Malliavin-Stein method for

Variance-Gamma approximation on Wiener space

Abstract

We combine Malliavin calculus with Stein’s method to derive bounds for the Variance-Gamma approximation of functionals of isonormal Gaussian processes, in particular of random variables living inside a fixed Wiener chaos induced by such a process. The bounds are presented in terms of Malliavin operators and norms of contractions. We show that a sequence of distributions of random variables in the second Wiener chaos converges to a Variance-Gamma distribution if and only if their moments of order two to six converge to that of a Variance-Gamma distributed random variable (six moment theorem). Moreover, simplified versions for Laplace or symmetrized Gamma distributions are presented. Also multivariate extensions and a universality result for homogeneous sums are considered.

Keywords. Contractions, cumulants, Gaussian processes, Laplace distribution, Malliavin calculus, non-central limit theorem, rates of convergence, Stein’s method, universality, Variance-Gamma distribution, Wiener chaos

MSC. Primary 60F05, 60G15; Secondary 60H05, 60H07.

1 Introduction

Let be an isonormal Gaussian process, defined on a probability space , over some real separable Hilbert space , fix an integer and let be a sequence of random variables belonging to the th Wiener chaos induced by (precise definitions follow in Section 2 below). Denote by and the th tensor product and the th symmetric tensor product of , respectively, and let be the isometry between (equipped with the modified norm ) and the th Wiener chaos of . If in particular is an -space of some -finite measure space without atoms, then a random variable with has the form of a multiple Wiener-Itô integral of order .

In recent years, many efforts have been made to characterize those sequences belonging to a Wiener chaos of fixed order, which verify a central limit theorem in the sense that converges in distribution, as , to a centered Gaussian random variable of unit variance (compare with the book [14] for an overview). The celebrated fourth moment theorem of Nualart and Peccati [21] asserts that if for all , then, as , converges in distribution to if and only if converges to , the fourth moment of the Gaussian random variable . This can be seen as a drastical simplification of the classical method of moments, which ensures convergence in distribution of to , provided that all moments of converge to that of .

Only a few years later, Nourdin and Peccati [12] combined Stein’s method for normal approximation with the Malliavin calculus on the Wiener space of variations to prove explicit bounds on the total variation distance , where the supremum runs over all bounded Borel sets (in fact, also other notions of distances have been considered in [12], but we restrict here to the total variation distance). They showed that for a sequence of random variables of the form with it holds that

| (1.1) |

where, for integers , we write for the th cumulant (semi-invariant) of a random variable . More recently, in [15], exact rates of convergence for the total variation distance have been found. Namely, if converges in distribution to , as , then there exist two constants (possibly depending on and on , but not on ), such that

| (1.2) |

for all , where, recall, and are the third and the fourth cumulant of , respectively. In other words this means that the rate provided by (1.1) is suboptimal by a squareroot factor. This, however, seems unavoidable using the Malliavin-Stein technique for normal approximation, which is based on the analysis of fourth moments, while the proof of (1.2) uses more refined arguments.

The main goal of this paper is to study non-central limit theorems (i.e., limit theorems with a non-Gaussian limiting distribution) for sequences belonging to a fixed Wiener chaos of order , as above. A first step in this direction is the paper [11] by Nourdin and Peccati, in which conditions on the sequence have been derived, under which convergence towards a centred Gamma distribution takes place. Moreover, in [12] rates of convergences for such Gamma approximations were considered, again by applying Stein’s method. It is an interesting fact that if is an odd integer, there is no sequence of chaotic random variables with bounded variances converging in distribution to a centred Gamma distribution. This is a consequence of the fact that a random variable with with being odd has third moment equal to zero, while the third moment of a centred Gamma distribution is strictly positive. Beyond the normal and Gamma approximation results in [12], up to our best knowledge there are no other quantitative limit theorems for chaotic sequences so far. Our paper is an attempt to fill this gap in case of the broad class of so-called Variance-Gamma distributions. This is a -parametric family of continuous probability distributions on the real line defined as variance-mean mixtures of Gaussian random variables with a Gamma mixing distribution. We emphasize that Variance-Gamma distributions are widely used in financal mathematics, for example. Particular examples of Variance-Gamma distributions are the Laplace distribution or more general symmetrized Gamma distributions, but also the classical normal or Gamma distribution, which show up as limiting cases. It is interesting to see that in our set-up, no parity condition on is necessary in general. It is also worth mentioning the recent work [9] of Kusuoka and Tudor, where it has been shown that within the so-called Pearson-family of probability distributions on the real line, only the normal and the Gamma distribution can appear as limit laws for a sequence of chaotic random variables. The Laplace distribution, the symmetrized Gamma distribution and, more generally, the Variance-Gamma distributions, are not members of the Pearson-family and this way our study goes beyond the theory developed in [9].

Besides the goal of identifying new limiting distributions for the sequence as considered above, another source of motivation for our paper comes from the area of free probability. In [6], Deya and Nourdin studied the convergence of a sequence of multiple stochastic integrals with respect to a free Brownian motion to what they call the tetilla law, which can be regarded as the commutator of the well-known Marchenko-Pastur distribution. Our aim here is to identitfy the non-free analogue of this distribution and to prove a related limit theorem for multiple stochastic integrals with respect to the classical Brownian motion. We will see that the Laplace distribution with parameter , which, as already mentioned above, is contained in the class of Variance-Gamma distributions, can be seen as such an analogue, see Remark 5.4 below for a more detailed description.

Let us describe our results and the structure of our paper in some more detail. In Section 2 we collect some background material related to isonormal Gaussian processes and the Malliavin calculus of variations on the Wiener space. We will recall in particular the definitions of the so-called -operators, which are central for our further investigations. Essential elements of Stein’s method for Variance-Gamma distributions are reviewed in Section 3. In particular, we state bounds on the solution of the Stein equation and introduce some particular subclasses and limiting cases of Variance-Gamma distributions, which are of special interest. An abstract bound for the Wasserstein distance between a (suitably regular) functional of an isonormal Gaussian process and a Variance-Gamma distributed random variable in the spirit of the Malliavin-Stein method is derived in Section 4. We will see that the bound is expressed in terms of the -operators mentioned above. This general bound is specialized in Section 5.1 to the case of elements living inside a fixed Wiener chaos of order . We derive a sufficient analytic criterium in terms of contractions for such a sequence to converge in distribution to a Variance-Gamma distributed random variable. In this context, we also recover the fourth moment theorem discussed above together with a rate of convergence for the Wasserstein distance, which improves (1.1), but is still not optimal in view of (1.2). Our general bound is specialized in Section 5.2 to the case , which is of particular interest in view of the theory of quadratic forms, for example. We show that in this case the previously derived sufficient criterium for convergence turns out to be necessary and, moreover, equivalent to a simple moment condition involving moments of up to order six only. For example, we show that a sequence of elements belonging to a second Wiener chaos converges in distribution to a random variable having a Laplace distribution with parameter if and only if

| (1.3) |

as . This this case, we also have the bound

| (1.4) |

on the Wasserstein distance, where, recall, stands for the th cumulant of and where are constants only depending on the parameter . We like to emphasize the following interesting observation. Namely, although the third cumulant shows up in the bound (1.4), it automatically vanishes in the limit, as , under the moment condition (1.3). Our result can be seen as a six moment theorem for the convergence to a Laplace distribution on the second Wiener chaos. An analogue for general Variance-Gamma distributions is one of the main achievements of this paper. We mention that this is also closely connected to the work [17] (see also the erratum [18]) of Nourdin and Poly, who characterize convergence of a sequences of random elements inside the second Wiener chaos associated with the ordinary (and the free) Brownian motion in terms of conditions on a sequence of consequtive moments. However, their results do not allow to derive rates of convergence. In the final Section 5.3 we deal with a universality question for so-called homogeneous sums with respect to Variance-Gamma convergence as well as with some multivariate extensions of the previously derived results.

The results of our paper complement those obtained in the recent study of Azmoodeh, Peccati and Poly [2], which has independently been conducted in parallel with our paper. They derive necessary and sufficient conditions under which a sequence as above converges to a limiting random variable, whose distribution is a finite linear combination of centred -distributions. However, these limit theorems are not quantitative in the sense that they just state the convergence in distribution without giving upper bounds on the rate of convergence. On the other hand, the results are for sequences living inside a Wiener chaos of arbitrary order.

2 Elements of Gaussian analysis and Malliavin calculus

Isonormal Gaussian processes.

Here we collect the essentials of Gaussian analysis and Malliavin calculus that are used in the paper, see the books [20] and [14] for further details.

For a real separable Hilbert space and , we write and to indicate, respectively, the th tensor power and the th symmetric tensor power of with convention . We denote by an isonormal Gaussian process over , i.e., is a centred Gaussian family, defined on some probability space and indexed by , with a covariance structure given by the relation . We assume that . For , the symbol denotes the th Wiener chaos of , defined as the closed linear subspace of , which is generated by the family , where is the th Hermite polynomial. For any the mapping can be extended to a linear isometry between and the th Wiener chaos . For we write , . When with being a non-atomic -finite measure on the measurable space , for every the random variable coincides with the -fold multiple Wiener-Itô-integral of with respect to the centred Gaussian measure canonically generated by , see [20, Section 1.1.2]. Here, stands for the subspace of composed by symmetric functions. It is well-known that can be decomposed into the infinite orthogonal sum of the spaces . Hence an admits the Wiener-Itô chaotic expansion

| (2.1) |

with , and the , uniquely determined by .

Let be a complete orthonormal system in . For and , for every , the contraction of and of order is the element of defined by

It is important to notice that the definition of does not depend on the particular choice of , and that is not necessarily symmetric. We denote its canonical symmetrization by . Clearly, and . Moreover, when and , the contraction is the element of given by

We will intensively use the isometry property and the product formula for multiple integrals, i.e. elements of a fixed Wiener chaos. Namely, if and , and , then

| (2.2) |

and

| (2.3) |

see [20, Proposition 1.1.3].

Malliavin operators.

Let be an isonormal Gaussian process and let be the set of random variables of the form with , and an infinitely differentiable function whose partial derivatives have polynomial growth. The Malliavin derivative of with respect to is the element of defined as

Hence for . By iteration, the th derivative is an element of for every . For and , denotes the closure of with respect to the norm

We use the notation . Every finite linear combination of multiple Wiener-Itô integrals is an element of and its law admits a density with respect to the Lebesgue measure on the real line. The Malliavin derivative satisfies the following chain rule. If is continuously differentiable with bounded partial derivatives and if is a vector of elements of , then and

| (2.4) |

If with -finite and non-atomic, then the derivative of as in (2.1) is given by

| (2.5) |

where stands for the function with one of its arguments fixed to be . The adjoint of the operator is denoted by and called the divergence operator. A random element belongs to the domain of (), if and only if it verifies for any , where is a constant depending only on . For the random variable is defined by the integration-by parts formula

| (2.6) |

which holds for every . The infinitesimal generator of the Ornstein-Uhlenbeck semi-group is given by , where for every as in (2.1). The domain of is . A random variable belongs to if and only if (i.e., and ) and in this case,

| (2.7) |

For any we define . The operator is called the pseudo-inverse of . For any one has that , and

| (2.8) |

The following result is used frequently throughout this paper (see [3, Lemma 2.3] and [11, Lemma 2.1]).

Lemma 2.1.

(1) Suppose that and . Then, and

(2) Suppose that with and . Then for every , we have

Cumulants and -operators.

Let be a real-valued random variable such that for some integer and define , , to be the characteristic function of . Then, for , the th cumulant of , denoted by , is given by

There is a well-known relation between cumulants and moments. In this paper, such a relation is needed for cumulants and moments up to order six, and only if . In this case, we have , , and .

The cumulants can be characterized in terms of Malliavin operators. For this, we need to introduce the so-called -operators , . For we define and, for very ,

| (2.9) |

Each is well-defined and an element of , since is assumed to be in , see [13, Lemma 4.2]. According to [13, Theorem 4.3], there is an explicit relation between and the th cumulant of . Namely, if , then has finite moments of all orders and for each integer it holds that

| (2.10) |

The relation continuous to hold under weaker assumptions on the regularity of , see [13, Theorem 4.3]. For , it follows that and and for , it holds that .

If belongs to a fixed Wiener chaos (i.e, if has the form of a multiple integral if as discussed above), there is a more explicit representation for , see Formula (5.25) in [13]. To state it, let and with . Then for any , applyling the product formula (2.3), we have

where the constants are recursively defined as follows:

and for ,

3 Elements of Stein’s method

Wasserstein distance and the standard normal distribution.

Stein’s method is a set of techniques allowing to evaluate distances between probability measures. In the present paper, we focus on the Wasserstein distance (-distance). For any two real-valued random variables and it is defined as

with (Lipschitz functions). We will make use of the fact that the elements in are exactly those absolutely continuous functions whose derivatives are a.e. bounded by in absolute value. We notice that as for a sequence of random variables implies convergence of to in distribution (the converse is not necessarily true).

A standard Gaussian random variable is characterized by the fact that for every absolutely continuous function for which it holds that

| (3.1) |

This together with the definition of the Wasserstein distance is the motivation to study the Stein equation

| (3.2) |

A solution of the Stein equation is a function , depending on , which satisfies (3.2). For , is bounded and twice differentiable such that and , see [5, Lemma 2.3]. If we replace by a random variable and take expectations in the Stein equation (3.2), we infer that

and hence

With (3.1), we obtain that for every such that we have for smooth functions that . It is a particular case of the consequence of Lemma 2.1(1), that for every with mean zero, . Hence, by Cauchy-Schwarz, we obtain

(see [12, Theorem 3.1]).

Symmetric Gamma distributions.

The main goal of our paper is to consider probabilistic approximations by Variance-Gamma random variables. To motivate the right choice of a Stein equation, first let us consider the case of Laplace distribution or, more generally, symmetrized Gamma distribution. The Lebesgue-density of a Laplace distribution with parameter is given by

| (3.3) |

while the Lebesgue-density of a symmetrized Gamma distribution with parameters and equals

| (3.4) |

In what follows we shall indicate the distribution with density by and by we denote the non-symmetric (i.e., classical) Gamma distribution. Note that the choice and leads to the Laplace distribution with density as at (3.3). A first-order Stein operator for a random variable with density can be obtained by the so-called density approach, see [27]. In fact, if has Lebesgue-density , then for all absolutely continuous for which the expectation exists. However, and it is in general technically highly sophisticated or even impossible to compute . To overcome this difficulty, we put, if is absolutely continuous, , to see that

Summarizing, we obtain that if has a Laplace distribution with parameter , and are absolutely continuous functions and exists, that

| (3.5) |

see [25, Lemma 1]. A major disadvantage of this characterization is that the machinery of Malliavin calculus usually enters by . Hence, we substitute by and obtain if is Laplace distributed with parameter . It is interesting to see that this leads to the same Stein characterization of a Laplace distribution (and similarly of a - distribution) as introduced recently in [8] from an entirely different perspective. We emphasize that second-order Stein operators are not commonly used in the literature, although in [24] the authors obtained a second-order Stein operator for the so-called Kummert- density.

Lemma 3.1.

Let be a real valued random variable. Then is distributed according to the symmetrized Gamma distribution (3.4) with parameters and if and only if, for all such that is piecewise twice continuously differentiable and , and are finite, we have

| (3.6) |

Lemma 3.1 suggests the following Stein equation for the -distribution:

| (3.7) |

where denotes the quantity with a random variable distributed according to . The following lemma collects bounds on the solution of (3.7) and its first and second derivative, see [8, Theorem 3.6] for a proof. In what follows, we denote by the th derivative of a function .

Lemma 3.2.

Suppose that , and and , then the solution of the Stein equation (3.7) and its derivatives up to order two satisfy

where , , and .

The Stein-type characterization (3.6) for the -distribution also allows a neat computation of its moments or cumulants. We state the result here only for the moments and cumulants of order , and as they will play a major role later in this paper.

Lemma 3.3.

Let be distributed according to . Then all odd moments and cumulants of are identically zero,

and

Proof.

Variance-Gamma distributions.

A random variable is said to have a Variance-Gamma distribution with parameters , , and if and only if its Lebesgue-density , , equals

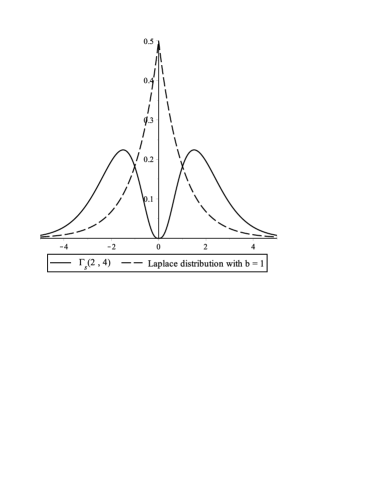

Here, denotes a modified Bessel function of the second kind (see [8, Appendix B] and references there). In what follows we write for such a Variance-Gamma distribution. It is known that and . We will mostly consider only the centred case and write for . Note that the symmetrized Gamma distribution considered in the previous paragraph corresponds to . Variance-Gamma distributions are widely used in finance modelling and contain as special or limiting cases the normal, Gamma or Laplace distribution. In particular, for certain parameter values, the Variance-Gamma distribution has semi-heavy tails that decay slower than those of the normal distribution, see [7, 8].

The parameter is known to be the scale parameter. As increases, the distribution becomes more rounded around its peak value. The parameter is called the tail parameter. As decreases, the tails drop off more steeply. Finally, the parameter is the asymmetry-parameter, for non-zero the distribution becomes skewed, that is, asymmetric, see Figure 1. In [8] a Stein equation for the -distribution was established. From this, the Stein equation for the distribution follows:

| (3.8) |

where stands for the integral over of with respect to the distribution. The next lemma presents bounds for the solution of (3.8) and its first and second derivative. It is interesting to note that in contrast to the case , uniform bounds are much harder to obtain if . In a first step these bounds can be expressed in terms of expressions involving modified Bessel functions, see Lemma 3.17 in [7]. The following lemma follows from this representation.

Lemma 3.4.

Suppose that , and , , , then the solution of the Stein equation (3.8) and its derivatives up to order two are bounded, that is, there exists a constant such that

| (3.9) |

Remark 3.5.

In contrast to the symmetric case discussed above, if , it seems rather difficult to express the constant appearing in Lemma 3.4 explicitly in terms of the parameters and .

With the same proof as for Lemma 3.3 we can compute the first six moments or cumulants of a centred Variance-Gamma random variable, which will be needed later.

Lemma 3.6.

If is distributed according to , we obtain

Moreover, the first six cumulants of are and

Let us collect some distributions, which are of particular interest and belong to the class of Variance-Gamma distributions, see [8, Proposition 1.2]:

-

•

A -distributed random variable has the symmetrized Gamma distribution, in particular corresponds to a Laplace distribution with parameter .

-

•

Suppose that has the bivariate normal distribution with correlation and marginals and . Then the product follows the -distribution.

-

•

Suppose that has the bivariate gamma distribution with correlation and marginals and . Then the random variable follows the -distribution.

4 A Malliavin-Stein bound for the Wasserstein distance

Our first result provides explicit bounds for the -approximation of general functionals of an isonormal Gaussian process . Recall the definition of the -operators given in (2.9).

Theorem 4.1.

Let be such that and let be -distributed random variable. Then there exist constants and such that

| (4.1) |

If in addition , then is square-integrable and

| (4.2) |

Proof.

Let be a twice differentiable function with bounded second derivative. Let and put . Then by our assumptions , using the chain rule (2.4) and . Hence, by Lemma 2.1 (1) we have that

Similarly, let now and , then by our assumptions , using the chain rule (2.4), and , which again by Lemma 2.1 (1) leads to

Next we will apply Lemma 2.1 (1) with and . Again with (2.4), we have that and that is square-integrable using (for a detailed argument see [14, Proof of Proposition 5.1.1]). Since , we have (see [13, Lemma 4.2]), whence

| (4.3) |

Summarizing, we arrive at the identity

and relation (4.1) can be deduced from the bounds in Lemma 3.2. Relation (4.2) is a consequence of [13, Lemma 4.2(2)]. Namely, with one has . ∎

Remark 4.2.

For a -distributed random variable we know from Lemma 3.6 that . Since , the second term in our bound (4.1) measures the distance between the variances of and . The interpretation of the -distance of and the -term on the right-hand side of (4.2) is not obvious and will be discussed for being in the th Wiener chaos in Section 5 below.

We will now derive two consequences from Theorem 4.1. The first one deals with two special Variance-Gamma distributions, the symmetric Gamma distribution and the distribution of of two random variables and having a - and -distribution, respectively.

Corollary 4.3.

Let be such that .

-

(a)

Let be a -distributed random variable for some . Then

with constants only depending on and .

-

(b)

Fix and let denote a real-valued random variable with a -distribution. Then

with constants depending only on and .

Our next result deals with two limiting cases of Variance-Gamma distributions, namely the normal and the (non-symmetrized) Gamma distribution. As discussed in the introduction, this has previously been considered in [12]. More precisely, Theorems 3.1 and 3.11 there show that if is a centred functional of an isonormal Gaussian process and if for some and for some that

with a constant only depending on and . In our context, we can derive another bound for and in terms of the Gamma-operator . We will see below that in the case of multiple stochastic integrals this is closely related to some of the results recently derived in [1].

Corollary 4.4.

Let be such that .

-

(a)

Let denote a centred Gaussian random variable with variance . Then there exist constants only depending on such that

(4.4) -

(b)

Let be a -distributed random variable with parameters and . Then there exist constants depending only on and such that

(4.5)

Proof.

Remark 4.5.

In case (a) of Corollary 4.4 one is able to get the same bound (with different constants) for the Kolmogorov-distance, see [14, Theorem 5.1.3]. It is interesting to compare our bound in (4.4) with (5.1.3) and (5.1.5) in [14]. While we have to consider , the estimate in [14] reads . As explained earlier, this comes from the fact that we consider the much larger class of Variance-Gamma distributions based on a second order-differential equation. This also implies that the stronger condition is needed.

5 Explicit bounds on a fixed Wiener chaos

5.1 The general case

Fix and consider , , a sequence of random variables belonging to the th chaos of an isonormal Gaussian process and assume that with , and . The sequence converges in distribution to , if and only if for every , , as , or equivalently if for every , as . This follows from the classical method of moments or cumulants, since the law is determined by its moments (compare with Proposition 5.2.2 in [14]).

One of our main result is, that the method of moments and cumulants for -approximation boils down to a sixth-moment method inside the second Wiener chaos, see Section 5.2. For general the next result provides an expression for the first term of the bound in Theorem 4.1 in terms of contraction operators. Note that if is an odd integer and , then there is no sequence , such that has bounded variances and such that converges in distribution to a random variable with a -distribution, as . This is a consequence of the fact that an element of a Wiener chaos of odd order has its third moment equal zero, while whenever .

Theorem 5.1.

Let be an even integer and let , where . Then we have

In case the last two sums are empty and have to be interpreted as .

Proof.

We start with the observation that (2) for leads to

Next, we rewrite . For this, let be even and put and , the set of those integers for which the so-called double contraction is well-defined. Then,

| (5.1) |

For , with , we know that . Combining this with [14, Equation (5.2.2)] and the notation introduced around (2) we find that

| (5.2) | |||||

Due to the multiplication formulae (2.3) one obtains that, for even , we have

| (5.3) |

According to (4.2) in Theorem 4.1, we have to compute

| (5.4) |

for , and . At first, we collect the constant terms. In (5.1), we obtain for that and therefore the constant term is . With the definition of in (2) and (5.3) we obtain . Hence, the constant in (5.4) equals

| (5.5) |

using . Next, we consider the so called middle-contractions in and , i.e., contractions of order . With in (5.2) we obtain the term and with in (5.1) we get and hence the term . Summarizing, the middle-contraction in (5.4) contributes

| (5.6) |

The remaining terms in (5.4) can be represented as follows:

| (5.7) | |||||

With (5.5), (5.6) and (5.7) we obtain that (5.4) is equal to

Using the isometric property (2.2) of multiple Wiener integrals we can now conclude the result. ∎

Let us have a closer look at the first summand appearing in the expression provided by Theorem 5.1. Using Lemma 3.6 we see that the moment assumption that and converge to and , respectively, ensures that converges to zero, as . Note moreover that the other contraction operators do not depend on . The dependence on is completely encoded in the moment assumption that and .

Next we consider the particularly attractive case separately corresponding to the symmerized Gamma distributions separately. As explained earlier, in this case no restriction on the parity of is necessary.

Theorem 5.2.

Let be an integer and let with . Then for being even we have

whereas for being odd we set and obtain

Proof.

For being even the result follows directly form Theorem 5.1. The case when is odd is similar. Here, we put and denote by the set of those integers for which the double contraction is well defined. We skip the details. ∎

Remark 5.3.

The symmetric Gamma distribution can be presented as a finite linear combination of independent chi-squared random variables. In [2, Theorem 3.2] the authors investigated necessary and sufficient conditions for convergence in distribution towards such a combination within the framework of random objects living on a fixed chaos. In the examples in [2, Section 4], the conditions are presented in terms of contractions.

Remark 5.4.

Comparing the contraction conditions implied by Theorems 4.1 and 5.2 for the symmetric Gamma distribution with those of Theorem 1.1 (ii) in [6] for the tetilla law arising in free probability we see that our condition in the case of coincides almost readily with that in [6]. The only difference are the coefficients , which arise as a consequence of the product formula (2.3). In contrast, these coefficients are all equal to in the free set-up (compare with Equation (2.6) in [6], for example). This way, we may identify the Laplace distribution with parameter as the non-free analogue of the tetilla law.

A particularly interesting question is whether the bounds derived in Theorems 5.1 and 5.2 are tight with respect to the convergence in distribution towards a Variance-Gamma distribution, in the sense that these bounds converge to zero if and only if a normalised sequence , living inside a fixed Wiener chaos, converges in distribution to a -distributed random variable. Fix , and consider a sequence such that , , where and suppose that . Moreover, by denote a random variable with -distribution. We conjecture that for the symmetric Variance-Gamma distributions (corresponding to ) (i) the convergence in distribution of to is equivalent to (ii) and , which in turn is equivalent to the contraction conditions (iii) that

where and is such that and . Our conjecture for reads similar. Namely, we conjecture that a sequence such that , , where and (i) converges in distribution to a -distributed random variable if and only if (ii) the moment condition is satisfied for or if and only if (iii) the contraction conditions for every and ,

and for every hold.

The technically sophisticated step in both situations is to show that (ii) implies (iii). The main difficulty is to deal with the involved combinatorial structure transmitted from the product formula to the collection of double contractions. In Section 5.2 below, we will obtain a positive answer to both of the above stated conjectures in the particular case , while general case remains open, because for general we were not able to express (or to estimate from above) the bounds of Theorems 5.1 or 5.2 in terms of the first six moments of the involved chaotic random variables.

The following discussion concerns the symmetric Gamma approximation of a finite sum of Wiener chaoses. Without loss of generality we discuss a sum of two Wiener chaoses. Consider two integers and a sequence of the form

where . In order to bound the second summand on the right hand side of (4.1) we have to compute . By the product formula (2.3) we obtain

Hence to ensure convergence of it is not necessary to that each of the summands converges. Next, we have to bound . Without loss of generality, we can assume that is an isonormal process over a Hilbert space of the type . For every , it is immediately checked that

and . Therefore, by the product formula,

Now, we consider the two summands and and choose . We observe that these summands can be re-presented as for . Summarizing, we have

with

By using the inequality and the isometric property (2.2) we obtain:

Proposition 5.5.

Consider two integers and a sequence of the form

where . Then for every we have

Using Proposition 5.5, it is in principle also possible to deduce bounds for the Variance-Gamma approximation of random variables living inside an infinite sum of Wiener chaoses.

We finally turn in this section to the case of normal approximation and recover the celebrated fourth moment theorem. Moreover, our more general framework implies the following result, which leads to a better rate of convergence (namely exponent 3/2 instead of 1) compared with [14, Theorem 5.2.7], for example. However, our rate is still not optimal as shown by the main result in [15].

Proposition 5.6.

Fix , and consider a sequence such that , , where . Assume that and , as . Then the sequence satisfies a central limit theorem and we have the following bound for the Wasserstein distance:

where is a constant only depending on and where . Moreover, we have that if and only if , as

Proof.

That the sequence satisfies a central limit theorem under our assumptions is ensured by Corollary 4.4 (a). Moreover, using the multiplication formula (2.3) we have

| (5.8) |

Hence a sufficient condition for a central limit theorem to hold is that for every and such that it holds that

as . Now, the double-contractions are dominated by the usual (single) contractions in the following way:

see [3, Equation (4.10)]. This proves the first part the result.

As shown above, the sequence satisfies a central limit theorem provided that . By the fourth moment theorem [14, Theorem 5.2.7], the central limit theorem for is equivalent to the condition that . This proves the second part of the result. ∎

5.2 The case of the second Wiener chaos

The goal of this subsection is to confirm the two conjectures spelled out in the previous subsection for elements of the second Wiener chaos (i.e., for double stochastic integrals). That is, we consider a sequence of elements of the second Wiener chaos of an isonormal process , that is, a sequence of random variables of the type with for each . For symmetric Variance-Gamma distributions () our result reads as follows.

Theorem 5.7.

Let be a -distributed random variable with and suppose that . Then, as , the following assertions are equivalent:

-

(a)

converges in distribution to ,

-

(b)

and ,

-

(c)

and .

In the general asymmetric case , stronger moment or contraction conditions are necessary in order to ensure convergence in distribution of to a Variance-Gamma distributed random variable.

Theorem 5.8.

Let be a -distributed random variable with and , and suppose that . Then, as , following assertions are equivalent:

-

(a)

converges in distribution to ,

-

(b)

for all ,

-

(c)

and .

Before entering the proofs of Theorems 5.7 and 5.8, we collect some general facts about random variables of the type , , belonging to the second Wiener chaos and introduce some notation. First recall that the law of is determined by its moments or, equivalently, by its cumulants. The latter are given by

| (5.9) |

thanks to relation (2.10). Here, is the sequence defined by and for by . In particular .

Proof of Theorem 5.8.

The implication (a) (b) is trivial and (c) (a) follows by combining Theorem 4.1 with Theorem 5.1. Thus, it remains to show that (b) implies (c).

Let with , . Theorem 4.1 for leads to

| (5.10) |

For , , with (5.3) we obtain

| (5.11) |

We represent the left hand side of (5.10) in terms of moments and cumulants of to be able to check that if the six moment condition on (condition (b) in Theorem 5.8) is satisfied, then condition (c) for the contractions follows. The left-hand side of (5.10) consists of six terms. Identity (5.8) gives

By (5.9) we obtain , implying that

Next, with (5.2) we get

using that , see (5.9). For the third term we have . Applying Part (1) of Lemma 2.1 with we obtain for the fourth term

With , the fifth term reads . Part (1) of Lemma 2.1 implies and part (2) says that

Hence , and it follows that . Hence the fifth term can be presented as

Finally, we have to compute . With (5.1), (5.2) and (5.9) we obtain

Summarizing, the left hand side of (5.10) is equal to

| (5.12) |

Using now the moments assumption (b) together with Lemma 3.6, we see that the term in (5.12) converges to zero as and hence the contraction condition (c) follows, see (5.10). This completes the proof. ∎

Proof of Theorem 5.7.

As in the asymmetric case, it suffices to show that (b) implies (c). In our case, and we put and obtain that

| (5.13) |

from (5.10) and (5.12). Hence with (5.11) and (5.13) we get

Into the last identity we plug the well known relationships between moments and cumulants stated in Section 2. Then, a simple calculation leads to

Now, we assume that , and . Then,

as . Since , the contraction conditions in (c) follow. ∎

Remark 5.9.

Let with , . Assume that . Here we list the different forms of conditions on contraction-operators which are equivalent to the convergence in distribution to a member of .

-

(a)

converges to if and only if , as .

-

(b)

converges to if and only if , as .

-

(c)

converges to if and only if and , as .

-

(d)

converges to if and only if and , as .

-

(e)

An example of case (d) is the convergence to , which can be interpreted as the distribution of the product of two correlated standard normal distributed random variables and with correlation . We obtain that converges to if and only if and , as . When , case (c) appears with .

After having characterized convergence in distribution of an element belonging to the second Wiener chaos , we turn now to quantitative bounds for the Wasserstein distance. In contrast to the bounds that follow from the results presented in Section 4 and Section 5.1, we are seeking for upper bounds in terms of moments. In view of Theorems 5.7 and 5.8 we can expect that these bounds only involve moments up to order six. Our next theorem presents bounds in terms of the first six cumulants, as they have a more compact form.

Theorem 5.10.

Let with , .

-

(a)

Let denote a -distributed random variable and assume that . Then there exist constants and such that

-

(b)

Let be -distributed random variable and assume that . Then there are constants and such that

Remark 5.11.

The bound in Theorem 5.10 (b) suggests that we have – in addition to the convergence of the second, fourth and sixth moment or cumulant – to assume that also the third moment or cumulant of converge to zero, as , to conclude convergence in distribution to the limiting random variable. However, we know already from Theorem 5.7 that convergence of the second, fourth and sixth moments or cumulants suffices to obtain convergence in law and hence we can conclude that the third moment of converges to zero automatically under these conditions.

We turn now to the case of normal approximation, which appears as a limiting case of a Variance-Gamma distribution, see Proposition 5.6. Our next result provides a bound for the Wasserstein distance between second chaos element and a Gaussian random variable in terms of the second, third and sixth cumulant. It implies that sequence converges in distribution to a -distributed random variable () if and if and , as . Clearly, this is weaker than the usual forth moment theorem for which we refer to [14].

Proposition 5.12.

Let with , . There exists constants such that

The same bound holds for the Kolmogorov-distance with different constants.

The next statement provides a further characterization of the convergence of the elements of the second chaos, i.e. for with . To avoid technical complications, we restrict for the rest of this section to a symmetrized Gamma distribution . To state the result, consider the Hilbert-Schmidt operator , associated with and write and , respectively, for the eigenvalues of and the corresponding eigenvectors. It is well known (see [14, Section 2.7.4]) that, the series converges for all , and that admits the expansion (in )

| (5.14) |

We notice that for the trace of the th power of one has the relation .

Theorem 5.13.

Let with , . Let denote a random variable with -distribution assume that . Then the following two conditions are equivalent to the conditions stated in Theorem 5.7:

-

(a)

As , and , where, for each , stands for the sequence of the eigenvalues of the Hilbert-Schmidt operator .

-

(b)

As , and for every ,

(5.15)

Proof.

To prove the equivalence of (a) to (c) in Theorem 5.7, we use (5.14) to deduce that

It follows that

Next we show that (a) is equivalent to (b). The proof of the implication is based on a recursive argument. By assumption we have . Moreover,

thus yielding that . Now, if (5.15) holds, then

and (5.15) with replaced by follows. To see the implication , just write

and apply (5.15) with . ∎

As a consequence of Theorem 5.13 we deduce the following characterization of a symmetrized Gamma random variable in the second Wiener chaos.

Corollary 5.14.

Fix an integer . Let with be such that . Then the following conditions are equivalent:

-

(a)

is distributed according to .

-

(b)

and .

-

(c)

and .

-

(d)

There exists for , such that , for and

Proof.

It remains to prove the implication . If (c) is verified, then for every we obtain and hence . Since and , we deduce that there are indices with and indices with . The conclusion follows from (5.14). ∎

Remark 5.15.

The statement of Corollary 5.14 remains true for arbitrary parameters , not only for . The choice just leads to the simple values . In general we would obtain .

On the other hand, suppose that with is such that for some . If is distributed according to ,

then necessarily is an integer and has a -distribution. This follows immediately as in the proof of Corollary 5.14.

5.3 Homogeneous sums and multivariate extensions

Let be a sequence of independent and identically distributed centred random variables with unit variance. Fix an integer and let, for each , be a symmetric function, which vanishes on diagonals in the sense that whenever there are at least two indices such that . Based on this data we define the sequence of homogeneous sum of order as

Universality for the family is a probabilistic phenomenon which asserts that converges, as , to a limiting random variable if and only if converges in distribution to , where is some particular sequence of independent and identically distribution random variables with mean zero and variance one. In our case, we take for a standard Gaussian random variable for each (whence the notation ). Usually, it is much easier to show convergence in distribution of than of . One reason for that being the interpretation of as a multiple stochastic integral of order , i.e., with given by

Moreover, a number of combinatorial tools are available to control the moments of such integrals, see [22] for details.

The universality phenomenon for homogeneous sums has been addressed by Rotar [26] and later also by Nourdin, Peccati and Reinert [16], who consider especially multivariate extensions in case of normal and Gamma limiting distributions by means of Stein’s method and Malliavin calculus. Using the results obtained in the previous sections, we can reduce a corresponding limit theorem to a simple moment condition in case and if the limiting distribution belongs to the broad class of Variance-Gamma distributions.

Proposition 5.16.

Suppose that , as , and let be a random variable having a -distribution with parameters and . Then, as , the following assertions are equivalent:

| (a) converges in distribution to , (b) converges in distribution to . |

If then (a) and (b) are equivalent to for . If and then (a) and (b) are even equivalent to and .

Proof.

We now turn to a multivariate version of the results presented in Section 4. For this, fix and let for each and , be such that . Let further be -distributed with parameters and for all , form the sequence of random vectors and put . Next, define the sequence by

| (5.16) |

and for define by

A distance between the random vectors and is measured by

where the supremum is taken over all functions possessing partial derivatives of order one and two, which are uniformly bounded in absolute value by . The distance is our multivariate version of the Wasserstein distance used in the one-dimensional situation. The proof of the next result closely follows the lines of the proof of Lemma 4.4. in [23], which in turn was inspired by the methods in [4]. To keep the paper reasonably self-contained, we decided yet to present the basic idea.

Proposition 5.17.

There are constants and only depending on and the parameters , and , , such that

| (5.17) |

Proof.

To simplify the notation and to keep the argument more transparent, we restrict to the case bivariate . Thus, what we have to show is that

| (5.18) |

with constants only depending on the parameters , and . We start by writing for an admissible test function ,

Conditioning on the first component of in leads to a one-dimensional situation, which has already been considered in the proof of Theorem 4.1. This contributes the term to the bound (5.18). Let us turn to . Writing for the distribution of an arbitrary random element , we re-write as

The term in brackets is now interpreted as the left-hand side of a Stein equation for , i.e.

| (5.19) |

Here, for fixed , stands for a solution of this equation for the text function . Also put , understood as a bivariate function. Using the smoothness properties of the test function together with the smoothness properties of (again taken from Lemma 3.17 in [7]), we see that

-

(i)

the mappings and are twice differentiable on ,

-

(ii)

there is a constant only depending on such that all partial derivatives up to order two of the mappings in (i) are bounded by

(compare with the proof of Lemma 4.4 in [23] for a similar argument). In terms of , the representation (5.19) of can be re-written as

| (5.20) |

where and indicate the first and second partial derivative in the first coordinate (similarly, we write and for those in the second coordinate). Applying the integration-by-parts-formula (2.6) together with the chain rule (2.4) we see that

Combining this with (5.20) and arguing as in the proof of Theorem 4.1, we see that this contributes the terms and to (5.18). Interchanging the role of and leads to a term and completes the argument. ∎

We now apply Proposition 5.17 to sequences of vectors belonging to a fixed Wiener chaos, i.e., we assume from now on that with , where . The next result ensures that convergence in distribution of the components of towards the components of already implies convergence in distribution of the involved random vector. This can be regarded as a quantitative version for Variance-Gamma distributions of the strong asymptotic independence properties on the Wiener chaos (see Remark 5.19 below for further discussion).

Proposition 5.18.

Proof.

Remark 5.19.

Without a rate of convergence, Proposition 5.18 is also a consequence of the strong asymptotic independence properties inside the Wiener chaos. In particular, the result is a consequence of Theorem 1.4 in [10] and the fact that the distribution of each , , is determined by its moments (alternatively, one can apply Theorem 3.1 in [19]).

Acknowledgements

We are grateful to Ehsan Azmoodeh, Giovanni Peccati and Guillaume Poly for sharing their results with us.

We like to thank Robert Gaunt for helpful discussions on uniform bounds for the solutions of the Stein equation for nonsymmetric Variance-Gamma distributions.

The authors have been supported by the German research foundation (DFG) via SFB-TR 12.

References

- [1] E. Azmoodeh, D. Malicet, and G. Poly, Generalization of the Nualart-Peccati criterion, arXiv:1305.6579, 2013.

- [2] E. Azmoodeh, G. Peccati, and G. Poly, Convergence towards linear combinations of chi-squared random variables: a Malliavin-based approach, preprint, 2014.

- [3] H. Biermé, A. Bonami, I. Nourdin, and G. Peccati, Optimal Berry-Esseen rates on the Wiener space: the barrier of third and fourth cumulants, ALEA Lat. Am. J. Probab. Math. Stat. 9 (2012), no. 2, 473–500.

- [4] S. Bourguin and G. Peccati, Portmanteau inequalities on the Poisson space: mixed regimes and multidimensional clustering, arXiv:1209.3098, 2012.

- [5] L. H. Y. Chen, L. Goldstein, and Q.-M. Shao, Normal approximation by Stein’s method, Probability and its Applications (New York), Springer, Heidelberg, 2011.

- [6] A. Deya and I. Nourdin, Convergence of Wigner integrals to the tetilla law, ALEA Lat. Am. J. Probab. Math. Stat. 9 (2012), no. 1, 101–127.

- [7] R. E. Gaunt, Rates of convergence of Variance-Gamma approximations via Stein’s method, Thesis, University of Oxford, the Queen’s College (2013).

- [8] , Variance-Gamma approximation via Stein’s method, Electronic Journal of Probability 19 (2014), no. 38, 1–33.

- [9] S. Kusuoka and C. Tudor, Extension of the fourth moment theorem to invariant measures of diffusions, arXiv:1310.3785, 2013.

- [10] I. Nourdin, D. Nualart, and G. Peccati, Strong asymptotic independence on Wiener chaos, arXiv:1401.2247, 2014.

- [11] I. Nourdin and G. Peccati, Noncentral convergence of multiple integrals, Ann. Probab. 37 (2009), no. 4, 1412–1426.

- [12] , Stein’s method on Wiener chaos, Probab. Theory Related Fields 145 (2009), no. 1-2, 75–118.

- [13] , Cumulants on the Wiener space, J. Funct. Anal. 258 (2010), no. 11, 3775–3791.

- [14] , Normal approximations with Malliavin calculus, from Stein’s method to universality, Cambridge Tracts in Mathematics, vol. 192, Cambridge University Press, Cambridge, 2012.

- [15] I. Nourdin and G. Peccati, The optimal fourth moment theorem, Proc. Am. Math. Soc., to appear, 2014.

- [16] I. Nourdin, G. Peccati, and G. Reinert, Invariance principles for homogeneous sums: universality of Gaussian Wiener chaos, Ann. Probab. 38 (2010), no. 5, 1947–1985.

- [17] I. Nourdin and G. Poly, Convergence in law in the second Wiener/Wigner chaos, Electron. Commun. Probab. 17 (2012), no. 36, 12.

- [18] , Erratum: Convergence in law in the second Wiener/Wigner chaos, Electron. Commun. Probab. 17 (2012), no. 54, 3.

- [19] I. Nourdin and J. Rosiński, Asymptotic independence of multiple Wiener-Ito integrals and the resulting limit laws, Ann. Probab. 42 (2014), no. 2, 497–526.

- [20] D. Nualart, The Malliavin calculus and related topics, second ed., Probability and its Applications (New York), Springer-Verlag, Berlin, 2006.

- [21] D. Nualart and G. Peccati, Central limit theorems for sequences of multiple stochastic integrals, Ann. Probab. 33 (2005), no. 1, 177–193.

- [22] G. Peccati and M.S. Taqqu, Wiener chaos: moments, cumulants and diagrams, Bocconi & Springer Series, vol. 1, Springer, Milan; Bocconi University Press, Milan, 2011, A survey with computer implementation, Supplementary material available online.

- [23] G. Peccati and C. Thäle, Gamma limits and -statistics on the Poisson space, ALEA Lat. Am. J. Probab. Math. Stat. 10 (2013), no. 1, 525–560.

- [24] E. A. Peköz, A. Röllin, and N. Ross, Degree asymptotics with rates for preferential attachment random graphs, Ann. Appl. Probab. 23 (2013), no. 3, 1188–1218.

- [25] J. Pike and H. Ren, Stein’s method and the Laplace distribution, preprint, arXiv:1210.5775, 2012.

- [26] I.V. Rotar, Limit theorems for polylinear forms, J. Multivariat Anal. 9 (1979), no. 4, 511–530.

- [27] C. Stein, P. Diaconis, S. Holmes, and G. Reinert, Use of exchangeable pairs in the analysis of simulations, Stein’s method: expository lectures and applications, IMS Lecture Notes Monogr. Ser., vol. 46, Inst. Math. Statist., Beachwood, OH, 2004, pp. 1–26.