On the Complexity of Bandit Linear Optimization

Abstract

We study the attainable regret for online linear optimization problems with bandit feedback, where unlike the full-information setting, the player can only observe its own loss rather than the full loss vector. We show that the price of bandit information in this setting can be as large as , disproving the well-known conjecture [9] that the regret for bandit linear optimization is at most times the full-information regret. Surprisingly, this is shown using “trivial” modifications of standard domains, which have no effect in the full-information setting. This and other results we present highlight some interesting differences between full-information and bandit learning, which were not considered in previous literature.

1 Introduction

We consider the problem of bandit linear optimization, which is a repeated game between a player and an adversary. At each round the player chooses a point from a compact subset of , and simultaneously the adversary chooses a loss vector (under some regularity assumptions described in Sec. 2). The player incurs a loss , and can observe the loss but not the loss vector . The player’s goal is to minimize its expected cumulative loss, , where the expectation is with respect to the player’s and adversary’s possible randomization. The performance of the player is measured in terms of expected regret, defined as

| (1) |

Bandit optimization has proven to be a useful abstraction of sequential decision-making problems under uncertainty, such as multi-armed bandits and online routing (see [4] for a survey). Moreover, using online-to-batch conversion techniques, algorithms for this setting can be readily applied to derivative-free stochastic optimization, where our goal is to stochastically optimize an unknown function given only noisy views of its values at various points.

The attainable regret in the bandit setting can be compared to the attainable regret in the full-information setting, where is revealed to the player after each round. Clearly, since the player receives less information in the bandit setting, the attainable regret will be larger. This degradation is known as the “price of bandit information” [9], and characterizing it for general domains has remained an open problem. However, the standard conjecture and common wisdom (as articulated in [9]) is that for linear optimization, this price is at most a multiplicative factor, where is the dimension. Indeed, as far as we know, this holds for all domains that have been previously studied in the literature:

-

•

When the domain is the corners of the -dimensional simplex (a.k.a. multi-armed bandits setting), the minimax optimal regret is , vs. in the full-information setting.

- •

-

•

When the domain is the unit Euclidean ball, there is an algorithm with regret , vs. in the full-information setting. [5]

-

•

There is an lower bound for a certain non-convex subset of the hypercube (a cartesian product of -dimensional spheres) [8]. The corresponding full-information regret bound is .

We note in passing that there are other partial-information settings where the situation is different, but these are distinct from the bandit linear optimization setting we focus here (e.g. non-linear bandit optimization [13] or using different information feedback, e.g. [7]).

The main contribution of this paper is disproving this conjecture, and showing that the price of bandit information for online linear optimization can be as large as rather than . We do this by proving that the regret upper bound for the Euclidean ball is surprisingly brittle, and the attainable regret becomes after “trivial” changes of the domain which do not matter at all in the full-information setting. These changes include (1) Shifting the ball away from the origin, and (2) Taking a simple convex subset of the Euclidean ball with a “flat” boundary, such as a cylinder or a capped Euclidean ball. We also explain how our techniques can be potentially applicable to other domains. Since the full-information regret in these cases is , this establishes a price of bandit information on the order of . This gap is tight as worst-case over all domains (or all convex domains), because for any domain, it is possible to get regret [5, 12], and the attainable regret in the full-information case is generally at least .

We note that our lower bounds hold even against a stochastic adversary, which chooses loss vectors i.i.d. from a given distribution. In such a setting, any algorithm attaining regret can be used to find an -optimal point after rounds (as described later). This allows us to re-phrase our result in the following manner, which might be conceptually interesting: If the price of bandit information was , then to find an -optimal point, we would need times more rounds in the bandit setting, compared to the full-information setting (e.g. vs. ). This is intuitively very appealing: Each round, we get to see only “ as much information” in the bandit setting (a single scalar compared to a -dimensional vector), hence we need times more rounds to get the same amount of information and return a point of similar accuracy. Unfortunately, our results show that there are cases where the price of viewing scalars vs. -dimensional vectors is quadratic in (e.g. vs. ). So in some sense, the number of rounds required and the amount of information per round cannot be traded-off without significant loss.

A second contribution of our paper lies in disproving another common intuition: Namely, that any regret lower bounds with respect to a given domain automatically extend to a its convex hull . For example, this has been implicitly used to argue that the regret lower bound for the boolean hypercube in [1] extends to the convex hypercube [4, 12]). Again, this is generally true for online linear optimization in the full-information setting, since the optimal points in lie in , and the player can always simulate playing over via randomization over . However, in the bandit setting the change in domain also changes the information feedback structure in non-intuitive ways. For example, if the loss vectors are binary and is the corners of the simplex (a.k.a. multi-armed bandits), there is a well-known regret lower bound [3]. However, when we convexify the domain and take to be the simplex, then it is possible to get regret - same as in the full-information setting! In fact, such a result can be shown to hold for most continuous domains. We emphasize that these regret upper bounds are achieved only for binary (or finitely-valued) losses, and in a manner which is of little practical value. However, they do demonstrate that one has to be careful when extending bandit optimization results from a finite domain to its convex hull, and that loss vectors supported on a finite set are not appropriate to prove bandit lower bounds for continuous domains. In any case, for completeness, we provide minimax optimal regret bounds for the simplex and the hypercube, using the techniques we develop here. For the hypercube, this bound is , and formally establishes that this is the minimax optimal regret for bandit linear optimization over convex domains.

1.1 Lower Bound Techniques and Main Ideas

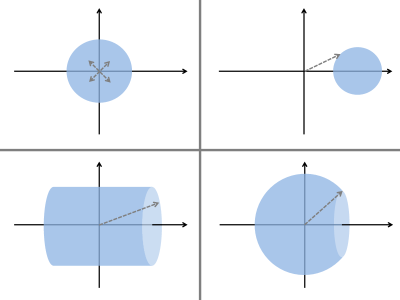

In this subsection, we informally sketch the technical ideas used to get our lower bounds. The various domains we discuss below are sketched in Figure 1. The result on continuous domains and finitely-valued losses is a bit orthogonal, and described separately in Sec. 5.

As mentioned earlier, our lower bounds are actually proven for the easier setting of stochastic bandit linear optimization, where the adversary is constrained to sample each loss vector i.i.d. from the same distribution. Moreover, some of the bounds also apply to the easier goal of minimizing error rather than regret, which may be of independent interest: In this case, the player may choose arbitrarily, observing , and then needs to return a vector which minimizes the expected error

| (2) |

where . This goal is more relevant in a stochastic optimization setting, where we attempt to optimize a stochastic linear function based on querying its values at various points. It is easy to show that any algorithm, attaining expected regret of after rounds, can attain an error by returning the vector . Thus, any lower bound for minimizing error in a stochastic setting implies the same lower bound on minimizing regret and a possible non-stochastic setting, times a factor. For example, a error lower bound implies a regret lower bound.

For the goal of minimizing error in a stochastic setting, it turns out that there is a simple strategy attaining error under appropriate conditions: In each round, we randomly sample from some hypercube centered around the origin, and use it to create an unbiased estimate of the loss vector, with variance . Repeating this for rounds and averaging, we get an estimate of the expected loss vector , which is unbiased and with variance . We then return the point , leading to an error bound.

Unfortunately, this method breaks down if we cannot sample from such an origin-centered hypercube. In particular, if the variance of for any in the domain is lower bounded by a constant (independent of the dimension), then the variance of the estimator becomes rather than . Clearly, this is not true when can be arbitrarily close to the origin: If , then the variance of is always zero. However, it can happen when the domain is bounded away from the origin. Using this key observation together with canonical information-theoretic tools (i.e. reduction to a hypothesis testing problem), we can show a error lower bound for a simple domain bounded away from the origin, such as a shifted Euclidean ball. Due to the relationship between error and regret, this leads to an regret lower bound for such domains.

Another way to force to have constant variance, even if the domain contains the origin, is when the player must pick points far away from the origin most of the time. This cannot be enforced when the goal is minimizing error. However, when the goal is minimizing regret, then we can construct a situation where any point close to the origin leads to a large regret. In that case, either the player picks points close to the origin, and gets large regret, or picks points far from the origin, leading to the variance of being large. This is a lose-lose situation, and carefully formalizing it leads to a regret lower bound, similar to the shifted Euclidean ball setting. We formally show this for a cylindrical domain (see figure 1) as well as a hypercube, but the proof technique appears applicable to other domains, such as a capped Euclidean ball, or more generally any domain with a flat surface orthogonal to the origin. In all these cases, the adversary strategy is to choose an expected loss vector at random from the flat surface, and introduce a constant amount of stochastic noise in the orthogonal dimension. Since the flat surface is far from the origin, the player must deal with constant variance if it wishes its regret to be small.

Although our lower bounds are shown for particular domains, we believe that the properties we identified – distance from origin, variance of the losses, and flatness of parts of the domain boundary – can play a key role in characterizing the attainable regret for any given domain.

2 Preliminaries

We use bold-faced letters to denote vectors (e.g. ). We let denote the Euclidean norm, and the -norm. We also define the function as

When is a symmetric convex set, then is the dual norm to the norm whose unit ball is , hence the notation. However, we will use this notation even when is not convex and symmetric. We also define to be the multivariate Gaussian distribution with mean and covariance matrix , and let denote the identity matrix.

As discussed in the introduction, our results focus on bandit linear optimization in a stochastic setting, where the loss vectors are assumed to be drawn i.i.d. from an unknown distribution with mean . In this setting, the expected regret (as defined in Eq. (1)) can be equivalently written as

| (3) |

Clearly, if any distribution is allowed, then the inner products above can be unboundedly large, and no interesting regret bound is possible. To prevent this, it is standard in the literature to assume that is essentially bounded. Formally, we assume that satisfies the following two conditions:

-

•

-

•

for all .

We denote any such distribution as a “valid” distribution. The latter condition requires to have sub-Gaussian tails (or more precisely, tails dominated by a standard Gaussian random variable), and is a slight relaxation of the standard ‘dual’ setting (e.g. [5, 1]), where it is assumed that with probability . We choose this purely for technical convenience, since it allows us to use Gaussian distributions for , and does not materially affect algorithmic approaches we’re aware of. Moreover, in terms of lower bounds, we lose almost nothing by this relaxation: Any lower bound for our setting can be transformed into an equivalent lower bound in the standard dual setting (where with probability ), at the cost of a factor. See Appendix A for details.

3 Expected Error

We begin by considering the attainable performance in terms of expected error (Eq. (2)), recalling that error lower bounds immediately transfer to regret lower bounds.

To motivate our results, let us show that it is easy to obtain error upper bounds under a mild condition. To do so, suppose that contains the set for some , and consider the following simple player strategy: In each round , the player draws a vector uniformly at random, computes (possible since ), and computes the estimator . It is easy to verify that

| (4) |

so is an unbiased estimator of with variance bounded by . After rounds, the player computes , and returns .

Theorem 1.

Suppose that is a subset of the unit Euclidean ball , and contains for some . Then for any distribution over loss vectors , such that and with mean , the player strategy described above satisfies

We note that [5] provides a more sophisticated algorithm with regret, even against a non-stochastic adversary.

Proof.

The idea of the proof is that since are unbiased estimate of , which are themselves random variables with mean , then their average will be a good estimate of , hence minimizing will approximately minimize .

More formally, let . Also, recall that any satisfies , and therefore for all by the Cauchy-Schwartz inequality. Finally, recall that . Using these observations, we have

and therefore

| (5) |

where the last step is by Jensen’s inequality. Recalling the definition of , this equals

According to equation Eq. (4), , but we also have , and therefore , so each summand in the equation above is zero-mean. Moreover, they are i.i.d. since each is computed based on the independent realization . Therefore, the equation above equals

which by Eq. (4) is at most as required. ∎

For example, a special case of the theorem above implies an error upper bound for the origin-centered unit Euclidean ball. The key property used was the ability to query at a random point in (a scaled origin-centered Boolean hypercube), which allowed computing an unbiased estimator of each with variance .

This observation leads us to guess that when we cannot query from such a set, the learning problem may be harder. One case in which querying such a set is impossible is when is convex and bounded away from the origin. In a full-information learning setting, shifting away from the origin doesn’t increase the learning complexity in general. Surprisingly, in the bandit setting this turns out to make a huge difference: Even for the unit Euclidean ball, shifting it so it doesn’t include the origin is sufficient to make the attainable error jump from to :

Theorem 2.

Suppose that , and let , where . Then for any player strategy returning , there exists a valid distribution over loss vectors with mean such that

where is a positive universal constant.

The formal proof appears in Sec. 6, and we note that due to the rotational symmetry of our linear optimization setting, the same lower bound would hold for a Euclidean ball shifted in any other direction. Although the result is specifically for a shifted Euclidean ball, we conjecture that the result can be generalized to other domains as well, as long as they are sufficiently large and at a constant distance from the origin.

Although the notion of a domain not containing the origin may appear unusual at first, it can actually be necessary to model some common situations. One example is when the domain has a linear constraint bounding it away from the origin, such as the probability simplex or a convex hull of points lying in the same quadrant. As another example, suppose our losses actually take the form where is some noise or other bias term not controlled by the player. This is possible to model in the bandit setting, by adding a dimension and playing over the domain , using loss vectors of the form . But this leads to a domain bounded away from the origin. In fact, if is the origin-centered Euclidean ball, then the techniques of Thm. 2 readily imply a error lower bound for the domain .

As discussed earlier, the key idea in proving Thm. 2 is that we can construct a distribution where the variance of for any is lower bounded by a positive constant, independent of the norm of or the dimension. The effect of this is best seen in the estimation procedure described before Eq. (4): Recall that there we chose a query point where , in which case the conditional second moment of the estimator , where ,satisfies

| (6) |

Since , we see that scales with , and therefore Eq. (6) is , independent of . In contrast, if was forced to have constant positive variance, then Eq. (6) is at least . Moreover, if has bounded norm, then , so Eq. (6) would scale as rather than , eventually leading to an error bound scaling as rather than .

4 From Error to Regret

Having considered domains bounded away from the origin, it is natural to ask whether this is the only condition leading to regret lower bounds. If the domain does contain the origin, then because of Thm. 1, it seems unlikely to show such lower bounds by proving error lower bounds. However, we can exploit the fact that attaining small regret is harder than attaining small error. In this section, we show how in fact it can be strictly harder: We identify a situation which leads to regret lower bounds, even if the domain contains the origin, and even though better error upper bounds are possible.

Specifically, the following theorem demonstrates such a lower bound for a domain consisting of an origin-centered cylinder.

Theorem 3.

Suppose that , and let . Then for any player strategy, there exists a valid distribution over loss vectors with mean such that

for any , where is a positive universal constant.

Note that the bound is a bit weaker than Thm. 2, in that it only holds for sufficiently large . However, since this is a lower bound, it is still sufficient for proving that no algorithm will attain regret in general here.

The proof relies on the following construction: The adversary chooses a vector uniformly at random, and constructs a loss vector distribution, whose expectation is (with being a small scaling factor, on the order of if is sufficiently large), and where the first coordinate has constant Gaussian noise. It is possible to show that to get small regret, the player essentially needs to identify . This would have been possible if the player queried at points whose first coordinate is . However, since has a large negative weight on the first coordinate, then must be large to get small regret. But because of the stochastic noise in the first coordinate, this means that will have large variance. A formal analysis of this leads to a regret lower bound of the form

The idea now is that no matter how the first coordinates are chosen by the player, the regret will be large: If they are significantly smaller than , then the first term above will be on the order of . But if is almost , then the square root term will be small, again leading to a large regret. A careful analysis shows that the regret will always be .

Although a precise characterization is non-trivial, the proof technique appears to be potentially applicable to any domain with a flat surface, which is sufficiently large to contain the points for some constant and suitable scaling factor (possibly after rotating the domain around the origin). For example, the same proof technique would apply to a capped Euclidean ball, for some constant . The flatness of the surface seems to be important. To see this, let us understand why the proof breaks down, when instead of a cylinder or a capped ball, our domain is the origin-centered Euclidean unit ball (for which we know that we can get regret [5]). First, when is sufficiently large compared to , we choose on the order of (this is the regime which makes detecting information-theoretically hard). In that case, we have , and the optimal play is . However, with an origin-centered ball, the player doesn’t need to detect to get small regret: The player can go “further” along the first coordinate, and just play the fixed point every round. The total expected regret is then

where we used the fact (immediate by Taylor expansion) that for all . So, we see that instead of regret as in the case of a cylinder or capped ball, here the player can achieve a much smaller regret (assuming is sufficiently large). In fact, this regret bound is tight for our construction – carrying through the lower bound derivation as in Thm. 3, but for the origin-centered ball, yields an regret lower bound for sufficiently large .

5 Loss Vectors from a Finite Set

Many of the regret lower bounds shown in the literature for finite domains (such as for the corners of the simplex and for the boolean hypercube [3, 9, 1]) use loss vectors from a finite set (e.g. where each entry is binary). Based on analogues to the full information setting, it is often argued that these lower bound constructions also extend to the (continuous) convex hull of these domains. In this section, we point out that these analogues can be dangerous and generally do not hold.

In particular, the theorem below demonstrates a possibly surprising fact: If we perform bandit linear optimization over a continuous domain, and the loss vectors come from a finite set, then we can actually get the same regret as in the full information case – generally much smaller than the lower bound one would hope to achieve. This also holds for non-stochastic adversaries. We hasten to emphasize that the way we achieve this is “cheating” and not very useful in practice, since it heavily relies on the ability to perform arbitrary-precision computations. Nevertheless, it demonstrates that one has to be careful when extending bandit optimization results from a finite domain to its convex hull. Moreover, it shows that loss vectors supported on a finite set are not suitable to prove bandit lower bounds for continuous domains.

For simplicity, we will prove the result for the simplex and for binary-valued loss vectors, but from the proof it is easily seen to be extendable to other continuous domains in general (such as the hypercube ), as well as the loss vectors coming from any finite set.

Theorem 4.

Suppose is the probability simplex in , and suppose the loss vectors are from the set . Then there exist a deterministic player strategy in the bandit setting, such that for any adversarial strategy for choosing loss vectors ,

Proof.

The proof uses the following observation: In the setting described above, it is possible for the player to determine precisely by perturbing its chosen point by an arbitrarily small amount, and feed it into a deterministic full-information algorithm for this domain, such as hedge [11, 6]. Such algorithms attain regret, from which the result follows.

More precisely, suppose that at the beginning of round , the full-information algorithm determines that one should play point . Let , and define

where clips every entry of (in its decimal representation) to places after the decimal point. Note that for any , if we get , then we can determine precisely: We just need to look at the digits in locations after the decimal point. A small technical issue is that does not lie in the simplex , so it cannot be chosen by the player. To fix this, the player picks , which indeed lies in the simplex. Given the loss , we just multiply it by the known quantity to get , from which we can read off and feed it back to the full-information algorithm.

By standard regret guarantees (e.g. [11, 6])111Strictly speaking, these algorithms are phrased so as to minimize , but they can be easily converted to our notion of regret by feeding them with where is the all-ones vector., we therefore get that

| (7) |

To get a regret bound using the actual plays , we note that we can lower bound the left hand side of Eq. (7) by

| (8) |

and that

By definition of and the fact that is on the simplex, it is easy to verify that and that , so the above equals at most , and we can lower bound Eq. (8) by

Combining this with Eq. (7), we get that

as required. ∎

In light of this type of result, we are not aware of explicit minimax regret bounds for the simplex (or unit -norm ball) and the hypercube in the literature. For completeness, we provide such bounds below. Besides relying on continuous-valued rewards, the lower bounds require the techniques of Thm. 2 and Thm. 3: For the simplex, we provide an error lower bound relying on the fact that the simplex is bounded away from the origin; Whereas for the hypercube, we rely on it having a flat surface orthogonal to the origin. The constructions we use are slightly different though, due to the different shapes of the domains.

Theorem 5.

Suppose that , and let be either the simplex or the unit -norm ball . Then for any player strategy returning some , there exists a valid distribution over loss vectors with mean such that

where is a positive universal constant.

This leads to a regret lower bound, which matches the upper bound for the simplex attained with multi-armed bandit algorithms such as EXP3 [3].

Theorem 6.

Suppose that , and let . Then for any player strategy, there exists a valid distribution over loss vectors with mean such that

for any , where is a positive universal constant.

This regret lower bound matches the upper bound attained in [5] (using an algorithm which actually plays only on the corners of the hypercube).

6 Proofs

6.1 Proof of Thm. 2

To simplify notation, suppose that the game takes place in for some . We denote the first coordinate as coordinate , and the other coordinates as .

By Yao’s minimax principle, it is sufficient to provide a randomized strategy to choose a loss vector distribution , such that for any deterministic player, the expected error is as defined in the theorem. In particular, we use the following strategy:

-

•

Choose uniformly at random.

-

•

Use the distribution over loss vectors , defined as follows: is fixed to be (where is a parameter to be chosen later), and has a Gaussian distribution .

First, let us verify that any is a valid distribution. We have

and moreover, for any in the support of and for any ,

by the fact that and our assumption on . is normally distributed with mean zero and variance , from which it is easily verified that for all as required.

We now start the proof. For any fixed , recall that , and define

It is easily verified that is a minimizer of over . Therefore,

Since and , we can lower bound the above by

| (9) |

where is the probability with respect to the joint randomness of and . Since each is uniformly distributed on , we can lower bound each probability term as follows:

Plugging this back to Eq. (9), we get the lower bound

To continue, recall that we assume the player is deterministic, in which case is a function of the sequence of losses observed by the player over rounds. Letting denote the probability density function over , and denote the indicator of the event , we can rewrite the above as

| (10) |

Each integral represents the total variation distance between the densities and . By Pinsker’s inequality, it can be upper bounded as follows:

| (11) |

where is the Kullback-Leibler (KL) divergence between and . By the chain rule, this can be upper bounded in turn by

| (12) |

Since the player is deterministic, any values determine the point that the player will choose on round . Thus, the distribution of depends on the distribution of , as determined by . By definition of :

-

•

Under the condition , has a Gaussian distribution with mean , and variance (note that here we crucially use the domain assumptions on , which imply ).

-

•

Under the condition , has a Gaussian distribution with mean , and variance .

By a standard result on the KL divergence of two Gaussian distributions, we therefore have that Eq. (12) is at most

Recalling that this constitutes an upper bound on the left hand side of Eq. (26), we get

| (13) |

To get rid of the conditioning on , note that the total variation is symmetric, so again using Pinsker’s inequality, we can get a variant of Eq. (26) of the form

Using the same derivation as above, this leads to the upper bound

| (14) |

Combining Eq. (13) and Eq. (14), and using the elementary inequality and the fact that is uniformly distributed on , we get

| (15) |

Plugging this back into Eq. (10), we get an expected error lower bound of

which by Jensen’s inequality is at least

By definition of , we have that always, so we can lower bound this by

| (16) |

Let us now consider two cases:

-

•

If , then we choose (which ensures the condition ), and Eq. (16) equals .

-

•

If , then we choose , and Eq. (16) is lower bounded by .

Therefore, by choosing appropriately, we can lower bound Eq. (16) by . Since this lower bound holds for a domain in for any , we get a lower bound for a domain in for any , as required.

6.2 Proof of Thm. 3

As in the proof of Thm. 2, to simplify notation, we assume the game takes place in for some , so the domain is . We denote the first coordinate as coordinate , and the other coordinates as .

The proof uses a somewhat different loss vector distribution than that of Thm. 2, designed to force the algorithm to choose points far from and to one side of the origin to ensure small regret.

By Yao’s minimax principle, it is sufficient to provide a randomized strategy to choose a loss vector distribution , such that for any deterministic player, the expected error is as defined in the theorem. In particular, we use the following strategy:

-

•

Choose uniformly at random.

-

•

Use the distribution over loss vectors , defined as follows: has a Gaussian distribution (where is a parameter to be chosen later), and is chosen independently according to a Gaussian distribution . Note that this is different than the construction in the proof of Thm. 2, and the distribution of is not zero-mean. The idea is that will have to be close to most of the time to get low regret, hence the points queried are far from and to one side of the origin.

First, let us verify that any is a valid distribution. We have

Moreover, for any in the support of and for any , by the Cauchy-Schwartz inequality,

is normally distributed with mean and variance , and each is independently normally distributed with mean at most and variance , from which it can be verified using Gaussian tail bounds that

for all as required.

We now start the proof. Define the scalar and -dimensional vectors

For any fixed , recall that . It is therefore easily verified that is a minimizer of over . Recalling the formulation of regret in Eq. (3), we can write it as

| (17) |

By definition of the domain, each has norm at most , and therefore , which is their average, also has norm at most . Therefore, , so we can lower bound the second expectation above by

where is the probability with respect to the joint randomness of and . Plugging this back into Eq. (17), we get a regret lower bound of the form

These probabilities can now be lower bounded as in the proof of Thm. 2 (see the derivation following Eq. (9)), which imply that

| (18) |

where are the sequence of losses observed by the player over the rounds, and is the probability density function over . As in the proof of Thm. 2, we can now use Pinsker’s inequality and the chain rule to upper the integral as follows:

| (19) |

where is the KL divergence. Since the player is deterministic, any values determine the point that the player will choose on round . Thus, the distribution of depends on the distribution of , as determined by . By definition of :

-

•

Under the condition , has a Gaussian distribution with mean

, and variance . -

•

Under the condition , has a Gaussian distribution with mean

, and variance .

By a standard result on the KL divergence of two Gaussian distributions, we therefore have that Eq. (19) is at most

| (20) |

As in the proof of Thm. 2, we can also upper bound Eq. (19) using the reverse order of probabilities:

which leads to Eq. (19) being upper bounded by

| (21) |

Combining Eq. (20) and Eq. (21) and using the elementary inequality and the fact that is uniformly distributed on , we get

| (22) |

Plugging this back into Eq. (18), we get an expected error lower bound of

which by Jensen’s inequality is at least

By definition of , we have that always. Using this and recalling that , we can lower bound the above by

| (23) |

The trick now is to argue that not matter what are the values of , this lower bound will be large: Either will tend to be bounded away from , and then Eq. (23) will be large due to the first term; Or that will tend to be very close to , but then Eq. (23) will be large due to the second term. To make this precise, we use the following technical lemma:

Lemma 1.

For any integer , and for any , it holds that .

Proof.

Since both sides of the inequality are the same for and , we can assume without loss of generality, that , and prove that over this domain.

By algebraic manipulations, this inequality is equivalent to the assertion that , or equivalently,

Considering the domain of , the left hand side is non-positive only when , because of the third term, but in that regime and , and therefore

as required. ∎

Applying this inequality, we can lower bound Eq. (23) by

Recalling that is a free parameter, let us choose (which satisfies the assumption , since we assume ). We therefore get

| (24) |

Note that this expression is convex with respect to , and by differentiating, has an extremal point at

Since we assume , this point is non-positive, and therefore the minimum in Eq. (33) is attained at , where it equals

Since this lower bound holds for a domain in for any , we get a lower bound for a domain in for any , as required.

6.3 Proof of Thm. 5

By Yao’s minimax principle, it is sufficient to provide a randomized strategy to choose a loss vector distribution , such that for any deterministic player, the expected error is as defined in the theorem. In particular, we use the following strategy:

-

•

Choose uniformly at random.

-

•

Use the distribution over loss vectors , defined as (where is a parameter to be chosen later).

First, let us verify that any is a valid distribution. We have

and moreover, for any in the support of and for any , is Gaussian with mean and variance , from which it is easily verified that for all as required.

We now start the proof. For any fixed , recall that , and define . It is easily verified that is a minimizer of over . Also, let denote expectation assuming that , and recall that is chosen uniformly at random from . Therefore,

Define the reference distribution over loss vectors, which has zero-mean, and let denote expectation assuming the loss vectors are chosen from that distribution. Then we can lower bound the above by

| (25) |

where in the last inequality we used the fact that has -norm at most . Now, recall that we assume that the player is deterministic, hence is a deterministic function of the sequence of loss observations made by the player over rounds. Letting and denote the density functions with respect to respectively, we can upper bound the expectation differences in Eq. (25) as follows:

By Pinsker’s inequality, and the chain rule, this can be upper bounded by

| (26) |

where is the Kullback-Leibler (KL) divergence between and . Since the player is deterministic, any values determine the point that the player will choose on round . Thus, the distribution of depends on the distribution of :

-

•

Under (corresponding to ), has a Gaussian distribution with mean and variance .

-

•

Under (corresponding to ), has a Gaussian distribution with mean and variance .

By a standard result on the KL divergence of two Gaussian distributions, we therefore have that Eq. (26) is at most

By Jensen’s inequality, this is at most

Plugging this back into Eq. (25), we get an error lower bound of

| (27) |

where we used the fact that . Let us now consider two cases:

-

•

If , then we choose (which ensures the condition ), and Eq. (27) equals .

-

•

If , then we choose , and Eq. (27) is lower bounded by .

Therefore, by choosing appropriately, we can lower bound Eq. (16) by as required.

6.4 Proof of Thm. 6

As in the proof of Thm. 3, to simplify notation, we assume the game takes place in for some , so the domain is . We denote the first coordinate as coordinate , and the other coordinates as .

The proof uses a similar loss vector distribution as that of Thm. 3, but with a different scaling to ensure a valid distribution.

By Yao’s minimax principle, it is sufficient to provide a randomized strategy to choose a loss vector distribution , such that for any deterministic player, the expected error is as defined in the theorem. In particular, we use the following strategy:

-

•

Choose uniformly at random.

-

•

Use the distribution over loss vectors , defined as follows: has a Gaussian distribution (where is a parameter to be chosen later), and is chosen independently according to a Gaussian distribution .

First, let us verify that any is a valid distribution. We have

Moreover, for any in the support of and for any , by Hölder’s inequality,

is normally distributed with mean and variance , and each is independently normally distributed with mean at most and variance , from which it can be verified using Gaussian tail bounds that

for all as required.

We now start the proof. Define the scalar and -dimensional vectors

For any fixed , recall that . It is therefore easily verified that is a minimizer of over . Recalling the formulation of regret in Eq. (3), we can write it as

| (28) |

Recalling that each is uniformly distributed on , the sum of expectations can be upper bounded as follows:

Since the player’s strategy is assumed to be deterministic, then is a deterministic function of the sequence of losses observed by the player over the rounds. Letting denote the probability density function of , we can rewrite the above as

| (29) |

where we used the fact that by the domain assumptions. We can now use Pinsker’s inequality and the chain rule to upper the integral as follows:

| (30) |

where is the KL divergence. Since the player is deterministic, any values determine the point that the player will choose on round . Thus, the distribution of depends on the distribution of , as determined by . By definition of :

-

•

Under the condition , has a Gaussian distribution with mean

, and variance . -

•

Under the condition , has a Gaussian distribution with mean

, and variance .

By a standard result on the KL divergence of two Gaussian distributions, we therefore have that Eq. (30) is at most

| (31) |

Applying Pinsker’s inequality on the reverse order of probabilities in Eq. (30), we can also upper Eq. (30) by

which leads to Eq. (30) being upper bounded by

| (32) |

Combining Eq. (31) and Eq. (32) and using the elementary inequality and the fact that is uniformly distributed on , we get

Plugging this back into Eq. (29), and that in turn into Eq. (28), we get an expected error lower bound of

which by Jensen’s inequality is at least

By definition of , we have that always. Using this and recalling that , we can lower bound the above by

Using Lemma 1 from the proof of Thm. 3, this expression can be lower bounded by

Recalling that is a free parameter, let us choose (which satisfies the assumption , since we assume ). We therefore get

| (33) |

Note that this expression is convex with respect to , and by differentiating, has an extremal point at

Since we assume , this point is non-positive, and therefore the minimum in Eq. (33) is attained at , where it equals

Since this lower bound holds for a domain in for any , we get a lower bound for a domain in for any , as required.

Acknowledgments

This research was supported by an Israel Science Foundation grant 425/13 and an FP7 Marie Curie CIG grant. We thank Sébastien Bubeck for several illuminating discussions.

References

- [1] J.-Y. Audibert, S. Bubeck, and G. Lugosi. Minimax policies for combinatorial prediction games.

- [2] J.-Y. Audibert, S. Bubeck, and G. Lugosi. Minimax policies for combinatorial prediction games. In COLT, 2011.

- [3] P. Auer, N. Cesa-Bianchi, Y. Freund, and R. Schapire. The nonstochastic multiarmed bandit problem. SIAM Journal on Computing, 32(1):48–77, 2002.

- [4] S. Bubeck and N. Cesa-Bianchi. Regret analysis of stochastic and nonstochastic multi-armed bandit problems. Foundations and Trends in Machine Learning, 5(1):1–122, 2012.

- [5] S. Bubeck, N. Cesa-Bianchi, and S. Kakade. Towards minimax policies for online linear optimization with bandit feedback. In COLT, 2012.

- [6] N. Cesa-Bianchi and G. Lugosi. Prediction, learning, and games. Cambridge University Press, 2006.

- [7] N. Cesa-Bianchi and G. Lugosi. Combinatorial bandits. Journal of Computer and System Sciences, 78(5), 2012.

- [8] V. Dani, T. Hayes, and S. Kakade. Stochastic linear optimization under bandit feedback. In COLT, 2008.

- [9] V. Dani, S. Kakade, and T. Hayes. The price of bandit information for online optimization. In NIPS, 2007.

- [10] O. Dekel, J. Ding, T. Koren, and Y. Peres. Bandits with switching costs: regret. 2014.

- [11] Y. Freund and R. Schapire. A decision-theoretic generalization of on-line learning and an application to boosting. J. Comput. Syst. Sci., 55(1):119–139, 1997.

- [12] E. Hazan, Z. Karnin, and R. Mehka. Volumetric spanners: an efficient exploration basis for learning. In COLT, 2014.

- [13] O. Shamir. On the complexity of bandit and derivative-free stochastic convex optimization. In COLT, 2013.

Appendix A From Sub-Gaussian to Bounded Distributions

As discussed in Sec. 2, our results use sub-Gaussian distributions rather than the more standard bounded distribution assumption. In this appendix, we explain why this is really without any loss of generality, and that lower bounds for the sub-Gaussian setting can be readily converted to the bounded setting, at the cost of a factor.

In particular, suppose there is a sub-Gaussian distribution over the cost vectors, for which any player’s strategy incurs expected error/regret at least . The trick is to consider a “shrinked” distribution, which simply re-scales all cost vectors by . Then the regret will be , and because the distribution is sub-Gaussian, then with very high probability all the cost vectors satisfy . This means that even if we modify the distribution to force it to be bounded, the expected error regret will still be . We note that a similar technique was used implicitly in [10].

A more formal result can be stated as follows:

Theorem 7.

Suppose that there exists a distribution satisfying and for all , such that for any player’s strategy, the expected error/regret is at least . Assuming , there exists a distribution satisfying , for which the expected error/regret of any player is at least for some universal constant .

Since the regret is virtually always at least , this means that we get the same error/regret up to constant and factors. The term can be replaced by for arbitrarily large , at the cost of affecting the constant.

Proof Sketch.

Let be a parameter to be determined later. Given the distribution , we algorithmically define and an auxiliary distribution as follows:

-

•

samples according to and returns . Let .

-

•

samples according to , and returns if , and otherwise returns . Let .

It is easily verified that . Moreover, if is large enough, then always returns a vector such that , and thus satisfies the lemma’s requirement. In that case, we also have .

It remains to show the error/regret lower bound. We sketch the proof for the expected error - the proof for the expected regret is identical by replacing by . By the lemma’s assumptions, we know that

where signifies expectation with respect to drawing cost vectors from , and . Since simply scales the vectors drawn from by a fixed factor , we have

Now, let be the event that for all cost vectors , we have . By the assumptions on and a union bound, for all sufficiently large . From the displayed equation above, it follows that

where we used the assumption that . Switching sides and using the assumption that , we get that

But conditioned on , the distribution of is the same under and , and therefore

where is the event that all cost vectors were drawn based on without modification. Since the error term is non-negative, this implies that

Finally, we have that , so we get

Picking sufficiently large, the result follows. ∎