Local risk-minimization for Barndorff-Nielsen and Shephard models

Takuji Arai111Department of Economics, Keio University, e-mail:arai@econ.keio.ac.jp,

Yuto Imai222Department of Mathematics, Waseda University

and Ryoichi Suzuki333Department of Mathematics, Keio University

Abstract

We obtain explicit representations of locally risk-minimizing strategies of call and put options for the Barndorff-Nielsen and Shephard models,

which are Ornstein–Uhlenbeck-type stochastic volatility models.

Using Malliavin calculus for Lévy processes, Arai and Suzuki [3] obtained a formula for locally risk-minimizing strategies for Lévy markets under many additional conditions.

Supposing mild conditions, we make sure that the Barndorff-Nielsen and Shephard models satisfy all the conditions imposed in [3].

Among others, we investigate the Malliavin differentiability of the density of the minimal martingale measure.

Moreover, some numerical experiments for locally risk-minimizing strategies are introduced.

Keywords: Local risk-minimization, Barndorff-Nielsen and Shephard models, Stochastic volatility models, Malliavin calculus, Lévy processes.

1 Introduction

The objective is to obtain explicit representations of locally risk-minimizing (LRM) strategies of call and put options for the Barndorff-Nielsen and Shephard (BNS) models:

Ornstein–Uhlenbeck (OU)-type stochastic volatility models developed by Barndorff–Nielsen and Shephard [4], [5].

On the other hand, local risk-minimization is a very well-known quadratic hedging method of contingent claims for incomplete financial markets.

Although its theoretical aspects have been well developed, little is known about its explicit representations.

Accordingly, Arai and Suzuki [3] have analyzed this problem for Lévy markets using Malliavin calculus for Lévy processes.

They gave in Theorem 3.7 of their paper an explicit formula for LRM strategies including some Malliavin derivatives.

Here, Lévy markets mean models for which the asset price process is described by a solution to the following stochastic differential equation (SDE):

(1.1)

where is a -dimensional Brownian motion, a compensated Poisson random measure; and , , and are predictable processes.

If , , and are deterministic, a representation for LRM strategies is given simply under some mild conditions.

Indeed, [3] calculated explicitly LRM strategies of call options, Asian options, and lookback options for the deterministic coefficient case.

However, according to Theorem 3.7 in [3], one needs to impose many additional conditions on models with random coefficients.

Thus, concrete calculations for such models were set aside.

In this paper, we obtain explicit LRM strategies for BNS models, which are popular examples for the random coefficient case.

In particular, various empirical studies confirm that BNS models capture well important stylized features of financial time series.

In a BNS model, the squared volatility process is given by an OU process driven by a subordinator, that is, a nondecreasing Lévy process.

More precisely, is given as a solution to the following SDE:

(1.2)

where , and is a subordinator without drift.

Now, the asset price process of a BNS model is described as

(1.3)

where , , .

Note that the last term accounts for the leverage effect, which is a stylized fact such that the asset price declines at the moment when volatility increases.

Moreover, defining , we denote by the Poisson random measure of .

Hence, we have . Denoting by the Lévy measure of , we find is the compensated Poisson random measure.

Then, the asset price process given in (1.3) is a solution to the following SDE:

(1.4)

where .

Therefore, BNS models correspond to instances where in (1.1) is random.

We shall use Theorem 3.7 of [3] in this paper to derive LRM strategies for BNS models described as in (1.3).

Therefore, the primary part of our discussion lies in confirming all the conditions imposed on Theorem 3.7 of [3].

In particular, we need to investigate the Malliavin differentiability of the density of the minimal martingale measure (MMM),

which is an indispensable equivalent martingale measure to discuss LRM strategies.

To the best of our knowledge, literature on LRM strategies for BNS models is very limited.

Arai [1] studied this problem for a different setting from ours.

In [1], the volatility risk premium is taken into account, but is restricted to .

Hence, is described as

where is called the volatility risk premium.

Note that is continuous.

Formulating a Malliavin calculus under the MMM, [1] gave an explicit representation of LRM strategies.

On the other hand, there is some previous research on mean-variance hedging, which is an alternative quadratic hedging method, for BNS models.

Cont, Tankov and Voltchkova [9], and Kallsen and Pauwels [13] studied this problem assuming is a martingale.

Kallsen and Vierthauer [14] treated the case where .

Recently, Benth and Detering [6] dealt with the BNS model framework to represent a future price process on electricity assuming that is a martingale and .

In addition, we also develop in this paper a numerical scheme for LRM strategies for call options using the method of Arai, Imai and Suzuki [2],

which is a numerical scheme of LRM strategies for exponential Lévy models.

Their scheme is based on the so-called Carr–Madan approach [7], which is based on the fast Fourier transform (FFT).

Moreover, we compare LRM strategies with the so-called delta-hedging strategies, which are given as the partial derivative of the option price with respect to the asset price.

The outline of this paper is as follows.

After giving preliminaries in Section 2, we address the main results in Section 3.

Theorem 3.1 gives an explicit representation of LRM strategies for put options.

LRM strategies for call options are provided as its corollary.

A proof of Theorem 3.1 is discussed in Section 4. Section 5 is devoted to the Malliavin differentiability of the density of the MMM.

Numerical experiments for LRM strategies are illustrated in Section 6. Conclusions are given in Section 7.

The statement of Theorem 3.7 of [3] for our setting, and some additional calculations, are provided in Appendix.

2 Preliminaries

We consider a financial market model in which only one risky asset and one riskless asset are tradable.

For simplicity, we assume the interest rate to be . Let be a finite time horizon.

The fluctuation of the risky asset is described as a process given by (1.3).

We adopt the same mathematical framework as in [3].

The structure of the underlying probability space will be discussed in Subsection 2.3 below.

Notice that the Poisson random measure and the Lévy measure of are defined on and , respectively, and that

by Proposition 3.10 of Cont and Tankov [8]. Let be the Lévy measure of ; we then have .

Denoting and , we have , which is the canonical decomposition of .

Further, we denote for , that is,

(2.1)

Remark 2.1

Noting that a.s. for any , we can regard and as predictable processes.

For example, we may identify in (1.4) with , if necessary.

Next, we state our standing assumptions:

Assumption 2.2

1.

, where for .

2.

, where .

Remark 2.3

1.

Item 1 in Assumption 2.2 ensures , which means .

In addition, we have , because .

2.

As seen in Subsection 2.3 of [3], the so-called (SC) condition is satisfied under Assumption 2.2.

For more details on the (SC) condition, see Schweizer [18], [19].

Moreover, Lemma 2.11 of [3] implies that .

3.

By (A.2) in Appendix, item 2 ensures that for any .

Remark 2.4

We state two important examples of introduced in Nicolato and Venardos [15] that fulfill Assumption 2.2 under certain conditions on the involved parameters.

For more details on this topic, see also Schoutens [17].

1.

The first concerns given by

where and . In this case, the invariant distribution of the squared volatility process follows an inverse-Gaussian distribution with parameters and .

is called an IG-OU process. If , then item 1 of Assumption 2.2 is satisfied.

2.

The second example is what we shall call a Gamma-OU process, where the invariant distribution of is given by a Gamma distribution with parameters and .

In this case, is described as

As well as the IG-OU case, item 1 of Assumption 2.2 is satisfied if .

3.

[15] and Section 7 in [17] estimated the parameter sets for the above two models using real data.

Table 1: Estimated parameters for IG-OU and Gamma-OU processes

Note that the discounted asset price process is assumed to be a martingale in both [15] and [17].

Hence, the value of is automatically determined. For any , the parameter set for IG-OU in [17] does not satisfy item 1 of Assumption 2.2.

In contradistinction, the other estimated parameter sets listed in Table 1 satisfy the condition.

2.1 Locally risk-minimizing strategies

In this subsection, we give a definition of LRM strategies based on Theorem 1.6 of [19].

Definition 2.5

1.

denotes the space of all -valued predictable processes

satisfying .

2.

An -strategy is given by a pair ,

where and is an adapted process such that is a right continuous process with for every .

Note that (resp. ) represents the number of units of the risky asset (resp., the risk-free asset) an investor holds at time .

3.

For claim , the process defined by is called the cost process of for .

4.

An -strategy is said to be locally risk-minimizing (LRM) for claim if and is a martingale orthogonal to , that is,

is a uniformly integrable martingale.

5.

An admits a Föllmer–Schweizer (FS) decomposition if it can be described by

(2.2)

where , and is a square-integrable martingale orthogonal to with .

For more details on LRM strategies, see [18], [19].

We now introduce Proposition 5.2 of [19].

Under Assumption 2.2, an LRM strategy for exists if and only if admits an FS decomposition; and its relationship is given by

Therefore, it suffices to derive a representation of in (2.2) to obtain the LRM strategy for claim .

Henceforth, we identify with the LRM strategy for .

2.2 Minimal martingale measure

To discuss the FS decomposition, we first need to study the MMM. A probability measure is called an MMM,

if is a -martingale; and any square-integrable -martingale orthogonal to remains a martingale under .

Next we consider the following SDE:

(2.3)

where .

The solution to (2.3) is a stochastic exponential of .

More precisely, denoting

for and , we have ; and

(2.4)

We remark here that

by Lemma A.7.

Noting the boundedness of by Lemma A.7, and

we have the martingale property of by Theorem 1.4 of Ishikawa [12].

Now, we get the following:

Proposition 2.7

1.

.

2.

The probability measure defined by is the MMM.

Proof. We first demonstrate item 1. Here (2.4) and Lemma A.7 imply that

where , and and are constants defined in (A.5). That is, denoting

(2.5)

for , we have

(2.6)

Therefore, we need only to show the process is a martingale.

First, the Brownian part of is a martingale as is bounded. Lemma A.7 again yields

and , that is, .

In addition, we have

Hence, all the conditions in Theorem 1.4 of [12] are satisfied, that is, is a martingale.

We proceed to item 2. The martingale property of implies that the product process is a -local martingale.

Thus, is a -martingale, because and are in .

Moreover, letting be a square-integrable -martingale with null at orthogonal to , we have that is a -local martingale.

By the square integrability of , remains a martingale under .

Therefore, is the MMM. This completes the proof of Proposition 2.7.

2.3 Malliavin calculus

In this subsection, we prepare Malliavin calculus based on the canonical Lévy space framework undertaken by Solé, Utzet and Vives [22].

The underlying probability space is assumed to be given by ,

where is a -dimensional Wiener space on with coordinate mapping process ;

and is the canonical Lévy space for , that is, ;

and for and .

Note that represents an empty sequence. Let be the canonical filtration completed for .

For more details, see Delong and Imkeller [10], and [22].

To begin, we define measures and on as

and

where and is the Dirac measure at .

For , we denote by the set of product measurable, deterministic functions satisfying

For and , we define

Formally, we denote and for .

Under this setting, any has the unique representation with functions that are symmetric in the pairs

, and we have .

We define a Malliavin derivative operator.

Definition 2.8

1.

Let denote the set of -measurable random variables with satisfying .

2.

For any , a Malliavin derivative is defined as

for -a.e. , -a.s.

3 Main results

Using the framework of Theorem 3.7 of [3], we introduce in this section explicit representations of LRM strategies for call and put options as the main results of this paper.

Note that the statement of Theorem 3.7 of [3] for our setting is introduced in Appendix as Theorem A.1.

To this end, denoting by the underlying contingent claim, we need (Condition AS1 in Theorem A.1).

If is a call option, this condition is not necessarily satisfied in our setting.

On the other hand, because put options are bounded, we need not care about any integrability condition for them.

Therefore, we treat put options first and derive LRM strategies for call options from the put–call parity.

With this procedure, we can do without any additional assumptions.

Theorem 3.1

For , the LRM strategy of put option is represented as

We begin with the Malliavin derivatives of put options.

Proposition 4.1

For , we have and

Proof. First, note that , and by Proposition A.6. However, is not necessarily Malliavin differentiable.

Hence, we regard as a functional of rather than to calculate its Malliavin derivative.

To this end, noting the boundedness of , we introduce the following function:

Then, and for any . We also note .

Proposition 2.6 in [21] implies that and

The same argument as Theorem 4.1 of [3] implies that, for -a.e. ,

We now prove Theorem 3.1 through Theorem A.1 (Theorem 3.7 of [3]).

To this end, we need only to make sure of Conditions AS2 and AS3 in Theorem A.1.

Note that Condition AS1 is ensured by Proposition 2.7 and the boundedness of .

We first confirm Condition AS2 listed below:

C1

, ; and for a.e. .

C2

, and .

C3

For -a.e. , there is an such that .

C4

.

C5

; and .

C6

, for -a.e. .

Here , and are defined as follows:

•

denotes the space of satisfying

(a)

for a.e. ,

(b)

,

(c)

.

•

is defined as the space of such that

(d)

for -a.e. ,

(e)

,

(f)

.

•

is defined as the space of such that

(g)

,

(h)

.

Condition C1:

First, we see . To this end, we check items (a)–(c) in the definition of .

Lemmas A.8 and A.7 ensure items (a) and (b), respectively. To see item (c), Lemma A.8 implies

Finally, we prove . Item (b) holds by Lemma A.7.

As and , Propositions 5.1 and 5.4 of [22], together with (4), imply item (a) and .

Moreover, a similar calculation with (4) gives

item (c) as follows:

Condition C2:

We first demonstrate . Items (d) and (e) in the definition of are given by Lemmas A.10 and A.7, respectively.

As for item (f), Lemmas A.9 and A.10 imply

Next, we show .

Note that we can demonstrate in the same manner as in the proof of condition C1.

Hence, we have only to see items (g) and (h) in the definition of .

Because , item (g) follows.

Next, Lemmas A.10 and A.9, and Assumption 2.2 imply

Condition C4:

Proposition A.11 implies that , and ,

from which follows by Lemma A.7 and Proposition 2.7.

Next, let be the increment quoting operator defined in [22].

That is, for any random variable , and , we define

where . As by Section 5, Proposition 5.4 of [22] yields that, for ,

(4.2)

As a result, condition C4 follows.

Condition C5:

Noting that by Theorem 4.1, we have , as .

Therefore, it suffices to show .

To this end, we prove that firstly.

Because by Propositions 4.1 and A.6,

we have .

Hence, we have only to show from the view of (A.3).

Now, as seen in the proof of Proposition 2.7, defined in (2.5) is a positive martingale.

Therefore, we can define a probability measure as , and we have

As a result, we can apply Theorem 117 of Situ [20] to (4.2);

we then conclude that (4.2) has a solution satisfying ,

which implies by the -property of .

Now, is a local martingale under , because we can rewrite (4.2) as

Consequently, Theorem I.51 of Protter [16] implies that is a -martingale satisfying for any .

Moreover, by Example 9.6 of Di Nunno et al. [11], the right-hand side of (4.9) is expressed by .

5 Malliavin differentiability of

This section is devoted to show for any . To this end, for , we define and

for . Furthermore, we denote, for ,

Note that .

Lemma 5.1

We have for every and any .

Moreover, there exist constants and such that

for any . Hence, holds.

As in , Lemma 17.1 of [11] implies that for .

Note that the Malliavin derivative in [11] is defined in a different way from ours.

Denoting by the Malliavin derivative operator in [11], we have for and .

Proof of Lemma 5.1.

We take an integer arbitrarily.

Suppose that and for any .

Lemma 5.2 below and Lemma 3.3 of [10] imply that for any ; and, for any and any ,

Consequently, by (5.3), (5)–(5.9) and Lemma 5.3 below, there are constants and such that

where and may vary from line to line.

Now, we prove two lemmas which are used in the proof of Lemma 5.1.

Lemma 5.2

Fix arbitrarily.

Assume that and for any .

We have and .

Proof. We show . By , and Lemmas A.7 and A.8,

we have for any .

Hence, item (a) in the definition of is given by Propositions 5.1 and 5.4 of [22].

Next, item (b) is satisfied by Lemma A.7.

As for item (c), there exist two constants and such that .

In addition, we have

As a result, item (c) follows.

This completes the proof of . is shown similarly.

Lemma 5.3

.

Proof. First, we can see inductively that is a martingale with .

Denoting for and , we have

In this section, we illustrate LRM strategies for the BNS models with numerical experiments.

[2] developed a numerical scheme of LRM strategies for exponential Lévy models using the Carr-Madan approach [7],

which is a numerical method for option prices based on the fast Fourier transform (FFT).

In the following, we shall compute (6.1) numerically for the call options using the method developed in [2].

Moreover, we compare LRM strategies with delta-hedging strategies, which are given as the partial derivative of the option price with respect to the asset price.

We treat the Gamma-OU model in which the Lévy measure is given as

where , .

Moreover, we use the parameter set estimated in [17] (see Table 1).

To do it, we need to adopt the same setting as [17].

Hence, we need to take into account the interest rate and the continuous dividend rate ;

that is, the discount factor is given by .

Moreover, suppose that the discounted asset price process is a martingale.

Hence, appearing in (1.3) is given as

We consider a call option with strike price . From the view of Theorem 3.1, Corollary 3.3 and Proposition 4.1, we have

which is ensured to be positive by Assumption 2.2.

Note that the right-hand side of (6.3) is independent of the choice of .

As a result, since the integrand of (6.3) is given by the product of and a function of , we can compute through the FFT.

Next, we calculate .

First, Proposition A.6 implies

for and , where for ,

and for .

Denoting

for , we have

In addition, as the process is a solution to the SDE (1.2) with ,

(6.2) implies that the characteristic function of given and is described as follows:

where , which is a function of .

Note that, as in the proof of Theorem 2.2 of [15], when , which is a subinterval of (6.4) for any .

Therefore, taking such an , we have

from which we can compute using the FFT.

Next, we discuss delta-hedging strategy for a call option with strike price , which is given as the partial derivative of the option price with respect to ,

that is,

Noting that

we have

Hence, the delta-hedging strategy is given from .

We show numerical results on LRM strategies and delta-hedging strategies using the parameter set estimated in [17].

We fix , and .

The asset price and the squared volatility at time are fixed to and , respectively.

Recall Table 1 as , , , .

Moreover, just like [17], we take .

Note that in [17] corresponds to in our setting, and is greater than 1.75.

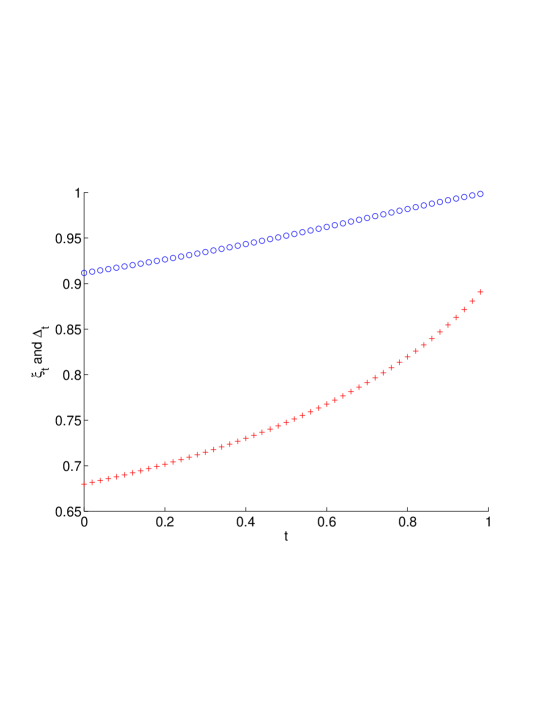

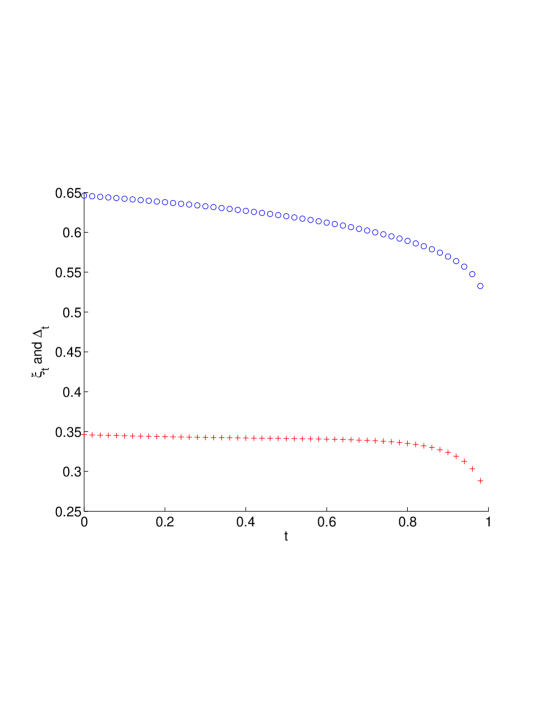

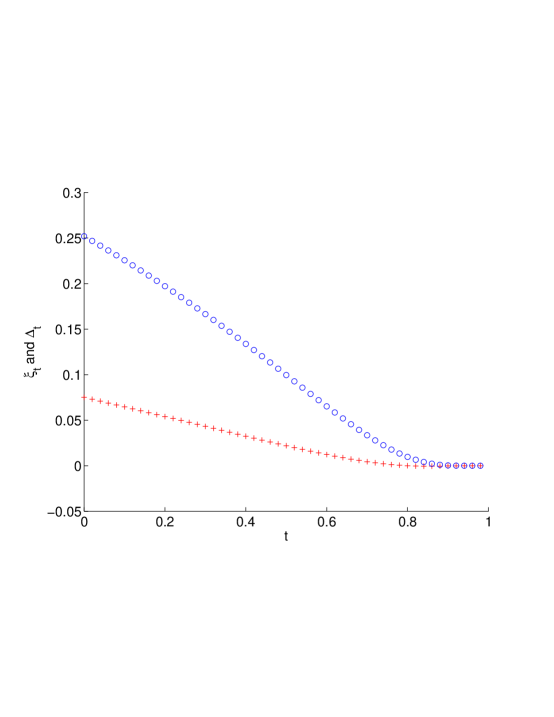

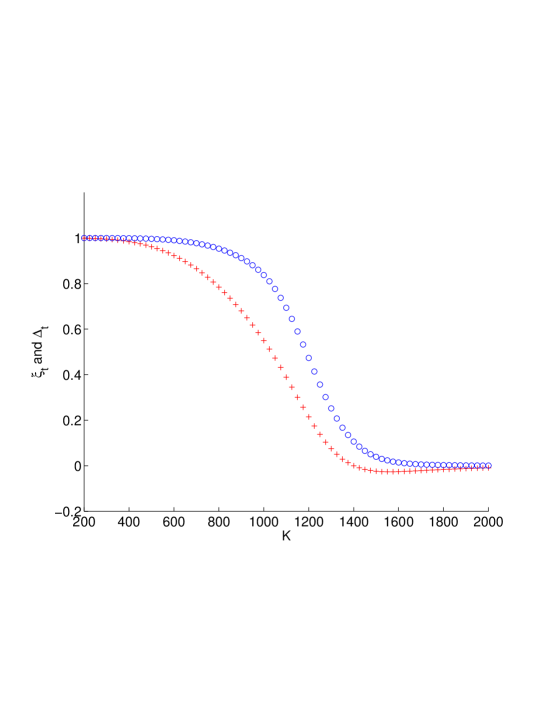

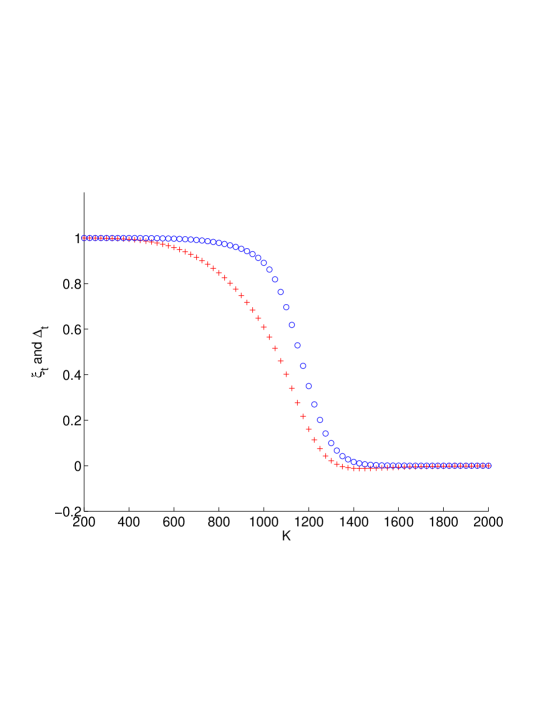

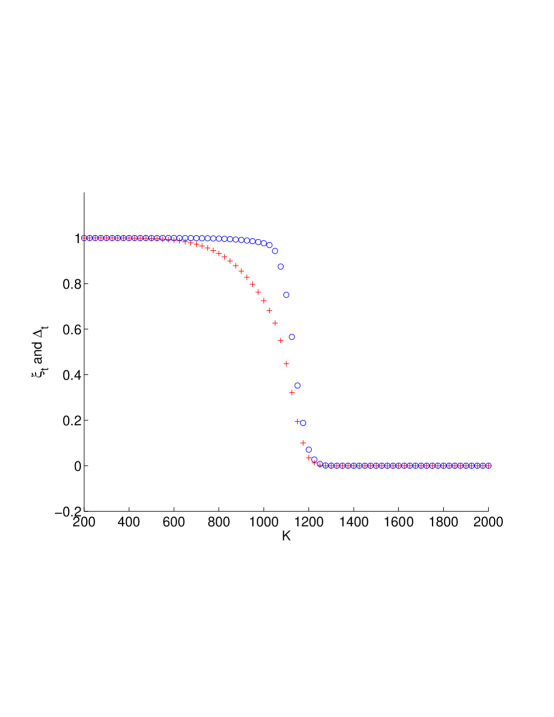

In Figures 1 and 2 below, red crosses and blue circles represent the values of and , respectively.

We implement the following two types of experiments: First, for fixed strike price , we compute and for times .

Note that we fix to 900, 1124.47, 1300, which correspond to “out of the money”, “at the money” and “in the money”, respectively.

Second, is fixed to 0, 0.5 and 0.9, and we instead vary from 200 to 2000 at steps of 25, and compute and .

Now, we discuss implications from Figures 1 and 2.

First, is always less than or equal to .

This fact suggests that local risk-minimization is more risk-averse than the delta-hedge.

Second, Figure 1 shows that both and are increasing functions of when the option is “in the money”,

and decreasing when “at the money” or “out of the money”.

Third, Figure 2 implies that both and tend to when the option is “deep in the money”, and when “deep out of the money”.

In addition, the values of strategies decrease from to around “at the money”, and its gradient is steep when the time to maturity is near to .

Finally, the spread between and in Figure 2 is wider when the option is “in the money” than “out of the money”.

(a)Values of and when is fixed to 900 vs. times .

In this case, the option is “in the money” at time .

Red crosses and blue circles represent the values of and , respectively.

(b)Example where the option is “at the money” at time , that is, is fixed to 1124.47

(c)Example where is fixed to 1300, that is, the option is “out of the money” at time

Figure 1: Values of and for fixed vs. times .

(a)Values of and at vs. strike price from 200 to 2000 at steps of 25.

Red crosses and blue circles represent the values of and , respectively.

(b)Example where .

(c)Example where .

Figure 2: Values of and at fixed vs. strike price from 200 to 2000 at steps of 25.

7 Conclusions

We obtain explicit representations of LRM strategies of call and put options for the BNS models given by (1.2) and (1.3), and implement related numerical experiments.

We impose only Assumption 2.2 as the standing assumptions.

Recall that Assumption 2.2 does not exclude the two important examples: IG-OU and Gamma-OU, although parameters are restricted.

Our discussion is based on the framework of [3].

We confirm all the additional conditions imposed in [3].

Above all, we need some integrability conditions on the underlying contingent claim .

For example, we need , which is almost equivalent to if is a call option.

However, is not in in our setting, which means that an additional condition is needed to treat call options directly in the framework of [3].

Thus, we consider put options first in this paper, as they are bounded. LRM strategies for call options are then given as a corollary.

With this simple idea, we do not need to impose any additional condition.

Moreover, to demonstrate condition C4, we need to investigate the Malliavin differentiability of the process .

Note that is a solution to the SDE (2.3). [11] showed the Malliavin differentiability of solutions to Markovian–type SDEs with the Lipschitz condition.

However, the SDE (2.3) is not Markovian, because and are random.

In Section 5, as an extension of Section 17 in [11], we show that .

This result should be a valuable mathematical contribution in its own right.

Recall that and are bounded by Lemma A.7,

and the Malliavin derivatives of and are equivalent to and simultaneously by Lemmas A.8 and A.9.

These facts play a vital role in the demonstration of the Malliavin differentiability of .

We consider, throughout the paper, BNS models for which the asset price process is given by (1.3).

Actually, the general form of BNS models is as follows:

where the parameter is called the volatility risk premium.

In other words, we restrict to .

If , the boundedness of and no longer holds, from which it is not easy to show that .

Thus, formulating a Malliavin calculus under the MMM, [1] took a different approach to study the case of and .

On the other hand, some new ideas are needed to treat fully general case.

It remains for future research.

Theorem 3.7 of [3], which provides an explicit representation formula of LRM strategies for Lévy markets, is frequently referred to in this paper.

Therefore, we introduce its statement for BNS models under Assumption 2.2.

Note that, although Assumption 2.1 of [3] is imposed on Theorem 3.7 of [3], it is satisfied under Assumption 2.2.

For more details, see Remark 2.3.

Moreover, we have .

By Definition 2.8, the lemma follows.

Lemma A.3

For any , we have ; and

for .

Furthermore, we have for .

Proof. Taking a -function such that is bounded; and for , we have by (A.2).

Proposition 2.6 in [21] implies , ; and

for , as is nonnegative by (A.4).

In addition, we have for .

Lemma A.4

We have ; and

for , where the function is defined in Assumption 2.2.

Proof. First, we have

From the view of Definition 2.8,

we obtain and for .

Lemma A.5

We have and

for .

Proof. To begin, we show . Lemma A.3 implies for any . We have by (A.3) and the integrability of . As by Lemma A.3, item (c) of the definition of is satisfied. Hence, Lemma 3.3 in [10] provides and

If , then ; otherwise, if , equivalently ,

then

by Assumption 2.2.

This completes the proof.

Next, we calculate some Malliavin derivatives related to and .

Lemma A.8

For any , we have ; and

(A.6)

for , where for . Moreover, we have

for some .

Proof. Note that and .

Because and , Proposition 2.6 in [21], together with Lemma A.3, implies and (A.6).

In particular, we have .

Further, Lemma A.3 again yields .

Moreover, as is bounded, we can find a such that .

Lemma A.9

For any , we have ; and

(A.7)

for , where for .

Moreover, we have

(A.8)

for some .

Proof. Note that and .

Hence, is bounded. Therefore, the same argument as Lemma A.8 implies (A.7).

In addition, (A.8) is given by the boundedness of and .

Lemma A.10

For any , we have ; and

for .

Moreover, we have .

Proof. For , we denote

Note that is a -function satisfying for all .

Because and by item 3 of Lemma A.7, we have

We discuss each term of (A.10) separately.

As seen in Section 4, we have .

Therefore, Lemma 3.3 of [10] implies that , and for .

Similarly, we have

, and

for .

As for , because by Section 4, Lemma 3.2 of [10] yields

for .

In particular, . For the fourth term of (A.10), because , Proposition 3.5 of [21] implies

for . Collectively, we conclude the following:

Proposition A.11

We have , ; and

for .

Acknowledgments

Takuji Arai gratefully acknowledges the financial support of Ishii Memorial Securities Research Promotion Foundation, and

Scientific Research (C) No.15K04936 from the Ministry of Education, Culture, Sports, Science and Technology of Japan.

References

[1]

Arai, T.: Local risk-minimization for Barndorff-Nielsen and Shephard models with volatility risk premium, to appear in Advances in Mathematical Economics (2015)

[2]

Arai, T., Imai, Y., Suzuki, R.: Numerical analysis on local risk-minimization for exponential Levy models,

to appear in International Journal of Theoretical and Applied Finance (2015)

[3]

Arai, T., Suzuki, R.: Local risk minimization for Lévy markets. International Journal of Financial Engineering, 2, 1550015 (2015)

[4]

Barndorff-Nielsen, O.E., Shephard, N.: Modelling by Lévy processes for financial econometrics. In: Barndorff-Nielsen, O.E., Mikosch,T., Resnick, S. (eds.):

Lévy processes—Theory and Applications, pp. 283–318.

Birkhäuser, Basel (2001)

[5]

Barndorff-Nielsen, O.E., Shephard, N.: Non-Gaussian Ornstein-Uhlenbeck based models and some of their uses in financial econometrics. J.R. Statistic. Soc. 63, 167–241 (2001)

[6]

Benth, F.E., Detering, N.: Pricing and Hedging Asian-Style Options in Energy. Finance and Stochastics,19, 849–889 (2015)

[7]

Carr, P., D. Madan: Option valuation using the fast Fourier transform. Journal of Computational Finance, 2, 61–73 (1999)

[8]

Cont, R., Tankov P.: Financial Modelling with Jump Processes. Chapman & Hall, London (2004)

[9]

Cont, R., Tankov, P., Voltchkova, E.: Hedging with options in models with jumps. In: F. Benth et al. (Ed.), Stochastic analysis and applications.

The Abel symposium 2005 (pp.197-217). Berlin: Springer (2007)

[10]

Delong, L., Imkeller, P.: On Malliavin’s differentiability of BSDEs with time delayed generators driven by Brownian motions and Poisson random measures.

Stochastic Process. Appl. 120, 1748–1775 (2010)

[11]

Di Nunno, G., Øksendal, B., Proske, F.: Malliavin Calculus for Lévy Processes with Applications to Finance. Springer, Berlin (2009)

[12]

Ishikawa, Y.: Stochastic Calculus of Variations for Jump Processes. Walter De Gruyter, Berlin (2013)

[13]

Kallsen, J., Pauwels, A.: Variance-optimal hedging in general affine stochastic volatility models. Adv. Appl. Prob. 42, 83–105 (2010)

[14]

Kallsen, J., Vierthauer, R.: Quadratic hedging in affine stochastic volatility models. Rev. Deriv. Res. 12, 3–27 (2009)

[15]

Nicolato, E., Venardos, E.: Option Pricing in Stochastic Volatility Models of the Ornstein-Uhlenbeck type. Mathematical Finance. 13 (4), 445–466 (2003)

[16]

Protter, P.: Stochastic Integration and Differential Equations. Springer, Berlin (2004)

[17]

Schoutens, W.: Lévy Processes in Finance: Pricing Financial Derivatives. John Wiley & Sons, Hoboken (2003)

[18]

Schweizer, M.: A Guided Tour through Quadratic Hedging Approaches. In: Jouini, E., Cvitanić, J., Musiela, M. (eds.):

Option Pricing, Interest Rates and Risk Management (Handbooks in Mathematical Finance), pp. 538–574. Cambridge University Press, Cambridge (2001)

[19]

Schweizer, M.: Local Risk-Minimization for Multidimensional Assets and Payment Streams. Banach Center Publ. 83, 213–229 (2008)

[20]

Situ, R.: Theory of Stochastic Differential Equations with Jumps and Applications (Mathematical and Analytical Techniques with Applications to Engineering). Springer, Berlin (2005)

[21]

Suzuki, R.: A Clark-Ocone type formula under change of measure for Lévy processes with -Lévy measure. Commun. Stoch. Anal. 7, 383–407 (2013)

[22]

Solé, J.L., Utzet, F., Vives, J.: Canonical Lévy process and Malliavin calculus. Stochastic Process. Appl. 117, 165–187 (2007)