Statistical Estimation of Composite Risk Functionals and Risk Optimization Problems

Darinka Dentcheva

Stevens Institute of Technology, Hoboken, NJ 07030, USA; Email: darinka.dentcheva@stevens.eduSpiridon Penev

The University of New South Wales, Sidney, 2052 NSW, Australia; Email: s.penev@unsw.edu.auAndrzej Ruszczyński

Rutgers University, Piscataway, NJ 08854, USA; Email: rusz@rutgers.edu

Abstract

We address the statistical estimation of composite functionals which may be nonlinear in the probability measure. Our study is motivated by the need to estimate coherent measures of risk, which become increasingly popular in finance, insurance, and other areas associated with optimization under uncertainty and risk. We establish central limit formulae for composite risk functionals. Furthermore, we discuss the asymptotic behavior of optimization problems whose objectives are composite risk functionals and we establish a central limit formula of their optimal values when an estimator of the risk functional is used. While the mathematical structures accommodate commonly used coherent measures of risk, they have more general character, which may be of independent interest.

Keywords: Risk Measures Composite Functionals Central Limit Theorem

1 Introduction

Increased interest in the analysis of coherent measures

is motivated by their application as mathematical models of risk quantification in finance and other areas.

This line of research leads to new mathematical problems in convex analysis,

optimization and statistics. The uncertainty in risk assessment is

expressed mathematically as a functional of random variable, which may be nonlinear with respect to the probability measure.

Most frequently, the risk measures of interest in practice arise when we evaluate gains or losses depending on the choice , which represents the control of a decision maker and random quantities, which may be summarized in a random vector . More precisely, we are interested in the functional , which may be optimized under practically relevant restrictions on the decisions . Most frequently, some moments of the random variable are evaluated. However, when models of risk are used, the existing theory of statistical estimation is not always applicable.

Our goal is to address the question of statistical estimation of composite functionals depending on random vectors and their moments. Additionally, we analyse the optimal values of such functionals, when they depend on finite-dimensional decisions within a deterministic compact set. The known coherent measures of risk can be cast in the structures considered here and we shall specialize our results to several classes of popular risk measures. We emphasize however, that the results address composite functionals of more general structure with a potentially wider applicability.

Axiomatic definition of risk measures was first proposed in [18].

The currently accepted definition of a coherent risk measure was introduced in [1] for finite probability spaces and was further extended to more general spaces in [34, 13]. Given a probability space , we consider the set of random variables, defined on it, which have finite -th moments and denote it by . A coherent measure of risk is a convex, monotonically increasing, and positively homogeneous functional , which satisfies the translation equivariant property for all . Here and we assume that represent losses, i.e., smaller realizations are preferred.

Related concepts are introduced in [31, 12].

A measure of risk is called law-invariant, if it depends only on the distribution of the random variable, i.e.,

if for all random variables having the same distribution.

A practically relevant law-invariant coherent measure of risk is

the mean–semideviation of order (see [24, 25], [36, s. 6.2.2]),

defined in the following way:

(1)

where . Note the nonlinearity with respect to the probability measure in formula (1).

Another popular law-invariant coherent measure of risk is the Average Value at Risk at level

(see [30, 26]), which is defined as follows:

(2)

Here, denotes the distribution function of . The reader may consult, for example, [36, Chapter 6] and the references therein, for more detailed discussion of these risk measures and their representation.

The risk measure plays a fundamental role as a building block in the description of every law-invariant coherent risk measure via the Kusuoka representation.

The original result is presented in [20] for

risk measures defined on , with an atomless probability space.

It states that for every law-invariant coherent risk measure , a convex set exists such that for all , it holds

(3)

Here denotes the set of probability measures on the interval .

This result is extended to the setting of spaces with ; see [14],

[27], [28], [36], [9], and the references therein.

The extremal representation of on the right hand side of (2) was used as a motivation in [19] to propose the following higher-moment coherent measures of risk:

(4)

These risk measures are special cases of a more general family considered in [7]; they are also examples of

optimized certainty equivalents of [3].

In the paper [9], the explicit Kusuoka representation for the higher-order risk measures (4) was described by utilising duality theorems from [29]. These risk measures are used for portfolio optimization in [19], where their advantages in

in comparison to the classical mean-variance optimization model of Markowitz ([21, 22]) is demonstrated on examples.

The recent work [23] indicates that if such type of risk measure is used as a risk criterion in European option portfolio optimization, the time evolution of the portfolio is superior to the evolution of a portfolio optimized with respect to the AVaR risk or with respect to the mean-variance optimization model of Markowitz. Similar observations were recently made in [15].

A connection of measures of risk to the utility theories is discussed in the literature. Many of the risk measures of interest can be expressed via optimization of the so-called optimized certainty equivalent [3] for a suitable choice of the utility function. Relations of risk measures to rank-dependent utility functions are given in [13]. In [10], it is established that coherent measures of risk are a numerical representation of certain preference relation defined on the space of bounded quantile functions.

In practical applications, we deal with samples and stochastic models of the underlying random quantities. Therefore, the questions pertaining to statistical estimation of the measures of risk are crucial to the proper use of law-invariant measures of risk.

Several measures of risk have an explicit formula, which can be used as a plug-in estimator, with the original measure replaced by the empirical measure. The empirical quantile is a natural estimator of the Value at Risk. A natural empirical estimator of leads to the use of the -statistic (see [16, 8]).

Furthermore, the Kusuoka representation, as well as the use of distortion functions in insurance has motivated the construction and analysis of empirical estimates of spectral measures of risk using -statistic. We refer to

[16, 6, 17, 4, 37, 2] for more details on this approach.

Some risk measures, such as the tail risk measures of form (4), cannot be estimated via simple explicit formulae but are obtained as a solution of a convex optimization problem with convex constraints. Although asymptotic behavior of optimal values of sample-based expected value models has been investigated before (see [32, Ch. 8], [36, Ch. 5] and the references therein), the existing results do not address models with risk measures.

Our paper is organized as follows. Section 2 contains the key result of our paper, which establishes a central limit formula for a composite risk functional. We provide a characterization of the limiting distribution of the empirical estimators for such functionals. Section 3, contains a central limit formula for risk functionals, which are obtained as a the optimal value of composite functionals.

Section 4 provides asymptotic analysis and central limit formulae for the optimal value of optimization problems which use measures of risk in their objective functions.

We pay special attention to some popular measures and we discuss several illustrative examples in Sections 2,3, and 4. In Section 5, we perform a simple simulation study to assess the accuracy of our approximations. Section 6 concludes.

2 Estimation of composite risk functionals

In the first part of our paper, we focus on functionals of the following form:

where is an -dimensional random vector, , , with and .

Let be the domain of the random variable .

We denote the probability distribution of by .

Given a sample of independent identically distributed observations, we consider the following plug-in empirical estimate of the value of :

Our construction is motivated by the aim to estimate coherent measures of risk from the family of mean–semideviations ([24, 25]).

Example 2.1(Semideviations).

Consider the functional (1)

representing the mean–semideviation of order .

In this case, we have , and

In order to formulate the main theorem of this section, we introduce several relevant quantities.

We define:

Suppose be compact subsets of such that , .

We introduce the notation ,

where is the space of continuous functions on with values in equipped with the usually

supremum norm. The space is equipped with the Euclidean norm and is assumed equipped with the product norm.

We use Hadamard directional derivatives of the functions at points in directions

, i. e.,

For every direction , we define recursively the sequence of vectors:

(5)

Theorem 2.2.

Suppose the following conditions are satisfied:

(i)

for all , and ;

(ii)

For all , the functions , , are Lipschitz continuous:

and .

(iii)

For all , the functions , , are Hadamard directionally differentiable.

Then

where is a zero-mean Brownian process on

. Here is a Brownian process

of dimension on , , and is an -dimensional normal vector. The

covariance function of has the following form:

(6)

Proof.

We define , , and the vector-valued function

with block coordinates

, , and . Similarly, we define with block

coordinates , , and .

Consider the

empirical estimates of the function :

Due to assumptions (i)–(ii), all functions are elements of the space

.

Furthermore, assumptions (i)–(ii) guarantee that the class of functions , , is Donsker,

that is, the following uniform Central Limit Theorem holds (see [38, Ex. 19.7]):

(7)

where is a zero-mean Brownian process on with covariance function

(8)

This fact will allow us to establish asymptotic properties of the sequence .

First, we define a subset of containing all elements for which

, .

We define an operator as follows

By construction the value of is equal to the value of and the value of is equal to the value of .

To derive the limit properties of the sequence we shall use Delta Theorem (see, [33]).

The essence of applying the theorem is in identifying conditions under which a statement about a limit result related to convergence in distribution of a

scaled version of a statistic can be translated into a statement about a convergence in distribution of a scaled version of a transformed statistic

To this end, we have to verify Hadamard directional differentiability of at .

Observe that the point is an element of , because , . Moreover,

due to assumption (ii), the following inequality is true for every :

Recursive application of this inequality demonstrates that

is an interior point of . Therefore, the quotients appearing in the definition of the Hadamard directional derivative

are well defined.

Conditions (ii) and (iii) imply that the functions and are also Hadamard directionally differentiable.

Consider the operator at . Let be a sequence of directions converging in norm to an arbitrary direction , when . For a sequence

and sufficiently large, we have

Consider now the operator

.

By the chain rule for Hadamard directional derivatives we obtain

In this way, we can recursively calculate the Hadamard directional derivatives of the operators

:

(9)

Now the Delta Theorem [33], relation (7), and the Hadamard directional differentiability of at

imply that

(10)

The application of the recursive procedure (9) at and leads to formulae (5).

The covariance structure (6) of follows directly from (8).

∎

We assume that and is a compact interval containing the support of the random variable .

The interval can be defined by choosing so that ; for example may be equal to the diameter of the support of raised to power .

The space is and we take a direction .

Following (5), we calculate

We obtain the expression

(11)

The covariance structure of the process can be determined from (6). The process has the constant covariance function:

It follows that has constant paths.

The third coordinate, has variance equal to . It also follows from (6)

that .

Therefore, and are, in fact, one normal random variable, which we denote by .

Observe that (11) involves only the value of the process at .

The variance of the random variable and its covariance with can be calculated from (6) in a similar way:

where the variance can be calculated in a routine way as a variance of the right hand side of (12),

by substituting the expressions for variances and covariances of , , and .

Remark 2.4.

Following Example 2.3, we could derive the limiting distribution of

for as well. However, the risk measure for enjoys a simpler form and is already analysed in the literature (see, [36, Section 6.5].)

3 Estimation of Risk Measures Representable as Optimal Value of Composite Functional

As an extension of the methods of section 2,

we consider the following general setting. Functions , , and a random vector in are given. Our intention is to estimate the value of a composite risk functional

(13)

where is a nonempty compact set.

We note that the compactness restriction is made for technical convenience and can be relaxed.

Let be a random iid sample from the probability distribution of .

We construct the empirical estimate

Our intention is to analyze the asymptotic behavior of , as .

Following the method of section 2,

we define the mapping as follows:

The space is equipped with the product norm of the euclidian norm on and the supremum norm on

. We also define the functional ,

(14)

Setting

we see that

Let denote for the set of optimal solutions of problem (13).

Theorem 3.1.

In addition to the general assumptions, suppose the following conditions are satisfied:

(i)

The function is measurable for all ;

(ii)

The function is differentiable for all ,

and both and its derivative with respect to the second argument, ,

are continuous with respect to both arguments;

(iii)

An integrable function exists such that

for all and all ; moreover,

.

Then

(15)

where is a zero-mean Brownian process on with the covariance function

(16)

Proof.

Observe that assumptions (i)-(ii) of Theorem 2.2

are satisfied due to the compactness of the set and assumptions (ii)–(iii) of this theorem.

Therefore, formula (7) holds:

The limiting process is a zero-mean Brownian process on with covariance function (16).

Furthermore, due to assumption (ii), the function is continuous. As the set is compact, problem (14) has a nonempty solution set . By virtue of [5, Theorem 4.13], the optimal value function is Hadamard-directionally differentiable at in every direction with

where is the Fréchet derivative of at .

Therefore, we can apply the delta method ([33]) to infer that

Substituting the functional form of , we obtain

where is the Dirac measure at . Application of this operator to the process yields formula (15).

Observe that has continuous paths and the minimum exists.

∎

Corollary 3.2.

If, in addition to conditions of Theorem 3.1, the set contains only one element , then the following

central limit formula holds:

(17)

where is a zero-mean normal vector with the covariance

The following examples show that two notable categories of risk measures fall into the structure (13)

Example 3.3(Average Value at Risk).

Average Value at Risk (2) is one of the most popular and most basic coherent measure of risk. Recall that

for a random variable , it is representable as follows:

This measure fits in the structure (13) by setting

The plug-in empirical estimators of (2) have the following form

If the support of the distribution of is bounded, then so is the support of all empirical

distributions and we can assume that the contains the support of the distribution.

Observe that all assumptions of Theorem 3.1 are satisfied. If the distribution function of the random variable is continuous at , then the solution of the optimization problem at the right-hand side of (2) is unique. In that case, also the assumptions of Corollary 3.2 are satisfied.

We conclude that

where is a normal random variable with zero mean and variance

We note that the assumption of bounded support of the random variable is not really essential because, we could take a sufficiently large set , which would contain the corresponding quantile of the distribution function of and all empirical quantiles for sufficiently large sample sizes.

Additionally, we refer to another method for estimating the average value at risk at all levels simultaneously, which is discussed in [8], where also central limit formulae under different set of assumptions are established.

Example 3.4(Higher-order Inverse Risk Measures).

Consider a higher order inverse risk measure (4) with :

(18)

where and is the norm in the space.

We define:

If the support of the distribution of is bounded, so is the support of all empirical

distributions. In this case, we can find a bounded set (albeit larger than the support of )

such that all solutions of problems (18) belong to this set.

For and problem (18) has a unique solution, which we denote by .

The plug-in empirical estimators of (18) have the following form

(19)

Observe that all assumptions of Theorem 3.1 and Corollary 3.2 are satisfied. We conclude that

(20)

where is a normal random variable with zero mean and variance

4 Estimation of Optimized Composite Risk Functionals

In this section, we are concerned with optimization problems in which the objective function is a composite risk functional. Our goal is to establish a central limit formula for the optimal value of such problems.

Our methods allow for the analysis of more complicated structures of optimized risk functionals:

(21)

Here is a -dimensional random vector, , , with and .

We assume that is a compact set in a finite dimensional space and

the optimal solution of this problem is unique.

We define the functions:

and the quantities

We assume that compact sets are selected

so that , and , .

Let us define the space

where is the space of -valued continuous functions on ,

which are differentiable with respect to the second argument with continuous derivatives on .

We denote the Jacobian of with respect to the second argument at by .

For every direction , we define recursively the sequence of vectors:

(22)

The empirical estimator is

We establish the following result.

Theorem 4.1.

Suppose the following conditions are satisfied:

(i)

for all , , , and

for all ;

(ii)

The functions , , and are Lipschitz continuous for every :

for all , ; moreover, , ;

(iii)

The functions , , are continuously differentiable

for every , ; moreover, their derivatives are continuous with respect to the first two arguments.

Then

where is a zero-mean Brownian process on

. Here is a Brownian process

of dimension on , , and is an -dimensional normal vector.

The covariance function of has the following form

(23)

Proof.

We follow the main line of argument of the proof of Theorem 2.2.

We define and the vector-valued function

with block coordinates

, , and . Similarly, we define with block

coordinates , , and .

Consider the

empirical estimates of the function :

Due to our assumptions, for sufficiently large all these functions are elements of the space .

Owing to assumptions (i)–(ii), the class of functions , , , is Donsker,

that is the following uniform Central Limit Theorem holds (see [38, Ex. 19.7]):

(24)

where is a zero-mean Brownian process on with covariance function

(25)

This fact will allow us to establish asymptotic properties of the sequence .

We define an operator as follows

By definition,

To apply Delta Theorem to the sequence , we have to verify Hadamard directional differentiability of the optimal value function at . Observe that our assumptions imply that

the conditions of [5, Thm. 4.13] are satisfied. As the optimal solution set is a singleton,

the function is differentiable at with the Fréchet derivative

where is the Fréchet derivative of at .

The remaining derivations are identical as those in the proof of Theorem 2.2. We only need

substitute as an additional argument of all functions involved.

∎

Example 4.2(Optimization problems with mean–semideviation).

Consider now an optimization problem involving a mean–semideviation measure of risk

(26)

where .

We have

and

We assume that .

Suppose is the unique solution of problem (26).

We set .

Then and .

Following (22), we calculate

We obtain the expression

(27)

The covariance structure of the process can be determined from (25), similar to Example 2.3.

The process has the constant covariance function:

The third coordinate, has variance equal to .

Also,

and thus

and have the same normal distribution and are perfectly correlated.

The variance function of and its covariance with (and ) can be calculated in a similar way:

We conclude that

where the variance can be calculated in a routine way as a variance of the right hand side of (27),

by substituting the expressions for variances and covariances of , , and .

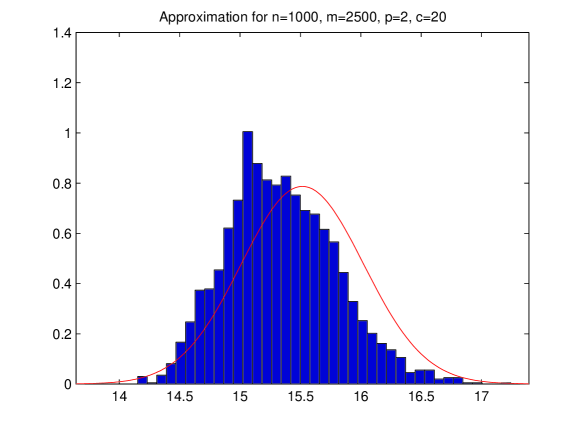

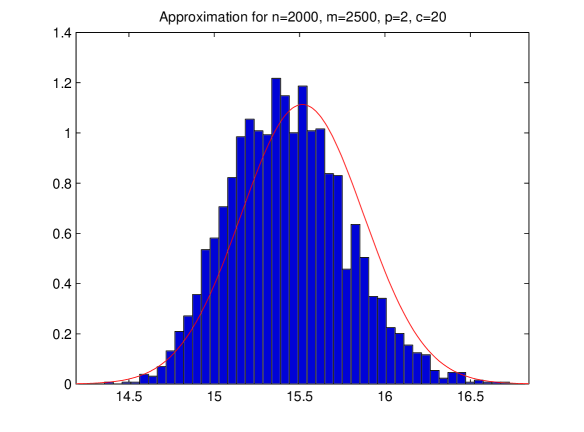

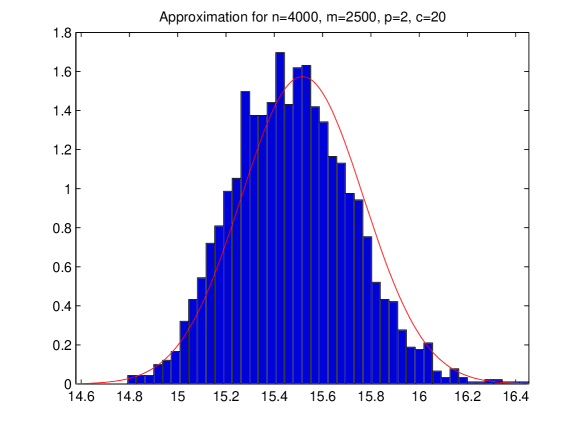

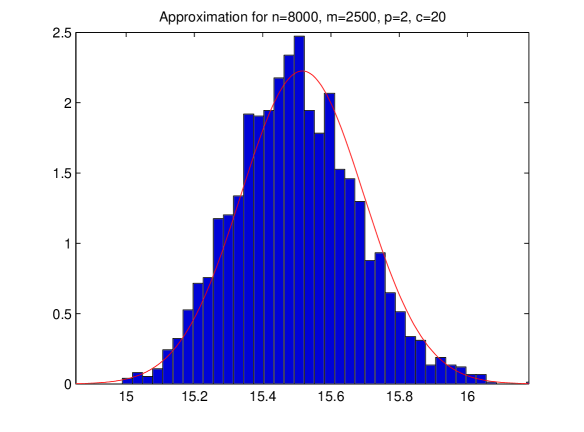

5 A simulation study

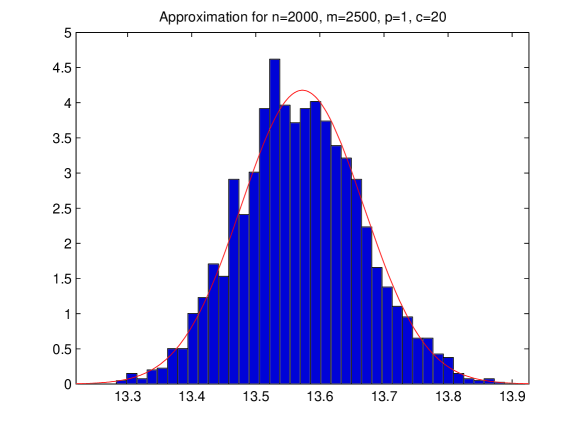

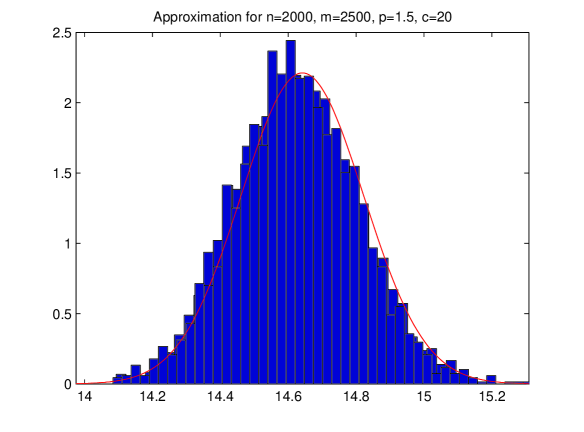

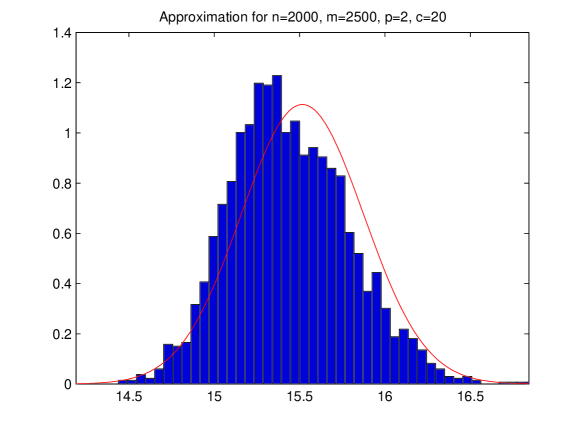

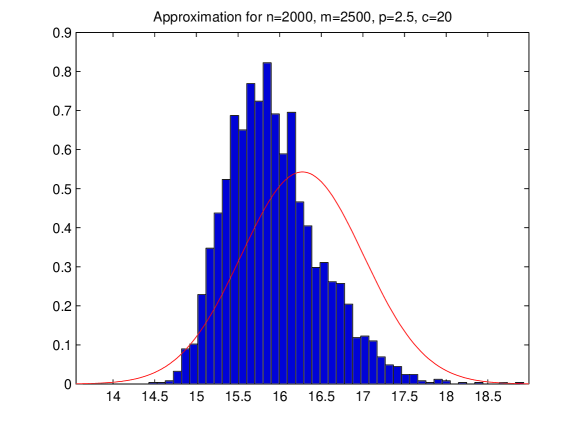

In this section we illustrate the convergence of some estimators discussed in this paper to the limiting normal distribution. Many previously known results for the case have been investigated thoroughly in the literature (see, e.g., [35]) and we will not dwell upon these here. We will only illustrate the case about Higher-order Inverse Risk Measures as discussed in Example 4 for the case

More specifically, we take independent identically distributed observations from an independent identically distributed observations. We take and

In that case Numerical calculation in Matlab delivers the theoretical argument minimum and the value of the risk in (18) being The standard deviation of the random variable in the right hand side of (20) is 16.032. The plug-in estimator of this risk can be represented as a solution of a convex optimization problem with convex constraints and hence a unique solution can be found by any package that solves such type of problems. We have used the cvx package that can be operated within matlab.

Denoting and putting all in a vector d we

can rewrite our optimization problem as follows:

(28)

subject to

The numerical solution to this optimization problem gives us the estimator To get an idea about the speed of convergence to the limiting distribution in (19) we simulate risk estimators for a given sample size and draw their histogram. The number of bins for the histogram is determined by the rough “squared root of the sample size” rule. This histogram is superimposed to the density. As is increased, our theory suggests that the histogram and the normal density graph will look more and more similar in shape. Their closeness indicates how quickly the central limit theorem pops up in this case.

(a)

(b)

(c)

(d)

Figure 1: Density histogram of the distribution of the estimator for increasing values of and its normal approximation using Theorem 2 and

(a)

(b)

(c)

(d)

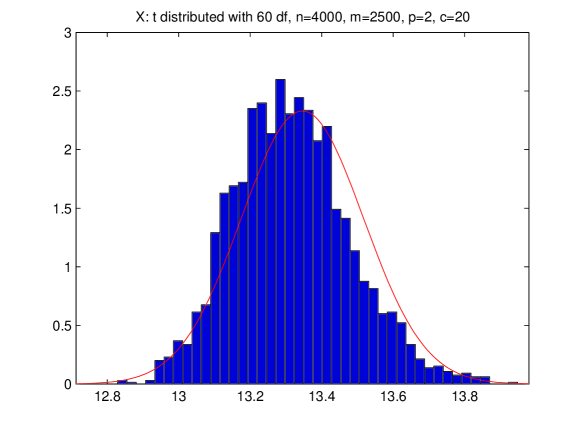

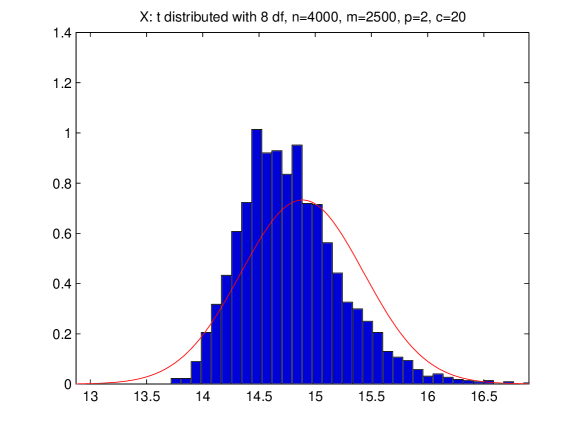

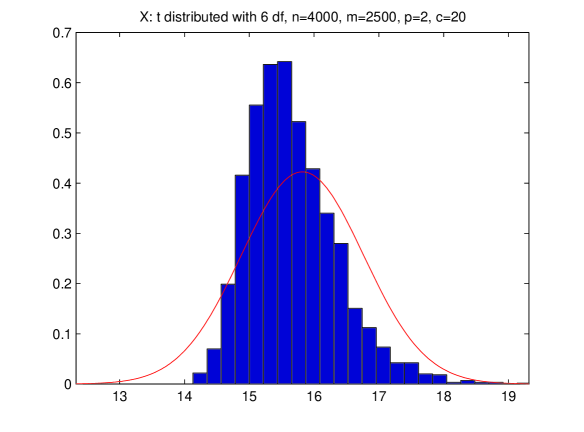

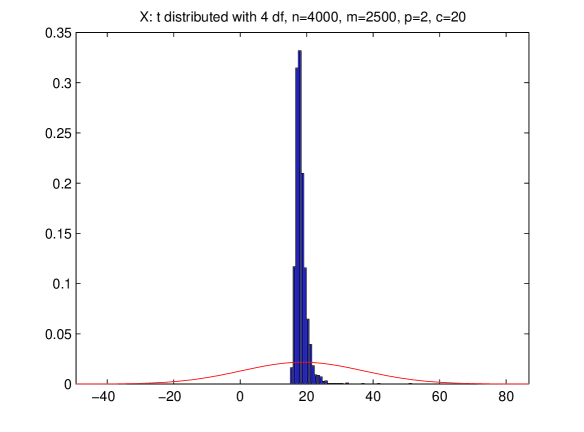

Figure 2: Density histogram of the distribution of the estimator for and with being 60, 8, 6 and 4.

(a)

(b)

(c)

(d)

Figure 3: Density histogram of the distribution of the estimator for different values of when

Figure 1 shows that the central limit theorem indeed represents a very good approximation which improves significantly with increasing sample size. The small downward

bias that appears in Figure 1 a) is getting increasingly irrelevant with growing sample size. We have experimented with different values of such as and and we have also changed the value of (respectively ). The tendency shown in Figure 1 is largely upheld, however, as expected, the standard errors are increased when and/or is increased. Also, the limiting normal approximation seems to be more accurate for the same sample sizes when a smaller value of is used. This discussed effect is illustrated on Figure 3 where (i.e., the case of AVaR), (where a different sample in comparison to the sample in Figure 1,) and was simulated). The remaining quantities have been kept fixed to and

We stress that increasing the sample size in Figure 3 d) makes the histogram look much more like the limiting normal curve so that the discrepancy observed there is indeed just due to the limiting approximation popping up at larger samples when is increased.

We also experimented with different distributions for the random variable We took specifically -distributions with degrees of freedom such as 4, 6, 8 and 60, shifted to have the same mean of 10 like in the normal simulated data. The results of this comparison for and are shown in Figure 2. The variances of the -distributed variables, being equal to are finite and even smaller than the variance of the normal random variable in Figure 1. However the heavier tails of the distribution adversely affect the quality of the approximation. Despite the fact that the limiting distribution of the risk estimator is still normal when and the heavy tailed data cause the normal approximation to be relatively poor even at The case is closer to normal distribution and hence the approximation works better in this case.

Note that the limiting distribution when involves the fourth moment of the distribution and this moment is finite for and but is infinite when As a result, it can be seen from Figure 2 d) that the normal approximation collapses in this case. Also, Figure 2 shows that for attaining similar quality in Kolmogorov metric for the asymptotic approximation like in the case of normally distributed in Figure 1 c), much bigger samples are needed. For the fixed sample size of 4000, the quality of the normal approximation worsens as decreases from 60 to 8 and then to 6. Furthermore, and outside of the scope of the present paper, we note that if the distribution of has even heavier tails than the distribution with (for example, if it is in the class of stable distributions

with stability parameter in the range (1,2)) then the limiting distribution of the risk may not be normal at all.

6 Conclusions

The infinity dimensional delta method is a standard statistical technique to evaluate the asymptotic distribution of estimators of statistical functionals. The applicability of the procedure hinges on veryfing smoothness conditions of the related functionals. Motivated primarily by the need to estimate coherent risk measures we introduce a general composite structure for such functionals in in which all known coherent risk measures can be cast. The potential applicability of our central limit theorems however extends beyond functionals representing coherent risk measures. Our short simulation study indicates that the central limit theorem-type approximations are very accurate when the sample size is large, is in reasonable limits between 1 and 3 and the distribution of is with not too heavy tails. We note that for smaller sample sizes, the technique of concentration inequalities may be more powerful and accurate when evaluating the closeness of the approximation. It is possible to derive concentration inequalities for estimators of statistical functionals with the structure that has been introduced in our paper. This is a subject of ongoing research.

Acknowledgements

The first author was partially supported by the NSF grant DMS-1311978.

The second author was partially supported by a research grant PS27205 of The University of New South Wales.

The third author was partially supported by the NSF grant DMS-1312016.

References

[1]

Artzner, P., Delbaen, F., Eber, J.-M., and Heath D. (1999)

Coherent measures of risk, Mathematical Finance, 9, 203–228.

[2]

Belomestny, D. and Krätschmer, V. (2012) Central limit theorems for

law-invariant coherent risk measures, Journal of Applied Probabability, 49 (1), 1–-21.

[3] Ben-Tal, A. , Teboulle, M. (2007) An old-new concept of risk measures: the optimized certainty equivalent. Mathematical Finance, 17, 3, 449-476.

[4]

Beutner, E. and Zähle, H., (2010) A modified functional

delta method and its application to the estimation of risk functionals.

Journal of Multivariate Analysis, 101 (10), 2452–2463.

[5]

Bonnans, J. F. and Shapiro, A. (2000) Perturbation Analysis of Optimization Problems,

Springer, New York.

[6]

Brazauskas, V., Jones, B.L., Puri, M.L., and Zitikis, R. (2008) Estimating conditional tail expectation

with actuarial applications in view. Journal of Statistical Planning

and Inference 138 (11), 3590–3604.

[7]

Cheridito, P. and Li, T. H. (2009)

Risk measures on Orlicz hearts, Mathematical Finance, 19, 189–214.

[8]

Dentcheva, D. and Penev, S. (2010)

Shape-restricted inference for Lorenz curves using duality theory,

Statistics & Probability Letters, 80, 403–412.

[9]

Dentcheva, D., Penev, S., and A. Ruszczyński (2010) Kusuoka representation of higher order dual risk measures. Annals of Operations Research. 181, 325–335.

[10]

Dentcheva, D, and A. Ruszczyński, (2014) Risk preferences on the space of quantile , Mathematical Programming, 148 (1–2),

181–200.

[11]

Dentcheva, D., G. J. Stock, G. J. and Rekeda, L., Mean-risk tests of stochastic dominance, Statistics & Decisions 28 (2011) 97-118.

[12]

Föllmer, H. and Schied, A. (2002), Convex measures of risk and trading constraints,

Finance and Stochastics, 6, 429–447.

[13]

Föllmer, H., and A. Schied (2011),

Stochastic Finance. An Introduction in Discrete Time, Third Edition,

de Gruyter, Berlin.

[14]

Frittelli, M. and Rosazza Gianin, E. (2005).

Law invariant convex risk measures.

In Advances in mathematical economics. Volume 7, volume 7 of

Adv. Math. Econ., pages 33–46. Springer, Tokyo.

[15]

Gülten, S. and Ruszczyński, A. (2014),

Two-Stage Portfolio Optimization with Higher-Order Conditional Measures of Risk, submitted for publication.

[16]

Jones, B. L. and Zitikis, R. (2003)

Empirical estimation of risk measures and related quantities, North American

Actuarial Journal 7 (4), 44–54.

[17]

Jones, B. L. and Zitikis, R. (2007), Risk measures, distortion

parameters, and their empirical estimation. Insurance : Mathematics

and Economics 41 (2), 279–297.

[18]

Kijima, M., Ohnishi, M. (1993) Mean–risk analysis of risk aversion and wealth effects on optimal portfolios

with multiple investment possibilities, Annals of Operations Research, 45, 147–163.

[19]

Krokhmal, P. (2007) Higher moment coherent risk measures,

Quantitative Finance 7 373-387.

[20]

Kusuoka, S. (2001) On law invariant coherent risk measures,

Adv. Math. Econ., 3 , 83–95.

[21]

Markowitz, H. M. (1952)

Portfolio selection,

Journal of Finance, 7, 77–91.

[22]

Markowitz, H. M. (1987)

Mean–Variance Analysis in Portfolio Choice and Capital Markets,

Blackwell, Oxford, 1987.

[23]

Matmoura, Y. and Penev, S. (2013) Multistage optimization of option portfolio using higher order coherent risk measures. European Journal fo Operational research, 227, 190–198.

[24]

Ogryczak, W. and Ruszczyński, A. (1999) From

stochastic dominance to mean-risk models: Semideviations and risk

measures, European Journal of Operational Research, 116, 33–50.

[25]

Ogryczak, W., Ruszczyński, A. (2001)

On consistency of stochastic dominance and mean–semideviation models,

Mathematical Programming, 89, 217–232.

[26]

Ogryczak, W., Ruszczyński, A. (2002), Dual stochastic

dominance and related mean-risk models. SIAM J. Optim., 13, 1, 60-78.

[27]

Pflug, G. and Römisch, W. (2007) Modeling, measuring and managing risk. World Scientific.

[28]

Pflug, G. and Wozabal, N., (2010) Asymptotic distribution of law-invariant risk functionals. Finance and Stochastics, 14, 397-418.

[29]

Rockafellar, R. T. (1974) Conjugate Duality and Optimization,

CBMS-NSF Regional Conference Series in Applied Mathematics 16

SIAM, Philadelphia.

[30]

Rockafellar, R. T. and Uryasev, S. (2002)

Conditional value-at-risk for general loss distributions.

Journal of Banking and Finance, 26, 1443–1471.

[31]

Rockafellar, R. T., Uryasev, S., Zabarankin, M. (2006) Generalized

deviations in risk analysis, Finance and Stochastics, 10, 51–74.

[32]

Römisch, W. (2005a) Stability of Stochastic Programming Problems, in: Stochastic Programming, A. Ruszczynski, A. Shapiro (Eds.),

Elsevier, Amsterdam.

[33]

Römisch, W. (2005) Delta method, infinite dimensional, Encyclopedia of Statistical Sciences (S. Kotz, C.B. Read, N. Balakrishnan, B. Vidakovic eds.), Second Edition, Wiley.

[34]

Ruszczyński, A. and Shapiro, A. (2006)

Optimization of Convex Risk Functions,

Mathematics of Operations Research, 31, 433–452.

[35] Stoyanov, S., Racheva-Iotova, B., Rachev, S. and Fabozzi, F. (2010) Stochastic models for risk estimation in volatile markets: a survey, Annals of Operations Research, 176, 293–309.

[36]

Shapiro, A., Dentcheva, D. and Ruszczyński, A. (2009) Lectures on Stochastic Programming: Modeling and Theory,

SIAM Publications, Philadelphia.

[37]

Tsukahara, H. (2013)

Estimation of Distortion Risk Measures, Journal of Financial Econometrics, 12 (1), 213–235.

[38]

Van der Vaart, A. W. (1998) Asymptotic Statistics, Cambridge University Press, Cambridge.