follow previous studies (Hans (2011)) and thin the spectral to evenly spaced wavelengths.

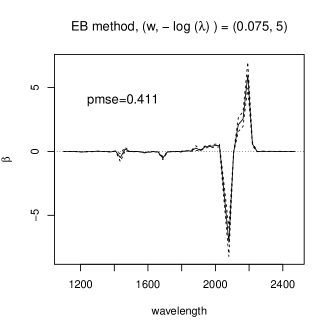

Figure 8 provides a general picture of the sensitivity analysis. The left plots provide two ways to visualize estimates of the BFs. To form the plot, we took the reference values of to be such that . In stage we ran each of the Markov chains at the above values of for iterations to obtain . In stage , we ran the same Markov chains for iterations each, to form the estimates over a fine grid that consists of different values, with the component ranging from to in increments of and the component ranging from to in increments of .

How trustworthy are these BF estimates? Their estimated standard errors are obtained using the BM method, based on Theorem 2. We choose to display the relative SE with respect to the BF estimates, as shown in the upper right panel of Figure 8. The relative SEs are smaller than or equal to , and we believe the BF estimates are accurate enough. Finally, the lower-right panel of Figure 8 shows the prediction mean squared error (pmse) over the test set for all .

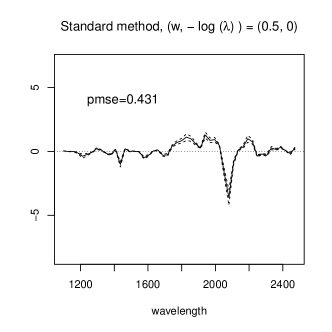

Based on our estimation, the BF attains the maximum value at . Recall when comparing any two models indexed by and respectively, the BF between them is given by . Also, according to Jeffreys (1998) and Kass and Raftery (1995), the evidence for over is considered to be strong only if is greater than or . Hence, all with BF over or times the maximum BF can be considered as reasonably well supported by the data as that of the empirical Bayesian choice. Comparing the lower two plots of Figure 8, we see that the set for and do overlap with an area that corresponds to relatively small pmse. Outside , a region that consists of larger and smaller also enjoys small pmse values, at around to . This region includes the common choice of . These suggest that and its vicinity might not be the only area of that has good prediction performances.

To better compare the effect of and the commonly used , Figure 9 displays the estimated posterior mean of regression coefficients at both choices of , together with the point-wise confidence intervals for the posterior means. Due to the small size of and , the empirical Bayesian method yields a model with a few covariates that have big coefficients. In comparison, the common choice has larger and values, leading to a regression model that combines more covariates each having smaller effects. It turns out these two opposite strategy of modeling both predict the test dataset well, with pmse being and respectively. For comparison, pmses were calculated for several frequentist penalized linear regression methods with their respective penalty parameters chosen by -fold cross validation. The resulting pmses for the ridge, the lasso and the elastic net method are , and , respectively.

The BM method for estimating SE is carried out above without the need of further user input. Theoretically, its competitor RS can be developed too, if enough regeneration times can be identified for each Markov chain. Recall that with the random-swap algorithm, each Markov chain lives on the discrete state space of size . A naive way to introduce regeneration is to specify a single point , then each visit of the Markov chain to marks a regeneration time. Note that the chance of visiting converges to , the posterior probability of . In our BVS model with states of , even could be very small. Take for example the Markov chain for the BVS model with , the point with the highest frequency appeared only out of a run of iterations. And that the waiting times between consecutive regenerations are highly variable, which ranges from less than ten iterations to a few thousand iterations. To obtain alternative schemes of identifying regeneration times, one can take the general minorization condition approach. It could potentially increase the chance of regeneration and reduce variability of the waiting times. Specifically, for any , one could define to contain the points with the highest posterior probabilities, and find and a probability mass function such that for all . Note that as increases, the chance of visiting improves, but , the conditional rate of regeneration given the current state is in , would decrease sharply. Finding a good to maximize the overall chance of regeneration requires tuning that is specific for both the model specification and the dataset. Even if we can find the optimal for each Markov chain used in the example, it is unlikely that all of them would regenerate often enough for the RS estimator to be stable.

References

- Brown et al. (2001) Brown, P. J., Fearn, T. and Vannucci, M. (2001). Bayesian wavelet regression on curves with application to a spectroscopic calibration problem. J. Amer. Statist. Assoc. 96 398–408.

- Buta and Doss (2011) Buta, E. and Doss, H. (2011). Computational approaches for empirical Bayes methods and Bayesian sensitivity analysis. Ann. Statist. 39 2658–2685.

- Clyde and George (2000) Clyde, M. and George, E. I. (2000). Flexible empirical Bayes estimation for wavelets. J. R. Stat. Soc. Ser. B. Stat. Methodol. 62 681–698.

- Clyde et al. (2011) Clyde, M. A., Ghosh, J. and Littman, M. L. (2011). Bayesian adaptive sampling for variable selection and model averaging. J. Comput. Graph. Statist. 20.

- Cappe et al. (2004) Cappé, O. and Guillin, A. and Marin, J. M. and Robert, C. P.(2004). Population Monte Carlo. J. Comput. Graph. Statist. 13 907–929.

- Christensen (2004) Christensen, O. F. (2004). Monte Carlo maximum likelihood in model based geostatistics. J. Comput. Graph. Statist. 13 702–718.

- Diggle et al. (1998) Diggle, P. J., Tawn, J. A. and Moyeed, R. A. (1998). Model-based geostatistics. Applied Statistics 47, 299–350.

- Doss (2010) Doss, H. (2010). Estimation of large families of Bayes factors from Markov chain output. Statist. Sinica, 20 537–560.

- Doss and Tan (2014) Doss, H. and Tan, A. (2014). Estimates and standard errors for ratios of normalizing constants from multiple Markov chains via regeneration. J. R. Stat. Soc. Ser. B. Stat. Methodol. 76 683–712.

- Elvira et al. (2015) Elvira, V. and Martino, L. and Luengo, D. and Bugallo, M. F. (2015). Generalized multiple importance sampling. ArXiv e-prints.

- Evangelou and Roy (2015) Evangelou, E. and Roy, V. (2015). geoBayes. http://cran.r-project.org/web/packages/geoBayes. R package version 0.3-3.

- Flegal et al. (2008) Flegal, J. M. and Haran, M. and Jones, G. L. (2008). Markov chain Monte Carlo: Can we trust the third significant figure? Statist. Sci. 23 250–260.

- Flegal and Jones (2010) Flegal, J. M. and Jones, G. L. (2010). Batch means and spectral variance estimators in Markov chain Monte Carlo. Ann. Statist., 38:1034–1070.

- George and Foster (2000) George, E. and Foster, D. (2000). Calibration and empirical Bayes variable selection. Biometrika 87 731.

- Geyer (1994) Geyer, C. J. (1994). Estimating normalizing constants and reweighting mixtures in Markov chain Monte Carlo. Tech. Rep. 568r, Department of Statistics, University of Minnesota.

- Gilks et al. (1998) Gilks, W. R., Roberts, G. O. and Sahu, S. K. (1998) Adaptive Markov chain Monte Carlo through regeneration. J. Amer. Statist. Assoc. 93 1045–1054.

- Gill et al. (1988) Gill, R. D., Vardi, Y. and Wellner, J. A. (1988). Large sample theory of empirical distributions in biased sampling models. Ann. Statist. 16 1069–1112.

- Hans (2011) Hans, C. (2011). Elastic net regression modeling with the orthant normal prior. J. Amer. Statist. Assoc. 106 1383–1393.

- Hastings (1970) Hastings, W. K. (1970). Monte Carlo sampling methods using Markov chains and their applications. Biometrika 57 97–109.

- Jeffreys (1998) Jeffreys, H. (1998). The theory of probability. 3rd ed. Oxford.

- Johnstone and Silverman (2005) Johnstone, I. M. and Silverman, B. W. (2005). Empirical Bayes selection of wavelet thresholds. Ann. Statist. 33 1700–1752.

- Jones, (2004) Jones, G. L. (2004). On the Markov chain central limit theorem. Probab. Surv., 1:299–320.

- Jones and Hobert (2004) Johns, G. and Hobert, J. (2004). Sufficient Burn-in for Gibbs Samplers for a Hierarchical Random Effects Model. Ann. Statist. 32 784–817.

- Kass and Raftery (1995) Kass, R. E. and Raftery, A. E. (1995). Bayes factors. J. Amer. Statist. Assoc. 90 773–795.

- Koehler et al. (2009) Koehler, E. and Brown, E. and Haneuse, S. (2009). On the assessment of Monte Carlo error in simulation-based statistical analyses. Amer. Statist. 63 155–162.

- Kong et al. (2003) Kong, A., McCullagh, P., Meng, X.-L., Nicolae, D. and Tan, Z. (2003). A theory of statistical models for Monte Carlo integration (with discussion). J. R. Stat. Soc. Ser. B. Stat. Methodol. 65 585–618.

- Kraemer and Boulesteix (2012) Kraemer, N. and Boulesteix, A. (2012). ppls: Penalized partial least squares, r package version 1.05.

- Liang et al. (2008) Liang, F., Paulo, R., Molina, G., Clyde, M. A. and Berger, J. O. (2008). Mixtures of -priors for Bayesian variable selection. J. Amer. Statist. Assoc. 103 410–423.

- Meng and Wong (1996) Meng, X.-L. and Wong, W. H. (1996). Simulating ratios of normalizing constants via a simple identity: A theoretical exploration. Statist. Sinica 6 831–860.

- Mengersen and Tweedie (1996) Mengersen, K. L. and Tweedie, R. L. (1996). Rates of convergence of the Hastings and Metropolis algorithms. Ann. Statist. 24 101–121.

- Mitchell and Beauchamp (1988) Mitchell, T. and Beauchamp, J. (1988). Bayesian variable selection in linear regression. J. Amer. Statist. Assoc. 83 1023–1036.

- Meyn and Tweedie (1993) Meyn, S. P. and Tweedie, R. L. (1993). Markov Chains and Stochastic Stability. Springer-Verlag, New York, London.

- Mykland et al. (1995) Mykland, P., Tierney, L. and Yu, B. (1995). Regeneration in Markov chain samplers. J. Amer. Statist. Assoc. 90 233–41.

- Osborne et al. (1984) Osborne, B. G., Fearn, T., Miller, A. R. and Douglas, S. (1984). Application of near infrared reflectance spectroscopy to the compositional analysis of biscuits and biscuit doughs. Journal of the Science of Food and Agriculture 35 99–105.

- Owen and Zhou (2000) Owen A. and Zhou, Y. (2000). Safe and effective importance sampling. J. Amer. Statist. Assoc. 95 135-143.

- Roy (2014) Roy, V. (2014) Efficient estimation of the link function parameter in a robust Bayesian binary regression model. Comput. Stat. Data. Anal., 73 87–102.

- Roy et al. (2016) Roy, V. and Evangelou, E. and Zhu, Z. (2016). Efficient estimation and prediction for the Bayesian binary spatial model with flexible link functions. Biometrics 72 289–298.

- Roy and Hobert (2007) Roy, V. and Hobert, J. P. (2007) Convergence rates and asymptotic standard errors for MCMC algorithms for Bayesian probit regression. J. R. Stat. Soc. Ser. B. Stat. Methodol. 69 607–623.

- Tan (2004) Tan, Z. (2004). On a likelihood approach for Monte Carlo integration. J. Amer. Statist. Assoc. 99 1027–1036.

- Tan et al. (2015) Tan, A. and Doss, H. and Hobert, J. P. (2015). Honest importance sampling with multiple Markov chains. J. Comput. Graph. Statist., 24 792–826.

- Tan and Hobert (2009) Tan, A. and Hobert, J. P. (2009). Block Gibbs sampling for Bayesian random effects models with improper priors: convergence and regeneration. J. Comput. Graph. Statist. 18 861-878.

- Tanner and Wong (1987) Tanner, M. A. and Wong, W. H. (1987) The calculation of posterior distributions by data augmentation(with discussion). J. Amer. Statist. Assoc. 82 528–550.

- Vardi (1985) Vardi, Y. (1985). Empirical distributions in selection bias models. Ann. Statist. 13 178–203.

- Vats et al. (2015a) Vats, D., Flegal, J. M., and Jones, G. L.. (2015a). Multivariate output analysis for Markov chain Monte Carlo. ArXiv e-prints.

- Vats et al. (2015b) Vats, D., Flegal, J. M., and Jones, G. L.. (2015b). Strong consistency of the multivariate spectral variance estimator in Markov chain Monte Carlo. ArXiv e-prints.

- Veach and Guibas (1995) Veach, E. and Guibas, L. (1995). Optimally combining sampling techniques for Monte Carlo rendering. SIGGRAPH 95 Conference Proceedings, Reading MA. Addison-Wesley, 419-428.

- Yuan and Lin (2005) Yuan, M. and Lin, Y. (2005). Efficient empirical Bayes variable selection and estimation in linear models. J. Amer. Statist. Assoc. 100 1215–1225.

- Zhang (2002) Zhang, H. (2002). On estimation and prediction for spatial generalized linear mixed models. Biometrics 58 129–136.

Department of Statistics, Iowa State University E-mail: vroy@iastate.edu

Department of Statistics and Actuarial Science, University of Iowa E-mail: aixin-tan@uiowa.edu

Department of Statistics, University of California, Riverside E-mail: jflegal@ucr.edu