Fast Randomized Kernel Methods With Statistical Guarantees

Abstract

One approach to improving the running time of kernel-based methods is to build a small sketch of the kernel matrix and use it in lieu of the full matrix in the machine learning task of interest. Here, we describe a version of this approach that comes with running time guarantees as well as improved guarantees on its statistical performance. By extending the notion of statistical leverage scores to the setting of kernel ridge regression, we are able to identify a sampling distribution that reduces the size of the sketch (i.e., the required number of columns to be sampled) to the effective dimensionality of the problem. This latter quantity is often much smaller than previous bounds that depend on the maximal degrees of freedom. We give an empirical evidence supporting this fact. Our second contribution is to present a fast algorithm to quickly compute coarse approximations to these scores in time linear in the number of samples. More precisely, the running time of the algorithm is with only depending on the trace of the kernel matrix and the regularization parameter. This is obtained via a variant of squared length sampling that we adapt to the kernel setting. Lastly, we discuss how this new notion of the leverage of a data point captures a fine notion of the difficulty of the learning problem.

1 Introduction

We consider the low-rank approximation of symmetric positive semi-definite (SPSD) matrices that arise in machine learning and data analysis, with an emphasis on obtaining good statistical guarantees. This is of interest primarily in connection with kernel-based machine learning methods. Recent work in this area has focused on one or the other of two very different perspectives: an algorithmic perspective, where the focus is on running time issues and worst-case quality-of-approximation guarantees, given a fixed input matrix; and a statistical perspective, where the goal is to obtain good inferential properties, under some hypothesized model, by using the low-rank approximation in place of the full kernel matrix. The recent results of Gittens and Mahoney [1] provide the strongest example of the former, and the recent results of Bach [2] are an excellent example of the latter. In this paper, we combine ideas from these two lines of work in order to obtain a fast randomized kernel method with statistical guarantees that are improved relative to the state-of-the-art.

To understand our approach, recall that several papers have established the crucial importance—from the algorithmic perspective—of the statistical leverage scores, as they capture structural non-uniformities of the input matrix and they can be used to obtain very sharp worst-case approximation guarantees. See, e.g., work on CUR matrix decompositions [3, 4], work on the the fast approximation of the statistical leverage scores [5], and the recent review [6] for more details. Here, we simply note that, when restricted to an SPSD matrix and a rank parameter , the statistical leverage scores relative to the best rank- approximation to , call them , for , are the diagonal elements of the projection matrix onto the best rank- approximation of . That is, , where is the best rank approximation of and where is the Moore-Penrose inverse of . The recent work by Gittens and Mahoney [1] showed that qualitatively improved worst-case bounds for the low-rank approximation of SPSD matrices could be obtained in one of two related ways: either compute (with the fast algorithm of [5]) approximations to the leverage scores, and use those approximations as an importance sampling distribution in a random sampling algorithm; or rotate (with a Gaussian-based or Hadamard-based random projection) to a random basis where those scores are uniformized, and sample randomly in that rotated basis.

In this paper, we extend these ideas, and we show that—from the statistical perspective—we are able to obtain a low-rank approximation that comes with improved statistical guarantees by using a variant of this more traditional notion of statistical leverage. In particular, we improve the recent bounds of Bach [2], which provides the first known statistical convergence result when substituting the kernel matrix by its low-rank approximation. To understand the connection, recall that a key component of Bach’s approach is the quantity , which he calls the maximal marginal degrees of freedom.111We will refer to it as the maximal degrees of freedom. Bach’s main result is that by constructing a low-rank approximation of the original kernel matrix by sampling uniformly at random columns, i.e., performing the vanilla Nyström method, and then by using this low-rank approximation in a prediction task, the statistical performance is within a factor of of the performance when the entire kernel matrix is used. Here, we show that this uniform sampling is suboptimal. We do so by sampling with respect to a coarse but quickly-computable approximation of a variant to the statistical leverage scores, given in Definition 8 below, and we show that we can obtain similar guarantees by sampling only columns, where . The quantity is called the effective dimensionality of the learning problem, and it can be interpreted as the implicit number of parameters in this nonparametric setting [7, 8].

We expect that our results and insights will be useful much more generally. As an example of this, we can directly compare the Nyström sampling method to a related divide-and-conquer approach, thereby answering an open problem of Zhang et al. [7]. Recall that the Zhang et al. divide-and-conquer method consists of dividing the dataset into random partitions of equal size, computing estimators on each partition in parallel, and then averaging the estimators. They prove the minimax optimality of their estimator, although their multiplicative constants are suboptimal; and, in terms of the number of kernel evaluations, their method requires , with in the order of , which gives a total number of evaluations. They noticed that the scaling of their estimator was not directly comparable to that of the Nyström sampling method (which was proven to only require evaluations, if the sampling is uniform [2]), and they left it as an open problem to determine which if either method is fundamentally better than the other. Using our Theorem 3, we are able to put both results on a common ground for comparison. Indeed, the estimator obtained by our non-uniform Nyström sampling requires only kernel evaluations (compared to and ), and it obtains the same bound on the statistical predictive performance as in [2]. In this sense, our result combines “the best of both worlds,” by having the reduced sample complexity of [7] and the sharp approximation bound of [2].

2 Preliminaries and notation

Let be pairs of points in , where is the input space and is the response space. The kernel-based learning problem can be cast as the following minimization problem:

| (1) |

where is a reproducing kernel Hilbert space and is a loss function. We denote by the positive definite kernel corresponding to and by a corresponding feature map. That is, for every . The representer theorem [9, 10] allows us to reduce Problem (1) to a finite-dimensional optimization problem, in which case Problem (1) boils down to finding the vector that solves

| (2) |

where . We let be the eigenvalue decomposition of , with , , and an orthogonal matrix. The underlying data model is

with , a deterministic sequence and are i.i.d. standard normal random variables. We consider to be the squared loss, in which case we will be interested in the mean squared error as a measure of statistical risk: for any estimator , let

| (3) |

be the risk function of where denotes the expectation under the randomness induced by . In this setting the problem is called Kernel Ridge Regression (KRR). The solution to Problem (2) is , and the estimate of at any training point is given by . We will use as a shorthand for the vector when the matrix is used as a kernel matrix. This notation will be used accordingly for other kernel matrices (e.g. for a matrix ). Recall that the risk of the estimator can then be decomposed into a bias and variance term:

| (4) |

Solving Problem (2), either by a direct method or by an optimization algorithm needs at least a quadratic and often cubic running time in which is prohibitive in the large scale setting. The so-called Nytröm method approximates the solution to Problem (2) by substituting with a low-rank approximation to . In practice, this approximation is often not only fast to construct, but the resulting learning problem is also often easier to solve [11, 12, 13, 1]. The method operates as follows. A small number of columns are randomly sampled from . If we let denote the matrix containing the sampled columns, the overlap between and in , then the Nyström approximation of is the matrix

More generally, if we let be an arbitrary sketching matrix, i.e., a tall and skinny matrix that, when left-multiplied by , produces a “sketch” of that preserves some desirable properties, then the Nyström approximation associated with is

For instance, for random sampling algorithms, would contain a non-zero entry at position if the -th column of is chosen at the -th trial of the sampling process. Alternatively, could also be a random projection matrix; or could be constructed with some other (perhaps deterministic) method, as long as it verifies some structural properties, depending on the application [6, 1, 4, 3].

We will focus in this paper on analyzing this approximation in the statistical prediction context related to the estimation of by solving Problem (2). We proceed by revisiting and improving upon prior results from three different areas. The first result (Theorem 5) is on the behavior of the bias of , when is constructed using a general sketching matrix . This result underlies the statistical analysis of the Nyström method. To see this, first, it is not hard to prove that in the sense of usual the order on the positive semi-definite cone. Second, one can prove that the variance is matrix-increasing, hence the variance will decrease when replacing by . On the other hand, the bias (while not matrix monotone in general) can be proven to not increase too much when replacing by . This latter statement will be the main technical difficulty for obtaining a bound on (see Appendix A). A form of this result is due to Bach [2] in the case where is a uniform sampling matrix. The second result (Theorem 7) is a concentration bound for approximating matrix multiplication when the rank-one components of the product are sampled non uniformly. This result is derived from the matrix Bernstein inequality, and yields a sharp quantification of the deviation of the approximation from the true product. The third result (Definition 8) is an extension of the definition of the leverage scores to the context of kernel ridge regression. Whereas the notion of leverage is established as an algorithmic tool in randomized linear algebra, we introduce a natural counterpart of it to this statistical setting. By combining these contributions, we are able to give a sharp statistical statement on the behavior of the Nyström method if one is allowed to sample non uniformly. All the proofs are deferred to the appendix.

3 Revisiting prior work and new results

3.1 A structural result

We begin by stating a “structural” result that upper-bounds the bias of the estimator constructed using the approximation . This result is deterministic: it only depends on the properties of the input data, and holds for any sketching matrix that satisfies certain conditions. This way the randomness of the construction of is decoupled from the rest of the analysis. We highlight the fact that this view offers a possible way of improving the current results since a better construction of -whether deterministic or random- satisfying the data-related conditions would immediately lead to down stream algorithmic and statistical improvements in this setting.

Theorem 1.

Let be a sketching matrix and the corresponding Nyström approximation. For , let . If the sketching matrix satisfies for and , where denotes the maximum eigenvalue and is the operator norm then

| (5) |

In the special case where contains one non zero entry equal to in every column with the number of sampled columns, the result and its proof can be found in [2] (appendix B.2), although we believe that their argument contains a problematic statement. We propose an alternative and complete proof in Appendix A. The subsequent analysis unfolds in two steps: (1) assuming the sketching matrix satisfies the conditions stated in Theorem 5, we will have , and (2) matrix concentration is used to show that an appropriate random construction of satisfies the said conditions. We start by stating the concentration result that is the source of our improvement (section 3.2), define a notion of statistical leverage scores (section 3.3), and then state and prove the main statistical result (Theorem 3 section 3.4). We then present our main algorithmic result consisting of a fast approximation to this new notion of leverage scores (section 3.5).

3.2 A concentration bound on matrix multiplication

Next, we state our result for approximating matrix products of the form when a few columns from are sampled to form the approximate product where contains the chosen columns. The proof relies on a matrix Bernstein inequality (see e.g. [14]) and is presented at the end of the paper (Appendix B).

Theorem 2.

Let be positive integers. Consider a matrix and denote by the column of . Let and be a subset of formed by elements chosen randomly with replacement, according to the distribution

| (6) |

for some . Let be a sketching matrix such that only if and 0 elsewhere. Then

| (7) |

Remarks: 1. This result will be used for , in conjunction with Theorem 5 to prove our main result in Theorem 3. Notice that is a scaled version of the eigenvectors, with a scaling given by the diagonal matrix which should be considered as “soft projection” matrix that smoothly selects the top part of the spectrum of . The setting of Gittens et al. [1], in which is a 0-1 diagonal is the closest analog of our setting.

2. It is known that is the optimal sampling distribution in terms of minimizing the expected error [15]. The above result exhibits a robustness property by allowing the chosen sampling distribution to be different from the optimal one by a factor .222In their work [15], Drineas et al. have a comparable robust statement for controlling the expected error. Our result is a robust quantification of the tail probability of the error, which is a much stronger statement. The sub-optimality of such a distribution is reflected in the upper bound (7) by the amplification of the squared Frobenius norm of by a factor . For instance, if the sampling distribution is chosen to be uniform, i.e. , then the value of for which (6) is tight is in which case we recover a concentration result proven by Bach [2]. Note that Theorem 7 is derived from one of the state-of-the-art bounds on matrix concentration, but it is one among many others in the literature; and while it constitutes the base of our improvement, it is possible that a concentration bound more tailored to the problem might yield sharper results.

3.3 An extended definition of leverage

We introduce an extended notion of leverage scores that is specifically tailored to the ridge regression problem, and that we call the -ridge leverage scores.

Definition 1.

For , the -ridge leverage scores associated with the kernel matrix and the parameter are

| (8) |

Note that is the diagonal entry of . The quantities are in this setting the analogs of the so-called leverage scores in the statistical literature, as they characterize the data points that “stick out”, and consequently that most affect the result of a statistical procedure. They are classically defined as the row norms of the left singular matrix of the input matrix, and they have been used in regression diagnostics for outlier detection [16], and more recently in randomized matrix algorithms as they often provide an optimal importance sampling distribution for constructing random sketches for low rank approximation [15, 17, 3, 4, 1] and least squares regression [18] when the input matrix is tall and skinny (). In the case where the input matrix is square, this definition is vacuous as the row norms of are all equal to 1. Recently, Gittens and Mahoney [1] used a truncated version of these scores (that they called leverage scores relative to the best rank- space) to obtain the best algorithmic results known to date on low rank approximation of positive semi-definite matrices. Definition 8 is a weighted version of the classical leverage scores, where the weights depend on the spectrum of and a regularization parameter . In this sense, it is an interpolation between Gittens’ scores and the classical (tall-and-skinny) leverage scores, where the parameter plays the role of a rank parameter. In addition, we point out that Bach’s maximal degrees of freedom is to the -ridge leverage scores what the coherence is to Gittens’ leverage scores, i.e. their (scaled) maximum value: ; and that while the sum of Gittens’ scores is the rank parameter , the sum of the -ridge leverage scores is the effective dimensionality . We argue in the following that Definition 8 provides a relevant notion of leverage in the context of kernel ridge regression. It is the natural counterpart of the algorithmic notion of leverage in the prediction context. We use it in the next section to make a statistical statement on the performance of the Nyström method.

3.4 Main statistical result: an error bound on approximate kernel ridge regression

Now we are able to give an improved version of a theorem by Bach [2] that establishes a performance guaranty on the use of the Nyström method in the context of kernel ridge regression. It is improved in the sense that the sufficient number of columns that should be sampled in order to incur no (or little) loss in the prediction performance is lower. This is due to a more data-sensitive way of sampling the columns of (depending on the -ridge leverage scores) during the construction of the approximation . The proof is in Appendix C.

Theorem 3.

Theorem 3 asserts that substituting the kernel matrix by a Nyström approximation of rank in the KRR problem induces an arbitrarily small prediction loss, provided that scales linearly with the effective dimensionality 333Note that depends on the precision parameter , which is absent in the classical definition of the effective dimensionality [8, 7, 2] However, the following bound holds: . and that is not too small444This condition on is not necessary if one constructs as (see proof).. The leverage-based sampling appears to be crucial for obtaining this dependence, as the -ridge leverage scores provide information on which columns -and hence which data points- capture most of the difficulty of the estimation problem. Also, as a sanity check, the smaller the target accuracy , the higher , and the more uniform the sampling distribution becomes. In the limit , is in the order of and the scores are uniform, and the method is essentially equivalent to using the entire matrix . Moreover, if the sampling distribution is a factor away from optimal, a slight oversampling (i.e. increase by ) achieves the same performance. In this sense, the above result shows robustness to the sampling distribution. This property is very beneficial from an implementation point of view, as the error bounds still hold when only an approximation of the leverage scores is available. If the columns are sampled uniformly, a worse lower bound on that depends on is obtained [2].

3.5 Main algorithmic result: a fast approximation to the -ridge leverage scores

Although the -ridge leverage scores can be naively computed using SVD, the exact computation is as costly as solving the original Problem (2). Therefore, the central role they play in the above result motivates the problem of a fast approximation, in a similar way the importance of the usual leverage scores has motivated Drineas et al. to approximate them is random projection time [5]. A success in this task will allow us to combine the running time benefits with the improved statistical guarantees we have provided.

Algorithm:

-

•

Inputs: data points , probability vector , sampling parameter , , .

-

•

Output: -approximations to .

-

1.

Sample data points from with replacement with probabilities .

-

2.

Compute the corresponding columns of the kernel matrix.

-

3.

Construct and as presented in Section 2.

-

4.

Construct such that .

-

5.

For every , set

(9) where is the -th row of , and return it.

Running time:

The running time of the above algorithm is dominated by steps 4 and 5. Indeed, constructing can be done using a Cholesky factorization on and then a multiplication of by the inverse of the obtained Cholesky factor, which yields a running time of . Computing the approximate leverage scores in step 5 also runs in . Thus, for , the overall algorithm runs in . Note that formula (9) only involves matrices and vectors of size (everything is computed in the smaller dimension ), and the fact that this yields a correct approximation relies on the matrix inversion lemma (see proof in Appendix D). Also, only the relevant columns of are computed and we never have to form the entire kernel matrix. This improves over earlier models [1] that require that all of has to be written down in memory. The improved running time is obtained by considering the construction (9) which is quite different from the regular setting of approximating the leverage scores of a rectangular matrix [5]. We now give both additive and multiplicative error bounds on its approximation quality.

Theorem 4.

Let , and . Let be a Nyström approximation of by choosing columns at random with probabilities , . If

then we have

and

with probability at least .

Remarks: 1. Theorem 4 states that if the columns of are sampled proportionally to then is a sufficient number of samples. Recall that , so our procedure is akin to sampling according to the squared lengths of the data vectors, which has been extensively used in different contexts of randomized matrix approximation [19, 15, 17, 6, 1].

2. Due to how is defined in eq. (1) the in the denominator is artificial: should be thought of as a “rescaled” regularization parameter . In some settings, the that yields the best generalization error scales like , hence is sufficient. On the other hand, if the columns are sampled uniformly, one would get .

4 Experiments

We test our results based on several datasets: one synthetic regression problem from [2] to illustrate the importance of the -ridge leverage scores, the Pumadyn family consisting of three datasets pumadyn-32fm, pumadyn-32fh and pumadyn-32nh 555http://www.cs.toronto.edu/~delve/data/pumadyn/desc.html and the Gas Sensor Array Drift Dataset from the UCI database666https://archive.ics.uci.edu/ml/datasets/Gas+Sensor+Array+Drift+Dataset. The synthetic case consists of a regression problem on the interval where, given a sequence and a sequence of noise , we observe the sequence

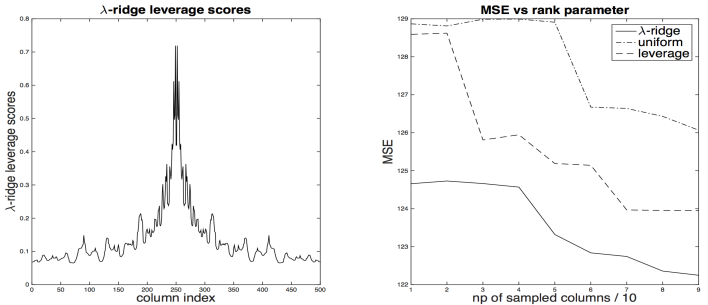

The function belongs to the RKHS generated by the kernel where is the -th Bernoulli polynomial [2]. One important feature of this regression problem is the distribution of the points on the interval : if they are spread uniformly over the interval, the -ridge leverage scores are uniform for every , and uniform column sampling is optimal in this case. In fact, if for , the kernel matrix is a circulant matrix [2], in which case, we can prove that the -ridge leverage scores are constant. Otherwise, if the data points are distributed asymmetrically on the interval, the -ridge leverage scores are non uniform, and importance sampling is beneficial (Figure 1). In this experiment, the data points have been generated with a distribution symmetric about , having a high density on the borders of the interval and a low density on the center of the interval. The number of observations is . On Figure 1, we can see that there are few data points with high leverage, and those correspond to the region that is underrepresented in the data sample (i.e. the region close to the center of the interval since it is the one that has the lowest density of observations). The -ridge leverage scores are able to capture the importance of these data points, thus providing a way to detect them (e.g. with an analysis of outliers), had we not known their existence.

For all datasets, we determine and the band width of by cross validation, and we compute the effective dimensionality and the maximal degrees of freedom . Table 1 summarizes the experiments. It is often the case that and , in agreement with Theorem 3.

| kernel | dataset | nb. feat | band width | risk ratio | ||||

| Bern | Synth | 500 | - | - | 24 | 500 | 1.01 () | |

| Linear | Gas2 | 1244 | 128 | - | 126 | 1244 | 1.10 () | |

| Gas3 | 1586 | 128 | - | 125 | 1586 | 1.09 () | ||

| Pum-32fm | 2000 | 32 | - | 31 | 2000 | 0.99 () | ||

| Pum-32fh | 2000 | 32 | - | 31 | 2000 | 0.99 () | ||

| Pum-32nh | 2000 | 32 | - | 32 | 2000 | 0.99 () | ||

| RBF | Gas2 | 1244 | - | 1 | 1135 | 1244 | 1.56 () | |

| Gas3 | 1586 | - | 1 | 1450 | 1586 | 1.50 () | ||

| Pum-32fm | 2000 | - | 5 | 0.5 | 142 | 1897 | 1.00 () | |

| Pum-32fh | 2000 | - | 5 | 747 | 1989 | 1.00 () | ||

| Pum-32nh | 2000 | - | 5 | 1337 | 1997 | 0.99 () |

5 Conclusion

We showed in this paper that in the case of kernel ridge regression, the sampling complexity of the Nyström method can be reduced to the effective dimensionality of the problem, hence bridging and improving upon different previous attempts that established weaker forms of this result. This was achieved by defining a natural analog to the notion of leverage scores in this statistical context, and using it as a column sampling distribution. We obtained this result by combining and improving upon results that have emerged from two different perspectives on low rank matrix approximation. We also present a way to approximate these scores that is computationally tractable, i.e. runs in time with depending only on the trace of the kernel matrix and the regularization parameter. One natural unanswered question is whether it is possible to further reduce the sampling complexity, or is the effective dimensionality also a lower bound on ? And as pointed out by previous work [20, 2], it is likely that the same results hold for smooth losses beyond the squared loss (e.g. logistic regression). However the situation is unclear for non-smooth losses (e.g. support vector regression).

Acknowledgements

An earlier draft of this paper contained a mistake in the proof of Theorem 5. We thank Xixian Chen for signaling it to us. We thank Francis Bach for stimulating discussions and for contributing to a rectified proof. We thank Jason Lee and Aaditya Ramdas for fruitful discussions regarding the same issue. We thank Yuchen Zhang for pointing out the connection to his work.

References

- [1] Alex Gittens and Michael W Mahoney. Revisiting the Nyström method for improved large-scale machine learning. In Proceedings of The 30th International Conference on Machine Learning, pages 567–575, 2013.

- [2] Francis Bach. Sharp analysis of low-rank kernel matrix approximations. In Proceedings of The 26th Conference on Learning Theory, pages 185–209, 2013.

- [3] Petros Drineas, Michael W Mahoney, and S Muthukrishnan. Relative-error CUR matrix decompositions. SIAM Journal on Matrix Analysis and Applications, 30(2):844–881, 2008.

- [4] Michael W Mahoney and Petros Drineas. CUR matrix decompositions for improved data analysis. Proceedings of the National Academy of Sciences, 106(3):697–702, 2009.

- [5] Petros Drineas, Malik Magdon-Ismail, Michael W Mahoney, and David P Woodruff. Fast approximation of matrix coherence and statistical leverage. The Journal of Machine Learning Research, 13(1):3475–3506, 2012.

- [6] Michael W Mahoney. Randomized algorithms for matrices and data. Foundations and Trends in Machine Learning, 3(2):123–224, 2011.

- [7] Yuchen Zhang, John Duchi, and Martin Wainwright. Divide and conquer kernel ridge regression. In Proceedings of The 26th Conference on Learning Theory, pages 592–617, 2013.

- [8] Jerome Friedman, Trevor Hastie, and Robert Tibshirani. The elements of statistical learning, volume 1. Springer series in statistics Springer, Berlin, 2001.

- [9] George Kimeldorf and Grace Wahba. Some results on Tchebycheffian spline functions. Journal of mathematical analysis and applications, 33(1):82–95, 1971.

- [10] Bernhard Schölkopf, Ralf Herbrich, and Alex J Smola. A generalized representer theorem. In Computational learning theory, pages 416–426. Springer, 2001.

- [11] Shai Fine and Katya Scheinberg. Efficient SVM training using low-rank kernel representations. The Journal of Machine Learning Research, 2:243–264, 2002.

- [12] Christopher Williams and Matthias Seeger. Using the Nyström method to speed up kernel machines. In Proceedings of the 14th Annual Conference on Neural Information Processing Systems, pages 682–688, 2001.

- [13] Sanjiv Kumar, Mehryar Mohri, and Ameet Talwalkar. Sampling techniques for the Nyström method. In International Conference on Artificial Intelligence and Statistics, pages 304–311, 2009.

- [14] Joel A Tropp. User-friendly tail bounds for sums of random matrices. Foundations of Computational Mathematics, 12(4):389–434, 2012.

- [15] Petros Drineas, Ravi Kannan, and Michael W Mahoney. Fast Monte-Carlo algorithms for matrices I: Approximating matrix multiplication. SIAM Journal on Computing, 36(1):132–157, 2006.

- [16] Samprit Chatterjee and Ali S Hadi. Influential observations, high leverage points, and outliers in linear regression. Statistical Science, pages 379–393, 1986.

- [17] Petros Drineas, Ravi Kannan, and Michael W Mahoney. Fast Monte-Carlo algorithms for matrices II: Computing a low-rank approximation to a matrix. SIAM Journal on Computing, 36(1):158–183, 2006.

- [18] Petros Drineas, Michael W Mahoney, S Muthukrishnan, and Tamás Sarlós. Faster least squares approximation. Numerische Mathematik, 117(2):219–249, 2011.

- [19] Alan Frieze, Ravi Kannan, and Santosh Vempala. Fast Monte-Carlo algorithms for finding low-rank approximations. Journal of the ACM (JACM), 51(6):1025–1041, 2004.

- [20] Francis Bach. Self-concordant analysis for logistic regression. Electronic Journal of Statistics, 4:384–414, 2010.

- [21] Francis Bach. Personal communication, October 2015.

- [22] Rajendra Bhatia. Matrix analysis, volume 169. Springer Science & Business Media, 2013.

Appendix A Proof of Theorem 5

Note: This proof is inspired by one of Bach [2]. We extend their result to the case of a general sketching matrix . Moreover, we believe their argument contains two problematic statements (about monotonicity of the bias) that we rectify with Lemma 2 and Lemma 3 below. Their result therefore holds also true with minimal change based on this argument.

For kernel ridge regression, the bias of the estimator can be expressed as

For , we consider again the regularized approximation with the sketching matrix. The result of the theorem follows from the three following lemmas.

Lemma 1.

Let where is orthogonal and diagonal positive. We have

| (10) |

Moreover, let

with . If for then

Lemma 2.

If then .

Lemma 3.

If and then the map is increasing. This in particular implies that under the same conditions, .

We next prove the above lemmas.

Proof of Lemma 1. With and , , we have

Due to the matrix inversion lemma, we have

with

and . This shows that for any

Now if for ,

which implies

∎

Since commutes with the identity, we have

Now,

On the other hand,

This yields,

Hence we have the bias inequality

∎

Proof of Lemma 3. Let . The task is to prove that is increasing if . We do so by computing the derivative of and showing that . Let . We have

Now we compute the terms and :

And

The first term is the last equality above is equal to

and the second one is equal to

Now combining the above and taking the limit we have

with

Therefore, the function is increasing for all such that , and the latter is true if . Moreover, since is symmetric we have

and it is sufficient to verify the condition

| (11) |

Now we finish the proof by showing that the above operator norm is smaller than . We have

Taking operator norms, and using the assumption ,

Hence, (11) is satisfied if therefore concluding the proof. ∎

Appendix B Proof of Theorem 7

The proof uses the matrix Bernstein inequality (see e.g. Theorem 6.1.1 in [14]):

Theorem 5.

Consider a sequence of independent random symmetric matrices with dimension . Assume that , , and let . Furthermore, assume that there exists such that . Then

Next , we exhibit the sequence and in our case. We have

and

where are i.i.d. binary random vectors for with (i.e. is the indicator of the chosen column at trial ). Let , then

We choose to be for every . Now we verify the assumptions of the above theorem. The matrices inherit independence from the random vectors , and we have , and . Now we control the spectral norm of the second moment of . Again with we have And for

To proceed, observe that for , since only one column is chosen at a time. This yields

Given that the probability distribution verifies , we get Hence We now apply the theorem with and which leads to the desired result.

Appendix C Proof of Theorem 3

Monotonicity of the variance.

First of all, we observe that the variance of the estimator is matrix-increasing as a function of . Indeed, we have

where is the th eigenvalue of arranged in a decreasing order. The function is increasing for . Moreover, if then by the Courant-Fischer minimax principle for all (e.g. see Corollary III.1.2 in [22]).

Risk bound.

Now, using Theorem 5 combined with the above fact, we have

We set and . The above holds if and . Now let . Then we have and . Using Theorem 7 on , and given that , for the result to hold with probability at least , it is sufficient to set such that which gives the desired lower bound .

Remark: Note that if one uses the regularized Nyström approximation with instead of in the algorithm then the proof would now be complete and the condition condition is not necessary. If one uses , then this latter condition needs to be verified to insure monotonicity of the bias (see Lemma 3).

Controlling .

Now it remains to control the operator norm of the sketching matrix appearing in the lower bound on . To this end we use a variant of the matrix Bernstein inequality (Theorem 5) for controlling operator norms of random matrices (see Corollary 6.2.1 in [14]).

Theorem 6.

Consider a sequence of independent random symmetric matrices with dimension . Assume that , , and let . Furthermore, assume that there exists such that . Then

We are interested in the sum

and similarly to the previous section we consider the sequence where is defined as before and in the standard basis in . Since with we have

with . On the other hand,

Hence

By choosing , we have with probability at least . Taking , the latter probability is greater than , and by the triangle inequality: with the same probability. By taking (thereby verifying the condition from the previous paragraph) we have

if , and therefore (since ) with probability at least .

Appendix D Proof of Theorem 4

First, it is clear that

with the -th element of the standard basis in . Now we bound the approximations by comparing the matrices and with respect to the semidefinite order. Since (Appendix A) and the map is matrix-increasing, we immediately get the upper bound for all . Next we derive the lower bound. For , we consider again the regularized approximation with the sketching matrix. Due the matrix inversion lemma, (Appendix A). Hence to get a lower bound on , it suffices to obtain a lower bound for the same quantity when is replaced by . We proved in Appendix A that if

for with , then

Therefore

where the last line follows by distributing the product and using the inequality for the second term. Hence . Now we choose again and for , we get the additive error bound on and similarly to the proof of Theorem 3, it suffices to have . To finish the proof, we choose the sampling distribution and appropriately. Since

by choosing , we have with , which yields .

As for the multiplicative error bound, using we get

For , . The result follows.