*[inlinelist,1]label=(), itemjoin=, , itemjoin*=, and

Semi-nonparametric singular spectrum analysis with projection

Abstract

Singular spectrum analysis (SSA) is considered for decomposition of time series into identifiable components. The Basic SSA method is nonparametric and constructs an adaptive expansion based on singular value decomposition. The investigated modification is able to take into consideration a structure given in advance and therefore can be called semi-nonparametric. The approach called SSA with projection includes preliminary projections of rows and columns of the series’ trajectory matrix to given subspaces. One application of SSA with projection is the extraction of polynomial trends, e.g., a linear trend. It is shown that SSA with projection can extract polynomial trends much better than Basic SSA, especially for linear trends. Numerical examples including comparison with the least-square approach to polynomial regression are presented.

1 Introduction

Singular spectrum analysis (SSA) can solve a wide range of problems in the time series analysis, from the series decomposition on the interpretable series components to forecasting, missing data imputation, parameter estimation and many others, see, e.g., [16, 4, 6, 7] and references within. The key feature of SSA is that the basic method is model-free, does not need a-priori information and therefore constructs an adaptive decomposition of a time series into a sum of e.g. a non-parametric trend, periodic components and noise (see [5, 17, 2, 14, 15] among others for application of SSA to the problem of trend extraction). This can be considered as a great advantage of the SSA-family methods for comparison with parametric ones. However, sometimes there is a-priori information about the considered time series. For example, the trend can be expected as linear or polynomial.

In [6, Section 1.7.1], SSA with single and double centering is developed to extract constant or linear trends with better accuracy. We generalize this approach. Approaches, which deal with a combination of parametric and nonparametric models, are sometimes called semi-parametric if the parametric part of the model is of interest and semi-nonparametric if both parts are important, see the references [3] and [10] as examples of such approaches to statistical econometric problems.

Let us explain the motivation for the suggested approach, which can be considered as a semi-nonparametric variation of singular spectrum analysis.

In SSA, the separability theory is responsible for a proper decomposition and component extraction. The separability of a series component means that the method is able to extract this time series component from the observed series, which is a sum of many components. Basic SSA is able to approximately separate a trend (e.g., a linear trend) from oscillations. However, there is no series, which can be exactly separated from a linear trend. As a consequence, the separation accuracy is not high. It is shown in [6, Sections 1.7.1 and 6.3.2] that SSA with double centering weakens the separability conditions and therefore improves the accuracy in conditions of approximate separability. Thus, it is expected that, within the SSA-family methods, SSA with projection can improve separability for components of a specific structure, which is in accordance with the projection subspaces.

In comparison with the linear regression technique (we will further mean the least squares approach to the estimation of regression parameters), SSA with double centering differs by the statement of the problem. Linear regression minimizes the prediction error, while SSA tries to separate the series components themselves using their orthogonality. For example, for a series with common term , where and , the least-squares approach generally cannot estimate the linear trend with no error, while in the conditions of separability SSA with double centering is able to find the exact linear trend. For long time series, the linear regression and SSA yield close estimates of the linear trend. Note that for the case of approximate separability the trend found by SSA with double centering will be only close to a straight line, while the linear regression always provides a linear function as a trend estimation. The analogous relation between the parametric regression and SSA with projection is expected for the general case of polynomial trends. In particular, we can suppose that for time series with seasonality the ‘SSA with projection’ method will be able to extract linear and polynomial trends more accurately than the parametric regression approach. It is important that the use of projection on a fixed basis does not contradict the non-parametric nature of SSA. Moreover, if the basis is chosen incorrectly, the decomposition will be not optimal and the trend estimate will be less accurate; however, the estimate will not have a considerable bias, since it can be accomplished by components of the adaptive part of the whole decomposition. This is not the case for the parametric approach.

The Basic SSA method consists of trajectory matrix construction from the original time series, its decomposition into a sum of rank-one matrices by SVD, their grouping and then each group’s return to time series to obtain a decomposition of the original time series into a sum of identifiable components. The grouping of the SVD can be considered as a projection of the trajectory matrix columns on a subspace, which is adaptively constructed based on the distinguished features of SVD decomposition. SSA with projection starts with projections of trajectory matrix columns and rows on subspaces chosen in advance and then decomposition of the residual, by the same way as in Basic SSA. In particular, SSA with double centering uses the projections on the subspaces spanning the vectors with elements equal to . A natural application of SSA with projection, which is mostly considered in this paper, serves for extraction of polynomial trends; however, the suggested method can be applied to a wider range of problems, e.g., for the use of information about a supporting series.

The structure of the paper is as follows. We start with a short description of the algorithm of Basic SSA and standard separability notion (Section 2). Section 3 is devoted to generalizing centering used in SSA and contains the underlying theory, including the proof of the algorithm and the separability conditions. Section 4 demonstrates the examples of the algorithm application for trend extraction. The real-life examples are studied in Sections 4.1 and 4.2 to show the relation between Basic SSA, SSA with projection and the linear regression (least-squares) approach. Numerical comparison is performed in Section 4.3. The paper is summarized and conclusions are drawn in Section 5.

2 Necessary information

2.1 Algorithm of Basic SSA

Consider a real-valued time series of length . Let () be some integer called window length and .

For convenience, denote the space of matrices of size and the space of Hankel matrices of size . Consider the lagged vectors , , and the trajectory matrix of the series .

Define the one-to-one embedding operator . as . Also introduce the projector (in Frobenius norm) of to . Projection is performed by the change of entries on auxiliary diagonals to their averages along the diagonal.

The Basic SSA algorithm consists of four steps.

1st step: Embedding. Let be chosen. At this step the -trajectory matrix is composed: .

2nd step: Singular Value Decomposition (SVD). The SVD of the trajectory matrix is constructed:

| (1) |

where are singular values, and are left and right singular vectors of , , .

The triple is called th eigentriple (abbreviated as ET).

3rd step: Eigentriple grouping. The grouping procedure partitions the set of indices into disjoint subsets .

Define . The expansion (1) leads to the decomposition

| (2) |

If and , , then the corresponding grouping is called elementary.

4th step: Diagonal averaging. Obtain the series by diagonal averaging of the matrix components of (2): .

Thus, the algorithm results in the constructed decomposition of the observed time series

| (3) |

A typical example of (3) is the decomposition into a sum of a trend, oscillations and noise.

Remark 1.

Columns of a grouped matrix are the projections of columns of the trajectory matrix to . Rows of are the projections of rows of to .

2.2 Separability by Basic SSA

To understand how SSA works, the notion of separability is very important. Separability of two time series and signifies the possibility of extracting from the observed sum . This means that there exists a grouping at Grouping step such that .

By properties of the SVD, the separability is concluded in the orthogonality of the column and row spaces of the trajectory matrices of the series and . In the case of approximate (asymptotic) separability we obtain the condition of approximate (asymptotic) orthogonality.

For sufficiently long time series, SSA can approximately separate, for example, a signal and noise, sine waves with different frequencies, a trend and a seasonality [6, 7].

The introduced separability, which is called weak separability, means that at the SVD step there exists such an SVD that allows the proper grouping. Strong separability means that each SVD decomposition allows the proper grouping. Several nonparametric modifications of SSA for improvement of the weak and strong separability are considered in [9]. In this paper we will improve the separability by a semi-nonparametric variation.

2.3 Series of finite rank and series governed by linear recurrence relations

Let us describe the class of series of finite rank, which is natural for SSA. In particular, only such time series can be exactly separated by Basic SSA.

Define the -rank of a series as the rank of its -trajectory matrix. Series with rank-deficient trajectory matrices are of special interest. A time series is called time series of finite rank if its -trajectory matrix has rank for any (it is convenient to assume that ). We will call the column and row spaces of the trajectory matrices column and row spaces of the series respectively.

Under some unrestrictive conditions [6, Section 5.2], series of finite rank is governed by a linear recurrence relation (LRR) of order , that is,

| (4) |

The LRR (4) is called minimal and is called the dimension of the series. Let us describe how we can restore the form of the time series by means of the minimal LRR.

Definition 1.

The polynomial is called a characteristic polynomial of the LRR (4).

Let the time series satisfy the LRR (4) with and . Consider the characteristic polynomial of the LRR (4) and denote its different (complex) roots by , where . All these roots are non-zero as . Let the multiplicity of the root be , where and . We will call characteristic roots of the series governed by an LRR.

It is well-known that the time series satisfies the LRR for all if and only if

| (5) |

where the coefficients are determined by the first series terms. For real-valued time series, (5) implies that the class of time series governed by the LRRs consists of a sum of products of polynomials, exponentials and sinusoids.

Rank of the series is equal to the number of non-zero terms in (5). For example, an exponentially-modulated sinusoid is constructed from two conjugate complex roots if its frequency . Therefore, the rank of this exponentially-modulated sinusoid is equal to . The rank of an exponential is equal to , the rank of a linear function corresponding to the root of multiplicity equals , and so on.

Also, the representation (5) helps to easily construct the bases of trajectory spaces of complex time series governed by LRRs: they are constructed from the linearly independent vectors . For linear series, the basis consists of and .

3 SSA with projection

Let us consider a time series of length , a window length , , the trajectory matrix of the series .

A general form of the considered modification can be expressed as

-

•

Calculation of a special matrix based on a-priori information.

-

•

Computation of .

-

•

Construction of the SVD: .

Thus, we have the decomposition .

Centering, which is a particular case of the general scheme, is considered in the following forms [6]:

-

1.

Single row centering when corresponds to averaging by rows, that is, each element of a row of consists of the average of the corresponding row of the trajectory matrix.

-

2.

Single column centering when corresponds to averaging by columns.

-

3.

Double centering when corresponds to averaging by both rows and columns.

Single centering can be considered as a projection of rows or columns of on , where , is equal to or . Therefore, centering in SSA can be considered as a preliminary projection of the trajectory matrix on a given subspace; the residual matrix will be subsequently expanded by SVD or any other decomposition.

Let us generalize this approach to projections to arbitrary spaces. Denote a basis of the column projection space and/or a basis of the row projection space . Let and be orthogonal projectors. For any , denote the matrix consisting of the columns, which result from projections of the columns of , while for any denote the matrix consisting of the rows, which result from projections of the rows of .

In SSA with projection, the scheme of SSA with centering is extended to arbitrary projections, that is, for column projection, for row projection and for double projection, where . If either the column or row basis is absent (that is, the corresponding projection should not be performed), then we formally set the corresponding projector to be the zero operator implying for any mode.

Note that the method of SSA with projection differs from Basic SSA only in the Decomposition step:

| (6) |

where is the SVD of . Let us show that (6) can be represented as a sum of elementary matrices and therefore Reconstruction steps can be performed in the same way as done in Basic SSA.

Without loss of generality we assume that and are orthonormal systems (otherwise, we can perform ortho-normalization). Denote , . Then and . Since and can be expressed as a sequential application of the projection operators and , (6) is a decomposition of on elementary matrix components unambiguously defined. For double projection, this representation depends on the order of projections; we will apply the row projector first.

Thus, the matrix can be considered as a sum of elementary matrices of the forms , , and , . The triples and have the same meaning as eigentriples.

The Reconstruction stage is exactly the same as in the Basic SSA method. Note that it makes little sense to include the eigentriples produced by projections to different groups, since the projections are performed on the subspaces as a whole.

3.1 Appropriate class of time series

For SSA with projection, a known series component with a trajectory matrix should be in agreement with projection so that for column projection, for row projection and for double projection.

Clearly, for column and row projections, this is true if the corresponding projection is performed on the column or row trajectory space of the known series component. For example, the trajectory space of an exponential component spans , while the trajectory space of a linear function spans and for any and non-zero .

Let us derive a condition sufficient for to hold for the general case of the double projection.

Lemma 1.

Let , for and . Then for

| (7) |

where and .

Proof. By the assumption, for any and matrix , while for any matrix . Therefore,

since .

It is easy to check that the trajectory matrix of a linear series satisfies the conditions of Lemma 1 for the case of double centering. However, for a general case the approach based on characteristic roots is more convenient. We start with a technical lemma.

Lemma 2.

For any polynomial of order and for any and such that the following expansion can be constructed:

where denotes a polynomial of and of order .

Proof. This lemma is proved by an appropriate grouping of the monomials , , of .

Recall that a series governed by an LRR, whose characteristic polynomial has the given set of roots called characteristic roots, is of the form (5).

Theorem 1.

Let a series () be governed by an LRR of order , be its trajectory matrix. Let be the set containing the characteristic roots of both series. Assume that has roots , , with multiplicities , . Let be the projector on the column space of , be the projector on the row space of , . Then if and only if the set of characteristic roots of the series consists of the roots , , of multiplicities .

Proof. Due to linearity of projectors and linear dependence of on and , it is sufficient to prove the theorem for the case of one root . Let have the characteristic root of multiplicity , have the characteristic root of multiplicity .

Thus, we should prove that if and only if the series has the form , where . It is sufficient to take .

By Lemma 2

This means that (7) holds for and such that the column space of coincides with and the column space of coincides with .

Since the dimension of the space of trajectory matrices that are kept by the projector is equal to , we found all such matrices. This completes the proof.

Corollary 1.

Let be a series of dimension , be its trajectory matrix, be the projection on its row trajectory space, be the projection on its column trajectory space. Consider the series with . Then , where .

Remark 2.

Note that multiplication of a series by means that the multiplicities of its characteristic roots increase by .

Corollary 2.

Let be the projection on the row trajectory space of the polynomial of order , be the projection on the column trajectory space of the polynomial of order . Then for the polynomial of order we have .

3.2 Separability

We expect that if a time series component is governed by a minimal LRR and this LRR is known, then the series component can be separated by a suitable version of SSA with projection better than it can be done by Basic SSA.

Using the notion of separability, we can formulate this improvement as follows. Let . We will say that a time series component is separated by SSA with projection if , where is as in (6).

Let be a series of finite rank, . Similar to [6], where conditions for separability by SSA with centering are considered, the following conditions of separability can be obtained.

-

1.

Basic SSA:

and are separable if (if and only if, by definition) their row and column spaces are orthogonal. -

2.

SSA with row projection on the row space of :

and are separable if their row spaces are orthogonal. -

3.

SSA with column projection on the column space of :

and are separable if their column spaces are orthogonal. -

4.

SSA with double projection on the row and column space of , where and are such that , :

and are separable if the row and column spaces of and are orthogonal.

Note that the separability by SSA with projection is always strong, since projections on linear spaces are uniquely defined.

For the approximate separability, where , the approximate orthogonality is necessary. Also, the asymptotic separability can be considered by analogy with the conventional separability for Basic SSA and SSA with centering.

Recall that the usual double centering in SSA corresponds to a constant series and therefore to a linear series . Orthogonality to a constant series is a much weaker condition than that to a linear series (moreover, the condition of orthogonality to a linear series can never be exactly satisfied). In particular, any sinusoid with frequency is asymptotically separable from the linear trend and the exact separability by SSA with projection takes place if and are integers, that is, if and are divisible by the period of the sinusoid. Therefore, for extraction of linear trends, the double centering is recommended.

In the case of a polynomial trend of degree larger than , the conditions of exact separability cannot be satisfied at all, even for SSA with double projection. However, we still can expect that in the case of polynomial trends, SSA with double projection also will work better than SSA with only row or column projections and also better than Basic SSA.

3.3 Algorithm

Let us summarize the steps of SSA with projection in the form of algorithms, splitting the whole algorithm into decomposition and reconstruction.

Similar to Basic SSA, SSA with projection provides a decomposition on matrices orthogonal by Frobenius; therefore, contributions of are given by . However, the obtained decomposition into a sum of rank-one matrices can be non-minimal (their number is larger than the rank of ), if at least one basis vector used for the projections does not belong to the column (row) trajectory space.

The only essential difference with the reconstruction by Basic SSA is that the set of the matrices , , produced by projections, should be included in the same group.

Note that formally, the sets and can be arbitrary. However, if the model of the series is partly known, then in the context of SSA this means that a time series component satisfies an LRR and we know its characteristic roots (see Section 2.3). Therefore, to extract, for example, a sine wave using projections, we should know its period, and to extract an exponential trend, we should know its rate. These conditions are often too restrictive. A clear exception is extraction of polynomial trends of a degree , when there is the unique characteristic root equal to of multiplicity and we should assume only the degree of the polynomial trend to obtain its trajectory space.

4 Examples

The presented examples are related to finding polynomial trends. For convenience, if the row and column projections are performed on the subspace generated by polynomials of degree and respectively, then we denote the method as ProjSSA(,). Recall (see Corollary 2) that the choice ProjSSA(,) corresponds to extraction of a polynomial trend of degree . In ProjSSA(,), the projection part of the decomposition, i.e., the matrix in (6), consists of rank-one matrices. ProjSSA(1,1) is used for extraction of a linear trend. The zero value for or means that the corresponding projection is not performed.

All the examples are implemented in R [13] with the help of the Rssa package [12]. For example, to perform ProjSSA(,) for a time series taken from the variable x with a window length L, the following code should be called:

s <- ssa(x, L = L, row.projector = q, column.projector = p)r <- reconstruct(s, groups = list(trend = 1:nspecial(s)))plot(r, add.residuals = FALSE, plot.method = "xyplot", superpose = TRUE)For more details on Rssa, see the help files in [12].

4.1 SSA with projection and regression

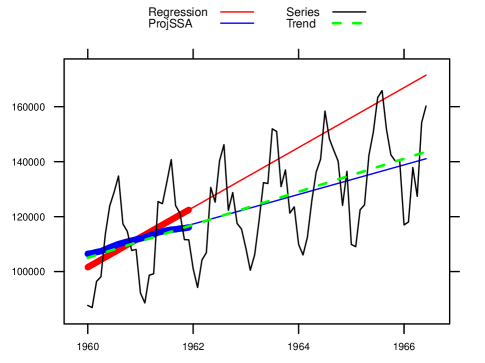

Let us demonstrate that the conventional linear regression and SSA with double centering, i.e., ProjSSA(1,1), use different statements of the solved problem and therefore can yield different results. It is clearly seen in short time series. For long time series the results are very close. Also, in the model of linear regression with Gaussian noise, the regression solution is optimal. Therefore, to demonstrate the difference, we consider a time series, which contains a seasonal component.

Here we examine the time series ‘Gasoline’ taken from [1] and containing the data GASOLINE DEMAND, MONTHLY, Jan 1960 – Jun 1967, ONTARIO, GALLON MILLIONS.

Let us consider the first two years and apply the linear regression and ProjSSA(1,1) with . To show the difference, we continue the linear regression line with the help of the estimated coefficients. In the Rssa, a method of forecasting for SSA with projection is implemented. Since it is not proved yet, we will construct the forecast by a linear regression applied to the reconstruction, which is performed by ProjSSA(1,1). Note that the forecasting procedure from Rssa provides a similar prediction. As a benchmark, the linear regression constructed by the whole series is considered.

One can see in Figure 1 that the ProjSSA(1,1) linear trend (blue) is very close to a linear trend constructed by the whole long time series (green). The linear regression line (red) gives a much worse approximation of the trend. This is explained by the following reasons. The least-squares approach to the linear regression estimation minimizes the prediction error and therefore the seasonal component can shift the linear regression trend. For ProjSSA(1,1), the seasonal component is well separated from the linear trend, since for the chosen parameters are divisible by the seasonal period .

4.2 SSA with projection and Basic SSA

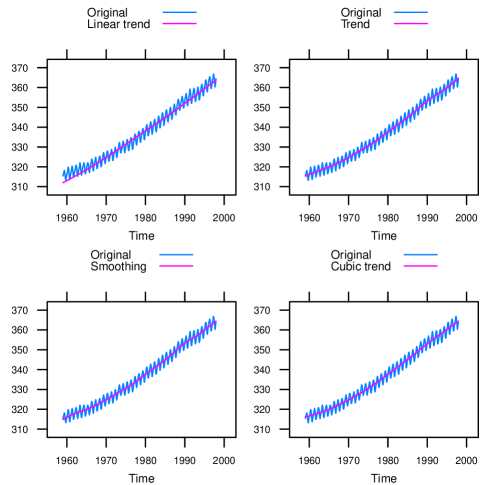

The example introduced in this section demonstrates that both SSA with projection and Basic SSA can extract trends in a similar manner. Let us consider the example ‘co2’ (Mauna Loa Atmospheric Concentration, 468 observations, monthly from 1959 to 1997 [11]).

We start with extraction of the linear trend and therefore choose ProjSSA(1,1) to perform SSA with double centering.

By analogy with SSA, large window lengths help to extract separable series components, while small window lengths correspond to smoothing. Therefore, we take , which is divisible by and is close to half of the time series length to obtain better separability, and a small value to smooth the series. Three of four versions of the extracted trends presented in Figure 2 almost coincide.

For the choice , the extracted trend is close to linear, see Figure 2 (left-top). Certainly, the accurate trend of ‘co2’ series is not linear. However, the projection components can be supplemented by the 1st and 4th SVD components (ET5,8) to improve the trend (Figure 2 (right-top)). Figure 2 (left-bottom) shows the result of smoothing with . Finally, the result of ProjSSA(2,2) with , which is designed for extraction of a cubic trend, is depicted in Figure 2 (right-bottom). The extracted trend is very similar to that in [8], which was extracted by Basic SSA (not depicted).

Identification of the components in the decomposition produced by SSA with projection is exactly the same as it is performed in Basic SSA.

4.3 Numerical comparison

The real-life examples presented in Sections 4.1 and 4.2 show that the results of Basic SSA, SSA with projection and linear regression can be either different or similar. To understand, what method is better, let us perform a numerical study.

We consider a time series of length with the common term

| (8) |

where is a trend, , is a Gaussian white noise with standard deviation .

For obtained estimations , where is the number of series with th realization of noise , , we will calculate the root-mean-square error (RMSE) as .

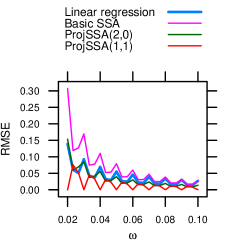

Linear trend and sine wave. Let us start with the noiseless case with and therefore take . Let . We fix , , and change from to (that is, the period is changed from to ).

Since the result of the least-square method strongly depends on the form of the residual, we consider the values of the phase, and .

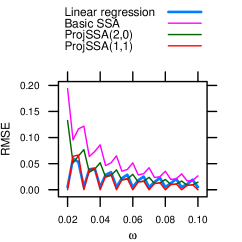

Figure 3 (left) contains the RMSE values in the case for Basic SSA with reconstruction by ET1–2, ProjSSA(2,0), ProjSSA(1,1) with , and for the linear regression. One can see that the worse cases for ProjSSA(1,1) are approximately equal to the best cases for the linear regression.

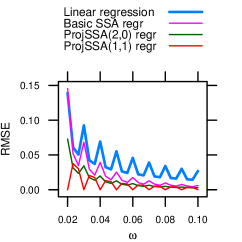

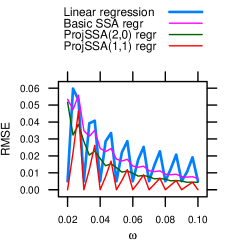

In Section 4.1, we perform forecasting by the linear regression applied to the trend reconstruction. Figure 3 (right) contains the RMSE for the linear regression lines constructed in this way; ‘regr’ is added to the legend. The ordering of the SSA methods is generally the same, while the SSA methods become better than the linear regression. Probably, is one of the worst values of for linear regression.

Now consider as one of the best cases for the linear regression. The behavior of the errors is quite different (Figure 4 (left)). However, the accuracy of ProjSSA(1,1) is still better than that of the linear regression. Linear least-square approximation of the SSA reconstructions considerably improves the accuracy of the SSA methods (Figure 4 (right)).

Note that zero values of the RMSE for ProjSSA(1,1) for frequencies are explained by the theory, since then and are integers. The errors for ProjSSA(2,0) lie between that for Basic SSA and ProjSSA(1,1). It is interesting that the minimal errors for Basic SSA are achieved for the middle points, when and are integers.

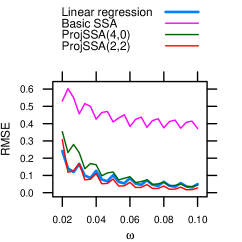

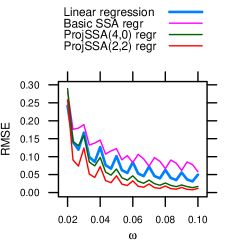

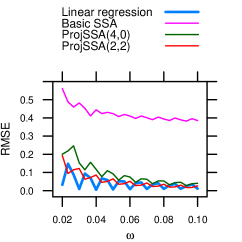

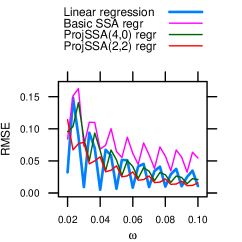

Cubic trend and sine wave. Let us consider a more complex case of the cubic trend . Since there is no exact separability for any choice of parameters, the results are unpredictable. Figures 5 (left) and 6 (left) contain the RMSE values for Basic SSA with reconstruction by ET1–4, ProjSSA(4,0), ProjSSA(2,2) with and for the cubic regression. One can see that ProjSSA(2,2) is the best method for , while it is just comparable with the linear regression for . Note that here the best parameters for ProjSSA(2,2) do not correspond to the case when and are integers. The cubic least-square approximation of the reconstructed trend again improves the estimates (Figures 5 (right) and 6 (right)).

Basic SSA fails for the chosen parameters because of lack of strong separability: the fourth trend component has a contribution comparable with the contribution of the periodic components that causes their mixture.

Note that one of the modifications described in [9], Iterative O-SSA, can be used to get strong exact separability for the considered noiseless examples. However, we do not involve this modification into the comparison, since Iterative O-SSA is not able to remove noise and should be applied after denoising in nested manner, while the compared methods are able to extract the trend without denoising.

Linear trend and noise. For the data which satisfy the model of the linear regression with white Gaussian noise, that is, for the amplitude equal to zero, we take and use . As expected, the smallest error is achieved for the regression estimate. However, the RMSE of the ProjSSA(1,1) estimate equal to is very close to . The error of the Basic SSA is equal to . Application of linear regression to the results of SSA reconstruction improves the SSA estimates. The RMSE for ProjSSA(1,1) and Basic SSA become equal to and respectively.

We do not show the results when the series has both periodic component and noise, since the errors are intermediate. To keep the advantage of SSA with projection, the noise standard should be considerably smaller than the amplitude of the periodic component.

5 Conclusion

The considered combination of singular spectrum analysis, which does not need a series model given in advance, and of a subspace-based parametric approach, which is incorporated by means of projections to subspaces given in advance, proves successful for extraction of polynomial (especially, linear) trends, when the residual has unknown structure and can include deterministic oscillations, e.g., the seasonality.

The general form of projections of columns and rows of the trajectory matrix, which keeps this trajectory matrix, was obtained. It was proved that projections to the row and column subspaces (so-called double projection) of the trajectory matrix of a series are related to extraction of the series . In particular, the linear trend can be obtained by double projection to the column and row subspaces of a constant series. The formulated conditions of separability of a series component, which is kept by projections, show that if a series component can be represented in the form , then the double projection is preferable.

Thus, the theory provides an additional theoretical support to SSA with double centering (ProjSSA(1,1)), which was known before, and also enlarges the range of applications of semi-nonparametric modifications of Basic SSA.

Applications of SSA with projection considered in the paper were related to the extraction of a polynomial trend, since its trajectory space is determined by the polynomial degree only.

We showed on the example ‘Gasoline’ that the linear regression approach can be inadequate for short series and large oscillations, in comparison with ProjSSA(1,1). Comparison of different SSA versions applied to the ‘co2’ data demonstrates that even if the model of a series component used for projection is wrong, the non-parametric part of SSA with projection can correct the bias.

A numerical study was performed for a better understanding of the difference between SSA with projection and the linear regression approach. First, it appears that if we extract a polynomial trend by SSA with projection, then the polynomial least-squares approximation of the trend reconstruction can considerably improve the accuracy.

The second found effect is related to the influence of the residual geometry on the estimate accuracy. In the considered example, we changed the phase of a sinusoid. The SSA estimates slightly depend on the phase, while the regression estimates demonstrate a considerable dependence.

Numerical experiments confirm that for a linear trend and a sine wave residual, ProjSSA(1,1) is more accurate than the linear regression estimate. For a noisy linear trend, when the model of the linear regression if fulfilled, the linear regression estimate is slightly more accurate than SSA. Thus, we can formulate conditions, when SSA with double projection can be recommended for use: series has a linear or polynomial trend (the polynomial degree is not large) and the regular oscillations are considerably larger than the noise level.

The further investigation can be performed in two directions. First, the forecasting algorithm for ProjSSA(,) implemented in Rssa should be proved. Then, the idea to use projection to involve the structure of a supporting series looks promising.

References

- [1] B. Abraham and J. Ledolter. Statistical Methods for Forecasting. Wiley, Toronto, 1983.

- [2] Theodore Alexandrov, Silvia Bianconcini, Estela Bee Dagum, Peter Maass, and Tucker S. McElroy. A review of some modern approaches to the problem of trend extraction. Econometric Reviews, 31(6):593–624, 2012.

- [3] Xiaohong Chen. Chapter 76 large sample sieve estimation of semi-nonparametric models. volume 6, Part B of Handbook of Econometrics, pages 5549 – 5632. Elsevier, 2007.

- [4] J. B. Elsner and A. A. Tsonis. Singular Spectrum Analysis: A New Tool in Time Series Analysis. Plenum, 1996.

- [5] Igor V. Florinsky, Robert G. Eilers, Brian H. Wiebe, and Michele M. Fitzgerald. Dynamics of soil salinity in the canadian prairies: Application of singular spectrum analysis. Environmental Modelling & Software, 24(10):1182 – 1195, 2009.

- [6] N. Golyandina, V. Nekrutkin, and A. Zhigljavsky. Analysis of Time Series Structure: SSA and Related Techniques. Chapman&Hall/CRC, 2001.

- [7] N. Golyandina and A. Zhigljavsky. Singular Spectrum Analysis for time series. Springer Briefs in Statistics. Springer, 2013.

- [8] Nina Golyandina and Anton Korobeynikov. Basic singular spectrum analysis and forecasting with R. Computational Statistics & Data Analysis, 71:934–954, 2014.

- [9] Nina Golyandina and Alex Shlemov. Variations of singular spectrum analysis for separability improvement: Non-orthogonal decompositions of time series. Statistics and Its Interface, 8(3):277–294, 2015.

- [10] Hidehiko Ichimura and Petra E. Todd. Chapter 74 implementing nonparametric and semiparametric estimators. volume 6, Part B of Handbook of Econometrics, pages 5369 – 5468. Elsevier, 2007.

- [11] C. D. Keeling and T. P. Whorf. Atmospheric CO2 concentrations — Mauna Loa Observatory, Hawaii, 1959-1997. Scripps Institution of Oceanography (SIO), University of California, La Jolla, California USA 92093-0220, 1997.

- [12] Anton Korobeynikov, Alex Shlemov, Konstantin Usevich, and Nina Golyandina. Rssa: A collection of methods for singular spectrum analysis, 2015. R package version 0.13.

- [13] R Core Team. R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria, 2015.

- [14] Shazlyn Milleana Shaharudin, Norhaiza Ahmad, and Fadhilah Yusof. Effect of window length with singular spectrum analysis in extracting the trend signal on rainfall data. AIP Conference Proceedings, 1643(1):321–326, 2015.

- [15] P. Unnikrishnan and V. Jothiprakash. Extraction of nonlinear rainfall trends using singular spectrum analysis. Journal of Hydrologic Engineering, 0(0):05015007, 2015.

- [16] R. Vautard, P. Yiou, and M. Ghil. Singular-Spectrum Analysis: A toolkit for short, noisy chaotic signals. Physica D, 58:95–126, 1992.

- [17] V. V. Vityazev, N. O. Miller, and E. Ja. Prudnikova. Singular spectrum analysis in astrometry and geodynamics. AIP Conference Proceedings, 1283(1):319–328, 2010.