Trend and Fractality Assessment of Mexico’s Stock Exchange

Abstract

The total value of domestic market capitalization of the Mexican Stock Exchange was calculated at 520 billion of dollars by the end of November 2013. To manage this system and make optimum capital investments, its dynamics needs to be predicted. However, randomness within the stock indexes makes forecasting a difficult task. To address this issue, in this work, trends and fractality were studied using over the opening and closing prices indexes over the past 23 years. Returns, Kernel density estimation, autocorrelation function and analysis and the Hurst exponent were used in this research. As a result, it was found that the Kernel estimation density and the autocorrelation function shown the presence of long-range memory effects. In a first approximation, the returns of closing prices seems to behave according to a Markovian random walk with a length of step size given by an alpha-stable random process. For extreme values, returns decay asymptotically as a power law with a characteristic exponent approximately equal to 2.5.

Keywords: Financial Time Series, Kernel Density Estimation, Empirical Autocorrelation function, analysis, Hurst exponent, Power law; PACS: GNU-R, stabledist, fBasics, pracma; MSC: 91B84, 62M10

1 Introduction

Financial markets exibit a dynamic behaviour in the form of fluctuations, trends, and volatility. Market regulations, globalization, changes in the interest rates, war conflicts, new technologies, social movements, news and housing are only a small sample of factors affecting the chaotic and complex structure of the financial markets [1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13].

To assess all these interacting elements within a coherent theoretical economic framework to create a prediction model is, at least for now, a nearly impossible task. The behaviour of an economic system integrates a collection of emerging properties of chaotic and complex systems [14, 15, 16, 17, 18, 19, 20, 21]. From a deteministic approach, the effort requiered to model and characterize a such system might be monumental. Complex correlations in the fluctuations of financial and economic indices [22, 23, 24, 25], the self-organization phenomena in market crashes [26, 27, 28, 29], the sudden high growth or sharp fall in the stock market during periods of apparent stability [30, 31, 32, 33], are only a few examples of situations that can be considered difficult to understand or represent mathematically.

On one hand, from the stochastic-deterministic point of view of the physical statistics [34, 35, 36, 37, 38, 39], the dynamic variation of prices in a financial market can be considered as a result of an enormous amount of interacting elements. For instance, stock prices are the result of multiple increments and decrements that result from a feedback response of every action defining the composition of an index, which result, at the same time, from decisions and flows of information that change from one moment to the next [40, 41, 42, 43, 44]. For this reason, a detailed description of each trajectory, within the structure of a system, would be almost imposible and futile: the series of events that gave birth to a specific trajectory might not repeat, and a detailed description would not have a predictive utility.

On the other hand, by considering axiomatic that we are unable to reach a deterministic understanding of a system as whole, a statistical approach might be useful tu describe the uncertainty involved. At least we would be able to gain some insight about the expected behaviour, size of fluctuations, or the corresponding probabilities of rare events. This, with the final intention of doing forecasts on the process future behaviour. The statistical description may even predict in an essentially deterministic way, such as the diffusion equation which describe the density of particles, each one performing a random walk in a microscopic scale [45, 46, 47].

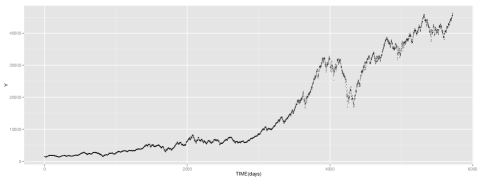

According to web portal of Mexican Stock Exchange, “The Prices and Quotations Index (MEXBOL) is the Mexican Market’s main indicator, it expresses the stock market return according to the prices variations of a balanced, weighted and representative Constituent List of the equities listed in the Mexican Stock Exchange, in accordance to best practices internationally applied” [48]. The daily values of the MEXBOL or IPC Index form a set of variables: The Opening Price, the Closing Price, the High an Low values, the Adjusted Price and the transaction Volume. The Fig. 1 show the variation in time of the closing price , .

2 Methodology

To perform this research, 23 years of observations from MEXBOL were used, from November the 8th, 1991, to September the 5th, 2014. This information is publicly available in several websites, see for instance the historical prices of IPC(^MXX) or IPC Index-Mexico in [49].

This paper presents an assessment of the dynamic behaviour of closing and opening princes of the IPC Index from three different perspectives: a) Analysis of the stochastic properties of the random behaviour and fluctuations of returns of closing price. b) Estimation of the degree of fractality and long term memory through the rescaled range or analysis and the Hurst exponent. c) Empirical autocorrelation function analysis.

All the analysis and the numeric and visual calculations of the IPC Index properties were done using the GNU-R free software environment within an Ubuntu-Linux 14.04 work enviroment.

2.1 Closing prices

The return values is a regular transformation used in economic data in order to standardize and remove the trending. Thus, a simple and fast way to detrending the closing price serie, Fig. 1, is given by the transformation

| (1) |

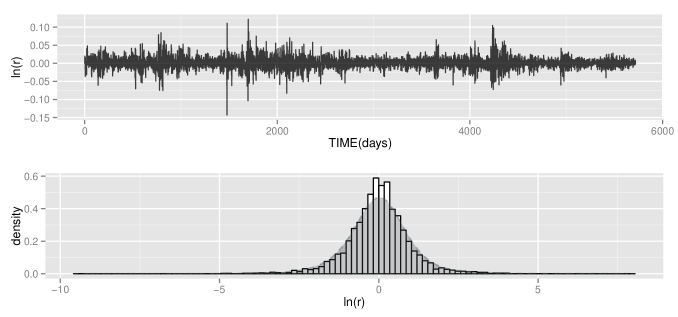

The mean value of this new series is , i.e., the daily closing price has a rate of return average of 7.29 per 1000 units. The corresponding standard deviation is . A comparison between normalized logarithms of returns (mean zero and variance 1) with the profile created by a Gaussian white noise, also with mean zero and variance 1, is shown in Fig. 2.

According to Figs. 2 and 3, unlike the normalized Gaussian white noise, the distribution of returns or logarithmic returns is more narrower with a higher concentration of values in from the mean but with a tail somewhat heavier.

From a sample or time serie , an empirical probability density distribution is given by the superposition of normalizated kernels through the Kernel Density Estimator or KDE approximation [50]

| (2) |

where is the bandwidth or scale parameter and is a normalizated kernel function.

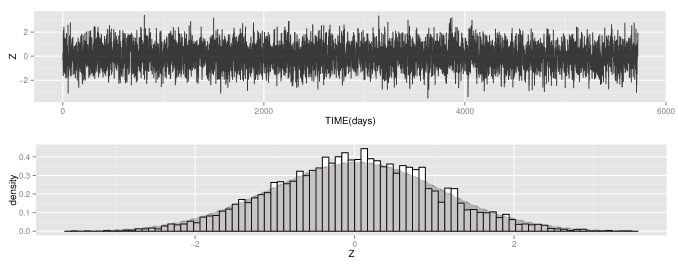

Using the library kedd in GNU-R [51], an empirical probability density distributions KDE-based with an optimal bandwidth for both, normalized Gaussian white noise and normalized logarithmic returns, are obtained. In the Fig. 4 the sharpe fall of respect the normalized Gaussian white noise becomes evident.

From the Fig. 4, for values approximately in around the mean, the distribution of is more sharply. On the other hand, approximately when heavy tails emerge and this indicates the presence of a coarse-grained power law underlying the dynamics of return fluctuations, very similar to the fluctuations in random variables with an Lévy distributions characterized by , , and , the stability, skewness, scale, and location parameters, respectively [52]. When , the density probability decays asymptotically as [53]

| (3) |

with .

A comment: Assuming that is the density probability function of the closing prices , the transformation , , define a density probability for the logarithmic returns showing an asymptotic fall with a slightly higher heavy-tail such that .

2.2 Opening and Closing prices

To concentrate on analyzing the financial noise, another way to detrending a time series is to obtain the first differences or jumps to nearest neighbors. So some examples of this transformation are: the first differences within the closing prices serie , or the first differences delayed one day between the opening and closing price series , both with .

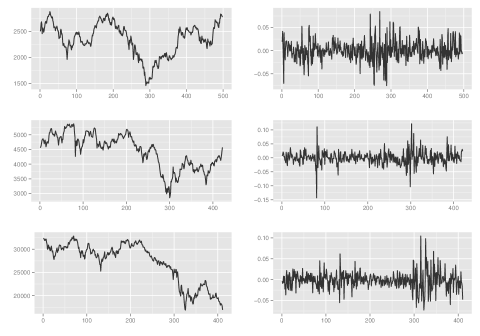

A graph with the differences between the opening prices of -th day and the -th closing price of the day before can be observed in Fig. 5 in top. Here, much more than the logarithmic returns series the appearance of extreme events is more evident. The mean and standar deviation values for this serie are and , respectively.

A special case of a transformation by differences are the first differences day by day between the closing and opening prices serie . Particularly, this serie shows a symmetrical pattern around the mean value with a standard deviation of . Also, although without apparent trend shows a high volatility increasing in time, see Fig. 5 in bottom.

Unlike a Gaussian white noise, one of the main features of stable distribution is the existence of long-term correlations. A measure of the intensity of this memory effect and the fractal behavior type of fluctuations in a stochastic process is given by the value of the Hurst exponent. The Hurst exponent can be obtained by the rescaled range analysis, or analysis, a standard technique to measure the fractality or the persistence in time of correlations in time series. In the next section, this technique is applied to the different series presented so far.

2.3 Hurst exponent

The Hurst exponent, a parameter introduced in 1951 by the British hydrologist Harold Edwin Hurst to study the Nile river risings, is an instrument used to measure at different scales the mean intensity of the fluctuations of a time series and its tendency to form clusters of persistence. For construction, the Hurst exponent (henceforth parameter) is a real number between and . If it is said that the mean tendency of the series is persistent (either persistently upwards or downwards). If it is said that the series is anti-persistent (it goes from upwards to downwards or vice-versa). Finally, when we can say that in average there is no persistence, and then it is a memory-less process: the values of the process are completely uncorrelated and the behaviour of the series is the one observed in a Gaussian white noise random process or like the uncorrelated incremets in the Brownian motion process [54].

The strong trend observed in the closing prices of Fig. 1 is the result of the persistence of high levels of correlation in time. In principle, the Hurst exponent allows to differentiate between series of Gaussian white noise created by a series of independent random variables as the increments of an ordinary Brownian motion, i.e., between a stochastic processes with a future completely determined by the present (current state) and a more complex movement where the quality associated with the estimation of future values depends, in principle, of all previous observations.

2.4 Rescaled range analysis

In the analysis the time series is divided into sub-series, each of approximate size . A heuristic form to take the partition of the serie is in power series of two, in this case the values of the index and are, respectively, , for some integer , and . For each sub-series find the mean and the standard deviation , . Data are normalized by substracting the mean of each sub-serie. With the cumulative deviations , ; the range is obtained and it is rescaled by the standar deviation , . The mean of rescaled range for each partition, in the time scale , is . Repeat the same with other partition for another value. Identifying , Hurst found that scales by power-law as time increases, i. e., where is a constant. In practice can be estimated as the slope of a plot of versus length .

2.5 Autocorrelation analysis

It is said to a stochastic process is weakly stationary or wide-sense stationary if the function of mean is constant in time and the autocovariance function only depends on the elapsed time [55]. Assuming the foregoing, the empirical autocovariance function for a finite sample of values of a wide-sense stationary time series can be estimated by [56]

| (4) |

with and the common empirical mean. And the empirical autocorrelation function is

| (5) |

with the variance of the time serie .

The autocorrelation function for the returns dies quickly after a lag of 1 into a pattern in appearance very similar to a Gaussian white noise, Fig. 8.

The progressive thinning of the autocorrelation function (an biased estimator) for a Gaussian white noise shown in Fig. 8 is a border effect due to the scaling factor in (5). In fact for a sample Gaussian white noise the distribution of the autocorrelation function for a maximum value is Gaussian approximately with mean and standar deviation decaying as [56].

Nevertheless, unlike the Gaussian white noise, the fluctuations of the autocorrelation function for the returns displays a strong correlation to first neighbors. Moreover the maximum value in the autocorrelation function for the returns of any order occurs for a lag of . In other words, the transition of the returns to a symmetrical non Gaussian autocorrelation function for , Fig. 8 in bottom, suggest as a first approximation the following simple Markovian random walk for the returns of closing prices

| (6) |

where the noise is an stable random noise whose distribution has a stability parameter (non Gaussian), see Table 1.

Additionally the behavior of the autcorrelation function (5) for the first differences of and series were estimated. The landscape of the autocorrelation function for the first differences show correlations more complex at different scales, Fig. 7 on the left side. On the other hand, the profile of the autocorrelation function for the differences are correlated beyond the first neighbors, Fig. 7 on the right side.

3 Results

The raw data used for this paper was the opening and closing prices of the MEXBOL Index in the period Nov/08/1991-Sept/05/2014.

The Table 1 displays the optimal values of parameter for the empirical distributions of the returns and logarithmic returns of closing price, respectively, obtained with the function stableFit of the library fBasics, implemented by GNU-R.

| Time serie | ||||

|---|---|---|---|---|

With the values of Table 1 and the equation (3) the asymptotic decay in power law for the normalized returns and the logarithmic returns are

| (7) | |||||

with and . For comparison, in [57, 58, 59, 60] have reported that an empirical distribution for the extreme values of the returns is a power-law type , with .

Given a set of parameters , using the library stabledist [53] the corresponding numerical values of an stable distribution are obtained. The differences between the stable distributions for the normalized returns and logarithmics returns of time serie of closing prices are presented inf Fig. 8.

The Table 2 shows the optimal stable parameters for the time series and .

| First differences | ||||

|---|---|---|---|---|

In the Fig. 9 at the left the empirical stable density probability, corresponding to the parameters of the Table 2, are shown. For comparison, a profile of Gaussian white noise, with stable parameters , is included too.

Hurst exponent for the different analized time series were estimated using different time scales, for example, daily return, return each 2 days and so on.

In the Table 3 the different values of hurst exponent calculated through analysis for all time series analyzed are shown.

| Data | ||

|---|---|---|

| Opening prices | 1.018647 | |

| Closing prices | 1.018856 | |

| Logarithmic returns | 0.532947 | |

| Logarithmic returns | 0.5318121 | |

| Differences within | 0.5284645 | |

| Differences between | 0.421346 | |

| Forward differences | 0.6051881 | |

| Gaussian white noise | 0.521465 |

The Fig. 9 at the right show the asymptotic behavior of Hurst exponent when for the analysis. When the time scale increases the autocorrelation also increases and the Hurst exponent approaches one, i.e., the effects of long-term memory are amplified.

A summary of some observed characteristics in IPC closing prices time series are shown in Fig. 10. In this graph it is possible identified at least three “bubble zones” corresponding each one of them with a specific financial crash, “The effect Tequila” of 1994, the Asian financial crisis from 1997 to 1998 and the recent Global financial crisis of 2008. The big fluctuations, argues, is an indicative of significant correlations effects of long-term, corroborated by the form of autocorrelation function between the opening price in the -th day and the closing price in the -th day, the differences.

4 Conclusions

Heavy tails in the series of the returns of opening or closing prices and in the delayed first differences between opening and closing prices, clearly indicates a non diffusive fluctuations dynamics or a non Gaussian behavior for MEXBOL IPC Index. At the same time, this allows the presence of long term correlations and memory effects not compatible with the concept of an efficent market. In other words, return values does not represent a simple random walk where jumps are independent with a finite variance.

Despite returns and the logarithmic returns of closing or opening prices, even the differences , exhibit a symmetric, stationary and homoscedastic behavior (Figs. 2 and 5 in top), the series of differences (Fig. 5 in bottom) show a growing volatility over time. This sistematic increment of fluctuations size, and the average difference between closing and opening prices create a clear large scale positive trend in the serie, see the Fig. 1. As before, even though the average margin of closing prices is small in a daily scale, with a value slightly bigger than 1, , it is big enough to create a global growth of closing prices.

Although the Hurst exponent for the return of closing prices in the MEXBOL Index given by the are very similar and close to (an expected value for Gaussian white noise), the strong difference between the time series of logarithmic returns and an empirical Gaussian white noise, Figs. 2, 3, and 4, results from the presence at different time scales of recurrent large fluctuations in returns or logarithmic returns , a behavior that captures the underlying fractal nature of many financial time series.

The IPC Index for closing and opening prices analysis shows an incresing growth for long time period, it means that the Mexican stock market and the economic stability is a good option to investment.

In spite of the recurrent crisis in past such as the Tequila effect, Asian crisis and the recent Global crisis, the results in this research show that the Mexican economy shown robustness along the past 23 years.

5 Acknowledgements

The authors would like to thanks CONACYT, PROMEP, PAICYT and the Universidad Autónoma de Nuevo León for support this research.

References

- [1] Cruz, Lopez Jorge and Mendes, Royce and Vikstedt, Harri. The Market for Collateral: The Potential Impact of Financial Regulation, Bank of Canada. Financial Systems Review, 45-53, 2013.

- [2] Borrius, Sjoerd, The impact of new financial regulations on financial markets instruments within banks, url = http://essay.utwente.nl/62286/, 2012.

- [3] Kose, M. Ayhan and Prasad, Eswar S. and Terrones, Marco E., How Does Globalization Affect the Synchronization of Business Cycles?, The American Economic Review, 93, 57-62, 2003.

- [4] Aguiar, Mark and Gopinath, Gita. Defaultable debt, interest rates and the current account, Journal of International Economics, 69, 64-83, 2006.

- [5] Neumeyer, Pablo A. and Perri, Fabrizi. Business cycles in emerging economies: the role of interest rates, Journal of Monetary Economics, 52, 345-380, 2005.

- [6] Guidolin, Massimo and La Ferrara, Eliana. Diamonds Are Forever, Wars Are Not: Is Conflict Bad for Private Firms?, The American Economic Review, 97, 1978-1993, 2007.

- [7] Schneider, Gerald and Troeger, Vera E. War and the World Economy: Stock Market Reactions to International Conflicts, Journal of Conflict Resolution, 50, 623-645, 2006.

- [8] Dicle, Mehmet and Levendis, John. The impact of technological improvements on developing financial markets: The case of the Johannesburg Stock Exchange, Review of Development Finance, 3, 204-213, 2013.

- [9] King, Brayden G. and Soule, Sarah A. Social Movements as Extra-Institutional Entrepreneurs: The Effect of Protests on Stock Price Returns, Administrative Science Quarterly, 52, 413-442, 2007.

- [10] Boyd, John H. and Hu, Jian and Jagannathan, Ravi.The Stock Market’s Reaction to Unemployment News: Why Bad News Is Usually Good for Stocks, The Journal of Finance, 60, 649-672, 2005.

- [11] Engle, Robert F. and Ng, Victor K. Measuring and Testing the Impact of News on Volatility, The Journal of Finance, 48, 1749-1778, 1993.

- [12] Pikorec, Matija and Antulov-Fantulin, Nino and Novak, Petra Kralj and Mozeti, Igor and Grar, Miha and Vodenska, Irena and muc, Tomislav. Cohesiveness in Financial News and its Relation to Market Volatility, Scientific Reports, 4, 1-8, 2014.

- [13] Case, Karl E. and Quigley, John M. and Shiller, Robert J. Comparing Wealth Effects: The Stock Market versus the Housing Market, Advances in Macroeconomics, 5, 1-32, 2005.

- [14] Holyst, J. A. and ebrowska, M. and Urbanowicz, K. Observations of deterministic chaos in financial time series by recurrence plots, can one control chaotic economy?, The European Physical Journal B, 20, 531-535, 2001.

- [15] Hsieh, David A. Chaos and Nonlinear Dynamics: Application to Financial Markets, 46, 1839-1877, 1991.

- [16] May, Robert M. and Levin, Simon A. and Sugihara, G. Complex systems: Ecology for bankers, Nature, 451, 893-895, 2008.

- [17] Peinke, J. and Bttcher, F. and Barth, St.Anomalous statistics in turbulence, financial markets and other complex systems, Annalen der Physik, 13, 450-460, 2004.

- [18] Bonanno, Giovanni and Lillo, Fabrizio and Mantenga, Rosario N. Levels of complexity in financial markets, Physica A: Statistical Mechanics and its Applications, 299, 16-27, 2001.

- [19] Stauffer, Dietrich and Sornette, Didier. Self-organized percolation model for stock market fluctuations, Physica A, 271, 496-506, 1999.

- [20] Didier Sornette, Why Stock Markets Crash: Critical Events in Complex Financial Systems, Princeton University, USA, 2003.

- [21] Thorsten Hens and Klaus Reiner Schenk-Hoppé, Handbook of financial markets. Dynamics and evolutions, North Holland, USA, 2009.

- [22] Preis, Tobias and Kenett, Dror Y. and Stanley, H. Eugene and Helbing, Dirk and Ben-Jacob, Eshel Quantifying the Behavior of Stock Correlations Under Market Stress, Scientific Reports, 2, 1-5, 2012.

- [23] Wang, Duan and Podobnik, Boris and Horvatić, Davor and Stanley, H. Eugene. Quantifying and modeling long-range cross correlations in multiple time series with applications to world stock indices, Phys. Rev. E, 83, 1-5, 2011.

- [24] Preis, Tobias and Reith, Daniel and Stanley, H. Eugene Complex dynamics of our economic life on different scales: insights from search engine query data, Philosophical Transactions of the Royal Society A, 368, 5707-5719, 2010.

- [25] Pasquini, Michele and Serva, Maurizio. Multiscale behaviour of volatility autocorrelations in a financial market, Economic Letters, 65, 275-279, 1999.

- [26] Focardi, Sergio and Cincotti, Silvano and Marchesi, Michele Self-organization and market crashes, Journal of Economic Behavior & Organization, 49, 241-267, 2002.

- [27] Turcotte, Donald L. and Rundle, John B. Self-organization and market crashes, Self-organized complexity in the physical, biological, and social sciences, 99, 2463-2465, 2002.

- [28] Huang, Zhi-Feng. Self-organized model for information spread in financial markets, The European Physical Journal B, 16, 379-385, 2000.

- [29] Martín-del-Brío, Bonifacio and Serrano-Cinca, Carlos. Self-organizing neural networks for the analysis and representation of data: Some financial cases, Neuro Computing & Applications, 1, 193-206, 1993.

- [30] Veldkamp, Laura L. Slow boom, sudden crash, Journal of Economic Theory, 124, 230-257, 2005.

- [31] Boldrin, Michele and Levine, David K. Growth Cycles and Market Crashes, Journal of Economic Theory, 96, 13-39, 2001.

- [32] Sornette, Didier. Predictability of catastrophic events: Material rupture, earthquakes, turbulence, financial crashes, and human birth, Proceedings of the National Academy of Sciences of the United States of America, 99, 2522-2529, 1999.

- [33] Johansen, A. and Sornette, D. Modeling the stock market prior to large crashes, The European Physical Journal B, 9, 167-174, 1999.

- [34] Voit, Johannes. From Brownian motion to operational risk: Statistical physics and financial markets, Physica A: Statistical Physics and its applications, 321, 286-299, 2003.

- [35] Plerou, Vasiliki and Gopikrishnan, Parameswaran and Rosenow, Bernd and Amaral, Luis A. N. and Stanley, H. Eugene. Econophysics: financial time series from a statistical physics point of view, Physica A, 279, 443-456, 2000.

- [36] Mantegna, Rosario N. and Palágyi, Zoltán and Stanley, H. Eugene. Applications of statistical mechanics to finance, Physica A: Statistical Mechanics and its Applications, 274, 216-221, 1999.

- [37] Mantegna, Rosario N. and Palágyi, Zoltán and Stanley, H. Eugene. Focus on statistical physics modeling in economics and finance, New Journal of Physics, 13, 025011-1-025011-6, 2011.

- [38] Ingber, L. Statistical mechanics of nonlinear nonequilibrium financial markets: Applications to optimized trading, Mathematical and Computer Modelling, 23, 101-121, 1996.

- [39] Johannes Voit, The Statistical Mechanics of Financial Markets, 3rd Edition, Springer, USA, 2005.

- [40] Kwon, O. and Yang, J. -S. Information flow between stock indices, Europhysics Letters, 82, 68003-1-68003-4, 2002.

- [41] Mitchell, Mark L. and Mulherin, J. Harold. The Impact of Public Information on the Stock Market”, journal = ”The Journal of Finance, 49, 923-950, 2012.

- [42] Zhang, X. Frank Information Uncertainty and Stock Returns, The Journal of Finance, 61, 105-137, 2006.

- [43] Marschinski, R. and Kantz, H. Analysing the information flow between financial time series, Eur. Phys. J. B, 30, 275-281, 2002.

- [44] French, Kenneth R. and Roll, Richard. Stock return variances: The arrival of information and the reaction of traders, Journal of Financial Economics, 17, 5-26, 1986.

- [45] Bassler, Kevin E. and Gunaratne, Gemunu H. and McCauley, Joseph L. Markov processes, Hurst exponents, and nonlinear diffusion equations: With application to finance, Physica A, 369, 343-353, 2006.

- [46] Sokolov, I. M. and Klafter, J. From diffusion to anomalous diffusion: A century after Einstein’s Brownian motion, Chaos: An Interdisciplinary Journal of Nonlinear Science, 15, 026103-1-026103-7, 2005.

- [47] Metzler, Ralf and Klafter, Joseph, The random walk’s guide to anomalous diffusion: a fractional dynamics approach, Physics Reports, 339, 1-77, 2000.

- [48] Bolsa Mexicana de Valores, Grupo BMV, url = http://www.bmv.com.mx/, 2014.

- [49] IPC, Yahoo Finance, url = http://finance.yahoo.com, 2014.

- [50] Sheather, Simin J. Density Estimation, Statistical Science, 19, 588-597, 2004.

- [51] A. C. Guidoum. kedd: Kernel estimator and bandwidth selection for density and its derivatives, R package version 1.0.1, url = http://CRAN.R-project.org/package=kedd, 2004.

- [52] Gennady Samorodnitsky and Murad S. Taqqu, Stable non-gaussian random processes, Chapman & Hall/CRC, USA, 2000.

- [53] Diethelm Wuertz and Martin Maechler and Rmetrics core team members. stabledist: Stable Distribution Functions., R package version 0.6-6, url = cran.r-project.org/web/packages/stabledist/index.html, 2014.

- [54] Carbone, A. and Castelli, G. and Stanley, H. E. Time-dependent Hurst exponent in financial time, Physica A, 344, 267-271, 2004.

- [55] Mario Lefebvre, Applied stochastic processes, Springer, USA, 2007.

- [56] Robert H. Shumway and David S. Stoffer, Time series analysis and its applications, 2st, Springer, USA, 2006.

- [57] Coronel-Brizio, H. F. and Hernández-Montoya, A. R. Asymptotic behavior of the daily increment distribution of the IPC, the mexican stock market index, Revista Mexicana de Física, 51, 27-31, 2005.

- [58] Coronel-Brizio, H. F. and de la Cruz-Laso, C. R. and Hernández-Montoya, A. R. Fitting the Power-law Distribution to the Mexican Stock Market index data, arXiv:cond-mat/0303568, 1-4, 2003.

- [59] Gabaix, X. and Gopikrishnan, Parameswaran. and Plerou, Vasiliki. and Stanley, H. Eugene. A theory of power-law distributions in financial market fluctuations, Nature, 423, 267-270”, 2003.

- [60] Gopikrishnan, Parameswaran and Plerou, Vasiliki. and Nunes Amaral, Luís A. and Meyer, Martin and Stanley, H. Eugene. Scaling of the distribution of fluctuations of financial market indices, Physical Review E, 60, 5305-5316, 1999.