Estimation of the time of change in panel data

Abstract.

We consider the problem of estimating the common time of a change in the mean parameters of panel data when dependence is allowed between the panels in the form of a common factor. A CUSUM type estimator is proposed, and we establish first and second order asymptotics that can be used to derive consistent confidence intervals for the time of change. Our results improve upon existing theory in two primary directions. Firstly, the conditions we impose on the model errors only pertain to the order of their long run moments, and hence our results hold for nearly all stationary time series models of interest, including nonlinear time series like the ARCH and GARCH processes. Secondly, we study how the asymptotic distribution and norming sequences of the estimator depend on the magnitude of the changes in each panel and the common factor loadings. The performance of our results in finite samples is demonstrated with a Monte Carlo simulation study, and we consider applications to two real data sets: the exchange rates of 23 currencies with respect to the US dollar, and the GDP per capita in 113 countries.

1. INTRODUCTION

In this paper, we consider the problem of estimating the time of a change in the mean present in panel data in which their are panels comprised of time series data of length . A common structural break in panel data is a quite natural occurrence. For example, if each panel represents the exchange rate of a currency with respect to US dollars, then a crisis in the US would be expected to simultaneously affect each panel. Similar phenomena may be produced my governmental policy changes, the introduction of a new technology, etc., and in these cases it is of interest to estimate the time at which such occurrences are manifested in sample data. The theory of change point analysis has been extensively developed to study problems of this nature, see Csörgő and Horváth (1997), Brodsky and Darkhovskii (2002), and Aue and Horváth (2012) for reviews of the field.

Classical methods in change point analysis consider univariate and multivariate data of a fixed dimension. In many panel data examples, however, the number of panels is comparable in size to the length of the series . In these cases asymptotics as remains fixed and tends to infinity, or as and jointly tend to infinity, are more appropriate. Although in principle one could detect the common change present in each panel by examining a single series, an analysis that utilizes all available panels should provide improved detection and estimation.

The literature on structural breaks in panel data has grown considerably in the last two decades. We refer to Arellano (2003), Hsiao (2003) and Baltagi (2013) for surveys of several panel data models and their applications to econometrics and finance. The early foundations for estimating structural changes in panel data were developed in Joseph and Wolfson (1992,1993), and many aspects of the problem have now seen at least some consideration; Li et al. (2014) and Qian and Su (2014) consider multiple structural breaks in panel data, and Kao et al. (2014) considers break testing under cointegration.

The works of Bai (2010), Kim (2011, 2014), and Horváth and Hušková (2012) are the most closely related to the present paper. Bai (2010) considers the problem of estimating a common break in the means of panel data that do not exhibit cross sectional dependence. A least squares estimator is proposed that is shown to be consistent when tends to infinity, and its asymptotic properties are derived as and jointly tend to infinity. Kim (2011) considers the least squares estimator of Bai (2010) with cross sectional dependence modeled by a common factor, and expands the test to detect a change in the slope of a linear trend in the mean component. Horváth and Hušková (2012) study testing for the presence of a change using a CUSUM estimator, and also assuming the presence of a common factor. In each of these papers, asymptotics are derived assuming the model errors are linear processes, and that the rates of divergence relative to and of the size of the changes and the magnitudes of the factor loadings are fixed.

In this paper, we expand the existing theory in two primary directions. We derive second order asymptotics for the CUSUM change point estimator assuming only an order condition on the long run moments. This extends the asymptotic theory of change point estimation to a wide variety of error processes, notably many nonlinear time series examples like the ARCH and GARCH processes. We also show explicitly how the asymptotic distribution and norming sequences of the estimator depend on the magnitude of the changes in each panel and the common factor loadings. This allows for the computation of the limit distribution under several conceivable rates of divergence for the magnitudes of changes and factor loadings.

The remainder of the paper is organized as follows. In Section 2, we present our assumptions and the main results of the paper. Section 3 contains examples of error processes that satisfy the assumptions of Section 2. Estimators for the norming sequences that appear in the results of Section 2 are developed and studied in Section 4. The implementation of the results of the paper as well as a Monte Carlo simulation study and data applications are detailed in Section 5. The proofs of all results are contained in Appendix A.

2. Assumptions, and main results

We consider the panel data model

| (2.1) |

where the idiosyncratic errors have mean zero, denotes the common factor with loadings , , and denotes the change in the mean of panel that occurs at the common, and unknown, change point .

Assumption 2.1.

(i) The sequences and

(ii)

According to Assumption 2.1(i), the only source of dependence between the panels is the common factor . The idiosyncratic errors form a stationary time series, similarly to the assumption in Bai (2010) and Kao et al. (2012, 2013). Throughout this paper and , , are allowed to depend on and . For the sake of simplicity, we consider the case when , but our results could be extended to the more general case of a vector valued factor loading and common factor.

Assumption 2.2.

The time of change in the mean satisfies

Assumption 2.2 is standard in change point analysis, and corresponds with the assumptions of Bai (2010), Kim (2011,2014), and Horváth and Hušková (2012). It is of interest in some econometric applications to allow for to depend on and and tend to the end points or at a certain rate; see Andrews (2003) and, in the panel data setting, Qian and Su (2014). The consideration of this problem in generality for our estimator is not a goal of the present paper, and requires a thorough study.

Our estimator for is defined as the location of the maximum of the sum of the CUSUM processes across the panels:

where

The estimator of Bai (2010) is

| (2.2) |

which is the maximum likelihood estimator for assuming that the panels are independent and normally distributed with the same variance, while maximizes the weighted log likelihood.

We impose only conditions on the long run moments of the error processes for our asymptotic results. The long run moments of the errors in panel are defined by

and we assume that they satisfy the following conditions:

Assumption 2.3.

(i)

and

(ii)

Additionally, we must assume an analogous condition on the common factors:

Assumption 2.4.

Assumptions 2.3 and 2.4 do not assume any specific structure on the error terms, in contrast to the structural break literature with panel data to date. We provide several examples in Section 3, including linear and nonlinear time series, martingales and mixing sequences, where Assumptions 2.3 and 2.4 are satisfied.

The size of the changes and the correlation between the panels will play a crucial role in the asymptotic distribution of the estimator, and these quantities will be measured by

The limit results below are proven when .

Assumption 2.5.

As ,

and

Assumption 2.5 means that the sizes of all changes cannot be too small and that the factor loadings cannot be much larger than the sample size and the size of the changes. Bai (2010) assumes that converges to a positive limit while under the assumptions of Kim (2011), the common factor dominates. A primary goal of our paper is to show how the relationship between the loadings and the sizes of the changes affect the limit distribution of the time of change estimator.

Our first result pertains to the asymptotic distribution of when is large.

The assumption in (2.4) may seem somewhat restrictive since it rules out the example of fixed break sizes and factor loadings. We note that due to the result on page 635 of Horváth and Hušková (2012), when the factor loadings are fixed the CUSUM test for the presence of a change point will reject with probability tending to one regardless of if a change exists or not, and so something along the lines of (2.4) must be assumed for the CUSUM estimator of the time of change to be consistent.

Remark 2.2.

The main difference between Remarks 2.1 and 2.2 is in the assumptions and . Remark 2.2 allows smaller changes to establish consistency but much stronger assumptions on the sequences and . If we cannot assume that and are sequences of uncorrelated random variables and the independence of and , then (2.6) can be proven under conditions of Remark 2.1. In this case (2.5) and (2.6) can hold only if when is fixed.

We now turn to the asymptotic distribution of when (2.3) does not hold, i.e. the sizes of the changes are small or occur in only a few panels:

Assumption 2.6.

(i)

(ii) and

(iii)

By Assumption 2.5, we have that , so Assumption 2.6(ii) holds if, . If , i.e. the number of the panels is large, then Assumption 2.6(iii) follows from Assumption 2.5. However, Assumption 2.5(ii) also holds if the number of panels is relatively small with respect to the length of the panels and the sizes of the changes.

Next we introduce an assumption that is a companion to Assumption 2.3:

Assumption 2.7.

(i) and,

(ii)

Assumption 2.7 requires an upper bound for the average correlation of the errors in the panels and a uniformity condition that augments Assumption 2.3(ii).

Our first result in this direction covers the case when the sizes of the changes are small and the effect of the correlation between the panels is negligible or moderate. We measure the dependence between the panels with respect to the sizes of the changes by

To describe the limit distribution of we need to introduce a drift function

and an asymptotic variance term

We note that by Assumption 2.3(i) we get that . Let

The function is the asymptotic covariance of , i.e. for all integers and

| (2.7) |

We note that . It follows from Assumption 2.3(i) that the covariance function is finite for all integers and . This function only appears in Theorem 2.2 below when is above some positive bound for all and . In this case if

The next result considers the case when the common factors are negligible.

Theorem 2.2.

Remark 2.3.

Since the proofs of Theorem 2.2 and the results to follow depend on normal approximations for the sums and , the independence of on could be relaxed as it is pointed out by Bai (2010) and Kim (2011). This would be an important consideration, for example, if the panels are indexed by locations, i.e. describes the location of the panel. In this case a spatial structure could be assumed on the errors. If Assumption 2.1(i) is replaced by a weak dependence or spatial assumption, the norming constants would change in our limit theorems.

Remark 2.4.

Remark 2.5.

The distribution of is known explicitly. Its density was derived by Ferger (1994) from Corollary 4 of Bhattacharya and Brockwell (1976) (cf. Csörgő and Horváth (1997, p. 177)).

Remark 2.6.

So far the common factor was part of the error term and it had a negligible contribution to the limit distribution in Theorem 2.2. However, it has been observed in testing for changes in panel data that the effect of strong correlation between panels might make standard statistical procedures invalid (cf. Horváth and Hušková (2012)). Bai and Zhang (2010) provide some economic examples when the common factor between the panels is strong so its effect must be built into testing and estimating procedures. Our next result covers the case when the order of the correlation between the panels and the sizes of the changes are essentially the same. Since the contribution of the ’s to the limit will not be negligible we need to specify the relation between the errors and the common factors:

Assumption 2.8.

Similarly to , we introduce

which will be part of the limit distribution when (2.12) holds or is proportional to . In all the other cases we assume the asymptotic normality of :

Assumption 2.9.

Theorem 2.3.

The effect of correlation between the panels is demonstrated in Theorem 2.3. The limit distribution in (2.15) remained the same as in (2.11) but the variance of the estimator increased by . The effect of the common factor is more transparent in (2.16) since an additional term appears in the limit which depends on the distribution of the common factors.

Theorem 2.4.

Theorem 2.4 covers the case when the limit distribution of the estimator for the time of change is completely determined by the common factors. The limit distribution in (2.18) is the same as in (2.11) and (2.15) but the rate of convergence is much slower. The effect of having several panels with changes is overshadowed by the strong influence of the common factor. For further results when the common factors dominate the limit distribution we refer to Kim (2011).

3. Examples

In this section, we study some examples of error processes that satisfy the assumptions of Section 1. We restrict our attention to establishing Assumption 2.3 for examples of possible model error sequences ’s, but the same sequences could be used for the common factors as well.

Example 3.1.

Let be independent, identically distributed random variables with , and Due to independence we have that

| (3.1) |

By the Rosenthal inequality (cf. Petrov (1995, p. 59)) we obtain for all that

where is an absolute constant, depending on only. If the error terms in each panel are independent and identically distributed, then, assuming for all , Assumption 2.3(i) holds; Assumption 2.3(ii) is satisfied if

| (3.2) |

If with some and , then Assumption 2.7(ii) is also fulfilled.

ARMA processes are very often used in classical time series analysis and our next example shows that stationary ARMA processes satisfy the basic assumptions of the first section. We consider the more general case of linear processes, which are investigated by Bai (2010), Kim (2011), and Horváth and Hušková (2012).

Example 3.2.

We assume that are independent and identically distributed random variables with and with some . The error terms form a linear process given by

where with some and . By the Phillips and Solo (1992) representation we get

where , if and , if Minkowski’s inequality and the discussion in Example 3.1 yield that we need to choose in Assumption 2.3(i) and we also have and , as .

The next example assumes a martingale structure of the errors.

Example 3.3.

Since the early 1980’s, ARCH, GARCH processes and their various extensions have become extremely popular models in the analysis of macroeconomic and financial data. For a survey and detailed study of volatility models we refer to Francq and Zakoïan (2010). The next example shows that a large class of volatility processes satisfies the assumptions in Section 1.

Example 3.4.

We assume that are independent and identically distributed random variables with and . The error terms are defined by

| (3.3) |

where the volatility process is measurable with respect to the –algebra generated by . Usually, is given by a recursion involving . Francq and Zakoïan (2010) provides conditions for the existence of a stationary solution of (3.3) in several models and establishes their basic properties. Assuming that with some , is a stationary orthogonal martingale satisfying the conditions in Example 3.3. In case of the most popular GARCH model The necessary and sufficient condition for the existence of the higher moments in case of GARCH(1,1) is given in Nelson (1990). He and Teräsvirta (1999), Ling and McAleer (2002) and Berkes et al. (2003) partially extends his results to the more general case. The existence of moments of augmented GARCH sequences are discussed in Carrasco and Chen (2002) and Hörmann (2008).

Linear processes and the volatility models of Example 3.4 are in the class of –decomposable processes.

Example 3.5.

We say the is a Bernoulli shift if it can be written as

with some functional , where are independent and identically distributed random variables. The conditions of Section 2 are satisfied if the Bernoulli shift is –decomposable, i.e. if

where , and the ’s are independent copies of , independent of . Berkes et al. (2011) proved that there is constant such that and , as , with some They also provide several examples for –decomposable Bernoulli shifts.

Example 3.6.

There is a well developed theory of partial sums of mixing random variables where the long run moments play a crucial role. It has been established under various conditions that and , as For surveys on mixing processes we refer to Bradley (2007) and Dedecker et al. (2007).

Example 3.7.

We assumed in Examples 3.2 and 3.4 that the innovations are independent and identically distributed. However, this assumption can be replaced with the less restrictive requirement that is a stationary sequence. Rosenthal–type inequalities for sums of functionals of stationary processes are developed in Wu (2002) and Merlevéde et al. (2006). These results can be used to establish Assumptions 2.3, and 2.7.

4. Estimation of norming sequences

Theorems 2.2–2.4 contain the limit distribution of with different normalizations to show the effects of the sizes of changes and the loading factors. However, in case of finite and it is impossible to check which specific condition on the growths of and holds, so we require norming sequences that would work in all possible cases. Let

Under the conditions of Theorems 2.2–2.4 we have that

| (4.1) |

The limit distribution in (4.1) is except in the special cases of (2.13) and (2.16). In these cases, the limit distribution is the argmax of a process defined on integers. The limits in (2.13) and (2.16)

depend on the distributions of . If is close to 0 in (2.13) or (2.16) the limiting distributions can be well approximated with . Bai (2010) provides numerical evidence that gives a reasonable approximation for the limit in (2.13) when . Hence we recommend that can be used as the limit in (4.1) in practice.

The limit result in (4.1) can only be used for hypothesis testing or confidence intervals if the norming factor can be consistently estimated from the sample. We estimate with

It is more difficult to estimate . Let

| (4.2) |

and

| (4.3) |

The estimator for is defined as

Theorem 4.1.

and

Since (4.4) and (4.5) hold, the limit result in (4.1) remains true when the norming is replaced with the corresponding estimators, i.e.

| (4.6) |

If the interaction between the panels is small. i.e. , as , then we need to estimate only and . Using , the long run variance estimators for , a possible estimator for is .

5. Simulations, and data examples

5.1. Simulations

Using the estimators defined in Section 4, we computed the empirical percentages when the variable defined in (3.5) is below the asymptotic quantiles for several and . We considered the case when there is no interaction between the panels, i.e. and also cases with correlations. We tried various values of . We observed that the applicability of the limit results presented in Section 1 does not depend on . In Tables 5.1 and 5.2 we used and they are based on 1,000 repetitions. The , and percentiles of the distribution of are , and , respectively. Table 5.1 illustrates that must be small to use Theorem 2.2(a) and the approximation improves when increases. In case of larger we are under the conditions of Theorem 2.1 and the distribution of is more concentrated than we would get from the asymptotics in Theorem 2.2(a).

| N/T | 90% | 95% | 99% | |

|---|---|---|---|---|

| 25/100 | 0.150 | 88.7% | 94.7% | 100% |

| 25/250 | 0.100 | 87.6% | 94.4% | 99.8% |

| 25/500 | 0.060 | 89.9% | 96.4% | 100% |

| 50/100 | 0.100 | 89.1% | 97.1% | 100% |

| 50/250 | 0.070 | 88.1% | 95.4% | 100% |

| 50/500 | 0.050 | 86.5% | 94.9% | 100% |

| 100/100 | 0.085 | 86.1% | 94.5% | 100% |

| 100/250 | 0.055 | 86.9% | 94.3% | 99.9% |

| 100/500 | 0.035 | 88.5% | 96.5% | 100% |

| N/T | 90% | 95% | 99% | |

|---|---|---|---|---|

| 25/100 | 0.150 | 86.9% | 94.9% | 100% |

| 25/250 | 0.100 | 90.7% | 95.6% | 100% |

| 25/500 | 0.060 | 89.2% | 97.2% | 100% |

| 50/100 | 0.100 | 87.6% | 95.6% | 100% |

| 50/250 | 0.070 | 91.0% | 96.4% | 100% |

| 50/500 | 0.050 | 88.3% | 96.3% | 100% |

| 100/100 | 0.085 | 89.4% | 95.9% | 100% |

| 100/250 | 0.055 | 85.1% | 94.0% | 99.9% |

| 100/500 | 0.035 | 90.1% | 96.5% | 100% |

Our comments also holds when interaction between the panels is allowed as illustrated by Table 5.2 but, due to the dependence, larger is needed to use limit results.

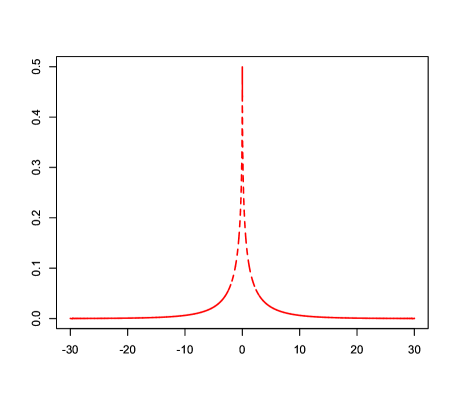

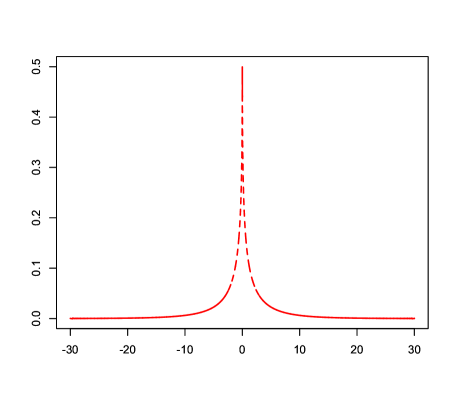

Figure 5.1 shows that the density function of the limit follows the shape of the histogram of closely.

5.2. Applications

In the first example we consider the exchange rates between the US dollar and 23 other currencies. The data can be found at the website www.federalreserve.gov

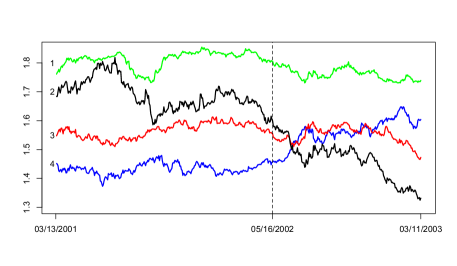

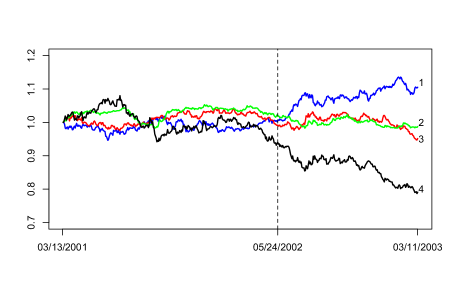

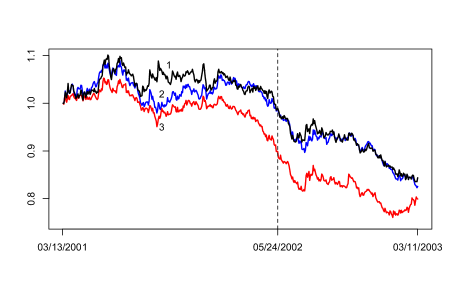

/releases/h10/hist/. Figure 5.2 contains the graphs of the exchange rates between the United Kingdom (UK), Canada (CA), Singapore (SI), Switzerland (SW), Denmark (DN), Norway (NO) and Sweden (SD). In our study we used the time period 03/13/2001–03/11/2003 so we have panels and each panel has observations. Using the testing method in Horváth and Hušková (2013) the no change in the mean of the panels null hypothesis is rejected. The estimated time of change is so the change is indicated on 05/16/2002. We also constructed confidence intervals using (4.6). Since is very large, the 90%, 95% and 99% confidence intervals contain only a single element, , i.e. the conditions of Theorem 2.1 hold in this case. It is clear from Figure 5.2 that the exchange rates are between 1.3 and 11, so if the same proportional change occurs in a panel with high values, this change will give a very large compared to the other panels. Hence a single panel can disproportionately contribute to . To overcome this problem we rescaled the observations in each panel with the first observation, i.e. with the exchange rate on 03/13/2001. Figure 5.3 contains the graphs of the relative changes in exchange rates with respect to the US dollar for the same countries as in Figure 5.2. We repeated our analysis for the relative changes (rescaled) in the exchange rates with respect to the US dollar, resulting in which corresponds to 05/24/2002. In the definition of we used . The 90%, 95% and 99% confidence intervals are and . Note that all these confidence intervals contain 297 which was obtained for the non–scaled exchange rates. Some of the graphs show a linear trend after the time of change instead of changing to an other constant mean. The limit distribution of the time of change is local, i.e. it is determined by the observations in the neighborhood of . Replacing the linear trend with an average value close to can justify the asymptotic validity of the confidence intervals. Also, after the change point was found and the means of the corresponding segments were removed, the stationarity of the residuals could not be rejected.

The exchange rates data and the scaled exchange rates contain further level shifts. Using the binary segmentation method one can divide the data into homogenous segments and provide confidence intervals for the time of changes. Sato (2013) investigates the number and the location of the changes in daily log returns in 30 currency pairs between 04/01/2001 and 30/12/2011 and points out that the study of the individual pairs might not find all the changes in the exchange rates mechanism.

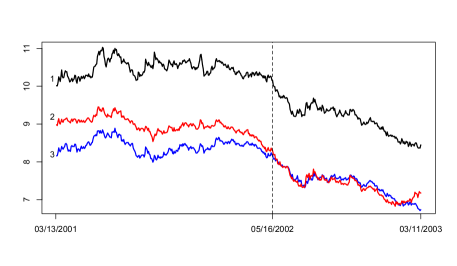

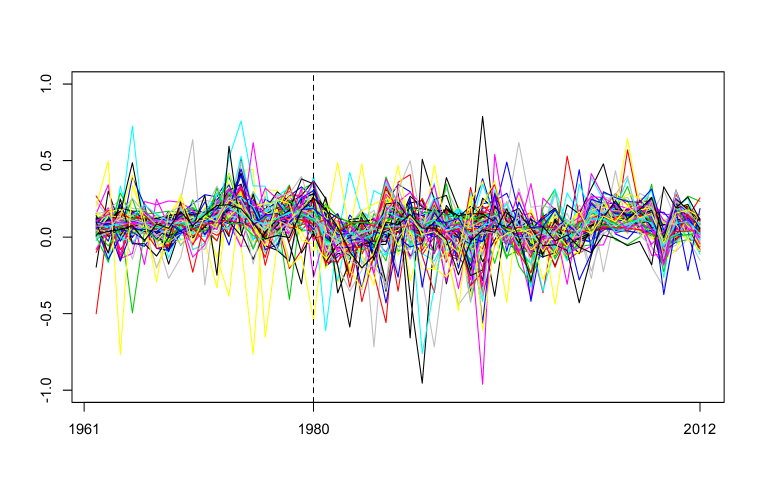

In the second example we compared the GDP/capita of countries. The data can be found at the website www://data.worldbank.org/indicator/NY.GDP.MKTP.CD. The data are recorded in current US dollar. We removed some countries from the data set due to large number of missing values, so we used panels with covering the time period 1961–2012. To achieve stationarity of the errors we transformed the data by taking differences. The graphs of the transformed GDP’s are exhibited in Figure 5.4. We used the CUSUM test of Horváth and Hušková (2013) to test the stability of the means of the panels which was rejected at very high significance level. The estimator for the time of change is which corresponds to 1979/1980. Applying the limit result in (4.6), is the asymptotic 90% and 95% confidence interval, while the 99% confidence interval is .

6. Conclusion

We established the first and second order asymptotic properties of a CUSUM estimator of the time of change in the mean of panel data. Our results are derived under long run moment conditions, which serve to extend the asymptotic theory to a broader family of error processes than had been previously considered in the literature, and we provided an in depth study on how the rates of divergence of the sizes of changes and the common factor loadings are manifested in the asymptotic behavior of the test statistic. Our results were demonstrated with a Monte Carlo simulation study, and we considered application to two real data sets.

6.1. Acknowledgements

We would like to thank three reviewers as well as the co–editor, Liangjun Su, for their helpful comments that lead to substantial improvements to this paper. This project was supported by NSF grant DMS 1305858 and grants GAČR 15-096635, GAČR 201/12/1277.

REFERENCES

Andrews, D. W. K. (2003) End-of-sample instability tests. Econometrica 71, 1661–1694.

Atak, A., O. Linton & Z. Xiao (2011) A semiparametric panel model for unbalanced data with application to climate change in the United Kingdom. Journal of Econometrics 164, 92–115.

Arellano, M. (2004) Panel Data Econometrics. Oxford University Press.

Aue, A. & L. Horváth (2013) Structural breaks in time series. Journal of Time Series Analysis 23, 1–16.

Bai, J. (2010) Common breaks in means and variances for panel data. Journal of Econometrics 157, 78–92.

Bai, J. & J.L. Carrioni–i–Silvestre (2009) Structural changes, common stochastic trends, and unit roots in panel data.The Review of Economic Studies 76, 471–501.

Bai, Y. & J. Zhang (2010) Solving the Feldstein–Horioka puzzle with financial frictions. Econometrica 78, 603–632.

Baltagi, B.H.: Econometric Analysis of Panel Data 5th Edition, Wiley, New York, 2013.

Baltagi, B.H., C. Kao & L. Liu (2012) Estimation and identification of change points in panel models with nonstationary or stationary regressors and error terms. Preprint.

Berkes, I., S. Hörmann & J. Schauer (2011). Split invariance principles for stationary processes. The Annals of Probability 39, 2441-2473.

Berkes, I., L. Horváth & P. Kokoszka (2003) GARCH processes: structure and estimation. Bernoulli 9, 201–227.

Bhattacharya, P.K. & P.J. Brockwell (1976) The minimum of an additive process with applications to

signal estimation and storage theory. Zeitschrift für Wahrscheinlichkeitstheorie verwandte Gebiete 37, 51–75.

Billingsley, P. (1968) Convergence of Probability Measures.

Wiley.

Bradley, R.C. (2007) Introduction to Strong Mixing Conditions. Vol. 1–3, Kendrick Press, Heber City, UT.

Brodsky, B.E. & B. Darkhovskii (2000) Non–Parametric Statistical Diagnosis. Kluwer.

Carrasco, M. & X. Chen (2002) Mixing and moment proprties of various GARCH and stochastic volatility models. Econometric Theory 18, 17–39.

Chan, J., L. Horváth & M. Hušková (2013) Darling–Erdős limit results for change–point detetction in panel data. Journal of Statistical Planning and Inference 143, 955–970.

Csörgő, M. & L. Horváth (1997) Limit Theorems in Change–Point Analysis. Wiley.

Csörgő, M. & P. Révész (1981) Strong Approximations in Probability and Statistics. Academic Press.

Dedecker, I., P. Doukhan, G. Lang, J.R.R. León, S. Louhichi & C. Prieur (2007) Weak Dependence with Examples and Applications. Lecture Notes in Statistics, Springer, Berlin.

Ferger, D. (1994) Change–point estimators in case of small disorders. Journal of Statistical Planning and Inference 40, 33–49.

Francq, C. & J.-M. Zakoian (2010) GARCH Models. Wiley.

Frees, E.W. (2004) Longitudinal and Panel Data: Analysis and Applications in the Social Sciences. Cambridge University Press.

He, C. & T. Teräsvirta (1999) Properties of moments of a family of GARCH processes. Journal of Econometrics 92(1999), 173–192.

Hörmann, S. (2008) Augmented GARCH sequences: dependence structure and asymptotics. Bernoulli 14(2008), 543–561.

Horváth, L. & M. Hušková (2012) Change–point detection in panel data. Journal of Time Series Analysis 33, 631–648.

Horváth, L. & G. Rice (2014) Extensions of some classical methods in change point analysis (with discussions) Test 23, 219–290.

Hsiao, C. (2003) Analysis of Panel Data. Second Edition. Cambridge University Press.

Hsiao, C. (2007) Panel data analysis–advantages and challenges. Test 16, 1–22.

Im, K.S., J. Lee & M. Tieslau (2005) Panel LM unit root test with level shifts. Oxford Bulletin of Economics and Statistics 67, 393–419.

Joseph, L. & D.B. Wolfson (1992) Estimation in multi–path change–point problems. Communications in Statistics–Theory and Methods 21, 897–913.

Joseph, L. & D.B. Wolfson (1993) Maximum likelihood estimation in the multi–path changepoint problem. Annals of the Institute of Statistical Mathematics 45 , 511–530.

Kao, C., L. Trapani & G. Urga (2012) Asymptotics for panel models with common shocks. Econometric Reviews 31, 390–439.

Kao, C., L. Trapani & G. Urga (2014) Testing for breaks in cointegrated panels. Econometric Reviews To appear.

Kim, D. (2011) Estimating a common deterministic time trend break in large panels with cross sectional dependence Journal of Econometrics 164, 310–330.

Kim, D. (2014) Common breaks in time trends for large panel data with a factor structure. Econometrics Journal In press.

Li, D., J. Qian, & L. Su (2014) Panel Data Models with Interactive Fixed Effects and Multiple Structrual Breaks. Under Revision

Qian, J., & L. Su (2014) Shrinkage Esimation of Common Breaks in Panel Data Models via Adaptive Group Fused Lasso. Working Paper, Singapore Management University.

Li, Y. (2003) A martingale inequality and large deviations. Statistics & Probability Letters 62, 317–321.

Ling, S. & M. McAleer (2002) Necessary and sufficient moment conditions for GARCH(r,s) and asymmetric GARCH(r,s) model. Econometric Theory 18, 722–729.

Merlevéde, F., M. Peligrad & S. Utev (2006) Recent advances in invariance principles for stationary sequences. Probability Surveys 3, 1–36.

Móricz, F. R. Serfling & W. Stout (1982) Moment and probability bounds with quasi-superadditive structure for the maximal partial sum. Annals of Probability 10, 1032–1040.

Nelson, D.B. (1990) Stationarity and persistance in the GARCH(1,1) model. Econometric Theory 6, 318–334.

Petrov, V.V. (1995) Limit Theorems of Probability Theory, Clarendon Press.

Phillips, P.C.P. & V. Solo (1992) Asymptotics for linear processes. Annals of Statistics 20, 971–1001.

Qian, J. & L. Su (2014) Shrinkage Estimation of Common Breaks in Panel Data Models via Adaptive Group Fused Lasso. Under Revision

Sato, A-H. (2013) Recursive segmentation procedure based on the Akaike information criterion test. 2013 IEEE 37th Annual Computer Software and Applications Conference, 226–233.

Wooldridge, J.M. (2010) Econometric Analysis of Cross Section and Panel Data. Second Edition, MIT Press.

Wu, W.B. (2002) Central limit theorems for functionals of linear processes and their applications. Statistica Sinica 12, 635–649.

Appendix A Proofs of Theorems 2.1–2.4 and Remarks 2.1 and 2.2

Throughout the proofs denotes unimportant constants whose values might change from line to line. Using (2.1) we have

where

| (A.1) |

and

| (A.2) |

Hence we have

| (A.3) | ||||

Let and define

Proof.

It is easy to see that for every

We prove that

| (A.6) |

Elementary arguments give

and therefore by Assumption 2.3(i) we have

Let . Using Assumption 2.1(i), for every by the Rosenthal inequality (cf. Petrov (1995, p. 59)) we have with

By the Cauchy–Schwarz inequality we conclude for all that

Using the definition of and Assumption 2.1(ii) we get that

and similarly

Also,

Thus applying Assumption 2.3(ii) we get that with some

Repeating the arguments used above we obtain that

and

resulting in

with some . Using Billingsley (1968, pp. 95 and 127) we conclude that the process is tight in

and therefore (A.6) holds.

The moment assumption in Assumption 2.4 with the maximal inequality of Móritz et al. (1982) yields that and therefore by Markov’s inequality we conclude

| (A.7) |

By (A.7) we get immediately that

| (A.8) |

Following the proof of (A.6) we get

and therefore by (A.7)

| (A.9) |

Similarly to (A.9) we have that

| (A.10) |

Using again Assumption 2.4 and the definition of , one can easily verify that

| (A.11) |

It follows from (A.6)–(A.11) that

and

which immediately implies Lemma A.1. ∎

According to (A.4), it is enough to consider the asymptotic behavior of

with any , where is defined in (4.2). It is easy to see that

| (A.12) | ||||

Lemma A.2.

Proof.

The result follows from Assumption 2.2 and the definition of . ∎

Proof.

We write

Using Assumption 2.3(i) we get that

| (A.14) |

Let . Elementary arguments give

| (A.15) | ||||

where in the last step we used Markov’s inequality. Let , where is given in Assumption 2.3(ii). The processes are independent in , so using the Rosenthal inequality (cf. Petrov (1995, p. 59)) we conclude with some , not depending on ,

Assumptions 2.1(i) and 2.3(ii) yield

| (A.16) |

and

| (A.17) |

Thus we conclude via (A.15)–(A.17)

Choosing with a large enough we get that

Let

| (A.18) |

It follows from the definition of that

Using Assumption 2.1(i), and 2.3(ii) with the Cauchy–Schwarz inequality we get that

and therefore

With we can write for that

By the Markov inequality we have

| (A.19) | ||||

Next we need a maximal inequality for double sum in the last term above. With we get that

By the independence of the processes in , Rosenthal’s inequality (cf. Petrov (1995, p.59)) implies that

| (A.20) |

We have via the Cauchy–Schwarz inequality

and therefore

Using that the ’s have mean zero and Assumption 2.3, we conclude

Similarly, by the definition of we get

and by applications of the Cauchy–Schwarz inequality we have

resulting in

Using the inequalities above, we get the upper bound for the moment in (A.20):

| (A.21) |

Applying the maximal inequality in Móritz et al. (1982) to (A.21) we conclude

Hence (A.19) implies that

resulting in

Similar arguments yield

which completes the proof of the lemma. ∎

Proof.

First we write

Applying the definition of with Assumptions 2.1(i) and 2.3(i), we get

It follows from the definition of that for all

where

Clearly, on account of Assumptions 2.1(i) and 2.3(i) and therefore

Repeating the arguments used in (A.19), by Markov’s inequality we have

| (A.22) | ||||

With we

Using Assumptions 2.1(i), 2.3(ii) and 2.5(ii) with Rosenthal’s inequality we conclude for all that

| (A.23) |

since by the multinomial theorem

The maximal inequality of Móricz et al. (1982) and (A.23) imply that

and therefore by (A.23) we have

| (A.24) | ||||

Thus we conclude that

and by similar arguments we have

which also completes the proof of the lemma. ∎

Proof.

We write . If , then

and therefore

Thus we get from Assumption 2.4 that

Repeating the arguments used in (A.19) we get that

Following the arguments used in the proofs of Lemmas A.3 and A.4 one can verify that

which implies that

Similar computations can be performed for and thus we conclude

As in the proof of Lemma A.3 we have that

| (A.25) |

The proof of the lemma is now complete. ∎

Proof.

Proof.

Proof of Remark 2.1. The proof of this remark follows Bai (2010) closely. We use (A.3). Since is fixed,

and by Assumption 2.3(i) and Markov’s inequality we have

By the Cauchy–Schwarz inequality and Assumption 2.3(i) we conclude

and therefore

Similar arguments give

and

The final term coming from (A.3) to consider is . Under the conditions of the remark, this is the asymptotically dominating term which has a unique maximum at . Hence Remark 2.1 is proven.

∎

Proof of Remark 2.2. Let

where and are defined in (A.1). We note that due to the assumption that the and are sequences of uncorrelated random variables we get that

| (A.28) |

and

| (A.29) |

with some constant . We write

with

where is defined in (A.2). We show that for all

| (A.30) |

which immediately implies Remark 2.2. We note that with some we have that for all . By the independence of the processes and V(t) we conclude

and therefore

Similarly,

since , completing the proof of (A.30). ∎

Proof.

By Lemma A.1 it is enough to prove that for all

| (A.32) |

Under Assumption 2.6(i) we choose , where is a constant. Using Lemmas A.2, A.3, A.5–A.7 and Assumption 2.5(ii) we obtain that

| (A.33) | ||||

for all . Also, by Lemmas A.2 and A.4 we obtain that

Hence Lemma A.8 is established under Assumption 2.6(i) and . ∎

Lemma A.9.

We assume that Assumptions 2.1–2.6 hold, and Then, as we have that

| (A.34) |

| (A.35) | ||||

| (A.36) |

| (A.37) |

| (A.38) |

and

| (A.39) |

for all , where and is defined in (A.18).

Proof.

First we note

Using the definition of and Assumption 2.5(i) we conclude

and

completing the proof of (A.34).

Similarly,

and

Computing the variance of we get

by Assumption 2.5(i), so (A.35) is proven.

Clearly,

By Assumption 2.4 we get that and therefore

We note that for all

and by Assumption 2.4 we have that and the process is tight in . Thus by stationarity we get

and similar arguments can be used on . We conclude that

| (A.40) |

completing the proof of (A.36) on account .

With we can write

We obtain from the proof of Lemma A.1 that

For every we have that

and

Next we show that is tight in . Using Rosenthal’s inequality (cf. Petrov (1995, p. 59)) we obtain that

with some constant . It is easy to see that

and

By the Cauchy–Schwarz inequality and Assumption 2.3(ii) we have for all

and therefore

where is a constant. Also, for of Assumption 2.3(ii) we have

with some constant . Thus we get via Assumption 2.3(ii) that

establishing tightness by Billingsley (1968, pp. 95 and 127). This also completes the proof of (A.37).

Following the arguments in the proof of (A.36) one can show that

and therefore (A.38) follows from Assumption 2.5(ii). To prove (A.39) we first write

Repeating the arguments used in the proof of (A.37) we obtain that

via applying Assumption 2.5(ii) and . ∎

Lemma A.10.

Proof.

For the sake of notational simplicity we write . Let and . Under (2.10) we write

Using Assumptions 2.1, 2.3, 2.7(i) and (2.10), we get that

Also, Assumptions 2.1(ii) and 2.7(ii) imply

| (A.41) | ||||

So using Lyapunov’s theorem (cf. Petrov (1995, p. 154)) we conclude via (2.8) that

where stands for a Wiener process. Applying the Cramér–Wold theorem (cf. Billingsley (1968, p. 49)) we obtain that the finite dimensional distributions of converge to that of . Next we show that is tight in . Following the arguments in (A.41), Rosenthal’s inequality yields for all

on account of Assumption 2.7(ii) and (2.8). The tightness now follows from Billingsley (1968, p. 127). ∎

Lemma A.11.

Proof.

Proof of Theorem 2.2. Let . It follows from Assumption 2.1(ii) and Lemma A.10 that for all

| (A.42) |

where is a two sided Wiener process. Also, and since by (A.40) we have that

| (A.43) |

By Lemma A.9 we conclude that for all

| (A.44) |

By the continuous mapping theorem we conclude from (A.44) that for all

| (A.45) |

According to the law of iterated logarithm, we have that

| (A.46) |

Now (2.11) follows from Lemma A.8, (A.45) and (A.46).

It follows from Assumption 2.1(ii), (A.43) and Lemmas A.9, A.11 that for every integer

| (A.47) | ||||

Observing that , the normality of with the Borel–Cantelli lemma yields that and therefore

Proof of Theorem 2.3. It follows from Assumption 2.8 that the Wiener processes in Assumption 2.9 and (A.42) are independent. Hence Lemma A.9 yields for all that

where is a two–sided Wiener process. Arguments used in (A.45) and (A.46) could be repeated to finish the proof of (2.15).

Referring again to Assumption 2.8 it is immediate that the Gaussian process and are independent. So applying Lemma A.9 we replace (A.47) with

for any . Observing that a.s. we need only minor modifications of the proof of (2.13) to complete the proof of (2.16). ∎

Proof.

Proof of Theorem 2.4. Let . Since is bounded, by (2.17) we have

| (A.50) |

Following the proof of Lemma A.9 one can show that for all

| (A.51) |

| (A.52) |

| (A.53) |

and

| (A.54) |

It follows from Assumptions 2.4 and 2.9 that for all

where denotes a two–sided Wiener process. Using now (A.51)–(A.54)

Arguments used in (A.45) and (A.46) could be repeated to complete the proof of Theorem 2.4. ∎

Appendix B Proof of Theorem 4.1

For the sake of brevity we use , and for , and , respectively . We start with the proof of (4.4). Let be a sequence satisfying

| (B.1) |

if the conditions of Theorem 2.2 or 2.3 hold and

| (B.2) |

under the assumptions of Theorem 2.4. First we show that for all satisfying we have that

| (B.3) |

Using (2.1) we have for all

Since , we have

| (B.4) |

Applying Assumption 2.4 with Markov’s and the maximal inequality of Móritz et al (1982) we obtained for all

| (B.5) | ||||

on account of Assumption 2.5. Following the proof of (B.5) but now using Assumptions 2.1(i) and 2.3, we conclude

| (B.6) | ||||

by Assumption 2.5(i). The stationarity in Assumption 2.1(ii) yields

| (B.7) | ||||

by Assumption 2.5(i) and the assumption that . Putting together (B.6) and (B.7) we obtain that

| (B.8) |

Following the proofs of (B.5) and (B.8) one can prove that

| (B.9) |

and

| (B.10) |

The result in (B.3) now follows from (B.4), (B.5) and (B.8)–(B.10). Since under our conditions

| (B.11) |

the proof of (4.4) is complete.

By (A.3) we have

where

and

It follows from the proofs of Lemmas A.3, A.5, A.6 and A.9 that for all satisfying (B.1) we have

where is defined in (4.3). Applying now Lemmas A.4, A.7 and A.9 we conclude

and

where

where

and

Using (B.1) and (B.11) one can verify that

and

where

Let and , as . Using Assumptions 2.3 and 2.4 we get

and

| (B.12) |

We claim that

| (B.13) |

The statement in (B.13) is a uniform weak law of large numbers, so we can repeat the proof of (B.4) to prove it. Namely, due to stationarity, it follows from Assumptions 2.3 and 2.4 that for every that

| (B.14) |

Now (B.13) follows from (B.14) if is tight. The tightness can be proven along the lines of the proofs of Lemmas A.4 and A.7. Our arguments show that

| (B.15) | ||||

Putting together (B.12), (B.13) and (B.15), the result in (4.5) follows.