Value of forecasts in planning under uncertainty:

Extended version

Abstract

In environments with increasing uncertainty, such as smart grid applications based on renewable energy, planning can benefit from incorporating forecasts about the uncertainty and from systematically evaluating the utility of the forecast information. We consider these issues in a planning framework in which forecasts are interpreted as constraints on the possible probability distributions that the uncertain quantity of interest may have. The planning goal is to robustly maximize the expected value of a given utility function, integrated with respect to the worst-case distribution consistent with the forecasts. Under mild technical assumptions we show that the problem can be reformulated into convex optimization. We exploit this reformulation to evaluate how informative the forecasts are in determining the optimal planning decision, as well as to guide how forecasts can be appropriately refined to obtain higher utility values. A numerical example of wind energy trading in electricity markets illustrates our results.

I Introduction

The intrinsically uncertain nature of renewable energy sources, for example their dependence on local weather conditions [1], impedes the reliable operation of the electricity grid [2]. Forecasts about the renewable energy generation provide a means to cope with this uncertainty. Hence the successful incorporation of forecasts into planning grid operation emerges as an important challenge, as well as the problem of obtaining forecasts that provide the most valuable information for planning.

Uncertainty is usually considered in a stochastic framework during the grid planning stage. Generation, for example, is modeled as a random variable, and planning decisions are made a certain length of time before the generation is realized at operation time. Planning in this context can provide probabilistic guarantees, for example, that undesirable events will happen with low probability, or that expected operation costs/utilities are optimized. Examples can be found in, e.g., dispatch problems [3], unit commitment [4], and participation in electricity markets [5, 6].

Solving such stochastic optimization problems relies on the availability of the underlying probability distribution of the uncertain quantities. The renewable generation forecasts however do not provide complete descriptions of the underlying uncertainty, in the sense that they do not completely describe the probability distribution of the generation. Certain questions arise in this context:

-

1.

How can forecasts of the quantities of interest be incorporated in a stochastic planning framework?

-

2.

How informative is a set of given forecasts to a specific planning problem?

The first question is crucial to reliably integrate renewable generation in the grid. The second question becomes practically relevant if obtaining forecasts during the planning stage incurs significant cost. This could be, for example, the computational cost of running complex renewable generation forecasting algorithms, typically combining numerical weather prediction models, historical data, local measurements, and simulations [7]. Alternatively these costs could be monetary, as is the case when grid operators and power producers do not create their own forecasts but instead purchase them in the form of products from companies specializing in forecasting [8, 9]. Understanding how valuable are the forecasts in determining planning decisions could help reduce the associated costs of obtaining such forecasts.

In this paper we take a step towards mathematically formalizing and answering the above questions. The simplest type of forecast for an uncertain quantity that is modeled as random is a point forecast, i.e., a single value thought as the most likely or the expected value of the quantity. However, more sophisticated types of forecasts, such as probabilistic forecasts, have been introduced for the case of renewable generation [7, 6]. Unlike point forecasts, probabilistic forecasts provide higher fidelity information about the probability distribution of the random quantity. Prediction intervals, i.e., bounds on the probability that the quantity takes values in certain intervals, are a common example [7].

We consider a general stochastic planning framework under probabilistic forecasts (Section II). We look for a planning decision that maximizes the expected value of a given utility function, but the probability distribution of the uncertain quantity, with respect to which the expectation is computed, is unknown and only described via the forecasts. We interpret the probabilistic forecasts as constraints defining a set of possible probability distributions for which the decision needs to account. Consequently a robust (max-min) planning problem is formulated to determine the decision that maximizes the worst-case expected utility, where the worst-case expectation is selected from the set of probability distributions consistent with the forecasts.

In Section III we utilize Lagrange duality theory [10] to show that the robust planning problem admits an equivalent reformulation to a single maximization problem with the introduction of auxiliary (dual) variables. This resulting problem is convex under certain relatively mild assumptions on the planning utility function, but it includes an infinite number of constraints. For the special case of forecasts in the form of prediction intervals we show that the constraints can be reduced to a finite number (Section III-A), resulting in a standard (finite-dimensional) convex optimization problem that can be solved readily [11].

The problem of selecting the worst-case probability distribution given probabilistic descriptions has been discussed previously in the context of optimal uncertainty quantification [12]. The difference in our formulation however is that an additional planning optimization level is considered. Related planning formulations under uncertainty about probability distributions have been considered in, e.g., [13, 14] and references therein, where the optimal planning is solved in a data-driven fashion based on samples from the unknown underlying distribution. Conceptually similar approaches have been considered in the context of power systems, where expected values in stochastic optimization are approximated using samples obtained from wind power forecasting algorithms [4, 15]. In contrast, planning in our work is decoupled from the data collection and does not rely on sample-based approximations, but instead utilizes the output of the forecasting procedures, i.e., the probabilistic forecasts themselves.

A further novelty of our approach is that it allows to characterize how valuable is the forecast information in determining the optimal planning decision. This characterization follows from a sensitivity analysis of the optimal planning objective value with respect to the forecast constraints (Section IV). Moreover, under the hypothesis that forecasts can be refined by, e.g., a forecasting oracle, we develop a sensitivity-driven procedure that sequentially selects forecast refinements to yield a higher robust planning utility value. Numerical examples of the proposed approach for trading wind energy in electricity markets [5, 6] are presented in Section V. Finally, we conclude with a discussion on our contributions and future work in Section VI.

II Problem description

We consider a decision-making framework under uncertainty. The unknown quantity of interest, for example the unknown renewable power generation, is denoted by and we assume that takes real values in a subset of the reals. We model as a random variable following some probability distribution on . As we will make clear, this distribution is not known completely. Hence there is uncertainty about the distribution of the random quantity of interest.

Suppose a decision-maker needs to select the value of a controlled parameter before the random quantity is realized, i.e., drawn from its probability distribution. We assume takes values in a convex subset of the reals. To rank the different choices for we assume that a function models the utility to the user if decision is taken a priori and the unknown quantity takes value . Technically we assume the utility function is continuous in both variables and , and also concave in for every value of , and concave in for every value of .

Example 1.

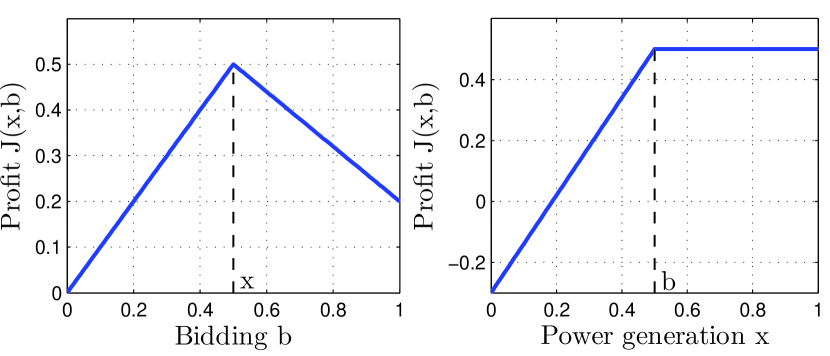

Consider the case of a wind power plant participating in a day-ahead electricity market [5, 6]. The producer provides a capacity bid in the market, which we can denote by a decision variable , representing the estimated renewable power generation that will be supplied to the grid at a future time interval. We let take values in the unit interval, , which can be interpreted as a normalized percentage with respect to the maximum capacity of the generator. If we denote by the actual realized power, also normalized in , a simple model [5] of the producer’s monetary profit from a realization after bidding is

| (1) |

where . The constant rewards high bids, while the constant penalizes a shortfall of generation compared to the bid, i.e., when . It is assumed that , implying that the profit decreases for higher shortfalls. The utility function, as can be seen in Fig. 1, satisfies the convexity assumptions of the general problem formulation.

A common assumption in planning problems under uncertainty is that the underlying probability distribution of the unknown quantity is known. In particular, if the random variable has a probability distribution , the expected utility to the user from a choice is given by

| (2) |

where the integral is over the range of values . The value that maximizes the expected utility in 2 becomes the optimal decision in this case.

In this paper however the underlying distribution is not completely known but only forecasts about the random quantity are available. We consider probabilistic forecasts [7, 6], which provide information about the underlying probability distribution of . More specifically we consider given (measurable) functions , for , of the random quantity , and forecasts stating that the expected value of these functions is upper bounded by some parameters , i.e.,

| (3) |

Both the functions and the parameters in these inequalities are given to the decision-maker, e.g., provided by some forecasting algorithm. We interpret the forecasts 3 as a set of constraints on the unknown underlying distribution , narrowing the uncertainty of the decision-maker regarding the distribution of . Based on this interpretation, we will interchangeably use the terms forecasts and constraints when referring to 3.

The constraint-based characterization of the uncertainty in 3 matches many common types of forecasts. For example bounds on mean value, second moment, or higher-order moments can be expressed in the form of 3 by appropriately selecting the function . In the following example we detail another special case, the prediction intervals. We will revisit this case later.

Example 2.

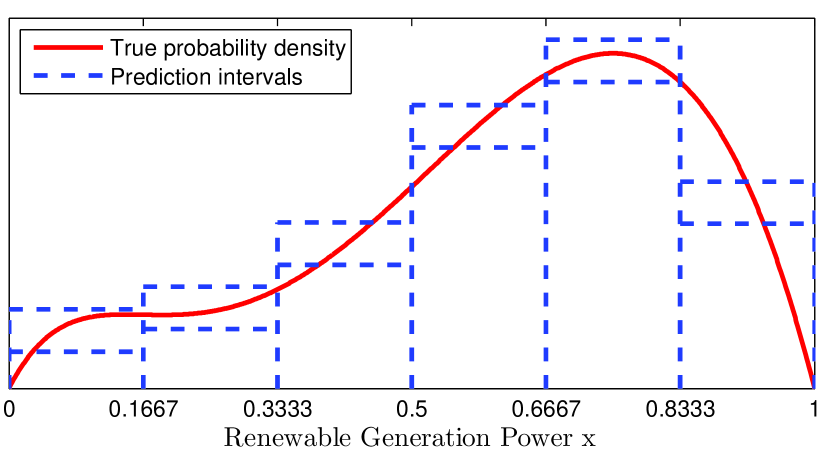

An example motivated by recent forecast methods for renewable generation [6] are prediction intervals. Suppose the renewable generation takes values in a normalized interval , partitioned into sub-intervals for , where , , and the forecasts take the form

| (4) |

In other words, this forecast provides upper and lower bounds on the probability that takes value in each of the intervals. These forecasts can be reformulated into the form of 3 by defining the indicator functions

| (5) |

for . Then the constraints 4 are equivalently written in the form of 3 as

| (6) |

A pictorial representation is given in Fig. 2.

We make the following technical assumption about the forecasts provided in 3.

Assumption 1.

There exists a probability distribution on such that the forecasts 3 are satisfied with strict inequality, i.e., for all .

This assumption states that the constraints 3 are feasible, and furthermore that strict feasibility holds. To motivate the feasibility, we can think of the actual underlying distribution of the random quantity, which is not known to the decision-maker, as satisfying the constraints 3. The strict feasibility is assumed for certain technical reasons in order to establish the results in the sequel of this paper, but is not practically restrictive. The parameters can always be perturbed to make the strict inequality assumption hold.

Given the constraint-based interpretation of the forecasts in 3, we can alternatively describe the planner’s uncertainty concerning the true distribution of the unknown quantity by a set containing the (possibly uncountably many) distributions that satisfy the forecasts 3. The set of all distributions consistent with forecasts 3 is

| (7) |

where we denote the set of all probability distributions on by . Here we parametrize the set with the forecast bounds , , grouped in a vector . For the current problem development, is fixed, but we introduce this parametrization for later use in Section IV. By Assumption 1 the set has a nontrivial interior, e.g., the true underlying distribution belongs in the set.

Having defined the utility of different choices to the decision-maker, as well as the possible distributions of the random quantity that the decision-maker can anticipate according to the probabilistic forecasts, we now pose a planning problem. The decision-maker needs to determine the value that robustly maximizes the worst-case expected utility anticipated from the forecasts, mathematically captured as a robust optimization problem

| (8) |

In other words, the planner looks for a decision that leads to the most favorable objective value assuming the worst-case distribution among the ones consistent with the forecast . We denote this robustly optimal objective value by , again parametrized by the forecast bounds for later use. We also denote the optimal planning decision as , assuming it exists.

The difficulty in solving the robust planning problem 8 lies in the max-min formulation. For every choice , one needs to solve a minimization problem with respect to the distribution to evaluate how good the choice is, and then infer how to improve on to maximize the objective function. To overcome this complexity, in the following section, we examine how the robust planning problem 8 can be equivalently written as a single-layer optimization problem. For the special case of forecasts given by prediction intervals (Example 2), we obtain an equivalent convex optimization problem from which can be determined efficiently.

We proceed in Section IV to characterize how informative the forecasts given by 3 are in determining the optimal planning decisions. To this end, we examine how sensitive the robust planning objective value is to changes in the forecast parameters . Based on this analysis, we also develop a methodology for improving the planning utility by appropriately refining forecasts.

III Robustly optimal planning

The robust planning problem described in 8 involves a max-min structure that makes it hard to determine the robustly optimal decision . In this section we follow an alternative path based on Lagrange duality theory [10]. Under certain technical conditions the inner minimization in 8 over probability distributions of the unknown quantity is equivalent to its Lagrange dual (maximization) problem. Replacing then the inner minimization in 8 with the equivalent maximization yields a maximization problem (with a single optimization layer) over the planning decision variable and additional (dual) variables. We state this result in the following theorem. Its proof relies on the results of [10].

Theorem 1.

Proof.

The proof relies on the strong duality results in [10]. First consider, for any value of , the inner minimization in 8, in which the optimization variable is a probability distribution over the unit interval . Formally this optimization variable can be expressed as a signed measure on the space equipped with the standard Borel -algebra. To be a probability measure, is required to be positive, denoted by , meaning that assigns a positive mass on any subset of that belongs in the standard Borel -algebra, and also to have a total mass equal to , . Under this change of variables from probability distributions to positive measures , and by the form of the set in 7, the inner minimization in 8 can be equivalently written as

| (12) | |||||

| subject to | (13) | ||||

| (14) | |||||

The robust optimization problem 8 is equivalent to .

The problem 12-14 is a linear program over measures [10]. It has constraints, stating that the -dimensional vector lies in a cone with a vertex at point . We now claim that if we perturb this vertex point to be anywhere in an open ball around the point , the resulting optimization problem of the form 12-14 is feasible.

Claim 1.

Let Assumption 1 hold. Then we can find an open ball around the point such that for any the set of signed measures

| (17) |

is non-empty.

We then derive the Lagrange dual problem of 12-14 by defining multipliers (dual variables) for each one of the inequality constraints 13, , as well as a multiplier for the equality constraint 14. Since every finite subset of the space belongs in the standard Borel -algebra, and all Dirac probability measures at points are candidates for positive measures in problem 12, it can be shown – see [10, p.11] – that the Lagrange dual problem becomes

| (18) | |||||

| subject to | |||||

| (19) | |||||

Then, [10, Prop. 3.4] shows that under the result of Prop. 1 the optimal values of the minimization in 12 and the maximization in 18 are equal, i.e., . This holds for any variable . Hence, returning to the original problem 8 and recalling that it can be written as , we also have that . In other words we can replace the minimization over distributions with the maximization over dual variables in 18-19. The resulting problem is a maximization over variables and corresponds exactly to problem 9. ∎

According to the theorem, the optimal choice of the robust planning problem 8 can be equivalently found by the optimization problem 9-11, and the optimal values of the two problems are equal. The advantage of the representation in 9-11 is that it bypasses the max-min structure of 8. There is a finite number of optimization variables in 9-11, i.e., the decision , as well as the dual variables and the vector . The caveat, although, is that the number of constraints is infinite and uncountable. Such optimization problems are called semi-infinite – see [16] for an overview. Nevertheless it is a convex optimization problem since the objective is linear and the constraint 10 for each value of defines a convex set due to the concavity of function in variable for any value .

General approaches for solving semi-infinite programs can be found in [16]. We examine however next the special case in which the forecasts 3 are given in the form of prediction intervals, described in Example 2. In that case it turns out that the number of constraints in the equivalent problem 9-11 can be reduced to a finite number. Hence we can pose the robust planning decision under prediction interval forecasts as a standard finite-dimensional convex optimization problem, for which efficient algorithms exist.

After this special case, we show in the following section that the optimal values of the additional variables in the optimization problem 9-11 can be interpreted as indicators of how valuable are the given forecasts in determining the optimal planning. Based on this interpretation, we also examine in the following section how updates on the forecasts can yield a higher planning objective value.

III-A Robust planning under prediction intervals

Consider forecasts given in the form of prediction intervals described in 4. By their reformulation into the generic form of forecasts presented in 6, we can pose the robust planning decision problem 8 into its equivalent form provided by Theorem 1 in 9-11. In particular, introducing dual variables for the upper bound constraints in 6, and similarly for the lower bounds, we have that robust planning follows from the solution to the problem

| (20) | ||||

| subject to | ||||

| (21) |

We note that the continuum of constraints 21 can be equivalently separated into the given intervals

| (22) |

for all . Note also that by the assumption that the function is concave in for all , it follows that , where the inequality is tight by continuity of function . Hence instead of checking 22 for a continuum of values for each , we only need to check at the two endpoints and . In other words, the problem 20-21 can be equivalently written as

| (23) | |||||

| subject to | |||||

| (24) | |||||

This optimization problem is convex and has a finite number of constraints. The number of constraints is twice the number of initial forecast intervals because essentially each forecast of the robust optimization is converted into two constraints, one for each of the two interval endpoints. The solution of 23 can be determined efficiently by standard convex optimization algorithms.

IV Relative value of forecasts

In this section we aim to quantify the value of the given forecasts 3 to the planner who needs to solve the robust planning problem 8. In particular, 3 defines a set of given forecasts and we are interested in determining how valuable information does each one of them provide to the planner. To this end, we examine how sensitive the robustly optimal objective , defined in 8, is to the given forecast values , i.e., what would the objective value become for deviations from the given parameters .

The forecast parameters determine the objective defined in 8 via the set of distributions appearing in the constraint of the inner minimization. To examine the sensitivity of when the given forecast parameters change to some new values for some , with the negative sign chosen for convention, we leverage the problem reformulation provided by Theorem 1. We exploit the well-known convex optimization fact that in general the optimal values of the Lagrange dual variables express the sensitivity of the objective of a convex optimization problem with respect to changes in the constraints - see [11, Ch. 5.6]. In our case, the robust planning 8 involves a two-layer (max-min) optimization objective, but a similar sensitivity result can be obtained. We state this result in the following theorem.

Theorem 2.

Proof.

Along with and already defined , let be a corresponding optimal solution to problem 9-11. Under Assumption 1 by Theorem 1, i.e., the equivalence of 8 and 9-11, we have for the optimal objective that

| (26) |

as well as

| (27) |

for all by the feasibility to constraints 10.

Fix any and consider defined by 8. By definition we have that

| (28) |

where the last inequality follows because is in general a suboptimal choice for . Following arguments similar to those in the proof of Theorem 1 we can show that the optimal value of the minimization on the right hand side of 28 is lower bounded by the optimal value of its Lagrange dual maximization problem111In fact in Theorem 1 we show that under Assumption 1 the two optimal values are equal for , but here for the equality might not hold.. Replacing this lower bound in 28 we have that

| (29) | |||||

| subject to | |||||

| (30) | |||||

Note now that and are feasible solutions for the last optimization problem as follows by 27, hence we have that

| (31) |

where the last equality follows by 26. Consequently the statement of the theorem holds. ∎

The theorem provides a lower bound on the optimal planning objective value of 8 after changes in the forecast bounds provided in 3. The change in the lower bound compared to is proportional to the change from to . The rate of change in planning objective units in each direction is given by the optimal value of the (dual) variable for each element . We can thus interpret the values as indicators of how valuable each one of the forecasts 3 is to the planner. A forecast with a high value is more informative compared to other forecasts because a small change in the given forecast bound gives a significant change in the (lower bound of the) objective. We also note that the values have already been obtained during the computation of the robust planning by 9, hence no further computation is required to determine them.

Remark 1.

The sensitivity analysis provided by Theorem 2 is performed with respect to the given forecast parameters , i.e., they are obtained locally for . At some other forecast parameter , the sensitivities, i.e., the values will differ. This difference matches the intuition that different forecasts provide different information. On the other hand the theorem provides a lower bound on the objective value at any deviation , not just locally around . It is also worth noting that the theorem does not provide any guarantee on how far the lower bound is with respect to the actual objective for such deviations.

Given the sensitivity-based characterization of how informative some given forecasts are, we next propose a method for refining/updating the forecasts in a way that increases the utility of the decision-making problem.

IV-A Forecast refinements

Suppose the decision-maker has access to a forecasting oracle, which upon request can refine one of the given forecasts in 3 – see Remark 2. Inspecting the particular type of forecasts we consider in 3 written as inequalities, a refined forecast of some inequality can be represented by decreasing the bound to a lower value . Equivalently, such decrease has the effect of shrinking the set of possible probability distributions that the decision-maker has to consider, as defined in 7, to a subset .

A question that arises in this context is how the decision-maker should select which of the forecasts of 8 to refine. This question is particularly important if the cost of refining forecasts is high, e.g., the computational cost of running extra simulations of a forecasting algorithm. The characterization of Theorem 2 suggests that the forecast that provides the most valuable information should be selected, i.e., the forecast with the highest value . Based on this intuition we propose the iterative forecast refinement procedure shown in Algorithm 1. On every iteration sensitivity values are obtained by solving the planning problem, and a refinement for the forecast bound with the highest sensitivity is requested (e.g. from the oracle) while all other bounds are kept constant. The procedure terminates, for example, if no further refinements are possible, or if the objective value improvements become insignificant.

Even though this procedure is motivated mainly by intuition, without theoretical claims in terms of optimality, convergence, etc., we note the following fact. On each iteration, according to 25 of Theorem 2, the robustly optimal utility value increases by at least an amount equal to . This minimum increase is proportional to the amount of change in the selected forecast parameter. If the selected forecast cannot be refined, i.e., , then no improvement in decision-making is achieved. In general, however, the result matches the intuition that with a better forecast, i.e., imposing a more constraining set in the minimization of 8, the objective value of the planning can only improve, i.e., the optimal value of 8 cannot decrease.

In the following section we present a numerical example for a wind power plant participating in an electricity market (Example 1) under prediction interval forecasts (Example 2). We demonstrate the methodology derived by Theorem 1 for determining the robustly optimal bidding decision. Additionally we perform the sensitivity analysis developed in this section and we implement the sensitivity-driven procedure for refining forecasts.

Remark 2.

The methodology for refining forecasts in this section is developed without considering a specific forecasting procedure. If, for example, an oracle obtains the forecasts by sampling from the true distribution of the unknown quantity, through simulations of an underlying stochastic model, then forecasts can be refined by drawing extra samples. However, a large number of extra samples might be required to improve upon the estimates of all the integrals in 3, e.g., in a Monte Carlo fashion. By focusing on only one of the integrals during refinement, as the oracle does in our hypothesis, the number of required samples can be reduced. This can be performed by variance reduction techniques, such as importance sampling [17], which aim at sampling more often from values important in estimating the selected integral.

V Application: Bidding in electricity markets under prediction intervals

In this section we apply our theoretical results in a numerical example of bidding renewable energy in electricity markets. This problem was introduced in Example 1, with the utility function representing the profit for the renewable generator and repeated here for convenience,

| (32) |

The utility involves a reward term proportional to the bid with a rate , and a penalty proportional to the generation shortfall with a rate . Here both and . Suppose also the generator obtains forecasts about the future generation value in the form of prediction intervals, introduced in Example 2. We consider the problem of determining the value of bidding that robustly maximizes the expected profit to the generator subject to the given forecasts about the renewable generation. This problem is mathematically described by the robust planning formulation 8. To solve this problem we adopt the reformulation into a convex optimization problem which was presented in Section III-A, and in particular takes the form 23-24.

In our numerical example, we consider forecasts for the probability that the random generation takes values in each of equal intervals that partition the total range of values , i.e., for – see also Example 2. To derive the lower and upper bounds, and respectively according to 4, we adopt the following procedure. We fix some true underlying probability distribution of the generation and we produce bounds by perturbing the true value computed with the underlying distribution. Specifically we consider perturbation by a constant amount below and above for each . Then only the resulting lower and upper bounds, and respectively, are available to the generator, not the underlying probability distribution used to create them.

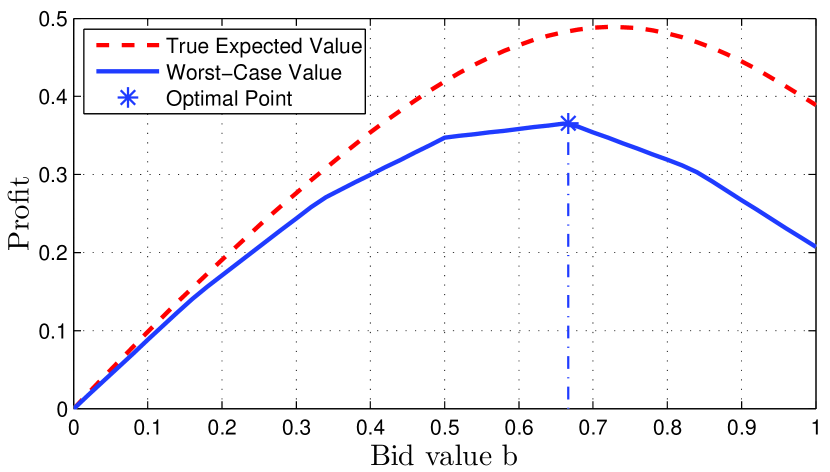

Given prediction intervals, shown in Fig. 2, we first solve the robust bidding problem, i.e., the convex optimization 23-24, for reward and penalty values in the profit function 32. We obtain an optimal bidding value roughly equal to . In Fig. 3 we illustrate the value of the worst-case expected profit, i.e., the objective in the planning problem 8, for all bid values as well as the optimal point. For comparison we also illustrate the expected profit computed using the underlying true probability distribution of for all bid values . The worst-case expected profit is an under-approximation of the true expected value, since the forecasts provide incomplete information about the underlying distribution. The optimal choice balances between the two extremes and , as expected by intuition, with being the most ”secure” bid but yielding a zero expected profit, and being the most ”risky” bid since it is certain that a shortfall will occur.

| Iter 1 | 0.66 | 0.39 | 0.12 | 0.00 | 0.00 | 0.00 |

| Iter 2 | 0.80 | 0.53 | 0.27 | 0.00 | 0.00 | 0.00 |

| Iter 3 | 0.80 | 0.53 | 0.27 | 0.00 | 0.00 | 0.00 |

| Iter 4 | 1.07 | 0.80 | 0.53 | 0.27 | 0.00 | 0.00 |

| Iter 1 | 0.00 | 0.00 | 0.00 | 0.14 | 0.41 | 0.41 |

| Iter 2 | 0.00 | 0.00 | 0.00 | 0.00 | 0.27 | 0.27 |

| Iter 3 | 0.00 | 0.00 | 0.00 | 0.00 | 0.27 | 0.27 |

| Iter 4 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

Moreover, we examine how the information provided by the given forecasts of Fig. 2 is valued by the decision maker. Following the development of Section IV, we examine the sensitivity of the robust bidding profit to the set of given forecasts. According to Theorem 2 this sensitivity is captured by the optimal values of the dual variables. In particular the sensitivity to upper and lower bounds of prediction intervals, and respectively, for , is captured by the dual variables and respectively, as introduced in Section III-A.

The sensitivity values in our example, as computed by solving 23-24, are shown in the first row of each of the Tables I, II. First we observe that at each interval , at most one of the upper or lower bound sensitivities is non-zero. The reason is that at most one of two bounds (cf. 4) is tight for the worst-case distribution at the robustly optimal point of problem 8. Second, from the dual values we see that the optimal profit is sensitive to the probability of both having a low generation (captured by ) as well as having a high generation (captured by ). In other words information about these events is the most informative. However the sensitivity is higher in the low generation case because the profit is significantly affected by shortfalls in this case.

Next we adopt the sensitivity-driven methodology developed in Section IV that uses a forecasting oracle to refine the given forecasts so that they become more informative for the robust bidding problem. Following Algorithm 1 we iteratively select to refine the forecast with the highest sensitivity value, i.e., one of the upper or lower bounds and for an interval in 4. If an upper bound is selected it gets decreased, and respectively if a lower bound is selected it gets increased. In our numerical example, the resulting new bound needs to be consistent with the true underlying distribution, so we model the following forecasting oracle. Upon request, the oracle can refine each upper or lower bound by a constant decrease or increase respectively, and the new bound is close enough to the true value so that the oracle cannot refine it any further. This model is chosen here for simplicity. In general, Algorithm 1 can be applied regardless of how the forecasting oracle operates.

We perform iterations of Algorithm 1 and the corresponding sensitivity values on each iteration are shown in Tables I, II. As already mentioned, has the higher value initially, so the upper bound on the first interval is refined (i.e., reduced). On the second iteration, after solving again the optimal planning 23-24, the new sensitivity values are obtained and again is the largest. Since the forecasting oracle described in our example cannot reduce the corresponding bound any further, the bound with the second largest sensitivity is selected to be refined, which is . On the third iteration, again are the largest, but due to the oracle model, the third largest is selected, and so on. It is worth noting that after some iterations we observe that the sensitivities of all lower bounds become zero. This means that currently they are not providing any valuable information, and refining (i.e., increasing) them does not necessarily offer an improvement in profit.

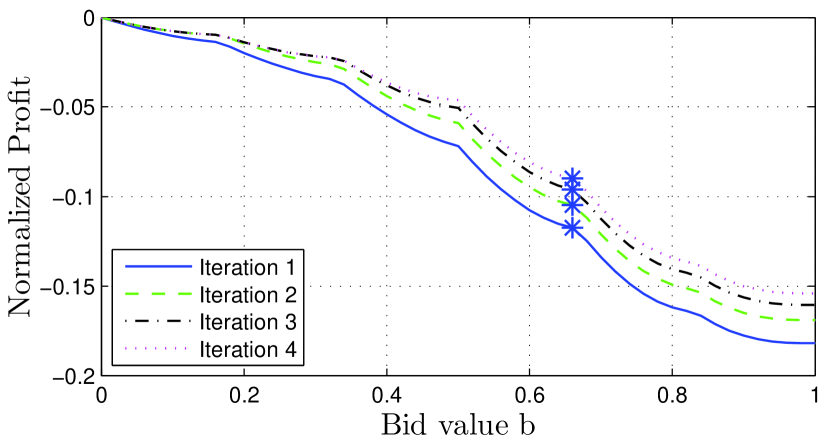

Finally, to examine the improvements in the bidding profit after these iterations of the refinement algorithm, we plot in Fig. 4 the worst-case expected profit, i.e., the objective in the planning problem 8, for all bid values . For visualization reasons the values are normalized by subtracting the true expected profit (the latter is larger, as shown in Fig. 3, so the plotted values are negative). We observe that as the forecasts are refined, the worst-case expected profit increases and gets closer to the actual expected profit (the baseline zero). In other words, the refined forecasts provide a more accurate model of the true profit. It is worth noting that the largest discrepancy between worst-case and true expected value happens at the high bid region, since the worst-case scenario assumes that generation takes the lowest possible values with the highest possible probability, making the associated shortfall costs large. We also note that in this example even though the optimal value of the profit increases with the forecast refinements, the optimal bidding value shown in Fig. 4 is the same. This is a consequence of the piecewise linear utility function in 32. For more general utility functions the optimal planning decision can change as well during the refinements, along with the optimal objective values, and our algorithm is able to track these changes.

VI Concluding remarks and future work

We examine how planning problems under uncertainty can utilize forecasts about uncertain quantities. By equivalently expressing forecasts as constraints on the possible probability distributions that the uncertain quantity can follow, the problem is cast as a robust optimization. The optimal planning seeks to maximize the expected value of a given utility function, integrated with respect to the worst-case distribution consistent with the forecasts. A reformulation into a convex optimization problem is presented, from which we can extract information about how valuable are the forecasts in determining the optimal planning decision.

Under the hypothesis that a forecasting oracle can refine the given forecasts upon request, i.e., that the set of possible probability distributions in the robust planning can be decreased, an iterative forecast refinement procedure is proposed in Section IV-A. Even though the procedure is justified theoretically, in practice the way refinements are performed depends on the employed forecasting algorithm. For example, it might be the case that many forecasts can be refined at the same time, instead of just one at a time as we consider, or that the requested forecast cannot be refined due to limitations of the oracle and/or because the forecast is very close to the true value. Moreover, besides just refining the set of given forecasts, as we consider, the oracle might generate new additional forecasts. Overall, coupling the proposed sensitivity-driven approach with forecasting algorithms used in practice requires further exploration.

More general problem formulations include the study of uncertain quantities evolving over time in a potentially correlated fashion, e.g., the random renewable generation during a time horizon in the future. Forecasting for such models has been considered in, e.g., scenario-based forecasts [18]. Furthermore, apart from uncertain quantities spread over time, the framework can be extended to include spatially distributed models as well, as in the case of correlated renewable generations at different physical locations in the grid.

-A Proof of Claim 1

The proposition equivalently states that we can find (the radius of ball ) such that for any that satisfies , , and , i.e., belongs in ball , the set 17 is non-empty. The proof is constructive. We first construct an appropriate ball radius , and then for any point in the ball we construct a measure in the set 17, i.e., satisfying

| (33) | |||

| (34) |

First, by Assumption 1 we have that there exists a probability measure such that

| (35) | |||

| (36) |

for some . Define the ball radius to be

| (37) |

Fix then any point . We need to show that there exists a signed measure such that 33 and 34 hold. Consider the measure defined by scaling the measure , i.e., at each set in the Borel -algebra of the set . Note that this measure is positive since , which follows from . Also this measure satisfies 34 since .

Hence it remains to show that 33 holds. The right hand side of 33 satisfies . Also, the left hand side of 33 satisfies

| (38) |

because of 35 and as we argued previously. Hence to show 33 it suffices to show that for all .

References

- [1] A. Mills, M. Ahlstrom et al., “Dark shadows,” IEEE Power and Energy Magazine, vol. 9, no. 3, pp. 33–41, 2011.

- [2] Y. V. Makarov, C. Loutan, J. Ma, and P. de Mello, “Operational impacts of wind generation on California power systems,” IEEE Transactions on Power Systems, vol. 24, no. 2, pp. 1039–1050, 2009.

- [3] P. P. Varaiya, F. F. Wu, and J. W. Bialek, “Smart operation of smart grid: Risk-limiting dispatch,” Proceedings of the IEEE, vol. 99, no. 1, pp. 40–57, 2011.

- [4] E. M. Constantinescu, V. M. Zavala, M. Rocklin, S. Lee, and M. Anitescu, “A computational framework for uncertainty quantification and stochastic optimization in unit commitment with wind power generation,” IEEE Transactions on Power Systems, vol. 26, no. 1, pp. 431–441, 2011.

- [5] E. Bitar, R. Rajagopal, P. Khargonekar, K. Poolla, and P. Varaiya, “Bringing wind energy to market,” IEEE Transactions on Power Systems, vol. 27, no. 3, pp. 1225–1235, 2012.

- [6] P. Pinson, C. Chevallier, and G. N. Kariniotakis, “Trading wind generation from short-term probabilistic forecasts of wind power,” IEEE Transactions on Power Systems, vol. 22, no. 3, pp. 1148–1156, 2007.

- [7] C. Monteiro, R. Bessa, V. Miranda, A. Botterud, J. Wang, G. Conzelmann et al., “Wind power forecasting: state-of-the-art 2009.” Technical Report, 2009, Available online.

- [8] K. Parks, Y.-H. Wan, G. Wiener, and Y. Liu, “Wind energy forecasting: A collaboration of the National Center for Atmospheric Research (NCAR) and Xcel Energy,” Technical Report, October 2011, Available online.

- [9] Innovations Across The Grid: Partnerships Transforming The Power Sector. The Edison Foundation, December 2013, Available online.

- [10] A. Shapiro, “On duality theory of conic linear problems,” in Semi-infinite programming. Springer, 2001, pp. 135–165.

- [11] S. Boyd and L. Vandenberghe, Convex Optimization. Cambridge University Press, 2009.

- [12] S. Han, U. Topcu, M. Tao, H. Owhadi, and R. M. Murray, “Convex optimal uncertainty quantification: Algorithms and a case study in energy storage placement for power grids,” in Proc. of the American Control Conference, 2013, pp. 1130–1137.

- [13] E. Delage and Y. Ye, “Distributionally robust optimization under moment uncertainty with application to data-driven problems,” Operations Research, vol. 58, no. 3, pp. 595–612, 2010.

- [14] E. Erdoğan and G. Iyengar, “Ambiguous chance constrained problems and robust optimization,” Mathematical Programming, vol. 107, no. 1-2, pp. 37–61, 2006.

- [15] Z. Zhou, A. Botterud, J. Wang, R. Bessa, H. Keko, J. Sumaili, and V. Miranda, “Application of probabilistic wind power forecasting in electricity markets,” Wind Energy, vol. 16, no. 3, pp. 321–338, 2013.

- [16] M. López and G. Still, “Semi-infinite programming,” European Journal of Operational Research, vol. 180, no. 2, pp. 491–518, 2007.

- [17] B. D. Ripley, Stochastic Simulation. John Wiley & Sons, 2009.

- [18] P. Pinson, H. Madsen, H. A. Nielsen, G. Papaefthymiou, and B. Klöckl, “From probabilistic forecasts to statistical scenarios of short-term wind power production,” Wind Energy, vol. 12, no. 1, pp. 51–62, 2009.