We consider exit problems for general Lévy processes, where the first passage over a threshold is detected either immediately or at an epoch of an independent homogeneous Poisson process. It is shown that the two corresponding one-sided problems are related through a surprisingly simple identity. Moreover, we identify a simple link between two-sided exit problems with one continuous and one Poisson exit. Finally, Poisson exit of a reflected process is connected to the continuous exit of a process reflected at Poisson epochs, and a link between some Parisian type exit problems is established. With the appropriate perspective, the proofs of all these relations turn out to be quite elementary. For spectrally one-sided Lévy processes this approach enables alternative proofs for a number of previously established identities, providing additional insight.

Financial support by the Swiss National Science Foundation Project 200020 143889 is gratefully acknowledged.

1. Introduction

Let be a real-valued Lévy process, and let be the epochs of an independent Poisson process with intensity ; add . The probability law corresponding to started at will be denoted by (with denoting the expectation).

When is not mentioned explicitly we assume that and write simply and .

Define

which we interpret as the first passage times under continuous and Poisson observations, respectively.

Observe that and, moreover, converges in probability to as (the same is true for and ). Thus exit theory under Poisson observation can be regarded as a generalization of the classical exit theory.

Throughout this paper, however, we keep fixed.

Observation at Poisson epochs is both of theoretical and practical interest.

Firstly, some exit problems with Poisson observation yield transforms

of certain occupation times, e.g.

Secondly, Poisson observation is relevant in various applications such as queueing (see e.g. [5]), reliability and insurance risk theory (see e.g. [1, 2]).

In particular,

in many applications discrete-time observation of stochastic processes would often be considered more natural, but for equidistant discrete time epochs the explicit and tractable analytical structure of continuous-time processes is typically destroyed, so that one is forced towards numerical techniques for the determination of exit probabilities and related quantities. The Poisson observation structure is a bridge between continuous-time and discrete-time observation that still leads to rather explicit, and as will be shown below, also somewhat elegant modifications of the continuous-time formulas.

1.1. Overview and organization

In order to stress the intuition behind the derivation of the identities, we will start with a simple case and gradually generalize the setup. Most of the results are stated in terms of relations between transforms, but can also be understood as relations between the corresponding laws in an obvious way.

Some of the wording throughout the manuscript will be in terms of the insurance application, where is the surplus process of a portfolio of insurance contracts, is the time of ruin of the portfolio, is the event of (infinite-time) survival, and is the time of observed ruin under Poisson observation of the surplus process (in the application the Poisson epochs can for instance be interpreted as the observation times of the regulatory authority).

In Section 2 we discuss survival probabilities corresponding to the two observation types, and then proceed to the general one-sided exit problems including the time of exit and the overshoot.

In Section 3 we consider more complex problems. Firstly, the two-sided exit problem with one continously observed and one (Poisson-)discretely observed boundary is related to the one where the observation types at the boundaries are interchanged. Secondly, we provide a link between Poisson exit of a reflected process and continuous exit of the process reflected at Poisson epochs. We also show that a two-sided problem with Poisson exit at both boundaries yields an identity as well, but with a non-standard first passage time. The latter quantity is then linked to a Parisian ruin problem with Erlang-distributed implementation delay.

Finally, we establish a link between Parisian ruin problems with continuous and Poisson observations. We conclude with Section 4, where we specialize to the case of spectrally-one sided processes and demonstrate the use of our simple identities, providing simpler proofs and additional insight to some identities established in earlier literature.

1.2. Preliminaries

The Wiener-Hopf factorization plays a crucial role in the derivations below. Define

the infimum and its (first) time of occurrence up to horizon . Similarly, the supremum and its (last) time of occurrence are defined by

Finally, let the pairs and be distributed as and respectively (under ), and sampled independently of each other and of everything else ( and stand for ‘down’ and ‘up’).

Recall that according to the Wiener-Hopf factorization we have

see, e.g., [6, Thm. VI.5], and [7] for applications of factorization embeddings.

2. One-sided exit

2.1. Survival probability

Let us first consider

(1)

which in the insurance application are the probabilities of survival with initial capital under continuous and Poisson observation, respectively.

In fact, the two quantities are connected by two very simple relations:

Proposition 1.

For it holds that

(2)

(3)

Figure 1. Schematic sample path and embeddings

Proof.

Survival under Poisson observation is determined by the sequence , whereas survival under continuous observation is determined by the sequence of infima in between the observation epochs (black and grey dots in Figure 1, respectively). Let and

define in the same way but for the shifted process and exponential time .

Let and be the partial sum processes corresponding to

respectively; and are the heights of the black and grey dots in Figure 1.

Observe that all and are independent, because of independence of increments and the Wiener-Hopf factorization.

Since the ’s have the law of we obtain

(4)

Similarly,

(5)

Hence

and, since ,

∎

Remark 1.

Relation (2) allows to interpret the transition from continuous to discrete Poisson observation simply as a (random) increase of the starting value (initial capital) by , as far as the survival probability is concerned; that is the structure of as a function of is otherwise completely preserved. Likewise, Relation (3) shows that moving from discrete Poisson to continuous observation preserves the structure, reducing the initial capital by (which has all its probability mass on the negative half-line).

Remark 2.

Suppose we modify the Poisson observation model, so that there is no observation at time . Then (2) is still valid (even for negative then), whereas (3) does not hold any more.

Remark 3.

By the same token one can connect the finite-time survival probabilities and for :

That is, survival under continuous observation up to an independent Erlang distributed time horizon is intimately related to survival under Poisson observation up to a certain arrival epoch.

2.2. The general identities

Proposition 2.

For and it holds that

(6)

(7)

Observe that the left-hand side of (7) gives the transform of the undershoot of the first grey point below 0 in Figure 1, according to the strong Markov property applied at . Now one can establish the relation between black and grey points as in the proof of Proposition 1, additionally taking time into account.

Essentially, we just shift the picture so that we start at the first grey point.

Let and define in the same way but for the shifted process and exponential time .

As in the proof of Proposition 1 we consider the sequences of black and grey dots in Figure 1, but now we also add the time component: and which are the partial sum processes corresponding to

respectively. Similarly to (4) and (5) we observe that

Letting and be the first passage epochs we can write

where in the last line we applied the strong Markov property at . Identity (7) can be derived analogously.

∎

3. Further exit problems

3.1. Two-sided exit with different observation types

In this section we consider two-sided exit problems with one continuous and one Poisson exit at the boundaries. It turns out that there is a simple relation between the problems when the roles of the continuous and the Poisson exit are interchanged, i.e. problems corresponding to and . Here we extend the ideas of Section 2 to their full potential.

Proposition 3.

For and it holds that

(8)

(9)

Proof.

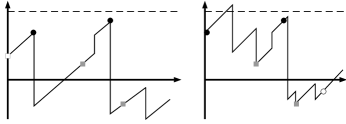

The proof is by inspection: For (8), consider the embeddings illustrated in Figure 2. In the left picture the grey dots correspond to the observations and the black to the suprema in between two observations. In the right picture the black dots correspond to observations and the grey to the infima in between observations.

Note that the position of a black point with respect to the previous grey point has the same distribution in both cases, namely . The same is true for the position of the grey points with respect to their previous black points with . So the patterns of points in each case have the same law up to a certain shifting; we illustrate this by using the same patterns of points in both pictures in Figure 2 and by drawing different sample paths.

Now it follows that , see the left picture, must coincide with , see the right picture, because the interpretation of points was ’reversed’.

Finally, we include the value of at first passage and its time using the strong Markov property at as in the proof of Proposition 2.

The same type of reasoning yields (9).

∎

Figure 2. Poisson observations are in grey (left picture) and in black (right picture)

By considering the negative of we immediately obtain the following result from Proposition 3.

Corollary 1.

For and it holds that

(10)

(11)

3.2. Reflected processes

In this section we consider the process reflected at a barrier in a continuous and Poisson manner, and study its first passage below 0 in Poisson and continuous manner respectively (with always opposite manners).

Again, these two problems are closely related.

Note that in an insurance context reflection at results when paying out dividends according to a barrier strategy, either continuously or at Poisson epochs (see e.g. [1]).

Let be the law of started in and continuously reflected at and let be the corresponding regulator, i.e. under is

Similarly, let be the law of started at and reflected in Poisson manner at , i.e. under is

Proposition 4.

For and it holds that

Proof.

Again, the proof follows merely by inspection in a similar way as for the previous results. The first relation can be seen from Figure 3,

where the left picture depicts continuous reflection at and Poisson observation at 0, and the right picture depicts the corresponding (shifted) Poisson reflection at and continuous observation at 0.

In the left picture Poisson observations yield the sequence:

. In the right picture the infima in between Poisson reflection epochs are given by , where we choose to be distributed as .

These sequences can be complemented with the respective times as in the proof of Proposition 2. Finally, it is easy to see that enters the transforms without requiring any changes. The second relation follows accordingly.

∎

Figure 3. Continuous reflection and Poisson exit (left), and Poisson reflection and continuous exit (right)

Remark 4.

It is easy to see that Proposition 4 can be generalized from reflection to so-called refraction. Concretely, consider the processes and for . In the insurance context such a refraction has the interpretation of taxation according to a loss-carry-forward scheme and tax rate , see e.g. [4].

3.3. Two-sided Poisson exit

The two-sided exit with Poisson observation at both barriers can be related to a model with another type of exit time.

Define the random time of the first observation such that the process has stayed above during the entire preceding inter-observation period, i.e. with . Similarly, define with as the first observation time such that the process has stayed below during the entire preceding inter-observation period.

Then for it holds that

(12)

To see this, one follows the same ideas as above: for the first equality consider infima in between two observations, see Figure 2, and for the second equality consider suprema in between two observations.

Similarly, we also have the reverse identities:

(13)

3.4. Parisian ruin

Parisian ruin is defined as the first time when an excursion of below 0 is longer than some time (sometimes referred to as implementation delay). Whereas the classical definition is in terms of a deterministic ,

for analytic tractability it is often assumed that is a random variable, and that an independent copy of is assigned to each excursion, see e.g. [11] and [10].

Firstly, from the memoryless property it follows that the time of Poisson ruin is also the time of Parisian ruin in the case where is an exponential random variable with rate .

Secondly, as defined in Section 3.3 is the time of Parisian ruin in the case where is Erlang distributed (since the latter is the sum of two independent exponential variables).

Similarly to (6), Equation 13 can easily be extended to

(14)

which under the present interpretation relates Parisian ruin quantities with exponential and Erlang(2)-distributed implementation delay (here we took for simplicity).

More generally, consider Parisian ruin with Erlang implementation delay and let denote the corresponding ruin time. So in particular , and . On the other hand, define as the first epoch such that , i.e. the process has been observed negative at the last Poisson epochs.

Then, along the same line of arguments, we can extend (14) (cf. Figure 4):

Figure 4. Poisson observations are in grey (left picture) and in black (right picture)

Proposition 5.

For and we have

(15)

and

(16)

4. The case of spectrally one-sided Lévy processes

If is a one-sided Lévy process, some of the identities lead to more explicit forms, and this will allow to retrieve a number of results previously obtained in the literature, now with alternative proofs, revealing some more structure of the formulas.

Without loss of generality assume that is a spectrally-negative Lévy process, i.e. it may only have negative jumps and it is not a non-increasing process. Consider its Laplace exponent

and put for .

4.1. Preliminaries

Let us first recall some basic functions which play a fundamental role in exit theory, see e.g. [8, Ch. 8].

Let be the largest (non-negative) zero of , and let be the so-called scale function: a continuous non-negative function determined by its Laplace transform . In addition, we need a second scale function

which can be rewritten as

(17)

for , see also [3].

The two basic one-sided exit identities under continuous observation are

(18)

(19)

and the Wiener-Hopf factors are given by

see e.g. [8, Ch. 8].

In order to apply Formula (6) of Proposition 2 to (19), we first need the following identities:

Lemma 1.

For it holds that

Proof.

Firstly,

(20)

which can be checked by taking transforms and comparing to the Wiener-Hopf factor.

Hence

according to (17). For the first identity it is left to note that .

Note that due to (20), for the spectrally negative Lévy process the identity (2) simplifies to the pleasant form

where is an exponential random variable with parameter . This for instance immediately explains why for a compound Poisson process with exponential jump sizes the discrete Poisson observation changes the classical ruin probability formula just by a multiplicative factor , where is the Lundberg adjustment coefficient (cf. [2, Eq.2.18]).

Using the standard identity (19), Proposition 2 and Lemma 1 we obtain

(21)

Also, by considering Proposition 2 for the negative of , see also Corollary 1, we

arrive at

because of (18) and the fact that on .

These two identities were obtained in [3, Thm. 3.1] by virtue of a rather technical argument using the expression for the potential density of .

4.3. Parisian ruin

Finally, we relate our results to previous literature on Parisian ruin. Firstly, taking and in (21) (use ) one retrieves Corollary 3.2 of [10], which is based on exponential implementation delay. Furthermore, from the form of [10, Eq.49] one can, after some lengthy calculations, obtain the following expression for

Erlang implementation delay:

(22)

where the derivative is with respect to the subindex.

We can alternatively obtain (22) directly using the results of this paper: (15) and (21) imply

which together with the expression for the Wiener-Hopf factor readily yields (22).

Acknowledgements

The authors would like to thank Ton Dieker for stimulating discussions on the topic.

References

[1]

H. Albrecher, E. C. K Cheung, and S. Thonhauser.

Randomized observation periods for the compound poisson risk model:

Dividends.

Astin Bull., 41(02):645–672, 2011.

[2]

H. Albrecher, E. C. K. Cheung, and S. Thonhauser.

Randomized observation periods for the compound Poisson risk model:

the discounted penalty function.

Scand. Actuar. J., (6):424–452, 2013.

[3]

H. Albrecher, J. Ivanovs, and X. Zhou.

Exit identities for lévy processes observed at poisson arrival

times.

Bernoulli, 2015.

(in press) arXiv:1403.2854.

[4]

H. Albrecher, J.-F. Renaud, and X. Zhou.

A Lévy insurance risk process with tax.

J. Appl. Probab., 45(2):363–375, 2008.

[5]

R. Bekker, O. J. Boxma, and J. A. C. Resing.

Lévy processes with adaptable exponent.

Adv. in Appl. Probab., 41(1):177–205, 2009.

[6]

J. Bertoin.

Lévy processes, volume 121.

Cambridge University Press, 1998.

[7]

A. B. Dieker.

Applications of factorization embeddings for Lévy processes.

Adv. in Appl. Probab., 38(3):768–791, 2006.

[8]

A. Kyprianou.

Introductory lectures on fluctuations of Lévy processes with

applications.

Universitext. Springer-Verlag, Berlin, 2006.

[9]

D. Landriault, J.-F. Renaud, and X. Zhou.

Occupation times of spectrally negative Lévy processes with

applications.

Stochastic Process. Appl., 121(11):2629–2641, 2011.

[10]

D. Landriault, J.-F. Renaud, and X. Zhou.

An insurance risk model with Parisian implementation delays.

Methodol. Comput. Appl. Probab., 16(3):583–607, 2014.

[11]

R. Loeffen, I. Czarna, and Z. Palmowski.

Parisian ruin probability for spectrally negative lévy processes.

Bernoulli, 19(2):599–609, 2013.