capbtabboxtable[][\FBwidth]

Parallelizing MCMC with Random Partition Trees

Abstract

The modern scale of data has brought new challenges to Bayesian inference. In particular, conventional MCMC algorithms are computationally very expensive for large data sets. A promising approach to solve this problem is embarrassingly parallel MCMC (EP-MCMC), which first partitions the data into multiple subsets and runs independent sampling algorithms on each subset. The subset posterior draws are then aggregated via some combining rules to obtain the final approximation. Existing EP-MCMC algorithms are limited by approximation accuracy and difficulty in resampling. In this article, we propose a new EP-MCMC algorithm PART that solves these problems. The new algorithm applies random partition trees to combine the subset posterior draws, which is distribution-free, easy to resample from and can adapt to multiple scales. We provide theoretical justification and extensive experiments illustrating empirical performance.

1 Introduction

Bayesian methods are popular for their success in analyzing complex data sets. However, for large data sets, Markov Chain Monte Carlo (MCMC) algorithms, widely used in Bayesian inference, can suffer from huge computational expense. With large data, there is increasing time per iteration, increasing time to convergence, and difficulties with processing the full data on a single machine due to memory limits. To ameliorate these concerns, various methods such as stochastic gradient Monte Carlo [1] and sub-sampling based Monte Carlo [2] have been proposed. Among directions that have been explored, embarrassingly parallel MCMC (EP-MCMC) seems most promising. EP-MCMC algorithms typically divide the data into multiple subsets and run independent MCMC chains simultaneously on each subset. The posterior draws are then aggregated according to some rules to produce the final approximation. This approach is clearly more efficient as now each chain involves a much smaller data set and the sampling is communication-free. The key to a successful EP-MCMC algorithm lies in the speed and accuracy of the combining rule.

Existing EP-MCMC algorithms can be roughly divided into three categories. The first relies on asymptotic normality of posterior distributions. [3] propose a “Consensus Monte Carlo” algorithm, which produces final approximation by a weighted averaging over all subset draws. This approach is effective when the posterior distributions are close to Gaussian, but could suffer from huge bias when skewness and multi-modes are present. The second category relies on calculating an appropriate variant of a mean or median of the subset posterior measures [4, 5]. These approaches rely on asymptotics (size of data increasing to infinity) to justify accuracy, and lack guarantees in finite samples. The third category relies on the product density equation (PDE) in (1). Assuming is the observed data and is the parameter of interest, when the observations are iid conditioned on , for any partition of , the following identity holds,

| (1) |

if the prior on the full data and subsets satisfy . [6] proposes using kernel density estimation on each subset posterior and then combining via (1). They use an independent Metropolis sampler to resample from the combined density. [7] apply the Weierstrass transform directly to (1) and developed two sampling algorithms based on the transformed density. These methods guarantee the approximation density converges to the true posterior density as the number of posterior draws increase. However, as both are kernel-based, the two methods are limited by two major drawbacks. The first is the inefficiency of resampling. Kernel density estimators are essentially mixture distributions. Assuming we have collected 10,000 posterior samples on each machine, then multiplying just two densities already yields a mixture distribution containing components, each of which is associated with a different weight. The resampling requires the independent Metropolis sampler to search over an exponential number of mixture components and it is likely to get stuck at one “good” component, resulting in high rejection rates and slow mixing. The second is the sensitivity to bandwidth choice, with one bandwidth applied to the whole space.

In this article, we propose a novel EP-MCMC algorithm termed “parallel aggregation random trees” (PART), which solves the above two problems. The algorithm inhibits the explosion of mixture components so that the aggregated density is easy to resample. In addition, the density estimator is able to adapt to multiple scales and thus achieve better approximation accuracy. In Section 2, we motivate the new methodology and present the algorithm. In Section 3, we present error bounds and prove consistency of PART in the number of posterior draws. Experimental results are presented in Section 4. Proofs and part of the numerical results are provided in the supplementary materials.

2 Method

Recall the PDE identity (1) in the introduction. When data set is partitioned into subsets , the posterior distribution of the subset can be written as

| (2) |

where is the prior assigned to the full data set. Assuming observations are iid given , the relationship between the full data posterior and subset posteriors is captured by

| (3) |

Due to the flaws of applying kernel-based density estimation to (3) mentioned above, we propose to use random partition trees or multi-scale histograms. Let be the collection of all -partitions formed by disjoint rectangular blocks, where a rectangular block takes the form of for some . A -block histogram is then defined as

| (4) |

where are the blocks and are the total number of posterior samples on the subset and of those inside the block respectively (assuming the same across subsets). We use to denote the area of a block. Assuming each subset posterior is approximated by a -block histogram, if the partition is restricted to be the same across all subsets, then the aggregated density after applying (3) is still a -block histogram (illustrated in the supplement),

| (5) |

where is the normalizing constant, ’s are the updated weights, and is the block-wise distribution. Common histogram blocks across subsets control the number of mixture components, leading to simple aggregation and resampling procedures. Our PART algorithm consists of space partitioning followed by density aggregation, with aggregation simply multiplying densities across subsets for each block and then normalizing.

2.1 Space Partitioning

To find good partitions, our algorithm recursively bisects (not necessarily evenly) a previous block along a randomly selected dimension, subject to certain rules. Such partitioning is multi-scale and related to wavelets [8]. Assume we are currently splitting the block along the dimension and denote the posterior samples in by for the subset. The cut point on dimension is determined by a partition rule . The resulting two blocks are subject to further bisecting under the same procedure until one of the following stopping criteria is met — (i) or (ii) the area of the block becomes smaller than . The algorithm returns a tree with leafs, each corresponding to a block . Details are provided in Algorithm 1.

In Algorithm 1, becomes the minimum edge length of a block (possibly different across dimensions). Quantities are the left and right boundaries of the samples respectively, which take the sample minimum/maximum when the support is unbounded. We consider two choices for the partition rule — maximum (empirical) likelihood partition (ML) and median/KD-tree partition (KD).

Maximum Likelihood Partition (ML)

ML-partition searches for partitions by greedily maximizing the empirical log likelihood at each iteration. For we have

| (6) |

where and are counts of posterior samples in and , respectively. The solution to (6) falls inside the set . Thus, a simple linear search after sorting samples suffices (by book-keeping the ordering, sorting the whole block once is enough for the entire procedure). For , we have

| (7) |

similarly solved by a linear search. This is dominated by sorting and takes time.

Median/KD-Tree Partition (KD)

Median/KD-tree partition cuts at the empirical median of posterior samples. When there are multiple subsets, the median is taken over pooled samples to force to be the same across subsets. Searching for median takes time [9], which is faster than ML-partition especially when the number of posterior draws is large. The same partitioning strategy is adopted by KD-trees [10].

2.2 Density Aggregation

Given a common partition, Algorithm 2 aggregates all subsets in one stage. However, assuming a single “good” partition for all subsets is overly restrictive when is large. Hence, we also consider pairwise aggregation [6, 7], which recursively groups subsets into pairs, combines each pair with Algorithm 2, and repeats until one final set is obtained. Run time of PART is dominated by space partitioning (BuildTree), with normalization and resampling very fast.

2.3 Variance Reduction and Smoothing

Random Tree Ensemble

Inspired by random forests [11, 12], the full posterior is estimated by averaging independent trees output by Algorithm 1. Smoothing and averaging can reduce variance and yield better approximation accuracy. The trees can be built in parallel and resampling in Algorithm 2 only additionally requires picking a tree uniformly at random.

Local Gaussian Smoothing

As another approach to increase smoothness, the blockwise uniform distribution in (5) can be replaced by a Gaussian distribution , with mean and covariance estimated “locally” by samples within the block. A multiplied Gaussian approximation is used: , where and are estimated with the subset. We apply both random tree ensembles and local Gaussian smoothing in all applications of PART in this article unless explicitly stated otherwise.

3 Theory

In this section, we provide consistency theory (in the number of posterior samples) for histograms and the aggregated density. We do not consider the variance reduction and smoothing modifications in these developments for simplicity in exposition, but extensions are possible. Section 3.1 provides error bounds on ML and KD-tree partitioning-based histogram density estimators constructed from independent samples from a single joint posterior; modified bounds can be obtained for MCMC samples incorporating the mixing rate, but will not be considered here. Section 3.2 then provides corresponding error bounds for our PART-aggregrated density estimators in the one-stage and pairwise cases. Detailed proofs are provided in the supplementary materials.

Let be a -dimensional posterior density function. Assume is supported on a measurable set . Since one can always transform to a bounded region by scaling, we simply assume as in [8, 13] without loss of generality. We also assume that .

3.1 Space partitioning

Maximum likelihood partition (ML)

For a given , ML partition solves the following problem:

| (8) |

for some and , where . We have the following result.

Theorem 1.

Choose . For any , if the sample size satisfies that , then with probability at least , the optimal solution to (8) satisfies that

where with and .

Median partition/KD-tree (KD)

The KD-tree cuts at the empirical median for different dimensions. We have the following result.

Theorem 2.

For any , define . For any , if , then with probability at least , we have

If is further lower bounded by some constant , we can then obtain an upper bound on the KL-divergence. Define and we have

When there are multiple functions and the median partition is performed on pooled data, the partition might not happen at the empirical median on each subset. However, as long as the partition quantiles are upper and lower bounded by and for some , we can establish results similar to Theorem 2. The result is provided in the supplementary materials.

3.2 Posterior aggregation

The previous section provides estimation error bounds on individual posterior densities, through which we can bound the distance between the true posterior conditional on the full data set and the aggregated density via (3). Assume we have density functions and intend to approximate their aggregated density , where . Notice that for any , . Let , i.e., is an upper bound on all posterior densities formed by a subset of . Also define . These quantities depend only on the model and the observed data (not posterior samples). We denote and by as the following results apply similarly to both methods.

The “one-stage” aggregation (Algorithm 2) first obtains an approximation for each (via either ML-partition or KD-partition) and then computes .

Theorem 3 (One-stage aggregation).

The approximation error of Algorithm 2 increases dramatically with the number of subsets. To ameliorate this, we introduce the pairwise aggregation strategy in Section 2, for which we have the following result.

Theorem 4 (Pairwise aggregation).

Denote the average total variation distance between and by . Assume the conditions in Theorem 3. Then with high probability the total variation distance between and is bounded by

where is a constant that does not depend on posterior samples.

4 Experiments

In this section, we evaluate the empirical performance of PART and compare the two algorithms PART-KD and PART-ML to the following posterior aggregation algorithms.

-

1.

Simple averaging (average): each aggregated sample is an arithmetic average of samples coming from subsets.

-

2.

Weighted averaging (weighted): also called Consensus Monte Carlo algorithm [3], where each aggregated sample is a weighted average of samples. The weights are optimally chosen for a Gaussian posterior.

-

3.

Weierstrass rejection sampler (Weierstrass): subset posterior samples are passed through a rejection sampler based on the Weierstrass transform to produce the aggregated samples [7]. We use its R package111https://github.com/wwrechard/weierstrass for experiments.

-

4.

Parametric density product (parametric): aggregated samples are drawn from a multivariate Gaussian, which is a product of Laplacian approximations to subset posteriors [6].

-

5.

Nonparametric density product (nonparametric): aggregated posterior is approximated by a product of kernel density estimates of subset posteriors [6]. Samples are drawn with an independent Metropolis sampler.

- 6.

All experiments except the two toy examples use adaptive MCMC [15, 16] 222http://helios.fmi.fi/~lainema/mcmc/ for posterior sampling. For PART-KD/ML, one-stage aggregation (Algorithm 2) is used only for the toy examples (results from pairwise aggregation are provided in the supplement). For other experiments, pairwise aggregation is used, which draws 50,000 samples for intermediate stages and halves after each stage to refine the resolution (The value of listed below is for the final stage). The random ensemble of PART consists of 40 trees.

4.1 Two Toy Examples

The two toy examples highlight the performance of our methods in terms of (i) recovering multiple modes and (ii) correctly locating posterior mass when subset posteriors are heterogeneous. The PART-KD/PART-ML results are obtained from Algorithm 2 without local Gaussian smoothing.

Bimodal Example

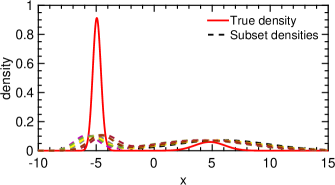

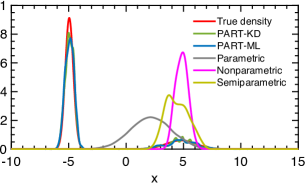

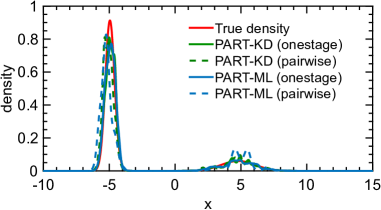

Figure 8 shows an example consisting of subsets. Each subset consists of 10,000 samples drawn from a mixture of two univariate normals , with the means and standard deviations slightly different across subsets, given by , and , , where , independently for and . The resulting true combined posterior (red solid) consists of two modes with different scales. In Figure 8, the left panel shows the subset posteriors (dashed) and the true posterior; the right panel compares the results with various methods to the truth. A few are omitted in the graph: average and weighted average overlap with parametric, and Weierstrass overlaps with PART-KD/PART-ML.

Rare Bernoulli Example

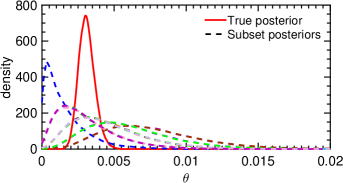

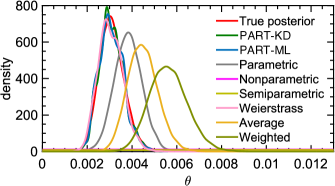

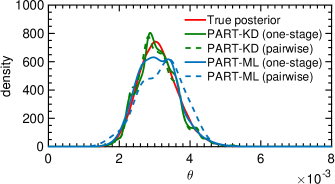

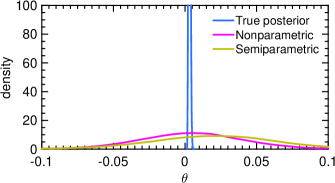

We consider Bernoulli trials split into subsets. The parameter is chosen to be so that on average each subset only contains 2 successes. By random partitioning, the subset posteriors are rather heterogeneous as plotted in dashed lines in the left panel of Figure 9. The prior is set as . The right panel of Figure 9 compares the results of various methods. PART-KD, PART-ML and Weierstrass capture the true posterior shape, while parametric, average and weighted average are all biased. The nonparametric and semiparametric methods produce flat densities near zero (not visible in Figure 9 due to the scale).

4.2 Bayesian Logistic Regression

Synthetic dataset

The dataset consists of observations in dimensions. All features are drawn from with and . The model intercept is set to and the other coefficient ’s are drawn randomly from . Conditional on , follows . The dataset is randomly split into subsets. For both full chain and subset chains, we run adaptive MCMC for 200,000 iterations after 100,000 burn-in. Thinning by 4 results in samples.

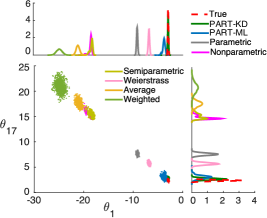

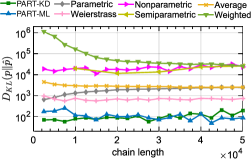

The samples from the full chain (denoted as ) are treated as the ground truth. To compare the accuracy of different methods, we resample points from each aggregated posterior and then compare them using the following metrics: (1) RMSE of posterior mean (2) approximate KL divergence and , where and are both approximated by multivariate Gaussians (3) the posterior concentration ratio, defined as , which measures how posterior spreads out around the true value (with being ideal). The result is provided in Table 4. Figure 6 shows the versus the length of subset chains supplied to the aggregation algorithm. The results of PART are obtained with , and 40 trees. Figure 4 showcases the aggregated posterior for two parameters in terms of joint and marginal distributions.

| Method | RMSE | |||

|---|---|---|---|---|

| PART (KD) | 0.587 | 3.94 | ||

| PART (ML) | 1.399 | 9.17 | ||

| average | 29.93 | 184.62 | ||

| weighted | 38.28 | 236.15 | ||

| Weierstrass | 6.47 | 39.96 | ||

| parametric | 10.07 | 62.13 | ||

| nonparametric | 25.59 | 157.86 | ||

| semiparametric | 25.45 | 156.97 |

Real datasets

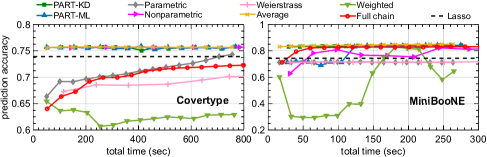

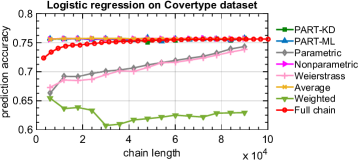

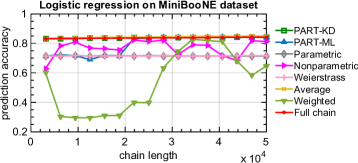

We also run experiments on two real datasets: (1) the Covertype dataset333http://www.csie.ntu.edu.tw/~cjlin/libsvmtools/datasets/binary.html [17] consists of 581,012 observations in 54 dimensions, and the task is to predict the type of forest cover with cartographic measurements; (2) the MiniBooNE dataset444https://archive.ics.uci.edu/ml/machine-learning-databases/00199 [18, 19] consists of 130,065 observations in 50 dimensions, whose task is to distinguish electron neutrinos from muon neutrinos with experimental data. For both datasets, we reserve of the data as the test set. The training set is randomly split into and subsets respectively for covertype and MiniBooNE. Figure 10 shows the prediction accuracy versus total runtime (parallel subset MCMC + aggregation time) for different methods. For each MCMC chain, the first 20% iterations are discarded before aggregation as burn-in. The aggregated chain is required to be of the same length as the subset chains. As a reference, we also plot the result for the full chain and lasso [20] run on the full training set.

[\FBwidth]

[\Xhsize]

5 Conclusion

In this article, we propose a new embarrassingly-parallel MCMC algorithm PART that can efficiently draw posterior samples for large data sets. PART is simple to implement, efficient in subset combining and has theoretical guarantees. Compared to existing EP-MCMC algorithms, PART has substantially improved performance. Possible future directions include (1) exploring other multi-scale density estimators which share similar properties as partition trees but with a better approximation accuracy (2) developing a tuning procedure for choosing good and , which are essential to the performance of PART.

References

- [1] Max Welling and Yee W Teh. Bayesian learning via stochastic gradient langevin dynamics. In Proceedings of the 28th International Conference on Machine Learning (ICML-11), 2011.

- [2] Dougal Maclaurin and Ryan P Adams. Firefly Monte Carlo: Exact MCMC with subsets of data. Proceedings of the conference on Uncertainty in Artificial Intelligence (UAI), 2014.

- [3] Steven L Scott, Alexander W Blocker, Fernando V Bonassi, Hugh A Chipman, Edward I George, and Robert E McCulloch. Bayes and big data: The consensus Monte Carlo algorithm. In EFaBBayes 250 conference, volume 16, 2013.

- [4] Stanislav Minsker, Sanvesh Srivastava, Lizhen Lin, and David Dunson. Scalable and robust bayesian inference via the median posterior. In Proceedings of the 31st International Conference on Machine Learning (ICML-14), 2014.

- [5] Sanvesh Srivastava, Volkan Cevher, Quoc Tran-Dinh, and David B Dunson. WASP: Scalable Bayes via barycenters of subset posteriors. In Proceedings of the 18th International Conference on Artificial Intelligence and Statistics (AISTATS), volume 38, 2015.

- [6] Willie Neiswanger, Chong Wang, and Eric Xing. Asymptotically exact, embarrassingly parallel MCMC. arXiv preprint arXiv:1311.4780, 2013.

- [7] Xiangyu Wang and David B Dunson. Parallel MCMC via Weierstrass sampler. arXiv preprint arXiv:1312.4605, 2013.

- [8] Linxi Liu and Wing Hung Wong. Multivariate density estimation based on adaptive partitioning: Convergence rate, variable selection and spatial adaptation. arXiv preprint arXiv:1401.2597, 2014.

- [9] Manuel Blum, Robert W Floyd, Vaughan Pratt, Ronald L Rivest, and Robert E Tarjan. Time bounds for selection. Journal of Computer and System Sciences, 7(4):448–461, 1973.

- [10] Jon Louis Bentley. Multidimensional binary search trees used for associative searching. Communications of the ACM, 18(9):509–517, 1975.

- [11] Leo Breiman. Random forests. Machine Learning, 45(1):5–32, 2001.

- [12] Leo Breiman. Bagging predictors. Machine Learning, 24(2):123–140, 1996.

- [13] Xiaotong Shen and Wing Hung Wong. Convergence rate of sieve estimates. The Annals of Statistics, pages 580–615, 1994.

- [14] Nils Lid Hjort and Ingrid K Glad. Nonparametric density estimation with a parametric start. The Annals of Statistics, pages 882–904, 1995.

- [15] Heikki Haario, Marko Laine, Antonietta Mira, and Eero Saksman. DRAM: efficient adaptive MCMC. Statistics and Computing, 16(4):339–354, 2006.

- [16] Heikki Haario, Eero Saksman, and Johanna Tamminen. An adaptive Metropolis algorithm. Bernoulli, pages 223–242, 2001.

- [17] Jock A Blackard and Denis J Dean. Comparative accuracies of neural networks and discriminant analysis in predicting forest cover types from cartographic variables. In Proc. Second Southern Forestry GIS Conf, pages 189–199, 1998.

- [18] Byron P Roe, Hai-Jun Yang, Ji Zhu, Yong Liu, Ion Stancu, and Gordon McGregor. Boosted decision trees as an alternative to artificial neural networks for particle identification. Nuclear Instruments and Methods in Physics Research Section A: Accelerators, Spectrometers, Detectors and Associated Equipment, 543(2):577–584, 2005.

- [19] M. Lichman. UCI machine learning repository, 2013.

- [20] Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society. Series B (Methodological), pages 267–288, 1996.

Supplementary Materials

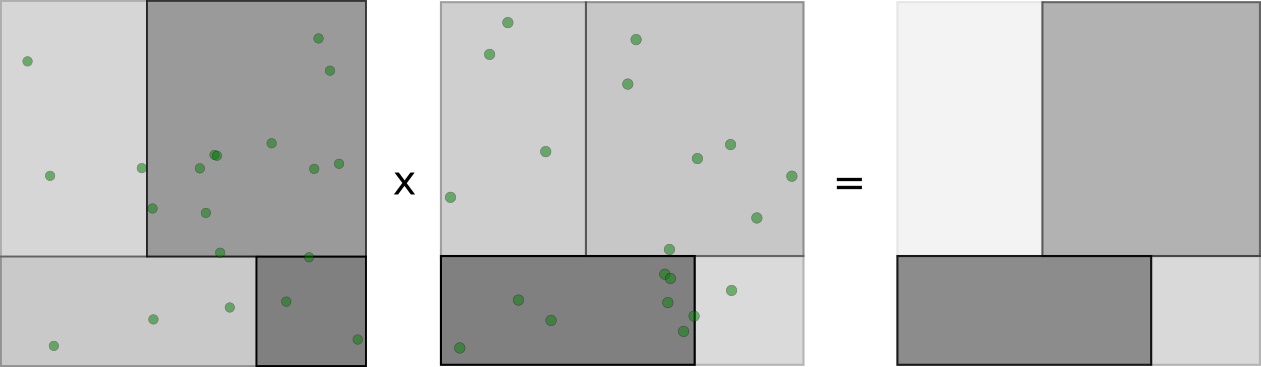

Appendix A: Schematic illustration of the algorithm

Here we include a schematic illustration of the density aggregation in PART algorithm.

Appendix B: Proof of Theorem 1

Let be a subset of defined as . We prove a more general form of Theorem 1 here.

Theorem 5.

For any , if the sample size satisfies that , then with probability at least , the optimal solution to (8) satisfies that

where .

Now choosing , the condition becomes , then with probability at least we have

where with and .

When multiple densities are presented, our goal of imposing the same partition on all functions requires solving a different problem (9). As long as remains true, where , the whole proof of Theorem 1 is also valid for (9). Therefore, we have the following Corollary.

Corollary 1 ( copies).

For any , if the sample size satisfies that and , then with probability at least , the optimal solution to (9) satisfies that

To prove Theorem 1 we need the following lemmas.

Lemma 1.

The optimal solution of (8) is also the optimal solution of the following problem,

| (10) |

Proof.

We write out the empirical log likelihood

For any fixed partition , under the constraint that , one can easily see that

maximizes the result. ∎

Next, we show that the optimal approximation

is a feasible solution to (10) with a high probability.

Lemma 2.

Let be the optimal approximation in , then satisfies that . In addition, with probability at least , we have , i.e., is a feasible soluton of (10).

Proof.

Let be the counts of data points on the partition of . Notice is a fixed function that does not depend on the data. Therefore, each follows a binomial distribution. Define . According to the definition of , we have . Using the Chernoff’s inequality, we have for any ,

Taking and union bounds we have

On the other hand, the following inequality shows the bound on ,

∎

Lemma 2 states that with a high probability we have . This result will be used to prove our main theorem.

Although the actual partition algorithm selects the dimension for partitioning completely at random for each iteration, in the proof we will assume one predetermined order of partition (such as ) just for simplicity. The order of partitioning does not matter as long as every dimension receives sufficient number of partitions. When the selection is randomly taken, with high probability (increasing exponentially with ), the number of partitions in each dimension will concentrate around the average. Thus, it suffices to prove the result for the simple case.

Proof of Theorem 1.

The proof consists of two parts, namely (1) bounding the excess loss compared to the optimal approximation in and (2) bounding the error between the optimal approximation and the true density.

For the first part, using the fact that , the excess loss can be expressed as

Assuming the partitions for and are and respectively, we have

| (11) |

Following a similar argument as Lemma 1, for we can prove that , thus we have for any . Similarly for we have . Therefore, the first term in (11) can be bounded as

The second term in (11) is the concentration of the empirical measure over all possible K-rectangular partitions. Using the result from [chen1987almost], we have the following large deviation inequality. For any , we have

| (12) |

if . For any , taking , we have that

with probability at least . Define . When , Lemma 2 holds with probability at least . Taking the union bound, we have

| (13) |

holds with probability greater than .

To prove the second part, we construct one reference density that gives the error specified in the theorem. According to the argument provided in the paragraph prior to this proof, we assume the dimension that we cut at each iteration follows an order . We then construct in the following way. At iteration , we check the probability on the whole region.

-

i

If the probability is greater than , we then cut at the midpoint of the selected dimension. If the resulting two blocks and satisfy that and , we continue to the next iteration. However, if any of them fails to satisfy the condition, we find the minimum-deviated cut that satisfies the probability requirement.

-

ii

If the probability on the whole region is less than , we stop cutting on this region and move to the next region for the current iteration.

It is easy to show that as long as , the above procedure is able to yield a -block partition before termination. Finally, the reference density is defined as

| (14) |

The construction procedure ensures the following property for . Assuming for some , then each must fall into either of the following two categories (could be both),

-

1.

,

-

2.

and the longest edge of cube must be less than .

We use and to denote the two different collections of sets. Now for any , let . We divide the KL-divergence between and into three regions and bound them accordingly.

We first look at . Because is a block-valued function, must be the union of all the that satisfies . Therefore, we have

Therefore, we have

Because , we have

Next, we look at . It is clear that

and hence we have

Now for , we first use the inequality that for any ,

Using the mean value theorem for integration, we have for some . Also because , is bounded, i.e., there exists some constant such that . Therefore, we have

and thus

Putting all pieces together we have

Now taking and , we have

Now defining and and combining with (13), we have

∎

Appendix C: Proof of Theorem 2

The KD-tree always cuts at the empirical median for different dimensions, aiming to approximate the true density by equal probability partitioning. For we have the following result.

Theorem 6.

For any , define . For any , if , then with probability at least , we have

If the function is further lower bounded by some constant , we can then obtain an upper bound on the KL-divergence. Define and we have

When there are multiple functions and the median partition is performed on pooled data, the partition might not happen at the empirical median on each subset. However, as long as the partition quantiles are upper and lower bounded by and for some , we can establish similar theory as Theorem 2.

Corollary 2.

Assume we instead partition at different quantiles that are upper and lower bounded by and for some . Define and . For any , if , then with probability at least we have

and if the function is lower bounded by , then we have

Following the same argument for Theorem 1, we will prove Theorem 2 by assuming a predetermined order of partition (such as ) for simplicity, though in the actual precedure, the dimensions are selected completely at random. We need the following two lemmas to prove Theorem 2. Let have the same partition as but with function value replaced by the true probability on each region divided by the area, i.e., .

Lemma 3.

With defined above, for any , if , then with probability at least , we have

and

If we instead partition at some different quantiles, which are upper bounded by and lower bounded by for some , then for any , if , with probability at least we have

and

Proof.

The proof is based on how close the data median is to the true median. Suppose there are points in the current region, condition on this region, and partition it into two regions and by cutting at the data median point . Denote the true median by and two anchor points , such that and for some . By Chernoff’s inequality we have

and

The above two inequalities indicate that with high probability is within the interval . Therefore, the probabilities on and also satisfy that

| (15) |

Now consider the regions of and . Each partition will bring an error of at most to the estimation of the region probability. Therefore, assuming we have for each region ( is a random variable) that

if , or

if . Notice that for all iterations before the current partition, we always have . Therefore the probability is guaranteed to be greater than . The above result indicates that

where . So if , then and we have

| (16) |

This result implies that the total variation distance satisfies that

Similarly, one can also prove that

Denote by and by . The KL-divergence can then be computed as

as long as , with probability at least . Consequently, for any , if , then with probability at least , we have

and

When the partition occurs at a different quantile, which is assumed to be for iteration , we have

where if takes the region containing smaller data values and if takes the other half. First, (15) can be updated as

| (17) |

if . Then we can bound the difference between and as

where . Thus if , then we have

and

The total variation distance follows

and the KL-divergence follows

if . Consequently, for any , if , then with probability at least , we have

and

∎

Our next result is to bound the distance between and the true density . Again, the proof depends on the control of the smallest value of and the longest edge of every block. One issue now is that each partition might not happen at the midpoint, but it should not deviate from the midpoint too much given the bound on the , i.e., we have the following proposition.

Proposition 1.

Assume we aim to partition an edge of length (on dimension ) of a rectangular region , which has a probability of and an area of . We distinguish the resulting two regions as the left and the right region and the corresponding edges (on dimension ) as and (i.e., ). Suppose the partition ensures that the left region has probability of , where . If , then the longer edge satisfies that

Proof.

It suffices to bound as . Let , where represents the variable of dimension and stands for the other dimensions. We then have , and

Therefore, using the mean value theorem for the integration, we know that

which implies that

Now if we solve the following inequality

with some simple algebra we can get

Plug in the corresponding value, we have

∎

With Proposition 1, we can now obtain the upper bound for and .

Lemma 4.

For any , define . If for any , then with probability at least , we have

If the is further lower bounded by some , the KL-divergence can be bounded as

where .

Now suppose we instead partition at different quantiles, upper and lower bounded by and for some . For any , if then the above two bounds hold with different and as

Proof.

The proof for the total variation distance follows similarly as Theorem 1. For any , we consider . We then partition the total variation distance formula into two parts

It is straightforward to bound . is a union of ’s which satisfies . Therefore,

Now for , the usual analysis shows that our result depends on the longest edge of each block, i.e.,

where is the longest edge of each block contained in . Now using Proposition 1, we know for iteration the partitioned edge at each block follows

When , each dimension receives stages of partitioning; therefore, we have for each block, the longest edge satisfies that

where . This implies

Now, according to (15), we know with probability at least ,

Taking , we get

with probability at least . So if , then the probability is at least . For the case when , we choose , then

with probability at least if .

For KL-divergence, if is lower bounded by some constant , then we know that

Because and are both lower bounded by , we can follow the proof for with and ignore . Thus we have

where . Similarly, if we take and , then with probability at least , we have

If we take and , then with probability at least , we have

∎

Proof of Theorem 2 and Corollary 2.

For any , define and as in Lemma 4. Thus, for any , if , then with probability we have

and

Also, with probability we have

and

Putting the two equations together we have

and

Using the same argument on random quantiles, if , then with probability at least we have

and

where and are defined as

∎

Appendix E: Proof of Theorem 3 and 4

Proof.

Assume . We want to bound and . Define

which clearly satisfies . Notice that if there exists some such that

where and , then we have

Now if we can pick , then the upper bound becomes . We deduce the corresponding condition for ML-cut and KD-cut respectively. For maximum likelihood partition, plug in into (12). Under the condition of Theorem 1, if

then with probability at least , we have

For median partition, choose and apply (16). Under the condition of Theorem 2, if

then with probability at least , we have

∎

Proof of Theorem 3.

Assume the average total variation distance between and is . It can be calculated directly as

Letting , we have

Thus

∎

Proof of Theorem 4.

Assuming , then after iterations, we will obtain our final aggregated density. At iteration , each true density is some aggregation of the original densities, which can be represented by , where is the set of indices of the original densities. Let be the total variation distance between the true density and the approximation for the pair caused by combining. For example, when , contain only a single element, i.e., and . Recall that , using the result from Theorem 3, we have

We prove the result by induction. Assuming we are currently at iteration , and the paired two densities are and where . By induction, the approximation obtained at iteration are and which satisfies that

Using Theorem 3 again, we have that

Consequently, the final approximation satisfies that

∎

Appendix D: Supplement to Two Toy Examples

Bimodal Example

Figure 8 compares the aggregated density of PART-KD/PART-ML for several alternative combination schemes to the true density. This complements the results from one-stage combination with uniform block-wise distribution presented in Figure 1 of the main text.

Rare Bernoulli Example

The left panel of Figure 9 shows additional results of posteriors aggregated from PART-KD/PART-ML random tree ensemble with several alternative combination strategies, which complement the results presented in Figure 2 of the main text. All of the produced posteriors correctly locate the posterior mass despite the heterogeneity of subset posteriors. The fake “ripples” produced by pairwise ML aggregation are caused by local Gaussian smoothing.

Also, the right panel of Figure 9 shows that the posteriors produced by nonparametric and semiparametric methods miss the right scale.

Appendix F: Supplement to Bayesian Logistic Regression

Figure 10 additionally plots the prediction accuracy against the length of subset chains supplied to the aggregation algorithms, for Bayesian logistic regression on two real datasets. For simplicity, the same number of posterior samples from all subset chains are aggregated, with the first 20% discarded as burn-in. As a reference, we also show the result for running the full chain. As can be seen from Figure 10, the performance of PART-KD/ML agrees with that of the full chain as the number of posterior samples increase, validating the theoretical results presented in Theorem 1 and Theorem 2 in the main text.

References

- [1] Max Welling and Yee W Teh. Bayesian learning via stochastic gradient langevin dynamics. In Proceedings of the 28th International Conference on Machine Learning (ICML-11), 2011.

- [2] Dougal Maclaurin and Ryan P Adams. Firefly Monte Carlo: Exact MCMC with subsets of data. Proceedings of the conference on Uncertainty in Artificial Intelligence (UAI), 2014.

- [3] Steven L Scott, Alexander W Blocker, Fernando V Bonassi, Hugh A Chipman, Edward I George, and Robert E McCulloch. Bayes and big data: The consensus Monte Carlo algorithm. In EFaBBayes 250 conference, volume 16, 2013.

- [4] Stanislav Minsker, Sanvesh Srivastava, Lizhen Lin, and David Dunson. Scalable and robust bayesian inference via the median posterior. In Proceedings of the 31st International Conference on Machine Learning (ICML-14), 2014.

- [5] Sanvesh Srivastava, Volkan Cevher, Quoc Tran-Dinh, and David B Dunson. WASP: Scalable Bayes via barycenters of subset posteriors. In Proceedings of the 18th International Conference on Artificial Intelligence and Statistics (AISTATS), volume 38, 2015.

- [6] Willie Neiswanger, Chong Wang, and Eric Xing. Asymptotically exact, embarrassingly parallel MCMC. arXiv preprint arXiv:1311.4780, 2013.

- [7] Xiangyu Wang and David B Dunson. Parallel MCMC via Weierstrass sampler. arXiv preprint arXiv:1312.4605, 2013.

- [8] Linxi Liu and Wing Hung Wong. Multivariate density estimation based on adaptive partitioning: Convergence rate, variable selection and spatial adaptation. arXiv preprint arXiv:1401.2597, 2014.

- [9] Manuel Blum, Robert W Floyd, Vaughan Pratt, Ronald L Rivest, and Robert E Tarjan. Time bounds for selection. Journal of Computer and System Sciences, 7(4):448–461, 1973.

- [10] Jon Louis Bentley. Multidimensional binary search trees used for associative searching. Communications of the ACM, 18(9):509–517, 1975.

- [11] Leo Breiman. Random forests. Machine Learning, 45(1):5–32, 2001.

- [12] Leo Breiman. Bagging predictors. Machine Learning, 24(2):123–140, 1996.

- [13] Xiaotong Shen and Wing Hung Wong. Convergence rate of sieve estimates. The Annals of Statistics, pages 580–615, 1994.

- [14] Nils Lid Hjort and Ingrid K Glad. Nonparametric density estimation with a parametric start. The Annals of Statistics, pages 882–904, 1995.

- [15] Heikki Haario, Marko Laine, Antonietta Mira, and Eero Saksman. DRAM: efficient adaptive MCMC. Statistics and Computing, 16(4):339–354, 2006.

- [16] Heikki Haario, Eero Saksman, and Johanna Tamminen. An adaptive Metropolis algorithm. Bernoulli, pages 223–242, 2001.

- [17] Jock A Blackard and Denis J Dean. Comparative accuracies of neural networks and discriminant analysis in predicting forest cover types from cartographic variables. In Proc. Second Southern Forestry GIS Conf, pages 189–199, 1998.

- [18] Byron P Roe, Hai-Jun Yang, Ji Zhu, Yong Liu, Ion Stancu, and Gordon McGregor. Boosted decision trees as an alternative to artificial neural networks for particle identification. Nuclear Instruments and Methods in Physics Research Section A: Accelerators, Spectrometers, Detectors and Associated Equipment, 543(2):577–584, 2005.

- [19] M. Lichman. UCI machine learning repository, 2013.

- [20] Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society. Series B (Methodological), pages 267–288, 1996.