A flexible bivariate location-scale finite mixture approach to economic growth

Abstract

We introduce a multivariate multidimensional mixed-effects regression model in a finite mixture framework. We relax the usual unidimensionality assumption on the random effects multivariate distribution. Thus, we introduce a multidimensional multivariate discrete distribution for the random terms, with a possibly different number of support points in each univariate profile, allowing for a full association structure. Our approach is motivated by the analysis of economic growth. Accordingly, we define an extended version of the augmented Solow model. Indeed, we allow all model parameters, and not only the mean, to vary according to a regression model. Moreover, we argue that countries do not follow the same growth process, and that a mixture-based approach can provide a natural framework for the detection of similar growth patterns. Our empirical findings provide evidence of heterogenous behaviors and suggest the need of a flexible approach to properly reflect the heterogeneity in the data. We further test the behavior of the proposed approach via a simulation study, considering several factors such as the number of observed units, times and levels of heterogeneity in the data.

1 Introduction

In modelling panel economic data, it is common to account for the unobserved heterogeneity between sample units, that is, the heterogeneity that cannot be explained by means of observable covariates (see e.g. Wooldridge, 2002 ; Fitzmaurice et al., 2008). This is normally accomplished by the introduction of latent variables or random effects. For instance, a typical approach consists of associating a random intercept to every sample unit which affects the distribution of each time-specific response in the same fashion. This allows us to account for a form of unobserved heterogeneity which is due to unobservable covariates and related factors. The above considerations are obviously pertinent when we deal with economic growth modelling, where sample units (i.e. countries) are characterized by heterogeneous income performances. Addressing the heterogeneity of analyzed processes is of fundamental importance to the study to the economic growth and has led to a substantial evidence for the existence of variations in growth patterns across countries. Indeed, since Solow’s seminal paper (1956), different econometric and statistical approaches are used to look at countries’ growth. Dynamic panel data with fixed effect (Caselli et al., 1996; Islam, 1995; Temple, 1999), as well as extreme bound analysis (Levine and Renelt, 1992; Temple, 2000), Bayesian model averaging (Doppelhofer et al., 2000; Fernandez et al., 2001) or model on varying coefficients are performed to deal with the main empirical challenges in growth theory: unobserved heterogeneity (Caselli et al., 1996; Pesaran and Smith, 1995; Lee et al., 1997; Durlauf and Johnson, 1995), uncertainty (Temple, 2000) and omitted variable bias (Durlauf and Quah, 1999).

Recently, data-driven approaches to estimate multiple (heterogeneous) growth processes have been employed within the wide class of mixture models (Alfó et al., 2008, Owen et al., 2009; Kerekes, 2012; Baştürk et al., 2012; Bertarelli and Bernardini Papalia, 2013).

We propose an approach to panel growth data based on a flexible bivariate location-scale finite mixture approach, which may be seen as an extension of the approach introduced by Alfó et al. (2008). We introduce a bivariate bidimensional discrete random effects model to account for dependence between outcomes (i.e. per capita income and growth) and heterogeneity between countries in the augmented Solow growth model. The proposed approach may be cast in the literature about finite mixture models for panel data. It is worth noting that other extensions of the finite mixture approach for panel data are available in the literature. We mention, in particular, the extensions proposed by Pittau et al. (2010) and Martínez-Zarzoso and Maruotti (2011), where countries are clustered into clubs depending on unobserved characteristics. Moreover, our approach is more general than those of Durlauf and Johnson (1995) and Ardıç (2006) in which clustering is performed beforehand (i.e. clustering is exogenously specified). Indeed, we develop an endogenous clustering approach lying on a bivariate bidimensional model recovering Bernanke and Gürkaynak (2002) intuition: country’s rate of investment and of human capital and the population growth rate are correlated with its long run growth of output per capita. Thus we contribute to this branch of literature by providing an empirical formulation of the augmented Solow model based on a multivariate-multidimensional specification, that allows to solve the unobserved heterogeneity issue. We address the heterogeneity issues related to: varying parameters across countries, omitted variables and non-linearities in the production function. Indeed, the incorrect specification of the country-specific effects leads to inconsistent parameter estimation, generating omitted variable bias (Caselli et al., 1996).

As a by-product, we provide a posterior classification of countries sharing the same latent structure, highlighting strong heterogeneous behaviours. With respect to the existing approaches, we relax the assumption of the same posterior classification for the gross domestic product (GDP) per capita level and the growth rate. This allows us to let free the posterior classification given the observed variable and the latent effect, and to analyze the uncertainty and the variation in the different economics performance. We are able to distinguish between between group, and within group variations allowing for the human and physical capital and the population growth rate to simultaneously affect the different country growth experience, in terms of growth path and variability in the GDP per capita and growth rate. We further allow for explicitly modelling the scale parameter as a function of covariates. Indeed, we introduce two separates equations for the location and scale parameters of the dependent variables, such that the explanatory variables are associated not only to high or low values of the dependent variable, but also to the unpredictability of the variable itself.

Computational complexity is often the price we have to pay to flexibility. However, we show that parameter estimates can be obtained by extending the Expectation-Maximization (EM) algorithm (Dempster et al., 1977) for finite mixture to the multidimensional case. Furthermore, we avoid any restriction on the covariance structure of the random effects as assumed e.g. by the so-called one-factor model (Winkelmann, 2000), which is more parsimonious but could be hard to justify in empirical applications. By allowing the number of mixture components to grow with the sample size, the proposed model can be also used as a semiparametric estimator of multivariate mixed effects models, where the distribution of the random effects is estimated by a discrete multivariate random variable with a finite number of support points. This can be seen as a possible solution to computational issues arising with multivariate mixed models.

We illustrate the proposal by a simulation study in order to investigate the empirical behaviour of the proposed approach with respect to several factors, such as the number of observed units and times and the distribution of the random term (with varying number of support points). Finally, we test the proposal by analysing a sample taken from the Summers-Heston Penn World Tables (PWT) version 8.0 for years 1975-2005 for non-oil countries. We identify a set of variables that affect the volatility of economic growth and remark the importance of including baseline GDP as a covariate in the model specification. Moreover, different levels of heterogeneity are detected in GDP and GDP growth, respectively. More precisely, we find that our sample is much more heterogeneous with respect to GDP levels than growth patterns. Although this result sounds obvious, previous empirical results, based on unidimensional specification of the latent structure, were not able to distinguish for different heterogeneity levels (see e.g. Alfó et al., 2008). Instead, our approach can easily accommodate for different heterogeneity levels in the univariate profiles and, simultaneously, accounts for association between outcomes. About obtained results, we get two clusters representing high-growth and low-growth countries, and six clusters are identified with respect to GDP levels.

The plan of the paper is as follows. In Section 2, we specify the proposed model in a general form and in Section 3 we provide the computational aspects of the adopted maximum likelihood algorithm. In Section 4, we give a comparison of the performance of several model specifications under different data generation schemes by means of a simulation study. In Section 5, we present an empirical application on real world data motivating this paper. In Section 6, we point out some remarks, along with drawbacks that may arise by adopting the proposed methodology.

2 Statistical framework

We start assuming that the analysed sample is composed of statistical units (e.g. countries): continuous responses , corresponding to outcomes and two vectors of covariates and , which can vary over outcomes, are recorded for each unit () at time (). Following the usual notation for longitudinal multivariate data, let denote the vector of observed responses for unit at the -th time. We assume that are realizations of conditionally independent random variables, with parameters . When we face multivariate analysis, and the primary focus of the analysis is not only to build a regression model, but even to describe association among responses, the univariate approach is no longer sufficient and needs to be extended. In this context, we are likely to face complex phenomena which can be characterized by having a non-trivial correlation structure. For instance, omitted covariates may affect more than one response; hence, modelling the association among the outcomes can be a fundamental aspect of research. Beyond that, the association structure could be of interest by itself, as we may be interested in understanding the nature of the stochastic dependence among the analysed phenomena. Furthermore, it is well known that, when responses are correlated, the univariate approach is less efficient than the multivariate one, since in estimating the parameters in the single equations, the multivariate approach takes into account of zero restrictions on parameters occurring in other equations (for a detailed discussion on this topic see e.g. Zellner, 1962; Davidson and MacKinnon, 1993).

A standard way to insert dependence among responses is to assume that they share some common latent structure. Thus, the model specification is completed by connecting the univariate submodels through a common latent structure, represented by a set of random effects which account for potential heterogeneity among statistical units and correlation between outcomes. In a regression setting, the interest is usually focused upon the mean which is modelled through a linear mixed model, providing a very broad framework for modelling dependence in the data (Verbeke et al., 2014). Nevertheless, statistical models rarely allow the modelling of parameters other than the mean of the response variable as functions of the explanatory variables. For instance, the scale parameter is usually not modelled explicitly in terms of the explanatory variables but implicitly through its dependence on the mean. In the following, we relax such a constrain and define a location-scale multivariate regression framework by specifying conditionally independent (given the covariates and the random effects) regression models. Let us decompose the design vector as , where the variables whose effects are assumed to be fixed are collected in , while those which vary across units are in . The -dimensional parameter vector is related to covariates and random effects. Let us specify as the location parameter, as the scale parameter and as a shape parameter (whenever needed) and let be a known monotonic link function relating to covariates and random effects, we define the following regression models

| (1) |

where represents unit- and outcome-specific random effects, drawn from a multivariate parametric density, , and are outcome- and moment-specific fixed parameters. Of course, covariates may be included in the shape-parameter model, but this may complicate results interpretation in empirical applications.

Given the model assumptions, the likelihood function can be written as follows:

| (2) |

where is a generic probability density function, represents the support for , the distribution function of , with .

Although, at first glance, the approach proposed so far is appealing, it has several computational drawbacks and limitations. Indeed, the random effects distribution is unknown and assuming a multivariate Gaussian distribution may be a too strong and unverifiable assumption and, moreover, may affect parameters estimate. Indeed, in some situations, the distribution of the random effects may depart from normality. This problem has been addressed, for example, by specifying a different parametric distribution family for the random terms, such as multivariate skewed and/or heavy-tailed distributions (Ferreira and Steel, 2006; (Ferreira and Steel, 2004)). An alternative approach is to use nonparametric maximum likelihood based on finite mixtures, which provide a more flexible framework to deal with departure from normality of the random effects distribution (see e.g. Böhning, 1995; Aitkin, 1999). Nevertheless, even if the latter is computationally efficient when compared to parametric random effect models, it is intrinsically unidimensional, since

it is based on a single categorical latent variable. This may lead to problems

when the task is testing for dependence between the random effects. Indeed, the model under independence

does not occur as a special case of the dependence model.

In the following, we consider a -variate -dimensional latent structure such that the independence model is nested in the multivariate one, and different levels of heteorgeneity in the univariate profiles can be identified. In order to specify a latent structure of this kind, we leave the distribution of the random effect completely unspecified and invoke the non-parametric maximum likelihood approach.

Formally, random effects distribution can be approximated through a discrete distribution with support points at the marginal level. Mass joint probability are attached to location for . Focusing on the bivariate () case, without lacking of generality, we define the following location-scale multivariate regression model

| (3) |

According to model assumptions, the likelihood function in the bivariate case is given by

| (4) |

where is the joint probability associated to each couple of locations . The following constraints hold

with

and

We would remark that the number of locations (i.e. mixture components) may vary between outcomes. Thus, we control for heterogeneity in the univariate profiles and for the association between latent effects in the two profiles. This approach results in a finite mixture with components, in which each of the locations are coupled with each of the locations of the second outcome. If , our proposal reduces to a univariate finite mixture model.

3 Computational details

Let be a short-hand notation for all non-redundant models parameters corresponding to the vectors , inference for the proposed model is based on log-transformation of the likelihood in (4).

To estimate , we maximized the log-transformation of (4) by using a version of the EM algorithm (Dempster et al., 1977). The EM algorithm alternates the following steps until convergence

- E-step:

-

compute the conditional expected value of the complete data log-likelihood given the observed data and the current estimate of model parameters; and

- M-step:

-

maximize the preceding expected value with respect to .

Let denote a dummy variable equal to 1 if unit is in component and in the two univariate profiles, respectively, and zero otherwise. The complete data likelihood, which we would compute if we knew these dummy variables, is

| (5) |

And its corresponding log-transformation is

| (6) |

where .

The conditional expected value of at the E-step has then the same expression as given previously in which we substitute the variable with its corresponding expected value

| (7) |

where is the posterior probability the the -th unit belongs jointly to the and components of the mixture. We can easily get the marginal posterior probabilities

| (8) |

At the M-step, the conditional expected value of (6) is maximized by separately maximizing its components. Indeed, the score function is

Let us partition the parameter vector , where collects the parameters of the -th profile such that

| (9) |

| (10) |

and

| (11) |

An explicit solution is available to maximize the last M-step equation, which consists of

To maximize the other two parts, we can use a standard iterative algorithm of Newton-Raphson type for linear mixed models. We take the value of at convergence of the EM algorithm as the maximum likelihood estimate. As it is typical for finite mixture models the likelihood may be multimodal and the point at convergence depends on the starting values for the parameters, which then need to be carefully chosen. In this regard, we run the EM algorithm from multiple random starting points for a number of steps, then pick the one with the highest likelihood, and continue the EM from the picked point until convergence. However, other methods can be used; for example, a gradient function based on directional derivatives can be used to get optimality criteria (see e.g. Wang, 2010).

At last, we approach the model selection problem by looking at penalized likelihood criteria, Akaike information criterion (AIC) and Bayesian information criterion (BIC). In this way we select the number of mixture components and we can also compare the different models. BIC, achieved in the Bayesian framework is found to be satisfactory in the model-based clustering context (see among others Fraley and Raftery, 2002, for further details). Both criteria are likelihood based and they differ for the different penalization used. In fact, denoting with the number of independent parameters to be estimated and with the sample size, BIC is obtained as , and AIC is given by .

4 Simulation study

To assess the properties of the maximum likelihood estimator described in Section 3, we carried out a simulation study, which is described subsequently. The same study allows us to assess the goodness of classification.

4.1 Simulation design

We considered two scenarios: the first with two response variables (both Gaussian-distributed) with mixture components each and the second with higher heterogeneity levels, i.e. by defining a bivariate model with and mixture components for each outcome respectively. Under each scenario, we considered two continuous covariates, one in the linear predictor for the mean and one in the regression model for the scale parameter, and generated 500 samples from the proposed model with (panel length) and (sample size). Under this setting,

Scenario 1. We assume that the outcomes are conditionally independent and proceeded to generate 500 samples from

where the following bivariate regression model (with a single covariate) holds

and

with

Scenario 2. We assume that the outcomes are conditionally independent and proceeded to generate 500 samples from

where the following bivariate regression model (with a single covariate) holds

and

with

4.2 Simulation results

For each sample, we computed the maximum likelihood estimate of the parameters and the corresponding standard errors, under the assumed model. We also evaluate the performance of the proposed in correctly clustering the statistical units into mixture components. The Rand Index (Hubert and Arabie, 1985) is considered. The true matrix of component membership and the crispy estimated matrix , where each element is defines as

are compared. Formally, let denote the number of all pairs of data points which are either put into the same cluster by both partitions or put into different clusters by both partitions. Conversely, let denote the number of all pairs of data points that are put into one cluster in one partition, but into different clusters by the other partition. The partitions disagree for all pairs and agree for all pairs . We can measure the agreement by the Rand index which is invariant with respect to permutations of cluster labels.

For Scenario 1, the simulation results in terms of bias and standard deviation of the maximum likelihood estimator of each parameter of interest are shown in Table 1, together with the Rand Index. We can observe that, the bias of each estimator is always low and decreases as increase; moreover, its standard deviation decreases. Indeed, for and the estimators are unbiased. By increasing the number of available times, the clustering performance improves as well as shown by the Rand Index. For sake of brevity, we do not report the results for . They do not provide any further insight to the already discussed results.

By considering Scenario 2, in which a higher degree of heterogeneity is assumed in one of the two outcomes, we can easily detect a different estimators behavior (see Table 2). Obviously, for small sample size () and , higher bias and standard deviations are estimated with respect to those in Scenario 1. However, estimates variability decreases at the expected rate of with respect to and at a faster rate with respect to . By increasing the sample size to , we get less biased estimates, as expected. Clustering performances are sensitive to and as well. Indeed ,the larger is the sample size the better is the recovered latent structure.

5 Empirical framework

5.1 Data

The sample is composed by an unbalanced panel of 101 countries over the period 1975-2010. Data on the dependent variables and the investment share on physical capital (sk) are retrieved from the Heston-Summers-Aten dataset (Penn World Table 8.0). Data on human capital (sk), measured as the total enrollment in secondary education, is retrieved from the World Bank. From the same database, we also collect: openness to trade (open), measured as the sum of exports and imports as share of GDP, and the credit to the Private Sector as a fraction of GDP (fin), used as a proxy for financial development. In order to understand the effect of financial factor on the growth fluctuations through the household consumption channel, the private sector on GDP is preferred as measure since it does not account for the credit provided from the Central and development bank to the public sector. Government consumption (govcons) is calculated as the general government final consumption expenditure (as share of GDP). Unemployment rate(unempl) and the inflation level (infl) are obtained from the Penn World Table 8.0 dataset.

In order to avoid the endogeneity problems related to growth model estimation, we consider non-overlapping 5-year period with explanatory variable averaged over the corresponding time period; while the dependent variables are taken 5 periods ahead (Bond et al., 2001). Indeed, endogeneity could be due to the fact that “country-specific heterogeneity cannot be captured if one does not look at between-countries variation which cannot be explained by observed covariates but remains persistent over the analysed time period.” (Alfó et al., 2008, pg. 495). Thus, the dependent variables are the average of GDP per capita over the 5-years period (), and the average annual growth of real GDP over the same non overlapping period (). Table 3 provides descriptive statistics, variables description, and data sources.

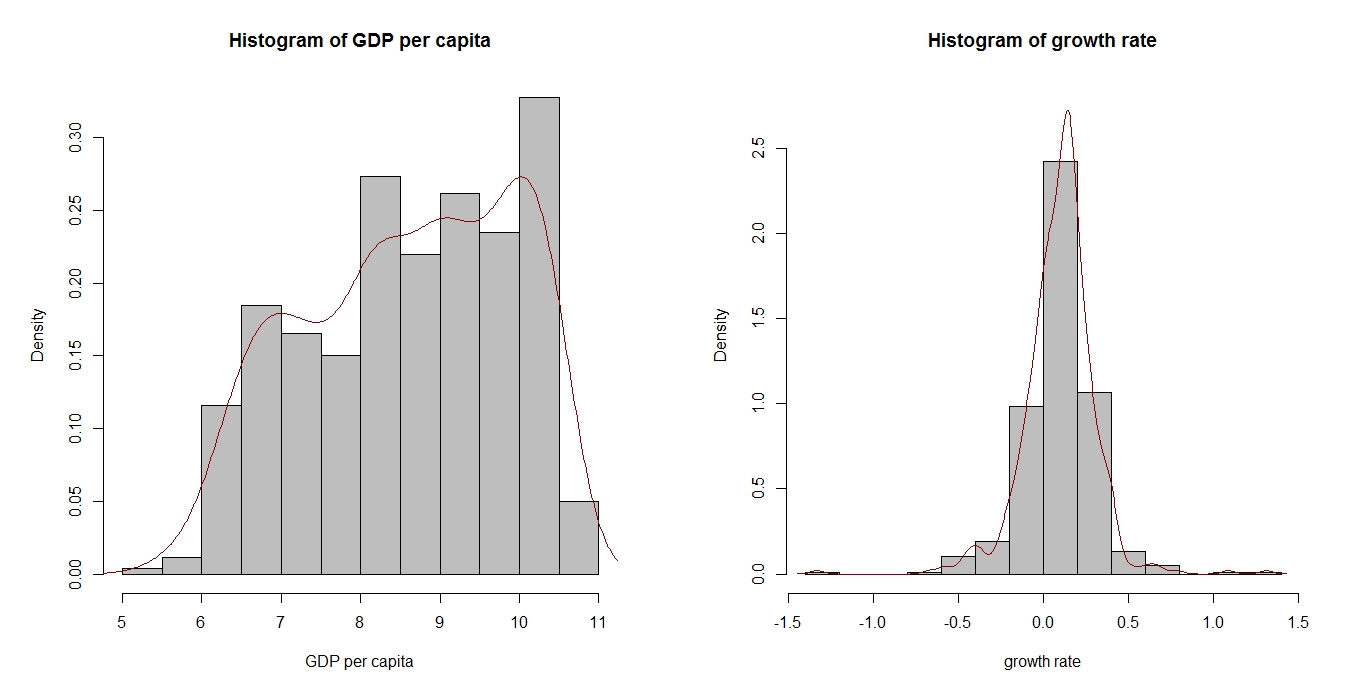

To analyze the marginal distribution of the response variables, graphical and statistical analysis are provided. Figure 1 displays a clear multimodal distribution for the GDP level, supporting the idea of different sub-populations in the outcome. The marginal distribution of growth rates does not show any multimodality, although a small bump can be detected on the left with respect to the distribution mode. However, we cast some doubts that growth rate follows a Gaussian distribution. Thus, to complement the graphical analysis, Shapiro-Wilk and Jarque-Bera tests and summary statistics are provided in Table 4 for the two outcomes. Skewness and kurtosis of each response variable indicate a departure from the normal distribution. Whilst, it is expected that both Shapiro-Wilk and Jarque-Bera tests indicate departure from marginal normality for the GDP level, we obtain a significant departure from normality for the growth rate outcome as well. Thus, we opt for a (mixture of) heavy-tailed distribution to properly model growth rates.

5.2 Economic growth

To understand the cross-country differences in income performances and to account for dependence between per capita income and growth, we introduce a flexible bivariate multidimensional finite mixture approach for the location and the scale parameters, and for the shape parameter when it is required, as described in Section 2. To jointly determine the evolution of income per capita and volatility of growth, instead of modelling the scale parameter through the dependence on the mean, we explicit the variance of the growth rate as dependent on explanatory variables. Thus, growth determinants are associated not only to high or low values of the dependent variable but also to unpredictability of the variable itself.

Formally, for each country at time , let the GDP level () be a Gaussian random variable, i.e. , and the GDP growth rate () be t-distributed to account for heavy tails in the growth distribution, i.e. . To explore the determinants of both growth level and growth volatility, we choose variables found to be robust in the economic growth literature (see e.g. Levine and Renelt, 1992; Mankiw et al., 1992; Cecchetti et al., 2006), and define the following mixed-effects regression model for

| (12) |

where and are the share of output invested in physical and human capital, respectively, is the depreciation rate, is the population growth rate and is the technological progress. As it is common in the growth literature, the term is assumed to be common across countries and equal to 0.5. Parameters in model (12) capture the effect of the human and physical capital accumulation process, and the population growth on the income per capita. They can be explicit as:

| (13) |

where and are respectively the share of physical and human capital, such that . It is worth noting that the and are expected to be positive, while to be negative, since human and physical capital accumulation boost economic growth, while the population growth rate is thought to discourage the evolution of the economy (see among others Solow, 1956; Mankiw et al., 1992; Barro, 1991). The random intercept is let free to vary across countries since it captures the unobserved heterogeneity due to the omission and/or the immeasurable nature of some country-specif factors.

According to Bernanke and Gürkaynak (2002), the definition of the augmented Solow model implies a bivariate growth model, in which the long run growth of output per capita is correlated with the accumulation of human and physical capital and the population growth rate. We adopt a reduced-form model for the location parameter of the growth rate (see Goetz and Hu, 1996for further details) such that

| (14) |

The random coefficient (attached to the initial level of income per capita) controls for the transitional dynamics affecting the evolution of the growth rate. It is worth recalling that the neoclassical approach predict a fixed and negative coefficient for the initial level of income per capita accounting for country convergence.

In our approach, economic stability is directly modelled by including an equation for the variance of the growth rate, that regress the unpredicatability of the response variable on financial development, international openness, government consumption, inflation and unemployment rate (e.g., Cecchetti et al., 2006; Giovanni and Levchenko, 2009). We expect that cyclical variables (unemployment rate and inflation) have a destabilizing effect on growth, i.e. and are expected to be positive, while financial development and government consumption decrease growth volatility. The effect of openness to trade on economic growth is still debated in the literature.

Again, the random terms and in the location parameter’s equation are let free to vary among countries and response variables, by allowing for a random slope as well. This allows us to simultaneously understand the variation across country in the standard of living and in the volatility of the outcome per capita, leaving the posterior classification of the mixture model to be free to vary among outcomes.

5.3 Results

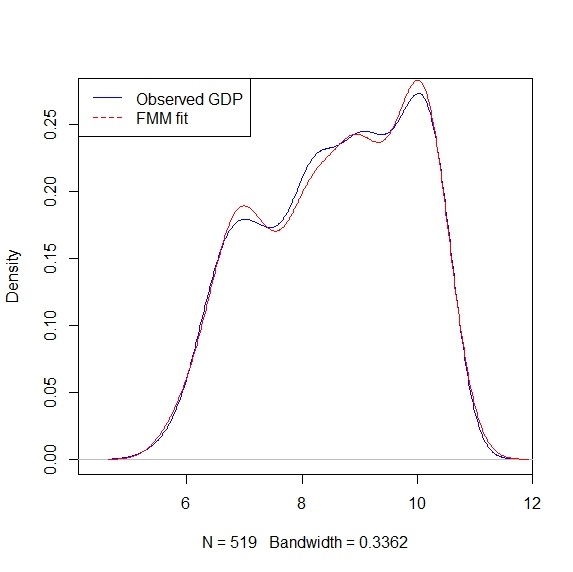

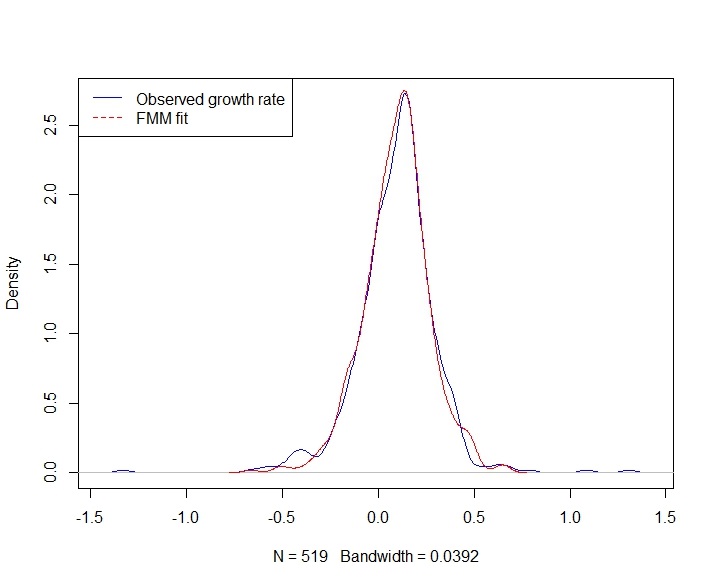

A major research question would concern the need of a complex model like the one we introduce to properly model economic growth. Thus, to remark the crucial role of the bivariate approach with respect to the univariate one, we start our empirical analysis by comparing univariate and multivariate approaches. Firstly, we fit univariate mixed-effects models for each outcome separately, with and . Model selection results are provided in Table 5, and models with and , respectively, are selected. Similarly, we perform model selection for the bivariate model specified in the previous section, with varying and . In the bivariate case the AIC is in favour of the and , while the BIC select the model with and groups (see Table 6). By comparing penalized likelihood criteria, it is clear that linking the two univariate profiles by a shared (correlated) random effects structure, i.e. adopting a bivariate approach, leads to better results in terms of trade-off between model fit and model complexity. In the following we look at the results obtained with the bivariate selects according to the BIC. This choice is motivated by looking at parsimony and for comparison purposes (with respect to univariate model specifications). In Figure2 we provide evidence of the goodness of fit of the proposed model, and of the relatively small increase in goodness of fit the and model selected according to the AIC. The Parameter estimates are provided in Table 7. The main difference between the univariate and the multivariate approaches is on the magnitude of covariates effects in the equation for the mean of GDP level. Indeed, the bivariate approach parameter estimates confirm the augmented Solow model intuition, i.e. the accumulation process of physical and human capital exhibits more reasonable value of the coefficients with respect to univariate case. As discussed before, the intercept term captures the omitted country-specific features, such as, above all, institutional characteristic. This is related to the idea that accumulation driven growth equation is incomplete (see e.g. Alfó et al., 2008), and, coherently with the literature, the highest value for the random effect is found for the component clustering the richest and more industrialized countries, such as USA and UK. However, we will investigate the obtained clustering in depth in Section 5.4.

As formalized before, the location parameter for the growth rate is estimated by applying a reduced-form model where the independent variables is the 5-years backward value of GDP per capita. This allows for avoiding biased estimation in the parameters due to the dependence among physical and human capital on income per capita (Goetz and Hu, 1996). Furthermore, to account for the difference in initial level of GDP per capita, we leave the initial level of GDP to vary among countries. Results show the existence of two groups: the first group characterized by a negative and significant effect of the initial level of GDP on the growth pattern, confirming economics theory about convergence; the second group is characterized by the possible existence of multipla equilibria and the lack of convergence. These results suggest the presence of a convergence club, that is, a group of countries with different levels of per capita real GDP within which countries converge to a group-specific growth path, i.e. the neoclassical prediction of the convergences is proved for those countries. The second component, clustering low income countries, shows lack of income convergence allowing for the potential existence of multipla equilibria, as obtained by Owen et al. (2009). To summarize, accounting for heterogeneity, we can conclude for the existence of two difference of groups in the growth process: one in which countries converge and one in which the positive and significant coefficient associated to the initial level of GDP per capita suggests the lack of convergence and the possible existence of multipla equilibria.

The volatility of growth rate is mainly due to the unemployment rate and to the financial development. This implies that changing in the labor market and in the financial sector are the main causes of the economics, respectively, instability and stability. The high level of financial development is found to be negatively related to the growth variability. This could be due to the direct connection between the financial development and the household consumption. As Aghion et al. (1999), and Easterly et al. (2001) suggest, an increase in the private credit to GDP generates more consumption smoothness, by reducing the household liquidity constraints; in turn, the less consumption volatility (smoothed by the less liquidity constraints) leads to less volatility in growth. Unemployment is found here to play a destabilizing role on output fluctuation. This could be due to the fact that an increase in the unemployment level generates a decrease in consumption. Inflation, openness to trade and government consumption are found to be non significantly different from zero in the bivariate equation for the scale parameters (see Table 7).

An high level of openness to trade is associated to an improvement in the financial and commercial risk sharing with foreign countries (Cecchetti et al., 2006) and to a consequent increase in the vulnerability to the demand and supply shock (Newbery and Stiglitz, 1984). On the other hand, stabilizing effect of the openness to trade could be due to the financial structure of country itself, i.e. the most exposed to capital flows, the most stabilizing effect on growth openness to trade (Cavallo et al., 2008), or to the degree of diversification of exports (Haddad et al., 2013). Furthermore, we obtain that cyclical fluctuations in the growth rate are negatively related to the labour market participation (Okun, 1962) and to the inflation rate.

5.4 Clustering

An interesting by-product of our approach is the possibility to cluster

countries on the basis of their posterior probabilities . The i-th country can be classified in the -th group if . It is worth nothing that each group is characterized by homogeneous values

of (estimated) random effects; thus, conditionally on observed covariates,

countries clustered in the same group share a similar behaviour with respect

to the event of interest (i.e. GDP level and growth). This represents a

substantial difference with conclusion derived by assuming any parametric

approach for the random terms.

Table 8 displays the a posteriori classification. With respect to the GDP level groups, and cluster well-developed countries (with any few exceptions), while the poorest countries are clustered in . It is interesting to notice that high levels of GDP are often associate to higher propensity to grow. Indeed, all countries (but Costa Rica, Mexico, Panama, Turkey and Venezuela) clustered in or are assigned to , i.e. the growth group with the highest propensity to growth, somehow alleviated by the initial GDP level. Similarly, the “poorest countries” share a lower propensity of economic growth with the exception of China and Thailand (as expected).

The obtained classification is, in this case, not only a mathematical tool able to capture the unobserved heterogeneity, but groups may have a “physical” meaning. Indeed, countries in the same cluster often share similar technological, institutional and/or geographical characteristics (e.g. OECD countries are clustered together), and in general a similar socio-economic background.

A final remark concerns the impact of initial GDP level on growth because it it important to check for convergence. Our results suggest two different process. The first one involves developed countries, whose growth is relatively high and in which higher values of GDP contributes to the growth process, thus leading to “convergence”. On the other hand, for “poorest” countries differences will increase as the initial GDP positively affects economic growth leading to divergence.

6 Conclusion

In this paper we introduce a flexible multivariate multidimensional random model allowing for all model parameters to depend on covariates in a regression framework. We relax the common unidimensionality assumption of the random effects distribution, allowing for a general and flexible association structure among the outcomes. The proposed approach is motivated by the analysis of economic growth in presence of heterogeneous behaviour. We jointly model GDP level and growth by further including a regression model for the variance of growth, to check for the effects of financial variables on the volatility of the growth process. Our empirical findings provide evidence of heterogeneous behaviours in both GDP level and growth rate, confirming the need of a flexible approach to properly reflect all data features. Such heterogeneous behaviours could be due to differences in institutional and technological factors and may contribute to reach (or not) economic convergence. At last, we would remark that estimated covariates effects are in line with the augmented Solow model theory, additionally the growth rate volatility is mainly related to unemployment and financial development. Of course, the model can be extended in several ways. Here, we account for heavy tails in the growth rate distribution, but other distributions than the t one can be considered, as well as approaches to deal with outliers (if any). More than two outcomes can be jointly modelled of the price of a high computational burden involved in the estimation step. An interesting extension would deal with time-varying heterogeneity. Indeed, a limitation of our proposal is that we assume time-constant random effects.

References

- (1)

- Aghion et al. (1999) [1] Aghion, P., E. Caroli, and C. Garcia-Penalosa (1999): “Inequality and economic growth: the perspective of the new growth theories”, Journal of Economic literature, pp. 1615–1660.

- Aitkin (1999) [2] Aitkin, M. (1999): “A general maximum likelihood analysis of variance components in generalized linear models”, Biometrics, Vol. 55, No. 1, pp. 117–128.

- Alfó et al. (2008) [3] Alfó, M., G. Trovato, and R. J. Waldmann (2008): “Testing for country heterogeneity in growth models using a finite mixture approach”, Journal of applied Econometrics, Vol. 23, No. 4, pp. 487–514.

- Ardıç (2006) [4] Ardıç, O. P. (2006): “The gap between the rich and the poor: Patterns of heterogeneity in the cross-country data”, Economic Modelling, Vol. 23, No. 3, pp. 538–555.

- Barro (1991) [5] Barro, R. J. (1991): “Economic growth in a cross section of countries”, The Quarterly Journal of Economics, Vol. 106, No. 2, pp. 407–443.

- Baştürk et al. (2012) [6] Baştürk, N., R. Paap, and D. van Dijk (2012): “Structural differences in economic growth: an endogenous clustering approach”, Applied Economics, Vol. 44, No. 1, pp. 119–134.

- Bernanke and Gürkaynak (2002) [7] Bernanke, B. S. and R. S. Gürkaynak (2002): “Is growth exogenous? taking mankiw, romer, and weil seriously”, in NBER Macroeconomics Annual 2001, Volume 16: MIT Press, pp. 11–72.

- Bertarelli and Bernardini Papalia (2013) [8] Bertarelli, S. and R. Bernardini Papalia (2013): “Nonlinearities in economic growth and club convergence”, Empirical Economics, Vol. 44, No. 3.

- Böhning (1995) [9] Böhning, D. (1995): “A review of reliable maximum likelihood algorithms for semiparametric mixture models”, Journal of Statistical Planning and Inference, Vol. 47, No. 1, pp. 5–28.

- Bond et al. (2001) [10] Bond, S. R., A. Hoeffler, and J. Temple (2001): “Gmm estimation of empirical growth models.”.

- Caselli et al. (1996) [11] Caselli, F., G. Esquivel, and F. Lefort (1996): “Reopening the convergence debate: a new look at cross-country growth empirics”, Journal of Economic Growth, Vol. 1, No. 3, pp. 363–389.

- Cavallo et al. (2008) [12] Cavallo, E. A., J. De Gregorio, and N. V. Loayza (2008): “Output volatility and openness to trade: A reassessment [with comments]”, Economia, pp. 105–152.

- Cecchetti et al. (2006) [13] Cecchetti, S. G., A. Flores-Lagunes, and S. Krause (2006): “Assessing the sources of changes in the volatility of real growth”,Technical report, National Bureau of Economic Research.

- Davidson and MacKinnon (1993) [14] Davidson, R. and J. G. MacKinnon (1993): “Estimation and inference in econometrics”, OUP Catalogue.

- Dempster et al. (1977) [15] Dempster, A. P., N. M. Laird, and D. B. Rubin (1977): “Maximum likelihood from incomplete data via the em algorithm”, Journal of the Royal Statistical Society. Series B (Methodological), pp. 1–38.

- Doppelhofer et al. (2000) [16] Doppelhofer, G., R. I. Miller, and X. Sala-i Martin (2000): “Determinants of long-term growth: A bayesian averaging of classical estimates (bace) approach”,Technical report, National bureau of economic research.

- Durlauf and Johnson (1995) [17] Durlauf, S. N. and P. A. Johnson (1995): “Multiple regimes and cross-country growth behaviour”, Journal of Applied Econometrics, Vol. 10, No. 4, pp. 365–384.

- Durlauf and Quah (1999) [18] Durlauf, S. N. and D. T. Quah (1999): “The new empirics of economic growth”, Handbook of macroeconomics, Vol. 1, pp. 235–308.

- Easterly et al. (2001) [19] Easterly, W., R. Islam, and J. E. Stiglitz (2001): “Shaken and stirred: explaining growth volatility”, in Annual World Bank conference on development economics, Vol. 191, p. 211.

- Fernandez et al. (2001) [20] Fernandez, C., E. Ley, and M. F. Steel (2001): “Model uncertainty in cross-country growth regressions”, Journal of applied Econometrics, Vol. 16, No. 5, pp. 563–576.

- Ferreira and Steel (2006) [21] Ferreira, J. T. S. and M. F. Steel (2006): “A constructive representation of univariate skewed distributions”, Journal of the American Statistical Association, Vol. 101, No. 474.

- Ferreira and Steel (2004) [22] Ferreira, J. and M. F. Steel (2004): “Bayesian multivariate regression analysis with a new class of skewed distributions”, Statistics Research Report, Vol. 419.

- Fitzmaurice et al. (2008) [23] Fitzmaurice, G., M. Davidian, G. Verbeke, and G. Molenberghs (2008): Longitudinal data analysis: Boca Raton, FL: Chapman and Hall;.

- Fraley and Raftery (2002) [24] Fraley, C. and A. E. Raftery (2002): “Model-based clustering, discriminant analysis, and density estimation”, Journal of the American Statistical Association, Vol. 97, No. 458, pp. 611–631.

- Giovanni and Levchenko (2009) [25] Giovanni, J. d. and A. A. Levchenko (2009): “Trade openness and volatility”, The Review of Economics and Statistics, Vol. 91, No. 3, pp. 558–585.

- Goetz and Hu (1996) [26] Goetz, S. J. and D. Hu (1996): “Economic growth and human capital accumulation: simultaneity and expanded convergence tests”, Economics Letters, Vol. 51, No. 3, pp. 355–362.

- Haddad et al. (2013) [27] Haddad, M., J. J. Lim, C. Pancaro, and C. Saborowski (2013): “Trade openness reduces growth volatility when countries are well diversified”, Canadian Journal of Economics/Revue canadienne d’économique, Vol. 46, No. 2, pp. 765–790.

- Hubert and Arabie (1985) [28] Hubert, L. and P. Arabie (1985): “Comparing partitions”, Journal of classification, Vol. 2, No. 1, pp. 193–218.

- Islam (1995) [29] Islam, N. (1995): “Growth empirics: a panel data approach”, The Quarterly Journal of Economics, pp. 1127–1170.

- Kerekes (2012) [30] Kerekes, M. (2012): “Growth miracles and failures in a markov switching classification model of growth”, Journal of Development Economics, Vol. 98, No. 2, pp. 167–177.

- Lee et al. (1997) [31] Lee, K., M. H. Pesaran, and R. P. Smith (1997): “Growth and convergence in a multi-country empirical stochastic solow model”, Journal of applied Econometrics, Vol. 12, No. 4, pp. 357–392.

- Levine and Renelt (1992) [32] Levine, R. and D. Renelt (1992): “A sensitivity analysis of cross-country growth regressions”, The American economic review, pp. 942–963.

- Mankiw et al. (1992) [33] Mankiw, N. G., D. Romer, and D. N. Weil (1992): “A contribution to the empirics of economic growth”,Technical report, National Bureau of Economic Research.

- Martínez-Zarzoso and Maruotti (2011) [34] Martínez-Zarzoso, I. and A. Maruotti (2011): “The impact of urbanization on co¡ sub¿ 2¡/sub¿ emissions: Evidence from developing countries”, Ecological Economics, Vol. 70, No. 7, pp. 1344–1353.

- Newbery and Stiglitz (1984) [35] Newbery, D. M. and J. E. Stiglitz (1984): “Pareto inferior trade”, The Review of Economic Studies, Vol. 51, No. 1, pp. 1–12.

- Okun (1962) [36] Okun, A. M. (1962): “The predictive value of surveys of business intentions”, The American Economic Review, pp. 218–225.

- Owen et al. (2009) [37] Owen, A. L., J. Videras, and L. Davis (2009): “Do all countries follow the same growth process?”, Journal of Economic Growth, Vol. 14, No. 4, pp. 265–286.

- Pesaran and Smith (1995) [38] Pesaran, M. H. and R. Smith (1995): “Estimating long-run relationships from dynamic heterogeneous panels”, Journal of econometrics, Vol. 68, No. 1, pp. 79–113.

- Pittau et al. (2010) [39] Pittau, M. G., R. Zelli, and P. A. Johnson (2010): “Mixture models, convergence clubs, and polarization”, Review of Income and Wealth, Vol. 56, No. 1, pp. 102–122.

- Solow (1956) [40] Solow, R. M. (1956): “A contribution to the theory of economic growth”, The quarterly journal of economics, pp. 65–94.

- Temple (1999) [41] Temple, J. (1999): “The new growth evidence”, Journal of economic Literature, pp. 112–156.

- Temple (2000) [42] Temple, J. (2000): “Growth regressions and what the textbooks don’t tell you”, Bulletin of Economic research, Vol. 52, No. 3, pp. 181–205.

- Verbeke et al. (2014) [43] Verbeke, G., S. Fieuws, G. Molenberghs, and M. Davidian (2014): “The analysis of multivariate longitudinal data: A review”, Statistical methods in medical research, Vol. 23, No. 1, pp. 42–59.

- Wang (2010) [44] Wang, Y. (2010): “Maximum likelihood computation for fitting semiparametric mixture models”, Statistics and Computing, Vol. 20, No. 1, pp. 75–86.

- Winkelmann (2000) [45] Winkelmann, R. (2000): “Seemingly unrelated negative binomial regression”, Oxford Bulletin of Economics and Statistics, Vol. 62, No. 4, pp. 553–560.

- Wooldridge (2002) [46] Wooldridge, J. (2002): “Econometric analysis of cross section and panel data. Massachusetts”.

- Zellner (1962) [47] Zellner, A. (1962): “An efficient method of estimating seemingly unrelated regressions and tests for aggregation bias”, Journal of the American statistical Association, Vol. 57, No. 298, pp. 348–368.

| True | Estimate | Bias | Std. dev. | |

|---|---|---|---|---|

| n=100, T=5 | ||||

| -1.00 | -1.020 | -0.020 | 0.265 | |

| 1.00 | 1.012 | 0.012 | 0.265 | |

| 0.50 | 0.505 | 0.005 | 0.111 | |

| 2.00 | 2.012 | 0.012 | 0.306 | |

| -2.00 | -2.005 | -0.005 | 0.243 | |

| 0.50 | 0.494 | -0.006 | 0.149 | |

| 0.50 | 0.489 | -0.011 | 0.072 | |

| 0.75 | 0.760 | 0.010 | 0.120 | |

| 1.00 | 0.991 | -0.009 | 0.068 | |

| 0.25 | 0.253 | 0.003 | 0.122 | |

| 0.40 | 0.420 | 0.020 | 0.048 | |

| 0.10 | 0.090 | -0.010 | 0.049 | |

| 0.20 | 0.196 | -0.004 | 0.047 | |

| 0.30 | 0.294 | -0.006 | 0.063 | |

| Average Rand Index= 0.800 | ||||

| n=100, T=10 | ||||

| -1.00 | -1.006 | -0.006 | 0.139 | |

| 1.00 | 1.000 | 0.000 | 0.142 | |

| 0.50 | 0.500 | 0.000 | 0.078 | |

| 2.00 | 2.017 | 0.017 | 0.171 | |

| -2.00 | -2.004 | -0.004 | 0.134 | |

| 0.50 | 0.495 | -0.005 | 0.098 | |

| 0.50 | 0.502 | 0.002 | 0.049 | |

| 0.75 | 0.741 | -0.009 | 0.086 | |

| 1.00 | 0.993 | -0.007 | 0.046 | |

| 0.25 | 0.257 | 0.007 | 0.078 | |

| 0.40 | 0.407 | 0.007 | 0.052 | |

| 0.10 | 0.096 | -0.004 | 0.034 | |

| 0.20 | 0.196 | -0.004 | 0.045 | |

| 0.30 | 0.300 | 0.000 | 0.041 | |

| Average Rand Index= 0.905 | ||||

| True | Estimate | Bias | Std. dev. | Estimate | Bias | Std. dev. | |

|---|---|---|---|---|---|---|---|

| n=100, T=5 | n=100, T=10 | ||||||

| -1.00 | -1.028 | -0.028 | 0.337 | -1.007 | -0.007 | 0.160 | |

| 1.00 | 1.035 | 0.035 | 0.252 | 1.016 | 0.016 | 0.123 | |

| 0.50 | 0.498 | -0.002 | 0.111 | 0.499 | -0.001 | 0.074 | |

| 2.00 | 2.200 | 0.200 | 0.715 | 2.071 | 0.071 | 0.403 | |

| -2.00 | -2.271 | -0.271 | 0.935 | -2.090 | -0.090 | 0.401 | |

| 0.00 | -0.136 | -0.136 | 0.746 | -0.066 | -0.066 | 0.616 | |

| 0.50 | 0.498 | -0.002 | 0.150 | 0.504 | 0.004 | 0.097 | |

| 0.50 | 0.490 | -0.010 | 0.071 | 0.496 | -0.004 | 0.049 | |

| 0.75 | 0.755 | 0.005 | 0.123 | 0.751 | 0.001 | 0.084 | |

| 1.00 | 0.989 | -0.011 | 0.079 | 0.993 | -0.007 | 0.050 | |

| 0.25 | 0.252 | 0.002 | 0.014 | 0.255 | 0.005 | 0.084 | |

| 0.10 | 0.038 | -0.062 | 0.048 | 0.038 | -0.062 | 0.048 | |

| 0.10 | 0.129 | 0.029 | 0.061 | 0.129 | 0.029 | 0.061 | |

| 0.20 | 0.230 | 0.030 | 0.058 | 0.230 | 0.030 | 0.058 | |

| 0.20 | 0.191 | -0.009 | 0.075 | 0.191 | -0.009 | 0.075 | |

| 0.30 | 0.360 | 0.060 | 0.070 | 0.360 | 0.060 | 0.070 | |

| 0.10 | 0.051 | -0.049 | 0.058 | 0.051 | -0.049 | 0.058 | |

| Average Rand Index= 0.740 | Average Rand Index= 0.841 | ||||||

| True | Estimate | Bias | Std. dev. | Estimate | Bias | Std. dev. | |

| n=1000, T=5 | n=1000, T=10 | ||||||

| -1.00 | -0.999 | 0.001 | 0.097 | -1.000 | 0.000 | 0.050 | |

| 1.00 | 1.000 | 0.000 | 0.073 | 1.002 | 0.002 | 0.039 | |

| 0.50 | 0.501 | 0.001 | 0.033 | 0.501 | 0.001 | 0.025 | |

| 2.00 | 2.054 | 0.054 | 0.215 | 2.005 | 0.005 | 0.100 | |

| -2.00 | -2.039 | -0.039 | 0.358 | -2.005 | -0.005 | 0.084 | |

| 0.00 | -0.016 | -0.016 | 0.542 | -0.002 | -0.002 | 0.185 | |

| 0.50 | 0.500 | 0.000 | 0.047 | 0.499 | -0.001 | 0.031 | |

| 0.50 | 0.500 | 0.000 | 0.022 | 0.500 | 0.000 | 0.015 | |

| 0.75 | 0.749 | -0.001 | 0.037 | 0.751 | 0.001 | 0.026 | |

| 1.00 | 1.000 | 0.000 | 0.021 | 0.999 | -0.001 | 0.015 | |

| 0.25 | 0.249 | -0.001 | 0.038 | 0.250 | 0.000 | 0.026 | |

| 0.10 | 0.072 | -0.028 | 0.038 | 0.086 | -0.014 | 0.014 | |

| 0.10 | 0.129 | 0.029 | 0.032 | 0.111 | 0.011 | 0.015 | |

| 0.20 | 0.213 | 0.013 | 0.032 | 0.203 | 0.003 | 0.021 | |

| 0.20 | 0.198 | -0.002 | 0.041 | 0.199 | -0.001 | 0.021 | |

| 0.30 | 0.299 | -0.001 | 0.054 | 0.299 | -0.001 | 0.023 | |

| 0.10 | 0.090 | -0.010 | 0.040 | 0.101 | 0.001 | 0.026 | |

| Average Rand Index= 0.774 | Average Rand Index= 0.859 | ||||||

| Mean | Std. Dev. | Variable Description | Sources | |

| GDP level | ||||

| sk | 0.002 | 0.001 | share of output invested in physical capital | PWT 8.0 |

| sh | 0.632 | 0.34 | share of output invested in human capital | World Bank |

| 0.067 | 0.012 | population growth rate | PWT 8.0 | |

| lnyc | 8.509 | 1.268 | log of income per capita | PWT 8.0 |

| Growth | ||||

| unemp | 0.612 | 0.077 | unemployment rate | PWT 8.0 |

| infl | 0.519 | 0.312 | log of consumer price | PWT 8.0 |

| open | 66.7 | 38.05 | openness to trade | World Bank |

| govcons | 15.329 | 5.853 | government consumption (as share of GDP) | World Bank |

| fin | 45.656 | 39.801 | domestic credit on GDP | World Bank |

| N | 519 | |||

Notes: (*): 0.05 is the commonly used value for approximating the depreciation growth rate and the technological rate.

| Mean | Std. Dev. | Skewness | Kurtosis | Min | Max | N | |

|---|---|---|---|---|---|---|---|

| GDP level | 8.6 | 1.3 | -0.27 | 1.96 | 5.42 | 10.70 | 519 |

| GDP growth | 0.9 | 0.2 | -0.37 | 10.47 | -1.33 | 1.31 | 519 |

| LLK | AIC | BIC | |

| -360.89 | 735.77 | 754.08 | |

| -312.95 | 643.89 | 667.43 | |

| -277.54 | 577.08 | 605.85 | |

| -265.11 | 556.22 | 590.22 | |

| -248.04 | 526.08 | 565.31 | |

| -258.81 | 551.62 | 596.08 | |

| LLK | AIC | BIC | |

| 172.22 | -322.44 | -293.67 | |

| 172.24 | -316.47 | -279.86 | |

| 173.19 | -312.37 | -267.91 | |

| 173.18 | -306.36 | -254.06 |

| llk | AIC | BIC | ||

|---|---|---|---|---|

| 2 | 2 | -187.32 | 414.64 | 466.94 |

| 2 | 3 | -186.55 | 421.1 | 483.86 |

| 2 | 4 | -185.51 | 427.02 | 500.24 |

| 2 | 5 | -185.57 | 435.14 | 518.82 |

| 2 | 6 | -184.91 | 441.82 | 535.96 |

| 3 | 2 | -147.21 | 340.42 | 400.57 |

| 3 | 3 | -136.14 | 328.28 | 401.50 |

| 3 | 4 | -152.45 | 370.9 | 457.20 |

| 3 | 5 | -141.97 | 359.94 | 459.31 |

| 3 | 6 | -134.52 | 355.04 | 467.49 |

| 4 | 2 | -97.18 | 246.36 | 314.35 |

| 4 | 3 | -96.29 | 256.58 | 340.26 |

| 4 | 4 | -93.43 | 262.86 | 362.23 |

| 4 | 5 | -91.77 | 271.54 | 386.61 |

| 4 | 6 | -85.44 | 270.88 | 401.64 |

| 5 | 2 | -66.97 | 191.94 | 267.78 |

| 5 | 3 | -57.64 | 187.28 | 281.42 |

| 5 | 4 | -55.25 | 196.5 | 308.95 |

| 5 | 5 | -54.27 | 208.54 | 339.30 |

| 5 | 6 | -66.52 | 247.04 | 396.10 |

| 6 | 2 | -50.42 | 164.84 | 248.52 |

| 6 | 3 | -39.72 | 159.44 | 264.04 |

| 6 | 4 | -36.47 | 168.94 | 294.47 |

| 6 | 5 | -61.48 | 234.96 | 381.41 |

| 6 | 6 | -35.29 | 198.58 | 365.95 |

| Univariate | Bivariate | ||||||

| Coef. | SE | Coef | SE | ||||

| Income per capita: | |||||||

| sk | 0.07 ** | 0.03 | 0.14 *** | 0.03 | |||

| sh | 0.72 *** | 0.02 | 0.46 *** | 0.03 | |||

| -0.33 *** | 0.10 | -0.61 *** | 0.1 | ||||

| 8.46 *** | 0.32 | 9.64 *** | 0.31 | ||||

| 9.02 *** | 0.06 | 7.48 *** | 0.31 | ||||

| 9.59 *** | 0.06 | 8.07 *** | 0.3 | ||||

| 10.19 *** | 0.06 | 6.97 *** | 0.31 | ||||

| 10.84 *** | 0.06 | 8.59 *** | 0.3 | ||||

| 11.29 *** | 0.09 | 9.01 *** | 0.3 | ||||

| -1.23 *** | 0.03 | -1.28 *** | 0.03 | ||||

| Observations | 519 | 519 | |||||

| 6 | 6 | ||||||

| -248.81 | |||||||

| -50.42 | |||||||

| Growth rate: | |||||||

| -0.01 | 0.05 | 1.05 *** | 0.12 | ||||

| 1.11 *** | 0.15 | -0.1 | 0.09 | ||||

| 0.01 ** | 0.01 | -0.09 *** | 0.12 | ||||

| -0.1 *** | 0.02 | 0.02 ** | 0.01 | ||||

| -1.53 *** | 0.52 | -1.52 *** | 0.51 | ||||

| unemp | 1.17 ** | 0.55 | 1.34 ** | 0.53 | |||

| infl | 0.01 | 0.08 | 0.03 | 0.08 | |||

| open | 0.05 | 0.08 | 0.05 | 0.08 | |||

| govcons | -0.11 | 0.11 | -0.15 | 0.11 | |||

| fin | -0.31 *** | 0.05 | -0.31 *** | 0.05 | |||

| 1.72 *** | 0.17 | 1.69 *** | 2.23 | ||||

| Observations | 519 | 519 | |||||

| 2 | 2 | ||||||

| 172.22 | |||||||

| -50.42 | |||||||

Significance level: : 0.1% : 1% : 5%

Notes: : log-likelihood for the univariate model, : log-likelihood for the bivariate model. Dependent variables: 5 years forward value of log of GDP per capita (top of the Table), and 5 years forward value of growth rate.

| 1 | Australia, Austria, Belgium, | |

|---|---|---|

| Canada, Czech Rep., Denmark, | ||

| Finland, France, Germany, | ||

| Hong Kong, Ireland, Israel, | ||

| Italy, Japan, Netherlands, | ||

| New Zealand, Norway, Spain, | ||

| Sweden, Switzerland, Trinidad & Tobago, UK, USA | ||

| 2 | Bangladesh, Benin, Burkina Faso, | |

| Burundi, Rep. Congo, India, | ||

| Kenya, Madagascar, Mali, | ||

| Moldova, Niger, Rwanda, | ||

| Sri Lanka, Syria, Tanzania, Uganda | ||

| 3 | China | Bolivia, Cameroon, Chad, |

| Djibouti, Egypt, Honduras, | ||

| Indonesia, Jamaica, Jordan, | ||

| Mauritania, Morocco, Pakistan, | ||

| Paraguay, Peru, Phillippines, | ||

| Senegal, Sierra Leone | ||

| 4 | Rep. Central African, Rep. Dem. Congo, | |

| El Salvador, Malawi, Mozambique, | ||

| Nepal, Nigeria, Togo | ||

| 5 | Thailand | Bulgaria, Colombia, Dominican Rep., |

| Ecuador, Guatemala, Serbia, | ||

| South Africa, Tunisia, Uruguay,Zimbabwe | ||

| 6 | Angola, Argentina, Botswana, | Costa Rica, Mexico, Panama, Turkey, Venezuela |

| Chile, Croatia, Estonia, Greece, | ||

| Hungary, Rep. of Korea, Latvia, | ||

| Malaysia, Maldives, Mauritius, | ||

| Poland, Poland, Portugal, | ||

| Romania, Russia, Slovakia | ||