Maximizing Profit of Cloud Brokers under Quantized Billing Cycles: a Dynamic Pricing Strategy based on Ski-Rental Problem

Abstract

In cloud computing, users scale their resources (computational) based on their need. There is massive literature dealing with such resource scaling algorithms. These works ignore a fundamental constrain imposed by all Cloud Service Providers (CSP), i.e. one has to pay for a fixed minimum duration irrespective of their usage. Such quantization in billing cycles poses problem for users with sporadic workload. In recent literature, Cloud Broker (CB) has been introduced for the benefit of such users. A CB rents resources from CSP and in turn provides service to users to generate profit. Contract between CB and user is that of pay-what-you-use/pay-per-use. However CB faces the challenge of Quantized Billing Cycles as it negotiates with CSP. We design two algorithms, one fully online and the other partially online, which maximizes the profit of the CB. The key idea is to regulate users demand using dynamic pricing. Our algorithm is inspired by the Ski-Rental problem. We derive competitive ratio of these algorithms and also conduct simulations using real world traces to prove the efficiency of our algorithm.

I INTRODUCTION

I-A Overview

There is no universal definition of cloud computing. However as far as our research is concerned, the most apt definition of cloud computing is found in [1] which can be quoted as: ”computing as a utility”. In our day to day life the most common utilities are electricity, water, gas, heat, postpaid mobile services etc. Similarly in cloud computing, computing resources (like CPU, memory, storage, network domains, virtual desktop) are rented to users based on their demand. From user’s viewpoint, it eliminates the need of an upfront investment as an user can pay based on the amount of resources it has used. This is termed as “pay-per-use” or “pay-as-you-go” model. Therefore, resource scaling is the most fundamental aspect of cloud computing and hence extensive amount of effort has been channeled to explore this area. Cloud Service Providers (or CSP’s), like Amazon, ElasticHost etc, rent computing resource to the users in form of Virtual Machines (also called instances) or VMs. Scaling of VMs revolves around two fundamental questions:

-

1.

From Users Perspective: How to scale VMs to optimize a certain objective?

-

2.

From CSP’s Perspective: How to support the active VMs using minimum number of physical servers?

In cloud computing literature the former is often called auto scaling while the latter is called dynamic provisioning. These two questions are indeed similar and rely on a common line of research. Various researchers approached these two problems with different objectives and by using different mathematical tools. In the following we will give a brief account of these approaches.

Concerning auto scaling, the most simplest methods are the Static Threshold based policies [2] where the scaling of VMs is triggered when certain CPU parameters (CPU load, response time) crosses a pre-defined threshold. Such methods are too simple and if not designed properly face the problem of limit-cycles. Queuing theory based techniques are also very well developed. Some well cited papers in this regard can be [3, 4]. Theoretic results available in queuing theory uses simplified models and hence cannot be directly applied to complex systems like those encountered in cloud computing framework. Also the results are statistical implying that the analysis is true only over a long run after the system reaches steady-state. Control Theory based approaches aim to solve the latter problem by trying to control the transients [5, 6]. They are generally reactive methods, and hence are not good for workloads which have a lot of sudden spikes. There is a lot of active research concerning proactive methods. They depend on predictive abilities and use tools like Model Predictive Controller [7], Time Series Analysis [8, 9], Machine Learning [10]. Work done in [9] is impressive in the sense that the prediction algorithm has low overhead and also has the ability to distinguish fine workload patterns. There are several tasks which are deadline sensitive. There is a separate line of research based on heuristic algorithms [11, 12] to handle these tasks.

Similar tools have been used to optimize performance of data centers. Queuing theory has been widely used. [13] is a good reference in this regard as it uses much less approximation to model a cloud data center. Control Theoretic approaches are very famous. One popular book dealing with this subject is [14]. [15] is as well cited paper which presents practically viable method to regulate a performance metric of data center using feedback control. A very interesting method to save energy of a cloud data center has been presented in [16] where they use feedback control to regulate CPU clock frequency based on incoming request rate. Optimization based techniques have been directly used to design resource allocation strategies to maximize profit of cloud data centers [17, 18]. Another line of research considers optimizing the electricity and the cooling cost required to run a data center. Such problems are not trivial when electricity [19] and the water cost [20] are time varying.

I-B Quantized Billing Cycles and the Cloud Broker

There is a fundamental misconception regarding resource scaling in cloud computing literature. Definitely, the main objective of cloud computing is elasticity, i.e. the user can scale-up or scale-down VMs based their short term needs. However this “short term” is not infinitely small in the sense that it may not be possible to return the VMs in the very next instant after it was rented.

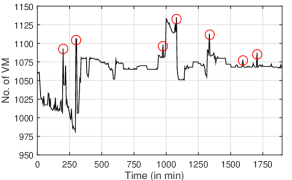

We will explain this situation using an example. Consider that we are using on-demand instances of Amazon EC2 to satisfy these demands. Billing Cycle of AmazonEC2 on demand instance is hour, i.e. you have to pay the same price if you use the VM for min or hour. We call this phenomenon as Quantized Billing Cycles (abbreviated as QBC) in the rest of the paper. This leads to serious problem especially for those users whose demand pattern is sporadic in nature. For e.g. Consider the workload trace shown in Figure 1 which shows the number of VMs required to satisfy user demand. There are few spikes in the demand curve to satisfy which one needs to buy extra VMs. These VMs may be in use for a very small fraction of hour after which it may be idle. However we cannot return these VMs before hour111The user may choose to return the VM but it won’t get any financial benefit. Therefore it is better to keep the VM for the entire billing cycle even though it remains idle. This is called smart-kill.. Hence there will be wastage of VMs.

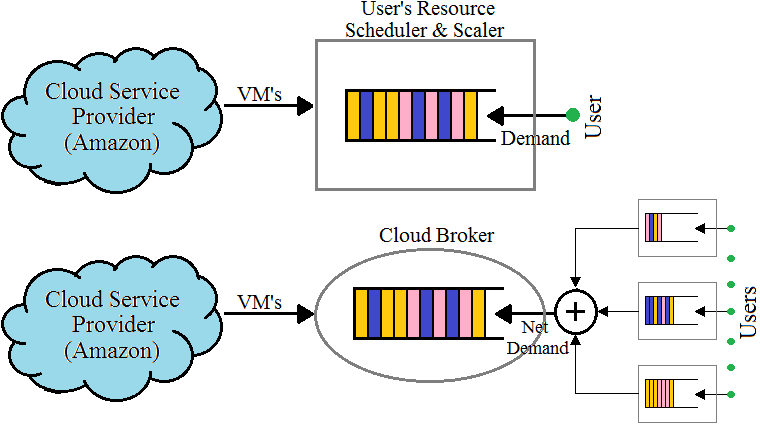

To mitigate this problem to some extent the concept of cloud broker has been proposed in recent literature [21, 22, 23]. A broker forms a middle man between the CSP and the general users as shown in Figure 2. The users send their job requests to the cloud broker. The cloud broker rents VMs from the Cloud Service Provider to service these demands. The cloud broker charges the user based on the fraction of VMs resources used to service the job request. This is called pay-what-you-use. It can also be based on per-request-basis. This transfers the challenge of QBC from the users to the cloud broker. However this issue is not as critical for the cloud broker as it is for the users. This can be understood as follows:

-

1.

QBC poses problems for those users whose demand is sporadic. Higher the sporadic nature, greater the loss.

-

2.

Cloud broker serves the aggregate demand of many users. In statistical sense, the sporadic/spiky nature in aggregated demand should be lesser compared to individual user’s demand. This is because a summer is a discrete integrator, a low pass filter which removes the noises.

In the rest of the paper we will concentrate on how a cloud broker can maximize its profit under QBC.

Remark: We would like to stress that the mathematical formulation, algorithms and analysis presented here can be applied to a single user without any change. However given that a cloud broker has a smoother workload pattern compared to a single user, a broker will benefit more compared to a user.

I-C Existing literature and our contribution

In our problem, every time a cloud broker has to buy a VM it faces the risk of under utilization of the VM in the subsequent time slots. The broker has to make a decision without knowledge of future demand. Study of such problems comes under the category of Online Algorithms, more specifically the Ski-Rental problems. There have been a few applications of Ski-Rental literature to solve real world problems. In this section we will discuss the ones pertaining to cloud computing. These works has close resemblance with our problem.

We derive our motivation from the work done in [24, 23]. In these two works the cloud broker has to decide in each time slot whether to reserve instances or to serve the demand using on-demand instances. If the demand persists for a long time then reserving is a better option. However if the demand falls down quickly it is better to use on-demand instances. Cloud broker has to make this decision without any knowledge of future demand or with partial knowledge of future demand. The authors designed both deterministic and randomized online algorithms and also derived their competitive ratio. [25] and [26] considers the same problem however the model used in [25] is more general. It tries to optimize the switching cost and electricity cost of a data center. If there is a decrease in demand then the data center has to decide whether to shut down few physical servers or let them run. To run a physical server one needs to bear the electricity bill while switching down the server incurs wear-and-tear cost. Wear-and-tear cost is higher than electricity bill in short run but smaller in the long run. If one decides to switch off the server and immediately later it is needed, then one saves a small electricity bill in the expense of suffering a large switching cost. Therefore taking such decisions without knowledge of future demand is difficult. In [25], author designed only deterministic algorithms to tackle this problem while [26] considers both deterministic and randomized algorithms. A recent work presented in [27] shows that the competitive ratio of the randomized algorithms can be improved if statistical information (like first and second order moment) of the demand process is available.

To the best of our knowledge the references given above constitutes almost all the major work dealing with the use of ski-rental framework for cloud computing applications. We make two main contributions to this literature:

-

1.

We suggest how dynamic pricing can be used to maximize the profit of the cloud broker under QBC. This can be used as an alternative to the work done in [24, 23] specially in the case where the workload is deferrable. One can also use this approach alongside [24, 23]. These two points will be discussed further in Section V.

-

2.

We show that the knowledge of future demand leads to better competitive ratio for the Partial Online algorithm. In [26] such attempts have been made but with a major assumption on the demand graph, i.e. the demand increases or decreases no more than one step in every time slot.

II Problem Formulation

II-A Motivating Example

We aim to use dynamic pricing as a control signal to regulate user demand. The motivation to use dynamic pricing in cloud computing setup is derived from the paper [28]. Before proceeding forward with the quantitative formulation of the problem, we will first consider an example to illustrate our idea. Consider the following scenario:

-

1.

Cloud broker buys VMs from Amazon at per VM. This is the cost price of the cloud broker. The billing cycle of each VM is hour min.

-

2.

Duration of a time slot = . Hence a VM is active for time slots.

-

3.

Nominal selling rate = per VM per time slot. Nominal selling rate should be such that if the VM is in use for all the time it is active ( time slots here) then the cloud broker should make a profit. In our case: . Hence the condition holds.

-

4.

The cloud broker has the freedom of changing the selling rate222In the work the term “VM price” inherently means the selling price of the VM not the cost price. at the beginning of each interval. The users remains totally aware of the current selling rate.

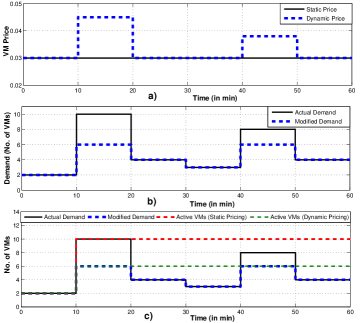

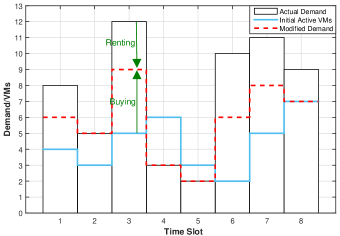

We will investigate two cases, one with static pricing and the other with dynamic pricing. Relevant graphs are shown in Figure 3. In both the cases we start with the assumption that at time the cloud broker has no VMs.

Case 1 (Static Pricing):

In static pricing, the selling price remains constant at nominal rate therefore, . In the interval the demand is of VMs while we have VMs. So we buy VMs incurring a cost of . In the interval, demand is of VMs while we have VMs (bought in the interval). So we buy VM incurring a cost of . In the next intervals the demand is less than VM and hence we don’t have to buy any more VMs. Therefore the net cost price of the cloud broker is . The net selling price of the cloud broker is . , i.e. the cloud broker suffered a loss.

Case 2 (Dynamic Pricing):

In this case the selling price varies in response to which the user’s demand gets modified. This case is similar to Case 1 except that in the and the interval the selling price goes up to and respectively. The cloud broker has to buy VMs and VMs in the interval and interval respectively incurring a cost price of . The net selling price of the cloud broker is . , i.e. the cloud broker makes a profit.

We will encapsulate the idea behind dynamic pricing by making the following key observations:

-

1.

The idea of increasing the selling price is to decrease the demand and not to increase the revenue. To understand this point consider the interval. The actual demand was VMs which could have lead to a revenue of if the rate was nominal. As the selling price increased to the demand reduced to VMs leading to an revenue of . Therefore the net revenue in the interval decreased even though the selling price increased. Similar argument is true for the interval. Therefore whenever there is an increase in price there is a decrease in revenue (and hence in profit) in that interval. Pictorially speaking, the revenue loss suffered in dynamic pricing can be captured by the area between the solid black curve and the dashed blue curve in Figure 3b.

-

2.

Yet dynamic pricing makes more profit than static pricing. This is because in static pricing, many VMs are underutilized and hence does not contribute to the revenue. This is clearly shown in Figure 3c. Underutilized VMs for static case corresponds to the area between the solid black curve and the dashed red curve while that in dynamic case corresponds to the area between the dashed green curve and the dashed blue curve. Definitely the area corresponding to static case is more.

-

3.

The idea behind dynamic pricing is: “Suffer a small loss in one interval by decreasing the demand (Refered as Demand Loss later) rather than buying a VM and then suffering a major loss in the subsequent intervals due to low demand (Refered as VM Loss later)”.

II-B Quantitative Modeling

Cloud brokerage mechanism basically consist of two blocks: 1) Resource Scheduler 2) Resource Scaler. This is shown in Figure 4. Both resource scheduler and resource scaler are controlled by the cloud broker. The job of the Resource Scheduler is to schedule the incoming tasks onto the available VMs. While doing so it has to consider service level agreement (or SLAs). Resource Scheduler can be designed using well established theoretic tools as discussed in Section I-A. The role of the resource scaler is to rent (scale-up) VMs from CSP and also to perform dynamic pricing in order to maximize the profit of the cloud broker. In this paper, we assume that resource scheduler is already designed and concentrate on designing algorithms for Resource Scaler. Note that the design of Resource Scheduler and Resource Scaler can be decoupled. The Resource Scheduler should just update the Resource Scaler regarding the number of VMs required to complete the tasks in a given time slot. Before moving forward, please note the scale-down valve which is controlled by CSP. As shown in Figure 4, this is not in control of the cloud broker. This aptly captures the notion of QBC and the process of smart-kill. As mentioned in Section I-B, due to the presence of QBC there is no point of giving back a VM before its billing cycle ends. This will be equivalent to the CSP automatically scaling down the VMs after its billing cycle. Therefore from cloud broker’s perspective: “Only scaling-up of VMs is controllable but scaling-down is not”.

We will now pose our problem mathematically. We consider that the user pays the cloud broker based on per-request/pay-what-you-use basis. In such a scenario the resource scaler has to solve the following profit optimization problem:

| subjectto | ||||

In optimization problem , is the profit to be maximized. The term is the profit at interval where, is the selling price per VM per time slot, is the number of VMs required to service the incoming job request and is the number of VMs bought at interval. Without any loss of generality we normalize the cost price of a VM to unit. is the period of the billing cycle and hence is the number of active VMs in the interval. is the modified VM demand when the selling price is . The relation between the actual demand and the modified demand is captured by the price-demand function . If , the nominal price, then . The revenue earned by selling a VM at the nominal price of for one complete billing cycle is . For the cloud broker to make profit, , being the cost price of a VM. It should be noted that all the variables associated with lies in the set .

In conventional sense, the optimization problems dealt in ski-rental framework are minimization problems. Therefore we are interested in formulating as an equivalent minimization problem. In this regard note that

| (1) | |||||

In equation (1) the first term is not controllable and hence the maximization of becomes equivalent to minimization of . We thus pose the following optimization problem which is equivalent to :

| subjectto | ||||

Intuitively speaking, does the following: Consider that there is a hike in demand which decays soon. In such a case will increase the selling price to reduce the demand. In this way the cloud broker will suffer a small “Demand Loss”. Buying enough VMs to support the demand hike is not a good option in such scenario as the cloud broker may suffer a huge “VM Loss” in subsequent intervals due to underutilized VMs. But if the hike in demand persists for a long time it is better to buy VMs to support this hike. However is an offline optimization problem, i.e. to solve we need for all . It is not possible to know in advance if an increase in demand is going to persist or will decay soon. The challenge is to design algorithms which can make such decisions online based on present and past data. Such algorithms are called online algorithms.

We now define the concept of Competitive Ratio which will be used later in Section III to compare the performance of the online algorithm with its optimal offline counterpart. Say that an online algorithm and the optimal algorithm ( here) suffers a loss and respectively for a given demand sequence . Then algorithm is called competitive if:

| (2) |

Indeed . In inequality (2) we have slightly misused the notation. is a dimensional vector of non negative real numbers not transpose of a non negative real number.

II-C Properties and Assumptions

Properties of Demand and Revenue Function

Most of the price demand function (also called demand function) found in real world must satisfy the following conditions:

-

1.

.

-

2.

is monotonically increasing in .

-

3.

is monotonically decreasing in in the range while it is constant333We assume that the demand cannot increase above the actual demand even if the price decreases below at in the range .

-

4.

The revenue function , is monotonically decreasing in in the range . This captures the idea that increasing the selling price is to decrease the demand and not to increase the revenue. As is constant in , it is obvious that will linearly increase in this range. Revenue function is maximum at and hence this is set as the nominal price.

Let . Then according to property 4 we have

| (3) |

Differentiating inequality (3) using chain rule we get

| (4) |

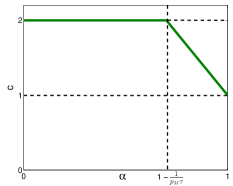

A demand function satisfying inequality (4) will be strictly monotonically decreasing if . Two cases may arise:

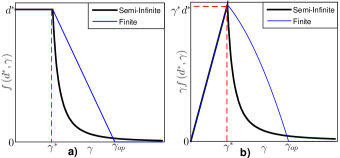

Case 1 (Semi-Infinite Operating Zone): for all and hence the demand function is strictly monotonically decreasing in this range.

Case 2 (Finite Operating Zone): for all . For , . Due to property 1, for all . Therefore the demand function is strictly monotonically decreasing in the range .

The range of where is strictly monotonically decreasing is called the operating zone. Figure 5 illustrates the concept of operating zone for the above two cases. Strict monotonic nature of in the operating zone implies that the function is invertible in this range. Mathematically, the following function exist in the operating zone,

| (5) |

The function returns the imposed price given the actual demand and the modified demand .

Remark: The role of dynamic pricing is to regulate the demand. In the range , price has no effect on the demand and yet the cloud broker will incur a demand loss. Therefore to minimize we work in the operating zone.

Assumptions in Problem Formulation

-

1.

We ignore the effect of reputation while formulating our optimization problem. By increasing the price we force some tasks to exit the queue. By doing this we earn negative reputation of the users. A static demand function of the form does not capture the effect of pricing history and hence the role of reputation.

-

2.

The partial online algorithm, discussed later in Section III, relies on demand prediction for future window . In reality, only an estimate of future demand is possible however we assume perfect knowledge of future demand.

-

3.

In real-life scenario, the relation between the modified demand and the actual demand is not governed by a deterministic function . Rather the demand has a probability distribution444One may consider that the function is the mean of this probability distribution. in the range for a given . However many works dealing with social welfare maximization using dynamic pricing (like [29, 28]) consider such deterministic demand function. We also assume the knowledge of .

-

4.

Define the following function in the operating zone,

(6) Also define two more variables,

(7) We impose the following constrains on and ,

(8) Inequality implies that renting is cheaper than buying in short run while the inequality implies that buying is cheaper in the long run. We will further elaborate this in Section III-A.

Let . Then according to inequality (8) we have

| (9) |

Differentiating inequality (9) using chain rule we get

| (10) |

According to inequality (4), the following inequality is true in the operating zone

| (11) |

| (12) |

III Online Optimization Problem

III-A Ski-Rental Problem

The ski-rental problem abstracts a class of problem in which a player has to decide whether to buy or rent a resource without a priori knowledge of the period of usage. Renting is cheaper if the period of usage is short while buying is cheaper in the long run. In the original problem a skier is faced with the option of either buying or renting a set of skis without knowing in advance the number of days she will be skiing.

Cost of buying skis is while renting cost per day where . If the skier knows in advance that she will be skiing for days then the choice of buying or renting is simple. If then the skier will buy the skis in the very first day. Otherwise she will keep renting the skis for days.

The online case is more challenging. In ski-rental literature, the concept of breakeven point is used to design online algorithms. Such algorithms suggest that the skier should keep on renting the skis till the day when the cost of renting , is more than the cost of buying, i.e. . On the day she should buy the skis. These is shown to be the most optimal deterministic online algorithm and has a competitive ratio of .

Ski-Rental problem has been used to solve real life problems like TCP acknowledgement problem [30], Bahncard problem [31] etc. Its application in cloud computing has already been discussed in Section I-C. The key step towards using ski-rental literature for our problem would be to map the following four entities in our context: 1) Renting 2) Buying 3) Buying Cost 4) Renting Cost. In remaining of this section we will define these entities.

1. Renting: It is the process of decreasing the demand by increasing the selling price of the VMs. To decrease actual demand to modified demand we impose selling price of .

2. Buying: It is the process of buying VMs to support the modified demand . If the number of active VMs in the beginning of time slot is then .

Figure 6 illustrates the renting and buying process. In the time slot renting is equivalent to reducing the demand from to while buying is the process of purchasing VMs. Similarly in the , and the time slot there is both renting and buying. There is no renting in the time slot, we only buy VMs. On contrary there is no buying in the time slot, we only rent the demand from to . In the and the time slot there is neither renting nor buying because the number of active VMs in the beginning of these time slots is more than the actual demand.

3. Buying Cost: It is the cost of buying VMs. As the cost price of VM is assumed to be unit, the cost of buying VMs is equal to units.

4. Renting Cost: It is the demand loss in a given time slot associated with reducing a demand from to , where , when the actual demand is . Mathematically

| (13) |

It should be noted that unlike the renting cost found in other ski-rental literature, for our case, is not a constant. It is a function of , and . However we will not mention these parameters explicitly for notational simplicity. Please Note: “Renting Cost” and “demand loss” means the same and will be used interchangeably.

Now we will explain the importance of inequality constrain (8). As mentioned before renting cost should be more than the buying cost in the long run. Given that the billing cycle is of period, the cost of renting for period should be greater than the cost of buying. Otherwise buying of VMs will never be required. The cost of buying VMs is while the cost of Renting of demands for period is . Hence, . Similarly renting cost should be lesser than the buying cost in the short run. Therefore the cost of renting demands for period should be less than the cost of buying VMs. Hence, . Therefore to formulate our problem in Ski-Rental framework, it is necessary that the following inequality holds

| (14) |

Proof: Consider the following,

| (15) | |||||

| (16) |

Equation (15) and inequality (16) comes from the definition of and (refer equation (6) and (7)). Similarly,

| (17) |

The qualitative interpretation of inequality (16) and inequality (17) is that the minimum and maximum renting cost of demand is and respectively. If inequality (8) holds, then . Substituting this in inequality (16) we get

| (18) |

Similarly if inequality (8) holds, then . Substituting this in inequality (17) we get

| (19) |

Combining inequality (18) and (19) we get inequality (14). This completes the proof.

III-B Online Algorithm

As discussed earlier in the previous subsection the concept of breakeven point has been widely used to design online algorithms in ski-rental literature. The key idea is to keep renting till the time renting cost equals buying cost. Here buying cost is the breakeven point. If renting cost exceeds the buying cost, we buy the resource. In this section we will apply these concepts to design two online algorithm: 1) Fully Online Algorithm which has no knowledge of future demand 2) Partial Online Algorithm, which assumes perfect future demand information for future window . Intuitively speaking, both Fully Online Algorithm and Partial Online Algorithm works in pessimistic sense. It always assumes that an increase in demand is not going to persist and hence it reduces the demand by increasing the selling price of the VMs. This reduction in demand incurs a renting cost. However at every time interval it calculates the Net Renting Cost in the past and the future intervals. If the Net Renting Cost exceeds unit (the buying cost of VM), it buys a new VM.

The psuedocode of partial online algorithm with future window of is given in Algorithm 1. The same psuedocode is applicable for the fully online algorithm if we substitute . Both fully/partial online algorithm consist of three basic steps. In the following we will explain these steps in relation to the fully online algorithm.

Let be the number of VM’s at time

1. Set

2. Predict actual demand for .

3.

4. Set Net Renting Cost . Also set .

5.

6.

7.

8.

9.

10.

11.

12. Buy a new VM: .

13. Update the number of VM’s that can be used in future:

14. Update the number of VM’s in the history indicating

that previous mistakes have been corrected:

15.

16.

17.

18.

19.

20.

21.

22. Jump to Step 2.

Step 1. Calculating Net Renting Cost

We calculate the net renting cost which we could have been saved if we rented less demand in each slot for the past period. Let be the number of active VMs at time . Then the net renting cost is

| (20) |

Equation (20) is valid only if . If for a given interval , the renting cost for that interval is . This is done in Steps 4 to 10 of Algorithm 1.

Step 2. Buying new VM

This is done in Steps 11 to 16 of Algorithm 1. In our case the cost of a VM is . If then the corresponding demands should not have been reduced. Rather we should have bought a VM to serve them. To compensate for this mistake we buy a VM in the current time slot. We increase the current and the future by to indicate that an extra VM is available. We also increase the past by to indicate that a corrective measure was taken. We then jump back to Step 1. However if , we jump to Step 3.

Step 3. Setting the Selling Price

Let the number of active VMs in the current time slot be after performing Step 2 and Step 3. Then is the modified demand. So we set our selling price as .

The partial online algorithm is almost same as the fully online algorithm. The difference lies in the calculation of Net Renting Cost in Step 1. In case of fully online algorithm it is calculated for the period to while for partial online algorithm it is calculated for the period to .

Theorem 1: Competitive Ratio of partial online algorithm is

| (21) |

where and .

Proof: Please refer appendix for the proof.

Corollary 1: Fully online algorithm is -competitive.

Proof: For fully online algorithm . Hence . According to inequality (8) we have . Also implying . Therefore and hence .

Note that the competive ratio of the partial online algorithm can be more explicitly written as

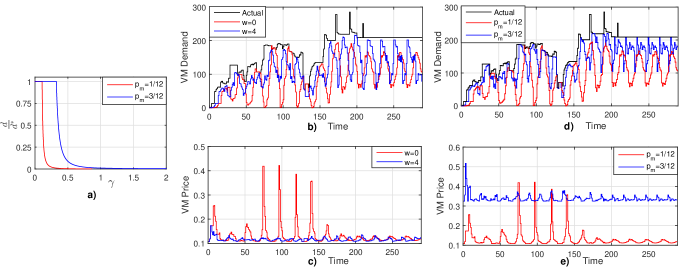

As , there always exist an such that . This gives the theoretical guarantee that future demand information indeed improves the performance of the online algorithm. Figure 7 shows a typical plot of equation (21).

IV Simulation Results

We performed simulations driven by real world traces to validate the online dynamic pricing algorithm proposed in the paper.

The first step is to generate the actual demand curve. To do this we have used google cluster usage traces available in [32]. The actual demand curve is shown in Figure 7b and 7d. The curve spans day and is slotted in min interval. Cost price of a VM is taken to be unit. A VM has a billing cycle of hour and hence . The next step is to generate the demand function. A real world demand function can only be inferred by doing a market survey. But for the sake of simulation, we have synthesized our own demand function. This can be explained in steps:

-

1.

We consider a demand function of the form .

-

2.

A value of and satisfying inequality (8) is chosen.

-

3.

A finite interval of price is uniformly divided into small parts.

- 4.

As part of this simulation we will conduct two comparative studies, first to study the effect of demand prediction and secondly the effect of .

To study the effect of demand prediction we first synthesized a demand function with and . We then simulated Algorithm 1 for and . The results of the simulation is clearly shown in Figure 7b and 7c. Compared to , the reduction in demand is more in . This shows the pessimistic nature of our online algorithm, i.e. it prefers reducing the demand compared to buying new VMs. With increase in future window the algorithm tends towards the optimal counterpart. The net profit for is units while for it is units. The net profit is more for and hence the net loss (refer ) is less. This is in consensus with Theorem 1.

We next studied the effect of on our algorithm. To do this we constructed another demand function with and . From Figure 7d and 7e we can observe that if is high the effect of pricing on demand is less. This is an obvious consequence of the definition of .

V Discussion and Extensions

We discussed the unique challenge posed by the presence of quantized billing cycles. The dynamic pricing strategy proposed in this paper can be considered as an alternative to the work done in [24] to maximize the profit of the cloud broker. Merging our algorithm with that of [24] should be very interesting. Such a merging will lead to a very interesting class of problems where the cloud broker has to decide whether to a) reduce the demand by increasing the VM price b) buy on-demand VMs to support the demand c) reserve VMs. This problem is similar to multislope ski-rental problem.

Two deterministic online algorithms were designed to increase the profit of cloud brokers in the presence of QBC. The competitive ratio of both the algorithms were derived. We showed the importance of demand prediction by deriving a better competitive ratio for the partial online algorithm than those found in ski-rental literature. In similar lines we would like to explicitly point out that the competitive ratio of Algorithm 3 of [24], i.e. deterministic algorithm with demand prediction window , has a competitive ratio of which is better than that reported in [24] (refer Proposition 5). This result is new in ski-rental literature.

It has been widely reported in ski-rental literature that randomized algorithms has better competitive ratio than its deterministic counterpart. Extending our algorithm to its randomized counterpart should be trivial. However deriving a better competitive ratio for the randomized algorithm with demand prediction may be challenging.

The key idea of our algorithms is to use pricing signal to regulate user demand. One may argue that such an algorithm gives poor service to the user as it pushes tasks out of the queue in order to maximize cloud broker’s profit. We would like to make few comments in this regard:

-

1.

Those tasks which gets pushed out of the queue can enter it again at a later instant. So we are not rejecting the tasks. Rather we are deferring it. Our algorithm is specifically good if is low. A low implies that even with a small increase in price there will be significant change in demand. Qualitatively, a low correspond to tasks with low priority. Such tasks can be deferred.

-

2.

Some literature considers penalizing the cloud provider when it fails to meet SLA’s (refer [33]. Such a practice is not encouraged in cloud computing as it is a service oriented computing paradigm. If the cloud provider accepts the task, it must meet the SLAs. If it cannot it is better that it rejects the task. We are following similar practice.

-

3.

We can penalize cloud broker to push tasks out of the queue by introducing reputation factor. As discussed in section II-C we need to consider dynamic price-demand function to include reputation factor. Such an extension of our work will be challenging but a very fruitful research.

As an immediate extension of our work we are interested in two areas. Assumption 4 discussed in Section II-C may not be true for all real world demand functions. We are exploring the implication of relaxing it. Our intuition is that if we make a small modification in Algorithm 1, the competitive ratio will remain the same. We are also actively working on the randomized algorithm for this problem. More specifically we are exploring the possibility of improving the competitive ratio of the randomized algorithm in the presence of statistical information about the actual demand. This is motivated by the work done in [27].

APPENDIX

We will denote the partial online algorithm with future window of by and the offline optimal algorithm by . We will first consider two lemmas which are important for the proof.

Lemma 1: Let buy VMs while buy VMs throughout the time duration of to . Then for any demand sequence , .

Lemma 1 is an obvious consequence of the pessimistic nature of the fully/partial online algorithm as discussed in Section III-B. Both these algorithms assumes that a rise in demand is not going to persist and hence has the tendency to reduce the demand by increasing the selling price rather than buying VMs to support the rise in demand. Therefore . Please refer Appendix A of [24] for the proof.

Lemma 2: The net renting cost of those demands that were served by the same VM in should be greater than or equal to (the breakeven point).

Proof: The proof directly follows from the definition of . We prove this lemma by contradiction. Consider that in a VM was bought to serve demands whose net renting cost is less than . The loss suffered to buy a VM to support these demands is more than the loss suffered to rent these demands. Therefore there can be a better algorithm to reduce the loss which contradicts the definition of .

Let and rent and demands respectively at time . Let and be the net renting cost of and respectively. We have,

Let denote the net renting cost incurred in which is not incurred in . Mathematically

where . We are interested in upper bounding . To do this, consider the demands that were rented in but not in . These demands were served by not more than VMs in . We focus on the demands served by one of these VMs. This is shown in the following figure

Figure 9 shows the demands served by a VM in which is bought at time and last till . The shaded areas shows the demands which are served by this VM. If the area is not shaded then in that time slot the VM does not serve any demand. The shaded areas can be scattered anywhere in the time interval . According to Lemma 1, the net renting cost of the demands depicted by these shaded areas should be greater than or equal to .

Now we investigate how these demands will be treated by . While calculating the net renting cost, considers both future demand and past demand. This is shown in figure 9 by the three arrows. calculates the net renting cost in the interval where is the current time, the interval corresponds to the past window while is the future window. If the net renting cost in the interval becomes , then will buy a VM. As mentioned before the net renting cost in the interval is definitely greater than or equal to (due to Lemma 1). Therefore there is definitely a time satisfying when will buy a VM. The demands in the interval will be rented while that in the interval will be served by the VM. The maximum renting cost of the demands in the interval is . This can be understood as follows:

-

1.

The maximum renting cost of one demand is (refer inequality (17)). If all the intervals in the past window has a demand, then the maximum renting cost in the past window is . However the renting cost in the interval is equal to and hence the renting cost in the interval cannot exceed . Therefore the maximum renting cost in the interval is .

-

2.

Due to inequality (8), there may be a satisfying such that .

Therefore if buys a VM at time then the demands in the interval was rented in while it is served by a VM in . The maximum renting cost of these demands is . As mentioned before, . Therefore the maximum renting cost of those demands which are served by a VM in but rented in is upper bounded by . Given that at most VMs serve such demands we have

| (22) | |||||

where . Let . We will use inequality (22) to upper bound :

| (23) | |||||

Let be the net loss incurred in . Then,

| (24) |

Similarly let be the net loss incurred in . We have,

| (25) | |||||

| (26) | |||||

| (27) |

Inequality (26) is obtained by substituting inequality (23) in equation (25). We now use Lemma 2 followed by inequality (24) in inequality (27) to get

| (28) | |||||

| (29) | |||||

| (30) |

Therefore the competitive ratio of is . This proves Theorem 1.

References

- [1] M. Armbrust, A. Fox, R. Griffith, A. D. Joseph, R. H. Katz, A. Konwinski, G. Lee, D. A. Patterson, A. Rabkin, I. Stoica, and M. Zaharia, “Above the clouds: A berkeley view of cloud computing,” EECS Department, University of California, Berkeley, Tech. Rep., 2009. [Online]. Available: http://www.eecs.berkeley.edu/Pubs/TechRpts/2009/EECS-2009-28.html

- [2] M. Z. Hasan, E. Magana, A. Clemm, L. Tucker, and S. L. D. Gudreddi, “Integrated and autonomic cloud resource scaling,” in Network Operations and Management Symposium (NOMS), 2012 IEEE. IEEE, 2012, pp. 1327–1334.

- [3] B. Urgaonkar, P. Shenoy, A. Chandra, P. Goyal, and T. Wood, “Agile dynamic provisioning of multi-tier internet applications,” ACM Transactions on Autonomous and Adaptive Systems (TAAS), vol. 3, no. 1, p. 1, 2008.

- [4] A. Ali-Eldin, J. Tordsson, and E. Elmroth, “An adaptive hybrid elasticity controller for cloud infrastructures,” in Network Operations and Management Symposium (NOMS), 2012 IEEE. IEEE, 2012, pp. 204–212.

- [5] X. Dutreilh, N. Rivierre, A. Moreau, J. Malenfant, and I. Truck, “From data center resource allocation to control theory and back,” in Cloud Computing (CLOUD), 2010 IEEE 3rd International Conference on. IEEE, 2010, pp. 410–417.

- [6] P. Padala, K.-Y. Hou, K. G. Shin, X. Zhu, M. Uysal, Z. Wang, S. Singhal, and A. Merchant, “Automated control of multiple virtualized resources,” in Proceedings of the 4th ACM European conference on Computer systems. ACM, 2009, pp. 13–26.

- [7] L. Wang, J. Xu, M. Zhao, and J. Fortes, “Adaptive virtual resource management with fuzzy model predictive control,” in Proceedings of the 8th ACM international conference on Autonomic computing. ACM, 2011, pp. 191–192.

- [8] E. Caron, F. Desprez, and A. Muresan, “Pattern matching based forecast of non-periodic repetitive behavior for cloud clients,” Journal of Grid Computing, vol. 9, no. 1, pp. 49–64, 2011.

- [9] Z. Gong, X. Gu, and J. Wilkes, “Press: Predictive elastic resource scaling for cloud systems,” in Network and Service Management (CNSM), 2010 International Conference on. IEEE, 2010, pp. 9–16.

- [10] P. Bodik, “Automating datacenter operations using machine learning,” Ph.D. dissertation, University of California, Berkeley, 2010.

- [11] R. N. Calheiros and R. Buyya, “Meeting deadlines of scientific workflows in public clouds with tasks replication,” Parallel and Distributed Systems, IEEE Transactions on, vol. 25, no. 7, pp. 1787–1796, 2014.

- [12] M. A. Rodriguez and R. Buyya, “Deadline based resource provisioningand scheduling algorithm for scientific workflows on clouds,” Cloud Computing, IEEE Transactions on, vol. 2, no. 2, pp. 222–235, 2014.

- [13] H. Khazaei, J. Misic, and V. B. Misic, “Performance analysis of cloud computing centers using m/g/m/m+ r queuing systems,” Parallel and Distributed Systems, IEEE Transactions on, vol. 23, no. 5, pp. 936–943, 2012.

- [14] J. L. Hellerstein, Y. Diao, S. Parekh, and D. M. Tilbury, Feedback control of computing systems. John Wiley & Sons, 2004.

- [15] T. F. Abdelzaher, K. G. Shin, and N. Bhatti, “Performance guarantees for web server end-systems: A control-theoretical approach,” Parallel and Distributed Systems, IEEE Transactions on, vol. 13, no. 1, pp. 80–96, 2002.

- [16] W. Qin and Q. Wang, “Modeling and control design for performance management of web servers via an lpv approach,” Control Systems Technology, IEEE Transactions on, vol. 15, no. 2, pp. 259–275, 2007.

- [17] D. Ardagna, M. Trubian, and L. Zhang, “Sla based resource allocation policies in autonomic environments,” Journal of Parallel and Distributed Computing, vol. 67, no. 3, pp. 259–270, 2007.

- [18] Z. Liu, M. S. Squillante, and J. L. Wolf, “On maximizing service-level-agreement profits,” in Proceedings of the 3rd ACM conference on Electronic Commerce. ACM, 2001, pp. 213–223.

- [19] M. Polverini, A. Cianfrani, S. Ren, and A. V. Vasilakos, “Thermal-aware scheduling of batch jobs in geographically distributed data centers,” Cloud Computing, IEEE Transactions on, vol. 2, no. 1, pp. 71–84, 2014.

- [20] S. Ren, “Batch job scheduling for reducing water footprints in data center,” in Communication, Control, and Computing (Allerton), 2013 51st Annual Allerton Conference on. IEEE, 2013, pp. 747–754.

- [21] K. Vermeersch, “A broker for cost-efficient qos aware resource allocation in ec2,” Ph.D. dissertation, Master’s thesis, University of Antwerp, 2011.

- [22] S. Nesmachnow, S. Iturriaga, and B. Dorronsoro, “Efficient heuristics for profit optimization of virtual cloud brokers,” Computational Intelligence Magazine, IEEE, vol. 10, no. 1, pp. 33–43, 2015.

- [23] W. Wang, D. Niu, B. Li, and B. Liang, “Dynamic cloud resource reservation via cloud brokerage,” in Distributed Computing Systems (ICDCS), 2013 IEEE 33rd International Conference on. IEEE, 2013, pp. 400–409.

- [24] W. Wang, B. Li, and B. Liang, “To reserve or not to reserve: Optimal online multi-instance acquisition in iaas clouds,” in Proc. USENIX Intl. Conf. Autonomic Computing (ICAC), 2013.

- [25] M. Lin, A. Wierman, L. L. Andrew, and E. Thereska, “Dynamic right-sizing for power-proportional data centers,” IEEE/ACM Transactions on Networking, vol. 21, no. 5, pp. 1378–1391, 2013.

- [26] T. Lu, M. Chen, and L. L. Andrew, “Simple and effective dynamic provisioning for power-proportional data centers,” Parallel and Distributed Systems, IEEE Transactions on, vol. 24, no. 6, pp. 1161–1171, 2013.

- [27] A. Khanafer, M. Kodialam, and K. P. N. Puttaswamy, “The constrained ski-rental problem and its application to online cloud cost optimization,” in Proc. IEEE INFOCOM, 2013, pp. 1492–1500.

- [28] M. Polverini, S. Ren, and A. Cianfrani, “Capacity provisioning and pricing for cloud computing with energy capping,” in Proc. Allerton Conference, 2013, pp. 413–420.

- [29] I. Menache, A. Ozdaglar, and N. Shimkin, “Socially optimal pricing of cloud computing resources,” in VALUETOOLS, 2011.

- [30] A. Karlin, C. Kenyon, and D. Randall, “Dynamic tcp acknowledgment and other stories about e/(e-1),” Algorithmica, vol. 36, no. 3, pp. 209–224, 2003.

- [31] R. Fleischer, “On the bahncard problem,” Theoretical Computer Science, vol. 268, no. 1, pp. 161–174, 2001.

- [32] C. Reiss, J. Wilkes, and J. Hellerstein. (2011) Google cluster-usage traces: format+schema. [Online]. Available: https://code.google.com/p/googleclusterdata/

- [33] S. Di and C.-L. Wang, “Error-tolerant resource allocation and payment minimization for cloud system,” Parallel and Distributed Systems, IEEE Transactions on, vol. 24, no. 6, pp. 1097–1106, 2013.