Computation of Gaussian orthant probabilities in high dimension

Abstract

We study the computation of Gaussian orthant probabilities, i.e. the probability that a Gaussian variable falls inside a quadrant. The Geweke-Hajivassiliou-Keane (GHK) algorithm [Geweke, 1991; Keane, 1993; Hajivassiliou et al., 1996; Genz, 1992], is currently used for integrals of dimension greater than . In this paper we show that for Markovian covariances GHK can be interpreted as the estimator of the normalizing constant of a state space model using sequential importance sampling (SIS). We show for an AR(1) the variance of the GHK, properly normalized, diverges exponentially fast with the dimension. As an improvement we propose using a particle filter (PF). We then generalize this idea to arbitrary covariance matrices using Sequential Monte Carlo (SMC) with properly tailored MCMC moves. We show empirically that this can lead to drastic improvements on currently used algorithms.

We also extend the framework to orthants of mixture of Gaussians (Student, Cauchy etc.), and to the simulation of truncated Gaussians.

1 Introduction

There are many applications where computing an orthant probability in high dimension with respect to a Gaussian or Student distribution is an issue of interest. For instance it is common in statistics to compute the likelihood of models, where we observe only an event with respect to multivariate Gaussian random variables. In Econometrics, the multivariate probit model [Train, 2009], where we observe a decision among alternative choices each of them corresponding to a Gaussian utility, is commonly studied. It can be written as an orthant problem. Other such models are the spatial probit [LeSage et al., 2011] and Thurstonian models [Yao and Bockenholt, 1999]. Other applications than direct modelization can be found, such as multiple comparison tests [Hochberg and Tamhane, 1987], where the integration is done with respect to a Student (see Bretz et al. [2001] for an example). Orthant probabilities are also of interest in other fields than statistics, i.e. stochastic programming [Prekopa, 1970], structural system reliability [Pandey, 1998], engineering, finance, etc.

The problem at hand is the computation of the integral,

| (1) |

where . The Student case will be written as a mixture of the above integral with an inverse Chi-square (see Section 5.1).

Many algorithms have been proposed to compute (1); for a review see Genz and Bretz [2009]. They can be divided into two groups. The first are numerical algorithms to deal with small dimensional integrals. In dimension there exist algorithms [Genz and Bretz, 2009] where after sphericization, such that the Gaussian has an identity covariance matrix, one applies recursively numerical computations of the error function. For higher dimensions than three Minwa et al. [2003] propose to express orthant probabilities as differences of orthoscheme probabilities, where an orthoscheme is (1) with correlation matrix satisfying . This can be easily computed by recursion. However the decomposition in orthoscheme probabilities has factorial complexity. The second group of algorithms is Monte Carlo based and may be used for dimensions higher than 10. In particular GHK due to Geweke [1991], Keane [1993] and Hajivassiliou et al. [1996] and conjointly to Genz [1992], has been widely adopted for the applications described above.

In this paper we show that in the case of Markovian covariances (i.e. covariances that can be written as those of Markovian processes), the GHK algorithm estimates the normalizing constant of a state space model (SSM), using sequential importance sampling (SIS) with optimal proposal. We show in addition for a first order autoregressive process (henceforth AR(1)) that the normalized variance diverges exponentially fast.

To avoid this behavior we propose to use a particle filter. We extend this methodology to the non Markovian case by using Sequential Monte Carlo (SMC). SMC allows additional gain in efficiency by considering different MCMC moves and proposals. In addition the algorithm is adaptive and simplifies automatically to the GHK if the integral is simple enough. In our numerical experiments we find a substantial improvement.

We start by reviewing the existing GHK algorithm (Section 2), we then discuss the algorithm’s behavior for Markovian covariance matrices and propose an extension to higher dimensions (Section 3). In Section 4 we extend this proposal to arbitrary covariance matrices. We propose some extensions for the simulation of truncated distributions and for other distributions (5). Finally we present some numerical results and conclude (Sections 6 and 7).

Notations

For any vector for we write for the vector of the first components, and we take . We let , and also write for the vector ; are respectively the Gaussian cdf and pdf, we write for the pdf, , of a Gaussian truncated to the set evaluated in . We will also abuse notation and use to denote the probability of a set when . For instance .

2 Geweke-Hajivassiliou-Keane (GHK) simulator

From now on to simplify notations, and without loss of generality, we limit ourselves to the study of the following multidimensional integral:

| (2) |

with . Note that the extension to integrals where some components of the vectors are respectively and is direct.

Let be the Cholesky decomposition of , i.e. with , and if . We can write the previous equation after the change of variable for which :

the -th truncation being such that , from the positivity of the . Thus we can write:

where the set is an interval.

The GHK algorithm is an importance sampling algorithm based on this structure. It proposes particles distributed under and evaluates the average of the weights . The algorithm is described in pseudo-code in Alg. 1.

⋆Recall that can be computed as a difference of two one dimensional cdf for the truncation defined above.

To generate truncated Gaussian variables the usual approach in the GHK simulator is to use the inverse cdf method. We follow this approach in the rest of the paper except where stated otherwise. When the numerical stability of the inverse cdf is an issue we will use the algorithm proposed in Chopin [2011].

In the next section we will study with more care the case where the covariance matrix of the underlying Gaussian vector has a Markovian structure.

3 The Markovian case

When the covariance matrix is Markovian, that is a matrix for which the inverse is tri-diagonal, the simulation step of Alg. 1 is the simulation of a Markov process . At time the weights depend on only. Let us take a lag autoregressive process (AR(1)) for the purpose of exposition, and study the probability of it being in some hyperrectangle . The integral of interest is therefore:

| (3) |

The GHK algorithm consists in sampling from the Markov process:

The matrix is tridiagonal, the weights at time are therefore . Eq. 3 can be seen as the likelihood of the state space model [Cappé et al., 2005]:

where is observed. The GHK can be interpreted as a sequential importance sampler (SIS) using proposal .

3.1 Toy example

Let us specify a bit more the problem to simplify notation and show some properties of a thus defined algorithm.

Consider the problem of finding the probability that an AR(1),

is inside the hyper-cube , for some . We have set , and a constant.

The GHK algorithm consists in this case in simulating the above Markov chain constrained to and in computing under this distribution the products of the weights . The simulations are therefore generated by the Markov probability kernel

| (4) |

For this model we have the following proposition:

Proposition 3.1

For the Markov model defined by , the normalized square product of weights of the normalizing constant has the following behavior:

| (5) |

where subscript denotes integration with respect to the invariant distribution of , the other expectation is taken relatively to the Markov chain , and , .

Proof:

A detailed proof is given in appendix A.

Under -Uniform ergodicity, that follows from our proof, the denominator is the square of the limit of the product of weights and can be interpreted as a scaling factor. Thus the result above shows that this renormalized squared estimator diverges exponentially fast as the dimension of the integral increases.

Remark 3.1

In the course of the proof we showed that the normalizing constant has a log-normal limiting distribution, resulting in a skewed distribution. We expect that the distribution of the estimator will have its mode away from the expected value resulting in some apparent bias. In fact one can show that the normalized third order moment will also grow exponentially.

GHK has quadratic complexity however we can show that for at least one covariance structure the variance diverges exponentially fast. This fully justifies the use of an algorithm of higher computational complexity. In the following section we propose a natural extension to deal with this issue in the Markovian case.

3.2 Particle filter (PF)

PF is a common extension of SIS that corrects the weight degeneracy problem. The solution brought by particle filtering [Gordon et al., 1993] is to use a resampling step, i.e. to kill those particles with low weights and to replicate those with high contribution. At time one resamples the particles by sampling from the distribution where stands for the -th renormalized weight at time , and the Dirac measure in . All the weights are then set to one.

We use an adaptive version of this algorithm where the resampling step is triggered only when the ESS of the weight is lower than some threshold, where the ESS is defined as

and indicates the number of draws from the independent distribution to obtain the same variance. Note that it is closely related to the inverse of equation (5), hence we expect that without resampling it goes to zero with exponential speed.

We define the state space model:

One can use a PF to compute the likelihood of such model,

A PF with proposal distribution is described in Alg. 2. Our application corresponds to the special case where:

where the set depends on only.

The proposal thus defined corresponds to the optimal one [Doucet et al., 2000], that is the distribution proportional to in our case proportional to hence the truncated Gaussian. The weights are given by the normalizing constant , in our case .

To resample we propose to use systematic resampling [Carpenter et al., 1999] (for other approaches see Douc et al. [2005]). Systematic resampling is described in Algorithm 4 (Appendix B).

The particle filter thus defined outputs an unbiased estimator of the likelihood Del Moral [1996], and thus the orthant probability in our case.

Note that the output of Algorithm 2 is of the form of a product of terms smaller than one, in our case those terms can be very small and lead to numerical issues. One way of dealing with this issue is to rewrite all the algorithm in log scale.

Remark 3.2

As we are here in the special case of being able to sample from the optimal distribution (as shown in Section 3) one could resort to the auxiliary particle filter (APF, Pitt and Shephard [1999]). In fact in this special case the algorithm amounts to exchanging the resampling step and the move step of the particle filter. We tested this approach on some Markov processes and observed no improvements in term of variance on repeated draws.

Example 3.1

We can show that the previous process (Section 3.1) benefits from resampling when the ESS goes beneath a given level.

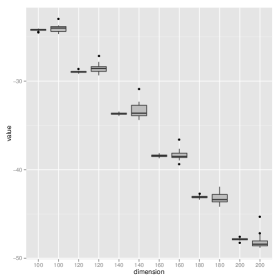

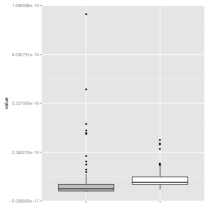

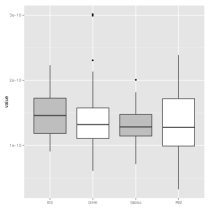

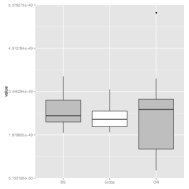

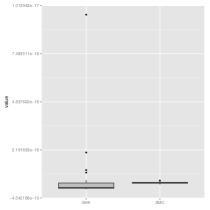

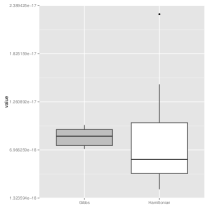

Figure (1) shows that the GHK algorithm’s variance increases more quickly as compared to the PF (that seem to have some stable variance on the considered dimension). In addition the distribution of the GHK estimator seem to be skewed towards smaller values as increases. This results in some bias on the last boxplot. As described in remark 3.1 this behavior is due to the log-Normal limiting distribution of the output of the algorithm. The skewness coefficient increases exponentially with .

Estimation of the log probability that an AR(1) process (defined previously) with has all its component in . GHK sampler (grey) and PF (white) on various dimension from 100 to 200. On the right panel the two ESS for dimension 200. On both cases is set to .

3.2.1 Thurstonian Model

Thurstonian models arise in Psychology and Economics [Yao and Bockenholt, 1999] to describe the ranking of alternatives by individuals (referred to as judges).

Suppose that we observe the rank of some independent Gaussian random variables,

where . The likelihood of one observation is an orthant probability:

| (6) |

with the convention that

This model is similar to the previous one but with .

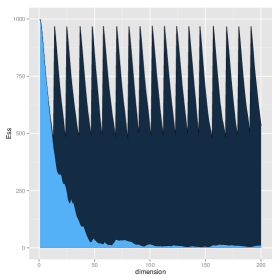

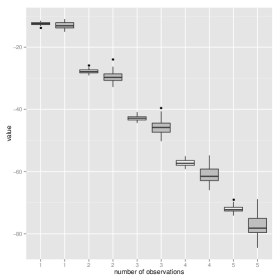

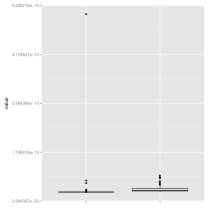

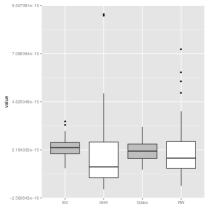

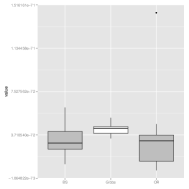

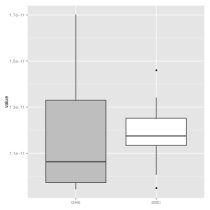

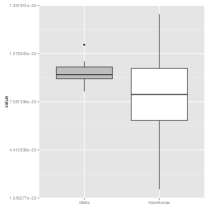

Estimation of the likelihood of a Thurstoninan model with and the number of observations is ranging from to the PF (white) and the GHK (grey). The threshold ESS is set to and the number of particles is set to . The right panel shows the ESS of both algorithms for and .

We find that the likelihood is estimated with smaller variance. In addition, because of the heavy tail distribution of the GHK simulator’s output we observe a bias (see Figure 2). Again one can explain the strong observed bias by remark 3.1 and the fact that we do not replicate enough the experiment to observe the tail of the distribution. In addition as suggested above the ESS of the GHK seems to decrease exponentially fast to zero.

From this observation we could apply this algorithm to perform inference by using Particle MCMC [Andrieu et al., 2010], where this estimation of the likelihood can be plugged in a Random walk Metropolis Hastings and still target the appropriate distribution.

4 Non Markovian case

For more general covariances we propose to use Sequential Monte Carlo (SMC) [Del Moral et al., 2006]. As previously we will base the algorithm on the proposal of GHK, increasing the dimension of the problem at each time step. However we now have an additional degree of freedom: the order in which we incorporate the variables. In the following section we study an approach to ordering the variables.

4.1 Variable ordering

We follow Gibson et al. [1994] in ordering the variables from the most difficult to the simplest, where difficult constraints are considered to be the one that impact the most the probability.

However we cannot evaluate exactly the probabilities as it is our final goal. Instead Gibson et al. [1994] propose to replace the simulations by the expected value of the truncated Gaussian.

The algorithm starts by choosing the first index , and defining as follows:

i.e. the smallest possible probability that the Gaussian will be in . This enables an approximation of the next probability as a function of .

where is the Cholesky decomposition of the matrix after substituting the first and the th variable.

We end up with the desired vector that gives us the order in which to choose the covariances and truncation points. The algorithm is summed up by Alg. 5 in appendix C. The algorithm has quadratic time complexity, however its cost is negligible as compared to the subsequent Monte Carlo algorithm.

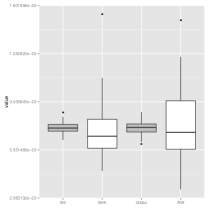

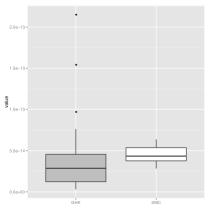

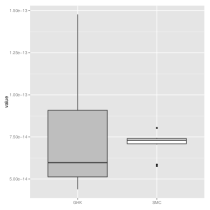

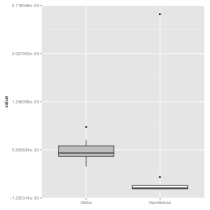

We show the use of the reordering in moderate dimensions (50 and 60) on the GHK simulator. This is already a great improvement especially as the dimension increases. Figure (3), shows boxplots of 50 repetitions of the GHK for both ordered (white) and non-ordered (grey) inputs.

Covariance matrices generated from random samples with heavy tails (see Section 6). In both case we use a GHK simulator with variable ordering (white), without (grey). The various dimension are simulated with the same algorithm and same seed, such that the small ones are subsets of the others. When the variables are not ordered we observe some outliers, and this phenomenon is reduced with Gibson et al. [1994]’s algorithm.

From dimension 50 and upwards we start observing some skewed distributions for the GHK estimator as noted in remark 3.1. The phenomenon seems to be reduced by ordering.

This effect is relatively dangerous as some draws depart a lot from the mean value. The ordering will be used on all examples from now on to reduce the variance. In Section 6 we have empirical evidence that using an appropriate move step deals with this tail effect, in our examples.

We have shown that in the particular case of Markov processes we can strikingly benefit from the use of resampling. In the next section we attempt to generalize our finding to a broader range of problems.

4.2 A sequential Monte Carlo (SMC) algorithm

The algorithm discussed in Section 3 can be generalized to non Markovian Gaussian vectors by applying the SMC methodology. Define the following sequence of distribution:

| (7) |

indexed by , where the unnormalized quantity is our target integrand. We thus want to compute an estimator of for a given ,

SMC samplers are a class of algorithms that generalize particle filters to non dynamic problems (Neal [2001],Chopin [2002], Del Moral et al. [2006]). Their aim is to sample from a sequence of measures where is easy to sample from and is our target. The algorithm works by moving from one target to the other by importance sampling, and avoid degeneracy of the weights by resampling if the ESS falls bellow a threshold. In the case of the GHK the sequence of distribution consist of adding a dimension at each step. To ensure particle diversity after resampling the particles are moved according to a MCMC kernel targeting the current distribution. This is the most computationally expensive step. Different alternatives are described in the next section.

The main steps are described in Algorithm (3) bellow:

An interesting feature of Algorithm 3 is that if the integral is simple enough the ESS will never fall under the threshold and the above algorithm breaks down to a GHK simulator. This allows the algorithm to adapt to simple cases at a minimal effort, that of computing the ESS.

4.3 Move steps

The moves step will have an important impact on the non-degeneracy of the particle system. We want to construct a Markov chain that moves the particles as far away from their initial position as possible. In addition this step will be the bulk of the added time complexity compared to GHK, so we want to make it as efficient as possible.

4.3.1 Gibbs sampler

The structure of our target (7), where the dependence of the Gaussian components lies within the truncation, does not allows a direct application of the Gibbs sampler of Robert [1995], without a change of variable. In this section, to simplify notations we consider the special case of . We write the conditional distribution at time as proportional to , where is the matrix built with the first lines and columns of . The conditional is given by:

We therefore have to compute those sets for each component up to and simulate according to a truncated Gaussian. Computing the set can lead to one or two sided truncations depending on the sign of the .

The main drawback about having to compute this step each time we resample is its complexity. This operation has time complexity per time step. This is easily seen as the set in the above equation is just the result of some matrix inversion for a lower triangular system of dimension . This leads to an SMC algorithm that seem to have a prohibitive complexity of , where the GHK simulator had an complexity. However we have shown that GHK’s variance diverges exponentially quickly on some examples suggesting that this complexity might be acceptable. In fact examples in high dimension show that even at constant computational cost the algorithm is able to over-perform GHK (see Section 6).

4.3.2 Hamiltonian Monte Carlo

An alternative to Gibbs sampler is to use Hamiltoninan Monte Carlo (HMC) (see [Neal, 2010] for a survey), and the idea of Pakman and Paninski [2012] for truncated Gaussians.

HMC is based on interpreting the variables of interest as the position of a particle with potential the opposite of the log target and by simulating the momentum as a Gaussian with given mass matrix. The proposal of the Metropolis-Hastings is then constructed by applying the equations of motion up to a time horizon to the problem. This leads to an efficient algorithm that makes use of the gradient of the target to explore its support. We refer the reader to Neal [2010] for more details on the algorithm and describe the approach proposed by Pakman and Paninski [2012] to adapt the algorithm to truncated Gaussians.

Based on the fact that the log density of a Gaussian random variable is a quadratic form, the movement equation can be dealt with explicitly. The scheme is written as an exact HMC (i.e. not resulting in numerical integration). Remains then to deal with the truncation. Pakman and Paninski [2012] show that they can be treated as “walls” for the given particle, a reflection principle can be applied for any particle hitting the constraint during the algorithm. In particular we must find the time at which occurs the first “hit”. In our experiment the time horizon is set to a uniform draw on as suggested in Neal [2010]. The average value is advocated by Pakman and Paninski [2012].

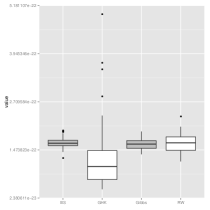

The computation of the first hitting time dominates the cost of the algorithm. This is particularly true when the truncation are small as the number of hitting times will be high. Figure 10 in appendix D shows a comparison of the SMC algorithm with the Gibbs sampler (grey) and exact HMC (white). Although this Markov chain algorithm seems to perform very well for a wide range of problems and has a neat formalism, we find that it does not outperform Gibbs sampling when used as a move. The specificity of the move step in SMC is that the particles are already distributed according to , therefore the move need not propagate each particle across all the support. In particular the strength of HMC in quickly exploring the target might be less useful in this context.

4.3.3 Overrelaxation

Overrelaxation for Gaussian random variables was proposed by Adler [1981] as a way of improving Gibbs sampling for a distribution with Gaussian conditionals.

For each component the proposal is for , and with and the expectation and variance of . The case is the classical Gibbs sampler, the case is a special case of random walk Metropolis-Hasting proposal. One can check that if then has the correct distribution.

Given a particle , we propose a new one according to:

Setting aside the constraint for a moment the invariant distribution of such kernel is an independent (0,1)-Gaussian. If we add an acceptation step such that we accept if it satisfies the constraint at time , the Markov kernel leaves the current distribution invariant (7).

We find that the fact that overrelaxation is close to a Metropolis adjusted Langevin algorithm (MALA) helps to calibrate the algorithm, , hence the proposal in MALA is . From Roberts and Rosenthal [1998] we have that should be . To calibrate the algorithm we propose to match the two drifts. We find that , the constant should then be close from a problem to an other because locally we are always in the case of independent Gaussians (locally the constraints have less impact). We find that in our case taking gives the expected behavior and acceptance ratio.

4.3.4 Repeating the move step

Dubarry and Douc [2011] have shown, for particle filters, that applying some Metropolis Hastings kernel targeting the filtering distribution on the particles leads to a close to optimal variance (the variance is the same as one coming from an sample). This convergence results happens after iteration of the Markov kernel. These results suggest repeating the move step after each resampling step until some criterion of convergence is satisfied.

We compute the sum of absolute distances that the particles have moved after each step (a similar metric was used in Schäefer and Chopin [2013] for the discrete case). We repeat the move until this scalar value stabilizes. The stabilization of the total metric should be associated with the cancellation of the dependence between the particles (leading to a close to independent system).

4.3.5 Block sampling

To diversify the particle system after each resampling we have relied until now on invariant kernels targeting the current distribution . An alternative to this approach is given by Doucet et al. [2006], where importance sampling is done on the space of with a given number of previous time steps. This limits the behavior of the particles all stemming from one path after a few iterations. We briefly describe the idea in the following.

Suppose at time we have a weighted set of particles such that ; instead of proposing a particle , propose a block of size , , and discard the particles . The distribution of the resulting system is intractable because of the marginalization. However Doucet et al. [2006] note that importance sampling is still possible on the extended set of particles by introducing some auxiliary distribution . This leads to the correct marginal whatever and the algorithm has the following incremental weights:

The authors show that the optimal proposal and resulting weights are given by:

In our case the optimal proposal can then be shown to be:

Notice that this is the density of a truncated Gaussian distribution, yielding a weight depending on an orthant probability (denominator). In most cases this is not available and in our particular case it is the quantity of interest. We can however compute explicitly this integral for and . The former is the usual case (block of size one). The case did not bring any improvement in terms of variance in all our simulation. We concentrated on the extension to blocks of higher dimension.

In this case we have to resort to approximations of the proposal. The first idea would be to approximate it by a Gaussian using expectation propagation [Minka, 2001]. However this approach did not perform better than the use of Gibbs sampler mentioned earlier. Another approach to approximate the distribution is to consider the Gibbs sampler on a block of size with the GHK proposal.

4.3.6 Partial conclusion

We have shown that the proposed Gibbs sampler outperforms HMC. Concerning block sampling the different approaches were tested on several dimensions only to find that the best performing approach was to use partial Gibbs sampling, i.e. a Gibbs sampler on a block. In the numerical tests we provide in Section 6 we show only the latter.

In our simulations we propose to repeat each kernels as was explained in Section 4.3.4. We propose to test the Gibbs sampler and the overrelaxed random walk.

In addition we have studied other kernels based on the geometry of the problem; in particular, one can draw random walks on the line between the current particle and the basic solution of our constraint. Those approach did not however outperform the proposals discussed above.

5 Extentions

5.1 Student Orthant

We can easily extend our approach to the computation of orthant probabilities for other distributions, in particular for mixtures of Gaussians, that is probabilities that can be written as:

| (8) |

where is a Gaussian. Several distributions can be created as such. For instance, the Student distribution where the variance is marginally distributed as an inverse-. Hence the distribution:

where is where we multiply by and . They are an interesting application to those algorithms because they come at a minimal additional cost and are of use in multiple comparison [Bretz et al., 2001].

Another example is the logistic distribution where is some transformation of a Kolmogorov-Smirnov distribution (see Holmes and Held [2006]). This could be used to perform Bayesian inference on multinomial logistic regression.

To deal with this integral we can extend the space on which the SMC is carried out at time . Hence the move step is performed on the extended space . In our Student example it amounts to taking as a target distribution

The normalizing constant that the SMC algorithm approximates is

At each move step we therefore move the particles using a Metropolis-Hastings algorithm targeting and perform the remaining Gibbs sampler updates conditionally on . This additional step allows for further mixing. Benefits from this step are already found in relatively low dimension as shown in Section 6.

5.2 SMC as a truncated distribution sampler

A natural extension is to use Alg. 3 to compute other integrals with respect to truncated Gaussians. At time the output of the algorithm is a weighted sample approximating . Hence any integral of the form , where expectation is taken with respect to , can be approximated by . The same argument goes for the truncated Student.

We test the idea for computing the expectation of truncated multivariate Student. We use a Gibbs sampler as a benchmark based on Robert [1995]’s sampler by adding a MH step to deal with (see previous section). The Gibbs update is done after a change of variable that leaves the truncations independent. This can be shown to be more efficient. We allocate times more computational time to the Gibbs sampler than the SMC.

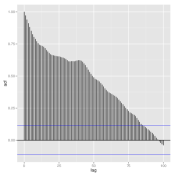

In Figure 4 we see that after thinning one out of points the ACF and trace plots point to bad exploration of the target’s support. This behavior shows that the convergence is too slow for the algorithm to be of practical use. On the other hand the SMC is still stable as is shown in the next section.

In addition of outperforming the Gibbs sampler for fairly moderate dimension, the SMC algorithm was found to be stable for approximating the expectation in dimensions up to .

The data are generated as explained in the “Numerical results section”, for dimension . The left panels are trace plots for two components. The right panels are the ACFs. Both are shown after a thinning of 1/1000. Both show a slow convergence, whereas we observe that SMC is stable.

6 Numerical results

6.1 Covariance simulation, tunning parameters

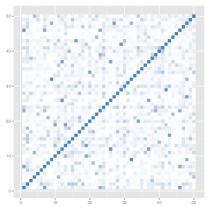

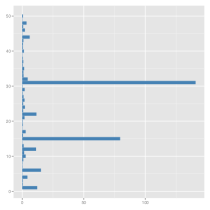

To build the covariance matrices we propose to use draws from a Cauchy distribution. We start by sampling a matrix and a vector a from an independent Cauchy distribution , then construct the covariance matrix as and the truncation as . Because of the heavy tails the resulting correlation matrix (figure 5a) has many close to zero entries and some high correlations. The truncations also have some very high levels (figure 5b).

We find that this approach leads to more challenging covariances than those built by sampling the spectrum of the covariance matrix as proposed for instance in Christen et al. [2012].

Covariance matrices generated from random samples with heavy tails. The various dimension are simulated with the same algorithm and same seed, such that the small ones are subsets of the others. The left panel shows a heatmap of the correlation, the right panel the left trucation of the integral.

The tuning parameters of the algorithm are the threshold that tunes the number of steps of the MCMC kernel, and the targeted ESS under which we resample, . The former is set to some small value (0.01) and has not much influence. The latter gives us a trade off between variance and computational cost. In our example we have found that allows good approximation, however this value should be increased with the difficulty of the problem.

6.2 GHK for moderate dimensions

All our results are shown at constant computational cost: we repeat the algorithm in a first time to get their execution time, and we then scale them accordingly. In the above example (dimension 40) for instance the number of draws associated with the GHK algorithm is . The number of particles of the SMC sampler with Gibbs Markov transition is .

The various dimensions are simulated as described in Section 6. Different moves are tested inside SMC. As we have already discussed GHK leads to a higher variance and outliers. Block sampling (BS) and Gibbs sampling (Gibbs) seem to outperform the overrelaxed random walk (RW). However all three stay stable until dimension 50.

We find that in moderate dimension () the GHK simulator breaks down in attempting to compute the probability of the orthant generated by our simulation scheme. This is all the more problematic as it gives an answer, and there is no way of checking its departure from the true value.

Another interesting aspect is the fact that the block sampling algorithm performs well in those dimensions. It is quicker than to move the particles in every dimension as is done with MCMC. The truncations that lead to a drop of probability are close together because of the ordering, hence once the difficult dimensions have been “absorbed” it is less and less paramount to visit the past truncations.

6.3 High dimension orthant probabilities

In dimensions higher than , the covariance we simulate lead to integrals that cannot be treated with the GHK algorithm. In our simulations GHK always returned NaN values due to the low values of the weights. For the SMC an indicator of the good behavior of the algorithm can be seen in either its reproducibility and the fact that we do not encounter asymmetry (see Remark 3.1) as for the GHK in the first two Sections. Furthermore the ESS does not fall very low along the particles’ draw (Figure 7c).

The various dimensions are simulated as described in Section 6. Different moves are tested inside SMC. As we have already discussed GHK leads to a higher variance and outliers. Gibbs sampling (Gibbs) seem to outperform the overrelaxed random walk (OR) and Block sampling (BS). However all three stay stable until dimension 180. The ESS for the Gibbs sampler is shown in panel for a threshold of and . Despite some sudden drops it seems to be stable.

For those dimensions the Gibbs sampler performs best in terms of variance. However if one’s goal is a fast algorithm, at the cost of higher variance the overrelaxation might be preferable at some point as the dimension of the target increases. The latter as a complexity smaller of one degree such that at constant computational cost it will have more and more particles allocated to it.

6.4 Student orthant probabilities

We use the same schemes as before to construct the covariance matrix and fix a degree of freedom of in our experiments. As before we show an improvement as compared to previous algorithms. This improvements appears also for moderate dimensions. It seems that there is an important gain in considering the extended target.

As for the Gaussian case we find that the output of GHK is heavily skewed. It seems that it is not the case for our algorithm.

Covariance matrices generated from random samples with heavy tails. We find that the SMC outperforms the GHK. As for the previous cases the GHK leads to some outliers.

6.5 Application to random utility models

Random utility models are an important area of research in Economics to model choice data [Train, 2009]. Consider an agent confronted to alternatives each giving utility modeled by with a Gaussian noise. Individual chooses alternative if . The likelihood is the probability of this set integrated over the unobserved alternatives. Hence the likelihood is given by:

where integration is taken over , where . The above integral is an orthant probability of dimension . A yet more challenging case occurs in the presence of panel data. The latter corresponds to sequential choices of an individual in time. We denote those choices by the subscript . We observe for every individual. Integration is now in dimension and takes the form:

We take the covariance structure studied in Bursh-Supan et al. [1992]. The noise term is where , where are correlated amongst choices, so are . The terms are all Gaussian.

The dataset is simulated to allow for examples that are more complex, and of variable size. In the model presented above individuals are independent so that we present results in computing the integral for , and have already a big advantage of using our methodology.

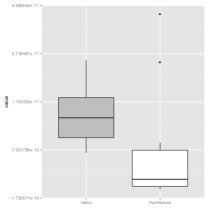

Dataset: The Data is simulated using the covariance proposed in Bursh-Supan et al. [1992], the value of the parameter for which the likelihood is evaluated is taken at random.

Figure (9) shows, for two problems of different size, the gain in precision at constant computational cost. The improvement is substantial and increases with the size of the problem. Taking would only increase this effect as it would consist in taking products of such estimators.

The latter result suggests that we could use the likelihood for inference using either maximum likelihood or PMCMC. Computing the likelihood with lowest possible variance is also a key issue in finding the evidence in the most precise manner possible.

When comparing the two algorithms we set the number of particles of SMC to , for the same computational cost we allocate to GHK. SMC has however still a lower variance. Regardless of computational time, the ability to compute precise integrals for a small number of particles can also be of importance. It is the case for instance in SMC2 [Chopin et al., 2013] where whole trajectories have to be kept in memory for several samplers.

One could extend these models to multivariate Probit with Student distribution and to multivariate logit models for more robustness. In this case we can use the algorithm based on the mixture representation built in Section 5.1.

7 Conclusion

We have shown empirically that the GHK algorithm collapses when the dimension of the problem increases (returning NaN values). In other cases, the distribution of estimates generated by GHK may have heavy tails (see also Remark 3.1). Theoretically for at least one covariance structure we have shown that the variance of the algorithm diverges exponentially fast with the dimension (Section 3). Our SMC algorithm seems to correct this behavior, and was found to be of practical use for many problems.

We have tested several kernels as part of the move step (Section 4.2). We advise the practitioners to use Gibbs sampling as the standard “go to” move step. However improvements in speed can be achieved for dimensions around 50 using only a partial update. In addition as the dimension increases one might want to use a method with lower complexity at the cost of having to repeat the move a bit more. In this case we recommend the use of an overrelaxed random walk Metropolis-Hastings.

We have shown that the same idea can be use for computing probabilities of mixtures of Gaussians. In addition we can use the weighted particles returned by the algorithm to compute other integrals (mean, variance, .etc). This approach can outperform a classical Gibbs sampler when the dimension exceeds .

Acknowledgment

This work is part of my PhD thesis under the supervision of Nicolas Chopin. I am grateful for his comments.

References

- Adler [1981] S. L. Adler. Over-relaxation method for the Monte Carlo evaluation of the partition function for multiquadratic actions. Physical Review D, 23(12):2901, 1981.

- Andrieu et al. [2010] C. Andrieu, A. Doucet, and R. Holenstein. Particle Markov Chain Monte Carlo. J. R. Statist. Soc. B, 72:269–342, 2010.

- Bretz et al. [2001] F. Bretz, A. Genz, and L. A. Hothorn. On the numerical availability of multiple comparison procedures. Biometrical journal, 5:645–656, 2001.

- Bursh-Supan et al. [1992] A. Bursh-Supan, V. Hajivassiliou, and L. J. Kotlikoff. Health, children and elderly arrangments: a multiperiod multinomial probit model with unobserved heterogeneity and autocorrelated errors. Topics in the Economics of Aging, pages 79–108, 1992.

- Cappé et al. [2005] O. Cappé, E. Moulines, and T. Ryden. Inference in Hidden Markov Models. Springer Series in statistics, 2005.

- Carpenter et al. [1999] J. Carpenter, P. Clifford, and P. Fearnhead. Improved particle filter for nonlinear problems. IEE Proceedings-Radar, Sonar and Navigation, 146(1):2–7, 1999.

- Chopin [2002] N. Chopin. A sequential particle filter method for static models. Biometrika, 89(3):539–551, 2002.

- Chopin [2011] N. Chopin. Fast simulation of truncated Gaussian distributions. Statist. Comput., 21(2):275–288, 2011. ISSN 0960-3174. doi: 10.1007/s11222-009-9168-1.

- Chopin et al. [2013] N. Chopin, O. Papaspiliopoulos, and P. E. Jacob. SMC2: an efficient algorithm for sequential analysis of state space models. J. R. Statist. Soc. B, 75(3):397–426, 2013.

- Christen et al. [2012] J. A. Christen, C. Fox, D. A. Pérez-Ruiz, and M. Santana-Cibrian. On optimal direction Gibbs sampling. arXiv preprint arXiv:1205.4062, 2012.

- Del Moral [1996] P. Del Moral. Non-linear filtering: interacting particle resolution. Markov processes and related fields, 2(4):555–581, 1996.

- Del Moral et al. [2006] P. Del Moral, A. Doucet, and A. Jasra. Sequential Monte Carlo samplers. J. R. Statist. Soc. B, 68(3):411–436, 2006. ISSN 1467-9868.

- Douc et al. [2005] R. Douc, O. Cappe, and E. Moulines. Comparison of resampling schemes for particle filtering. In Proc. 4th Int. Symp. Image and Signal Processing and Analysis ISPA 2005, pages 64–69, 2005.

- Doucet et al. [2000] A. Doucet, S. Godsill, and C. Andrieu. On sequential monte carlo sampling methods for bayesian filtering. Statistics and computing, 10(3):197–208, 2000.

- Doucet et al. [2006] A. Doucet, M. Briers, and S. Senecal. Efiicient Block Sampling Strategies for Sequential Monte Carlo. J. Comput. Graph. Statist., 15(3):693–711, 2006.

- Dubarry and Douc [2011] C. Dubarry and R. Douc. Particle approximation improvement of the joint smoothing distribution with on the fly variance estimation. arXiv:1107.5524v1, pages 1–19, June 2011.

- Flecher et al. [2009] C. Flecher, D. Allard, and P. Naveau. Truncated skew-normal distributions: Estimation by weighted moments and application to climatic data. Technical Report 39, Institut National de la Recherche Agronomique, 2009.

- Genz [1992] A. Genz. Numerical Computation of Multivariate Normal Probabilities. J. Comput. Graph. Statist., 1(2):141–149, June 1992.

- Genz and Bretz [2009] A. Genz and F. Bretz. Computation of Multivariate Normal and t Probabilities, volume 195 of Lecture Notes in Statistics. Springer, 2009.

- Geweke [1991] J. Geweke. Efficient simulation from the multivariate normal and student-t distributions subject to linear constraints. Computing Science and Statistics, 23:571–578, 1991.

- Gibson et al. [1994] G. J. Gibson, C. A. Glasbey, and D. A. Elston. Monte-carlo evalution of multivariate normal integrals and sensitivity to variate ordering. Advances in Numerical Methods & applications, pages 120–126, 1994.

- Gordon et al. [1993] N. J Gordon, D. J Salmond, and A. FM Smith. Novel approach to nonlinear/non-gaussian bayesian state estimation. In IEE Proceedings F (Radar and Signal Processing), volume 140, pages 107–113. IET, 1993.

- Hajivassiliou et al. [1996] V. Hajivassiliou, D. McFadden, and P. Ruud. Simulation of multivariate normal rectangle probabilities and their derivatives theoretical and computational results. Journal of Econometrics, 72(1-2):85–134, May–June 1996.

- Hochberg and Tamhane [1987] Y. Hochberg and A. C. Tamhane. Multiple comparison procedures. John Wiley & Sons, Inc., 1987.

- Holmes and Held [2006] C. Holmes and L. Held. Bayesian auxiliary variable models for binary and multinomial regression. Bayesian Analysis, 1(1):145–168, 2006.

- Keane [1993] M. Keane. Simulation estimation for panel data models with limited dependent variables. MPRA Paper 53029, University Library of Munich, Germany, 1993.

- LeSage et al. [2011] J. P. LeSage, Pace R. K., N. Lam, R. Campanella, and Liu X. New Orleans buisness recovery in the aftermath of huricane Katrina. App. Stat., 174(4):1007–1027, October 2011.

- Meyn and Tweedie [2009] S. Meyn and R. L. Tweedie. Markov chains and Stochastic Stability. Cambridge University Press, 2nd edition, 2009.

- Minka [2001] T. Minka. Expectation Propagation for approximate Bayesian inference. In Proc. 17th Conf. Uncertainty Artificial Intelligence, UAI ’01, pages 362–369. Morgan Kaufmann Publishers Inc., 2001.

- Minwa et al. [2003] T. Minwa, A. J. Hayter, and S. Kuriki. The evaluation of general non-centered orthant pro. J. R. Statist. Soc. B, 65:223–234, 2003.

- Neal [2010] M. Neal. MCMC using Hamiltonian dynamics. Handbook of Markov Chain Monte Carlo, page 51, 2010.

- Neal [2001] R. Neal. Annealed importance sampling. Statist. Comput., 11(2):125–139, 2001.

- Pakman and Paninski [2012] A. Pakman and L. Paninski. Exact Hamiltonian Monte Carlo for Truncated Multivariate Gaussians. arXiv:1208.4118, pages 1–30, 2012.

- Pandey [1998] M.D. Pandey. An effective approximation to evaluate multinormal integrals. Structural Safety, 20(1):51–67, 1998.

- Pitt and Shephard [1999] M. Pitt and N. Shephard. Filtering via simulation: Auxiliary particle filters. J. Am. Statist. Assoc., 94(446):590–599, June 1999.

- Prekopa [1970] A. Prekopa. On probabilistic constrained programming. In Proceedings of the Princeton symposium on mathematical programming, pages 113–138. Princeton, New Jersey: Princeton University Press, 1970.

- Robert [1995] C. P. Robert. Simulation of truncated normal variables. Statist. Comput., 5(2):121–125, 1995.

- Roberts and Rosenthal [1998] G. Roberts and J. Rosenthal. Optimal scaling of discrete approximations to langevin diffusions. J. R. Statist. Soc. B, 60(1):255–268, 1998.

- Schäefer and Chopin [2013] C. Schäefer and N. Chopin. Sequential Monte Carlo on large binary sampling spaces. Statistics and Computing, 23(2):163–184, 2013. ISSN 0960-3174. doi: 10.1007/s11222-011-9299-z. URL http://dx.doi.org/10.1007/s11222-011-9299-z.

- Train [2009] K. E. Train. Discrete Choice methods with simulation. Cambridge University Press, 2009.

- Van der Vaart [1998] A. Van der Vaart. Asymptotic statistics. Cambridge university press, 1998.

- Yao and Bockenholt [1999] G. Yao and U. Bockenholt. Bayesian estimation of Thurstonian ranking models based on the Gibbs sampler. British Journal of Mathematical and Statistical Psychology, 52:79–92, 1999.

Appendix A Proof of proposition 2.1

Proof:

We have that for the transition density , associated with the kernel with respect to the Lebesgue measure, is lower bounded by a constant and the transition is continuous. This Markov chain is a -irreducible on a compact support. Hence we can show that the whole support is small [Meyn and Tweedie, 2009].

Hence by theorem 16.1.2 to show V-Uniform ergodicity the transition must satisfy the drift condition:

for , and a certain with value in . We take , . In the following we check this condition.

The left hand side is given by for the above transition probability,

The ratio is continuous on the bounded set , and can be bounded by a constant, such that the by taking the drift condition is satisfied for a depending on .

In addition we can compute exactly the invariant measure. It is unique and given by the solution of:

The solution of the above equation is a truncated skew-Normal distribution,

The moments of this distribution have been studied in Flecher et al. [2009], in particular note that .

Define , by theorem 17.0.1 [Meyn and Tweedie, 2009] to obtain a CLT for we must ensure that there exist a constant such that on . Such a constant can be found by noting that is bounded as long as and that is strictly increasing of with value on . The value of depends on . We obtain the following convergence result,

where the variance term is defined because is bounded on , and . By taking the exponential and using the continuous mapping theorem (p.7 Van der Vaart [1998]) we get a log-normal limiting distribution

By Portmanteau’s Lemma (p.6 Van der Vaart [1998]) for as a continuous and positive function,

where the last line is obtained by Jensen inequality. The denominator is the square of limit value of the normalizing constant under -Uniform ergodicity that follows from the above statement.

Appendix B Resampling

Appendix C Variable Ordering

Where is updated accordingly when the order is changed.

Appendix D Hamiltonian Monte Carlo

Covariance matrices generated from random samples with heavy tails. The various dimension are simulated with the same algorithm and same seed, such that the small ones are subsets of the others. The grey boxplot corresponds to the Gibbs sampler the white to the HMC. The Gibbs sampler seem to have smaller variance and no outliers.