Time-consistency of risk measures with GARCH volatilities and their estimation

Abstract

In this paper we study time-consistent risk measures for returns that are given by a GARCH model. We present a construction of risk measures based on their static counterparts that overcomes the lack of time-consistency. We then study in detail our construction for the risk measures Value-at-Risk (VaR) and Average Value-at-Risk (AVaR). While in the VaR case we can derive an analytical formula for its time-consistent counterpart, in the AVaR case we derive lower and upper bounds to its time-consistent version. Furthermore, we incorporate techniques from Extreme Value Theory (EVT) to allow for a more tail-geared statistical analysis of the corresponding risk measures. We conclude with an application of our results to a data set of stock prices.

2010 AMS subject classifications: 60G70, 91B30, 91G80, 91G70

2010 JEL classification: C02, C22, C58, G17, G32

Key words and phrases: dynamic risk measure, time-consistency, GARCH, Extreme Value Theory, Value-at-Risk, Average Value-at-Risk, Expected Shortfall, Generalized Pareto distribution, aggregate returns.

1 Introduction

In the wake of the financial crisis risk management constitutes a constant active field that attracts both mathematical research and quantitative requirements for the practical implementation. Most financial institutions need to abide with the Basel II/III accords that prescribe certain risk management rules to be applied to internal risk control and that are under periodic regulatory supervision. Over the last two decades the key notion of risk management arose in the form of a risk measure referred to as Value-at-Risk (VaR). Simply put, VaR determines the risk capital of a financial institution as the quantile of a profit-and-loss distribution with respect to some prescribed (either by regulation or by internal rules) time horizon and confidence level. An axiomatic approach to the field of risk measures is given by Artzner et al. (1999) in which the notion of the coherent risk measure is introduced and where it has been realized that VaR does not always satisfy the property of coherence. Artzner et al. (1999) introduce a risk measure that amends the lack of coherence that is nowadays known as the Average-Value-at-Risk (AVaR). An extension to convex risk measures is given in Föllmer and Schied (2002), which integrates existing notions of risk into the mathematical framework of convex dual theory and, hence, allows for deep and powerful dual characterizations. In order to account for the dynamic stochastic evolution of profit-and-loss positions the static risk measurement has been extended to the class of dynamic risk measures, which treats the risk measure not only as a (nonlinear) expectation but as a stochastic process, see e.g. Detlefsen and Scandolo (2005) and Riedel (2004) for the extension to the dynamic setting by means of convex dual theory. It has been realized in this dynamic framework that most existing static risk measures do not transfer in a straightforward manner into processes without violating the required property of time-consistency. A time-consistent dynamic risk measure secures the consistent behavior of a risk measure that, if a portfolio is riskier than another portfolio at some future time, then this portfolio has been riskier that the other portfolio at any time before. The literature on time-consistency of risk measures is diverse and rich as different mathematical viewpoints can be adopted to prevent the consistency property. An incomplete chronicle of research done in the field of time-consistent risk measures includes Peng (2004), Riedel (2004), Detlefsen and Scandolo (2005), Weber (2006), Föllmer and Penner (2006), Roorda and Schumacher (2007), Penner (2007), Bion-Nadal (2009), and Bielecki et al. (2015). A major result from the research on time-consistency reveals that in the class of law-invariant risk measures there is only one risk measure that, upon transfer into a time-dynamic process setting, supports time-consistency, namely the entropic risk measure (cf. Föllmer and Knispel (2011)).

In parallel to the aforementioned theoretical work statistical models and methods have been developed to calibrate and integrate risk measures to real world data. As the industry standard VaR and its coherent counterpart AVaR are law-invariant risk measures, the main goal for an implementation of (A)VaR is to find a good estimate of the profit-and-loss distribution in the relevant region. In this field, the major class of estimation methods comprise the historical simulation method, methods based on Gaussian distribution assumptions and methods based on Extreme Value Theory (EVT). We refer to McNeil et al. (2005), in particular Chapter 2 and Chapter 7, for a detailed account and references to methods of profit-and-loss distribution estimation. More background on extreme value theory can be found in the monograph Embrechts et al. (1997). McNeil and Frey (2000) propose an implementation of VaR and AVaR that is based on an estimation of the log-returns distribution using a combination of a GARCH model fit and an EVT approach for the residuals. Their method proceeds in a two-step scheme: first, the GARCH model mimics the inherent stochastic volatility of financial time series, and the GARCH parameters are estimated by a pseudo maximum likelihod method. Second, they adopt a Peaks-over-Threshold (POT) approach to the residuals and only consider those residuals that exceed a critical value. The POT method justifies fitting a Generalized Pareto distribution (GPD) by means of a maximum likelihood method (e.g. Embrechts et al. (1997), Section 3.4 and Section 6.5) It is also in accord with the typically high confidence levels that are imposed on (A)VaR to zoom into the extreme branch of losses. Applying the POT method to the residuals rather than directly to the log-returns has the advantage that the fitting procedure to the extremes only needs to be applied once due to the white noise property of the residuals. Using these two steps, McNeil and Frey (2000) succeed to estimate (A)VaR by fitting a distribution that adequately accounts for the extremes in the tail and under mild conditions allows for closed form formulas for VaR and AVaR.

The goal of our paper is to incorporate dynamic time-consistency for VaR and AVaR. We investigate the extension of static risk measures to dynamic counterparts that satisfy time-consistency. A key property to succeed in this transfer is the dynamic programming principle, see Cheridito and Stadje (2009), Cheridito and Kupper (2011).

The two-step estimation scheme from McNeil and Frey (2000) using GARCH and EVT allows us to derive a closed form expression for the dynamic time-consistent VaR that is easily implemented using the estimated GPD and the GARCH parameters. For AVaR however, such a closed form expression cannot be obtained and we derive closed form lower and upper approximations to AVaR. On top of being more conservative than their static counterparts, the dynamic time-consistent VaR offers the benefit that the risk measurement of aggregated losses, which in e.g. McNeil and Frey (2000) have to be estimated by simulation methods, can now be estimated in a (semi-)closed way by simply aggregating the VaRs of the single positions at different future time points.

The paper is structured as follows. In Section 2 we present preliminaries on dynamic risk measures along with the dynamic programming principle characterization. Moreover, we introduce the GARCH loss model, which establishes the model framework for the entire paper. In Section 3 we apply the new methodology from the previous section to derive a closed form expression for the time-consistent VaR and investigate its properties concerning the evolution over time and prove the linearization of aggregated losses. Section 4 is devoted to the study of AVaR. Since a closed form expression for time-consistent AVaR is not possible, as an alternative, we derive closed form expressions for pragmatic bounds to AVaR and study the properties as in the previous section. The proofs of the results of Sections 3 and 4 are postponed to the Appendix. In the last Section 5 we give a rehash on the part of extreme value theory that is relevant for our purpose, and apply our results to a data set of stock prices.

2 Conditional risk measures

Given a probability space we consider a filtration where . We denote by with the set of all -measurable random variables . In this paper, the space represents the space of all financial positions for which we need a risk assessment. Typically, we will be interested in losses, i.e. the negatives of log-returns of financial data.

Since conditional risk measures are random variables, all properties, equalities and inequalities below hold almost surely with respect to , and we assume this throughout without making extra mention of it.

Definition 2.1.

For a family of mappings with is a dynamic monetary risk measure if it satisfies the following properties:

-

(i)

Normalization: for ;

-

(ii)

Monotonicity: for all such that , for ;

-

(iii)

Translation invariance: for all and , for .

If represents the space of all profit and loss variables, the above definition leads to the notion of a dynamic monetary utility function, see Definition 2.1 in Cheridito and Kupper (2011). If a dynamic monetary risk measure satisfies in addition to Definition 2.1 (i)-(iii)

-

•

Positive homogeneity: for all and , for ;

-

•

Subadditivity: for all , for ,

then we say that is a coherent (dynamic monetary) risk measure.

Definition 2.2.

A dynamic monetary risk measure is time-consistent if

for all , for .

The following useful characterization of time-consistency can be found in Cheridito and Kupper (2011).

Proposition 2.3.

A dynamic monetary risk measure is time-consistent if and only if it satisfies the Bellman principle

| (2.1) |

for all , and .

It has been noted in Cheridito and Stadje (2009) and Cheridito and Kupper (2011) that there is another way to construct time-consistent dynamic risk measures: let be an arbitrary dynamic monetary risk measure

then the backward iteration

| (2.2) |

defines a process which by definition is a time-consistent dynamic risk measure. The following property is a straightforward consequence of the construction of .

Corollary 2.4.

For we have for

| (2.3) |

For a coherent risk measure , its subadditivity property implies that for any fixed and such that and any for we have

| (2.4) |

We construct our time-consistent dynamic risk measures by backwards iteration.

2.1 The GARCH(1,1) model for loss positions

Recall that we are interested in the risk assessment of losses. The focus of this paper is on a particular class of loss processes : its dynamics is governed by a GARCH(1,1) process and typically represent (negative) log-returns. It holds that satisfies

| (2.5) | ||||

where are the model parameters, and are -measurable initial random variables, and is a strict white noise process (independently identically distributed with zero mean and unit variance). Note also that by (2.5) is measurable with respect to for every .

We denote by and the distribution function and the left-continuous quantile function of each , respectively; i.e.,

| (2.6) |

For properties of the quantile function we refer to Resnick (1987), Section 0.2, or Embrechts et al. (1997), Proposition A1.6.

We assume that is strictly increasing, thus is continuous, and that the right endpoint of is infinite; i.e.,

If necessary we identify with . Since has infinite right endpoint, and is close to 1, is as a rule positive. We shall also need the quantile function of and note that for symmetric, . Note further that for , hence (for )

| (2.7) |

We summarize the assumptions which we will assume throughout the paper.

Assumptions A: We assume that is strictly increasing with support and that .

For simplicity, we also assume that is symmetric.

Since we often work with distribution tails, we note that can also be represented as

| (2.8) |

3 Conditional time-consistent Value-at-Risk

In this section we study Value-at-Risk (VaR) in the framework of dynamic time-consistent risk measures. One typically considers which represents a possibly large loss position, for which the probability of exceeding a loss threshold should be bounded by a small probability , i.e. is typically close to . The smallest loss threshold which satisfies this bound is the . Several versions of the (conditional) VaR definition can be found in the literature. In analogy to (2.8) we work throughout with the following, which caters best to the purpose of the treatments in this paper.

Definition 3.1.

Given a loss position the Value-at-Risk at level at time for is defined by

| (3.1) |

3.1 Time-consistent VaR for single day losses

We start this section with the following example, which is the core object of interest in McNeil and Frey (2000).

Example 3.2.

There are examples showing that Value-at-Risk from Definition 3.1 is not time-consistent (e.g. Cheridito and Stadje (2009) or Föllmer and Schied (2011, Example 11.13)). As the GARCH model (2.5) is defined by an iteration, one could hope that for this specific model is time-consistent. However, this is not true and we provide a counterexample, which makes use of Proposition 2.3.

Example 3.3.

In order to see why in the framework of GARCH losses VaR cannot be time-consistent, recall that according to Proposition 2.3 is time-consistent if and only if it satisfies the dynamic programming principle

For , by (3.2), we have and, hence,

We compute and for the GARCH model:

Since the function is strictly increasing in and -measurable, we obtain

| (3.4) |

Next we compute

Now assume that for all . We denote by the conditional probability with respect to and calculate

Now note for the first integral that decreases in to 0 and has minimum 1 over the integral range. This implies for the probability under the integral, that the left-hand random variable scaled by decreases with to . Moreover, since the support of has infinite right endpoint, the second integral is positive. Hence, we estimate the right-hand side by

where . However, for close to 1 we have .

Cheridito and Stadje (2009) propose to amend the time-inconsistency of VaR using the backward iteration (2.2). This gives rise to the following definition.

Definition 3.4.

Given a loss position and from Definition 3.1. Then the time-consistent Value-at-Risk at level for is defined by

| (3.5) |

In the notation of the construction from the recursion (2.2), this corresponds to and . As a consequence of the construction of we find for

| (3.6) |

The choice of the GARCH model (2.5) entails the convenient feature that the -day ahead VaR assessment allows for a closed form solution. More precisely, we can derive an analytical solution for the time risk assessment of the GARCH(1,1) loss at terminal time as follows (as usual we set ). The proof is given in Appendix A.

Theorem 3.5.

Let be the loss process given by the GARCH(1,1) model (2.5). Then we have

| (3.7) |

where is an -measurable mapping given by

| (3.8) |

3.2 Time-consistent VaR for aggregated losses

We now come to the computation of the -day-ahead . So far, we have considered risk positions at a fixed day that is ahead of time up to which information in the form of the filtration is available. The -day-ahead is a risk assessment of aggregated losses from the time period for . Next we show that linearizes across the aggregation of GARCH losses.

Proposition 3.6.

Let be the loss process given by the GARCH(1,1) model (2.5), then we have for fixed and such that ,

| (3.9) |

Proof.

First note that for we know from (3.3) that

where the second line follows from (3.2). By (2.5) we have which transforms the last equation into

By the definition of and the fact that is a strictly increasing -measurable function of , we find that

| (3.10) |

which is equal to the sum and also equal to the corresponding sum in the center. We proceed by induction and assume that (3.9) is true for . Since the sum is -measurable, we obtain by (3.6)

where the last identity follows by the induction hypothesis, which also implies

We use from (2.5) and observe that

is a strictly increasing function in . Hence we can proceed by the same argument as in the pretext leading to (3.10) to achieve ultimately

This finishes the proof. ∎

4 Conditional time-consistent Average Value-at-Risk

This section is devoted to the study of time-consistent alternatives for the Average Value-at-Risk (AVaR). Due to coherence AVaR is commonly considered as a more reasonable rectification of VaR. For more details we refer to Föllmer and Schied (2011, Chapter 4). For we define as the set of all -integrable losses, where denotes the conditional probability with respect to and the corresponding conditional expectation. The following definition relates AVaR to VaR.

Definition 4.1.

Given a loss position the Average Value-at-Risk at level at time is given by

| (4.1) |

with as in Definition 3.1.

Whereas VaR quantifies the risk associated to one particular level of risk, reflected in the choice of , AVaR as an integrated VaR takes into account VaR at the entire bandwidth of risk levels between and and thus better reflects volume of extreme risks that VaR might neglect.

The following is the analog of a fact well-known for unconditional AVaR (e.g. Lemma 2.16 of McNeil et al. (2005)).

Remark 4.2.

If the loss position has a continuous distribution function, then

| (4.2) |

Due to (4.2), AVaR is often also referred to as conditional VaR or Expected Shortfall.

Assumption B: Additionally to Assumptions A we require from now on also that has a continuous distribution function.

4.1 Time-consistent AVaR for single day losses

We focus again on the GARCH model from (2.5).

Example 4.3.

Assume the setting as in Example 3.2. For let be given by (2.5). Then is the -day-ahead-AVaR. If the innovations have a continuous distribution function , then by linearity of the conditional expectation and -measurability of we get for ,

This calculation can also be found in McNeil and Frey (2000).

In analogy to Section 3, a time-consistent version of AVaR is constructed as follows.

Definition 4.4.

Given a loss position and the as in Definition 4.1. Then the time-consistent Average Value-at-Risk at level for is defined by

| (4.3) |

For the Average Value-at-Risk of the squared loss at time we can derive an explicit formula similar to (3.7). Note that, though AVaR of allows for an interpretation as the conditonal volatility at time , our purpose of investigation is to employ AVaR of to derive pragmatic bounds to AVaR itself, see Section 4.2 below.

Theorem 4.5.

Let be given by the GARCH(1,1) model (2.5). Then we have for the squared loss at terminal time

| (4.4) |

where is an -measurable mapping given by

It is also possible to derive expressions for day ahead . As usual we define .

Proposition 4.6.

Proof.

For note that by (4.1) as in Example 4.3. For simplicity we set . For we use this and then Lemma B.1 and compute for

| (4.7) | ||||

| (4.8) | ||||

| (4.9) | ||||

since is -measurable. Assume that (4.6) holds for . Then

where

Setting , then since is -measurable, factorization of gives another integral and another factor in the denominator. ∎

4.2 Almost sure bounds for AVaR

Finding an analytical expression for for the (unsquared) GARCH(1,1) loss is not straightforward. It is however possible to derive closed form bounds for .

4.2.1 AVaR-bounds for single day losses

We now derive a closed form upper bound to which arises from an application of Jensen’s inequality. For the proof of the following Proposition we refer to Appendix B.

Proposition 4.7.

An easy alteration of the proof of the previous result yields a closed form lower bound for .

Proposition 4.8.

4.2.2 AVaR-bounds for aggregated losses

Unfortunately, for AVaR there exists no result corresponding to Proposition 3.6, hence AVaR does not linearize across aggregation of GARCH losses. A key obstacle is that Lemma B.1 does not apply. However, due to the subadditivity of AVaR and the property (2.4), we can derive an upper bound for the aggregation of GARCH losses.

Proposition 4.9.

Let be given by the GARCH model (2.5). Then, for and such that , the -day-ahead of aggregated losses is bounded by

| (4.12) |

Proof.

Remark 4.10.

Due to the lack of linearization across aggregation of GARCH losses, the aggregation of the -ahead AVaR bounds from Proposition 4.8 do not produce a proper lower bound for . Whereas in case of the single -day-ahead is a true lower bound to , their aggregation is rather a lower bound to the upper bound . It can happen that is either an upper bound or a lower bound for . Nevertheless, we will use as a weak lower bound in our numerical experiments to get an orientation about how much the upper bound is tailing off.

5 Extreme value theory based quantile estimation

5.1 Generalized Pareto Distribution

Up to now we have not fixed the noise distribution, only assumed certain properties like infinite right endpoint or continuity of the distribution function. Throughout we worked with close to 1 corresponding to the noise distribution function to be close to 1. Thus it is sufficient to specify the distribution function above some high threshold . This is a typical assumption in extreme value theory, and we will apply the Peaks-over-Threshold method (as in McNeil and Frey (2000)). We first explain the setting in general.

The Generalized Pareto distribution (GPD) is given by

| (5.1) |

where and . If (5.1) is defined for and if (5.1) is defined on , see e.g. Section 3.4 in Embrechts et al. (1997). Assume that we fix some high threshold . Given a random variable with distribution function and right endpoint , its associated excess distribution function is defined as

| (5.2) |

The strength of the GPD is compressed in a result by Pickands (1975) and Balkema and de Haan (1974) which classifies the GPD as the limit distribution of a large class of excess distributions. More precisely, under mild conditions there exists a measurable non-negative parameter such that

holds, see Theorem 3.4.13 in Embrechts et al. (1997) for a rigorous statement of this result. The density of (5.1) is given by

| (5.3) |

Under the assumption that has the distribution function , which for some high enough threshold satisfies for and for some and , we find for (for we interpret this quantile as the quantile of the corresponding exponential distribution)

| (5.4) | ||||

| (5.5) |

By (2.7) we obtain

Unfortunately, there is no explicit expression for .

5.2 Statistical model fitting

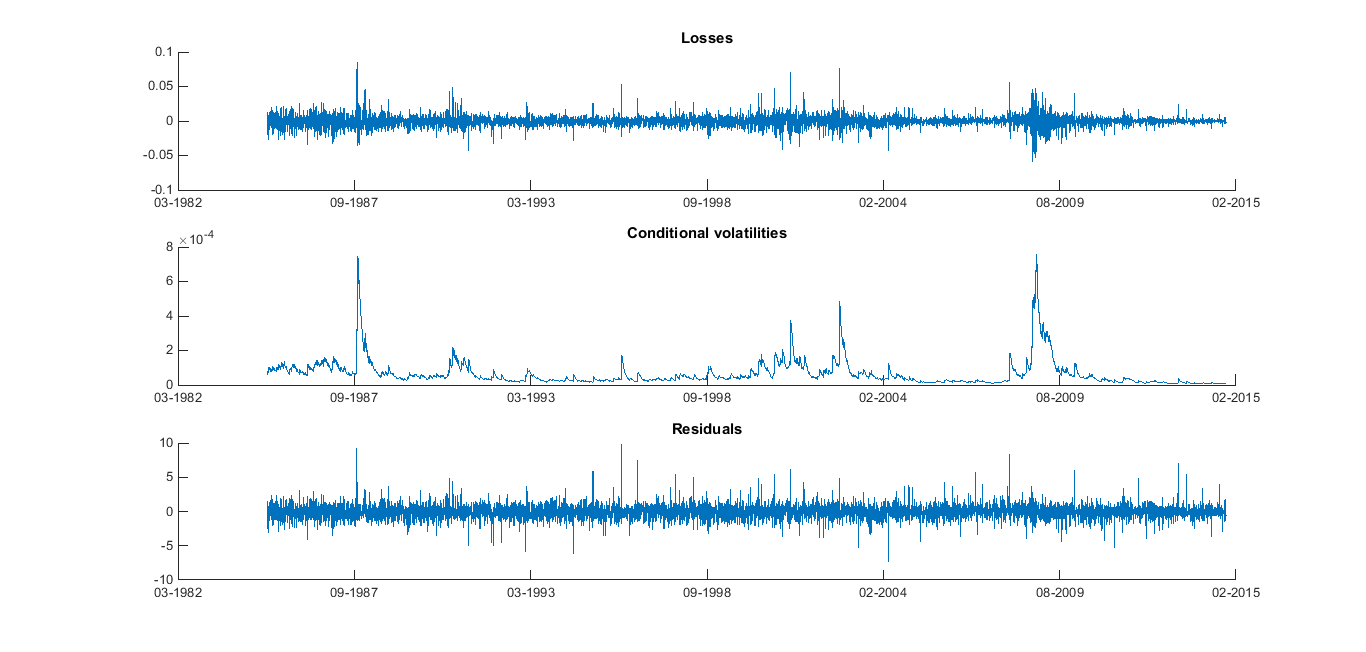

In this section we apply the theory and formulas derived previously to a data set. We choose the historical daily closing prices of the Motorola stock from 1st March 1985 until 15th October 2014 as this data set provides several canonical features of financial time series. We transform prices into negative log-returns; i.e., into losses, and fit the GARCH parameters using Quasi Maximum Likelihood Estimation (QMLE) (e.g. Franq and Zakoian (2010), Chapter 7). The parameter estimates can be found in Table 1, and the outcome is depicted in Figure 1.

| Parameter | Value | Standard error | |

|---|---|---|---|

| 2e-07 | 1.09e-07 | ||

| 0.0451 | 0.0014 | ||

| 0.9531 | 0.0013 |

We see in the middle plot of Figure 1 major clustering of volatility in October 1987 (Black Monday), in a pronounced period between 2000 until 2002 (Dot-com bubble and wake of 9/11 attacks) and in a longer lasting period following the financial crisis between 2008 until 2010.

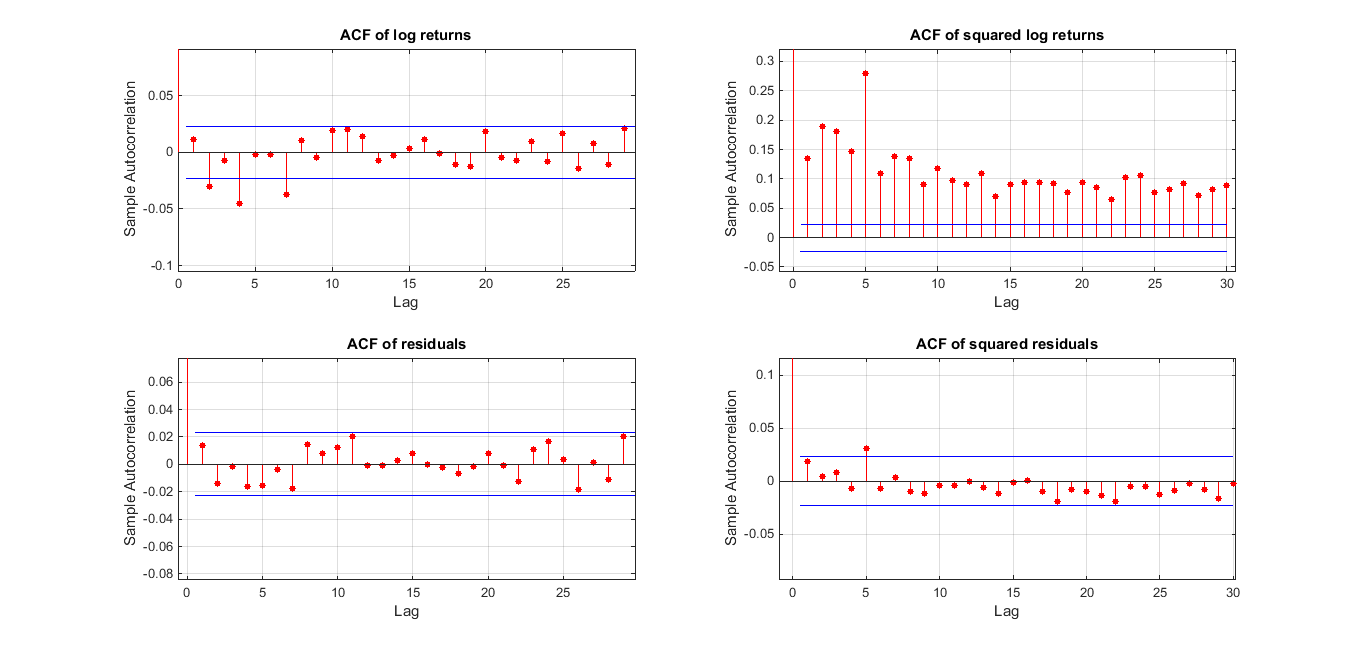

In a next step we examine the sample autocorrelation functions of the loss data and the residuals after fitting a GARCH model. In Figure 2 the bottom plots depict the acf of the residuals and the squared residuals and is supportive for the our assumption of i.i.d. GARCH residuals . This is also reflected in several runs of the Ljung-Box for various lags for the residuals. The residuals also pass the augmented Dickey-Fuller and the KPSS stationarity tests.

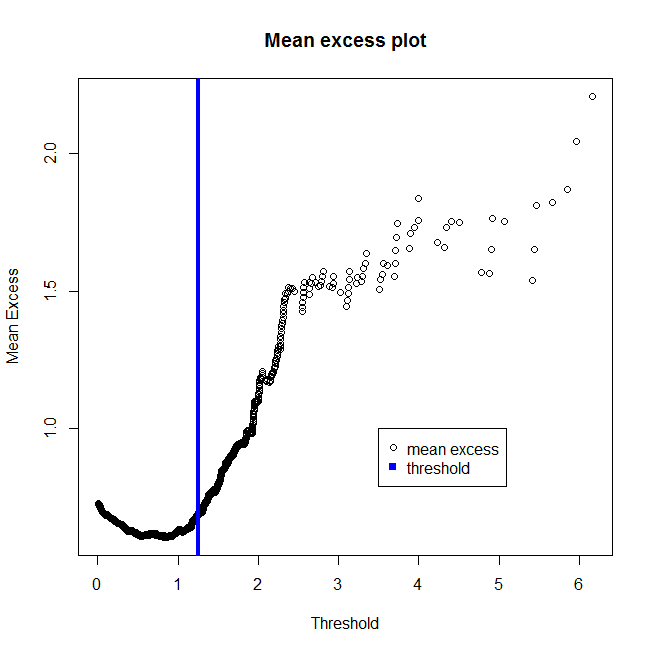

As explained in Section 5.1 we fit a GPD to the upper tail of the residuals. We first have to choose a high enough threshold value and we choose it as the approximate quantile of the residuals. This is supported by studying the mean excess plot of the nonnegative residuals in Figure 3: the quantile of the residuals (solid blue line) yields a threshold which sufficiently marks the beginning of the linear behaviour of the mean excess plot. Since the empirical mean excesses are increasing, we may assume that the shape parameter is positive. This is confirmed by the parameter estimates for and . The Maximum Likelihood Estimators are with a confidence interval and with a confidence interval .

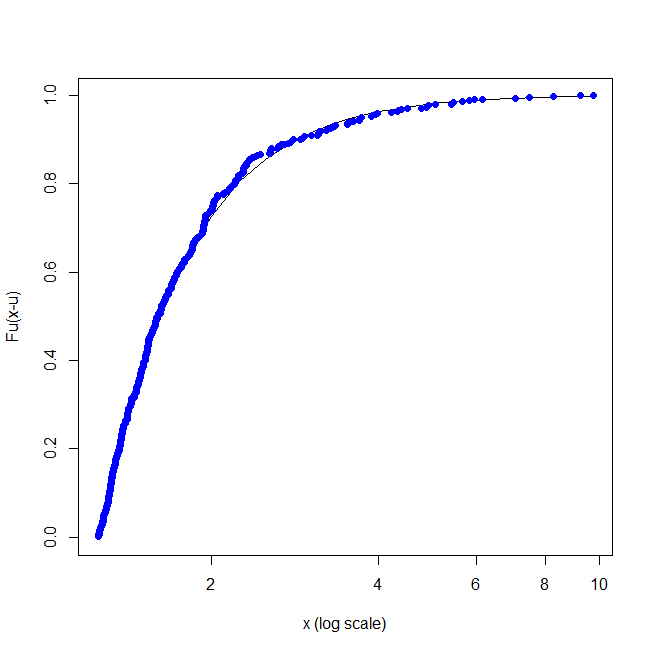

In Figure 3, the right hand plot depicts the GPD fit of the excess distribution superimposed on empirical estimates of excess probabilities. Note how well the GPD model fits to the empirical estimates of the excess probabilities.

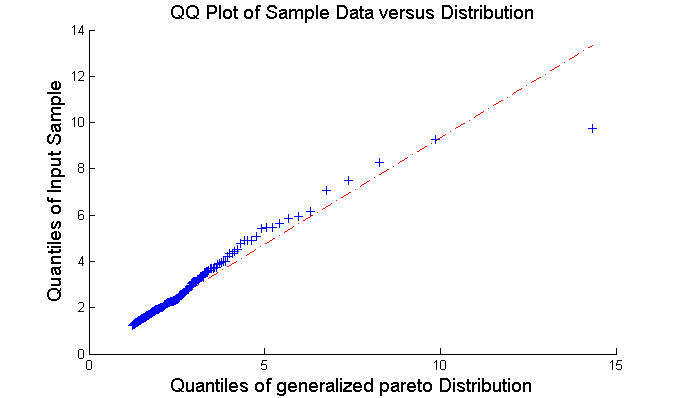

A QQ-plot of the empirical quantiles against the fitted quantiles is depicted in Figure 4. Note again the good correspondence of the fitted GPD with the empirical estimates.

5.3 Fitting time-consistent risk measures to data

5.3.1 Time consistent VaR estimation

In a first step, for a single loss position we compute the -day-ahead time-consistent VaR given by Proposition 3.5 for different levels of ; i.e., we fix and consider for various .

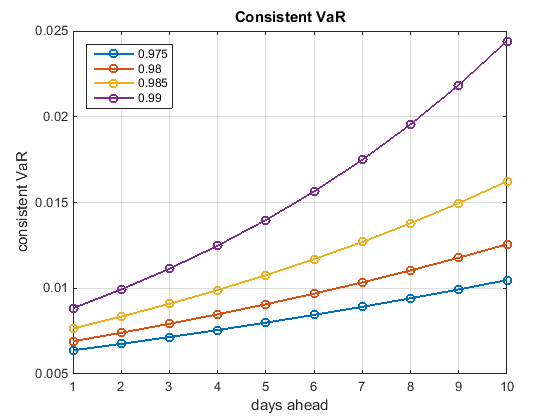

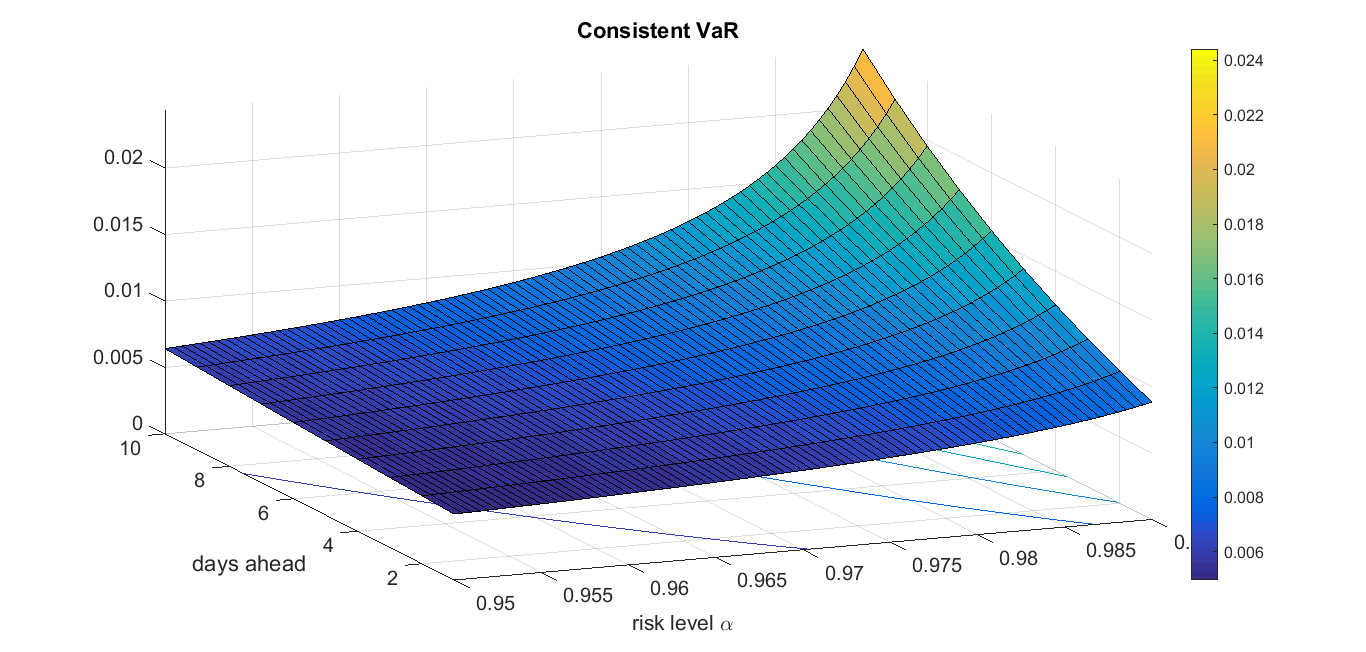

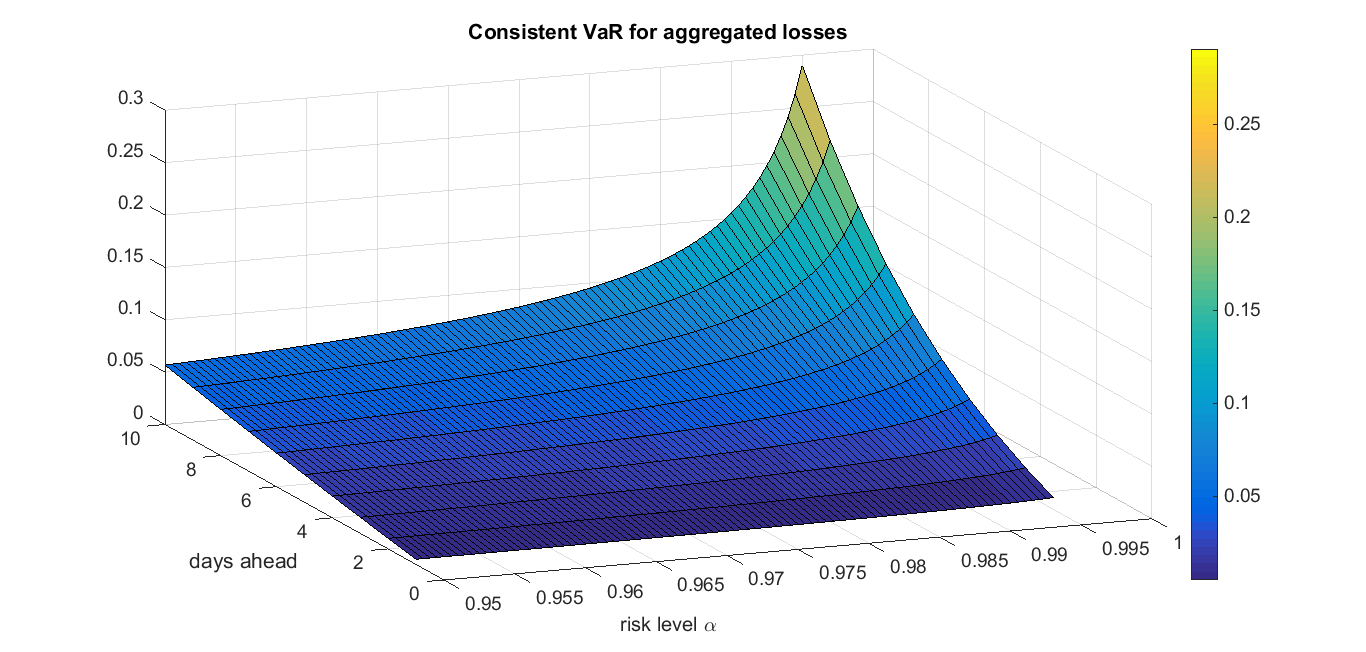

In Figure 5 we plot for .

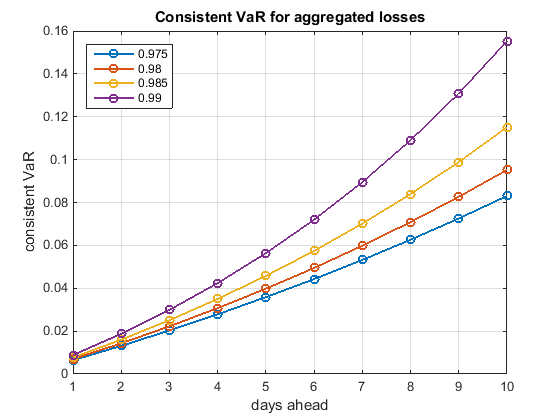

Once the single time consistent risk measures are computed, we simultaneously get the risk measure of the aggregated losses over days from Proposition 3.6 by aggregation; i.e.,

In Figure 6 we plot for . Table 2 shows the values of for single losses and aggregated losses for various levels of and .

| single loss | aggr. loss | |||||||

|---|---|---|---|---|---|---|---|---|

| 97.5% | 98% | 98.5% | 99% | 97.5% | 98% | 98.5% | 99% | |

| 1 | 0.0064 | 0.0069 | 0.0077 | 0.0088 | 0.0064 | 0.0069 | 0.0077 | 0.0088 |

| 2 | 0.0068 | 0.0074 | 0.0083 | 0.0099 | 0.0132 | 0.0143 | 0.0160 | 0.0187 |

| 3 | 0.0072 | 0.0079 | 0.0091 | 0.0111 | 0.0204 | 0.0222 | 0.0251 | 0.0297 |

| 4 | 0.0076 | 0.0085 | 0.0099 | 0.0125 | 0.0280 | 0.0307 | 0.0350 | 0.0422 |

| 5 | 0.0080 | 0.0091 | 0.0108 | 0.0140 | 0.0360 | 0.0398 | 0.0458 | 0.0562 |

| 6 | 0.0084 | 0.0097 | 0.0117 | 0.0156 | 0.0444 | 0.0495 | 0.0575 | 0.0718 |

| 7 | 0.0089 | 0.0103 | 0.0127 | 0.0175 | 0.0533 | 0.0598 | 0.0702 | 0.0893 |

| 8 | 0.0094 | 0.0110 | 0.0138 | 0.0196 | 0.0627 | 0.0708 | 0.0840 | 0.1089 |

| 9 | 0.0099 | 0.0118 | 0.0150 | 0.0218 | 0.0726 | 0.0826 | 0.0990 | 0.1307 |

| 10 | 0.0105 | 0.0126 | 0.0162 | 0.0244 | 0.0831 | 0.0952 | 0.1152 | 0.1551 |

5.3.2 Time consistent AVaR estimation

In a second step, we compute the approximate upper and lower AVaR bounds for single loss position and we compute the -day-ahead for different levels of ; i.e., we fix and consider and for various . The risk measure of the aggregated losses over days we obtain from Propositions 4.7.

| lower | bound | upper | bound | |||||

|---|---|---|---|---|---|---|---|---|

| 97.5% | 98% | 98.5% | 99% | 97.5% | 98% | 98.5% | 99% | |

| 1 | 0.0098 | 0.0106 | 0.0118 | 0.0135 | 0.0098 | 0.0106 | 0.0118 | 0.0135 |

| 2 | 0.0115 | 0.0127 | 0.0145 | 0.0177 | 0.0131 | 0.0146 | 0.0168 | 0.0206 |

| 3 | 0.0134 | 0.0152 | 0.0180 | 0.0231 | 0.0173 | 0.0199 | 0.0239 | 0.0313 |

| 4 | 0.0157 | 0.0182 | 0.0222 | 0.0302 | 0.0230 | 0.0271 | 0.0340 | 0.0475 |

| 5 | 0.0183 | 0.0217 | 0.0275 | 0.0394 | 0.0304 | 0.0370 | 0.0483 | 0.0721 |

| 6 | 0.0214 | 0.0260 | 0.0340 | 0.0515 | 0.0402 | 0.0504 | 0.0686 | 0.1093 |

| 7 | 0.0250 | 0.0311 | 0.0420 | 0.0672 | 0.0532 | 0.0687 | 0.0974 | 0.1658 |

| 8 | 0.0291 | 0.0371 | 0.0520 | 0.0878 | 0.0704 | 0.0936 | 0.1384 | 0.2515 |

| 9 | 0.0340 | 0.0444 | 0.0643 | 0.1146 | 0.0932 | 0.1276 | 0.1966 | 0.3813 |

| 10 | 0.0398 | 0.0531 | 0.0795 | 0.1497 | 0.1232 | 0.1738 | 0.2792 | 0.5783 |

| aggr. | aggr. | |||||||

|---|---|---|---|---|---|---|---|---|

| 97.5% | 98% | 98.5% | 99% | 97.5% | 98% | 98.5% | 99% | |

| 1 | 0.0098 | 0.0106 | 0.0118 | 0.0135 | 0.0098 | 0.0106 | 0.0118 | 0.0135 |

| 2 | 0.0213 | 0.0233 | 0.0263 | 0.0312 | 0.0229 | 0.0252 | 0.0286 | 0.0341 |

| 3 | 0.0347 | 0.0385 | 0.0443 | 0.0543 | 0.0402 | 0.0451 | 0.0525 | 0.0654 |

| 4 | 0.0504 | 0.0567 | 0.0665 | 0.0845 | 0.0632 | 0.0722 | 0.0865 | 0.1129 |

| 5 | 0.0687 | 0.0784 | 0.0940 | 0.1239 | 0.0936 | 0.1092 | 0.1348 | 0.1850 |

| 6 | 0.0901 | 0.1044 | 0.1280 | 0.1754 | 0.1338 | 0.1596 | 0.2034 | 0.2943 |

| 7 | 0.1151 | 0.1355 | 0.1700 | 0.2426 | 0.1870 | 0.2283 | 0.3008 | 0.4601 |

| 8 | 0.1442 | 0.1726 | 0.2220 | 0.3304 | 0.2574 | 0.3219 | 0.4392 | 0.7116 |

| 9 | 0.1782 | 0.2170 | 0.2863 | 0.4450 | 0.3506 | 0.4495 | 0.6358 | 1.0929 |

| 10 | 0.2180 | 0.2701 | 0.3658 | 0.5947 | 0.4738 | 0.6233 | 0.9150 | 1.6712 |

5.4 Conclusions

Obviously, the interpretation for the dynamic time-consistent (A)VaR differs considerably to that of the static (A)VaR: the dynamic (A)VaR evolves via the composition of the static (A)VaR over time. This results in a much more conservative risk measurement as the risky positions that are due far in the future not only enter the risk assessment through their own dynamics at the future maturity but rather enter through their risk assessment along any time point up to maturity. This has the intended effect that risky effects which arise until maturity are cushioned at any time. As one would expect, the higher safety margins are required the more dramatic is the increase of safety capital when more days-ahead risk management is envisioned.

Table 2 contrasts single and aggregated time-consistent VaR values for different and maturities . It shows convincingly, how much higher capital reserves are needed to guarantee uniform safety at the same level over the whole time to maturity. Already at a level of the time-consistent aggregate loss VaR more than doubles from maturity 1 to 2 and multiplies by a factor of more than 12 to maturity 10. There is a high price to pay to safeguard against all uncertainties, which may lie in the far future.

For a comparison recall a standard industry method to estimate a 10-day VaR based on the central limit theorem, or normality of future losses (e.g. McNeil et al. (2010), Section 2.3.4). Recall that the loss from time over the next periods can be written as the sum over the negative returns during this period. If returns are iid with mean zero and variance (or even normally distributed), then this sum is again (approximately) normally distributed with mean zero and variance . This motivates the estimation of the sum of losses over days by the estimation of the 1-day VaR and multiply it by .

Let us compare the values for from Table 2 with this industry standard. We find for a 10-day VaR of (which we have to compare with the time-consistent , which is more than 4 times as large), and for a 10-day VaR of (which we have to compare with the time-consistent , which is more than 5 times as large). One reason for this huge difference is the well-known fact that GARCH losses do not scale with , but scaling depends strongly on the parameters; cf. Franq and Zakoian (2010), Chapter 4. However, this alone does not explain the huge difference between the simple industry standard and the time-consistent VaR for the aggregated losses.

Due to their construction the composed VaR and AVaR for aggregated future losses produce much more conservative reserve requirements than the standard VaR and AVaR for the same level of . As an implication the standard reserving requirement of excessively high levels of like or covering - or -year events may be put to a test taking into consideration reduced levels of , e.g. in the bandwidth . The reduction of such extremely high levels would also be very reasonable from a statistical point of view as lower level quantiles give rise to much more reliable estimators.

Appendix A Proofs of Section 3

Proof of Theorem 3.5 We proceed by backward induction. Firstly, by (3.2), at we have the 1-day-ahead-VaR

which agrees with (3.7) for . Assume that (3.7) holds for all . We have

We denote by the conditional probability with respect to . Note that

Using the definition of the GARCH volatility (2.5) for this can be continued by

Since is -measurable and is independent of we conclude that

This finishes the proof.

Appendix B Proofs of Section 4

We need the following lemma.

Lemma B.1.

For assume that is a -measurable, and strictly increasing mapping. Then we have

In particular,

Proof.

Proof of Theorem 4.5 We apply again backward induction. From (4.1) and Example 4.3 we have

which agrees with (4.4) for . For simplicity we write . Now assume that (4.4) holds for all . Then it remains to prove (4.4) for . We have by (4.1) and (2.5)

We denote , which is a measurable function of , and take the constant out of the expectation, which yields

Now note that by Definition 3.1

We denote by the conditional probability with respect to . We compute further, using the definition of the GARCH volatility (2.5) for

where in the last line we have used that is -measurable and the independence of and . We can thus conclude that

From Lemma B.1 we know that . Hence, it follows from the independence of and that

| (B.1) |

Moreover, we calculate

which in combination with (B.1) yields

This finally amounts to

which proves the assertion.

Proof of Proposition 4.7 A careful proof tracking reveals its similarity to the proof of Theorem 4.5. For simplicity we set and .

At we have which coincides with . Since by Definition and (4.8) and (4.9),

we obtain

by Lemma B.1. An application of Jensen’s inequality yields

We obtain further

which amounts to

This proves for that is an upper bound for .

Now assume that holds true for . We show next that also

To this end notice that

| (B.2) |

Moreover, we have by the induction assumption

By a similar calculation as in the proof of Theorem 4.5 and Lemma B.1, we can see that the above expression simplifies to

where the last line follows from Jensen’s inequality. Note that

which implies

Finally it follows from (B.2) that .

Proof of Proposition 4.8 At , coincides with . At we obtain

For simplicity we write . By continuity of the distribution function inherited from ,

which by Lemma B.1 rewrites as

Using the -measurability of and , we calculate further,

| (B.3) |

Hence, it follows that

This proves for that as in (4.11) is a lower bound for .

Now assume that holds true for . We show next that also

To this end notice that

| (B.4) |

Moreover, we have by the induction assumption

where the last equality follows from Lemma B.1. Then by the same calculation which lead to (B),

this yields together with (B.4),

Acknowledgements

We are grateful to one of the Reviewers and Marcin Pitera, who pointed out some errors in a previous version of this paper.

References

- Artzner et al. (1999) P. Artzner, F. Delbaen, J.-M. Eber, and D. Heath. Coherent measures of risk. Mathematical Finance, 9(3):203–228, 1999.

- Balkema and de Haan (1974) A. A. Balkema and L. de Haan. Residual life time at great age. Annals of Probability, 2:792–804, 1974.

- Bielecki et al. (2015) T. Bielecki, I. Cialenco, and M. Pitera. A unified approach to time consistency of dynamic risk measures and dynamic performance measures in discrete time. arXiv:1409.7028v2[math.PR], 2015.

- Bion-Nadal (2009) J. Bion-Nadal. Time consistent dynamic risk processes. Stochastic Processes and Their Applications, 119(2):633–654, 2009.

- Cheridito and Kupper (2011) P. Cheridito and M. Kupper. Composition of time-consistent dynamic monetary risk measures in discrete time. International Journal of Theoretical and Applied Finance, 14(01):137–162, 2011.

- Cheridito and Stadje (2009) P. Cheridito and M. Stadje. Time-inconsistency of VaR and time-consistent alternatives. Finance Research Letters, 6(1):40–46, 2009.

- Detlefsen and Scandolo (2005) K. Detlefsen and G. Scandolo. Conditional and dynamic convex risk measures. Finance and Stochastics, 9(4):539–561, 2005.

- Embrechts et al. (1997) P. Embrechts, C. Klüppelberg, and T. Mikosch. Modelling Extremal Events for Insurance and Finance. Springer, Berlin, 1997.

- Föllmer and Knispel (2011) H. Föllmer and T. Knispel. Entropic risk measures: Coherence vs. convexity, model ambiguity and robust large deviations. Stochastics and Dynamics, 11(02n03):333–351, 2011.

- Föllmer and Penner (2006) H. Föllmer and I. Penner. Convex risk measures and the dynamics of their penalty functions. Statistics & Decisions, 24(2006(1)):61–96, 2006.

- Föllmer and Schied (2002) H. Föllmer and A. Schied. Convex measures of risk and trading constraints. Finance and Stochastics, 6(4):429–447, 2002.

- Föllmer and Schied (2011) H. Föllmer and A. Schied. Stochastic Finance: An Introduction in Discrete Time. de Gruyter, Berlin, extended edition, 2011.

- Franq and Zakoian (2010) C. Franq and J. Zakoian. GARCH Models: Structure, Statistical Inference and Financial Applications. Wiley, Chichester, 2010.

- McNeil and Frey (2000) A. McNeil and R. Frey. Estimation of tail-related risk measures for heteroscedastic financial time series: an extreme value approach. Journal of Empirical Finance, 7(3):271–300, 2000.

- McNeil et al. (2005) A. McNeil, R. Frey, and P. Embrechts. Quantitative Risk Management: Concepts, Techniques, and Tools. Princeton Series in Finance. Princeton University Press, Princeton, NJ, 2005.

- McNeil et al. (2010) A. J. McNeil, R. Frey, and P. Embrechts. Quantitative Risk Management: Concepts, Techniques, and Tools. Princeton University Press, 2010.

- Peng (2004) S. Peng. Nonlinear expectations, nonlinear evaluations and risk measures. In M. Frittelli and W. Runggaldier, editors, Stochastic Methods in Finance, pages 165–253. Springer, New York, 2004. Lecture Notes in Mathematics, vol. 1856.

- Penner (2007) I. Penner. Dynamic Convex Risk Measures: Time Consistency, Prudence, and Sustainability. PhD thesis, Humboldt-Universität zu Berlin, 2007.

- Pickands (1975) J. Pickands. Statistical inference using extreme order statistics. Annals of Statistics, 3:119–131, 1975.

- Resnick (1987) S. Resnick. Extreme Values, Regular Variation, and Point Processes. Springer, New York, 1987.

- Riedel (2004) F. Riedel. Dynamic coherent risk measures. Stochastic Processes and Their Applications, 112(2):185–200, 2004.

- Roorda and Schumacher (2007) B. Roorda and J. Schumacher. Time consistency conditions for acceptability measures, with an application to tail value at risk. Insurance: Mathematics and Economics, 40(2):209 – 230, 2007.

- Weber (2006) S. Weber. Distribution-invariant risk measures, information, and dynamic consistency. Mathematical Finance, 16(2):419–441, 2006.