Operational Distributed Regulation for Bitcoin

Abstract

On February 2014, $650.000.000 worth of Bitcoins disappeared. Currently it is unclear whether hackers or MtGox, the largest Bitcoin exchange, are to be blamed. In either case, the anonymous and unregulated nature of the Bitcoin system makes it practically impossible for innocent victims to get their money back. We have investigated the technical possibilities, solutions and implications of introducing a regulatory framework based on redlisting Bitcoin accounts. Despite numerous proposals, the Bitcoin community has voiced a strong opinion against any form of regulation. However, most of the discussions were based on speculations rather than facts. We strive to contribute a scientific foundation to these discussions and illuminate the path to crypto-justice.

1 Introduction

We discuss the technical possibilities and implications regarding the regulation of cryptocurrencies. Furthermore, we provide an operational implementation of a regulatory system based on redlisting. We will look at the first cryptocurrency that has experienced wide adoption[1], namely Bitcoin. A large part of the Bitcoin developer community has voiced a strong opinion against regulation of any form, stating that it undermines the foundational principles of Bitcoin. In this article we want to shed a light on these claims and test whether they actually hold in practice and to what extent. Recent events regarding illicit activities financed with and revolving around Bitcoins have shown that regulation should be, at the very least, considered as a possibility to counter such activities. After discussing the system behind Bitcoin, its implications and principles, we will look at specific cases in which Bitcoins were used for illicit purposes and discuss why regulation, and in particular redlisting, offers a discussable (partial) solution. Furthermore, we will also discuss why regulation could offer viable solutions to societal problems surrounding Bitcoin. Following this, we will propose an implementation on top of the reference Bitcoin implementation to regulate the Bitcoin system through redlisting. This implementation will be examined in depth on its viability and possible consequences, both on technical level as well as on foundational level.

2 Bitcoin

There are many cryptocurrencies active currently, nevertheless we will only use Bitcoin as the basis for our discussion. We find this appropriate since Bitcoin is currently the most widely adopted cryptocurrency on which most alternative currencies are more or less, if not entirely, based on.

2.1 Overview

In his publication[2], Satoshi Nakamoto proposed a peer-to-peer payment system called Bitcoin. In this system, the creation and exchange of money is governed by cryptographic algorithms, hence the name cryptocurrency. Payments are sent directly from one peer to another without intervention of a financial institution. Users send payments by broadcasting a digitally signed message to the Bitcoin network to request an update of the public ledger, a sequential record of all transactions. The transaction requests are bundled together into a so-called block. Approximately every 10 minutes a block is added to the public ledger, which is referred to as the block chain. Multiple chains of blocks can exist in the network, but only the longest chain represents the consensus of what transactions happened in the network. A process called mining is conducted by individual clients called miners. Mining is the process of providing computing power in order to verify and record payments into the block chain. In exchange, miners receive a fixed reward, which is periodically decreased by 50%. As of this writing, the reward is set at 25 BTC (Bitcoin) per block added to the block chain. This is what creates incentive for users to mine Bitcoins, which in turn facilitates the maintenance of the block chain so that Bitcoin owners can transfer ownership of their Bitcoins to others, i.e. make payments.

2.2 Technical Description

Bitcoin uses cryptography, a mathematically proven technique for validating and verifying signatures. The signatures are created by the Elliptic Curve Digital Signature Algorithm which are included at every transaction. The transactions are hashed (SHA256) together with a reference to the previous block in the block chain and a nonce to create a block. The nonce is used to influence the hash of the block, as only blocks with hashes of a specific form are considered valid. Finding a nonce that satisfies this restriction is what makes Bitcoin mining a cpu-intensive process. For this reason, the nonce is often referred to as a proof of work.

The proof of work is what ensures that the history of transactions is indeed a matter of consensus, where virtually every CPU gets a vote. To rewrite the blockchain, one would have to create a chain that is longer than the current chain, which would require more CPU power than the rest of the network.

Each block is broadcasted to the network, verified at the receiving nodes and then included in the blockchain so that spent Bitcoins cannot be spent twice.

2.3 Foundational Principles

Transactions are validated by a distributed consensus mechanism. The systems reliability stems from its cryptographic foundation. Consensus is reached by nodes accepting a newly mined block into their local block chain. There is a possibility of disagreement, e.g. different parts of the network accepting different blocks into the chain. This leads to branches which will then compete for unanimous acceptance in the network. There is no higher authority in the system than the code itself. As such, the system eliminates the necessity of traditional banks, drastically lowering transaction fees.

Bitcoin provides pseudo-anonymity[3] to its users. The wallets are collections of addresses which are not linked to ones identity, neither locally nor in a centralised database. This allows for a system with the same privacy that comes with cash money. This is a breakthrough for state-of-the-art digital transaction systems.

2.4 Foundational Volatility

Bitcoin appeals to those skeptical of the role of central bankers in the economy. As an independent, stateless currency it bypasses the involvement of governments and the power of regulators. After the failure of central banks to predict and react to the recent financial crash, this skepticism might be understandable. However, it must be mentioned that monetary policy and the vital tools financial regulators have at their disposal form an important factor in maintaining a stable economy. Bitcoin uses a fixed formula to control the money supply which is a very different concept in that it has no facilities to detect and react to the rise and fall of economic cycles[4]. Our economic history has taught us that the economy is far from stable and indeed consists of cycles which should be acted upon. A basic algorithm, with current technology, is unable to consider the complexity of human (inter)actions that impact the state of the economy and prevent necessary action when crises arise. While Bitcoin has grown in popularity and it is slowly being accepted in certain instances of the regular economy it currently can’t fill the vital role of a central bank. In order to stabilise the value of Bitcoin, it might prove beneficial to consider the implementation of certain regulatory measures. Remaining an independent currency seems to carry a high risk of devaluation, which is demonstrated by the incidents involving Bitcoin discussed below.

3 Bitcoin Incidents

In this section we will present the status quo of Bitcoin usage in order to conduct or facilitate illicit activities. Obviously, Bitcoins are not only used for such activities. In fact, the majority of Bitcoin users utilize the payment system for legal activities. However, for our purpose we will focus on the illicit activities in this section. In particular we want to convey that the current Bitcoin system makes it very hard[5] for authorities to counter malicious activities and apprehend the criminals involved. This impacts legitimate users as well, because the integrity of the payment system is constantly questioned by the public opinion. Furthermore, the current situation makes it very difficult to accept the Bitcoin system as a proper and legitimate payment method as any other non-digital currency. Therefore, we want to explore whether governmental regulation of the Bitcoin network will be beneficial for the system and the involved legitimate parties.

3.1 Silk Road

Silk Road[6] is an hidden online market, operating on the Tor network, as a part of the so-called Deep Web. The Silk Road was launched in February 2011. Among other goods, the primary product offered on the Silk Road are illegal narcotics. When conducted properly, users are able to browse the website anonymously and securely without potential traffic monitoring. Combined with the anonymous[7] payment method that Bitcoin facilitates, it is very difficult for authorities to take control of these illegal activities. Therefore, very few of the buyers and sellers have been apprehended. Although in October 2013 the FBI seized the Silk Road and arrested some of the websites operators, a new website called the Silk Road 2.0 has been launched to take the place of the previous one.

3.2 Mt. Gox

In July 2010 one of the first Bitcoin exchanges that emerged was Mt. Gox based in Tokyo, Japan. By 2013 Mt. Gox was handling approximately 70% of all Bitcoin transactions. In February 2014, Mt. Gox filed for bankruptcy protection, following the loss[8] of 850.000 BTC ($450 million). As of this writing it is unclear what actually happened with the coins that were lost, either unknown hackers have them in possession, or Mt. Gox has conducted embezzlement. In either case, a large part of Bitcoin owners lost money because of this situation. The following graph shows the drastic fall of the value of BTC around the time of the alleged hack.

![[Uncaptioned image]](/html/1406.5440/assets/mtgox.png)

To make matters even worse, it is very difficult to track when and where the stolen coins were part of a transaction. This makes it practically impossible for anyone to find the criminals behind this ordeal. We believe that in cases such as this, a redlist of rogue Bitcoin wallets could help to put back pressure on such activities. Through the redlist, the wallets in question can be blocked from ever getting a transaction in the block-chain. This makes it very difficult for the criminals to move the money around, i.e. conduct transactions. As such the stolen coins lose their value. Moreover, with a redlist implemented in the Bitcoin clients, the miners won’t be facilitating criminal activities anymore. Nowadays, miners that keep on mining after they were robbed from their coins, are in fact facilitating the theft of their own money. Obviously, this is a problem that must be dealt with and we believe that a redlist is potentially a proper solution.

3.3 Prohibition

Russia’s Prosecutor General’s Office has released the following statement: ”The monitoring of the use of virtual currencies shows an increasing interest in them, including for the purpose of money laundering, profit obtained through illegal means”. The statement further says: ”Russia’s official currency is the ruble. The introduction of other types of currencies and the issue of money surrogates are banned,” meaning that cryptocurrencies (the most popular of which is bitcoin) cannot be used by Russian citizens or corporations. Russia’s Central Bank (CBR) warned people against using virtual currencies, as they could be tied to gangs involved in money laundering and terrorist financing. Other countries, including China and Denmark, have also banned cryptocurrencies, for similar reasons. This reputation problem seems to be a consequence of the unregulated nature of Bitcoin. The lack of regulation attracts criminals and discourages banks, governments and regulators[9].

4 Regulation Through Redlisting

In order for Bitcoins to be accepted as a legitimate payment system, by both governmental authorities and the general public, it needs to be offered as a banking service. Just like existing banks, such a service would need to comply with existing regulations on national and international level. Without such compliance it will be difficult for Bitcoin to blend into the regular economy. This will not benefit the stability nor the popularity of Bitcoin. Bitcoins self-regulatory (i.e. unregulated) means of existence seems unacceptable in todays financial and judicial framework. Without some form of governmental regulation, it might be impossible for Bitcoin to become trustworthy and take the place of, or even live along-side, current financial systems. There are several ways in which one can go about regulating the Bitcoin system. We will focus on regulation through a governmentally maintained redlist. This redlist would contain the hashes which identify wallets that have been involved in criminal activities. The redlist could be enforced by the miner client software by simply refusing to mine transactions involving redlisted accounts. Such refusal of mining would make the value of the coins in criminal wallets practically worthless, since no transactions can be conducted with them. The only way criminals could enforce the addition of their transactions to the block-chain is by owning the majority of all computing power currently active on the Bitcoin mining network. The possession of such an amount of computing power makes it insensible for the owner(s) to conduct criminal activities since they can also use that computing power to acquire all the Bitcoin rewards by simply mining. The ability to generate an enormous amount of legal income would overshadow the incentive to conduct criminal activities.

4.1 The Redlist Opposition

There are many outspoken opponents of redlisting in the Bitcoin community. They present a few important arguments against the introduction of redlisting:

-

•

it introduces a central component, namely the regulatory organ, into the decentralized nature of the Bitcoin system.

-

•

redlisting (or tainting) coins would be subject to abuse.

-

•

tying a public key to an individual is technically impossible, making redlisting tricky.

We recognize all of these problems. However, we are of opinion that none of these arguments are strong enough to reject redlisting as a regulatory measure.

The first argument is often heard first in a discussion about redlisting in the Bitcoin world. It can be resolved however by allowing miners to choose whether or not to abide by a redlist. The argument against tainting coins fails to consider that other means of redlisting might be considered. The solution that we propose, focusses on redlisting public keys, rather than coins.

The third argument is an important one, as it sets a limit of what can be achieved by redlisting wallets. It is clear that redlisting alone would not suffice as a solution against illicit Bitcoin activities, but should be thought of as a tool in battling them. A tool that is important to have at one’s disposal.

Considering the above mentioned we intend to present a redlist implementation in order to test whether or not the mechanism would imply a negative impact on Bitcoins foundational principles. This work will also serve as an exploratory study into the implications of redlisting systems in crypto currencies. In this way we hope the discussion regarding regulation will gain fact-based arguments which can be discussed thoroughly by the community.

5 Redlist Regulatory Framework

In order to illustrate the technical possibility of Bitcoin regulation through redlisting, we will present the Redlist Regulatory Framework. This framework consists of three parts, namely a webservice that maintains the redlist, an update of the Bitcoin reference implementation client to enforce the redlist, and a change in the Bitcoin GUIMiner to visualize the process of redlisting. The framework we will present serves as a demonstrational one in order to show an discuss the possibilities. The actual implementation could be different from ours.

5.1 Implementation

The changes to the Bitcoin reference implementation should be such that the speed of mining and the security of the application are not compromised. The implementation is lean, in the sense that is only comprises about 450 lines added to the reference implementation.

The implementation111https://github.com/DistributedRegulation is split into several parts:

-

1.

retrieval, updating and building of the redlist in memory

-

2.

checking of new transactions by the miner against the redlist, to prevent them from ending up in a block

-

3.

checking of new blocks against the redlist and forking the blockchain if necessary to keep the blockchain clean

We will take a look at implementation in the following paragraphs.

1) Retrieval and building of the Redlist: The redlist is implemented as a simple c++ api containing functions to check a single public key, a transaction or an entire block against the redlist and return a boolean indicating whether it should be treated as redlisted.

This API is backed for now by a global hashset of redlisted public keys, which is build on first use, and checked for updates at every next use. The keys themselves are retrieved from a preset host. Checking for updates can be lean, by retrieving only the HTTP header and checking timestamps.

Checking a transaction is done by extracting all destinations from a pay-to-pubkey-hash-transaction and checking them against the hashset one by one.

Finally, checking a block is done similarly but extracting all output transactions and checking them and then extracting all signatures that release the inputs and checking them as well.

2) Checking new transactions seen by the miner: The reference miner has a pool of un-mined transactions. The miner gets a sequence of transactions from there and checks some basic requirements, before it tries to mine them into a block. There we break in to add check each of the transactions against the global redlist. Because the redlist is implemented as a hashset, the amortized runtime for this check is . If it sees a transaction that contains redlisted keys it simply does not process it into a block.

3) Checking incoming blocks: To discourage lone miners from mining redlisting transactions for the reward, nodes that do abide by the redlist try to ignore blocks that contain those transactions, unless they cannot keep up with the rate at which that branch is creating blocks. As described by Nakamoto[2], the nodes need to switch branches when they find out they cannot keep up. In order for this to be possible nodes cannot entirely discard redlisted blocks, but they have to keep them in the index of known blocks. The reference implementation of the node normally automatically switches to the longest branch in the index.

In order for us to allow a branch to be the longest branch in the index, but not switch to it (yet), we changed the comparator that compares different branches. Once a block gets into a branch that contains a redlisted transaction, we mark the branch as tainted. When we compare to branches and , we then take into a account the tainted marker and only treat the branch as longer if:

-

•

is also tainted and contains more work than

-

•

it’s contains more blocks than and is greater than the switching threshold

Once a node gives up and switches back to a branch that contains redlisted items, it resets the marker for that branch.

5.2 End-to-End System Test

The purpose of our tests is to verify both the correctness of our redlisting mechanism and the branching behaviour of a network populated by both the reference and the redlist version of the Bitcoin client. The test consists of a sequence of 5 steps, each involving the mining of a block containing a single transaction. In this environment, nodes W and R are the only miners, while A and B are simply used as transaction endpoints. We will focus our analysis on the evolution of the blockchain in W and R. For the sake of conciseness we will adopt a switching threshold of 2 blocks.

Initially, both nodes W and R have an identical ’view’ of the blockchain:

W: […]-[…]-[…]

^

R: […]-[…]-[…]

^

With each pair of square parenthesis ([…]) we represent a block, while the triple dots indicate an unspecified number of transactions inside a block. The ^ symbol indicates the block to which the tip of the blockchain is currently pointing at.

In the first step, node W sends transaction T1 to node A and starts mining the block containing it. This transaction will contain W’s signature, and will thus be tainted since W’s address is redlisted. After the block containing T1 is successfully mined, it will be broadcasted in the network. Upon accepting it, nodes W, A and B will set it as the tip of their blockchain, whereas R will not advance the tip, therefore creating an artificial fork.

W: […]-[…]-[…]-[T1]

^

R: […]-[…]-[…]

^ \

[T1]

Step 2 is a repetition of the first one; the behaviour of the nodes is completely identical and the result is the addition of a block to the chain in W and redlisted branch in R.

W: […]-[…]-[…]-[T1]-[T2]

^

R: […]-[…]-[…]

^ \

[T1]-[T2]

In step 3, node R sends a clean transaction to node B (T3), mines the block containing it and broadcasts it into the network. Node W will receive the block and discard it, since it is not part of the longest branch. More interesting is the case that involves R’s blockchain. The incoming clean block will reference R’s current tip, therefore being accepted and becoming the new tip of its blockchain. At the same time, R will keep the other branch containing the redlisted blocks in memory.

W: […]-[…]-[…]-[T1]-[T2]

^

R: […]-[…]-[…]-[T3]

\ ^

[T1]-[T2]

Steps 4 and 5 are again repetitions of step 1. The result is the extension of the redlisted branch with two extra blocks. While W will simply advance the tip of it’s blockchain, R will find itself in the situation in which the redlisted branch is too further ahead with regard to the current tip (the branch height difference has surpassed the switching threshold). R will have no other choice but to give up its effort to maintain a clean blockchain, thus switching to the redlisted branch. This will invalidate the block containing transaction T3, which will be returned to the mempool and mined at later time.

W: […]-[T1]-[T2]-[T4]-[T5]

^

R: […]-[T3]

\

[T1]-[T2]-[T4]-[T5]

^

5.3 An Incentive to Use the Redlist

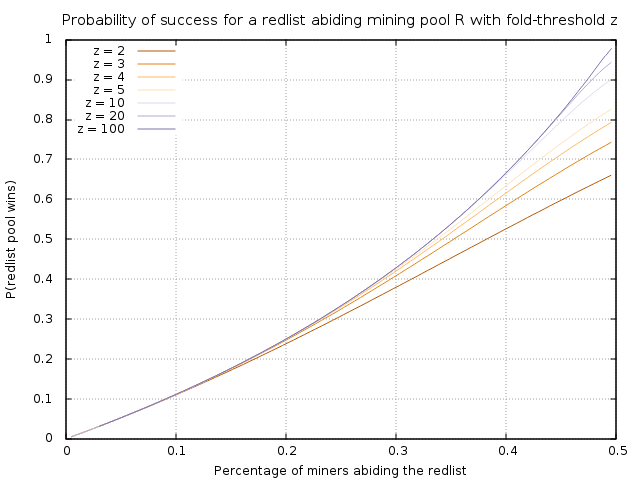

Although we have shown, using the tests, that the implementation works, it seems that miners that use the redlist are severely disadvantaged as long as they do not make up a majority in the network. That is: every time that they cannot gain in on the tainted branch, their work will be discarded; which in turn will mean that they miss their reward from mining valid blocks. In this section we show that although it is true that a risk is attached to abiding by the redlist, the redlist-abiding miners do not need a majority for their approach to pay off. Which leads to the suprising fact that there is an incentive for miners that only care about their profit to abide to the redlist from the point where the redlist abiding miners only make up 35% percent of the network hash rate.

To see how this can be true, we model the “race” between the tainted and non-tainted branch as a simple game between two players. Let player be the redlist-abiding group, and be a pool of miners that are indifferent w.r.t. the use of the redlist. We assume that all miners in use the same redlist and that every block found by is tainted. Furthermore, we assume that the folding-threshold for is . From the Bitcoin protocol if follows that the folding-threshold for is , i.e. they switch to the other branch as soon as it becomes the longest one. Lastly, let be the probability that finds the next block, such that is the probability that finds the next block; and let be linear in the relative size of . Now we are interested in the probability that does not need to fold it’s branch.

The game outlined above is known widely as the gambler’s ruin problem[10]. We interpret the fold threshold as an amount of starting cash for each player. The probability of interest then corresponds with the probability that the player is ruined. Figure 1 shows the probability against the relative size of . It can be seen that for the relatively low fold-threshold of , for a relative size of of 35%, already wins 50% of the time. And when occupies 50% of the miners, they can always win the game.

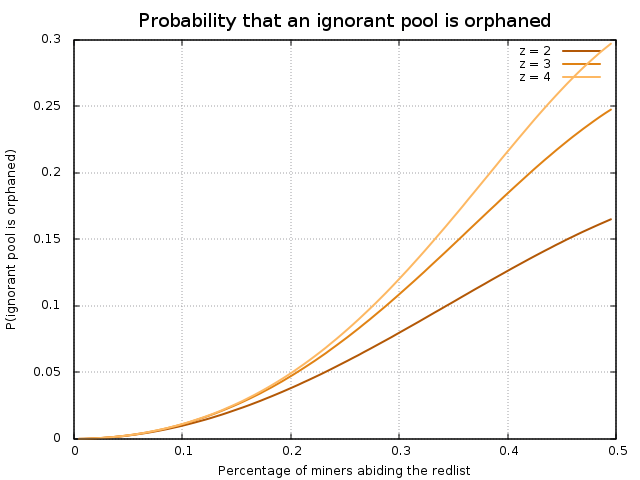

Another interesting probability is . needs to fold and give up at least one block whenever finds the first block, but wins the race. Figure 2 shows this probability, again against the relative size of . We can see that with 35% of the miners abiding by the redlist, already loses more than 15% of it’s rewards. This gives an incentive for indifferent miners to adopt the redlist early.

5.4 Bitcoin Attack Based on the Redlist Implementation

There are several known attacks to the Bitcoin system[11]; in this section we describe an example attack that might be conducted if our implementation of the Bitcoin client would be adopted. This attack assumes non-unanimous consensus on the redlist. The attack shows that a too simplistic approach would be naive and gives us a handle on what future work is still needed.

We consider the following, possibly over-simplified, scenario:

-

•

Miners are split in two groups: and .

-

•

has adopted redlist , whereas has adopted redlist .

-

•

Let be the strongest group, meaning that if and chase each-other for the longest chain, will win.

Now consider a Bitcoin public key , which is on but not on , owned by an attacker . can now shut out of the network: i.e. keep them busy on work that will never make it into the block-chain.

can do so by creating transactions using his private key.

Miners from will create blocks containing , whereas miners from will reject and mine blocks where is NOT included.

This introduces a fork in the chain and and will both attempt to uphold their chain for blocks.

Because is the strongest group, will loose and switch to after those blocks are mined.

A: […]-[Tq]-[…]-[…]

\

B: […]-[…]-[…]

If another transaction from is then in the network, the attack will start from the beginning. As such, can occupy with useless work.

It seems in line with Bitcoin’s idea of ”consensus” that the redlist with the largest backing group ”wins”, i.e. consensus about what transactions should be included in the blockchain is reached by votes weighted according to CPU power. But this attack exposes a vulnerability that goes beyond that, as the largest group can keep a minority from doing any work. It exploits the fact that miners will attempt to uphold their chain to effectively ban them from the pool of miners that contribute to the longest chain.

Two solutions can be considered:

-

1.

All miners accept the same redlist.

-

2.

Miners can pick their redlist, but do not reject blocks containing redlisted transactions.

The second option falls when we recognize that there will always be an incentive for miners to mine redlisted transactions; and there only need be one in order for a transaction to end up in the block-chain. An attack such as this would be an incentive to adopt one single redlist. Although we leave it as future work if this attack could be countered appropriately.

6 Conclusion

In this article we have discussed the Bitcoin cryptocurreny, its foundations, implications and status quo. We have debated several problems that currently surround Bitcoin and we have proposed to open up the discussion on whether regulation could and/or should be a solution to some of these issues. An initial implementation has been created (based on the Bitcoin reference implementation) that realises a redlisting mechanism. We have also presented an analysis of our implementation and the probabilities tied to its effectiveness. Surprisingly we have found that a mere 35% of the Bitcoin miners abiding the redlist is sufficient to enforce the mechanism. As such, Bitcoin will have gained some regulatory measures which can be used to counter some of the problems mentioned in this article. The question still remains whether this is indeed something that would benefit the Bitcoin system and community as a whole. Is the cure worse than the disease? Further work should be conducted in order to test and verify the workings of the proposed redlisting mechanism. Also other solutions should be investigated and weighed against our results. We hope that this paper can provide fruitful ground for a (fact-based) discussion about the future of Bitcoin.

7 Future Work

We provide a basis for experimentation and discussion, meaning that experimentation will have to be conducted before any fact based conclusions can be reached about the viability of this solution. Some important issues at hand are:

-

•

Can any other attacks on a redlist-based implementation be thought of and can these attacks be countered appropriately?

-

•

Assuming adaptation of our implementation, is is viable to prevent the outflow of Bitcoins from a redlisted wallet fast enough to prevent the owner from obfuscating the money before the network can respond?

-

•

Is a network with partial adaptation stable and fair?

We leave this for those that are willing to experiment with our implementation.

8 Acknowledgements

The presented work has been conducted by five anonymous students guided by prof. Johan Pouwelse at the Delft University of Technology. - WDIL

References

- [1] D. Ron and A. Shamir, “Quantitative analysis of the full bitcoin transaction graph,” in Financial Cryptography and Data Security. Springer, 2013, pp. 6–24.

- [2] S. Nakamoto, “Bitcoin: A peer-to-peer electronic cash system,” Consulted, vol. 1, p. 2012, 2008.

- [3] S. Martins and Y. Yang, “Introduction to bitcoins: a pseudo-anonymous electronic currency system,” in Proceedings of the 2011 Conference of the Center for Advanced Studies on Collaborative Research. IBM Corp., 2011, pp. 349–350.

- [4] J. Brito and A. Castillo, Bitcoin: A primer for policymakers. Mercatus Center at George Mason University, 2013.

- [5] F. Reid and M. Harrigan, “An analysis of anonymity in the bitcoin system,” in Security and Privacy in Social Networks. Springer, 2013, pp. 197–223.

- [6] N. Christin, “Traveling the silk road: A measurement analysis of a large anonymous online marketplace,” in Proceedings of the 22nd international conference on World Wide Web. International World Wide Web Conferences Steering Committee, 2013, pp. 213–224.

- [7] E. Androulaki, G. O. Karame, M. Roeschlin, T. Scherer, and S. Capkun, “Evaluating user privacy in bitcoin,” in Financial Cryptography and Data Security. Springer, 2013, pp. 34–51.

- [8] B. Wallace, “The rise and fall of bitcoin,” Wired Magazine.[Online]. Available, 2011.

- [9] O. Marian, “Are cryptocurrencies super tax havens?” Mich. L. Rev. First Impressions, vol. 112, pp. 38–38, 2013.

- [10] W. Feller, An Introduction to Probability Theory and Its Applications: Volume One. John Wiley & Sons, 1950.

- [11] S. Barber, X. Boyen, E. Shi, and E. Uzun, “Bitter to better—how to make bitcoin a better currency,” in Financial Cryptography and Data Security. Springer, 2012, pp. 399–414.