Toward robust early-warning models:

A horse race, ensembles and model uncertainty111 We are grateful to Johannes Beutel, Andras Fulop, Benjamin Klaus,

Jan-Hannes Lang, Tuomas A. Peltonen, Roberto Savona, Gregor von Schweinitz,

Eero Tölö, Peter Welz and Marika Vezzoli for useful comments on previous

versions of the paper. The paper has also benefited from comments

during presentations at BITA’14 Seminar on Current Topics in Business,

IT and Analytics in Helsinki on 13 October 2014, seminars at the Financial

Stability Surveillance Division at the ECB in Frankfurt am Main on

21 November 2014 and 12 January 2015, a seminar at the Bank of Finland

in Helsinki on 28 November 2014, the 1st Conference on Recent Developments

in Financial Econometrics and Applications at Deakin University in

Geelong on 4–5 December 2014, the XXXVII Annual Meeting of the Finnish

Economic Association in Helsinki on 12 February 2015, 8th Financial

Risks International Forum on Scenarios, Stress and Forecasts in Finance

in Paris on 30–31 March 2015, seminar at the European Commission

Joint-Research Centre in Ispra on 13 April 2015, seminar at the University

of Brescia on 14 April 2015, Financial Stability seminar at the Deutsche

Bundesbank in Frankfurt am Main on 21 May 2015, the SYRTO conference

’A Critical Evaluation of Econometric Measures for Systemic Risk’

in Amsterdam on 5 June 2015, the INFINITI conference in Ljubljana,

Slovenia on 9 June 2015, Financial Stability seminar at the Bank of

Estonia on 30 June 2015, seminar at University of Pavia on 3 September

2015, keynote at the 5th CCCS Student Science Fair at University of

Basel on 16 September 2015, and seminar at Aalto University on 11

January 2016. The horse race in this paper is an implementation of

a proposal for a Lamfalussy Fellowship in 2012. Several of the methods

and exercises presented in this paper have also been implemented in

an online platform for interactive modeling (produced in conjunction

with and is property of infolytika): http://cm.infolytika.com.

For further information see Holopainen and Sarlin [43]. The second

author thanks the GRI in Financial Services and the Louis Bachelier

Institute for financial support. All errors are our own. Corresponding

author: Peter Sarlin, Hanken School of Economics, Arkadiankatu 22,

00100 Helsinki, Finland, tel. +358405727670. E-mail: peter@risklab.fi.

Abstract

This paper presents first steps toward robust models for crisis prediction. We conduct a horse race of conventional statistical methods and more recent machine learning methods as early-warning models. As individual models are in the literature most often built in isolation of other methods, the exercise is of high relevance for assessing the relative performance of a wide variety of methods. Further, we test various ensemble approaches to aggregating the information products of the built models, providing a more robust basis for measuring country-level vulnerabilities. Finally, we provide approaches to estimating model uncertainty in early-warning exercises, particularly model performance uncertainty and model output uncertainty. The approaches put forward in this paper are shown with Europe as a playground. Generally, our results show that the conventional statistical approaches are outperformed by more advanced machine learning methods, such as -nearest neighbors and neural networks, and particularly by model aggregation approaches through ensemble learning.

keywords:

financial stability, early-warning models, horse race, ensembles, model uncertainty JEL codes: E440, F300, G010, G150, C430Non-technical summary

The repeated occurrence of financial crises at the turn of the 21st century has stimulated theoretical and empirical work on the phenomenon, not least early-warning models. Yet, the history of these models goes far back. Despite not always referring to macroprudential analysis, the early days of risk analysis relied on assessing financial ratios by hand rather than with advanced statistical methods on computers. During the 1960s, discriminant analysis emerged, being the most dominantly used technique until the 1980s. After the 1980s, DA has mainly been replaced by logit/probit models. Applications of these models range from early models for currency crises to recent ones on systemic financial crises. In parallel, the simple yet intuitive signal extraction approach that simply finds thresholds on individual indicators has gained popularity. With technological advances, a soar in data availability and a thriving need for progress in systemic risk identification, a new group of flexible and non-linear machine learning techniques have been introduced to various forms of financial stability surveillance. Recent literature indicates that these novel approaches hold promise for systemic risk identification because of their ability to identify and map complex dependencies. The premise of difference in performance relates to how methods treat two aspects: individual vs. multiple risk indicators and linear vs. non-linear relationships. While the simplest approaches linearly link individual indicators to crises, the more advanced techniques account for both multiple indicators and different types of non-linearity, such as the mapping of an indicator to crises and interaction effects between multiple indicators.

Despite the fact that some methods hold promise over others, the use and ranking of them is not an unproblematic task. This paper touches upon three problem areas. First, there are few objective and thorough comparisons of conventional and novel methods, and thus neither unanimity on an overall ranking of methods nor on a single best-performing method. Second, given an objective comparison, it is still unclear whether one method can be generalized to outperform others on every single dataset. It is not seldom that different approaches capture different types of vulnerabilities, and hence can be seen to complement each other. Despite potential differences in performance, this would contradict the existence of one single best-in-class method, and instead suggest value in simultaneous use of multiple approaches, or so-called ensembles. Yet, the early-warning literature lacks a structured approach to the use of multiple methods. Third, even if one could identify the best-performing methods and come up with an approach to make use of multiple methods simultaneously, the literature on early-warning models lacks measures of statistical significance or uncertainty. Although crisis probabilities may breach a threshold, there is no work testing the possibility of an exceedance to have occurred due to sampling error alone. Likewise, little or no attention has been given to testing equality of two methods’ early-warning performance or individual probabilities and thresholds.

This paper aims at providing a solution to all of the three above mentioned challenges. First, we conduct an objective horse race of methods for early-warning models, including a large number of common techniques from conventional statistics and machine learning, with a particular focus on the problem as a classification task. The objectivity of the exercise derives from identical sampling into in-sample and out-of-sample data for each method, identical model selection, and identical model specification. For generalizability and comparability, we make use of cross-validation and recursive real-time estimation to assure that and assess how results generalize to out-of-sample data. The two exercises differ in their sampling of data, particularly the in-sample and out-of-sample partitions used for each estimation. While cross-validation is common in machine learning and allows an efficient use of small samples, exercises may benefit from the fact that data are sampled randomly despite most likely exhibiting time dependence. The recursive exercises, on the contrary, account for time dependence in data by strictly using historical samples for out-of-sample predictions, which nevertheless requires more data, particularly in the time-series dimension. These two exercises allow exploring performance across methods, and how that is impacted by the evaluation exercise.

Second, acknowledging the fact that no one method can be generalized to outperform all others, we put forward two strands of approaches for the simultaneous use of multiple methods. A natural starting point is to collect model signals from all methods in the horse race, in order to assess the number of methods that signal for a given country at a given point in time. Two structured approaches involve choosing the best method (in-sample) for out-of-sample use, and relying on the majority vote of all methods together. Then, moving toward more standard ensemble methods for the use of multiple methods, we combine model output probabilities into an arithmetic mean of all methods. With potential further gains in aggregation, we take a performance-weighted mean by letting methods with better in-sample performance contribute more to the aggregated model output. Third, we provide approaches to testing statistical significance in early-warning exercises, including both model performance and output uncertainty. With the sampling techniques of repeated cross-validation and bootstrapping, we estimate properties of the performance of models, and may hence test for statistical significance when ranking models. Further, through sampling techniques, we may also use the variation in model output and thresholds to compute properties for capturing their reliability for individual observations. Beyond confidence bands for representation of uncertainty, this also provides a basis for hypothesis testing, in which an interest of importance ought to be whether a model output is statistically significantly different from the cut-off threshold.

The approaches put forward in this paper are illustrated in a European setting, for which we use a large number of macro-financial indicators for 15 European economies since the 1980s. First, we present rankings of all methods for the objective horse race, after which we proceed to aggregation and statistical significance tests. Generally, our results show that the classical approaches are outperformed by more advanced machine learning methods, such as -nearest neighbors and neural networks, in terms of the Usefulness and Area Under the Curve (AUC) measures. This holds for both horse race exercises. While several of the differences in rankings are statistically insignificant, a particular finding is the outperformance of ensemble models, which is significant in both exercises. More importantly, the objective exercises in this paper provide strong evidence that early-warning modeling in general is a useful tool to identify systemic risk at an early stage.

1 Introduction

Systemic risk measurement lies at the very core of macroprudential oversight, yet anticipating financial crises and issuing early warnings is intrinsically difficult. The literature on early-warning models has, nevertheless, shown that it is no impossible task. This paper provides a three-fold contribution to the early-warning literature: (i) a horse race of early-warning methods, (ii) approaches to aggregating model output from multiple methods, and (iii) model performance and output uncertainty.

The repeated occurrence of financial crises at the turn of the 21st century has stimulated theoretical and empirical work on the phenomenon, not least early-warning models. Yet, the history of these models goes far back. Despite not always referring to macroprudential analysis, the early days of risk analysis relied on assessing financial ratios by hand rather than with advanced statistical methods on computers (e.g., Ramser and Foster [66]). After Beaver’s [9] seminal work on a univariate approach to discriminant analysis (DA), Altman [4] further developed DA for multivariate analysis. Even though DA suffers from frequently violated assumptions like normality of the indicators, it was the dominant technique until the 1980s. Frank and Cline [38] and Taffler and Abassi [83], for example, used DA for predicting sovereign debt crises. After the 1980s, DA has mainly been replaced by logit/probit models. Applications of these models range from the early model for currency crises by Frankel and Rose [39] to a recent one on systemic financial crises by Lo Duca and Peltonen [62]. In parallel, the simple yet intuitive signal extraction approach that simply finds thresholds on individual indicators has gained popularity, again ranging from early work on currency crises by Kaminsky et al. [51] to later work on costly asset booms by Alessi and Detken [1]. Yet, these methods suffer from assumptions violated more often than not, such as fixed distributional relationship between the indicators and the response (e.g., logistic/normal), and the absence of interactions between indicators (e.g., non-linearities in crisis probabilities with increases in fragilities). With technological advances, a soar in data availability and a thriving need for progress in systemic risk identification, a new group of flexible and non-linear machine learning techniques have been introduced to various forms of financial stability surveillance. Recent literature indicates that these novel approaches hold promise for systemic risk identification (e.g., as reviewed in Demyanyk and Hasan [24] and Sarlin [71]).222See also a number of applications, such as Nag and Mitra [63], Franck and Schmied [37], Peltonen [64], Sarlin and Marghescu [76], Sarlin and Peltonen [77], Sarlin [73] and Alessi and Detken [2]. The premise of difference in performance relates to how methods treat two aspects: individual vs. multiple risk indicators and linear vs. non-linear relationships. While the simplest approaches linearly link individual indicators to crises, the more advanced techniques account for both multiple indicators and different types of non-linearity, such as the mapping of an indicator to crises and interaction effects between multiple indicators.

Despite the fact that some methods hold promise over others, the use and ranking of them is not an unproblematic task. This paper touches upon three problem areas. First, there are few objective and thorough comparisons of conventional and novel methods, and thus neither unanimity on an overall ranking of methods nor on a single best-performing method. Though the horse race conducted among members of the Macro-prudential Research Network of the European System of Central Banks aims at a prediction competition, it does not provide a solid basis for objective performance comparisons [3]. Even though disseminating information of models underlying discretionary policy discussion is a valuable task, the panel of presented methods are built and applied in varying contexts. This relates more to a horse show than a horse race. Second, given an objective comparison, it is still unclear whether one method can be generalized to outperform others on every single dataset. It is not seldom that different approaches capture different types of vulnerabilities, and hence can be seen to complement each other. Despite potential differences in performance, this would contradict the existence of one single best-in-class method, and instead suggest value in simultaneous use of multiple approaches, or so-called ensembles. Yet, the early-warning literature lacks a structured approach to the use of multiple methods. Third, even if one could identify the best-performing methods and come up with an approach to make use of multiple methods simultaneously, the literature on early-warning models lacks measures of statistical significance or uncertainty. Moving beyond the seminal work by El-Shagi et al. [33], where the authors put forward approaches for assessing the null of whether or not a model is useful, there is a lack of work estimating statistically significant differences in performance among methods. Likewise, although crisis probabilities may breach a threshold, there is no work testing the possibility of an exceedance to have occurred due to sampling error alone. While Hurlin et al. [47] provide a general-purpose equality test for firms’ risk measures, little or no attention has been given to testing equality of two methods’ early-warning performance or individual probabilities and thresholds.

This paper aims at providing a solution to all of the three above mentioned challenges. First, we conduct an objective horse race of methods for early-warning models, including a large number of common techniques from conventional statistics and machine learning, with a particular focus on the problem as a classification task. The objectivity of the exercise derives from identical sampling into in-sample and out-of-sample data for each method, identical model selection, and identical model specification. For generalizability and comparability, we make use of cross-validation and recursive real-time estimation to assure that and assess how results generalize to out-of-sample data. Rather than an absolute ranking that could be generalized to any context, this provides evidence on the potential in more advanced machine learning approaches in these types of exercises, as well as points to the importance of using appropriate resampling techniques, such as accounting for time dependence. Second, acknowledging the fact that no one method can be generalized to outperform all others, we put forward two strands of approaches for the simultaneous use of multiple methods. A natural starting point is to collect model signals from all methods in the horse race, in order to assess the number of methods that signal for a given country at a given point in time. Two structured approaches involve choosing the best method (in-sample) for out-of-sample use, and relying on the majority vote of all methods together. Then, moving toward more standard ensemble methods for the use of multiple methods, we combine model output probabilities into an arithmetic mean of all methods. With potential further gains in aggregation, we take a performance-weighted mean by letting methods with better in-sample performance contribute more to the aggregated model output. Third, we provide approaches to testing statistical significance in early-warning exercises, including both model performance and output uncertainty. With the sampling techniques of repeated cross-validation and bootstrapping, we estimate properties of the performance of models, and may hence test for statistical significance when ranking models. Further, through sampling techniques, we may also use the variation in model output and thresholds to compute properties for capturing their reliability for individual observations. Beyond confidence bands for representation of uncertainty, this also provides a basis for hypothesis testing, in which an interest of importance ought to be whether a model output is statistically significantly different from the cut-off threshold.

The approaches put forward in this paper are illustrated in a European setting, for which we use a large number of macro-financial indicators for 15 European economies since the 1980s. First, we present rankings of all methods for the objective horse race, after which we proceed to aggregation and statistical significance tests. Generally, our results show that the classical approaches are outperformed by more advanced machine learning methods, such as -nearest neighbors and neural networks, in terms of the Usefulness and Area Under the Curve (AUC) measures. This holds for both horse race exercises. While several of the differences in rankings are statistically insignificant, a particular finding is the outperformance of ensemble models, which is significant in both exercises. More importantly, the objective exercises in this paper provide strong evidence that early-warning modeling in general is a useful tool to identify systemic risk at an early stage.

This paper is organized as follows. In Section 2, we describe the used data, including indicators and events, the methods for the early-warning models, and estimation strategies. Then, we present the set-up for the horse race, as well as approaches for aggregating model output and computing model uncertainty. In Section 4, we present results of the horse race, its aggregations, and model uncertainty in a European setting. Finally, we conclude in Section 5.

2 Data and methods

This section presents the data and methods used in the paper. Whereas the dataset covers both crisis event definitions and vulnerability indicators, the methods include classification techniques ranging from conventional statistical modeling to more recent machine learning algorithms.

2.1 Data

The dataset used in this paper has been collected with the aim of covering as many European economies as possible. While a focus on similar economies might improve homogeneity in early-warning models, we aim at collecting a dataset as large as possible for the data-demanding estimations. The data used in this paper are quarterly and span from 1976Q1 to 2014Q3. The sample is an unbalanced panel with 15 European Union countries: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Spain, Sweden, and the United Kingdom. In total, the sample includes 15 crisis events, which cover systemic banking crises. The dataset consists of two parts: crisis events and vulnerability indicators. In the following, we provide a more detailed description of the two parts.

Crisis events

The crisis events used in this paper are chosen as to cover country-level distress in the financial sector. We are concerned with banking crises with systemic implications and hence mainly rely on the IMF’s crisis event initiative by Laeven and Valencia [59]. Yet, as their database is partly annual, we complement our events with starting dates from the quarterly database collected by the European System of Central Banks (ESCB) Heads of Research Group, and as reported in Babecky et al. [7]. The database includes banking, currency and debt crisis events for a global set of advanced economies from 1970 to 2012, of which we only use systemic banking crisis events.333To include events after 2012, as well as some minor amendments to the original event database by Babecky et al. (2013), we rely on an update by the Countercyclical Capital Buffer Working Group within the ESCB. In general, both of the above databases are a compilation of crisis events from a large number of influential papers, which have been complemented and cross-checked by ESCB Heads of Research. The paper with which the events have been cross-checked include Kindleberger and Aliber [53], IMF [48], Reinhart and Rogoff [67], Caprio and Klingebiel [19], Caprio et al. [20], and Kaminsky and Reinhart [50] among many others.

Early-warning indicators

The second part of the dataset consists of a number of country-level vulnerability indicators. Generally, these cover a range of macro-financial imbalances. We include measures covering asset prices (e.g., house and stock prices), leverage (e.g., mortgages, private loans and household loans), business cycle indicators (GDP and inflation), measures from the EU Macroeconomic Imbalance Procedure (e.g., current account deficits and government debt), and the banking sector (e.g., loans to deposits). In most cases, we have relied on the most commonly used transformation, such as ratios to GDP or income, growth rates, and absolute and relative deviations from a trend. The indicators are sourced from Eurostat, OECD, ECB Statistical Data Warehouse and the BIS Statistics.

For detrending, the trend is extracted using one-sided Hodrick–Prescott filter (HP filter). This means that each point of the trend line corresponds to the ordinary HP trend calculated recursively from the beginning of the series to each point in time. By doing this, we do not use future information when calculating the trend, but rather use the information set available to the policymaker at each point in time. The smoothness parameter of the HP filter is specified to be 400 000 as suggested by Drehmann et al. [25]. This has been suggested to appropriately capture the nature of financial cycles in quarterly data. Growth rates are defined to be annual, whereas we follow Lainà et al. [60] by using both absolute and relative deviations from trend, of which the latter differs from the former by relating the deviation to the value of the trend. The indicators used in this paper combine several sources for broad coverage and for deriving ratios of appropriate variables, and are presented in Table 1. Their descriptive statistics are shown in Table 2.

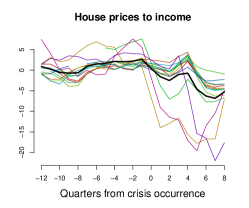

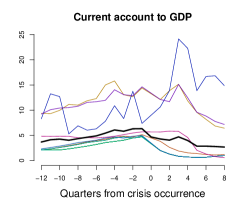

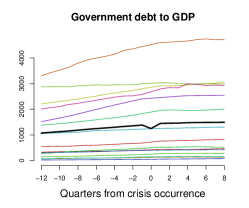

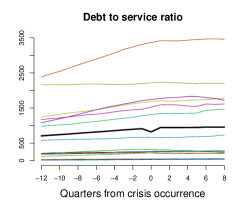

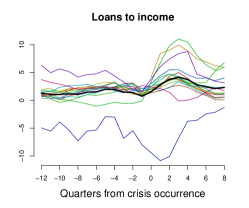

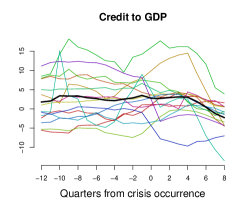

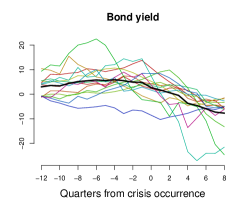

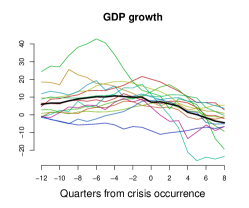

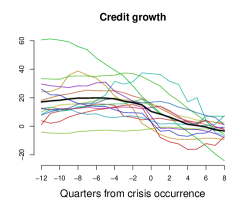

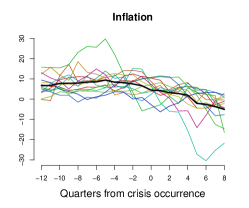

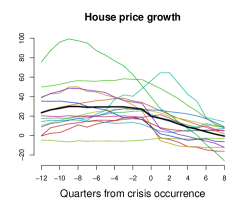

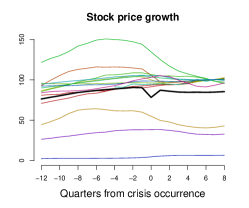

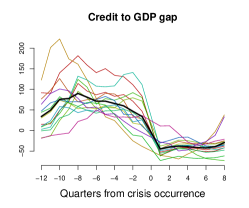

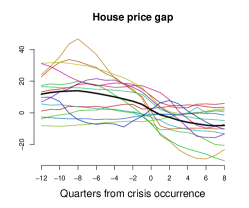

As proper use of data is essential in order to obtain an objective indication of the usefulness of any modeling approach, a note regarding the relationship between crisis events and indicators is in order. Whilst the uncertainty regarding the definitions of crisis events cannot be disputed, this holds true for any empirical exercise. To visualize the relationship between the actual crisis events and the indicators, as well as their lead time, we include time-series plots for each indicator from to around crisis occurrences in Figure A.1. The figure illustrates that patterns of several indicators, such as the credit gap and asset price changes, for instance, take elevated values prior to crisis events, which is indeed in line with the early-warning literature.

![[Uncaptioned image]](/html/1501.04682/assets/x1.png)

![[Uncaptioned image]](/html/1501.04682/assets/x2.png)

2.2 Early warning as a classification problem

Early-warning models require evaluation criteria that account for the nature of the underlying problem, which relates to low-probability, high-impact events. It is of central importance that the evaluation framework resembles the decision problem faced by a policymaker. The signal evaluation framework focuses on a policymaker with relative preferences between type I and II errors, and the usefulness that she derives by using a model, in relation to not using it. In the vein of the loss-function approach proposed by Alessi and Detken [1], the framework applied here follows an updated and extended version in Sarlin [74].

To mimic an ideal leading indicator, we build a binary state variable for observation (where ) given a specified forecast horizon . Let be a binary indicator that is one during pre-crisis periods and zero otherwise. For detecting events using information from indicators, we need to estimate the probability of being in a vulnerable state . Herein, we make use of a number of different methods for estimating , ranging from the simple signal extraction approach to more sophisticated techniques from machine learning. The probability is turned into a binary prediction , which takes the value one if exceeds a specified threshold and zero otherwise. The correspondence between the prediction and the ideal leading indicator can then be summarized into a so-called contingency matrix, as described in Table 3.

| Actual class | |||

|---|---|---|---|

| Pre-crisis period | Tranquil period | ||

| Predicted class | Signal | Correct call | False alarm |

| True positive (TP) | False positive (FP) | ||

| No signal | Missed crisis | Correct silence | |

| False negative (FN) | True negative (TN) | ||

The frequencies of prediction-realization combinations in the contingency matrix can be used for computing measures of classification performance. A policymaker can be thought to be primarily concerned with two types of errors: issuing a false alarm and missing a crisis. The evaluation framework described below is based upon that in Sarlin [74] for turning policymakers’ preferences into a loss function, where the policymaker has relative preferences between type I and II errors. While type I errors represent the share of missed crises to the frequency of crises FN/(TP+FN), type II errors represent the share of issued false alarms to the frequency of tranquil periods FP/(FP+TN). Given probabilities of a model, the policymaker then finds an optimal threshold such that her loss is minimized. The loss of a policymaker includes and , weighted by relative preferences between missing crises () and issuing false alarms (). By accounting for unconditional probabilities of crises and tranquil periods , as classes are not of equal size and errors are scaled with class size, the loss function can be written as follows:

| (1) |

Further, the Usefulness of a model can be defined in a more intuitive manner. First, the absolute Usefulness () is given by:

| (2) |

which computes the superiority of a model in relation to not using any model. As the unconditional probabilities are commonly unbalanced and the policymaker may be more concerned about the rare class, a policymaker could achieve a loss of by either always or never signaling a crisis. This predicament highlights the challenge in building a Useful early-warning model: With a non-perfect model, it would otherwise easily pay-off for the policymaker to always signal the high-frequency class. Second, we can compute the relative Usefulness as follows:

| (3) |

where of the model is compared with the maximum possible usefulness of the model. That is, the loss of disregarding the model is the maximum available Usefulness. Hence, reports as a share of the Usefulness that a policymaker would gain with a perfectly-performing model, which supports interpretation of the measure. It is worth noting that better lends to comparisons over different .

Beyond the above measures, the contingency matrix may be used for computing a wide range of other quantitative measures.444Some of the commonly used evaluation measures include: Recall positives (or TP rate) = TP/(TP+FN), Recall negatives (or TN rate) = TN/(TN+FP), Precision positives = TP/(TP+FP), Precision negatives = TN/(TN+FN), Accuracy = (TP+TN)/(TP+TN+FP+FN), FP rate = FP/(FP+TN), and FN rate = FN/(FN+TP) Receiver operating characteristics (ROC) curves and the area under the ROC curve (AUC) are also used for comparing performance of early-warning models and indicators. The ROC curve plots, for the complete range of , the conditional probability of positives to the conditional probability of negatives:

2.3 Classification methods

The purpose of any classification algorithm is to identify to which of a set of classes a new observation belongs, based on one or more predictor variables. Classification is considered an instance of supervised learning, where a training set of correctly identified observations is available. In this paper, a number of probabilistic classifiers are used, whose outputs are probabilities indicating to which of the qualitative classes an observation belongs. In our case, the dependent (or outcome) variable represents the two classes of pre-crisis periods (1) and tranquil periods (0).

Generally, a classifier attempts to assign each observation to the most likely class, given its predictor values. For the binary case, where there are only two possible classes, an optimal classifier (which minimizes the error rate) predicts class one if , and class zero otherwise. This classifier is denoted as the Bayes classifier. Ideally, one would like to predict qualitative responses using the Bayes classifier, but for real-world data, however, the conditional distribution of given is unknown. Thus, the goal of many approaches is to estimate this conditional distribution and classify an observation to the category with the highest estimated probability. For real-world applications, it may also be noted that the optimal threshold between classes is not always 0.5, but varies. This optimal threshold may be a result of optimizing the above discussed Usefulness, and is examined in further detail later in the paper.

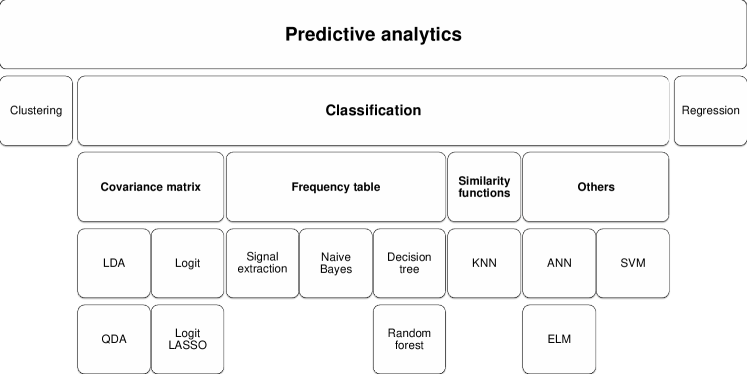

This paper aims to gather a versatile set of different classification methods, from the simple approach of signal extraction to the considerably more computationally intensive neural networks and support vector machines. The methods used for deriving early-warning models have been put into context in Figure 1 and papers applying these methods in an early-warning exercise have been reviewed in Table 4. The methods are presented in more detail below.

Signal extraction

The signal extraction approach introduced by Kaminsky et al. [51] simply analyzes the level of an indicator, and issues a signal if the value exceeds a specified threshold. In order to issue binary signals, we specify the threshold value as to optimize classification performance, which is herein measured with relative Usefulness [50]. However, the key limitation of this approach is that it does not enable any interaction between or weighting of indicators, while an advantage is that it demonstrates a more direct measure of the importance and provides a ranking of each indicator.555We are aware of the multivariate signal extraction, but do not consider it herein as we judge logit analysis, among others, to cover the idea of estimating weights for transforming multiple indicators into one output. Despite this, it is one of the most commonly applied early-warning techniques.

Linear Discriminant Analysis (LDA)

LDA, introduced by Fisher [36], is a commonly used method in statistics for expressing one dependent variable as a linear combination of one or more continuous predictors. LDA assumes that the predictor variables are normally distributed, with a mean vector and a common covariance matrix for all classes, and implements Bayes’ theorem to approximate the Bayes classifier. LDA has been shown to perform well on small data sets, if the above-mentioned conditions apply. Yet even though DA suffers from the frequently violated assumptions, it was the dominant technique until the 1980s, after which it was oftentimes replaced by logit/probit models.

Quadratic Discriminant Analysis (QDA)

QDA is a variant of LDA, which estimates a separate covariance matrix for each class (see, e.g., Venables and Ripley [86]). This causes the number of parameters to estimate to rise significantly, but consequently results in a non-linear decision boundary. To the best of our knowledge, QDA has not been applied for early-warning exercises at the country level.

Logit analysis

Much of the early-warning literature deals with models that rely on logit/probit regression. Logit analysis uses the logistic function to describe the probability of an observation belonging to one of two classes, based on a regression of one or more continuous predictors. For the case with one predictor variable, the logistic function is . From this, it is obvious to extend the function to the case of several predictors. Logit and probit models have frequently been applied to predicting financial crises, as can be seen in an early review by Berg et al. [11]. However, the distributional (logistic/normal) assumption on the relationship between the indicators and the response as well as the absence of interactions between variables may often be violated. Lo Duca and Peltonen [62], for example, show that the probability of a crisis increases non-linearly as the number of fragilities increase.

Logit LASSO

The LASSO (Least Absolute Shrinkage and Selection Operator) logistic regression (Tibshirani [84]) attempts to select the most relevant predictor variables for inference and is often applied to problems with a large number of predictors. The method maximizes the log likelihood subject to a bound on the sum of absolute values of the coefficients , for which the is penalized by the norm. This implies that the LASSO sets some coefficients to equal zero, and produces sparse models with a simultaneous variable selection. The optimal penalization parameter is oftentimes chosen empirically via cross-validation. We are only aware of the use of the Logit LASSO in this context in Lang et al. [61], wherein it is mainly used to identify risks in bank-level data, but also aggregated to the country level for assessing risks in entire banking sectors.

Naive Bayes

In machine learning, the Naive Bayes method is one of the most common Bayesian network methods (see e.g. Kohavi et al. [57]). Bayesian learning is based on calculating the probability of each hypothesis (or relation between predictor and response), given the data. The method is called ’naive’ as it assumes that the predictor variables are conditionally independent. Consequently, the method may give high weights to several predictors which are correlated, unlike the methods discussed above, which balance the influence of all predictors. However, the method has been known to scale well to large problems. To the best of our knowledge, Naive Bayes has not been applied for early-warning exercises at the country level.

-nearest neighbors (KNN)

KNN is a non-parametric method which uses similarity functions to determine the class of an observation based on its nearest observations (see, e.g. Altman [5]). Given a positive integer and an observation , the algorithm first identifies the points in the data closest to . The probability for belonging to a class is then estimated as the fraction of the closest points, whose response values correspond with the respective class. The method is considered to be among the simplest in the realm of machine learning, and has two free parameters, the integer and a parameter which affects the search distance for neighbors, which can be optimized for each data set. As with Naive Bayes, we are not aware of previous use of KNN in early-warning exercises at the country level.

Classification trees

Classification trees, as discussed by Breiman et al. [17], implement a decision tree-type structure, which reach a decision by performing a sequence of tests on the values of the predictors. In a classification tree, the classes are represented by leaves, and the conjunctions of predictors are represented by the branches leading to the classes. These conjunction rules segment the predictor space into a number of simpler regions, allowing for decision boundaries of complex shapes. Given similar loss functions, an identical result could also be reached through sequential signal extraction. The method has proven successful in many areas of machine learning, and has the advantage of high interpretability. To reduce complexity and improve generalizability, sections of the tree are often pruned until optimal out-of-sample performance is reached. The degree of pruning is determined by a complexity parameter, which is used in this paper as a free parameter. In the early-warning literature, the use of classification trees has been fairly common.

Random forest

The random forest method, introduced by Breiman [15], uses classification trees as building blocks to construct a more sophisticated method, at the expense of interpretability. The method grows a number of classification trees based on differently sampled subsets of the data. Additionally, at each split, a randomly selected sample is drawn from the full set of predictors. Only predictors from this sample are considered as candidates for the split, effectively forcing diversity in each tree. Lastly, the average of all trees is calculated. As there is less correlation between the trees, this leads to a reduction in variance in the average. In this paper, two free parameters are considered: the number of trees, and the number of predictors sampled as candidates at each split. To the best of our knowledge, random forests have only been applied to early-warning exercises in Alessi and Detken [2].

Artificial Neural Networks (ANN)

Inspired by the functioning of neurons in the human brain, ANNs are composed of nodes or units connected by weighted links (see, e.g., Venables and Ripley [86]). These weights act as network parameters that are tuned iteratively by a learning algorithm. The simplest type of ANN is the single hidden layer feed-forward neural network (SLFN), which has one input, hidden and output layer. The input layer distributes the input values to the units in the hidden layer, whereas the unit(s) in the output layer computes the weighted sum of the inputs from the hidden layer, in order to yield a classifier probability. Despite ANNs with no size restrictions are universal approximators for any continuous function [44], computation time increases exponentially and their interpretability diminishes as ANNs grow in size. Further, discriminant and logit/probit analysis can in fact be related to very simple ANNs [68, 70]: so-called single-layer perceptrons (i.e., no hidden layer) with a threshold and logistic activation function. This paper uses a basic SLFN with three free parameters: the number of units in the hidden layer, the maximum number of iterations, and the weight decay. The first parameter controls the complexity of the network, while the last two are used to control how the learning algorithm converges. The use of ANNs has been fairly common in the academic early-warning literature.

Extreme Learning Machines (ELM)

As introduced by Huang et al. [46], the ELM refers to a specific learning algorithm used to train a SLFN-type neural network. Unlike conventional iterative learning algorithms, the ELM algorithm randomizes the input weights and analytically determines the output weights of the network. When trained with this algorithm, the SLFN generally requires a higher number of units in the hidden layer, but computation time is greatly reduced and the resulting neural network may have better generalization ability. In this paper, two free parameters are considered: the number of units in the hidden layer, and the type of activation function used in the network. To the best of our knowledge, we are not aware of previous applications of the ELM algorithm to crisis prediction.

Support Vector Machines (SVM)

The SVM, introduced by Cortes and Vapnik [23], is one of the most popular machine learning methods for supervised learning. It is a non-parametric method that uses hyperplanes in a high-dimensional space to construct a decision boundary for a separation between classes. It comes with several desirable properties. First, an SVM constructs a maximum margin separator, i.e. the chosen decision boundary is the one with the largest possible distance to the training data points, enhancing generalization performance. Second, it relies on support vectors when constructing this separator, and not on all the data points, such as in logistic regression. These properties lead to the method having high flexibility, but still being somewhat resistant to overfitting. However, SVMs lack interpretability. The free parameters considered are: the cost parameter, which affects the tolerance for misclassified observations when constructing the separator; the gamma parameter, defining the area of influence for a support vector; and the kernel type used. We are not aware of studies using SVMs for the purpose of deriving early-warning models.

| Method | Currency crisis | Sovereign crisis | Banking crisis |

|---|---|---|---|

| Signal extraction | [51] | [54] | [12] [1] |

| LDA | – | [38] [83] | – |

| QDA | – | – | – |

| Logit | [32] [39] [69] [10] [18] | [80] [40] | [8] [62] |

| Logit LASSO | – | – | [61] |

| KNN | – | – | – |

| Trees | [49] [21] | [79] | [26] |

| Random forest | – | – | [2] |

| ANN | [63] [37] [64] [76] | [34] | [71] |

| ELM | – | – | – |

| SVM | – | – | – |

3 Horse race, aggregation and model uncertainty

This section presents the methodology behind the robust and objective horse race and its aggregation, as well as approaches for estimating model uncertainty.

3.1 Set-up of the horse race

To continue from the data, classification problem and methods presented in Section 2, we herein focus on the set-up for and parameters used in the horse race, ranging from details in the use of data and general specification of the classification problem to estimation strategies and modeling. The aim of the set-up is to mimic real-time use as much as possible by both using data in a realistic manner and tackling the classification problem using state-of-the-art specifications. The specification needs also to be generic in nature, as the objectivity of a horse race relies on applying the same procedures to all methods.

Model specifications

This section describes the choices regarding model specifications that underlie the exercises in this paper. In all choices, we have tried to follow the convention in the most recent literature on the topic. Despite the fact that model output is country-specific, the literature has preferred the use of pooled data and models (e.g., Fuertes and Kalotychou [40], Sarlin and Peltonen [77]). In theory, one would desire to account for country-specific effects describing crises, but the rationale behind pooled models descends from the aim to capture a wide variety of crises and the relatively small number of events in individual countries. Further, as we are interested in vulnerabilities prior to crises and do not lag explanatory variables for this purpose, the benchmark dependent variable is defined as a specified number of years prior to the crisis. In the horse race, the benchmark is 5–12 quarters prior to a crisis.

As proposed by Bussière and Fratzscher [18], we account for post-crisis and crisis bias by not including periods when a crisis occurs or the two years thereafter. The excluded observations are not informative regarding the transition from tranquil times to distress events, as they can neither be considered “normal” periods nor vulnerabilities prior to crises. Following the same reasoning, observations 1–4 quarters prior to crises are also left out. To issue binary signals with method , we need to specify a threshold value on the estimated probabilities , which is set as to optimize Usefulness (as outlined in Section 2.2). We assume a policymaker to be more concerned of missing a crisis than giving a false alarm. Hence, the benchmark preference is assumed to be 0.8. This reasoning follows the fact that a signal is treated as a call for internal investigation, whereas significant negative repercussions of a false alarm only descend from external announcements.

For comparability, we consistently transform output probabilities of each method into their own percentile distributions of in-sample data. This is particularly relevant for model aggregation, as it is important for model output to be on the same scale. More specifically, the empirical cumulative distribution function is computed based on the in-sample probabilities for each method, and both the in-sample and out-of-sample probabilities are converted to percentiles of the in-sample probabilities.

Estimation strategies

With the aim of tackling the classification problem at hand, this paper uses two conceptually different estimation strategies. First, we use cross-validation for preventing overfitting and for objective comparisons of generalization performance. Second, we test the performance of methods when applied in the manner of a real-time exercise.

The resampling method of cross-validation, as introduced by Stone [82] in the 1970s, is commonly used in machine learning to assess the generalization performance of a model on out-of-sample data and to prevent overfitting. Out of a range of different approaches to cross-validation, we make use of so-called -fold cross-validation. In line with the famous evidence by Shao [81], leave-one-out cross-validation does not lead to a consistent estimate of the underlying true model, whereas certain kinds of leave-n-out cross-validation are consistent. Further, Breiman [14] shows that leave-one-out cross-validation may also run into trouble with the problem that a small change in the data causes a large change in the model selected, whereas Breiman and Spector [16] and Kohavi [56] found that -fold works better than leave-one-out cross-validation. For an extensive survey article on cross-validation see Arlot and Celisse [6]. Cross-validation is used here in two ways. The first aim of cross-validation is to function as a tool for model selection for obtaining optimal free parameters, with the aim of generalizing data rather than (over)fitting on in-sample data. The other aim relates to objective comparisons of models’ performance on out-of-sample data, given an identical sampling for the cross-validated model estimations. The scheme used herein involves sampling data into folds for cross-validation and functions as follows:

-

1.

Randomly split the set of observations into folds of approximately equal size.

-

2.

For the out-of-sample validation fold, fit a model to and compute an optimal threshold using with the remaining folds, also called the in-sample data. Apply the threshold to the fold and collect its out-of-sample .

-

3.

Repeat Steps 1 and 2 for , and collect out-of-sample performance for all validation sets as .666This is only a simplification of the precise implementation. We in fact sum up all elements of the contingency matrix, and only then compute a final Usefulness .

For model selection, a grid search of free parameters is performed for the methods supporting those. As stated previously, -fold cross-validation is used and the free parameters yielding the best performance on the out-of-sample data are stored and applied in subsequent analysis. The literature has generally preferred small values for , with being among the most prominently used number of folds (see e.g. Zhang [88].) The cross-validated horse race makes use of 10-fold cross-validation to provide objective relative assessments of generalization performance of different models. The latter purpose of cross-validation is central for the horse race, as it allows for comparisons of models, and thus different modeling techniques, but still assures identical sampling.

The standard approach to cross-validation may not, however, be entirely unproblematic. As we make use of panel data, including a cross-sectional and time dimension, we should also account for the fact that the data are more likely to exhibit temporal dependencies. Although the cross-validation literature has put forward advanced techniques to decrease the impact of dependence, such as a so-called modified cross-validation by Chu and Marron [22] (further examples in Arlot and Celisse [6]), the most prominent approach is to limit estimation samples to historical data for each prediction. To test models from the viewpoint of real-time analysis, we use a recursive exercise that derives a new model at each quarter using only information available up to that point in time.777It is worth noting that it is still well-motivated to use two separate tests, cross-validated and recursive evaluations. If we would also optimize free parameters with respect to recursive evaluations, then we might risk overfitting them to the specific case at hand. Thus, in case optimal parameters chosen with cross-validation also perform in recursive evaluations, we can assure that models are not overfitting data. This enables testing whether the use of a method would have provided means for predicting the global financial crisis of 2007–2008, and how methods are ranked in terms of performance for the task. This involves accounting for publication lags by lagging accounting based measures with 2 quarters and market-based variables with 1 quarter. The recursive algorithm proceeds as follows. We estimate a model at each quarter with all available information up to that point, evaluate the signals to set an optimal threshold , and provide an estimate of the current vulnerability of each economy with the same threshold as on in-sample data. The threshold is thus time-varying. At the end, we collect all probabilities and thresholds, as well as the signals, and evaluate how well the model has performed in out-of-sample analysis. As any ex post assessment, it is crucial to acknowledge that also this exercise is performed in a quasi real-time manner with the following caveats. Given how data providers report data, it is not possible to account for data revisions, and potential changes may hence have occurred after the first release. Moreover, we experiment with two different approaches for real-time use of pre-crisis periods as the dependent variable. With a forecast horizon of three years, we will at each quarter know with certainty only after three years whether or not the current quarter is a pre-crisis period to a crisis event (unless a crisis has occurred in the past three years). We test both dropping a window of equal length as the forecast horizon and using pre-crisis periods for the assigned quarters.888Drawbacks of dropping a pre-crisis window are that it would require a much later starting date of the recursion due to the short time series and that it would distort the real relationship between indicators and pre-crisis events. The latter argument implies that model selection, particularly variable selection, with dropped quarters would be biased. For instance, if one indicator perfectly signals all simultaneous crises in 2008, but not earlier crises, a recursive test would show bad performance, and point to concluding that the indicator is not useful. In contrast to lags on the independent variables, which impact the relationship to the dependent variable, it is worth noting that using the approach with pre-crisis periods does not impact the latest available relationship in data and information set at each quarter. As a horse race, the recursive estimations test the models from the viewpoint of real-time analysis. Using in-sample data ranging back as far as possible, the recursive exercise starts from 2005Q2, with the exception of the QDA method, for which analysis starts from 2006Q2, due to requirements of more training data than for the other methods. This procedure enables us to test performance with no prior information on the build-up phase of the recent crisis.

3.2 Aggregation procedures

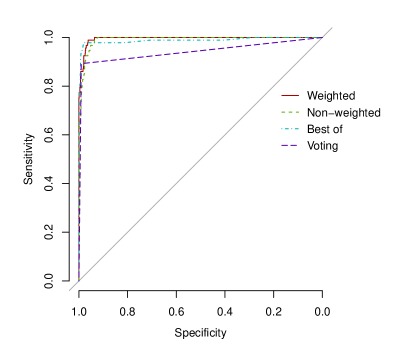

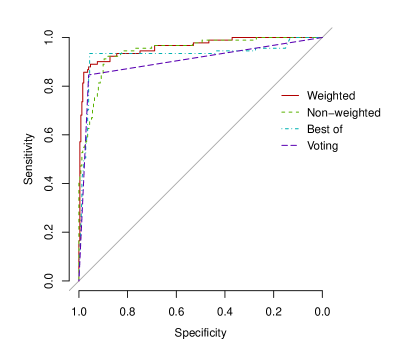

From individual methods, we move forward to combining the outputs of several different methods into one through a number of aggregation procedures. The approaches here descend from the subfield of machine learning focusing on ensemble learning, wherein the main objective is the use of multiple statistical learning algorithms for better predictive performance. Although we aim for simplicity and do not adopt the most complex algorithms herein, we make use of the two common approaches in ensemble learning: bagging and boosting. Bagging stands for Bootstrap Aggregation [13] and makes use of resampling from the original data, which is to be aggregated into one model output. While being an approach for ensemble learning, we discuss this under the topic of resampling and model uncertainty, as can be seen in Section 3.3. Boosting [78] refers to computing output from multiple models and then averaging the results with specified weights, which we mainly rely on in our aggregation procedures below. A third group of stacking approaches [87], which add another layer of models on top of individual model output to improve performance, are not used in this paper for the sake of simplicity. Again, we use the optimal free parameters identified through cross-validated grid searches, and then estimate individual methods. For this, we make use of four different aggregation procedures: the best-of and voting approaches, and arithmetic and weighted averages of probabilities.

The best-of approach simply makes use of one single method by choosing the most accurate one. To use information in a truthful manner, we always choose the method, independent of the exercise (i.e., cross-validation or recursion), which has the best in-sample relative Usefulness. Voting simply makes use of the signals of all methods for each observation in order to signal or not based upon a majority vote. That is, the aggregate chooses for observation the class that receives the largest total vote from all individual methods:

where is the binary output for method and observation , and is the binary output of the majority vote aggregate.

Aggregating probabilities requires an earlier intervention in modeling. In contrast to the best-of and voting approaches, we directly make use of the probabilities of each method for all observations to average them into aggregate probabilities. The simpler case uses an arithmetic mean to derive aggregate probabilities . For weighted aggregate probabilities , we make use of in-sample model performance when setting the weights of methods, so that the most accurate method (in-sample) is given the most weight in the aggregate. The non-weighted and weighted probabilities for observations can be derived as follows:

where the probabilities of each method are weighted with its performance measure for all observations . In this paper, we make use of weights , but the approach is flexible for any chosen measure, such as the AUC. This weighting has the property of giving the least useful method the smallest weight, and accordingly a bias towards the more useful ones. The arithmetic mean can be shown to result in for . To make use of only available information in a real-time set-up, the used for weighting refers always to in-sample results. In order to assure non-negative weights, we drop methods with negative values (i.e., ) from the vector of performance measures. In the event that all methods show a negative Usefulness, they are given weights of equal size. After computing aggregate probabilities , they are treated as if they were outputs for a single method (i.e., ), and optimal thresholds identified accordingly. In contrast, the best-of approach signals based upon the identified individual method and voting signals if and only if a majority of the methods signal, which imposes no requirement of a separate threshold. Thus, the overall cross-validated Usefulness of the aggregate is calculated in the same manner as for individual methods. Likewise, for the recursive model, the procedure is identical, including the use of in-sample Usefulness for weighting.

3.3 Model uncertainty

We herein tackle uncertainty in classification tasks concerning model performance uncertainty and model output uncertainty. While descending from multiple sources and relating to multiple features, we are particularly concerned with uncertainties coupled with model parameters.999Beyond model parameter uncertainty, and no matter how precise the estimates are, models will not be perfect and hence there is always a residual model error. To this end, we are not tackling uncertainty in model output (or model error) resulting from errors in the model structure, which particularly relates to the used crisis events and indicators in our dataset (i.e., independent and dependent variables). Accordingly, we assess the extent to which model parameters, and hence predictions, vary if models were estimated with different datasets. With varying data variation in the predictions is caused by imprecise parameter values, as otherwise predictions would always be the same. Not to confuse variability with measures of model performance, zero parameter value uncertainty in the predictions would still not imply perfectly accurate predictions. To represent any uncertainty, we need to derive properties of the estimates, including standard errors (SEs), confidence intervals (CIs) and critical values (CVs). To move toward robust statistical analysis in early-warning modeling, we first present our general approach to early-warning inference through resampling, and then present the required specification for assessing model performance and output uncertainty.

Early-warning inference

The standard approaches to inference and deriving properties of estimates descend from conventional statistical theory. If we know the data generating process (DGP), we also know that for data , we have the mean as an estimate of the expected value of , the SE showing how well estimates the true expectation, and the CI through (where is the CV). Yet, we seldom do know the DGP, and hence cannot generate new samples from the original population. In the vein of the above described cross-validation [82], we can generally mimic the process of obtaining new data through the family of resampling techniques, including also permutation tests [35], the jackknife [65] and bootstraps [27]. At this stage, we broadly define resampling as random and repeated sampling of sub-samples from the same, known sample. Thus, without generating additional samples, we can use the sampling distribution of estimators to derive the variability of the estimator of interest and its properties (i.e., SEs, CIs and CVs). For a general discussion of resampling techniques for deriving properties of an estimator, the reader is referred to original works by Efron [28, 29] and Efron and Tibshirani [30, 31].

Let us consider a sample with independent observations of one dependent variable and explanatory variables . We consider our resamplings to be paired by drawing independently pairs from the observed sample. Resampling involves drawing randomly samples from the observed sample, in which case an individual sample is (). To estimate SEs for any estimator , we make use of the empirical standard deviation of resamplings for approximating the SE . We proceed as follows:

-

1.

Draw independent samples () of size from .

-

2.

Estimate the parameter through for each resampling .

-

3.

Estimate by , where .

Now, given a consistent and asymptotically normally distributed estimator , the resampled SEs can be used to construct approximate CIs and to perform asymptotic tests based on the normal distribution, respectively. Thus, we can use percentiles to construct a two-sided asymmetric but equal-tailed CI, where the empirical percentiles of the resamplings ( and ) are used as lower and upper limits for the confidence bounds. We make use of the above Steps 1 and 2, and then proceed instead as follows:

-

4.

Order the resampled replications of estimator such that . With the th and th ordered elements as the lower and upper limits of the confidence bounds, the estimated CI of is .

Using the above discussed resampled SEs and approximate CI, we can use a conventional (but approximate) two-sided hypothesis test of the null . In case is outside the two-tailed CI with the significance level , the null hypothesis is rejected. Yet, if we have two resampled estimators and with non-overlapping CIs, it is obvious that they are necessarily significantly different, but it is not necessarily true that they are not significantly different if they overlap. Rather than mean CIs, we are concerned with the test statistic for the difference between two means. Two means are significantly different for confidence levels when the CI for the difference between the group means does not contain zero: .101010In contrast to the test statistic, we can see that two means have no overlap if the lower bound of the CI for the greater mean is greater than the upper bound of the CI for the smaller mean, or . While simple algebra gives that there is no overlap if , the test statistic only differs through the square root and the sum of squares: . As , it is obvious that the mean difference becomes significant before there is no overlap between the two group-mean CIs. Yet, we may be violating the normality assumption as the traditional Student distribution for calculating CIs relies on a sampling from a normal population.

Even though we could by the central limit theorem argue for the distributions to be approximately normal if the sampling of the parent population is independent, the degree of the approximation would still depend on the sample size and on how close the parent population is to the normal. As the common purpose behind resampling is not to impose such distributional assumptions, a common approach is to rely on so-called resampled intervals. Thus, based upon statistics of the resamplings, we can solve for and use confidence cut-offs on the empirical distribution. Given consistent estimates of and , and a normal asymptotic distribution of the -statistic , we can derive approximate symmetrical CVs from percentiles of the empirical distribution of all resamplings for the -statistic.

-

1.

Consistently estimate the parameter and using the observed sample: and .

-

2.

Draw independent resamplings () of size from .

-

3.

Assuming , estimate the -value for where and are resampled estimates of and its SE.

-

4.

Order the resampled replications of such that . With the th ordered element as the CV, we have and .

With these symmetrical CVs, we can utilize the above described mean-comparison test. Yet, as CVs for the resampled intervals may differ for the two means, we amend the test statistic as follows:

Model performance uncertainty

For a robust horse race, and ranking of methods, we make use of resampling techniques to assess variability of model performance. We compute for each individual method and the aggregates resampled SEs for the relative Usefulness and AUC measures. Then, we use the SEs to obtain CVs for the measures, analyze pairwise among methods and aggregates whether intervals exhibit statistically significant overlaps, and produce a matrix that represents pairwise significant differences among methods and aggregates. More formally, the null hypothesis that methods and have equal out-of-sample performance can be expressed as (and likewise for AUC). To this end, the alternative hypothesis of a difference in out-of-sample performance of methods and is .

In machine learning, supervised learning algorithms are said to be prevented from generalizing beyond their training data due to two sources of error: bias and variance. While bias refers to error from erroneous assumptions in the learning algorithm (i.e., underfit), variance relates to error from sensitivity to small fluctuations in the training set (i.e., overfit). The above described -fold cross-validation may run the risk of leading to models with high variance and non-zero yet small bias (e.g., Kohavi [56], Hastie et al. [41]). To address the possibility of a relatively high variance and to better derive estimates of properties (i.e., SEs, CIs and CVs), repeated cross-validations are oftentimes advocated. This allows averaging model performance, and hence ranking average performance rather than individual estimations, as well as better enables deriving properties of the estimates.111111Repeated cross-validations are not entirely unproblematic (e.g., Vanwinckelen and Blockeel [85]), yet still one of the better approaches to simultaneously assess generalizability and uncertainty. For both individual methods and aggregates, we make use of 500 repetitions of the cross-validations (i.e., ).

In the recursive exercises, we opt to make use of resampling with replacement to assess model performance uncertainty due to limited sample sizes for the early quarters. The family of bootstrapping approaches was introduced by Efron [27] and Efron and Tibshirani [31]. Given data , bootstrapping implies drawing a random sample of size through resampling with replacement from , leaving some data points out while others will be duplicated. Accordingly, an average of roughly 63% of the training data is utilized for each bootstrap. However, the standard bootstrap procedure assumes data to be i.i.d., and thus does not account for possible dependencies present in the data. Since early-warning models commonly use panel data, both cross-sectional and time-series dependence are to be assumed. In line with Kapetanios [52] and Hounkannounon [45], we thus utilize a double bootstrap for the robust recursive horse race, consisting of two components: cross-sectional resampling and the moving block bootstrap. For panel data of dimensions , where is the number of entities, and is the number of periods, cross-sectional resampling entails drawing full time-series for entities with replacement. The moving block bootstrap, introduced by Künsch [55], draws blocks of a defined size of observations, in order to preserve temporal dependency within the resampled blocks. Our double bootstrap procedure combines both in the following way:

-

1.

From the available in-sample data of dimensions , draw entities with replacement. This constitutes the pseudo-sample .

-

2.

From the obtained pseudo-sample , draw a randomly selected block of size from all entities.

-

3.

Repeat 2. until the length of all combined blocks is > by cutting at the end. This constitutes the final bootstrap sample

For each quarter, we draw randomly the bootstrap sample from the available in-sample data using the above procedure, which is repeated 500 times. Each of these bootstraps are treated individually to compute the performance of individual methods and the aggregates. These results are then averaged to obtain the corresponding results of a robust bootstrapped classifier for each method and aggregate.

Model output uncertainty

In order to assess the reliability of estimated probabilities and optimal thresholds, and hence signals, we study the notion of model output uncertainty. The question of interest would be whether or not an estimated probability is statistically significantly above or below a given optimal threshold. More formally, the null hypothesis that probabilities and optimal thresholds are equal can be expressed as . Hence, the alternative hypothesis of a difference in probabilities and optimal thresholds is . This can be tested both for probabilities of individual methods and probabilities of aggregates as well as their thresholds and .

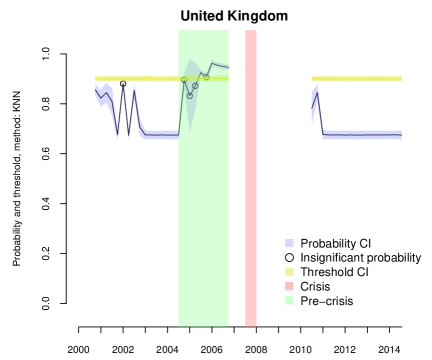

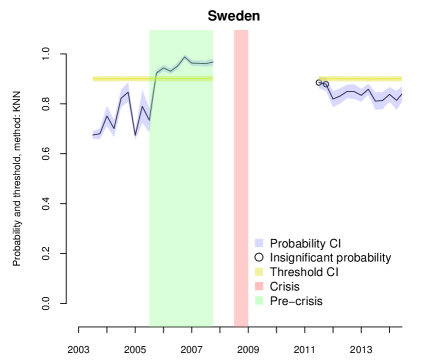

We assess the trustworthiness of the output of models, be they individual methods or aggregates, by computing SEs for the estimated probabilities and the optimal thresholds. We follow the approach for model performance uncertainty to compute CVs and mean-comparison tests. For both cross-validation and bootstraps, the 500 resamplings of the out-of-sample probabilities are computed separately for each method and averaged with and without weighting, as above discussed (i.e., ). From these, the mean and the SE are drawn and used to construct a CV for individual methods and the aggregates, based on bootstrapped crisis probabilities and optimal thresholds, which allows us to test when model output is statistically significantly above or below a threshold. The above implemented bootstraps also serve another purpose. We make use of the CI as a visual representation of uncertainty. Thus, we produce confidence bands around time-series of probabilities and thresholds for each method and country, which is useful information for policy purposes when assessing the reliability of model output.

3.4 Summary of horse race exercises

To sum up the above described exercises, we herein provide a simplified description of the cross-validated and the recursive horse races, as well as steps within them.

-

1.

Cross-validation: Split the full sample into folds of equal size, and estimate models and thresholds using the remaining folds of data. Collect out-of-sample probabilities and binary predictions for each left-out fold.

-

2.

Recursive: Utilize an out-of-sample span split into individual quarters, for which the model is estimated and optimal threshold computed using all data available up until each quarter.

For both exercises, all out-of-sample output is finally reassembled and performance summarized in terms of a range of evaluation measures. The two exercises differ in their sampling of data, particularly the in-sample and out-of-sample partitions used for each estimation. While cross-validation is common in machine learning and allows an efficient use of small samples, exercises may benefit from the fact that data are sampled randomly despite most likely exhibiting time dependence. The recursive exercises, on the contrary, account for time dependence in data by strictly using historical samples for out-of-sample predictions, which nevertheless requires more data, particularly in the time-series dimension. These two exercises allow exploring performance across methods, and how that is impacted by the evaluation exercise.

For both exercises, we go through the following steps to estimate individual models, aggregate model output and represent model and performance uncertainty:

-

1.

Following the above exercises, estimate models with all individual methods .

-

2.

Aggregate model output from models to using four approaches: best-of, voting, non-weighted and weighted.

-

3.

Represent model performance uncertainty for individual and aggregated methods by repeating the exercises using sampling of in-sample data with and without replacement and reporting statistically significant rankings.

-

4.

Represent model output uncertainty for individual and aggregated methods by repeating the exercises using sampling of in-sample data with and without replacement and reporting statistically significant signals and non-signals.

4 The European crisis as a playground

This section applies the above introduced concepts in practice. Using a European sample, we implement the horse race with a large number methods, apply aggregation procedures and illustrate the use and usefulness of accounting for and representing model uncertainty.

4.1 Model selection

To start with, we need to derive suitable (i.e., optimal) values for the free parameters for a number of methods. Roughly half of the above discussed methods have one or more free parameters relating to their learning algorithm, for which optimal values are identified empirically. In summary, these methods are: signal extraction, LASSO, KNN, classification trees, random forest, ANN, ELM and SVM. To perform model selection for these six methods, we make use of a grid search to find optimal free parameters with respect to out-of-sample performance. A set of tested values are selected based upon common rules of thumb for each free parameter (i.e., usually minimum and maximum values and regular steps in between), whereafter an exhaustive grid search is performed on the discrete parameter space of the Cartesian product of the parameter sets. To obtain generalizable models, we use 10-fold cross-validation and optimize out-of-sample Usefulness for guiding the specifications of the algorithms. Finally, the parameter combinations yielding the highest out-of-sample Usefulness are chosen, as is optimal for each method. For the signal extraction method, we vary the used indicator, and the indicator with the highest Usefulness is chosen (for a full table see Table A.1 in the Appendix).121212As the poor performance of signal extraction may arise questions, we also show results for in Table A.2 in the Appendix. Given the unconditional probabilities of events, this preference parameter has potential to yield the largest Usefulness. Accordingly, we can also find much larger Usefulness values for most indicators. This highlights the sensitivity of signal extraction to the chosen preferences. The chosen parameters are reported in Table 5.131313It may be noted the the optimal amount of hidden units for the ELM method returned by the grid-search algorithm is unusually high. However, as seen below in the cross-validated and particularly real-time exercises, the results obtained using the ELM method do not seem to exhibit overfitting. Also, by comparing results of the ELM to those of the ANN, which has only eight hidden units, out-of-sample results are in all tests similar in nature.

| Method | Parameters | ||

|---|---|---|---|

| Signal extraction | Debt service ratio | ||

| Logit LASSO | |||

| KNN | = 2 | Distance = 1 | |

| Trees | Complexity = 0.01 | ||

| Random forest | No. of trees = 180 | No. of predictors sampled = 5 | |

| ANN | No. of hidden layer units = 8 | Max no. of iterations = 200 | Weight decay = 0.005 |

| ELM | No. of hidden layer units = 300 | Activation function = Tan-sig | |

| SVM | = 0.4 | Cost = 1 | Kernel = Radial basis |

4.2 A horse race of early-warning models

We conduct in this section two types of horse races: a cross-validated and a recursive. This provides a starting point for the ranking of early-warning methods and simultaneous use of multiple models.

Cross-validated race

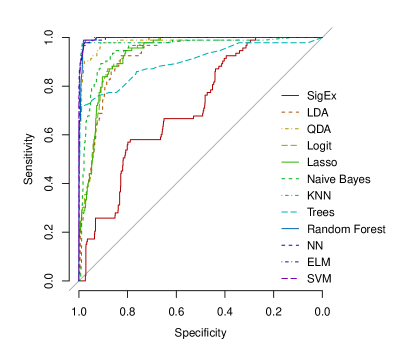

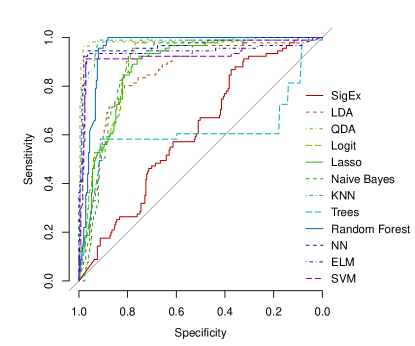

The first approach to ranking early-warning methods uses 10-fold cross-validation. Rather than optimizing free parameters, the cross-validation exercise aims at producing comparable models with all included methods, which can be assured due to the similar sampling of data and modeling specifications. For the above discussed methods, we use the optimal parameters as shown in Table 5. Methods with no free parameters are run through the 10-fold cross-validation without any further ado. Table 6 presents the out-of-sample results of the cross-validation horse race for the individual early-warning methods, sorted by descending Usefulness. At first, we can note that the simple approaches, such as signal extraction, LDA and logit analysis, are outperformed in terms of Usefulness by most machine learning techniques. At the other end, the methods with highest Usefulness are KNN and SVM. In terms of AUC, QDA, random forest, ANN, ELM and SVM yield good results. It is still worth noting that a standard cross-validated test does not account for potential excessive correlation across folds due to dependence in data, and hence the more flexible non-linear approaches are also more prone to exhibit a too good model fit. Yet, this can easily be controlled for with the recursive real-time analysis.

![[Uncaptioned image]](/html/1501.04682/assets/x4.png)

Recursive race

To further test the performance of all individual methods, we conduct a recursive horse race among the approaches. As outlined in Section 3.1, we estimate new models with the available information in each quarter to identify vulnerabilities in the same quarter, starting from 2005Q2 (2006Q2 for QDA). Besides for a few exceptions, the results in Table 7 are in line with those in the cross-validated horse race in Table 6. For instance, the top six methods are the same with only minor differences in ranks, and classification trees perform poorly in the recursive exercise and logit in the cross-validated exercise. Generally, machine learning based approaches again outperform more conventional techniques from the early-warning literature.