Parametric estimation of Lévy processes

11institutetext:

Hiroki Masuda 22institutetext: Institute of Mathematics for Industry, Kyushu University,

744 Motooka, Nishi-ku, Fukuoka 819-0395, Japan

22email: hiroki@imi.kyushu-u.ac.jp

*

Abstract

The main purpose of this chapter is to present some theoretical aspects of parametric estimation of Lévy processes

based on high-frequency sampling, with a focus on infinite activity pure-jump models.

Asymptotics for several classes of explicit estimating functions are discussed.

In addition to the asymptotic normality at several rates of convergence,

a uniform tail-probability estimate for statistical random fields is given.

As specific cases, we discuss method of moments for the stable Lévy processes in much greater detail,

with briefly mentioning locally stable Lévy processes too.

Also discussed is, due to its theoretical importance,

a brief review of how the classical likelihood approach works or does not,

beyond the fact that the likelihood function is not explicit.

AMS Subject Classification 2000:

Primary:

60F05, 62F12, 60G51, 60G52.

Secondary:

60G18.

keywords:

Asymptotic normality, Convergence of moments, Estimating function, Fisher information matrix, Lévy process, Likelihood inference, (Locally) Stable Lévy process.1 Introduction

Lévy processes form the basic class of continuous-time stochastic processes, serving as building blocks to make up more general models, such as a solution to a Lévy driven stochastic differential equation. An estimation paradigm with a universal implementable manner is, however, hard or impossible to be available because of the diversity of the driving Lévy measure, and this has been attracting much interest from statisticians. The main objective of this chapter is to present several asymptotic results concerning parametric estimation of Lévy processes observed at high frequency. Explicit case studies will be presented along topics.

Throughout, we are given an underlying probability space endowed with a real-valued Lévy process . The expectation operator is denoted by . Let and stand for the characteristic function and the distribution of a random variable , respectively. We recall that there is one-to-one distributional correspondence between a Lévy process and an infinitely divisible distribution on . The celebrated Lévy-Khintchine formula for a Lévy process says that for each Lévy process there uniquely corresponds a generating triplet associated with the truncation function being the identity on and otherwise:

| (1.1) |

where is the constant trend, is the variance of the Gaussian part, and is the Lévy measure, namely, a -finite measure on such that and , and finally stands for the indicator function of the set . We may always deal with càdlàg (right-continuous and having left-hand side limits) modifications of , implying that a.s. takes values in the space , , equipped with the Skorokhod topology; hence we may always deal with separable Lévy process, so that, e.g., probabilities of union or intersection of seemingly uncountable corrections of events can be defined. The generating triplet uniquely determines the law of on the space . As usual, we will denote by the (directed) jump size of at time . If (resp. ), then is said to be infinite-activity (resp. finite-activity), meaning that sample paths of a.s. have infinitely (resp. finitely) many jumps over each finite time interval. We refer to Ber96 , JacShi03 , and Sat99 for systematic and comprehensive accounts of Lévy processes.

We are concerned with parametric estimation of . We denote by the finite-dimensional parameter of interest, and by the family of the induced image measures of ; in general, there may be nuisance elements of , so that may not completely determine . Throughout this chapter, we assume that is a bounded convex domain in unless otherwise mentioned; the boundedness may or may not necessary according to each situation, but we put it as a standing assumption just for convenience. The closure of will be denoted by .

There do exist many infinitely divisible distributions admitting a closed-form density, and we indeed have a wide variety of with explicit density of . Even so, however, the likelihood function of for may not be necessarily explicit due to the lack of the reproducing property of ; one such an example is the Student- Lévy process Cuf07 , where is Student- hence fully explicit, but for is not. Also, as in the case of the stable Lévy processes (see Section 3), it can happen that the Lévy measure is given in a simple closed form while the transition density of is intractable for any .

Although it has been a long time since the rigorous probabilistic structure of Lévy processes has been clarified, we do not have any absolute way to perform statistical estimation for its general class. The problem exhibits rather different features and solutions according as what the true data-generating triplet is: for example, the concrete structure of may essentially affect estimation of the drift ; and also, coexistence of both diffusion and jump parts can make estimation much more difficult than in continuous or purely-discontinuous cases.

More important from a statistical viewpoint is the structure of available data, that is to say, how much one can observe ’s sample path. We can single out the following two cases as basic situations in developing a large-sample theory.

-

•

Having continuous-time data with should be ideal, in which case we may estimate some parameters without error, rendering the statistical theory void.

-

•

Suppose that we observe at discrete-time points such that

(1.2) for each . Then, we will refer to the sampling scheme as low-frequency sampling if the sampling intervals satisfy that

(1.3) which entails that . In contrast, high-frequency sampling means that we have

(1.4) as , and in this case the terminal sampling time may or may not tend to infinity. In either case, we are led to consider estimation based on the infinitesimal array of independent random variables , where

denotes the th increments of . Asymptotic results can become drastically different from the case of low-frequency sampling; in particular, best possible convergence rate of an estimator can differ for each component. For brevity, we assume that

for and (1.5) whenever discrete-time sampling is concerned. The equidistance of sampling could be weakened if we render asymptotically not so deviating from one another with a suitable control of balance between behaviors of , , and .

Our main interest is in parametric estimation of pure-jump Lévy processes having some nice explicit features, based on high-frequency sampling; the cases of continuous-time data and low-frequency sampling will be mentioned only briefly. Needless to say, “high-frequency” of data in statistical model is a relative matter, for there is no universal way to associate model time with actual time; one may put one day, one minute, one second, and so on to , and more concretely, daily data over three years can be as high-frequency as one thousand intraday data over one day.

Here is the outline of this chapter. Section 2 overviews some basic aspects of the maximum-likelihood approach for both continuous-time and discrete-time data. When attempting parametric inference for the unknown parameter based on a realization of , , the maximum-likelihood estimator (MLE) is theoretically the first to be looked at, although it requires full specification of and may be fragile against model misspecification. Since the likelihood function directly depends on , it takes different forms according as structure of available data. Specific case studies given in Section 2 are based on KawMas11 , KawMas13 , and Mas09 .

In Sections 3, we will look at the non-Gaussian stable Lévy processes in much greater details. Although the stable Lévy processes has the intrinsic scaling property allowing us to make several estimates of probabilities and expectations tractable, the transition density does not have a closed form except for a few special cases. More severely, as long as the joint estimation of the stable-index and the scale parameters are concerned, the asymptotic Fisher information matrix will turn out to be singular at any admissible parameter value. Nevertheless, we can provide some practical moment estimators, which are asymptotically normally distributed with non-singular asymptotic covariance matrices. The contents of this section are based on Mas09_slp and Mas10_proc . In Section 3.6, we will briefly mention the locally stable Lévy processes, a far-reaching extension of the stable Lévy processes.

Section 4 presents a somewhat general framework for deducing the convergence of moments of scaled -estimators, which plays a crucial role in asymptotic analysis concerning the expectation of an estimator-dependent random sequence, such as the mean squared prediction and the AIC-like bias correction in model assessment. Thanks to the polynomial type large deviation inequality developed in Yos11 , we will give a set of easy sufficient conditions for the uniform tail-probability estimate for a class of statistical random fields associated with possibly multi-scaling -estimation.

Finally, we conclude in Section 5 with a few remarks on related issues.

Throughout this chapter, we will use the following basic notation. We denote by and the convergences in law and probability, respectively. For a multilinear form and variables , we write

Sometimes we will write (resp. ) for the th (resp. th) entry of a vector (resp. matrix ). We denote by the th partial differential operator with respect to a multidimensional variable , and by the -identity matrix. For a matrix , denotes its transpose. We write if there exists a generic positive constant , possibly varying from line to line, such that for every large enough. We also write for two deterministic functions and if the ratio tends to . The map takes values according as , , , respectively. Given two measures and on some measurable space, we write if they are equivalent, i.e., if they have the same null sets. Finally, we will write and for the -variate normal distribution and the probability density with mean vector and covariance matrix , respectively.

2 Classical maximum-likelihood approach

2.1 Local asymptotics for continuous-time and low-frequency sampling

2.1.1 Continuous-time data

We denote by the restriction of to , where is the natural filtration of , namely, the smallest -field to which is adapted. The asymptotics here is taken for . No one doubts this situation is “ideal”; in particular, we can completely distinguish the continuous part and possibly infinite-activity jump part. Although practically irrelevant and far from being realistic, the statistical theory based on continuous-time data is fruitful in its own right and enables us to get some insight into what we can do best for estimating . In particular, we will see that continuous-time data may allow us to pinpoint some (not necessarily all!) parameter components “path-wise”, so that no statistics is required. We refer to the review article (Jac09, , Sections 2.4 and 4.1) for related discussions.

We need a criterion for the equivalence between and , so as to make the likelihood ratio (the Radon-Nikodym derivative) well-defined. The equivalence can be effectively characterized in terms of the generating triplet, say (recall (1.1)):

Theorem 2.1

Given any and , we have if and only if both of the following conditions hold.

- (a)

-

.

- (b)

-

with the function

(2.1) satisfying that

-

•

for some ,

-

•

.

-

•

If , then we may have much wider possible choices for , , and . See (Sat99, , Theorem 33.1) for the proof of Theorem 2.1; see also (AkrJoh81, , Theorem 4.1), (JacShi03, , Theorem IV.4.32), (KabLipShi80, , Theorem 15), and Sat00 .

When the absolute continuity fails, we may identify some parameters without statistical error. If and for each are mutually singular whenever , then, given a specific value of we may pathwise determine whether or not the true value equals .

Example 2.2

Consider the model with , where is the -stable Lévy process with . Especially if , it follows from Theorem 2.1 that if and only if (the integrals in the conditions of the theorem should be zero), rendering that continuous-time data leads to no sensible result for all the parameters involved. Thus likelihood based arguments lose their meaning, while the statistical problem still a priori makes sense. In Section 3 we will look at the stable Lévy process in more detail, but let us here illustrate a possible error-free identification in the simple setting where and are known, so that . Fix any constant so that , and write . Having observed a sample path , we can compute

for any , hence too as soon as it exists. Thanks to the scaling property of the stable Lévy process, we can see that and . It follows from the Borel-Cantelli argument that is a strongly consistent estimator: . \qed

Example 2.3

The generalized hyperbolic distribution is a very popular infinitely divisible distribution in the fields of turbulence and mathematical finance; a nice systematic review can be found in BibSor03 and Ham10 . The distribution of the generalized hyperbolic Lévy process is characterized by the five parameters ; in particular, and represent scale and location, respectively, and the corresponding Lévy density, say , admits the asymptotic expansion (Rai00, , Proposition 2.18)

By means of Theorem 2.1, (Rai00, , Sections 2.5 and 2.6) proved that if and only if and . As mentioned before, continuous-time sample allows us to distinguish all jump times and jump sizes, hence for each we can identify all such that . Also proved in Rai00 is that the statistics

are strongly consistent estimators of and , respectively, as . A continuous-time data allows us to compute and . It is possible to see that is an example of the locally Cauchy Lévy process in the sense that weakly tends to the Cauchy distribution as (see Section 3.6 for brief remarks on locally stable Lévy processes); in Section 2.3.4, we will look at this point in more detail for the normal-inverse Gaussian Lévy process, the special case where . \qed

Fix a , assume that for each , and let

be a non-random positive definite diagonal matrices such that as for , and a non-random nonnegative definite symmetric matrix. Let and

When we may assume that . The family of probability measures is said to satisfy the local asymptotic normality (LAN) at with rate and (constant) Fisher information matrix , if for each the stochastic expansion

| (2.2) |

holds under , where ; a nice concise exposition of interpretation of the LAN as the weak convergence to a Gaussian experiment can be found in (vdV98, , Chapter 7).

From a decision theoretic point of view, the LAN is of dominant importance in asymptotic statistics. If we have the LAN, the notion of asymptotic optimality in regular statistical estimation and testing hypotheses come into effect, and the asymptotic optimality is described in term of the sequence up to deterministic factors. Especially, the matrix corresponds to the maximal (multiscale) rate at which we can infer the true value of . We here recall that an estimator of is called regular if for each the distribution weakly converges along to some distribution free of . The celebrated Hajék-Inagaki convolution theorem (Haj70 and Ina70 ) tells us that for some distribution , based on which we can deduce the asymptotically maximal concentration property: for any convex set symmetric around the origin and any regular estimator of we have

| (2.3) |

Moreover, we have

| (2.4) |

in the matrix sense; hence, is the minimal possible asymptotic covariance matrix, and if under , then should be non-negative definite.

It is also possible for several kinds of tests to construct a locally asymptotically optimal test function. We refer to LeCYan00 , Str85 and vdV98 for more details of what we can benefit from the LAN theory in testing hypothesis.

We should note that, in order to apply the general asymptotic optimality theory based on the LAN, the matrix should be positive definite over ; if not, the LAN may not be of much help. It will turn out that in our framework the singularity of will very naturally occur for every (see Sections 2.2.3 and 3.2).

The LAN for continuously observed pure-jump Lévy processes was proved in (AkrJoh81, , Theorem 5.1) (see also Lus92 and Sor91 for related general results concerning continuously observed multidimensional models containing non-null diffusion part). To state the result, let denote the random measure of jumps associated with (cf. (JacShi03, , II §1b)), and its compensated version under .

Theorem 2.4

Let be a Lévy process having the generating triplet . Assume that for and that there exists an -valued measurable function on for which,

- (a)

-

The Fisher information matrix

is finite and positive definite for each .

- (b)

-

The following convergences hold (recall (2.1)):

-

•

as ,

-

•

as ,

-

•

For each , we have as

-

•

Then, the stochastic expansion (2.2) holds at with and

Having the LAN in hand, we then look for an estimator such that . The consistency and asymptotic normality for general pure-jump Lévy processes were studied by Akr82 .

Remark 2.5

Given a Lévy measure and with , we can form a natural exponential family generated by based on the newly defined Lévy measure . This simple transform makes it possible to do several explicit computations. See (KucSor97, , Chapter 2 and Section 11.5) for details of the exponential family generated by a general semimartingale models. The special form leads to a handy asymptotically optimal estimator of even for discrete-time data (Woe01, , Section 3.1); needless to say, the estimator may not be of direct use when also depends on unknown parameters. \qed

In the rest of this chapter, we will concentrate on discrete-time data. The filtration of the underlying statistical experiments are then much smaller than in the case of continuous-time data, and estimation without error is seldom possible.

We will suppose that for . According to the distributional identity

the problem amounts to estimation based on the rowwise independent triangular-array data. Even if we know that is absolutely continuous with respect to the Lebesgue measure, the likelihood function can be in general described only in terms of the seemingly intractable Fourier-inversion formula:

| (2.5) |

This annoying fact prevents us from developing a (more or less) universally feasible procedure for studying asymptotic behavior of likelihoods; with a positive thought, we could get a nice opportunity of research. As will be seen later, there do exist some specific examples where we may get rid of the integral in (2.5) to obtain a tractable form, from which we can derive valuable information about asymptotically optimal inference.

Remark 2.6

The above situation is somewhat similar to estimation of the discretely observed nonlinear diffusion model

Under some regularity conditions on the coefficients we can prove the existence of the likelihood (transition density). However, its closed-form is seldom known. We then face the statistical problem: how can we estimate the parameter based on ? There is a large literature on this subject, and still lively ongoing in several directions. See (Pra99, , Chapters 3 and 5) and Sor12 for an extensive review of recent developments. \qed

2.1.2 Low-frequency sampling

Woerner, in her thesis Woe01 , systematically studied the LAN with several case studies, largely under low-frequency sampling. Suppose that , so that the situation is a special case of the classical i.i.d. sample

having the infinitely divisible population . The model is then to be estimated at usual rate . In order to deduce the LAN, it is therefore possible to resort to the classical criterion based on the differentiability in quadratic mean of the family :

Theorem 2.7

Assume that admits a parametric density with respect to some measure : , and that for there exists a measurable -valued function such that

| (2.6) |

as . Then:

-

1.

;

-

2.

the Fisher information matrix

exists and is finite;

-

3.

for each , we have the stochastic expansion

(2.7) under , where .

See (vdV98, , Theorem 7.2) for the proof of Theorem 2.7. For (2.6) to hold, it is sufficient that:

-

•

for each , the nonnegative map is of class ;

-

•

and the matrix is well-defined and continuous as a function of .

Indeed, we can then apply Scheffé type argument to deduce (2.6) with , which may be defined to be when . See (vdV98, , Lemma 7.6) for details.

What should be noted here is the dependence of the Fisher information matrix on the sampling step size , which may clarify how estimation of each component of is affected by . If we can let vary as increases in such a way that for some positive sequence , then the -consistency for the MLE of can be expected. The high-frequency sampling scheme corresponds to such a situation, where we will see later that both and may occur, depending on the concrete structure of the underlying Lévy process. In Theorem 2.12 below, we will present a unified treatment of low- and high-frequency sampling schemes for proving LAN under somewhat more restrictive conditions involving the second derivative of .

2.2 Local asymptotics for high-frequency sampling

From now on we will concentrate on the equidistant high-frequency sampling scheme; recall (1.2), (1.4), and (1.5).

2.2.1 On small-time behavior of increments

When , things become entirely different from the low-frequency sampling. The high-frequency sampling is theoretically fruitful, for it allows us to take into account approximation of the underlying model structure in small time, providing a somewhat unified picture for asymptotics. As was already mentioned, this brings about special phenomena in estimating an underlying continuous-time model. In particular, various optimal rates of convergence of regular estimators become available through the LAN. A criterion for deducing the LAN in case of high-frequency sampling and univariate was proved in (Woe01, , Theorem 1.6). Theorem 2.12 below will put similar conditions, but importantly, it can deal with cases where optimal rate may be different componentwise.

Since each vanishes as , it is meaningful to clarify a transform giving rise to a nontrivial weak limit. The simplest yet important one is the location-scale linear transform

| (2.8) |

for some and with as . In this case the limit is necessarily strictly stable (cf. Section 3), and moreover, due to (BerDon97, , Proposition 1) much more is true:

Lemma 2.8

Assume that is a Lévy process in and that there exist a non-random positive function and a non-degenerate distribution (i.e. is not a Dirac measure) such that

| (2.9) |

Then we have the following.

-

1.

is regularly varying with index (i.e. as for each ) where , and is strictly -stable.

-

2.

for each , hence in particular admits a continuous Lebesgue density, say .

- 3.

Apart from the -stable Lévy processes, for which the stable approximation is trivial due to the scaling property, several familiar Lévy processes are known to fulfill (2.9) with , hence in (2.8). Such a Lévy process may be called locally -stable, which we will briefly discuss in Section 3.6.

Some information about small-time asymptotic behaviors of an increment both in probability and a.s. can be found in (Don07, , Chapter 10).

Remark 2.9

One may wonder what will occur when is not weakly convergent for any and . In such cases, the Lévy measure does not behave as any -stable Lévy process, and some non-linear transform of , say , might be relevant. The right should be strongly model-dependent, so that it may be hard to formulate a general way to find it. Nevertheless, there exists a concrete example concerning subordinators; recall that a subordinator is a univariate Lévy process whose sample path is a.s. nondecreasing, and whose general form of the Lévy-Khintchine formula is given by

for some and supported by . Recently, BarLopWol12 characterized the class of drift-free () subordinators for which

| (2.10) |

where () denotes the Pareto distribution corresponding to the density . For example, BarLopWol12 proved that the above weak convergence holds if admits a Lebesgue density such that

| (2.11) |

Building on (2.10), one may think of making semiparametric inference based on the array , leaving the parameters other than unknown; a simple and fully explicit example satisfying (2.11) is the gamma subordinator with the density of being , . We do not pursue this subject further in this chapter, but only make a small remark about simulations: it may happen that a -random number is too small to be regarded as non-zero by computer, causing a trouble in taking its reciprocal. \qed

2.2.2 LAN with multi-scaling

We will assume some regularity conditions.

Assumption 2.10

The support of does not depend on and . For each and the distribution under admits a Lebesgue density , which is in turn of the class for each as a function of .

The log-likelihood function a.s. exists as the sum of the rowwise independent triangular arrays:

We will present a criterion for the LAN under discrete-time sampling, which is applicable to both low- and high-frequency sampling schemes.

Assumption 2.11

The following convergences hold true as :

- (a)

-

;

- (b)

-

;

- (c)

-

for every , where .

Of course, Assumption 2.11 are partly related to the Lindeberg-Feller central limit theorem. Once is specified and is explicit, verification of Assumption 2.11 may not be so difficult. We note that (c) ensures the Lindeberg condition:

for every .

Let denotes the restriction of to .

Theorem 2.12

Theorem 2.12 can be proved all the same as in (KawMas13, , Section 4.1); we should note that it is somewhat straightforward to extend Theorem 2.12 to deal with ergodic models, with the help of limit theorems for mixing random variables and/or martingale limit theorems. So far, several explicit examples have been known for which we can apply Theorem 2.12. Real difficulty arises when is not explicit, even if its existence can be verified; obviously, without restricting the target class of Lévy processes it is impossible to deduce any LAN with specific and . Research in this direction is currently under investigation.

The asymptotic orthogonality of parameters (diagonal Fisher information matrix) is known to be very useful in statistics; e.g. CoxRei87 and JorKnu04 . In the high-frequency sampling scheme, we quite naturally encounter the opposite-side phenomenon, namely, the determinant of the normalized observed information matrix tends in probability to zero (so the Fisher information matrix ) for every . This problem does not seem to be sidestepped simply by using an off-diagonal norming . We will look at some such examples in Sections 2.2.3 and 3.2. As mentioned before, the LAN itself is not quite meaningful if , although it reveals which parameters cause the unpleasant asymptotic singularity, giving us a caution for adopting the likelihood approach. In this case, there would exist no unbiased estimator with finite variance, and the possible asymptotic distributions of the maximum likelihood estimators would be no longer normal and have infinite-variance (see LiuBro93 and StoMar01 ). Nevertheless, it is worth mentioning that we may bypass the non-invertibility of the asymptotic covariance matrix at the expense of the optimal rate of convergence, retaining asymptotic normality (Kaw13 , Mas09_slp and Tod13 ); some examples will be given in Sections 3.3 and 3.4 for the stable models.

2.2.3 Example: Meixner Lévy process

The Meixner distribution, denoted by , is infinitely divisible and admits a density

| (2.14) |

We write , a bounded convex domain whose closure satisfies that

The Lévy measure of admits the explicit Lebesgue density

We refer the reader to Gri99 and SchTeu98 for more details of the Meixner distribution.

Let be a Lévy process such that . The characteristic function of is given by

implying that for each and ,

| (2.15) |

For each , we define the i.i.d. random variables by

| (2.16) |

with common distribution . We can also see that has mean, variance, skewness and kurtosis, respectively,

Further, converges to the standard Cauchy distribution, as : indeed, for each

The Meixner Lévy process possesses the small-time Cauchy property as well as the long-time Gaussianity in the functional sense; see KawMas11 and the references therein.

The log-likelihood function is

and we have the following LAN result:

Theorem 2.13

If , then we have the LAN for each at rate

and Fisher information matrix

| (2.17) |

The Fisher information matrix (2.17) is singular for every , which is obviously caused solely by the joint maximum-likelihood estimation of and ; as soon as or is fixed, the resulting Fisher information matrix becomes purely diagonal, ensuring that the maximum likelihood estimators are asymptotically independent. The asymptotic singularity also acts as a practical warning in the maximum likelihood estimation for the Meixner Lévy process with a very small under low-frequency sampling scheme, since, as seen by (2.15), the parameter and the time play the same role. The form of of (2.17) is much simpler compared with that of the Fisher information matrix in the low-frequency sampling; see (GriPro09, , Appendix A).

As we will see in Section 3.2, the joint maximum-likelihood estimation of the stability index and the scale parameter of the stable Lévy processes also leads to a constantly singular Fisher information matrix. It can be expected that the asymptotic singularity occurs for every Lévy process satisfying the small-time stable approximation and having unknown index (Lemma 2.8) and scale; a discussion on this issue can be found in Kaw13 . In this direction, the case of the Meixner Lévy processes is not directly relevant since we beforehand know that the small-time stability index equals one.

We may expect from the definition of of (2.16) that the asymptotic singularity stems from the non-identifiability between the parameters and in small time; they may be identifiable only in the product form . The case of continuous-time data captures this point more directly:

Proposition 2.14

Let and let , . The probability measures and are equivalent if and only if and .

Proof 2.1.

Since for every , the function

is well-defined. The mean of is given by , hence

Now, according to Theorem 2.1 it suffices to show that the following two conditions hold if and only if and :

- (a)

-

;

- (b)

-

.

Let us look at the behaviors of the Lévy density near the origin and at infinity. By means of the approximation

we see that the Lévy density satisfies that

| (2.18) |

Since behaves like (resp. ) as (resp. ), we have

| (2.19) |

| (2.24) |

for some positive constants and , depending on . Hence (a) holds if and only if , which is to be imposed in the rest of this proof.

The condition (b) is equivalent to

In the case , the last display can be rewritten as

Denote the part on the left-hand side by . We show that is identically zero (given any positive and ), entailing that (b) holds if and only if hence completing the proof. We have

since the integrand is odd, continuous in , and exponentially decreasing as . Using the fact that the variance of equals , we get

Hence

We can deduce that in a similar manner. It follows that is identically zero. ∎

2.3 Uniform asymptotic normality of MLE with non-degenerate Fisher information

2.3.1 Basic result

When the Fisher information matrix is non-degenerate, we can go further in an elegant way. The contents of this section is essentially a special case of Sweeting’s general result Swe80 (also relevant is (BasSco83, , Chapter 1, Section 4)), based on which we can provide a simple set of sufficient conditions for the asymptotic normality and the asymptotic optimality of the MLE, as well as for the LAN. A nice feature of the results is that it is almost enough to look at the uniform asymptotic behavior of the normalized observed information matrix having a positive definite limit (the Fisher information matrix) continuous in the parameter, and need not take care of the central limit theorem for the score-function part.

We will assume that the log-likelihood function a.s. belongs to the class , and we write the score function and the observed information matrix by

respectively. To state the result we need to introduce some more definitions. Let us recall that the convergences in distribution and in probability of random vectors are metrizable. We will need their uniform versions. Let the symbol stand for the ordinary uniform convergence over each compact subset of . For vector-valued random functions and on with each being -measurable, we write and if and , respectively. Here, and denote any metric characterizing and under , respectively: for example, we may take

| (2.25) | ||||

| (2.26) |

where

is the bounded-Lipschitz norm; by the definitions, implies ; e.g., (BasSco83, , Appendix A.1). Finally, let be as in (2.12), now satisfying that .

Recall that stands for the restriction of to . With the above-mentioned notation, we will say that the family of probability measures is uniform LAN (ULAN) in with rate and Fisher information if there exists a non-random function with being positive definite for any , such that , that , and that

| (2.27) |

for any non-random bounded sequence .

The normalized observed information matrix is defined by

The following theorem provides a simple tool for verifying ULAN, uniform asymptotic normality, and asymptotic efficiency.

Theorem 15.

Assume that

- (a)

-

The log-likelihood functions are of class ,

- (b)

-

For each and ,

(2.28) where the supremum is taken over all such that .

- (c)

-

There exists a continuous map with being positive definite for each , such that and that for each .

Then, we have the following.

-

1.

The family of probability measures is ULAN with rate and Fisher information matrix .

-

2.

There exists a local maximizer of with probability tending to one, for which .

Proof 2.2.

First we prove 2. We have

so that by (2.26),

| (2.29) |

For and a constant we let , and

where the supremum is taken over all such that for . We have

for each , hence

| (2.30) |

Given any functions on , we have if and only if for any convergent . It follows from (2.29) that

| (2.31) |

Based on (2.28), (2.29), and (2.31), the claims 2 follows from (Swe80, , Theorems 1 and 2).

Needless to say, we can remove the condition (b) in Theorem 15 as soon as is free of . We should note that under the conditions of Theorem 15, the convolution theorem automatically ensures the asymptotic optimality of the MLE among the class of all regular estimators, in terms of the maximal concentration and the minimal asymptotic covariance matrix: recall (2.3) and (2.4) in Section 2.1.1.

2.3.2 Example: Gamma subordinator

Let be the gamma subordinator such that whose density is given by

| (2.32) |

The Lévy density of is given by

In this model, the stable approximation in small time through (2.8) fails to hold, but a certain nonlinear transform is in force instead (Remark 2.11). We also note that, given any , , and , it follows from Theorem 2.1 that and are not mutually absolutely continuous when .

The log-likelihood function based on is given by

| (2.33) |

Denoting by the digamma function, we get the following likelihood equations for :

| (2.34) | ||||

| (2.35) |

It is easy to see that the equation admits a unique root for each positive , hence it is straightforward to solve (2.34) numerically.

The following results can be obtained by a direct application of Theorem 15:

Theorem 16.

Remark 17.

Here are some observations concerning Theorem 16.

-

•

If does not tend to infinity, then the observed information associated with is stochastically bounded in without normalization: we have . That is to say, data over fixed time period does not carry enough information to estimate consistently.

-

•

In contrast, it is possible to deduce even when is bounded, with leaving the true value of unknown; note that we can still use the estimating equation (2.34) for . We then have the ULAN for with rate and Fisher information , and the MLE is asymptotically efficient.

-

•

Using a naive estimator may result in essential loss of asymptotic efficiency, and even worse, we may have a slower rate of convergence. For example, consider the method of moments based on

By means of the Lindeberg-Feller central limit theorem and the delta method, it is easy to prove that the resulting moment estimator satisfies the asymptotic normality with the slower rate of convergence for estimating and with the non-diagonal asymptotic covariance matrix:

Thus, considerable amount of information of contained in high frequency of data has been thrown away. As for , the rate is optimal but the relative efficiency is .

- •

∎

2.3.3 Example: Inverse-Gaussian subordinator

Let be the inverse-Gaussian subordinator such that , which admits the density

The positive half-stable subordinator appears as the limit for . The Lévy measure admits the density

In case where a continuous-time data is available, Theorem 2.1 tells us that, given any , , and , the measures and fail to be mutually absolutely continuous if .

The log-likelihood function of is

| (2.38) |

based on which the MLE is explicitly given by

| (2.39) |

As soon as , we have for each and . In fact, it can be shown that

where , , denotes the modified Bessel function of the third kind with index (see AbrSte92 ; sometimes also referred to as “modified Bessel function of the second kind” or “modified Hankel function”):

| (2.40) |

In particular, for the negative-order moments we have

which follows from the formula

It follows that

| (2.41) |

and also that

Now we can apply Theorem 15 to derive the following, a quite similar phenomenon to Theorem 16:

Theorem 18.

2.3.4 Example: Normal inverse-Gaussian Lévy process

In this section, we will present a fully explicit example of a real-valued Lévy process whose likelihood is well-behaved.

The normal inverse-Gaussian (NIG) distribution on is defined by the density

| (2.43) |

where is the modified Bessel function given by (2.40). We will consider estimation of , with being a bounded convex domain whose closure satisfies that

| (2.44) |

Note that we precluded the Cauchy case (), which occurs as the total-variation limit of for .

The distribution is infinitely divisible whose generating triplet of the form (1.1) is given as follows:

-

•

The Lévy measure admits the density

(2.45) -

•

;

-

•

, with denoting the mean of .

We refer to Bar95 and Bar98 for more details of the NIG distribution and the NIG Lévy process.

Let be the univariate NIG Lévy process such that . Once again, some of the parameters could be estimated without error if a continuous-time data were available. Fix any , and let , , denote the distribution of associated with , . Applying Theorem 2.1, we see that and are equivalent if and only if and .

We now specify what will occur for high-frequency data. The LAN and non-degeneracy of the Fisher information has been previously obtained by KawMas13 , where the most materials given in the proof of the next theorem were presented. In the light of Theorem 15, we can refine (KawMas13, , Theorem 3.1) as follows:

Theorem 19.

Assume the aforementioned setting, and let and . Then we have the ULAN with rate

| (2.46) |

and Fisher information matrix

| (2.47) |

where the entries are given as follows:

For each the integral in is finite and is positive definite. Further, we have .

Remark 20.

Proof 2.3 (Theorem 19).

In view of Theorem 15, we need to verify the uniform convergence of and for the observed information matrix . The proof is divided into several steps.

Step 1. We begin with the locally Cauchy distributional property in small time. We have

from which

| (2.48) |

for any and . Observe that for each the i.i.d. triangular array

has the common distribution . We denote by the density of . The goal of this first step is to prove that

| (2.49) |

where and denotes the standard symmetric Cauchy density corresponding to the characteristic function .

Let . Then, we trivially have

Put and . Then, simple manipulation gives

| (2.50) |

It follows that for each . The expression (2.50) also leads to the estimate

| (2.51) |

By means of the Fourier inversion formula we have

| (2.52) |

Then (2.49) follows on applying the dominated convergence theorem to the upper bound of (2.52) under (2.51).

Step 2. We introduce the functions

| (2.53) |

where we used the identity for (2.53). The function and its derivatives are to be defined at as limits from the right. These functions will play important roles later on. In this step, we will prove the following three properties.

- (a)

-

The functions , , and are bounded in .

- (b)

-

is bounded and continuous in . Moreover, as and as .

- (c)

-

as and as . In particular, is bounded and continuous in .

The claim (a) follows from the fact for each . As for (b), the continuity of is obvious. It is known that

| (2.56) | ||||

| (2.57) |

where denotes the Euler-Mascheroni constant and (see AbrSte92 ). The desired behavior of as follows on applying (2.56) to (2.53). Further, we can deduce the desired behavior of as by applying (2.57) for and then expanding the fraction as a power series of . Now the boundedness of is trivial.

Turning to (c), we note the identity , hence . This follows on applying (2.53) together with the identity , which is valid for each . These expressions combined with (b) prove (c).

Step 3. In view of (2.43) and (2.48), we can express the log-likelihood function as

| (2.58) |

The introduction of the standard Cauchy density in the expression (2.58) will turn out to be convenient in the process of deriving various limiting values as well as deducing estimates of stochastically small terms.

Let

Noting that , , , , and , we can differentiate (2.58) to get the following partial derivatives:

The task is to verify the uniform convergences of and , and also the positive definiteness of . For the former we will only prove ; as a matter of fact, we can prove that in an analogous and simpler way, making use of the statements (a)(c) in Step 2.

It is straightforward to deduce the convergences except for the case , by using the identities and , the convergence (2.49), and (a)(c) together with the bounded convergence theorem, and also by reminding the identity ; for example,

Here and in the sequel, the asterisk means that it holds uniformly over each compact subset of . To prove the remaining

| (2.59) |

we need some preliminary facts.

Step 4. Let

In this step, we will prove that

| (2.60) |

each limit being finite. Applying (2.53), we have

| (2.61) |

Let .

First we look at . The change of variable leads to , where

Obviously, for each

| (2.62) |

In order to apply the dominated convergence theorem to derive the limit of , we have to look at the behaviors of as and uniformly in small .

By means of (b) in Step 2 and (2.57), we have

| (2.63) |

the upper bound being Lebesgue integrable at infinity since . It follows form (2.56) and (b) that as , so that . Consequently, we have

| (2.64) |

the upper bound being Lebesgue integrable near the origin. Having (2.62), (2.63) and (2.64) in hand, we can apply the dominated convergence theorem to conclude that

In the same manner, we can deduce that

where . Thus we arrive at

Step 5. Now we prove (2.59), for which it suffices to show

| (2.65) |

By (2.60), the left-hand side of (2.65) equals

so that (2.65) follows on showing . We note that for any , and that, for any ,

| (2.66) |

By (2.40) and (2.66), straightforward computation with Fubini’s theorem gives .

Step 6. It remains to prove the positive definiteness of . To this end we note an alternative expression for : let and , then . Then, a computation similar to the one in Step 5 gives

so that

It suffices to show that, for any and the function

is positive in . We introduce the probability density

Using the identity

we get

Then, some elementary manipulations and Cauchy-Schwarz’s inequality lead to

where the last strict inequality does hold since is not a constant on . We thus get the positivity of , and the proof is complete. ∎

3 Estimation of stable Lévy process

The objective of this section is parametric estimation of some stable-process models based on high-frequency sampling.

3.1 Some preliminaries

The stable distributions form a pretty special subclass of general infinitely divisible distributions. There are several books containing a systematic account of the general stable distributions and the stable Lévy processes: Ber96 , IbrLin71 , JanWer94 , SamTaq94 , Sat99 , and Zol86 . See also BorHarWer05 for discussion from financial point of view.

The -stable Lévy process is characterized by

| (3.1) |

with the stable index , the scale , the degree of skewness , and the deterministic trend ; then, we will write

For , the stable distribution is characterized by the Lévy measure plus a trend, where takes the form

with satisfying . The parameters and are related by the identities

which readily follow on invoking, e.g., (Sat99, , Lemma 14.11). Here we will focus on the non-Gaussian case (), so that for each

Remark 1.

We say that a stochastic process has the selfsimilarity, also referred to as the scaling property, if there exist positive constants and for which in distribution; the parameter is called the selfsimilarity (or Hurst) index. It is known that it is only the stable Lévy process that can have the selfsimilarity among all Lévy processes. Specifically, for each we have

| (3.4) |

In other words, if then

This implies that has the selfsimilarity (with index ) if and only if (resp. ) when (resp. ). Note that the right-hand sides of (3.4) are free of . This fact is particularly useful when attempting simulations on computer, since in order to simulate it suffices to have a recipe for generating -random numbers. Let us mention the highly efficient algorithm for generating univariate stable-random numbers (ChaMalStu76 and Wer96 ), based on which we can readily generate a discrete-time random sample .

Algorithm 2

Fix any .

-

0.

For , set

-

1.

Draw random numbers and independently from the uniform over and the exponential with unit mean, respectively, and then set

Then in both cases. (The original Eq.(3.9) of Wer96 contains the error: for the expression of when , we need the multiplicative constant in the numerator inside the logarithm.)

-

2.

Set

Then in both cases.

Remark 3.

Taking formally and in Algorithm 2 results in the Box-Muller transform for generating increments of a scaled Wiener process with drift. ∎

In the case where the Lévy measure is symmetric, we have

Denote by the density of the symmetric -stable distribution corresponding to the characteristic function ; we will use the shorthands

The following well-known facts will be frequently used later.

-

•

The map is everywhere positive and of class .

-

•

The relation for all and is valid, as easily seen from the Fourier inversion formula

In particular, .

-

•

For any , there exist constants such that

-

•

It follows from the series expansion of the density (e.g. (Sat99, , Remark 14.18)) that for any

(3.5) for some constant .

In the rest of this section we will proceed as follows. In Section 3.2, we will look at the local asymptotics for the log-likelihood function when the Lévy density is symmetric, and then Section 3.3 presents some practical moment estimators which are asymptotically normally distributed. In Section 3.4, we will formulate a practical estimation procedure when the Lévy density is skewed and the scale is time-varying. Sections 3.5 and 3.6 give some brief remarks concerning simple estimation of general -stable Lévy processes and locally stable Lévy processes, respectively.

3.2 LAN with singular Fisher information: symmetric jumps

This section is concerned with the LAN when we observe under the high-frequency sampling from a -stable Lévy process such that . The parameter of interest is

the parameter space being a convex domain with compact closure

It will turn out that, although the log-likelihood admits a LAN structure, the asymptotic Fisher information matrix is constantly singular whenever both the index and the scale are to be estimated (AitJac08 and Mas09_slp ). This asymptotic singularity is inevitable, so we are in a similar situation to the case of the Meixner Lévy process mentioned in Section 2.2.3.

For and , we write

| (3.6) |

According to the scaling property (3.4), the random variables under are i.i.d. with common distribution . The log-likelihood function of is

Let

| (3.7) |

We are assuming (1.5), hence as soon as .

Theorem 4.

Fix any . For each we have the stochastic expansion

where under with

| (3.8) |

where

| (3.9) |

both being finite. In particular, the Fisher information matrix is singular for any .

Proof 3.1.

We may and do assume without loss of generality. Fix any and in the sequel. Let and . Obviously we have , hence it suffices to verify Assumptions 2.11(b) and 2.11(c).

First we consider Assumption 2.11(b):

| (3.10) |

Put and

Then,

| (3.11) | ||||

| (3.12) | ||||

| (3.13) |

Since forms an i.i.d. array with common distribution , it is straightforward to deduce (3.10) by substituting (3.11), (3.12) and (3.13) in

Here, we note that the finiteness of the limit can be ensured by means of Schwarz’s inequality together with (3.5); in particular, we have since is odd.

Next we turn to verifying Assumption 2.11(c). Fix any . It follows from the expressions (3.11) to (3.13) that (note that depends on )

For the latter estimate we used the elementary fact: a positive function is bounded below and above if and only if . Thus we get

| (3.14) |

It remains to look at . It is straightforward, though a bit tedious, to get

From these expressions we can deduce as before that

which combined with (3.14) verifies Assumption 2.11(c), completing the proof. ∎

Remark 5.

We refer to DuM83 and the references therein for the asymptotic normality in the low-frequency sampling case, where the Fisher information matrix is non-singular. As long as the high-frequency sampling is concerned, the constant asymptotic singularity also emerges in the case of -stable subordinators (see Mas09_slp ), and we conjecture that this is the case for the whole class of stable Lévy processes. ∎

Remark 6.

If is the Cauchy Lévy process such that , then the LAN holds at each with rate and Fisher information matrix ; we refer to (Mas09_slp, , Sections 3.4 and 4.2) for further exposition. Concerning the MLE of , Theorem 15 ensures the asymptotic efficiency as well as the uniform asymptotic normality . ∎

3.3 Symmetric Lévy measure

In this section, we discuss how to construct asymptotically normally distributed estimators of with non-singular asymptotic covariance matrix.

3.3.1 Scenario for constructions of easy joint estimators

As we have seen in Theorem 4, the MLE has a disadvantage for the joint estimation of the index and the scale . More suitable for practical use would be to adopt an -estimation based on moment fitting, with giving preference to simplicity of implementation over theoretical asymptotic efficiency.

In view of the scaling property of , the sample mean satisfies that

for each under . We immediately notice the following unpleasant features:

-

•

has infinite variance for each ;

-

•

is -consistent only when and ;

-

•

Since for , is not rate-optimal for estimating (see Theorem 4).

Hence the sample mean is of rather limited use as an estimator of , and we need something else. In what follows, we will prove that the sample median based estimator (equivalently, the least absolute deviation estimator) of attains the optimal rate whatever is. Then, it will be used to construct an asymptotically normally distributed joint estimator of , which has a non-singular asymptotic covariance matrix in compensation for the optimal -rate of convergence in estimating .

In the rest of this section we fix a as the true value, and the stochastic convergences are taken under .

In order to construct estimators via moment fitting, we will of course make use of the law of large numbers for of (3.6):

| (3.15) |

for suitable functions . The point here is two-fold: first, we can replace the unknown in (3.15) by the sample median (to be defined later) by virtue of the forthcoming Theorem 7; second, applying the delta method suitably we can eliminate the effect of involved in the summand . Specifically, we will consider the two moment-matching procedures:

-

•

the logarithmic moments and ;

-

•

the lower-order fractional moments and for .

3.3.2 Median-adjusted central limit theorem

Here we step away from the main context, and prove a simple yet unusual central limit theorem, which will play an important role later on.

The setting we consider in this section is as follows. Let be an i.i.d. sequence of -valued random variables with common continuous Lebesgue density , and let denote the sample median of with odd , i.e.,

where denotes the ordered sample. Let be a measurable function. The objective here is to derive a central limit theorem for where

and denotes the median of . The form of , where the term is eliminated from the sum, enables us to deal with cases where cannot be defined, such as and for some .

If happens to be sufficiently smooth and integrable and if , then Taylor’s formula and the stochastic expansion for (e.g., (vdV98, , Example 5.24)) yield that

| (3.18) |

where , for which we can readily apply the usual central limit theorem. However, it is not so clear what will occur when is not smooth enough. Theorem 7 below clarifies that we do have a central limit theorem in that case as well, provided that satisfies a mild smoothness assumption.

Theorem 7.

Assume that

- (a)

-

is of class and admits a unique median for which , and there exist a constant and a Lebesgue integrable function such that

- (b)

-

.

Then, we have

| (3.19) |

as , where is given by

Theorem 7 allows the function to be non-differentiable. If admits a finite variance, , and , then the claim of Theorem 7 reduces to the result of Zeigler Zei50 since we have .

Proof 3.2 (Theorem 7).

Let denote the characteristic function of the random variable on the left-hand side of (3.19), and fix any in the sequel. Write

Then we have

| (3.20) |

We will show that .

The joint distribution admits the density

| (3.21) |

and moreover the variables form a Markov chain, so that and are independent conditional on ; see (DavNag03, , Chapter 2). Substituting (3.21) in (3.20) and then changing the order of the integrations so that the integration with respect to is carried out last, we get

| (3.22) |

Put , then and the integration by parts for the Lebesgue-Stieltjes integral yields that . Repeating this inductively and also handling in a similar manner, we get

Substituting these two expressions in (3.22) and then going through the change of variable , we can continue as follows:

| (3.23) |

We know Stirling’s formula , hence it suffices to look at the integral .

Let , with the standard convention for . Then

| (3.24) | ||||

| (3.25) |

Pick a constant such that , and introduce the event . Since , (3.24) gives

hence . Moreover, we have whenever , which together with (3.25) implies that . To apply the dominated convergence theorem for , it remains to look at the point-wise convergence of .

Fix any and let be large enough so that . First we look at . Divide the domain of integration as

| (3.26) |

For brevity, we write , so that . Using the inequality

and the identity , we have

| (3.27) |

Here, the second equality follows from the estimate and the assumption (a):

For we proceed in a similar manner to the above:

| (3.28) |

Combining (3.26), (3.27), and (3.28) gives

| (3.29) |

where

We deal with in the same way: dividing the domain of integration as , we get

| (3.30) |

where

From (3.29) and (3.30), we arrive at

| (3.31) |

Let us obtain the limit of the part in (3.31). Direct computation gives

Under the assumption (a) we can apply the dominated convergence theorem to conclude that

| (3.32) |

Making use of a similar argument for the integrals (plugging in , , and so on), we can proceed as

| (3.33) |

where we wrote , , and .

3.3.3 Rate-efficient sample median

Let us return to our model. We will keep to set in what follows. Denote by the order statistics of the -i.i.d. array : a.s. Let denote the sample median of and

| (3.35) |

Observe that the central limit theorem (3.19), or the standard asymptotic theory for the least absolute deviation estimator, gives

This means that the pretty simple statistic serves as a rate-optimal and asymptotically normally distributed estimator of . We note that the unbiasedness of follows from the argument (Zol86, , p.241).

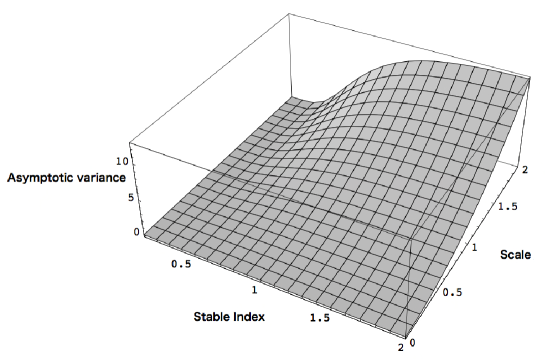

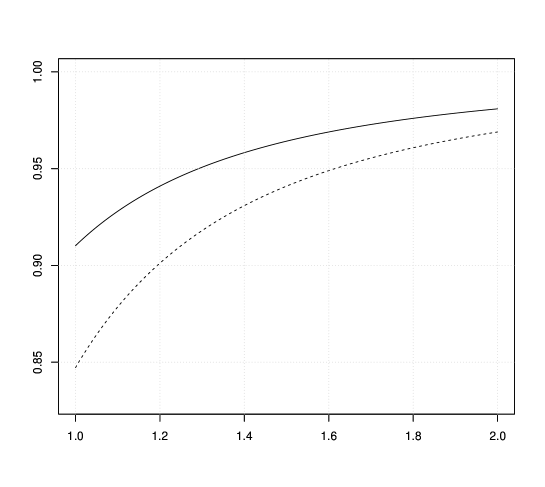

Figure 1 shows the asymptotic variance of . It is expected that the estimator shows good performance especially for small , since the rate of convergence of is then faster than with the asymptotic variance being quite small; for fixed, the function decreases to zero as .

Unlike with the Gaussian case we may consider a bounded-domain asymptotics (i.e. ) for estimating , while the optimal rate may become arbitrarily slow as gets close to ; we have if . This is in accordance with the fact that we need for consistent estimation of the drift in the Gaussian case ().

3.3.4 Preliminary formulation for estimating and

By the definition, for each

Let be measurable functions symmetric around the origin such that

A direct application of Theorem 7 with yields that

| (3.39) | ||||

| (3.43) |

where

and the asymptotic covariance matrix is given by

| (3.44) |

For convenience, we introduce the notation for the second leading principal submatrix of :

| (3.45) |

Having (3.43) in hand, we can apply the delta method. Assume that the function has an inverse at , and let denote a solution of the estimating equation

| (3.46) |

which uniquely exists with -probability tending to ; note that (3.46) is free of the unknown quantity since we have replaced it by . Let

| (3.47) |

Then we obtain the joint estimator such that

| (3.57) | ||||

| (3.58) |

where, in view of (3.45) and (3.47), the asymptotic variance is block diagonal:

| (3.59) |

Here are some remarks on (3.58).

-

•

The estimator so constructed is rate-efficient for , while not so for (recall Theorem 4).

-

•

The estimations of and are asymptotically independent.

-

•

Thanks to the -consistency of and (1.5), we have , so that . Then we can readily get the -confidence interval about :

with denoting the upper th percentile of .

In order to make use of (3.58), we are left to computing for each specific choices of , .

3.3.5 Logarithmic moments

Set

The distribution admit finite logarithmic moments of any positive order, the first two being given by

where () denotes the Euler constant; see (NikSha95, , p.69). Write for the ordered . Solving the corresponding (3.46) gives the explicit solutions

| (3.60) | ||||

| (3.61) |

Observe that the unknown factor “” involved in were cancelled out in the computation of , making the quantities (3.60) and (3.61) usable.

Let us compute the corresponding . We denote by and () the mean and th central moments of with , respectively. Then,

where denotes Riemann’s zeta function; . From (3.44), we get , , and . Further, we note that , and that

Therefore is positive definite. After some computations we obtain the explicit expressions for the matrix :

Finally using the continuity of , we arrive at the following.

Theorem 8.

Remark 9.

Sometimes it would be more convenient to take the logarithm in estimating the positive quantity for approximate normality of in moderate sample size:

| (3.67) |

The second leading principal submatrix of the asymptotic covariance matrix is free of , hence a function only of . We also note that the variance-stabilizing transform for is available: we have for

Moreover, since for , we see that

which satisfies that , is an unbiased estimator of . ∎

Remark 10.

If we beforehand know the true value of for some reason, then it is possible to construct a rate-efficient estimator of simply via the logarithmic-moment fitting. In fact, simple manipulation leads to the relation

where , but from Theorem 7 we know that the left-hand side tends in distribution to . It follows from Slutsky’s theorem that

| (3.68) |

can serve as an asymptotically normally distributed rate-efficient estimator. As is expected, the estimator exhibits excellent finite-sample performance; see Tables 1 and 2 in Section 3.3.7. ∎

3.3.6 Lower-order fractional moments: power-variation statistics

Now let set

in applying (3.58); we can also pick a , but do not consider it here. Especially when , this setting is related to the power-variation statistics applicable to a general class of semimartingales driven by a stable Lévy process; see CorNuaWoe07 and Tod13 together with their references. When concerned with joint estimation of , we should be careful in applying the power-variation result directly because the effect of may not be ignorable.

We know that where (e.g., (NikSha95, , Section 3.3))

Using Theorem 7 together with the present choice of we obtain a moment estimator of as a solution to

| (3.69) |

The solution takes the convenient form:

| (3.70) |

where

The factor “” in (3.69) can be effectively cancelled out in the first equation in (3.70). We can see that, for each , the right-hand side of the first one in (3.70) is a constant multiple of the map

Since this map is strictly increasing in , it is straightforward to find the root by a standard numerical procedure.

Let ; recall that denotes the digamma function. Then, the asymptotic covariance matrix in the present case can be explicitly computed as follows:

We can prove that is positive definite for any admissible , for the details of which we refer to (Mas09_slp, , Section 3.2).

Theorem 11.

Fix any and and define

| (3.71) |

where is a solution of (3.70). Then,

| (3.72) |

where is positive-definite.

3.3.7 Simulation experiments

In this section, we will first make some comparisons between the asymptotic covariances and given in Sections 3.3.5 and 3.3.6, respectively, and then observe finite-sample performance of our estimator through simulation experiments.

Comparing asymptotic variances.

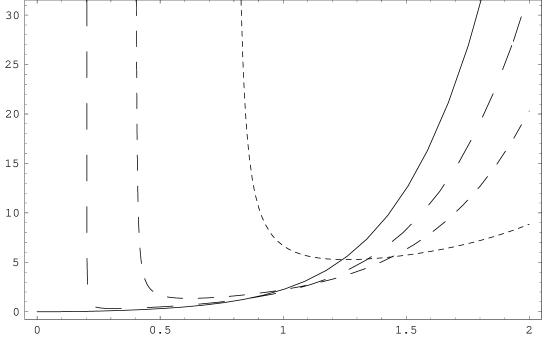

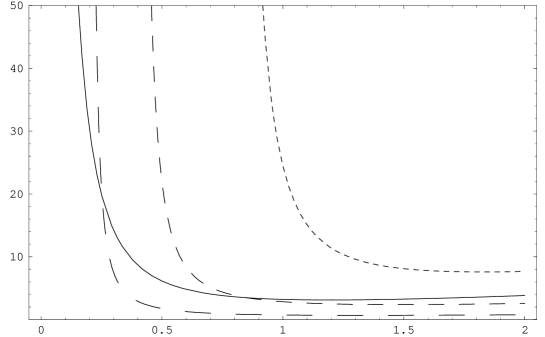

For conciseness, we will focus on comparisons between “ and ” and “ and ” individually. The function has a simple structure, while the dependence structure of on is somewhat more messy. According to the construction of , the value for a given diverges as decreases. Figure 2 shows plots of and on for and ; we refer to Tod13 for plots of the asymptotic variances in estimation of the stable-index and the integrated-scale parameters in a general class of pure-jump Itô-process models.

From Figure 2, we can observe the following.

-

•

Concerning : the asymptotic performance of monotonically changes with over , better for smaller and worse for larger . Further, the asymptotic performance of gets worse for smaller ; more precisely, the function on takes a unique minimum around , increases to a finite value as and to infinity as .

-

•

Concerning : we expect that smaller (resp. larger) leads to smaller asymptotic variance of for smaller (resp. larger) , the thresholds lying in the region . In contrast, given any , smaller leads to better performance of .

For implementation we have to fix the value a priori when applying , the permissible zone of which depends on the unknown . We will briefly discuss this point based on simulation results. As a matter of fact, it will turn out that selection of actually has non-negligible influence on the behavior of .

We have remarked that given a , the asymptotic behavior of should be better for smaller . This is, however, only based on the expressions of the asymptotic variance. Finite-sample performance of the estimator must depend on that of , so that it may occur and indeed we will see shortly that, e.g., behaves better than for behaving better than .

Setting and results.

We will observe different finite-sample behaviors according to the true value of . In each simulation below, we generate independent estimates of the parameter, and tabulate corresponding sample means and sample root mean-square errors (RMSEs).

We take and for . In each trial except for the cases where , we tabulate the estimates

| (3.73) |

all of which are computed from a single realization of . We set and as well as for the true values and also () and () for the sampling schemes.

Tables 1 and 2 report the means and the RMSEs of the estimates (3.73) with different sample sizes , and , and the different true value of . Just for reference and the sake of comparison, each numerical result includes the rate-efficient , for which the scale is assumed to be known (see Remark 3.68); as was expected, surpasses by far all the other estimators of . In both of Tables 1 and 2, the best estimates for are , , , and , for and , respectively (the bold-letter elements). The performances for estimating seem to bear no relation to sampling frequency, while larger may lead to better finite-sample performance in estimation of . Both tables show that finite-sample performance of joint estimation of can exhibit a different feature from the individual comparison through the asymptotic variances. For instance, Figure 2 says that individually behaves best for , while is actually the best one in Tables 1 and 2. This would be due to the better behaviors of for .

| Case of | ||||||||

|---|---|---|---|---|---|---|---|---|

| True | ||||||||

| 0.8 | 501 | 0.807 (0.049) | 0.807 (0.050) | 0.809 (0.056) | 0.800 (0.013) | |||

| 1001 | 0.803 (0.034) | 0.803 (0.034) | 0.804 (0.039) | 0.800 (0.008) | ||||

| 2001 | 0.800 (0.024) | 0.801 (0.024) | 0.801 (0.028) | 0.800 (0.005) | ||||

| 1.0 | 501 | 1.010 (0.070) | 1.009 (0.066) | 1.009 (0.067) | 1.001 (0.018) | |||

| 1001 | 1.003 (0.048) | 1.003 (0.045) | 1.003 (0.046) | 1.000 (0.011) | ||||

| 2001 | 1.003 (0.033) | 1.003 (0.033) | 1.003 (0.033) | 1.000 (0.007) | ||||

| 1.5 | 501 | 1.526 (0.162) | 1.518 (0.130) | 1.514 (0.112) | 1.514 (0.100) | 1.500 (0.031) | ||

| 1001 | 1.516 (0.115) | 1.511 (0.093) | 1.508 (0.080) | 1.507 (0.073) | 1.500 (0.018) | |||

| 2001 | 1.505 (0.081) | 1.504 (0.066) | 1.504 (0.058) | 1.504 (0.053) | 1.500 (0.011) | |||

| 1.8 | 501 | 1.857 (0.288) | 1.804 (0.151) | 1.807 (0.133) | 1.809 (0.109) | 1.801 (0.042) | ||

| 1001 | 1.824 (0.189) | 1.804 (0.125) | 1.805 (1.108) | 1.805 (0.085) | 1.799 (0.024) | |||

| 2001 | 1.815 (0.133) | 1.807 (0.095) | 1.807 (0.081) | 1.805 (0.062) | 1.800 (0.016) | |||

| True | ||||||||

| 0.8 | 501 | 0.518 (0.178) | 0.521 (0.200) | 0.531 (0.306) | -0.500 (0.050) | |||

| 1001 | 0.511 (0.139) | 0.513 (0.147) | 0.516 (0.181) | -0.500 (0.006) | ||||

| 2001 | 0.513 (0.109) | 0.513 (0.115) | 0.517 (0.139) | -0.500 (0.003) | ||||

| 1.0 | 501 | 0.511 (0.152) | 0.510 (0.147) | 0.511 (0.155) | -0.497 (0.036) | |||

| 1001 | 0.511 (0.120) | 0.511 (0.116) | 0.512 (0.123) | -0.502 (0.025) | ||||

| 2001 | 0.504 (0.093) | 0.503 (0.089) | 0.503 (0.095) | -0.500 (0.018) | ||||

| 1.5 | 501 | 0.508 (0.134) | 0.504 (0.107) | 0.502 (0.094) | 0.501 (0.098) | -0.501 (0.180) | ||

| 1001 | 0.504 (0.111) | 0.503 (0.090) | 0.502 (0.080) | 0.502 (0.080) | -0.503 (0.093) | |||

| 2001 | 0.508 (0.095) | 0.504 (0.076) | 0.503 (0.067) | 0.501 (0.067) | -0.504 (0.014) | |||

| 1.8 | 501 | 0.508 (0.144) | 0.513 (0.095) | 0.507 (0.077) | 0.502 (0.062) | -0.484 (0.306) | ||

| 1001 | 0.509 (0.125) | 0.509 (0.089) | 0.505 (0.073) | 0.502 (0.059) | -0.510 (0.125) | |||

| 2001 | 0.505 (0.100) | 0.503 (0.075) | 0.501 (0.062) | 0.500 (0.048) | -0.501 (0.284) | |||

| Case of | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| True | |||||||||

| 0.8 | 501 | 12.021 | 0.806 (0.047) | 0.806 (0.048) | 0.807 (0.054) | 0.801 (0.017) | |||

| 1001 | 15.855 | 0.802 (0.033) | 0.802 (0.034) | 0.804 (0.038) | 0.800 (0.011) | ||||

| 2001 | 20.917 | 0.802 (0.024) | 0.802 (0.024) | 0.803 (0.027) | 0.800 (0.006) | ||||

| 1.0 | 501 | 12.021 | 1.012 (0.071) | 1.011 (0.067) | 1.012 (0.069) | 1.001 (0.022) | |||

| 1001 | 15.855 | 1.005 (0.048) | 1.005 (0.045) | 1.005 (0.046) | 1.002 (0.014) | ||||

| 2001 | 20.917 | 1.003 (0.033) | 1.003 (0.031) | 1.003 (0.033) | 1.000 (0.009) | ||||

| 1.5 | 501 | 12.021 | 1.529 (0.171) | 1.520 (0.135) | 1.516 (0.115) | 1.514 (0.099) | 1.502 (0.041) | ||

| 1001 | 15.855 | 1.508 (0.111) | 1.505 (0.090) | 1.504 (0.078) | 1.505 (0.071) | 1.500 (0.025) | |||

| 2001 | 20.917 | 1.508 (0.085) | 1.506 (0.069) | 1.505 (0.059) | 1.504 (0.053) | 1.501 (0.016) | |||

| 1.8 | 501 | 12.021 | 1.878 (0.308) | 1.812 (0.158) | 1.813 (0.139) | 1.813 (0.114) | 1.803 (0.053) | ||

| 1001 | 15.855 | 1.824 (0.179) | 1.807 (0.122) | 1.807 (0.104) | 1.805 (0.080) | 1.801 (0.033) | |||

| 2001 | 20.917 | 1.811 (0.130) | 1.805 (0.096) | 1.804 (0.080) | 1.801 (0.062) | 1.800 (0.020) | |||

| True | |||||||||

| 0.8 | 501 | 12.021 | 0.509 (0.131) | 0.512 (0.144) | 0.519 (0.196) | -0.500 (0.012) | |||

| 1001 | 15.855 | 0.509 (0.106) | 0.509 (0.112) | 0.510 (0.131) | -0.500 (0.008) | ||||

| 2001 | 20.917 | 0.504 (0.081) | 0.504 (0.084) | 0.504 (0.098) | -0.500 (0.005) | ||||

| 1.0 | 501 | 12.021 | 0.503 (0.119) | 0.503 (0.125) | 0.509 (0.272) | -0.499 (0.036) | |||

| 1001 | 15.855 | 0.504 (0.089) | 0.505 (0.086) | 0.505 (0.091) | -0.500 (0.025) | ||||

| 2001 | 20.917 | 0.501 (0.067) | 0.501 (0.065) | 0.501 (0.072) | -0.499 (0.018) | ||||

| 1.5 | 501 | 12.021 | 0.503 (0.102) | 0.501 (0.083) | 0.501 (0.074) | 0.500 (0.072) | -0.498 (0.137) | ||

| 1001 | 15.855 | 0.507 (0.084) | 0.504 (0.068) | 0.503 (0.060) | 0.502 (0.061) | -0.500 (0.110) | |||

| 2001 | 20.917 | 0.502 (0.069) | 0.501 (0.056) | 0.501 (0.049) | 0.501 (0.047) | -0.505 (0.084) | |||

| 1.8 | 501 | 12.021 | 0.497 (0.115) | 0.507 (0.075) | 0.503 (0.062) | 0.500 (0.051) | -0.501 (0.199) | ||

| 1001 | 15.855 | 0.053 (0.087) | 0.504 (0.062) | 0.502 (0.051) | 0.501 (0.040) | -0.493 (0.171) | |||

| 2001 | 20.917 | 0.054 (0.073) | 0.503 (0.055) | 0.502 (0.045) | 0.502 (0.035) | -0.505 (0.153) | |||

Though omitted here, we could also observe that the logarithmic transform of the estimators of mentioned in Remark 9 could gain accuracy of the normal approximations for in finite-sample. Further, we could observe reasonably accurate normal approximation of upon a suitable choice of within our estimators.

Some practical remarks. In practice, we may roughly proceed as follows: first we apply which has no fine-tuning parameter. Then, building on the estimated values and taking the interrelationship of and , we apply anew with a suitable choice of , or keep using if the estimate of is small. In many applications in practice, the case of , i.e., finite-mean case, may be relevant. Then, we may simply adopt from the beginning with a small such as , and then adaptively change according to the estimated value of (e.g., pick if the first estimate of is greater than ).

3.4 Skewed Lévy measure with possibly time-varying scale

In the previous section, we considered a joint estimation of the index, scale, and location parameters when the Lévy density is symmetric. There we have seen that the sample median based estimator is rate-efficient. The primary objective of this section is to provide a practical moment estimator of a process of the form where is a possibly skewed strictly stable Lévy process without drift and is a positive càdlàg process independent of . We will consider estimation of integrated scale when the scale parameter is time-varying. The topic of this section is based on Mas10 ; a closely related work is (Tod13, , Section 4).

Our estimation procedure utilizes empirical-sign statistics and realized multipower variations (MPV for short; see Section 3.4.2). Its implementation is quite simple and requires no hard numerical optimization, hence preferable in practice. Using MPVs essentially amounts to the classical method of moments with possibly random targets. Several authors investigated asymptotic behaviors of MPVs for estimating integrated-scale quantities of pure-jump models. Among others, we refer to (BarShe05, , Section 6), CorNuaWoe07 , Tod13 with the references therein, and Woe03-3 ; in all the papers, the underlying model is driven by either a stable or locally stable Lévy process (see Section 3.6 for the definition of the latter). It will turn out that estimation of the integrated time-varying scale by substituting a -consistent estimator of into the MPV statistics will lead to the slower rate of convergence (Section 3.4.4).

3.4.1 Setup and description of estimation procedure

To describe the model setup, we will adopt another parameterization of a strictly -stable distribution: with a slight abuse of notations, we write for if

| (3.74) |

Instead of the skewness parameter we now have the positivity parameter , whose range of value is given as follows:

For , the parametrizations (3.1) and (3.74) are linked by the one-to-one relation

| (3.75) |

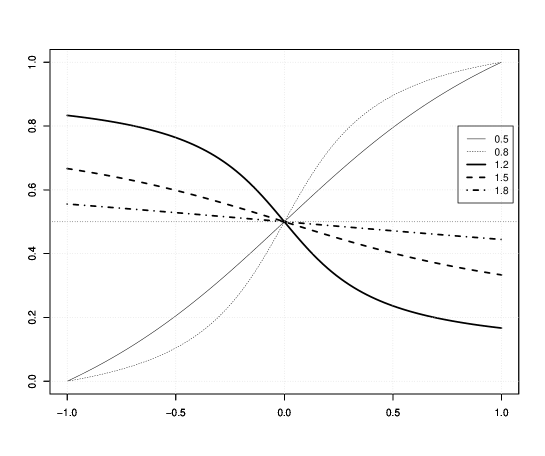

For any fixed , is monotonically decreasing on as a function of . Hence and have opposite signs for , while the same signs for ; Figure 3 illustrates this point.

The primary reason why we have chosen the parametrization (3.74) is that, as is expected from Figure 3, estimation performance of based on the empirical sign statistics, which we will make use of later, is destabilized for close to : that is to say, the slope of the curve gets gentler for larger , so that a small change of the empirical sign statistics results in a wide gap between the estimate of and the true value. Also, note the difference between the scale parameters of (3.1) with and (3.74), which will turn out to be convenient for considering time-varying scale in a unified manner.

Let be a -stable Lévy process such that

| (3.76) |

Note that according to the scaling property, we have for each . We will focus on the case where

| (3.77) |

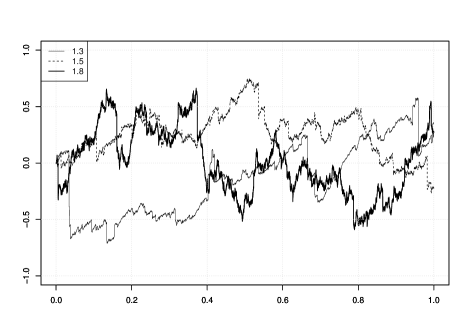

so that jumps are not one-sided and are of infinite variation; nevertheless, it will be obvious from the subsequent discussion that our estimation procedure remains in force for too. Figure 4 shows typical sample paths of .

We now accommodate a possibly time-varying scale process , which is assumed to be càdlàg adapted and independent of , and also bounded away from zero and infinity. Let be the process given by

| (3.78) |

where the stochastic integral is well-defined since ; see, e.g., JacShi03 and/or Pro05 .

Remark 12.

We may equivalently (in distribution) define of (3.78) by the time-change representation with “clock” process :

Such kind of distributional equivalence can occur only for stable among general Lévy processes: see KalShi01 for details. It is a matter of no importance that the target time period is from the very beginning: enlarging the length of the period is reflected in making larger through the process . ∎

In the sequel, we fix a true value of . Note that the scaling property and the independence between and give the -conditional distribution

Our objective is to estimate the following quantities under (3.77) from a sample :

- (A)

-

when is constant;

- (B)

-

when is time-varying.

We will provide an explicit estimator of in each case, which is asymptotically (mixed) normal at rate . The case (A) is obviously included in the case (B), however, the case (B) will exhibit an essentially different feature from the case (A), requiring a separate argument. In both cases:

-

•