On jump-diffusion processes with regime switching: martingale approach

Abstract.

We study jump-diffusion processes with parameters switching at random times. Being motivated by possible applications, we characterise equivalent martingale measures for these processes by means of the relative entropy. The minimal entropy approach is also developed. It is shown that in contrast to the case of Lévy processes, for this model an Esscher transformation does not produce the minimal relative entropy.

Key words and phrases:

jump-telegraph process; jump-diffusion process; martingales; relative entropy; financial modelling2000 Mathematics Subject Classification:

60G44; 60J75; 60K991. Introduction

We investigate some basic properties of the jump-diffusion processes

with time-dependent deterministic driving parameters switching simultaneously at random times. Here denotes the Wiener part, defined by the stochastic integral (w.r.t. Brownian motion ) of the process which is formed by switching at random times of the deterministic diffusion coefficients by is denoted the jump part, i.e. the stochastic integral (w.r.t. process counting number of the regime switchings) applied to the switching functions and is path-by-path integral in time of switching velocity regimes (see the detailed definitions in Section 2). In the case of and exponentially distributed inter-switching time intervals such processes are called telegraph-jump-diffusion processes, Ratanov (2010), or Markov modulated jump-diffusion.

In this paper the random inter-switching time intervals are assumed to be independent and arbitrary distributed. In general, such a process is not Markovian, and it is not a Lévy process as well. We study these processes from the martingale point of view, including Girsanov’s measure transform.

Similar models without a diffusion component were considered first in Melnikov and Ratanov (2007) and more recently have been analysed in detail by Di Crescenzo and Martinucci (2013); Di Crescenzo et al (2013), Ratanov (2015, 2013, 2014a), see also the particular cases in Di Crescenzo (2001); Di Crescenzo and Martinucci (2010). The model with missing jump component is presented in Di Crescenzo et al (2014); Di Crescenzo and Zacks (2015). The processes with random driving parameters are studied in Ratanov (2013). The recent paper Ratanov (2014b) is related to the model of random switching intensities.

This setting is widely used for applications, see e.g. Weiss (1994). The martingale approach developed in this paper is motivated by financial modelling, see Runggaldier (2004) for jump-diffusion model. See also Ratanov (2007) for jump-telegraph model (and a more detailed presentation in Kolesnik and Ratanov (2013)).

The Markov modulated jump-diffusion model of asset pricing (with additive jumps superimposed on the diffusion) has been studied before, see Guo (2001); Ratanov (2010). This model for a single risky asset possesses infinitely many martingale measures, and thus the market is incomplete. The model can be completed by adding a further asset; for the jump-diffusion model see Runggaldier (2004), and for the telegraph-jump-diffusion model see Ratanov (2010).

In this paper we explore another approach. We describe the set of equivalent martingale measures and determine the Föllmer-Schweizer minimal probability measure (so called the minimal entropy martingale measure (MEMM)), Föllmer and Schweizer (1990). In his seminal paper Fritelli (2000) Fritelli has showed the equivalence between maximisation of expected exponential utility and the minimisation of the relative entropy. Then, by this approach the models based on Lévy processes have been studied in Fujiwara and Miyahara (2003).

Observe that for Lévy processes and for regime switching diffusions the usual technique is based on an Esscher transform, which produces the MEMM, see Fujiwara and Miyahara (2003); Esche and Schweizer (2005) and Elliott et al (2005, 2007).

In our model this method does not work. The Esscher transform under regime switching does not affect the switching intensities. In the Lévy model Fujiwara and Miyahara (2003) this contradicts the minimal entropy condition (if the process is not already a martingale), see (5.4). In the case of the regime switching model Elliott et al (2005) some additional entropy given by the jumps embedded into this model can be reduced by more flexible measure transformation, see Section 5.

Moreover, in contrast with Lévy model and with the regime switching diffusions without jumps our model has the following important feature: the entropy minimum as well as calibration of MEMM depend on the time horizon under consideration.

The paper is organised as follows. Section 2 contains the definition and the main properties of the regime switching jump-diffusion processes with arbitrary distributions of inter-switching time intervals. We construct Girsanov’s transformation in Section 3. Then, we define the entropy and derive the corresponding Volterra equations. In Section 4 we describe the set of equivalent martingale measures for the regime switching jump-diffusion processes. The minimal entropy equivalent martingale measures are studied in Section 5 for the case of constant parameters.

Some applications including financial modelling will be presented elsewhere later.

2. Generalised telegraph-jump-diffusion processes. Distributions and expectations

Let be a complete probability space with the given right-continuous filtration satisfying the usual hypotheses, Jeanblanc and Chesney (2009). We start with a -state -adapted semi-Markov (see Jacobsen (2006)) random process The switchings occur at random times and process is right-continuous with left-hand limits.

Let be the counting process, .

2.1. The definition of telegraph-jump-diffusion process

For the set of deterministic measurable functions we construct first the piecewise deterministic random process combining by means of the switching process :

| (2.1) |

Here and is the indicator function. Process starts from the origin at the switching time ; at each further switching time the process is renewed.

Second, consider the integrals of of the following three types:

-

(1)

the generalised -state telegraph process (path-by-path integral)

(2.2) -

(2)

the pure jump process (integral w.r.t. counting process )

(2.3) -

(3)

the Wiener process (Itô integral)

(2.4) where is an -adapted Brownian motion, independent of . Note that is a Gaussian -martingale.

Let and be deterministic measurable functions. We assume that functions are locally integrable, and are locally square integrable,

In this paper we analyse the jump-diffusion process with switching regimes of the following form

| (2.5) |

with the components and which are defined by (2.2), (2.3) and (2.4) respectively. Process satisfies the stochastic equation

Equivalently, processes can be expressed by summing up the paths between the consequent switching instants :

| (2.6) | ||||

| (2.7) | ||||

| (2.8) |

where the following notations are used

| (2.9) |

Note that are deterministic and the variables are zero-mean normally distributed with the variances .

We say that the regime switching jump-diffusion process defined by (2.5)-(2.9) is characterised by the triplet with distributions of inter-switching time intervals which are determined by the hazard rate functions (see the definition in (2.11)).

We apply the notations and , if the initial state of the underlying process is given, .

Further, we will need the following explicit expression for the stochastic exponential of . It is known, see e.g. Jeanblanc and Chesney (2009), that

| (2.10) |

where Here is the telegraph process (2.6) with the velocities instead of and is the pure jump process (2.7) with the jump values instead of switching at random times

2.2. Semi-Markov process

In order to state the distribution of we introduce conditions on the driving processes and .

Denote by the transition probabilities of the form (Jacobsen, 2006, (3.17)):

Let Consider the hazard functions

Let functions be differentiable, . Thus the hazard functions are expressed by

Here

| (2.11) |

are the hazard rate functions, and are the density functions of the interarrival times. We assume the non-exploding condition to be hold:

| (2.12) |

Note that

| (2.13) |

The survival function of the first switching time is given by

| (2.14) |

where

| (2.15) |

Furthermore, let

| (2.16) |

Due to (2.13) is an inhomogeneous Poisson process with switchings at and with the instantaneous intensities .

If the process is observed beginning from the time the corresponding conditional distributions can be described by the following conditional survival functions,

| (2.17) |

with the density functions

Moreover, let

| (2.18) |

see (2.14).

Notice that

2.3. The distribution and expectation of

Our further analysis is based on the following observation.

Let be the first switching time, where is the fixed initial state of the process Owing to the renewal character of the counting process , see Cox (1962), we have the following equalities in distribution:

| (2.19) | ||||

where is the regime switching jump-diffusion process independent of which starts at time . Here is the indicator of event .

Let

be the density functions of . Note that , .

In these terms equalities (2.19) take the following form

| (2.20) | ||||

Here is the density function of the Gaussian random variable

where .

In the Markov case of two-state processes, with constant parameters and with exponentially distributed inter-switching times the distributions of and have been analysed in detail in Ratanov (2010).

Let us study the expectations

and

of the -state process

Note that . Moreover, for .

Proposition 2.1.

The expectations satisfy the following Volterra system of integral equations,

| (2.21) |

If functions solve system (2.21), then the conditional expectations are given by

| (2.22) |

Proof.

Corollary 2.2.

Proof.

Remark 2.3.

Condition (2.23) has the sense of Doob-Meyer decomposition. These type of conditions for the jump-telegraph processes appears first in (Ratanov, 2007, Theorem 1) in the case of constant deterministic parameters ( see also Kolesnik and Ratanov (2013)). In this case condition (2.23) is intuitively evident. It means that the displacement performed by the telegraph process during a time-period equal to the mean-switching-time is identical to the jump’s size performed in the opposite direction.

This intuitively explains why this is a martingale condition.

3. Girsanov’s transformation

In this section we analyse the problems which are important for applications, e.g. for financial modelling. First, we describe all possible martingales in our setting. Then, we derive a generalisation of Girsanov’s Theorem.

3.1. Martingale’s characterisation

Since the diffusion part is already a -martingale, it is sufficient to investigate the process

Theorem 3.1.

Let be the process with the parameters switching at random times Let the inter-switching times be distributed with hazard rate functions see (2.11), (2.15).

Process is a martingale if and only if the equalities in (2.23) are fulfilled.

Proof.

Notice that if jumps vanish, process is a martingale only in the trivial case: and thus see (2.23).

Corollary 3.2 (Ratanov (2010)).

Let be the jump-diffusion process with switching constant parameters and . Let .

Process is a martingale if and only if and the distributions of the inter-switching times are exponential, with parameters . In this case the underlying is a Markov process.

Remark 3.3.

In the paper by Di Crescenzo et al Di Crescenzo et al (2014) the generalised -state geometric telegraph-diffusion process with constant parameters and is studied,

where is a standard Brownian motion and the inter-switching times are independent and arbitrarily distributed. The authors expected that the process can be transformed in a martingale by superimposing of a jump component. This expectation is not justified.

The process is the stochastic exponential of After the inclusion of a jump component with constant jump amplitudes , such that processes and become martingales only in the standard case of exponentially distributed inter-arrival times, with constant intensities

(see Corollary 3.2).

3.2. Girsanov’s Theorem

The problem of existence and uniqueness of an equivalent martingale measure is extremely significant for applications, especially in the theory of financial derivatives. It is important to understand how the equivalent martingale measures can be constructed if such a measure exists.

Let be the switching process on the filtered probability space governed by the hazard rate functions of the inter-switching times, see (2.15), (2.11), satisfying the non-exploding condition (2.12).

Let and be measurable functions satisfying the martingale condition (2.23),

| (3.1) |

We assume to be locally integrable and Thus,

| (3.2) |

Furthermore, let

| (3.3) |

Consider the jump-diffusion martingale with regime switching, where

| (3.4) | ||||

Here, see (2.9),

where are locally square integrable functions.

Let be the stochastic exponential of . By (2.10)

| (3.5) | ||||

Here is the -state generalised telegraph process (2.6) with the velocity regimes instead of and is the pure jump process (2.7) with the jump values instead of

Theorem 3.4 (Girsanov’s Theorem).

Let measure be equivalent to under the fixed time horizon with the density

| (3.6) |

Under the measure

-

(a)

the inter-arrival times are independent and distributed with the survival functions

(3.7) The hazard rate functions of these distributions are given by

(3.8) and the non-exploding condition

(3.9) holds;

-

(b)

the process is the standard -Brownian motion, where is the generalised telegraph process with switching velocities i.e.

- (c)

Proof.

| (3.10) |

Hence, . Since by (3.1) and (3.8) is completely proved. The non-exploding condition (3.9) follows from (3.3).

The part (b) of the theorem follows from the classical Girsanov’s Theorem, see e.g. Jeanblanc and Chesney (2009), Proposition 1.7.3.1.

The part (c) holds by the following observation. The Wiener part of process under measure becomes , see part (b). Here is the -Wiener process, i.e. the Itô integral w.r.t. -Brownian motion , and is the -telegraph process which is driven by the subsequently switching velocities .

Therefore, under measure the process is still the jump-diffusion process with switching regimes,

characterised by . The theorem is proved. ∎

3.3. Relative entropy

Let and be two equivalent measures. Under the time horizon the relative entropy of w.r.t. is defined by the set of functions

| (3.11) |

see Fritelli (2000). Here the Radon-Nikodým derivative is presented by (3.5)-(3.6).

Theorem 3.5.

The relative entropy functions are expressed by

| (3.12) |

and satisfy the system of the integral equations

| (3.13) |

where functions are defined by

| (3.14) |

Here

| (3.15) | ||||

Proof.

Owing to (3.5)

| (3.16) |

where the alternating tendencies , the jump process and the Wiener process are defined by (3.4) (with instead of and instead of ).

It is easy to see that functions defined by (3.15) are non-negative, Hence, functions defined by (3.14) are also non-negative,

Remark 3.6.

By applying the Laplace transform to (3.13) one can obtain the system:

if the transformations exist. The above system yields the unique solution.

For example, if and (see (3.15)) are constants; if the alternating distributions of inter-arrival times are exponential, therefore in this simple case

where

| (3.17) |

This corresponds to the following explicit solution of (3.13): the relative entropy functions are expressed by

| (3.18) | ||||

4. Equivalent martingale measure

Consider the jump-diffusion process with the switching hazard rate functions of inter-arrival times see the definitions in (2.6)-(2.8).

Let the equivalent measure be defined by the Radon-Nikodým density , see (3.5)-(3.6). Let driving parameters and satisfy (3.1)-(3.3). By Theorem 3.4 under measure the hazard rate functions are defined by (3.8).

The family of the equivalent martingale measures for can be disclosed precisely.

Theorem 4.1.

Measure is the martingale measure for process if and only if

| (4.1) |

Proof.

This result is well known, see e.g. Bellami and Jeanblanc (2000), Proposition 3.1. The proof follows from Theorem 3.1 and Theorem 3.4.

Let measure be defined by (3.5)-(3.6). Then, by Theorem 3.4, part (c), under measure the process

is again the jump-diffusion process with switching regime. The martingale condition (2.23) of Theorem 3.1 becomes (4.1).

The theorem is proved. ∎

The relative entropy functions of the martingale measure w.r.t. solve system (3.13) with functions specified by (3.14) and (3.15). Driving parameters and switching intensities satisfy (3.8) and (4.1).

Consider the following examples when the equivalent martingale measure is unique.

Example 4.2 (Jump-telegraph process).

Assume, that almost everywhere,111If, in contrary, on a whole interval, then, due to (4.1) with we have no martingale measures (if on the interval ), or infinitely many ones (if with free fragment of hazard rate function ). and is of the opposite sign with

| (4.2) |

Moreover, let functions be locally integrable and

| (4.3) |

Then, by Theorem 4.1 the equivalent martingale measure exists and it is unique with the hazard rate functions of interarrival times defined by

| (4.4) |

Here (4.3) is the non-exploding condition for measure . The corresponding measure transformation is determined by the functions

if see (3.8) and (4.4). 222Measures and are equivalent. If -distribution of the interarrival times has a “dead” zone: for some time interval then due to (3.8) and (4.1) for any martingale measure the hazard rate function also vanishes on and

The entropy functions solve system (3.13) with

where are defined by (4.4). The survival functions are defined in (2.13).

If the inequalities (4.2) do not hold, the martingale measure does not exist.

In particular, if the parameters are constant such that with exponentially distributed inter-switching times, then by (4.4) under the martingale measure the inter-switching times are again exponentially distributed with the switching intensities If , then the closed form of the entropy functions is found, see Remark 3.6, formulae (3.17)-(3.18), and more detailed analysis in Section 5 below. In this case the unique martingale measure is defined by the Radon-Nikodým density (3.5)-(3.6) with constant and :

| (4.5) |

where are the new alternating intensities of the inter-switching times, see e.g. Kolesnik and Ratanov (2013).

Example 4.3 (Diffusion process).

Consider the diffusion process missing the jump component and switching, is locally integrable and functions are locally square integrable. Assume that

Let be an equivalent measure. In this case the Radon-Nikodým derivative of is defined by

where is the locally square integrable function. By Girsanov’s Theorem the process

is -Brownian motion. Hence, process takes the form

This is a martingale if and only if .

By (3.11) the relative entropy of w.r.t. is

Therefore, the relative entropy of the (unique) martingale measure is given by

Remark 4.4 (Diffusion process with switching tendencies and diffusion coefficients).

Consider the case of the diffusion process,

with the switching tendencies and diffusion coefficients where the jump component is missing.

In this case there are infinitely many equivalent martingale measures.

Theorem 4.1 shows that the measure transformation defined by see (3.5) with and eliminates the drift component similarly as in Example 4.3. Under measure process becomes the martingale of the form whereas by (4.1) the inter-switching times are arbitrary distributed. Here is the stochastic integral (2.8) based on -Brownian motion

This model has been analysed in Elliott et al (2005) by using the Esscher transform under switching regimes. This transformation does not affect the distribution of inter-switching times and the corresponding equivalent martingale measure is of the minimal relative entropy, see Elliott et al (2005), Proposition 3.1.

In the next section we study in detail the jump-diffusion model with switching regimes based on the Markov underlying process . We have discovered that in this case the Esscher transform does not produce the minimal relative entropy.

5. Esscher transform and minimal entropy martingale measure

Typically, the jump-diffusion model with switching regime has no martingale measure or it has infinitely many. The rare examples of the unique martingale measure are presented above (Example 4.2 and Example 4.3). In this section we discuss the case when the infinitely many martingale measures exist and discuss some methods to select one. The first method is based on the so-called the Esscher transform under switching regimes.

Let be the jump-diffusion process with switching regime, see (2.6)-(2.8), defined on the filtered probability space .

Let a. s. The case with missed diffusion () is analysed in Example 4.2.

To choose an equivalent martingale measure by a reasonable way consider the deterministic measurable functions which define the regime switching processes similarly as in (2.1). Let measure (equivalent to ) be defined by the density

| (5.1) |

Here see (2.10), and is the -augmentation of the natural filtration generated by . This particular choice of the new measure is named a regime switching Esscher transform (or exponential tilting), see Elliott et al Elliott et al (2005).

It is easy to see that

Therefore the Radon-Nikodým derivative of the Esscher transforms is given by

which corresponds to Radon-Nikodým derivative (3.5) with

| (5.2) |

Observe, that by Girsanov’s Theorem (see Theorem 3.4, equation (3.8)) due to (5.2) the distribution of inter-switching times are not changed under such defined measure, .

Hence, due to (5.2), the martingale condition (see Theorem 4.1, equation (4.1)) can be written as

| (5.3) |

It is known that the Esscher measure transform defined by (5.1) with parameters determined by (5.3) corresponds to the minimal relative entropy, see Elliott et al (2005), Proposition 3.1. The similar approach with the Esscher measure transform produces the minimal relative entropy in the case of Lévy processes (see Esche and Schweizer (2005); Fujiwara and Miyahara (2003)).

For our model based on Brownian motion with jumps and with switching regimes the Esscher transform does not produce the minimal relative entropy.

In the rest of this section for the sake of simplicity, we consider the Markov case with , when the alternating distributions of inter-switching times are exponential both under measure and under an equivalent measure , i.e.

and the driving parameters are constant. Here measure is defined by (3.4)-(3.6) with constant parameters satisfying (3.1)-(3.3).

To analyse the set of equivalent martingale measures from the viewpoint of the relative entropy we are looking for the solution of the integral equations (3.13). Since this jump-diffusion process is bounded, by Theorem 2.1 of Fritelli (2000) there exists a unique minimal entropy martingale measure.

Remark 5.1.

Note that (or, equivalently, if and only if process is already a -martingale. Indeed, if and only if and (see (3.15)) , or equivalently, . Hence and .

Remark 5.2.

Let the jump-diffusion process be a Lévy process, i.e. the alternation is missing and are constant. This is the case of a Markov jump-diffusion process.

Therefore, by (3.18) the relative entropy functions are identical and linear in

where, due to (3.17), and Here and are the constant jump intensities under measure and measure respectively; the parameter satisfies martingale condition (4.1):

In this case the martingale measure with the minimal relative entropy is defined by the jump intensity which satisfies the algebraic equation:

| (5.4) |

The latter equation is equivalent to

| (5.5) |

where the following change of variables is applied. In this particular case of Lévy process equation (5.5) coincides with condition (C) of Fujiwara and Miyahara (2003), which gives the minimal relative entropy under a measure defined by the Esscher transformation. In this example equation (3.18) becomes

| (5.6) |

where is the (unique) solution of (5.5). Equation (5.6) corresponds to equation (3.9) from Fujiwara and Miyahara (2003).

In the case of the jump-diffusion process with alternating parameters, such coincidence is not available. In this case the minimal entropy functions depend on the initial state and they have a bit more complicated behaviour.

Observe that functions are expressed by summing up of the two nonnegative and convex functions, (with for ) and (with for ). Hence, and are nonnegative and convex. Therefore, function is also nonnegative.

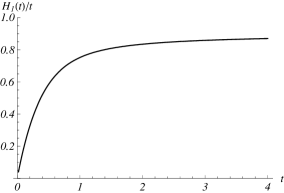

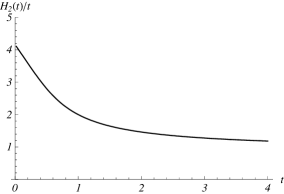

We analyse the relative entropy functions and for small and big times separately. These functions possesses the following time-asymptotics.

Proposition 5.3.

We choose the equivalent measure minimising the relative entropy function under the martingale condition (4.1), i.e. satisfy the following relations:

| (5.9) |

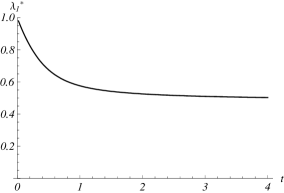

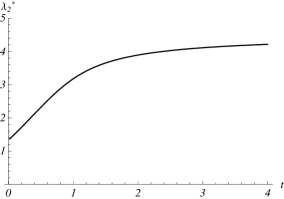

If measure is constructed by way of minimising and , we say that is the short-term minimal entropy martingale measure (MEMM), see (5.7); measure is the long-term MEMM, if minimises , see (5.8).

The short-term and the long-term minimal entropy equivalent martingale measures are defined as the solutions of the following optimisation problems subject to martingale condition (5.9):

-

•

the short-term MEMM is defined by solving the problem w.r.t. and

(5.10) -

•

the long-term MEMM is defined by solving the problem w.r.t. and

(5.11)

Theorem 5.4.

Proof.

If , then (5.9) gives

| (5.12) |

Hence problem (5.10) is equivalent to minimisation of the function

If, additionally, , then problem (5.10) has the unique solution . In this case we return to the Markov modulated diffusion process, see Remark 4.4 and Elliott et al (2005). This confirms again that in this case the minimum of entropy and the Esscher transform (5.1) lead to the same result.

If , then we have jump-telegraph model (see Example 4.2). In this case the martingale condition (5.9) gives , which corresponds to the unique equivalent martingale measure.

On the contrary, if , then the minimal entropy and the Esscher transform (5.1) give different results. Observe that with given by (5.12) can be rewritten as

| (5.13) |

where and

Differentiating (5.13) we have:

| (5.14) | ||||

We remark that functions and vary monotonically from to as and increase from 0 to . Hence, the system (and minimisation problem (5.10)) has the unique solution.

Moreover, if then the solution of the corresponding equation satisfies if then Therefore, the solution of (5.10) is always between and whereas the Esscher transform gives .

By a similar reasoning as before, one can easily see that system (5.15)-(5.16) also has (unique) solution. Indeed, owing to (5.13) and (5.14) we have

Thus,

Hence, function increases monotonically from to as increases from 0 to , which means that equation (5.15) has the unique solution for any fixed positive . Therefore system (5.15)-(5.16) is equivalent to

Differentiating this identity and (5.14) one can see that

Hence, function decreases as goes from 0 to , whereas strictly increases from to . Therefore system (5.15)-(5.16) has the unique solution.

Remark 5.5.

Theorem 5.4 and Proposition 5.3 show that the minimal entropy martingale measure differs from the measure supplied by Esscher transformation. This is confirmed by the plots presented in Fig. 5.1 and Fig. 5.2, where an asymmetric situation is considered. Surprisingly, the minimal entropy is supplied by which depend on time horizon. Moreover, the entropy functions , are not linear (cf. (5.6), Remark 5.2).

In Elliott et al (2007) the Esscher transform is applied to option pricing under a Markov-modulated jump-diffusion model.

In the symmetric case,

| (5.17) |

the solution of the minimal entropy problem is constant.

Proposition 5.6.

References

- Bellami and Jeanblanc (2000) N. Bellamy and M.Jeanblanc. Incompleteness of markets driven by a mixed diffusion. Finance Stochast. 4, 209–222 (2000).

- Cox (1962) D. R. Cox. Renewal Theory. Wiley, New York (1962).

- Di Crescenzo (2001) A. Di Crescenzo. On random motions with velocities alternating at Erlang-distributed random times. Adv. Appl. Prob. 33, 690–701 (2001).

- Di Crescenzo and Martinucci (2010) A. Di Crescenzo and B. Martinucci. A damped telegraph random process with logistic stationary distribution. J. Appl. Prob. 47, 84–96 (2010).

- Di Crescenzo and Martinucci (2013) A. Di Crescenzo and B. Martinucci. On the generalized telegraph process with deterministic jumps. Meth. Comput. Appl. Prob. 15, 215–235 (2013).

- Di Crescenzo et al (2013) A. Di Crescenzo, A. Iuliano, B. Martinucci and S. Zacks. Generalized telegraph process with random jumps. J. Appl. Prob. 50, 450–463 (2013).

- Di Crescenzo et al (2014) A. Di Crescenzo, B. Martinucci and S.Zacks. On the geometric Brownian motion with alternating trend. In: Mathematical and Statistical Methods for Actuarial Sciences and Finance, C. Perna and M. Sibillo, editors, pp. 81–85, Springer (2014).

- Di Crescenzo and Zacks (2015) A. Di Crescenzo and S. Zacks. Probability law and flow function of Brownian motion driven by a generalized telegraph process. Meth. Comput. Appl. Prob. 17, 761–780 (2015)

- Elliott et al (2005) R. J. Elliott, L. Chan and T. K. Siu. Option pricing and Esscher transform under regime switching. Ann. Finance 1, 423–432 (2005).

- Elliott et al (2007) R. J. Elliott, T. K. Siu, L. Chan and J. W. Lau. Option pricing under generalized Markov-modulated jump-diffusion model. Stoch. Anal. Appl. 25, 821-843 (2007).

- Esche and Schweizer (2005) F. Esche and M. Schweizer. Minimal entropy preserves the Lévy property: how and why. Stoch. Proc. Appl. 115, 299–327 (2005).

- Föllmer and Schweizer (1990) H. Föllmer and M. Schweizer. Hedging of contingent claims under incomplete information. In: Applied Stochastic Analysis, M.H.A. Davis and R.J. Elliott, editors, pp. 101–134, Gordon and Breach, London (1990).

- Fritelli (2000) M. Frittelli. The minimal entropy martingale measure and the valuation problem in incomplete markets. Math. Finance 10, 215–225 (2000).

- Fujiwara and Miyahara (2003) T. Fujiwara and Y. Miyahara. The minimal entropy martingale measure for geometric Lévy processes. Finance and Stochastics 27, 509–531 (2003).

- Guo (2001) X. Guo. Information and option pricings. Quant. Finance, 1, 38–44 (2001).

- Jacobsen (2006) M. Jacobsen. Point Process Theory and Applications. Marked Point and Piecewise Deterministic Processes. Birkhäuser, Boston, Basel, Berlin (2006).

- Jeanblanc and Chesney (2009) M. Jeanblanc, M. Yor and M. Chesney. Mathematical Methods for Financial Markets. Springer (2009).

- Jeanblanc and Rutkowski (2002) M. Jeanblanc and M. Rutkowski. Default risk and hazard process. In: Mathematical Finance Bachelier Congress 2000, Geman, H., Madan, D., Pliska, S.R., Vorst, T., editors, pp. 281–313. Springer, Berlin (2002).

- Kolesnik and Ratanov (2013) A. D. Kolesnik and N. Ratanov. Telegraph Processes and Option Pricing. Springer, Heidelberg (2013)

- Melnikov and Ratanov (2007) A. V. Melnikov and N. E. Ratanov. Nonhomogeneous telegraph processes and their application to financial market modeling. Doklady Math. 75, 115–117 (2007).

- Ratanov (2007) N. Ratanov. A jump telegraph model for option pricing. Quant. Finance 7, 575–583 (2007).

- Ratanov (2010) N. Ratanov. Option pricing model based on a Markov-modulated diffusion with jumps. Braz. J. Probab. Stat. 24, 413–431 (2010).

- Ratanov (2013) N. Ratanov. Damped jump-telegraph processes. Stat. Prob. Lett. 83, 2282–2290 (2013).

- Ratanov (2014a) N. Ratanov. On piecewise linear processes. Stat. Prob. Lett. 90, 60–67 (2014a).

- Ratanov (2014b) N. Ratanov. Double telegraph processes and complete market models. Stoch. Anal. Appl. 32, 555–574 (2014b).

- Ratanov (2015) N. Ratanov. Telegraph processes with random jumps and complete market models. Meth. Comput. Appl. Prob., 17, 677–695 (2015).

- Runggaldier (2004) W. J. Runggaldier. Jump-diffusion models. In: Handbook of Heavy Tailed Distributions in Finance, Rachev, S.T., editor. North Holland (2004).

- Weiss (1994) G. H. Weiss. Aspects and applications of the random walk. North-Holland, Amsterdam (1994).