Exact solution of a generalized version

of the Black-Scholes equation

Abstract

We analyze a generalized version of the Black-Scholes equation depending on a parameter . It satisfies the martingale condition and coincides with the Black-Scholes equation in the limit case . We show that the generalized equation is exactly solvable in terms of Hermite polynomials and numerically compare its solution with the solution of the Black-Scholes equation.

keywords:

econophysics, quantum finance , Black-Scholes equation , option pricingMSC:

[2010] 91B80 , 91G801 Introduction

The mathematical model based on the Black-Scholes equation

| (1) |

anticipates rather well the observed prices for options in the case of a strike price that is not too far from the current price of the underlying asset [8]. The price of an option at a moment of time depends on the current price , the volatility , the risk-free interest rate , the strike price and the maturity time . In the case of an European option, the price is described by the solution of equation (1) satisfying the condition

| (2) |

in the case of a call option, and

| (3) |

in the case of a put option. The alternative version of the equation (1)

| (4) |

obtained by using the change of independent variable

| (5) |

allows one to use the formalism of quantum mechanics in option pricing [1, 2, 4, 7]. In the new variable the conditions (2) and (3) become

| (6) |

and respectively,

| (7) |

The more general version of (4) depending on a function

| (8) |

satisfies the martingale condition [1] and hence can be used for studying processes in finance. Our purpose is to investigate the particular case

| (9) |

that is, the equation

| (10) |

where is a parameter. The equation (10) is exactly solvable in terms of Hermite polynomials and coincides in the limit case with the equation (4) which corresponds to the standard Black-Scholes equation.

2 A shifted oscillator

Let and be two constants. By using the Hermite polynomial

| (11) |

we define for each the function

| (12) |

If we denote

| (13) |

then the previous relation can be written as

| (14) |

By substituting this relation into the diferential equation

| (15) |

satisfied by the Hermite polynomial we get the equality

| (16) |

which can be written in the form

| (17) |

This means that is an eigenfunction of the shifted oscillator [3, 5, 6].

| (18) |

corresponding to the eigenvalue , for any . Since

| (19) |

the system of functions is orthonormal, that is,

| (20) |

One can prove that it is complete in the space of square integrable functions.

3 A generalized version of the Black-Scholes equation

A straightforward generalization of the equation

| (21) |

is the equation

| (22) |

satisfying the martingale condition [1]. It can be written in the form

| (23) |

by using the Hamiltonian

| (24) |

The Hamiltonian is equivalent with the Hermitian Hamiltonian

| (25) |

by the similarity transformation

| (26) |

where

| (27) |

In the particular case considered in this article

| (28) |

The Hamiltonian is up to the multiplicative factor the Hamiltonian of a shifted oscillator, namely

| (29) |

where

| (30) |

with

Therefore, for each the function

| (31) |

is an eigenfunction of corresponding to the eigenvalue

| (32) |

The equation (23) can be written as

| (33) |

or in the form

| (34) |

A function is the solution of (23) satisfying (6) if and only if

| (35) |

that is, the function

| (36) |

is the solution of the equation

| (37) |

satisfying the condition

| (38) |

But, the solution of (37) satisfying (38) is

| (39) |

with the coefficients determined from the relation

| (40) |

namely,

| (41) |

In the case of the call option, the solution of the generalized Black-Scholes equation expressed in terms of Hermite polynomials is

| (42) |

The case of a put option can be analyzed in a very similar way.

The Black-Scholes equation is exactly solvable. By denoting

| (43) |

the formulas for the values of a European option can be written in the form

| (44) |

where [8]

| (45) |

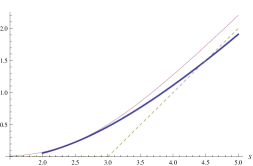

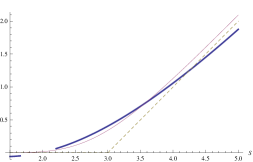

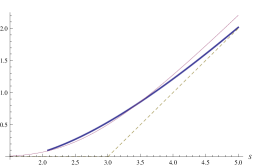

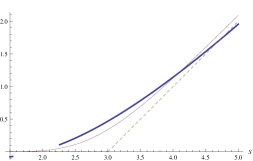

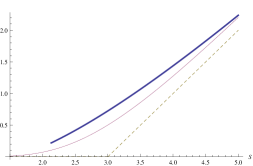

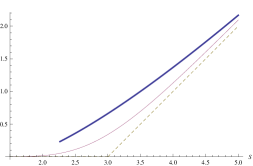

In Fig. 1 we present (thick line) versus (thin line) and (dashed line) for (left side), (right side) and (first row), (second row), (third row) by choosing the following values of the parameters: , , and .

4 Concluding remarks

In quantum mechanics as well as in econophysics, exact solutions are known only in a small number of particular cases and, generally, they play an important role. The generalized version of the Black-Scholes equation investigated in this article:

- is exactly solvable for any ,

- satisfies the martingale condition for any ,

- coincides with the Black-Scholes equation in the limit case .

In practice, there are some deviations of prices from those described by the solution of

the Black-Scholes equation. We think that the solution of the generalized Black-Scholes

equation might describe some observed prices, and the parameter might have a certain financial meaning.

References

- [1] B.E. Baaquie, Quantum Finance, Cambridge University Press, 2004.

- [2] F. Bagarello, A quantum statistical approach to simplified stock markets, Physics A 388 (2009) 4397.

- [3] F. Cooper, A. Khare, U. Sukhatme, Supersymmetry and quantum mechanics, Phys. Rep. 251 (1995) 267.

- [4] L.-A. Cotfas, A finite-dimensional quantum model for the stock market, Physics A 392 (2013) 371.

- [5] N. Cotfas and L.A. Cotfas, Hypergeometric type operators and their supersymmetric partners, J. Math. Phys. 52 (2011) 052101.

- [6] M.A. Jafarizadeh and H. Fakhri, Parasupersymmetry and shape invariance in differential equations of mathematical physics and quantum mechanics, Ann. Phys. NY 262 (1998) 260.

- [7] T.K. Jana and P. Roy, Supersymmetry in option pricing, Physica A 390 (2011) 2350-55.

- [8] Ö. Uǧur, An Introduction to Computational Finance, Imperial College Press, London, 2009.