Estimation of Zero Intelligence Models by L1 Data

Abstract

A unit volume zero intelligence (ZI) model is defined and the distribution of its L1 process is recursively described. Further, a generalized ZI (GZI) model allowing non-unit market orders, shifts of quotes and general in-spread events is proposed and a formula for the conditional distribution of its quotes is given, together with a formula for price impact. For both the models, MLE estimators are formulated and shown to be consistent and asymptotically normal. Consequently, the estimators are applied to data of six US stocks from nine electronic markets. It is found that more complex variants of the models, despite being significant, do not give considerably better predictions than their simple versions with constant intensities.

Keywords: Limit Order Market, Stochastic Models, Econometric Methods,

1 Introduction

With the recent wide expansion of trading according to continuous double auction (CDA), the importance of mathematical modelling of this trading mechanism grows.

A number of models of CDA exist which assume a rational behaviour of agents involved (see, e.g., Parlour and Seppi (2008) and the references therein); these models are, however, dependent on many arbitrary assumptions and do not give much better empirical results than models assuming a purely random behaviour of agents (see Gode and Sunder (1993) for a discussion). Thus, as an alternative to the “rational” approach, zero intelligence (ZI) models of the CDA started to be studied: out of a number of similar models of that kind, let us name Stigler (1964); Maslov (2000); Challet and Stinchcombe (2001); Luckock (2003); Smith et al. (2003); Mike and Farmer (2008) or Cont et al. (2010). All these models assume unit order sizes, Poisson arrivals of market and limit orders and locally constant cancellation rates depending on the distance to the quotes.111The only exceptions are Maslov (2000) and Challet and Stinchcombe (2001) with a discrete time (which could, however, be regarded as Poisson events’ time) and Mike and Farmer (2008), in which the cancellation rate also depends on the order books’ size and imbalance For a survey of the ZI models and their characteristics, see Chakraborti et al. (2011a) and Chakraborti et al. (2011b), especially Section II of the latter paper. For the recent developments, see Abergel et al. (2011).

Although, according to their advocates, the ZI models are able to mimic many stylised empirical facts such as fat tails or non-Gaussianity (Slanina (2001, 2008); Šmíd (2008); Cont (2011)), no rigorous statistical evidence in that respect has been presented yet due to intractability of these models. In Šmíd (2012), a conditional distribution given L1 data is described; however, the model considered in this paper is too general to ensure consistency of statistical estimators.

The present paper simplifies the approach of Šmíd (2012) by assuming only a finite number of prices so that it is possible to construct consistent asymptotically normal estimators of the models’ parameters.

The exposition is started by introducing a sufficiently general setting covering a wide range of existing zero intelligence (ZI) models, e.g., an early work of Stigler (1964), the model by Cont et al. (2010), a discretised version of Luckock (2003) and a slightly modified version of Smith et al. (2003). After demonstrating ergodicity of the covered models, a conditional density of jumps of the L1 process (i.e., the bid, the ask, and the corresponding offered volumes) given its history is formulated.222Although order book (L2) data might seem more natural to be used for the estimation, the better availability and lower price of L1 data speak for using them. This approach, in addition, allows us to avoid a problem of hidden limit orders, which are invisible in the books but affect sizes of quotes’ jumps.

Further, in order to treat the most obvious discrepancies between the ZI models and reality, a generalised (GZI) setting is proposed, which allows shifts of the quotes, non-unit market orders and general distributions of inside-the-spread events. A formula for a conditional density of the out-of-spread jumps of the quotes, later used in estimating the in-book parameters, is given.

Subsequently, Maximum Likelihood estimators are formulated and several variants of both the ZI and GZI models are estimated by means of L1 data for six stocks on nine US electronic markets. Further, for each stock-market pair, the variants of the models are compared by their ability to forecast magnitudes of the quotes’ jumps. It is found that more complicated variants of the models do not bring significant improvements in comparison with the simple variant with constant intensities, which itself, however, nearly always performs significantly better than a naive prediction of the jumps. It is also found that GZI variants of the models do not perform significantly better than their ZI counterparts.

This paper is organised as follows: First, the ZI setting is defined (Section 2) and the distribution of the L1 process given its history is derived. Consequently, the GZI setting is introduced and a formula for the density of the out-of-spread jumps and volume changes is given (Section 3). Finally, the empirical evidence is discussed (Section 4) and the paper is concluded (Section 5). The Appendix includes a proof of Theorem 2.2 (Appendix A), a proof of asymptotic properties of the MLE estimator (Appendix B), and detailed results on the estimation (Appendix C).

2 Zero Intelligence Model

2.1 Definition

Consider a general discrete-price continuous-time zero intelligence model with unit order sizes described by a pure jump type process

where

and

are the sell limit order book and buy limit order book, respectively; here, is a number of possible prices (ticks) and, for any , () stands for the number of the sell (buy) limit orders with price waiting at time . Further, denote by

the (best) ask and bid respectively. The list of possible events causing jumps of together with the notation for their intensities is given in the following table:

| code - | intensity - | description |

|---|---|---|

| An arrival of a buy market order, causing to decrease by one (if the sell limit order book is empty then the arrival of the market order has no effect). | ||

| An arrival of a sell limit order with limit price causing an increase of by one. | ||

| A cancellation of a pending sell limit order with a limit price causing a decrease of by one. | ||

| An arrival of a sell market order, causing to decrease by one (if the buy limit order book is empty then the arrival of a market order has no effect). | ||

| An arrival of a buy limit order with limit price causing an increase of by one. | ||

| A cancellation of a pending buy limit order with a limit price causing a decrease of by one. |

Here, all are measurable functions.

It is assumed that all the flows of the market orders, and the flows of limit orders as well as their cancellations are mutually independent in the sense that the conditional distribution of the relative time of the first event following given the history of up to is exponential with parameter

| (1) |

and that

| the probability that the next event will be of type equals to | (2) |

where is the intensity of event at . It is obvious that is then a Markov chain in a countable state space.

Finally, it is assumed that are deterministic and

| (3) |

where are constants, and that a symmetric assumption holds for .

2.2 Relation to Existing Models

The following table shows how some of the models mentioned in the Introduction comply with our setting. When speaking about Luckock (2003), we have its discretised version (see Šmíd (2012), Sec 3.3) in mind. When speaking about Smith et al. (2003), we are considering its bounded version (i.e., contrary to Smith et al. (2003) we assume zero arrival intensities for prices smaller than one and greater than ).

Here, , where , are (continuous) cumulative distribution functions, are measurable functions and the rest of the symbols are constants.

Some of the models from the Introduction were not mentioned in the table: We did not include either Maslov (2000) or Challet and Stinchcombe (2001) because they both consider discrete time and are very similar to Smith et al. (2003) with , Cont et al. (2010), respectively. The model by Mike and Farmer (2008) was not included because of its complicated cancellation sub-model and because, apart from the cancellations, it is similar to that of Cont et al. (2010). Finally, we did not include Stigler (1964) because it is a special version of Luckock (2003) (with ).

2.3 Distribution

Let us start with a result which will guarantee that sampling from the model will give enough information to a statistician.

Proposition 2.1.

If , , and . then is ergodic.

Proof.

The Proposition may be proved analogously to Cont et al. (2010), Proposition 2, where the ergodicity is verified by finding a Markov chain in dominating the total number of orders with a recurrent zero state. In particular, it suffices to replace the definition of and from Cont et al. (2010) by

and

∎

Our next goal is to derive a recursive analytic expression of the distribution of

(the L1 process). To do so, let us denote by the jumps of and, in order to avoid frequent double indexing, let us write instead of and instead of for any process . For each , we want to evaluate

starting with

To this end, note that

-

•

jumps down if and only if a limit order arrives into the spread, in which case a limit price of the new order becomes a new value of .

-

•

jumps up if and only if the offered volume of the ask decreases to zero due to either a market order arrival or a cancellation, in which case the closest occupied tick becomes a new value of .

Formally,

| (4) |

where is the type of an event happening at and where by definition. Thus, to determine the conditional distribution of , it suffices to know a joint distribution of which is described by the following Theorem in three steps:

Theorem 2.2.

(i) For any and ,

where

and, for any ,

(ii) Denote by the Dirac measure concentrated in (i.e., the distribution of constant ) and write for convolution (i.e., summation of two independent variables). For any and ,

where

and, for any ,

(iii) are mutually conditionally independent given .

Proof.

See Appendix A. ∎

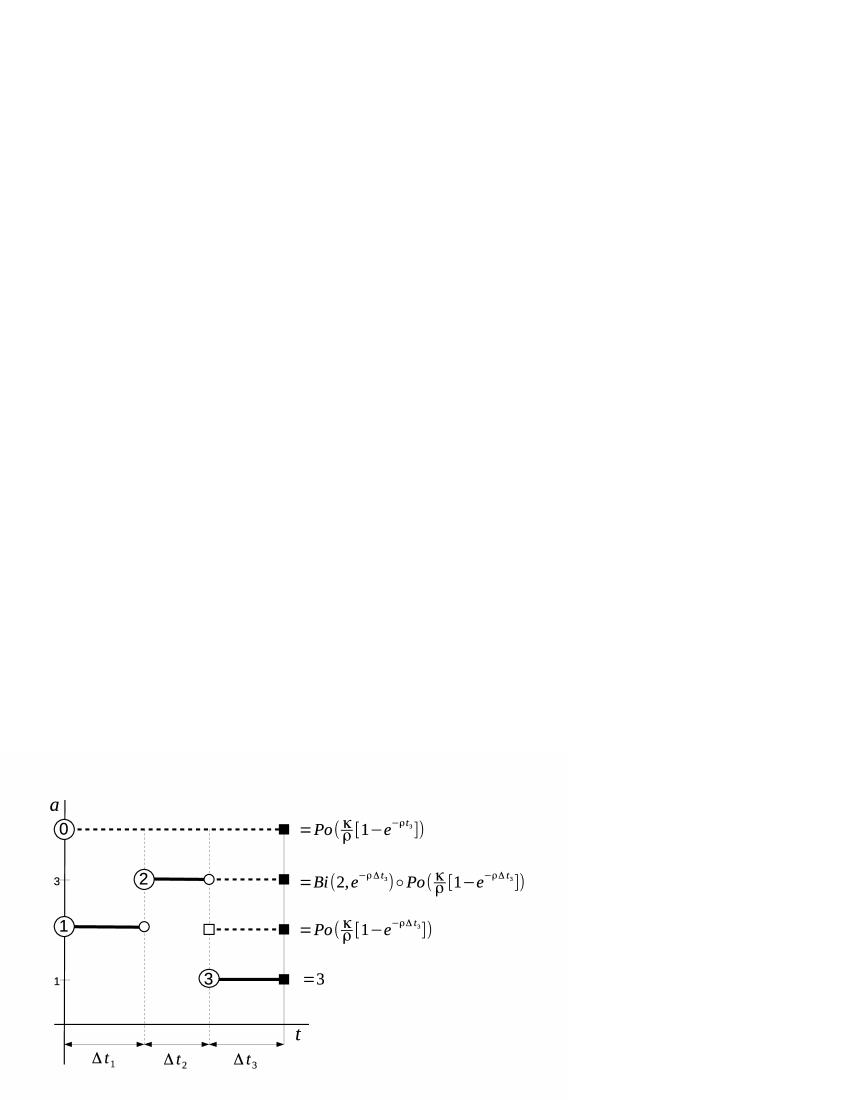

Before proceeding further, let us illustrate point (ii) of the Theorem, which is somewhat opaque, by an example.

Exapmle 2.3.

Consider model by Smith et al. (2003) with (implying ). Let , , , , , , (see Figure 1 for an illustration).

Let us start with : as no orders could be present in tick before (the ask was above 2 that time), all the in-book orders present in the tick are those having arrived between and and not being cancelled. According to Appendix A, number of those orders is (to check it, note that so and which, according to Appendix A, is actually the distribution of the immigration and death process of length ).

For , the situation is the same with the difference that number of initial orders having survived until , which is distributed according to , has to be added to .

Further, as the orders present in tick 4 at are exactly those having arrived from the start and not being cancelled, - it is easy to check that (ii) gives the same result.

Finally, because , we have , and so, according to (ii), .

From the Theorem and (4), we get that

Corollary 2.4.

(i) Conditional density of is given by

(ii) conditional density of is given by

where denotes indicator function and

(iii) conditional density of given is given by

Remark 1.

As the definitions of and are symmetric, formulas for the (conditional) distribution of are symmetric to those for . Moreover, as changes of and are mutually exclusive almost sure, i.e.,

almost sure and vice versa, is conditionally constant given events which cause changes of (and vice versa) so the conditional distribution of is uniquely determined by Corollary 2.4 and a formula for .

In the rest of the paper, we shall deal only with the ask side, i.e., with , leaving aside due to the symmetry.

Because density depends on all the parameters related to (i.e., ), it is straightforward to estimate these parameters by Maximum Likelihood based on and a sample from (). Moreover, if we put

| (5) |

and, quite realistically, assume that and depend only on a distance to the ask, i.e.,

| (6) |

for some and , and that the “inside-the-book” intensities

| (7) |

depend on different parameters than the “spread” intensities

| (8) |

then the estimation of the “ask-side” parameters could be split into the estimation of the parameters underlying (8), based on , and that of the parameters underlying (LABEL:eq:parssob), based on . In the present paper, only the latter case of an estimation is discussed.

3 Generalised Model

Despite the popularity of the ZI models, there is no doubt that they are too rough and neglect many aspects of real-life trading. The most obvious issues in this respect are two:

-

(i)

the volumes are non-unit in reality,

-

(ii)

agents, at least sometimes, act strategically rather than in a random way.

To deal with (i), authors of ZI models usually argue that the sizes of a majority of orders are one-lot and, when an order is larger, it may be imagined that several subsequent one-lot orders have been issued. However, this simplification may be tolerable only in the case of limit orders (if the order book is observed only at certain time instants then larger orders are indeed interchangeable with several subsequent unit ones) but it is unacceptable for non-unit market orders which could not be imaginatively split without a serious violation of the assumption that their arrival intensity is constant.

To justify the ZI models against (ii), it is usually argued that the strategic reasoning is so complex that taking it as random is less evil than constructing wrong models. This argument, however, has a drawback, too: no matter how reasonable it may sound, one still has to deal with empirical phenomena stemming from (bounded) rationality, such as shifts and rapid insertions and cancellations of orders (especially quotes) in response to changes of the book.

To meet those issues, the setting defined in Section 2.1 might be generalised by assuming tbat

- M

-

volumes of market orders are possibly non-unit,

- S1

-

once a (unit) limit order stops to be a quote due to an in-spread sell limit order, it is, with probability , immediately cancelled or shifted to the position of the new quote,

- S2

-

once a quote jumps out of the spread, there is a non-zero probability that the move was caused not by a market order or cancellation but by a shift of the quote.

Moreover, to give more freedom to modelling of (possibly complex) behaviour of the quotes, it is allowed that

- D

-

the distribution of is arbitrary and, moreover, and may jump by more than one unit.

The list of events potentially changing at is newly as follows:

| code | description |

|---|---|

| a buy market order of volume | |

| a sell limit order with price and size put into the spread | |

| a cancellation of orders of the ask | |

| ] | a shift of orders with price to tick , |

| ] | a shift of orders with price to tick , |

plus symmetric events concerning .

Even though, given this generalisation, (i) of Theorem 2.2 ceases to be true, its Assertions (ii) and (iii) would keep holding with instead of if it is additionally assumed that

-

•

the volumes of market orders are i.i.d. random, independent of all the past and the present events on the market

-

•

the (Bernoulli) variables indicating the shifts are mutually independent, independent of the past and the present events on the market.333To see it, note that the proof continues to be valid with instead of in (A).

What does change, however, is the distribution of quote jumps outside of the spread after the ask is depleted, which are now non-zero if and only if

| (9) |

in which case

where

is the total number of the orders in the book between the former and the present value of the ask and

is the number of the orders the particular change would like to “eat” from the inside of the book.

As, by (ii) and (iii) of (the modified version of) Theorem 2.2,

and, by (iii) of the Theorem, is conditionally independent of given , we are getting

Corollary 3.1.

On set (9), the distribution of is given by density

Remark 2.

Thus, if we keep assuming (5) and (6), we may estimate parameters underlying and together with by means of MLE based on ; as it could be checked in Appendix B, the asymptotic properties of the estimator are not harmed by the generalisation provided that the generalised process is ergodic, which may be guaranteed, e.g., by requiring that

- E

-

is stochastically dominated by a Markov chain with a zero recurrent state.

Under this assumption, Proposition 2.1 keeps holding because none of the generalisations, except for D, which is treated by E, increase the total number of orders in in comparison with the ZI.

Remark 3.

Unlike in the unit-volume ZI model, price impact may be predicted in the GZI model: denoting the impact of a trade with volume at time , we have

4 Empirical Evidence

4.1 Data

For our empirical analysis, tick-by-tick trade and quote data was used, i.e., values

where is an amount traded at , defined by

In particular, data of six stocks

-

•

Exxon Mobile (XOM)

-

•

Microsoft (MSFT),

-

•

General Electric (GE)

-

•

MarketAxess Holdings (MKTX)

-

•

J2 Global (JCOM)

-

•

American Realty Investors (ARL)

from nine US electronic markets

-

•

NASDAQ OMX BX

-

•

NSE

-

•

Chicago

-

•

NYSE

-

•

ARCA

-

•

NASDAQ T

-

•

CBOE

-

•

BATS

-

•

ISE

from ten months starting from March were analysed.

Our choice of the titles was done so as to cover both “large” and the “smaller” stocks. The first three ones - XOM, MSFT and GE - belong to the top ten companies by market capitalization and usually exhibit large trading volumes. MKTX and JCOM, on the ather hand, are usually ranked as “small caps” (having market capitalization around $1 bilion) with moderate trading volumes. Company ARL, belonging to the category of “micro caps” (capitalisation around $100 million), could be counted among illiquid stocks.

As to the markets, we did not pre-select which of them to analyse; contrarily, all the markets were included on which the examined stocks were traded and for which at least some data were available444Our dataset came from Tickdata, Inc.- the only exception is NASDAQ ADF, which is a platform for recording trades rather than a limit order market (see FINRA (2015)).

As the trade data (process ) came from a different data source than the quote data (process ), it was necessary to algorithmically match individual trades with the L1 data changes in which our algorithm, designed for that purpose, succeeded in about 70 percent of trades (the rest could not be uniquely attributed to any L1 change ). This fact, however, did not harm the estimation other way than by decreasing the sample size.555To be absolutely rigorous, we should assume that the success in matching is stochastically independent of the quote process to claim this.

4.2 Estimation

For the actual estimation, only records originating between 9:40 a.m. and 3:30 p.m. were used when the process could be assumed to be near its stationary distribution; the inclusion of the ten-minute “warm-up” period following the opening at 9:30 also partially justifies our assumption (5).

When estimating within the ZI models, all the jumps of up666The jumps of down and the changes of preserving could be omitted without any loss of information because the corresponding these changes are conditionally constant hence not depending on any parameter. could serve as a sample while, in the case of the GZI models, only the jumps of matched with trades were included; the reason for this restriction is that the jumps of caused by unpaired trades, shifts and cancellations could not be distinguished from each other in the L1 data, so the corresponding values of could not be determined. For each paired trade record, on the other hand, the value of may be obtained from the volume of the trade and from the (known) volume of the former ask.

For both the ZI and the GZI settings, and for each stock-market pair, the following estimation procedure was run: as its first step, a simple version of the model with

(Smith et al. (2003) in its ZI variant), which we later call basic model, was estimated. Subsequently, three power tail models with and , defined by

were estimated gradually. As a “true” model, the one was chosen in which all the parameters came out significant while the likelihood ratio comparing this model with the subsequent one came out insignificant.

Each estimation procedure was run on a sample of at most observations; even though there were many more observations available for a majority of the stock-market pairs, a restriction had to be made due to the large time requirement of the estimation, caused by complex formulas for conditional densities involved. In case that the optimisation algorithm could not find maximum of the ML function within a time limit of sec (approx. min) for none of the four variants of the model, the procedure was repeated once more with a sample of size .

The prediction power of each model was evaluated by

where is a sample size, is the number of out-of-sample observations, are the magnitudes of the jumps of up, is their average and where the conditional expectation in the numerator was computed by means of the estimated parameters. By its construction, can be understood as a percentage improvement in comparison with a naive prediction of the out-of-spread jumps by their mean. In the GZI setting, may also be seen as a measure of accuracy of the market impact prediction.

For automation of the whole procedure including matching of trades, and the model selection, a C++ package has been developed by the author, using the NLOPT library, namely LBFGS and BOBYQUA optimisation algorithms, to compute maxima of the ML functions.777As a default choice LBFGS has been used, the BOBYQUA was employed only in instances in which it could not find a maximum within the time limit). For more on these algorithms and the NLOPT library, see Johnson (2012). A source code of the package is available at https://github.com/cyberklezmer/fepp under branch qf15.

4.3 Results

Results of the estimation procedure of the ZI modelsd for the “big-cap” stocks XOM, MSFT and GE are summarised in Table 1. It may be seen that 21 out of all the 27 estimations were successful in the sense that a significant model was found, which exhibits a positive improvement (measured by ). Out of the “failed” cases, four times a significant model was found giving a negative 888In two of these instances, all the jump increments were exactly one; hence their average predicted the jumps with zero error, which lead to minus infinity for ., once the time limit was reached even with a reduced sample, and once no data was available.

Out of all the 21 successful instances, the basic model was chosen nine times, the simplest tail model six times and model six times; model never came out significant within the time limit. Higher ’s values in comparison with a basic model were reached in only seven out of the 12 cases when a tail model was selected, while the basic model came out better in two cases; in the three remaining cases, the was identical up to two decimal digits. Even though, on average, the tail model performed better, the difference was not found statistically significant according to a Wilcoxon test. Detailed results of this estimation can be found in Appendix C.1.

Summary results for the GZI model for big-caps may be found in Table 2. Here, the estimation was successful in 21 out of 25 cases with at least some data, three times the time-out was reached; came out negative in one case.

In order to answer the question whether it is worth using the more complicated GZI model rather than the ZI one, the estimation procedure was run for ZI models once more using the same samples as those used for the GZI ones (i.e., only the changes with trades matched); the corresponding results are displayed in the second column below each stock. Out of the 20 cases when both estimations were successful, eight times the GZI model reached a higher while three times was higher for the ZI model; nine times was the same up to two decimal digits. Again, it could not be statistically proved that the GZI model performs significantly better.

Detailed results of the GZI estimation may be found in Appendix C.2 (the GZI models) and Appendix C.3 (their ZI counterparts).

Tables 3 and 4 summarise estimates of tail exponents of and . It may be seen that a dispersion of the values of is great; however, their average is not far from present empirical evidence (see, e.g., Chakraborti et al. (2011a), III.C).999It should be noted, however, that only the first several values of and played a role in the estimation, especially when the average jump out of the spread was small, so the results say very little about the actual power law behaviour. The results for tail exponents of , which have never been statistically estimated yet to the best of the author’s knowledge, are similar to the case of , with average value .

Results of the estimation of the small caps MKTX, JCOM and the micro-cap ARL may be found in Table 5 and Table 6. For the small caps, the ZI model was successful for 10 of 13 pairs with sample size at least , once a negative was reached, two times the optimization failed.101010In particular, the solver stopped the optimization without changing the initial parameters reporting that its tolerance criterion was reached which suggest that the MLE function is too flat to be optimized. For ARL, the procedure was successful only once (with a disappointing prediction power) with all of the failures due to failed optimizations. A closer look to the results suggests two possible causes of the failures: small sample sizes and/or large average jumps of , causing large evaluation times of the densities (see Appendix C for detailed values). The situation is not much better in the case of GZI models either: small caps are successful in 7 out of 9 cases, ARL is only once half-way successful out of three cases. Results of a comparison of more complex ZI models with their basic variant are similar to those of the big-caps: out of 8 cases when the comparison is possible, more complex models won three times, four times the basic model was more successful, once the results were the same. Similarly, from 8 comparisons of GZI and ZI variants of the model, the GZI variant was more successful four times, the ZI one three times, once the results were equal.

| XOM | MSFT | GE | |

|---|---|---|---|

| NASDAQ OB | |||

| NSE | |||

| Chicago | |||

| NYSE | |||

| ARCA | |||

| NASDAQ T | |||

| CBOE | |||

| BATS | |||

| ISE |

| XOM | MSFT | GE | ||||

|---|---|---|---|---|---|---|

| GZI | ZI | GZI | ZI | GZI | ZI | |

| NASDAQ OB | ||||||

| NSE | ||||||

| Chicago | ||||||

| NYSE | ||||||

| ARCA | ||||||

| NASDAQ T | ||||||

| CBOE | ||||||

| BATS | ||||||

| ISE | ||||||

| XOM | MSFT | GE | ||||

|---|---|---|---|---|---|---|

| ZI | GZI | ZI | GZI | ZI | GZI | |

| NASDAQ OB | ||||||

| NSE | ||||||

| Chicago | ||||||

| NYSE | ||||||

| ARCA | ||||||

| NASDAQ T | ||||||

| CBOE | ||||||

| BATS | ||||||

| ISE | ||||||

| XOM | MSFT | GE | ||||

|---|---|---|---|---|---|---|

| ZI | GZI | ZI | GZI | ZI | GZI | |

| NASDAQ OB | ||||||

| NSE | ||||||

| Chicago | ||||||

| NYSE | ||||||

| ARCA | ||||||

| NASDAQ T | ||||||

| CBOE | ||||||

| BATS | ||||||

| ISE | ||||||

| MKTX | JCOM | ARL | |

|---|---|---|---|

| NASDAQ OB | |||

| NSE | |||

| Chicago | |||

| NYSE | |||

| ARCA | |||

| NASDAQ T | |||

| CBOE | |||

| BATS | |||

| ISE |

| MKTX | JCOM | ARL | ||||

|---|---|---|---|---|---|---|

| GZI | ZI | GZI | ZI | GZI | ZI | |

| NASDAQ OB | ||||||

| NSE | ||||||

| Chicago | ||||||

| NYSE | ||||||

| ARCA | ||||||

| NASDAQ T | ||||||

| CBOE | ||||||

| BATS | ||||||

| ISE | ||||||

5 Conclusions

A setting covering many of the existing zero intelligence (ZI) models and its generalisation allowing for non-unit market orders and shifts of quotes (GZI) were introduced. Several variants of both the ZI and GZI settings, differing in their complexity, were tested on trade and quote data for 54 real-life stock-market pairs. It was found that, especially for liquid stocks, both the ZI and GZI models came out significant with a substantial prediction power; however, their more complicated variants did not produce significantly better predictions in comparison with a simple model with constant intensities. Finally, as the rewults of the ZI and the GZI variants are comparable, our suggestion is to use the GZI models which are more realistic and are capable of predictions of market impact.

References

- Abergel et al. (2011) Abergel, F., Chakrabarti, B.K., Chakraborti, A. and Mitra, M., Econophysics of order-driven markets, 2011, Springer Science & Business Media.

- Bradley (2005) Bradley, R.C., Basic properties of strong mixing conditions. A survey and some open questions. Probability surveys, 2005, 2, 37.

- Chakraborti et al. (2011a) Chakraborti, A., Toke, I.M., Patriarca, M. and Abergel, F., Econophysics review: I. Empirical facts. Quantitative Finance, 2011a, 11, 991–1012.

- Chakraborti et al. (2011b) Chakraborti, A., Toke, I.M., Patriarca, M. and Abergel, F., Econophysics review: II. Agent-based models. Quantitative Finance, 2011b, 11, 1013–1041.

- Challet and Stinchcombe (2001) Challet, D. and Stinchcombe, R., Analyzing and modeling 1+ 1¡ i¿ d¡/i¿ markets. Physica A: Statistical Mechanics and its Applications, 2001, 300, 285–299.

- Cont (2011) Cont, R., Statistical modeling of high-frequency financial data. Signal Processing Magazine, IEEE, 2011, 28, 16–25.

- Cont et al. (2010) Cont, R., Stoikov, S. and Talreja, R., A Stochastic Model for Order Book Dynamics. Operations Research, 2010, 56, 549–563.

- Cornfeld et al. (1982) Cornfeld, I.P., Fomin, S.V. and Sinai, Y.G., Ergodic theory, 1982 (Springer: New York).

- Crowder (1976) Crowder, M.J., Maximum likelihood estimation for dependent observations. Journal of the Royal Statistical Society. Series B (Methodological), 1976, pp. 45–53.

- Daley and Vere-Jones (2003) Daley, D.J. and Vere-Jones, D., An Introduction to the Theory of Point Processes, second , 2003 (Springer: New York).

- FINRA (2015) FINRA, Alternative Display Facility (ADF). http://www.finra.org/industry/adf Accessed: 2015-04-17, 2015.

- Gode and Sunder (1993) Gode, D.K. and Sunder, S., Allocative efficiency of markets with zero-intelligence traders: Market as a partial substitute for individual rationality. Journal of political economy, 1993, pp. 119–137.

- Hoffmann-Jørgenson (1994) Hoffmann-Jørgenson, J., Probability with a View Towards to Statistics I., 1994 (Chapman and Hall: New York).

- Johnson (2012) Johnson, S.G., The NLopt nonlinear-optimization package (Version 2.3). URL http://ab-initio. mit. edu/nlopt, 2012.

- Kallenberg (2002) Kallenberg, O., Foundations of Modern Probability, second , 2002 (Springer: New York).

- Luckock (2003) Luckock, H., A Steady-State Model of the Continuous Double Auction. Quantitative Finance, 2003, 3, 385–404.

- Mandjes and Żuraniewski (2011) Mandjes, M. and Żuraniewski, P., M/G/∞ transience, and its applications to overload detection. Performance Evaluation, 2011, 68, 507–527.

- Maslov (2000) Maslov, S., Simple Model of a Limit Order Driven Market. Physica A, 2000, 278, 571–578.

- Mike and Farmer (2008) Mike, S. and Farmer, J.D., An empirical behavioral model of liquidity and volatility. Journal of Economic Dynamics & Control, 2008, 32, 200–234.

- Parlour and Seppi (2008) Parlour, C.A. and Seppi, D.J., Limit order markets: A survey. Handbook of financial intermediation and banking, 2008, 5, 63–95.

- Slanina (2001) Slanina, F., Mean-Field Approximation for a Limit Order Driven Market. Phys. Rev., 2001, 64, 056136 Preprint at http://xxx.sissa.it/abs/cond-mat/0104547.

- Slanina (2008) Slanina, F., Critical comparison of several order-book models for stock-market fluctuations. The European Physical Journal B-Condensed Matter and Complex Systems, 2008, 61, 225–240.

- Šmíd (2008) Šmíd, M., Price Tails in the Smith and Farmer’s Model. Bulletin of the Czech Econometric Society, 2008, 25.

- Šmíd (2012) Šmíd, M., Probabilistic Properties of the Continuous Double Auction. Kybernetika, 2012, 48, 50–82 Available at: http://www.kybernetika.cz/content/2012/1/50/paper.pdf.

- Smith et al. (2003) Smith, E., Farmer, J.D., Gillemot, L. and Krishnamurthy, S., Statistical Theory of the Continuous Double Auction. Quantitative finance, 2003, 3, 481–514.

- Stigler (1964) Stigler, G., Public regulation of the securities markets. Journal of Business, 1964, pp. 117–142.

Appendix A Proof of Theorem 2.2

Before starting the proof, recall that that a Markov chain on is called immigration and death process with immigration intensity and death intensity and with initial population (we abbreviate this by ) if its transition matrix has zero components except of , , and if . Notice also that number of customers in an in queuing theory model follows an process. It is well known (see, e.g., Mandjes and Żuraniewski (2011), Section 2) that, for any positive ,

| (10) |

Further, let us introduce the following (re)formulation of process restricted to time interval , which will be used repeatedly in the subsequent proof: Let be independent uniform variables, independent of . By Kallenberg (2002), Theorem 6.10, there exist mappings from to the space of stochastic processes on such that, for each , and . By Kallenberg (2002), Proposition 6.13., are mutually conditionally independent given , so we may assume, without a change of distributions,

| (11) |

Using this reformulation and noting that both , are functions of , we see that

| (12) |

where denotes conditional indepdence of and given .

Because, by the definition of the ask, and , i.e, are conditionally constant, we have, for any ,

| (13) |

where the last “=” follows from Hoffmann-Jørgenson (1994), (6.8.14) (with and ) and from the fact that the jumps of ’s do not coincide with probability one (which guarantees that , , almost sure).

As a first step of proving the assertions of the Theorem, let us deal with one-step-ahead distribution :

Proposition A.1.

(i) For any and ,

(ii) For any ,

(iii) For any ,

Proof.

Thanks to the homogeneity of the process, we may assume .

(i) It follows from textbook knowledge that , being the first jump time of Markov chain , is exponential with rate , while , coding a type of the chain’s first jump, is (conditionally w.r.t. ) independent of with probabilities of particular events being equal to the rates of the events’ intensities to , which is formally expressed by (i).

(iii) Let and put . Clearly,

| (14) |

where

Further, it follows from the dynamics of the process and from the almost sure exclusivity of jumps of that

| (15) |

Now, because are functions of , we have so we may use the Law of Iterated Expectation to get

| (16) |

(at the third “=”, we have used Proposition 6.6 of Kallenberg (2002), the fourth one is due to measurability of the inner term w.r.t. the condition of the expectation, the fifth one is due to (13)).

Proof of the Theorem

Ad (i)

By the Law of Iterated Expectation, the strong Markov property of , and Proposition A.1 (i), it follows

| (18) |

(we could get rid of the outer conditional expectation at the last equality because its integrand is measurable with respect to its condition).

Ad (ii)

Before deriving the distribution of , let us formulate an auxiliary result:

Lemma A.2.

Let be random variables, let be as -algebra and let . If on and on for some -measurable variables then on .

Proof.

Let be variables mutually conditionally independent given , such that, on , , , and, for each , , , (outside , all the variables could be e.g., zero). Assume, without a change of the examined distributions, that and where , . Clearly, is (conditionally) Binomial with parameters and . Further, by Daley and Vere-Jones (2003), 2.3.4, . As are mutually conditionally independent given (which is because each of them depends on independent variables) we get that . The Lemma now follows from the fact that a convolution of two Poisson variables is again Poisson. ∎

Let . First we prove, by induction, that, for any ,

| (19) |

First, we show that (19) holds for : indeed, by Proposition A.1 (i) and Kallenberg (2002), Proposition 6.6., we get that (recall that ), which, by the Proposition 6.6. and by (3), gives (19) for .

Now, assume (19) to hold for . Similarly as in (18), we get, by Proposition A.1, (iii), that

| (20) |

giving, by Lemma A.2 applied to the induction hypothesis and (20), validity of (19) on . As, on , is conditionally constant, i.e.,

(19) is proved on because on the set so , and on the set. As (19) on follows similarly (here, ), (19) is proved for .

Ad (iii)

Let , , denote , and assume that are conditionally independent given , i.e., that

| (21) |

holds for any and for .

Let and put

From (13), we have that

for some . So, by the Law of Iterated Expectation, strong Markov property and the homogeneity, applied gradually,

| (22) |

(we could get rid of the expectation on the RHS because its integrand is measurable).

Let , let and . By evaluating (22) with and with , we get

(we could write the last “=” because the right-hand side of (22) does not depend on no with ). Thus, by the Complete Probability Theorem,

| (23) |

proving conditional independence of of given for any , which implies mutual conditional independence of given (see Kallenberg (2002), p. 109 below).

It remains to prove (21) for . To this end, put for any , and observe that, on each , are conditionally constant while , for . As are mutually conditionally independent given by (23) and as (conditional) constants are trivially (conditionally) independent of any random element, we get that are mutually conditionally independent given on by Local Property (Kallenberg (2002), Lemma 6.2), and, as ’s cover all the underlying space, the conditional independence holds universally. Relation (21) now follows from (i) of Proposition A.1 (the same way as in proof of (iii) of the Proposition).

Appendix B MLE Estimation

In the present Section, asymptotic properties of the MLE estimator are proved both for the ZI and the GZI model.

Before starting, let us formulate an auxiliary result:

Lemma B.1.

If is a continuous time stationary ergodic Markov chain in countable space then , where are the jump times of , is a stationary ergodic stochastic process.

Proof.

Denote the intensity of the first jump of given that . From the strong Markov property (Theorem 12.14 of Kallenberg (2002)), from Lemma 12.16 of Kallenberg (2002) and from the scalability of exponential distribution we have that , where , , is a sequence of i.i.d. (unit exponentially) distributed variables, independent of . As - being an i.i.d. sequence - is a strong mixing and is a strong mixing by Bradley (2005), process is a strong mixing (note that, for any , , , , it holds that where is a shift operator; the case of general follows from their approximation by rectangles) we get the ergodicity of by the well known fact that strong mixing implies ergodicity. Finally, as is a function of , the Lemma is proved. ∎

It follows from the Lemma that, once is understood as a process with then, thanks to its ergodicity (see Proposition 2.1) process , , is also ergodic. Hence by Birkhoff-Khinchin theorem (Cornfeld et al. (1982), Appendix 3), for any measurable function ,

| (24) |

in probability given that the expression written on the RHS exists.

Now, let be a vector of true parameters. Denote

( being called Fischer information matrix) where stands for . Substituting mappings assigning and for in (24), we get, by (24), that

| (25) |

for some non-random matrix which, being a limit of positive semidefinite matrices, is also positive semidefinite. By taking expectations on both sides of (25), we further get

| (26) |

Now put

and observe that

As by the definition of density, any of the integral’s first or second derivatives has to be zero, and, in particular, (we may interchange the integral and derivative in our discrete case) so

implying

| (27) |

If we now, as usual, assume to be regular, then, by (26) and (27),

| (28) |

Let for some and, for any matrix , denote . By (28) and basic linear algebra,

| (29) |

where is the smallest eigenvalue of . If, in addition, the parameter space is open and both and are twice continuously differentiable with respect to all the parameters (which is true for all the versions of the model we use), then is asymptotically Lipschitz on so

| (30) |

where is a suitable norm and is a Lipschitz constant, further implying, by using the fact that together with (29) and (29), we get

where . From the differentiability it follows that as for some so there has to exist and such that for all . Weak consistency now follows from (2.3) of Crowder (1976) with for suitable .

For the asymptotic normality it suffices, by Crowder (1976), (4.13) and the considerations explained below, that the absolute -th moments of the observations are bounded for a certain . This, however, can be easily achieved by determining a large enough constant and excluding from the sample any observation with .

Appendix C Detailed Results

Notation

- sample size, - average jump of up, - average market order volume. The number of stars stands for signification on levels , and , respectively.

C.1 ZI Model

| XOM on NASDAQ OB , , | XOM on NSE , | XOM on Chicago , |

| XOM on NYSE , | XOM on ARCA , | XOM on NASDAQ T , |

| XOM on CBOE , | XOM on BATS , | XOM on ISE , |

| MSFT on NASDAQ OB , | MSFT on NSE , | MSFT on Chicago , |

| MSFT on NYSE , No data | MSFT on ARCA , | MSFT on NASDAQ T , |

| MSFT on CBOE , | MSFT on BATS , | MSFT on ISE , |

| GE on NASDAQ OB , | GE on NSE , | GE on Chicago , |

| GE on NYSE , | GE on ARCA , Timeout reached. | GE on NASDAQ T , |

| GE on CBOE , | GE on BATS , | GE on ISE , |

| MKTX on NASDAQ OB , Optimization failed | MKTX on NSE , No data | MKTX on Chicago , No data |

| MKTX on NYSE , No data | MKTX on ARCA , | MKTX on NASDAQ T , |

| MKTX on CBOE , | MKTX on BATS , | MKTX on ISE , |

| JCOM on NASDAQ OB , | JCOM on NSE , Optimization failed | JCOM on Chicago , No data |

| JCOM on NYSE , No data | JCOM on ARCA , | JCOM on NASDAQ T , |

| JCOM on CBOE , | JCOM on BATS , | JCOM on ISE , |

| ARL on NASDAQ OB , No data | ARL on NSE , No data | ARL on Chicago , No data |

| ARL on NYSE , Optimization failed | ARL on ARCA , Optimization failed | ARL on NASDAQ T , |

| ARL on CBOE , Optimization failed | ARL on BATS , Optimization failed | ARL on ISE , Optimization failed |

C.2 GZI Model

| XOM on NASDAQ OB , , | XOM on NSE , , | XOM on Chicago , , |

| XOM on NYSE , , | XOM on ARCA , , | XOM on NASDAQ T , , |

| XOM on CBOE , , | XOM on BATS , , | XOM on ISE , , |

| MSFT on NASDAQ OB , , | MSFT on NSE , , | MSFT on Chicago , , |

| MSFT on NYSE , , No data. | MSFT on ARCA , , Timeout reached | MSFT on NASDAQ T , , No data |

| MSFT on CBOE , , | MSFT on BATS , , | MSFT on ISE , , |

| GE on NASDAQ OB , , | GE on NSE , , | GE on Chicago , , |

| GE on NYSE , , | GE on ARCA , , Timeout reached | GE on NASDAQ T , , Timeout reached |

| GE on CBOE , , | GE on BATS , , | GE on ISE , , |

| MKTX on NASDAQ OMX BX , , | MKTX on NSE , , No data | MKTX on Chicago , , No data |

| MKTX on NYSE , , No data | MKTX on ARCA , , | MKTX on NASDAQ T , , No data |

| MKTX on CBOE , , | MKTX on BATS , , | MKTX on ISE , , |

| JCOM on NASDAQ OMX BX , , | JCOM on NSE , , | JCOM on Chicago , , No data |

| JCOM on NYSE , , No data | JCOM on ARCA , , | JCOM on NASDAQ T , , No data |

| JCOM on CBOE , , | JCOM on BATS , , | JCOM on ISE , , |

| ARL on NASDAQ OMX BX , , No data | ARL on NSE , , No data | ARL on Chicago , , No data |

| ARL on NYSE , , | ARL on ARCA , , Optimization failed | ARL on NASDAQ T , , |

| ARL on CBOE , , No data | ARL on BATS , , | ARL on ISE , , |

| ARL on NASDAQ OMX BX , , No data | ARL on NSE , , No data | ARL on Chicago , , No data |

| ARL on NYSE , , | ARL on ARCA , , | ARL on NASDAQ T , , |

| ARL on CBOE , , No data | ARL on BATS , , | ARL on ISE , , |

C.3 ZI Model with Trades

| XOM on NASDAQ OB , | XOM on NSE , | XOM on Chicago , |

| XOM on NYSE , | XOM on ARCA , | XOM on NASDAQ T , |

| XOM on CBOE , | XOM on BATS , | XOM on ISE , |

| MSFT on NASDAQ OB , | MSFT on NSE , | MSFT on Chicago , |

| MSFT on NYSE , No data | MSFT on ARCA , | MSFT on NASDAQ T , No data |

| MSFT on CBOE , | MSFT on BATS , | MSFT on ISE , |

| GE on NASDAQ OB , | GE on NSE , Timeout reached | GE on Chicago , |

| GE on NYSE , | GE on ARCA , Timeout reached | GE on NASDAQ T , Timeout reached |

| GE on CBOE , | GE on BATS , | GE on ISE , |

| MKTX on NASDAQ OB , No data | MKTX on NSE , No data | MKTX on Chicago , No data |

| MKTX on NYSE , No data | MKTX on ARCA , | MKTX on NASDAQ T , No data |

| MKTX on CBOE , | MKTX on BATS , | MKTX on ISE , |

| JCOM on NASDAQ OB , | JCOM on NSE , No data | JCOM on Chicago , No data |

| JCOM on NYSE , No data | JCOM on ARCA , | JCOM on NASDAQ T , No data |

| JCOM on CBOE , | JCOM on BATS , | JCOM on ISE , |

| ARL on NASDAQ OB , No data | ARL on NSE , No data | ARL on Chicago , No data |

| ARL on NYSE , | ARL on ARCA , Optimization failed | ARL on NASDAQ T , |

| ARL on CBOE , No data | ARL on BATS , No data | ARL on ISE , No data |