Measuring Systemic Risk:Robust Ranking Techniques Approach

Amirhossein Sadoghi

Frankfurt School of Finance & Management,Frankfurt am Main E.mail: a.sadoghi@fs.de

Abstract

In this research, we introduce a robust metric to identify Systemically Important Financial Institution (SIFI) in a financial network by taking into account both common idiosyncratic shocks and contagion through counterparty exposures. We develop an efficient algorithm to rank financial institutions by formulating a fixed point problem and reducing it to a non-smooth convex optimization problem. We then study the underlying distribution of the proposed metric and analyze the performance of the algorithm by using different financial network structures. Overall, our findings suggest that the level of interconnection and position of institutions in the financial network are important elements to measure systemic risk and identify SIFIs. Results show that increasing the levels of out- and in-degree connections of an institution can have a diverse impact on its systemic ranking. Additionally, on the empirical side, we investigate the factors which lead to the identification of Global Systemic Important Banks (G-SIB) by using a panel dataset of the largest banks in each country. Our empirical results supports the main findings of the theoretical model.

keywords:

Financial Network, Systemic Risk, SIFI, Nonsmooth Convex ProblemJEL classification : D85, E58, G01, G21, G33.

† † journal: working paper at arXiv.org

{blockarray} cccccccc&12…n{block} c(cccc)|cc|c@0Ω12…Ω1n(Lint)1(LE)1L1Ω210…Ω2n(Lint)2(LE)2L2Π=⋮⋮⋱⋮⋮⋮⋮Ωn1Ωn2⋯0(Lint)n(LE)nLn(Aint)1(Aint)2⋯(Aint)n(AE)1(AE)2⋯(AE)nA1A2…An

Thepresentationofthematrixofinterbankexposure.Thesummationofelementsofcolumnsandrowsareinterbankassetsandliabilities,respectively.

Typically,financialnetworksarelargeweightednetworks.Inaweightednetwork,theadjacencymatrixcontainsinformationonweightsrepresentedtherelativenodesstrengths.Later,wewilldiscussaboutpropertiesoftheweightedadjacencymatrixandhowtouseitinourmodel.

3

Asamajoreffectofthecomplexityofthecontemporaryfinancialnetworkandlackofanadequatemethodologyformeasuringsystemicrisk,anticipatingtheimpactofdefaultsinthefinancialsystembecomesachallengingwork.Foralongtime,thesizeoffinancialinstitution′sbalancesheethasbeenusedtoranktheinstitutionsinthesystem,andlargeinstitutionsbasedontheirbalancesheetsizearestatedas"TooBigtoFail".However,therecenteconomiccriseshasindicatedthatrelativelysmallinstitutionscanhavethesignificantimpactthefinancialsystem.TherearetwomainapproachesforidentificationofSIFIs:model-basedapproachandindicator-basedapproach.Thefirstapproachisbasedonmainindicators,tocomprisebroadcharacteristicsoffinancialinstitutions.Thesecondoneisbasedondynamicsoffinancialinstitutions′relationships.TheBaselCommitteeonBankingSupervision(BCSBS)

board2013global weistroffer2011identifying

TheacademicapproachtoidentifySIFIisthemodel-basedapproach.Themodel-basedmethodologytoanalyzethesystemicimportanceoffinancialinstitutionsgoesbacktotheoreticalpapersby

allen2000financial Freixas2000 acharya2010measuring Adrian2008

Duetolackofsufficientinformationforallfinancialinstitutions,models′instabilityoverbusinesscyclesandthecomplexlyoffinancialsystem,modelingapproachisnotrobustandcannotcaptureallthewaysthataninstitutionissystemicallyimportant.Toovercomethetraditionalmethodslimitations,somenetwork-basedmodelsweredeveloped.TheDebtRankalgorithmby

battiston2012debtrank Sorama2012 eisenberg2001systemic

Tocapturedifferentdimensionsofthesystemicimportanceofaninstitution,weneedtomeasurevariousaspectsofitsfinancialactivities.Thismeasurementshouldberobustintermsofuncertaintyinmarketdataqualityandexogenousfactors,andtobeapplicableforalltypesoffinancialinstitutions.Indicator-basedmeasurementisasimplemethodtorankinstitutionsandisrobustwithrespecttosomeuncertaintiesofthemodelingapproach.Nonetheless,thisapproachisstaticandcannotreflectdynamicsofthefinancialsystem.BaselIIIagreementintroducedasetoftoolsandmethodologytoregulatetheSIFIs,toreducetheprobabilityoffailureandlimitSIFIsfailuresconsequences.Asaresult,itcanenhancethefinancialstabilityandmitigatethecostofgovernments′interventions.Thesetoolscanbeclassifiedinfollowingcategories:(i)thereductionoftheSIFIssize:institutions′sizerepresentsthepotentialofposingrisktotheentiresystempartially,(ii)re-organizingtheSIFIs′structurecanreducethesystemicimportanceofaninstitution,(iii)limitingoftheinstitutionactivitycanreducethecontagionofstressthroughthesystem,(iv)anadditionalcapitalbuffercanreducetheprobabilityofSIFIs′failureand(v)improvingstoreliquidationofSIFIsmayhelpintheeventoffailure.Thescopeoftheseregulationsislimitedtoavailableinformationoninstitutions′characteristicsandtheiractivities.

4

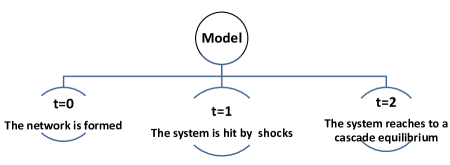

Inthissection,weexplainourmodelandintroduceanindextoquantifyfinancialrelationsamonginstitutions,regardingtheimpactofthedistressofinstitutionstotheircounter-partiesacrosstheentiresysteminarecursiveway.Inthisapproach,wedeterminesystemicallyimportantinstitutionsbyanalyzingthedynamicsoftheirdependencies.Weuseadirectednetworkwheretheverticesrepresentfinancialinstitutions,andtheedgesrepresentfinancialrelations.Ourmodelstudiesnetworkeffectsofliquidityhoardingprocedure.Mainly,itshowshowliquidityshortagescanspreadthroughthefinancialsystemviainterbanklinkages.Themodelexaminesthefinancialsystemstructure,suchasjointdistributionoflendingandborrowinglinksandconnectivitydegreestounderstandhowshocksspread.Thesystemattimet=0isinanormalstateandthenetworkisformed.Attimet=1,thesystemishitbyashockorseveralshockswhichhaveimpactsnetwork.Thestressednodesstarttotransmitshockstotheircounterpartiesandcascadebegins.Basically,weassumethereisnochannelforfiresaleandchangingofallexternalcashflows,assetsthroughoutthecascadearenotconsidered.Attimet=2,thecascadecontinuesuntilitreachesequilibrium(SeeFigure:

Figure 2 :

Gairspa20090410 Gairspa20090410

whereϕistheportionofbanks′obligationtoadefaultedbank.Wecandeterminethesolvencyconditionofbank(i)withhavinganassumptionwhichislosingofinterbankassetofaninstituationattimeofdefault(

Gairspa20090410

From

Gairspa20090410 7

Thisconditionshowstheabilityofaninstitutionoveracashflowtimehorizontomeetitsobligationwhendebtsarecollectedbyitsdebtors.Withusingnetworkcentralitymeasurements,wedefinesolvencyindexasfollowing:

Definition 5 .

Solvency Index Letεshbetheaggregateorindividualdeposits′shocks.Fromequation(8

where(¯Ω)iistheaverageofinterbankexposuresofnodeianddeginianddegoutiarein-degreeandout-degreeofnodei.SolvencyIndexofnodei(Solvi)isdefinedasinstitution(i)′sinabilitytosatisfythesolvencyconditionandthencontagionstartstospread.Thisindexcabbeexpressedby:

Inacounterpartynetwork,thevulnerabilityweightofanodecanbedefinedasafractionofcapitalwhichisdecreasedbytheimpactofthedefaultofitscounterparty.WithgiventhecapitalbufferoftheinstitutioniCpai,whichisusedagainstfinancialrisk,wedefinethevulnerabilityweightindexasthefollowing:

Definition 6 .

Vulnerability Weight Vulnerabilityweightoftheinstitutioniisexpressedasitsabilitytomitigatetheinterbankactivitiestensionswhichmakethefinancialsystemsusceptibletocounterpartyrisk.Itcanbequantifiedastheproportionofthecapitalofaninstitutionusedagainstinterbankexposure:

𝐰 𝑖𝑗 = min ( Ω 𝑖𝑗 𝐶𝑝𝑎 i , 1 ) . subscript 𝐰 𝑖𝑗 superscript 𝛺 𝑖𝑗 superscript 𝐶𝑝𝑎 𝑖 1 \mathbf{w}_{ij}=\min(\frac{\Omega^{ij}}{Cpa^{i}},1). (12)

Theeconomicvalueoftheimpactofoneinstitutiononothersiscalculatedbymultiplyingtheimpactbytherelativeeconomicvalueofitscounterparties.Wedefine

Relative Impact asafractionofsolvencyindexoneinstitutiononaccumulativesolvencyindexesofitscounterparties.

Theimpactvalueofanindividualinstitutiononitscounterpartiescanbedefinedas:

𝐩 ~ i = ∑ j 𝐰 i j 𝐫 i , subscript ~ 𝐩 𝑖 subscript 𝑗 subscript 𝐰 𝑖 𝑗 subscript 𝐫 𝑖 \mathbf{\tilde{p}}_{i}=\sum_{j}\mathbf{w}_{ij}\mathbf{r}_{i}, (13)

whereristhesolvencyratiowhichrepresentstherelativesolvencyofaninstitutiontoitscounterparties:

𝐫 i = S o l v i ∑ j S o l v i { j | a i j > 0 } . subscript 𝐫 𝑖 𝑆 𝑜 𝑙 subscript 𝑣 𝑖 subscript 𝑗 𝑆 𝑜 𝑙 subscript 𝑣 𝑖 conditional-set 𝑗 subscript 𝑎 𝑖 𝑗 0

\mathbf{r}_{i}=\frac{Solv_{i}}{\sum_{j}Solv_{i}}\qquad\quad\{j|a_{ij}>0\}. (14)

Inaddition,aninstitution′scounterpartieshaveanimpact,weaddthesecondterminequation(

14 Impact Index asmeasuringoftheexpectedloss,whichisgeneratedbythefailureofagroupofinstitutionsasfollows.

Definition 7 .

Similarto

battiston2012debtrank

𝐩 i = α ∑ j 𝐰 𝑖𝑗 𝐵𝐶 i 𝐫 i ⏟ expected loss of institution’s failure (direct effects) + β ∑ j 𝐰 𝑖𝑗 𝐶𝐶 i 𝐩 j ⏟ expected loss by counter-parties’ failure (indirect effects) ( β = 1 − α ) , subscript 𝐩 𝑖 subscript ⏟ 𝛼 subscript 𝑗 subscript superscript 𝐰 subscript 𝐵𝐶 𝑖 𝑖𝑗 subscript 𝐫 𝑖 expected loss of institution’s failure (direct effects) subscript ⏟ 𝛽 subscript 𝑗 subscript superscript 𝐰 subscript 𝐶𝐶 𝑖 𝑖𝑗 subscript 𝐩 𝑗 expected loss by counter-parties’ failure (indirect effects) 𝛽 1 𝛼 \mathbf{p}_{i}=\underbrace{\alpha\sum_{j}\mathbf{w}^{BC_{i}}_{ij}\mathbf{r}_{i}}_{\text{expected loss of institution's failure (direct effects)}}+\underbrace{\beta\sum_{j}\mathbf{w}^{CC_{i}}_{ij}\mathbf{p}_{j}}_{\text{expected loss by counter-parties' failure (indirect effects)}}\\

(\beta=1-\alpha), (15)

whereα<1istheprobabilityofimposingshockbyanodeandβ=1-αistheprobabilityofrevivingshocksbycounterparties,andCCiandBCiaretheclosenessandBetweennesscentralityofthenode(institution)i.

Thefirsttermismeasuringtheproportionaloftheexpectedloss,generatedbythefailureofaninstitution(directeffects),andthesecondproportioncanbecomingfromthefailureofitscounterparties(indirecteffects).Asabovementioned,inanetworktheclosenesscentralityofanodeindicatestherelativedistanceofthenodetoothernodesandanothercentralitymeasurementwhichiscalledbetweennesscentralityindicateswhohascontroloverflowbetweenothers.Inotherwords,theseindexescanshowthescopeofimpactsofaninstitution′sdistressorfailureonthesystem.Withthehighervalueofbetweennesscentralityofanodeshowsthevulnerabilityofanodetocontrolthetransmissionofcounterparties′stress.Similarly,thehighervalueoftheclosenessofanodecanintensifytheimpactofanodeonitscounterparties.

4.1

Thevectorpcontainsinformationonimpactindexesofinstitutionsinthenetwork,wecanrewriteequation(

15

𝐩 = 𝐌𝐩 , 𝐩 𝐌𝐩 \mathbf{p}=\mathbf{M}\mathbf{p}, (16)

whereletmatrixMdefinedonRn×nasanon-negative(positive)matrixfromequation(

16

𝐌 = α 𝐖 C C + β 𝐖 B C 𝐑 , ( β = 1 − α ) , 𝐌 𝛼 superscript 𝐖 𝐶 𝐶 𝛽 superscript 𝐖 𝐵 𝐶 𝐑 𝛽 1 𝛼

\mathbf{M}=\alpha\mathbf{W}^{CC}+\beta\mathbf{W}^{BC}\mathbf{R},\quad\quad\quad(\beta=1-\alpha), (17)

wherethematrixRisadiagonalmatrixwithentriesonthemaindiagonalarethevectorr.WecandecomposeaperturbedmatrixMintotwomatrices:nominalmatrixPwhichcontainsinformationonvulnerabilityweightedofimpactindexesofinstitutionsandaperturbationmatrixΞwhichincludesinformationontheaggregateorindividualdeposits′shocksεsh.

𝐌 = 𝐏 + 𝚵 𝐌 𝐏 𝚵 \mathbf{M}=\mathbf{P}+\mathbf{\Xi} (18)

LetPbeasetofperturbedmatrixandM⊂P.Wearelookingforarobustsolution¯pofthedominanteigenvectorofmatrix