Branching Brownian motion with absorption and the all-time minimum of branching Brownian motion with drift

Abstract

We study a dyadic branching Brownian motion on the real line with absorption at 0, drift and started from a single particle at position When is large enough so that the process has a positive probability of survival, we consider the number of individuals absorbed at 0 by time and for the functions We show that if and only of for some and we study the properties of these functions. Furthermore, for is the cumulative distribution function of the all time minimum of the branching Brownian motion with drift started at 0 without absorption.

We give three descriptions of the family through a single pair of functions, as the two extremal solutions of the Kolmogorov-Petrovskii-Piskunov (KPP) traveling wave equation on the half-line, through a martingale representation and as an explicit series expansion. We also obtain a precise result concerning the tail behavior of . In addition, in the regime where almost surely, we show that suitably centered converges to the KPP critical travelling wave on the whole real line.

1 Introduction

Consider a branching Brownian motion in which particles move according to a Brownian motion with drift and split into two particles at rate independently one from another. Call the population of all particles at time and call the position of a given particle . When we start with a single particle at position we write for the law of this process.

In a seminal paper, [13], Kesten considered the branching Brownian motion with absorption, i.e. the model just described with the additional property that particles entering the negative half-line are immediately absorbed and removed. We write for the set of particles alive (not absorbed) in the branching Brownian motion with absorption and the number of particles that have been absorbed up to time . The system with absorption is said to become extinct if and to survive otherwise. We let .

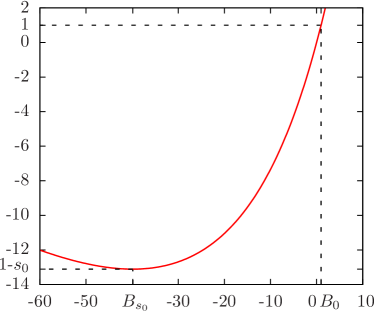

Depending on the value of one has the following behaviours (see Figure 1)

-

Regime A:

if , the drift towards origin is so large that the system goes extinct almost surely. is finite and non-zero.

-

Regime B:

if there is a non-zero probability of survival. On survival, there will always be particles near 0 and almost surely.

-

Regime C:

if there is still a non-zero probability of survival, but the system is drifting so fast away from 0 that, on survival, drifts to almost surely as ; is thus almost surely finite. Furthermore, there is a non-zero probability that .

The behaviour of in regime () has been the subject of very active research recently, including a conjecture by Aldous which was recently settled by P. Maillard [15] (we discuss Maillard’s results bellow), improving earlier results of L. Addario-Berry and N. Broutin [1] and E. Aïdékon [2]. Surprisingly, relatively little was known concerning the regimes B and C. Our main results in the present work concern the study of and of certain related KPP-type equations.

1.1 The tail behaviour of

In [15], Pascal Maillard has shown that in regime A () the variable has a very fat tail. More precisely he shows that, as , there exists two constants which depend on such that

In regime B () it is clear that on survival so one would essntially condition on extinction to study the tail behaviour of . This is outside the scope of the present work.

In regime C (), however, is almost surely finite. We introduce for and ,

| (1) |

When this quantity is the generating function of . We show that is finite for some values of larger than 1:

Theorem 1.

In regime C (), there exists a finite depending only on such that

-

1.

For , is finite for all ,

-

2.

For , is infinite for all .

The functions are increasing for any and decreasing for any , converging to 1 when , and one has .

Furthermore, one has for large

| (2) |

Using the branching structure and a simple coupling allows to relate the with each others, as in the following result (which is already present in [17, 15]):

Theorem 2.

In regime C (),

-

1.

For each , ,

-

2.

For each ,

We do not have an explicit expression for as a function of , but we can evaluate it numerically with a good precision as shown in Figure 2. In the critical case , we obtain .

We can prove the following property:

Proposition 3.

is an increasing function of and furthermore for some constant as .

1.2 Distribution of the all-time minimum in a branching Brownian motion

The probability that for a system started from , is also the probability that the all-time minimum of a full branching Brownian motion with drift started from zero does not go below :

| (3) |

This quantity, of course, is not trivial only in regime C (). Then, since

almost surely, we see that there is a well defined all-time minimum for the branching Bownian motion and we conclude that

It is not hard to see by standard arguments that must satisfy a KPP-type differential equation with boundary conditions:

| (4) |

In fact, introduced in (1), if finte, is solution to the same equation with the boundary condition replaced by :

| (5) |

This is an example of the deep connection between branching Brownian motion and the KPP equation which goes back to McKean [16] who noticed that one can represent solutions of the KPP equation as expectations of functionals of branching Brownian motions.

Until now this is very classical, however there is one unexpected difficulty here: both (4) and (5) admit infinitely many solutions and are not sufficient to characterize . Figure 3 gives several numerical solutions to (4).

In this work , we present three largely independent ways to characterize which are laid out in the three following subsections. The first approach relies on partial differential equations, the second gives as the expectation of a certain martingale and the third one gives as a power series.

One salient property of is that it converges to 1 rather quickly:

Proposition 4.

There exists such that

| (6) |

Furthermore, is the only solution of (4) which remains in and converges that fast to 1.

Similarly, for any , there exists such that

| (7) |

where when and when .

This fast decay was actually an unexpected result for reasons explained in Section 1.2.4.

To simplify notation, we call the exponential decay rate of as given in (6):

| (8) |

It is the largest solution of .

1.2.1 from partial differential equations

A first way to characterize is to track the probability that no particle got absorbed up to time . Define

| (9) |

The function is increasing in and decreasing in and, clearly, for each , as . Furthermore, satisfies the KPP equation with boundary conditions

| (10) |

which, by Cauchy’s Theorem has only one solution.

Therefore, to obtain , one can in principle solve (10) and take the large time limit. This route leads to the following Theorem:

1.2.2 Martingale representation for

There is an explicit probabilistic representation of the maximum standing wave in regime C (). Recall that is the population of all the particles in the branching Brownian motion with no absorption and is the population of particles alive at time when we kill at 0. We now define on the same probability space a third process based on the branching Brownian motion in which particles that hit 0 are stopped but not removed from the system (they neither move nor branch). We denote by the set of particles alive at time in this model. With a slight abuse of notations we continue to write for the positions of particles when

Let us define the following two processes:

| (11) |

where is the asymptotic decay of as given in (8). Rewriting it is clear that is simply a standard branching Brownian motion with no drift. Therefore is the usual exponential martingale with parameter associated with the branching Brownian motion The process is the martingale stopped on the line (i.e. particles are stopped at time or when they hit 0 for the first time). It is therefore also a martingale.

Lemma 6.

In regime C () the martingale converges almost surely and in to and therefore

Following the probability tilting method pioneered by [14] and [8] we introduce a new probability measure

Note that since is a closed martingale we have that Thus

Under this tilted probability measure, the law of the process is the same as the original law except for the movement and branching rate of a distinguished particle (the spine particle ). The spine moves according to a Brownian motion with drift , branches at an accelerated rate of and stops (i.e. sticks and stops reproducing) upon hitting 0.

Theorem 7.

In regime C (),

Furthermore, converges to a finite constant when and thus, as ,

More generally, for any , one has

and the expectation converges to a finite positive constant as .

We will see in the proof that we can give an explicit representation of the constant which appears in Proposition 4 as the expectation of under the measure (similar to but with the spine particle “started at infinity”).

1.2.3 as a series expansion

The function can be understood in terms of series expansion. Let be the sequence defined by

| (12) |

(recall that was defined in (8), that and that ) and the function defined by the series

| (13) |

We have

Proposition 8.

The radius of convergence of is non-zero and there exists such that

More generally, for any , there exists a number such that

| (14) |

is decreasing, positive for , zero for , and negative for . In particular, for , the condition is automatically fulfilled.

The proof is contained in Section 2.2.4. Numerically, it seems that is large enough that for all and all , but we haven’t proved that point. The representation (14) makes it very easy to compute numerically by first computing , see Figure 4; the value is then obtained as 1 minus the first minimum of for negative arguments. This follows easily from the facts that and that for all .

,

1.2.4 About the asymptotic decay (6)

The KPP partial differential equation,

| (15) |

where , and , describes how a stable phase ( on the left) invades an unstable phase ( on the right). It is well known that it admits travelling wave solutions of the form

for any velocity greater or equal to . The travelling wave is then solution to

| (16) |

The solution to (16) is unique up to translation.

Equation (16) for is very similar to equation (4) for , but , surprisingly, does not have the same asymptotic behaviour as for large , in the region where and are close to 1. Indeed, linearising (16) around 1, one gets

| (17) |

(a term of order has been neglected) and the general solution to (17) is, for some constants and ,

| (18) |

For large, is close to with the meaning that for some constant and , (see the discussion in Section 2.2.3). Of course, if , the term in factor of is negligible compared to the term in factor of and the term alone is an equivalent to . When solving (16), it turns out that the solution has a non-zero term and that, therefore,

| (19) |

where depends on .

We now consider equation (4) for . Of course, the boundary condition of (4) is not sufficient to determine a unique solution, and for a range of values of there exists a solution to

| (20) |

(The difference with equation (4) for is the added condition . Figure 3 shows several solutions.)

One can then do, as above, a large analysis of and, the partial differential equation being the same, one finds again that ( large) as given in (18) for some and dependent values of and . Generically, is non-zero and decays as in (19) (up to a multiplicative constant; the is usually different and can even be negative, see Figure 3).

However, for a well chosen value of (depending on ), one has , and the asymptotic decay of is given by the term (that is: it decays much faster). The meaning of Proposition 4 is that is precisely that very special solution to (4) that decays unlike all the other ones and unlike the travelling wave .

It is also interesting to remark that an equation very similar to (4) appears in the study [11, 6] of the the extinction probability of a branching Brownian motion with absorption and supercritical drift (regimes B and C): let be the extinction probability when the system is started from ; then one has

| (21) |

Equations (4) and (21) differ only by their boundary conditions; however (21) has a unique solution, whereas (4) has many.

A possible way to understand the difference is that an asymptotic analysis of for large similar to (18) yields only one possible exponential decay: for some constant , which means that, up to translations, there is only one solution which does converge to zero at infinity, whereas for there were two possible exponential decays and infinitely many solutions. Otherwise said, if one were to impose and , there would only be one value of for which would converge to zero at infinity.

1.3 A travelling wave result

In regimes A and B () one has because almost surely, which is not very interesting. What is more interesting is the way that , defined in (9) as , converges to zero: it does so by assuming the shape of the critical travelling wave of the KPP equation. Let us recall quickly the well known facts on this critical travelling wave.

Consider the KPP equation (15) without drift on the whole line with Heaviside initial conditions:

| (22) |

It is well known that is the probability that the leftmost particle at time of a branching Brownian motion started at is to the right of zero. Furthermore, this probability converges to the critical travelling wave in the following sense:

with

| (23) |

and where is the travelling wave moving at the minimal possible velocity , see (16). To fix the invariance by translation, we impose the further condition :

| (24) |

and the solution to (24) is now unique.

Adding a drift to (22) would only shift the solutions by and would make (22) very similar to (10): the only difference would be that is defined on and on , but as both equations converge quickly to zero around the origin in regimes A and B , this difference turns out to be minimal and one has

Theorem 9.

It is interesting to compare this result about the behaviour of when to the behaviour of the extinction probability when It is not hard to see that satisfies the same equation (10) as with different boundary conditions, which is minus the boundary condition in (10); namely solves

| (25) |

What is particularly striking is that in the critical case it is known since Kesten [13] (see also [5]) that to survive up to time one must start with an initial particle at position . This means that if converges to some limit front shape then the centering term giving the position of the front has to be of order . However the convergence of the solution of (25) to a travelling wave is at present an open problem.

2 Proofs

The proofs section are presented mostly in the same order as the results: Section 2.1 contains the proofs to Theorems 1 and 2 about the structure of the functions in regime C (). Section 2.2 contains the proofs to Proposition 4, Theorem 5, Lemma 6, Theorem 7 and Proposition 8 about the different representations of in regime C (). Finally, Section 2.3 contains the proof of Theorem 9 about the establishment of a travelling for in regimes A and B () and the asymptotic behavior of established in Proposition 3 is proven last.

2.1 Proof concerning the tail behaviour of

In this section we consider exclusively regime C () and we focus on the problem of the exponential moments of . We first establish some properties of as defined in (1) and proceed to prove Theorems 2 and Proposition 3. We then prove the asymptotic behaviour (LABEL:asymptNhits) to complete the proof of Theorem 1.

The first property we need is that for a given , the quantity is either finite for all or infinite for all :

Lemma 10.

For a given ,

Proof.

Fix , and . There is a positive probability, which we note , that the initial particle starting from reaches position before any branching or killing happens. Then

Therefore, if is finite, then is also finite. ∎

Remark: in the following, we write when the conditions of the lemma are met. Clearly, this is the case when . Furthermore, as is obviously increasing, if for some , then for all .

When , it is clear by standard arguments that is solution to

| (26) |

Let us now prove Theorem 2. A slightly more general result is given by the following Lemma:

Lemma 11.

If then, for any and ,

Setting and renaming as gives the first line of the Theorem. Once we have proved that exists, setting and renaming as gives the second line of the Theorem.

Proof.

Instead of starting our branching process at position and killing particles at , it is here more convenient to think of the process as started at 0 and particles being absorbed at . This allows to couple different values of the killing position. In particular, if designates the particles stopped when they first hit and is the number of particles in , we have that

where is the total number of descendent of the particle which are killed at (which by translation invariance of the branching Brownian motion and the branching property is an independent copy of ). ∎

We now have a monotonicity result:

Lemma 12.

-

1.

If , is an increasing function converging to 1.

-

2.

If and , is a decreasing function converging to 1.

Proof.

Once the increasing/decreasing part is proved, the fact that the limit is 1 is obvious: from its definition, it is clear that if and if . Assuming is increasing or decreasing (depending on ), it must have a limit, and from (26) that limit must be 1.

From its interpretation as the distribution of the all-time minimum of a branching Brownian motion, see (3), it is furthermore clear that is an increasing function. Then, the coupling provided by Lemma 11 (or more simply Theorem 2) implies that is an increasing function for all .

Therefore, it only remains to prove that for , is decreasing when it is finite.

Assume and . We first show that is monotonous by considering two cases:

-

•

If then, for all small enough, . But, for fixed, is a strictly increasing function so . Then by Lemma 11, for all and all small enough: is increasing.

-

•

If then, for all small enough, because in the limit case , one has from (26). Then, as in previous case, for all and all small enough: is decreasing.

It now remains to rule out the possibility that is increasing for . Imagine that and increases. Then, from (26), and , which becomes negative for large enough, in contradiction with the fact that increases. So must decrease for . ∎

We need now to characterize the values of for which .

Lemma 13.

Assume . If there exists a function which solves

| (27) |

then .

Remark: The converse is obvious: when is finite, it is one of the solutions to (27). This Lemma allows to define

| (28) | ||||

and because increases, one has for all .

Proof.

We present two proofs: one probabilistic and one analytical.

Choose such that (27) has a solution . We introduce the process

where we recall that is the set of particles in the branching Brownian motion where particles are frozen at the origin, see Section 1.2.2.

is a positive local martingale and therefore a positive super-martingale which thus converges almost surely to . Observe that under

But since for all one has

we see that and therefore

The same result can be proved analytically through the maximum principle. Let us introduce

| (29) |

which is clearly solution to

| (30) |

(Compare to (9).) With as above, one clearly has , . Therefore, by the maximum principle we have that

and as as we see that . ∎

It is obvious that defined in (28) depends only on the ratio by a simple scaling argument: the branching Brownian motion with drift and branching rate is transformed, when time is scaled by and space by , into a branching Brownian motion with drift and branching rate . In particular, with the obvious new notation. What remains to be shown are the following properties of : is finite, is finite, and .

Lemma 14.

, that is: does not have exponential moments of all orders.

Proof.

For the system started from , consider the following family of events for :

In words, for each there is one particle alive at time , it sits in , and during a time interval one, this particle splits exactly once, one the offspring gets absorbed and the other is again in at time . The one particle alive at time generates a tree drifting to infinity with no more absorbed particles.

Let be the probability that a particle sitting at has, during a time interval one, exactly one splitting event with one offspring being absorbed and the other one ending up in . Define furthermore

is the minimal probability for a particle sitting somewhere in to have, during a time interval one, exactly one splitting event with one offspring being absorbed and the other one ending up in . It is clear that and that, furthermore,

This implies that and that . ∎

Lemma 15.

.

Proof.

If , this is trivial as . Assume now and let us fix . For any , as is decreasing, one has . This implies that (using the monotone convergence Theorem) is finite which entails the result. ∎

Lemma 16.

.

Proof.

The proof that for all is divided into two steps. First, we show that in the critical case . Then we conclude by proving Proposition 3, which states that is an increasing function of .

Lemma 17.

In the critical case , for small enough, there exists solutions to (27), that is .

Proof.

Assume . After the change of variables , (27) reads

| (31) |

Let us consider the solution to (31) with for some . We want to prove that if is small enough. Assume otherwise and call . Then, as , we have and thus on (where ),

We conclude that

which is strictly positive for small enough. This contradicts the definition of and thus we have found a solution of (31) such that for all . Then is a solution to (27) started from ; in other words in the case. ∎

We now proceed to prove that is a strictly increasing function of .

Proof of Proposition 3.

Let us fix . One can easily construct two branching Brownian motions with parameters and on the same probability space to realise a coupling so that the particles of the second one are a subset of the particles of the first one. It is then clear that for any one has

| (32) |

(with the obvious extension of notation) so that

| (33) |

This already gives non-strict monotonicity and concludes the proof that for all , with .

Finally, the only remaining point to complete the proof of Theorem 1 is the asymptotic behaviour (2), i.e. the assertion that for fixed

| (34) |

Write for the open disc of the complex plane with center and radius . We extend the definition of to :

| (35) |

This quantity is analytical on because the in (35) are positive and the first singularity on the real axis is at . Furthermore, it is finite on by uniform convergence because it is finite at .

The arguments we use are extremely close to those used by Maillard in [15]. The key argument, which improves on usual Tauberian theorems, is an application of [9, Corollary VI.1] relying on the analysis of generating functions near their singular points. We need to show that

Lemma 18.

Fix . There exists such that is analytical in and

| (36) |

and that

Lemma 19.

Fix . There exists such that is analytical on .

Then, applying Corollary VI.1 in [9] to , Lemmas 18 and 19 lead to

| (37) |

which obviously implies (34).

Proof of Lemma 18.

We know that and Since solves the KPP traveling wave differential equation, for each we can extend analytically on a neighborhood of zero in (see e.g. [18]). In particular for we have the following expansion:

| (38) |

The function is analytic and zero is a zero of order two of , by Theorem 10.32 of [18] there exists and a function analytic and invertible on such that

| (39) |

This means that

| (40) |

for any in such that (so that the right-hand side is well defined and is analytic on this domain when using the standard definition of the complex square root).

Recall from Lemma 11 that for any non-negative real and one has

| (41) |

Replace the in the right-hand side by its expression (40) and write as to obtain

| (42) |

for for some . But (42) is an equality between analytical functions as long as for some small enough (one must have for to be analytical, which is possible by the open mapping Theorem, and one must have small enough for to be also analytical). From the analytical continuation principle, (42) must hold on the whole domain. Now differentiate with respect to to get

| (43) |

yielding

| (44) |

A straightforward computation shows that which concludes the proof. ∎

Proof of Lemma 19.

is already analytical on . To prove the Lemma it is sufficient to show that it can be analytically extended around any point . Indeed, by the finite covering property of compacts one can then show analycity on a open containing the compact with defined in Lemma 18, and then we conclude with the help of Lemma 18.

So it now remains to see why can be analytically extended to neighboorhoods of any with . This is essentially the content of Lemma 6.2 in [15]. As in Maillard, we define

| (45) |

where we recall that the prime is a derivatice with respect to . We first show analycity of on by writing an integral representation of : multiply (5) by and integrate on . Integrate several times by part to get rid of the derivatives of ; one is left with

| (46) |

For any and one has . This implies that the convergence for close to infinity of the integral in (46) is uniform on the disk . As is analytical on , this is sufficient to ensure that is also analytical on . Furthermore, notice that the series (35) defining converges uniformly on because we know it converges absolutely (all the are non-negative) at . This implies that is continuous on and, from the expression (46), so is (by dominated convergence Theorem since on the closed disc).

We proceed to show that can be extended analytically around any point with and show that the property extends to .

In Lemma 11 we showed for any and any and one had

| (47) |

One can check that the proof of Lemma 11 extends to complex so that (47) remains valid for any such that is finite.

For fixed (complex) , by deriving (47) with respect to and then setting , one gets

| (48) |

Derive again with respect to , and then set :

| (49) |

so that the differential equation (26) on applied at gives

| (50) |

which is equation (3.5) in [15]. This equation is valid for all .

We now use the Fact 5.2 in [15], which we reproduce here with some change of notation for clarity:

Fact 5.2 in [15] Let be a region in and analytic in . Let be a region in such that for each and suppose that there exists an analytic function such that

Let Suppose is continuous at and that . Then is a regular point of i.e. admits an analytic continuation at .

We apply to our case with , and . From (50), the only candidate values of in such that are 0 and 1, and we know that , so the condition “ for each ” is verified. The function is obtained from (50): , and is obviously analytical on ; we have already shown that is continuous on . Therefore, for any point such that (because we want ), the function admits an analytic continuation at . We know that , and we prove now that one has for any , which will conclude the proof that can be analytically continued around any point in . From (35) one can write as a series:

| (51) |

We know that (because and ) and that for , (because and ). Since , we write

| (52) |

All the terms on the left hand side are non-negative and infinitely many of them are non-zero since (50) does not have polynomial solutions. Thus, for any one has

| (53) |

In particular, because it is the sum of two terms (the and the term ) with different moduli and can be extended analytically around .

We now show how the analycity of translates into analycity of . First derive (47) again but this time with respect to , then set , and rename into to obtain

| (54) |

where we used (48) for the second equality.

For each given we consider a neibourhood V of where is analytical and we apply again Fact 5.2 in [15] to prove that is also analytical around . This time, we take and from (54). We pick and . For any one has so that the condition “ for each ” is satisfied. We have already shown that is continuous on , so we conclude that is a regular point of .

∎

2.2 Proofs concerning

In this section we consider exclusively regime C () and prove our results concerning the properties of and .

2.2.1 Proof of Theorem 5

We need to prove that is the maximal solution remaining below 1 of the differential equation (4). This is an elementary application of the maximum principle again. Suppose that is any solution of (4) which stays below 1. Since is a standing wave solution of (10), that is for all is a solution of

and since for all we have that

where is the solution of (10). As for each we know that we conclude that and therefore is the maximal solution of (4) bounded by 1. The same argument is easily generalized to the case of an arbitrary value of .

2.2.2 Proof of the martingale representation, Theorem 7

We start by proving Lemma 6, i.e. that the martingale converges -almost surely and in to and therefore that

Proof of Lemma 6.

Recall that by (11)

| (55) |

are positive martingales which therefore converge -almost surely to their respective limits and . Furthermore, as is the usual additive martingale with parameter , one has . As the bounds

always hold, it is clear that . The only thing left is to show that the convergence also holds in .

We start by recalling the description of the measure which is defined by

Standard arguments (see [10]) allow us to conclude that under the process behaves as follows: for , there is a distinguished line of descent (the spine) denoted . Under the particle moves according to a Brownian motion with drift and therefore almost surely hits 0 in finite time; we call the time at which it reaches 0. For , the spine branches at rate creating non-spine particles which start new independent branching Brownian motion behaving according to the usual law. After , the spine particle is frozen at zero (no motion, no branching). Observe that is actually the projection of the measure just described since under we do not know which is the spine particle

To prove the convergence of towards its limit , it is sufficient to show that

As the time at which the spine is absorbed at 0 is -almost surely finite, there are only finitely many branching events from the spine -almost surely as well. At each of these events, a non-spine particle starts its own independent branching Brownian motion and we call the total number of particles frozen at 0 that are descended from . Let us also call the analogue of the limit (but we sum only on particles descended from ) and is the same as but without any absorption or freezing at 0. It is clear as above that

and that . We conclude that , -almost surely, and finally

Observe that since almost surely under , we have . Thus we know that under in . Hence, ∎

We now move to the proof of Theorem 7.

Lemma 20.

Recall and for as usual. Then

and

Proof.

As -almost surely, it is sufficient to prove the second assertion. Using that -almost surely,

∎

Since we already know from Proposition 4 (its proof is analytical and is independent of the present discussion) that tends to a constant , it is now clear that the expectations in Lemma 20 also converge to as . However, we are now going to define as the law of the process under which we can couple all the together and interpret the limit constant as the expectation of a limit variable under . Loosely speaking, we want to be the law of the process where the spine particle starts at before drifting to 0. In fact it is easier to reverse time and have the spine start at 0 and drift to

We start with the following Lemma:

Lemma 21.

Let be a Brownian motion with drift , started from 0 conditioned to never hit 0. Otherwise said, is solution of the following stochastic differential equation

Let be a Poisson point process on with intensity . For each start a branching Brownian motion with law and call the total number of absorbed particles at 0 for this process.

Fix , then the distribution of the variable under is the same as that of

under where .

This result should be clear once it is realized that the process is the reversed path of the spine .

Proof.

We only treat the case since the zero-drift case is similar. The only thing we need to prove here is that if is a Brownian motion with drift started form and stopped at time , then

This follows for instance from [3].

∎

The upshot of Lemma 21 is that we can now construct the variables under for all values of simultaneously. We write for the joint law of the variables described above. Then under , clearly is an increasing process in . We call its limit which is also the total number of particles absorbed at 0 under

Lemma 22.

We have that -almost surely.

Proof.

We start with the case. First observe that for fixed, there exists almost surely a random such that

This simply comes form the fact that and almost surely. Now, because under we have that almost surely and therefore Hence, for any we have that

for some positive constant . Thus a straightforward application of Borel-Cantelli Lemma shows that almost surely, there exists such that which yields the desired result. The zero-drift case is similar. One just needs to start the argument by observing that for fixed, there exists almost surely a random such that

where is a constant. The proof then follows as before. ∎

The following Lemma completes the proof of Theorem 7.

Lemma 23.

For small enough, we have that

| (56) |

Proof.

The monotone convergence Theorem applies when so we suppose . Observe that the map is decreasing on and increasing on Thus we write

where the first convergence comes from the dominated convergence Theorem and the second from the monotone convergence Theorem.

∎

2.2.3 Proof of Proposition 4

We consider here all the solutions to (4) that remains in . By Cauchy’s theorem, a solution to (4) is entirely determined once the derivative at the origin is given.

Let and be the two roots of the polynomial :

(See also (8).) From the general theory of differential equations, one has

Lemma 24.

Let be a solution to

| (57) |

such that converges to 1 as . Then, for some non-zero constant or ,

-

•

if one has either or as .

-

•

If one has either or as .

Furthermore, up to invariance by translation, there are exactly two solutions which converges to 1 in the fast way (as ); one of them approaching 1 by above and the other from below.

This lemma simply tells that the solutions to the non-linear equation (57) behave around as the solutions to the equation linearised around 1. We already used implicitly this result in Section 1.2.4.

Proof.

This follows from a result of Hartman [12] who shows that if

| (58) |

is a non-linear differential system of dimension 2 with a hyperbolic (eigenvalues have a non-zero real part) matrix and is with as (so 0 is a critical point) , then there exists a diffeomorphism with derivative the identity at the origin such that solves

| (59) |

Otherwise said the solutions of the linearized system and the solutions of the non-linear system are (locally around 0) in one-to-one correspondence through .

We apply this result to the following system where is a solution of (57)

| (60) |

which has a critical point at . In this case

| (61) |

with eigenvalues and (for simplicity we only consider the case here) and corresponding eigenvectors and . The solutions of are of the form

| (62) |

Thus the only solutions such that for some constant are those such that If then approaches by above, if approaches by below. Hartman’s Theorem tells us that there exists

| (63) |

such that the solutions of the non-linear system are locally

| (64) |

Thus, (after a shift in the argument, replacing by ) there is exactly one solution to the non linear system such that has a non degenerate limit and such that , the first coordinate of , is eventually positive (resp. eventually negative). ∎

Let be such that there is a solution of (57) with , , and for all (we now know that such an exists). Then being the maximal solution of (4) that starts from and stays below 1, we must have

Since we also know that the only two possibilities for the asymptotic behavior of are that either or we conclude that it is the former that holds. The same argument apply for for any and in the critical case. This concludes the proof of Proposition 4 for .

2.2.4 Proof of Proposition 8

We consider the series defined in (13) with the coefficients defined in (12). The function is a well defined object because, by induction on (12) one has easily and, therefore, . It is then very easy to check by direct substitution that for any , the function

| (65) |

is solution to the partial differential equation which appears in (4) (when discussing ) and in (26) (when discussing ). Recall that is the larger root of .

As the coefficients are positive, is non-negative and increasing for . As and , it is easy to find a such that . This implies that there must exists a (smaller than ) such that . With , the function in (65) is smaller than 1 and converges to 1 for large as . Using Proposition 4, this implies that .

Recall by Theorem 2 that for is simply equal to correctly shifted to have . This implies that, for , where is such that .

The case is trivial, we now turn to . As for , we have the following points:

- •

- •

Now consider for negative arguments. Because and , there must exists such that is negative on . Then, the function is solution to (26) for , remains above 1 for and converges to 1 as . Therefore, it must be for that particular .

But all the functions for are related through Theorem 2: they are all shifted versions of . Therefore, for any , one has for a well chosen negative (which represents the shift), at least for values of sufficiently large to have .

2.3 Proof of Theorem 9

We assume to be in regime A or B () and we want to show how converges to a KPP travelling wave.

The proof is essentially analytic and relies on Bramson’s result [7] and the maximum principle. The key step is to compare to a new function (where is a parameter) where is defined as the probability, in the standard branching Brownian motion (without absorption nor stopping) with drift starting from , that no particles are present in the negative half-line between times and . In symbols

| (66) |

where we recall that is the population of particles at time in a branching Brownian motion without absorption or stopping.

The advantage of is that since it is defined on it satisfies a KPP equation on the whole real line:

Otherwise said the function solves the KPP equation on the whole line with initial condition . Since for fixed, goes to 0 as with a super exponential decay (like the tail of a Gaussian), Bramson’s convergence Theorem [7, Theorem A], ensures that there exists a constant such that we have

| (67) |

where Bramson’s displacement is given in (23). The value depends on because for different we plug different initial conditions in the KPP equation .

Since when , one obtains taking :

| (68) |

Therefore we only need to show that for large enough, is close to :

Lemma 25.

| (69) |

In addition, there exists such that as

Indeed, assuming that Lemma 25 holds, we can conclude the

Proof of Theorem 9.

It now remains to prove Lemma 25. We start with

Lemma 26.

For any there exists such that for all one has

(The in the denominator makes the following easier.)

Proof.

We use the representation (66). Let ; obviously

where is the solution of (22). is by definition the probability that the leftmost particle at time of a driftless branching Brownian motion is to the right of ; it is also the probability that the leftmost particle at time of a branching Brownian motion with drift is to the right of zero. For (regimes A and B), this probability is known to tend to zero when . ∎

The next step is the following Lemma:

Lemma 27.

For any and any one has

Proof.

follows immediately from their definitions as probabilities. Let us introduce

We have that

Performing simple calculations we arrive at

since and .

The last step is then to prove that has a limit for large .

As is strictly increasing and continuous, and , we may define by

Fix . We have that

as long as and are large enough by (68) and (69). From this we deduce

| (70) |

Consequently

Since can be chosen arbitrarily small we have that , for some constant . This and (70) immediately yields that

where we used that . This concludes the proof of Lemma 25.

3 Radius of convergence and asymptotic behavior of

In Section 1.2.3, we related the to a function defined as a series of which the coefficients follows the recursive equation (12). We write here the same property in a slightly different but equivalent way. Let be defined by

and introduce and . These quantities satisfy the relations

| (71) |

Let be the radius of convergence of . We know that there exists a relating and through

The following observation will be useful. Since and , the function (defined on a domain containing zero) has a local maximum in zero. This implies that for the function has a local minimum in . In fact is the first local minimum (and indeed the first point where the first derivative cancels) one encounters left of zero for

The steps of the proof are the following:

-

1.

We show that for small enough (including ).

-

2.

We prove that there exists which is the first minimum one encounters left of zero for and that

(72) for some .

-

3.

We show that converges to uniformly on . This implies that

(73) -

4.

Since we conclude that that is within the radius of convergence of for small enough. The identity

shows that

where we made the dependance of on explicit.

We now prove these points.

-

1.

The key remark is that if for a real and an integer , one has for all then, as can be shown by a very simple recursion, the property holds for all .

Computing the first values of , one checks easily that the maximum of for is around 14.14. For small enough, by continuity of , the maximum of for will be no more than and hence one has

(74) As a consequence, for small enough (including ).

-

2.

The bound (74) applies for . Thus, for any using only the the fifty first terms of the expansion leads to an error of at most . In that way we computed and . Therefore is smaller than both and , and the function must have a minimum in . In other words we proved . It is easy to check that for . Estimating an error by we conclude that for . In this way we get (72).

- 3.

Acknowledgments

PM’s research was supported by NCN grant DEC-2012/07/B/ST1/03417".

References

- [1] L. Addario-Berry and N. Broutin. Total progeny in killed branching random walk. Probab. Th. Related Fields, 151(1-2):265–295, 2011.

- [2] E. Aïdékon. Tail asymptotics for the total progeny of the critical killed branching random walk. Electron. Comm. Probab., 15:522–533, 2010.

- [3] L. Alili, P. Graczyk, and T. Żak. On inversions and doob -transforms of linear diffusions. 2012. arXiv:1209.5322.

- [4] H. Berestycki and F. Hamel. see Theorem 24, chapter 2 of book in preparation.

- [5] J. Berestycki, N. Berestycki, and J. Schweinsberg. Critical branching brownian motion with absorption: survival probability. Probab. Th. Related Fields, to appear, 2012.

- [6] J. Berestycki, N. Berestycki, and J. Schweinsberg. The genealogy of branching Brownian motion with absorption. Ann. Probab., 41(2):527–618, 2013.

- [7] M. Bramson. Convergence of solutions of the Kolmogorov equation to travelling waves. Mem. Amer. Math. Soc., 44(285):iv+190, 1983.

- [8] B. Chauvin and A. Rouault. KPP equation and supercritical branching Brownian motion in the subcritical speed area. Application to spatial trees. Probab. Th. Related Fields, 80(2):299–314, 1988.

- [9] P. Flajolet and R. Sedgewick. Analytic combinatorics. Cambridge University press, 2009.

- [10] J. W. Harris and S. C. Harris. Survival probabilities for branching Brownian motion with absorption. Electron. Comm. Probab., 12:81–92 (electronic), 2007.

- [11] J. W. Harris, S. C. Harris, and A. E. Kyprianou. Further probabilistic analysis of the Fisher-Kolmogorov-Petrovskii-Piscounov equation: one sided travelling-waves. Ann. Inst. H. Poincaré Probab. Statist., 42(1):125–145, 2006.

- [12] P. Hartman. On local homeomorphisms of Euclidean spaces. Bol. Soc. Mat. Mexicana (2), 5:220–241, 1960.

- [13] H. Kesten. Branching Brownian motion with absorption. Stochastic Proc. Appl., 7(1):9–47, 1978.

- [14] R. Lyons, R. Pemantle, and Y. Peres. Conceptual proofs of criteria for mean behavior of branching processes. Ann. Probab, 23(3):1125–1138, 1995.

- [15] P. Maillard. The number of absorbed individuals in branching Brownian motion with a barrier. Ann. Inst. H. Poincaré Probab. Statist., 49(2):428–455, 2013.

- [16] H. P. McKean. Application of Brownian motion to the equation of Kolmogorov-Petrovskii-Piskunov. Comm. Pure Appl. Math., 28(3):323–331, 1975.

- [17] J. Neveu. Multiplicative martingales for spatial branching processes. In Seminar on Stochastic Processes, 1987 (Princeton, NJ, 1987), volume 15 of Progr. Probab. Statist., pages 223–242. Birkhäuser Boston, Boston, MA, 1988.

- [18] W. Rudin. Real and complex analysis. Tata McGraw-Hill Education, 1987.