Algorithms for CVaR Optimization in MDPs

Abstract

In many sequential decision-making problems we may want to manage risk by minimizing some measure of variability in costs in addition to minimizing a standard criterion. Conditional value-at-risk (CVaR) is a relatively new risk measure that addresses some of the shortcomings of the well-known variance-related risk measures, and because of its computational efficiencies has gained popularity in finance and operations research. In this paper, we consider the mean-CVaR optimization problem in MDPs. We first derive a formula for computing the gradient of this risk-sensitive objective function. We then devise policy gradient and actor-critic algorithms that each uses a specific method to estimate this gradient and updates the policy parameters in the descent direction. We establish the convergence of our algorithms to locally risk-sensitive optimal policies. Finally, we demonstrate the usefulness of our algorithms in an optimal stopping problem.

1 Introduction

A standard optimization criterion for an infinite horizon Markov decision process (MDP) is the expected sum of (discounted) costs (i.e., finding a policy that minimizes the value function of the initial state of the system). However in many applications, we may prefer to minimize some measure of risk in addition to this standard optimization criterion. In such cases, we would like to use a criterion that incorporates a penalty for the variability (due to the stochastic nature of the system) induced by a given policy. In risk-sensitive MDPs [18], the objective is to minimize a risk-sensitive criterion such as the expected exponential utility [18], a variance-related measure [32, 16], or the percentile performance [17]. The issue of how to construct such criteria in a manner that will be both conceptually meaningful and mathematically tractable is still an open question.

Although most losses (returns) are not normally distributed, the typical Markiowitz mean-variance optimization [22], that relies on the first two moments of the loss (return) distribution, has dominated the risk management for over years. Numerous alternatives to mean-variance optimization have emerged in the literature, but there is no clear leader amongst these alternative risk-sensitive objective functions. Value-at-risk (VaR) and conditional value-at-risk (CVaR) are two promising such alternatives that quantify the losses that might be encountered in the tail of the loss distribution, and thus, have received high status in risk management. For (continuous) loss distributions, while VaR measures risk as the maximum loss that might be incurred w.r.t. a given confidence level , CVaR measures it as the expected loss given that the loss is greater or equal to VaRα. Although VaR is a popular risk measure, CVaR’s computational advantages over VaR has boosted the development of CVaR optimization techniques. We provide the exact definitions of these two risk measures and briefly discuss some of the VaR’s shortcomings in Section 2. CVaR minimization was first developed by Rockafellar and Uryasev [29] and its numerical effectiveness was demonstrated in portfolio optimization and option hedging problems. Their work was then extended to objective functions consist of different combinations of the expected loss and the CVaR, such as the minimization of the expected loss subject to a constraint on CVaR. This is the objective function that we study in this paper, although we believe that our proposed algorithms can be easily extended to several other CVaR-related objective functions. Boda and Filar [10] and Bäuerle and Ott [25, 4] extended the results of [29] to MDPs (sequential decision-making). While the former proposed to use dynamic programming (DP) to optimize CVaR, an approach that is limited to small problems, the latter showed that in both finite and infinite horizon MDPs, there exists a deterministic history-dependent optimal policy for CVaR optimization (see Section 3 for more details).

Most of the work in risk-sensitive sequential decision-making has been in the context of MDPs (when the model is known) and much less work has been done within the reinforcement learning (RL) framework. In risk-sensitive RL, we can mention the work by Borkar [11, 12] who considered the expected exponential utility and those by Tamar et al. [34] and Prashanth and Ghavamzadeh [21] on several variance-related risk measures. CVaR optimization in RL is a rather novel subject. Morimura et al. [24] estimate the return distribution while exploring using a CVaR-based risk-sensitive policy. Their algorithm does not scale to large problems. Petrik and Subramanian [27] propose a method based on stochastic dual DP to optimize CVaR in large-scale MDPs. However, their method is limited to linearly controllable problems. Borkar and Jain [15] consider a finite-horizon MDP with CVaR constraint and sketch a stochastic approximation algorithm to solve it. Finally, Tamar et al. [35] have recently proposed a policy gradient algorithm for CVaR optimization.

In this paper, we develop policy gradient (PG) and actor-critic (AC) algorithms for mean-CVaR optimization in MDPs. We first derive a formula for computing the gradient of this risk-sensitive objective function. We then propose several methods to estimate this gradient both incrementally and using system trajectories (update at each time-step vs. update after observing one or more trajectories). We then use these gradient estimations to devise PG and AC algorithms that update the policy parameters in the descent direction. Using the ordinary differential equations (ODE) approach, we establish the asymptotic convergence of our algorithms to locally risk-sensitive optimal policies. Finally, we demonstrate the usefulness of our algorithms in an optimal stopping problem. In comparison to [35], while they develop a PG algorithm for CVaR optimization in stochastic shortest path problems that only considers continuous loss distributions, uses a biased estimator for VaR, is not incremental, and has no convergence proof, here we study mean-CVaR optimization, consider both discrete and continuous loss distributions, devise both PG and (several) AC algorithms (trajectory-based and incremental – plus AC helps in reducing the variance of PG algorithms), and establish convergence proof for our algorithms.

2 Preliminaries

We consider problems in which the agent’s interaction with the environment is modeled as a MDP. A MDP is a tuple , where and are the state and action spaces; is the bounded cost random variable whose expectation is denoted by ; is the transition probability distribution; and is the initial state distribution. For simplicity, we assume that the system has a single initial state , i.e., . All the results of the paper can be easily extended to the case that the system has more than one initial state. We also need to specify the rule according to which the agent selects actions at each state. A stationary policy is a probability distribution over actions, conditioned on the current state. In policy gradient and actor-critic methods, we define a class of parameterized stochastic policies , estimate the gradient of a performance measure w.r.t. the policy parameters from the observed system trajectories, and then improve the policy by adjusting its parameters in the direction of the gradient. Since in this setting a policy is represented by its -dimensional parameter vector , policy dependent functions can be written as a function of in place of . So, we use and interchangeably in the paper. We denote by and the -discounted visiting distribution of state and state-action pair under policy , respectively.

Let be a bounded-mean random variable, i.e., , with the cumulative distribution function (e.g., one may think of as the loss of an investment strategy ). We define the value-at-risk at the confidence level as VaR. Here the minimum is attained because is non-decreasing and right-continuous in . When is continuous and strictly increasing, VaR is the unique satisfying , otherwise, the VaR equation can have no solution or a whole range of solutions. Although VaR is a popular risk measure, it suffers from being unstable and difficult to work with numerically when is not normally distributed, which is often the case as loss distributions tend to exhibit fat tails or empirical discreteness. Moreover, VaR is not a coherent risk measure [2] and more importantly does not quantify the losses that might be suffered beyond its value at the -tail of the distribution [28]. An alternative measure that addresses most of the VaR’s shortcomings is conditional value-at-risk, CVAR, which is the mean of the -tail distribution of . If there is no probability atom at VaR, CVaR has a unique value that is defined as CVaR. Rockafellar and Uryasev [29] showed that

| (1) |

Note that as a function of , is finite and convex (hence continuous).

3 CVaR Optimization in MDPs

For a policy , we define the loss of a state (state-action pair ) as the sum of (discounted) costs encountered by the agent when it starts at state (state-action pair ) and then follows policy , i.e., and . The expected value of these two random variables are the value and action-value functions of policy , i.e., and . The goal in the standard discounted formulation is to find an optimal policy .

For CVaR optimization in MDPs, we consider the following optimization problem: For a given confidence level and loss tolerance ,

| (2) |

| (3) |

To solve (3), we employ the Lagrangian relaxation procedure [5] to convert it to the following unconstrained problem:

| (4) |

where is the Lagrange multiplier. The goal here is to find the saddle point of , i.e., a point that satisfies . This is achieved by descending in and ascending in using the gradients of w.r.t. , , and , i.e.,111The notation in (6) means that the right-most term is a member of the sub-gradient set .

| (5) | ||||

| (6) | ||||

| (7) |

We assume that there exists a policy such that CVaR (feasibility assumption). As discussed in Section 1, Bäuerle and Ott [25, 4] showed that there exists a deterministic history-dependent optimal policy for CVaR optimization. The important point is that this policy does not depend on the complete history, but only on the current time step , current state of the system , and accumulated discounted cost .

In the following, we present a policy gradient (PG) algorithm (Sec. 4) and several actor-critic (AC) algorithms (Sec. 5.5) to optimize (4). While the PG algorithm updates its parameters after observing several trajectories, the AC algorithms are incremental and update their parameters at each time-step.

4 A Trajectory-based Policy Gradient Algorithm

In this section, we present a policy gradient algorithm to solve the optimization problem (4). The unit of observation in this algorithm is a system trajectory generated by following the current policy. At each iteration, the algorithm generates trajectories by following the current policy, use them to estimate the gradients in (5)-(7), and then use these estimates to update the parameters .

Let be a trajectory generated by following the policy , where and is usually a terminal state of the system. After visits the terminal state, it enters a recurring sink state at the next time step, incurring zero cost, i.e., , . Time index is referred as the stopping time of the MDP. Since the transition is stochastic, is a non-deterministic quantity. Here we assume that the policy is proper, i.e., for every . This further means that with probability , the MDP exits the transient states and hits (and stays in ) in finite time . For simplicity, we assume that the agent incurs zero cost in the terminal state. Analogous results for the general case with a non-zero terminal cost can be derived using identical arguments. The loss and probability of are defined as and , respectively. It can be easily shown that .

Algorithm 1 contains the pseudo-code of our proposed policy gradient algorithm. What appears inside the parentheses on the right-hand-side of the update equations are the estimates of the gradients of w.r.t. (estimates of (5)-(7)) (see Appendix A.2). is an operator that projects a vector to the closest point in a compact and convex set , and and are projection operators to and , respectively. These projection operators are necessary to ensure the convergence of the algorithm. The step-size schedules satisfy the standard conditions for stochastic approximation algorithms, and ensures that the VaR parameter update is on the fastest time-scale , the policy parameter update is on the intermediate time-scale , and the Lagrange multiplier update is on the slowest time-scale (see Appendix A.1 for the conditions on the step-size schedules). This results in a three time-scale stochastic approximation algorithm. We prove that our policy gradient algorithm converges to a (local) saddle point of the risk-sensitive objective function (see Appendix A.3).

| Update: | |||

| Update: | |||

| Update: |

5 Incremental Actor-Critic Algorithms

As mentioned in Section 4, the unit of observation in our policy gradient algorithm (Algorithm 1) is a system trajectory. This may result in high variance for the gradient estimates, especially when the length of the trajectories is long. To address this issue, in this section, we propose actor-critic algorithms that use linear approximation for some quantities in the gradient estimates and update the parameters incrementally (after each state-action transition). To develop our actor-critic algorithms, we should show how the gradients of (5)-(7) are estimated in an incremental fashion. We show this in the next four subsections, followed by a subsection that contains the algorithms.

5.1 Gradient w.r.t. the Policy Parameters

The gradient of our objective function w.r.t. the policy parameters in (5) may be rewritten as

| (8) |

Given the original MDP and the parameter , we define the augmented MDP as , , , and

where is any terminal state of the original MDP and is the value of the part of the state when a policy reaches a terminal state after steps, i.e., . We define a class of parameterized stochastic policies for this augmented MDP. Thus, the total (discounted) loss of this trajectory can be written as

| (9) |

From (9), it is clear that the quantity in the parenthesis of (8) is the value function of the policy at state in the augmented MDP , i.e., . Thus, it is easy to show that (the proof of the second equality can be found in the literature, e.g., [26])

| (10) |

where is the discounted visiting distribution (defined in Section 2) and is the action-value function of policy in the augmented MDP . We can show that is an unbiased estimate of , where is the temporal-difference (TD) error in , and is an unbiased estimator of (see e.g. [8]). In our actor-critic algorithms, the critic uses linear approximation for the value function , where the feature vector is from low-dimensional space .

5.2 Gradient w.r.t. the Lagrangian Parameter

We may rewrite the gradient of our objective function w.r.t. the Lagrangian parameters in (7) as

| (11) |

Similar to Section 5.1, (a) comes from the fact that the quantity in the parenthesis in (11) is , the value function of the policy at state in the augmented MDP . Note that the dependence of on comes from the definition of the cost function in . We now derive an expression for , which in turn will give us an expression for .

Lemma 1

The gradient of w.r.t. the Lagrangian parameter may be written as

| (12) |

Proof. See Appendix B.2.

From Lemma 1 and (11), it is easy to see that is an unbiased estimate of . An issue with this estimator is that its value is fixed to all along a system trajectory, and only changes at the end to . This may affect the incremental nature of our actor-critic algorithm. To address this issue, we propose a different approach to estimate the gradients w.r.t. and in Sec. 5.4 (of course this does not come for free).

Another important issue is that the above estimator is unbiased only if the samples are generated from the distribution . If we just follow the policy, then we may use as an estimate for (see (20) and (22) in Algorithm 2). Note that this is an issue for all discounted actor-critic algorithms that their (likelihood ratio based) estimate for the gradient is unbiased only if the samples are generated from , and not just when we simply follow the policy. Although this issue was known in the community, there is a recent paper that investigates it in details [36]. Moreover, this might be a main reason that we have no convergence analysis (to the best of our knowledge) for (likelihood ratio based) discounted actor-critic algorithms.222Note that the discounted actor-critic algorithm with convergence proof in [6] is based on SPSA.

5.3 Sub-Gradient w.r.t. the VaR Parameter

We may rewrite the sub-gradient of our objective function w.r.t. the VaR parameters in (6) as

| (13) |

From the definition of the augmented MDP , the probability in (13) may be written as , where is the part of the state in when we reach a terminal state, i.e., (see Section 5.1). Thus, we may rewrite (13) as

| (14) |

From (14), it is easy to see that is an unbiased estimate of the sub-gradient of w.r.t. . An issue with this (unbiased) estimator is that it can be only applied at the end of a system trajectory (i.e., when we reach the terminal state ), and thus, using it prevents us of having a fully incremental algorithm. In fact, this is the estimator that we use in our semi trajectory-based actor-critic algorithm (see (21) in Algorithm 2).

One approach to estimate this sub-gradient incrementally, hence having a fully incremental algorithm, is to use simultaneous perturbation stochastic approximation (SPSA) method [9]. The idea of SPSA is to estimate the sub-gradient using two values of at and , where is a positive perturbation (see Sec. 5.5 for the detailed description of ).333SPSA-based gradient estimate was first proposed in [33] and has been widely used in various settings, especially those involving high-dimensional parameter. The SPSA estimate described above is two-sided. It can also be implemented single-sided, where we use the values of the function at and . We refer the readers to [9] for more details on SPSA and to [21] for its application in learning in risk-sensitive MDPs. In order to see how SPSA can help us to estimate our sub-gradient incrementally, note that

| (15) |

Similar to Sections 5.1 and 5.2, (a) comes from the fact that the quantity in the parenthesis in (15) is , the value function of the policy at state in the augmented MDP . Since the critic uses a linear approximation for the value function, i.e., , in our actor-critic algorithms (see Section 5.1 and Algorithm 2), the SPSA estimate of the sub-gradient would be of the form (see (18) in Algorithm 2).

5.4 An Alternative Approach to Compute the Gradients

In this section, we present an alternative way to compute the gradients, especially those w.r.t. and . This allows us to estimate the gradient w.r.t. in a (more) incremental fashion (compared to the method of Section 5.2), with the cost of the need to use two different linear function approximators (instead of one used in Algorithm 2). In this approach, we define the augmented MDP slightly different than the one in Section 5.2. The only difference is in the definition of the cost function, which is defined here as (note that has been replaced by and has been removed)

where is any terminal state of the original MDP . It is easy to see that the term appearing in the gradients of (5)-(7) is the value function of the policy at state in this augmented MDP. As a result, we have

Gradient w.r.t. : It is easy to see that now this gradient (5) is the gradient of the value function of the original MDP, , plus times the gradient of the value function of the augmented MDP, , both at the initial states of these MDPs (with abuse of notation, we use for the value function of both MDPs). Thus, using linear approximators and for the value functions of the original and augmented MDPs, can be estimated as , where and are the TD-errors of these MDPs.

Gradient w.r.t. : Similar to the case for , it is easy to see that this gradient (7) is plus the value function of the augmented MDP, , and thus, can be estimated incrementally as .

Sub-Gradient w.r.t. : This sub-gradient (6) is times one plus the gradient w.r.t. of the value function of the augmented MDP, , and thus using SPSA, can be estimated incrementally as .

5.5 Actor-Critic Algorithms

In this section, we present two actor-critic algorithms for optimizing the risk-sensitive measure (4). These algorithms are based on the gradient estimates of Sections 5.1-5.3. While the first algorithm (SPSA-based) is fully incremental and updates all the parameters at each time-step, the second one updates at each time-step and updates and only at the end of each trajectory, thus given the name semi trajectory-based. Algorithm 2 contains the pseudo-code of these algorithms. The projection operators , , and are defined as in Section 4 and are necessary to ensure the convergence of the algorithms. The step-size schedules satisfy the standard conditions for stochastic approximation algorithms, and ensures that the critic update is on the fastest time-scale , the policy and VaR parameter updates are on the intermediate time-scale, with -update being faster than -update , and finally the Lagrange multiplier update is on the slowest time-scale (see Appendix B.1 for the conditions on these step-size schedules). This results in four time-scale stochastic approximation algorithms. We prove that these actor-critic algorithms converge to a (local) saddle point of the risk-sensitive objective function (see Appendix B.4).

| TD Error: | (16) | |||

| Critic Update: | (17) | |||

| Actor Updates: | (18) | |||

| (19) | ||||

| (20) |

| Update: | (21) | |||

| Update: | (22) |

6 Experimental Results

We consider an optimal stopping problem in which the state at each time step consists of the cost and time , i.e., , where is the stopping time. The agent (buyer) should decide either to accept the present cost or wait. If she accepts or when , the system reaches a terminal state and the cost is received, otherwise, she receives the cost and the new state is , where is w.p. and w.p. ( and are constants). Moreover, there is a discounted factor to account for the increase in the buyer’s affordability. The problem has been described in more details in Appendix C. Note that if we change cost to reward and minimization to maximization, this is exactly the American option pricing problem, a standard testbed to evaluate risk-sensitive algorithms (e.g., [34]). Since the state space is continuous, solving for an exact solution via DP is infeasible, and thus, it requires approximation and sampling techniques.

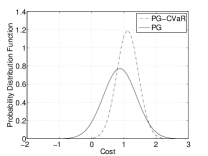

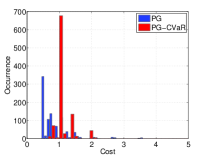

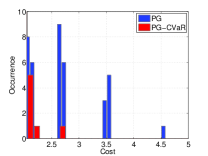

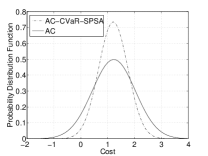

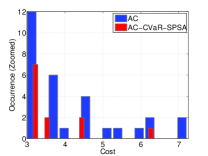

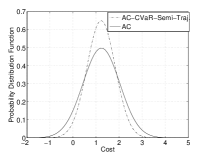

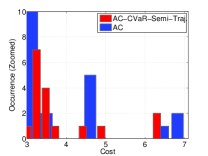

We compare the performance of our risk-sensitive policy gradient Alg. 1 (PG-CVaR) and two actor-critic Algs. 2 (AC-CVaR-SPSA,AC-CVaR-Semi-Traj) with their risk-neutral counterparts (PG and AC) (see Appendix C for the details of these experiments). Fig. 1 shows the distribution of the discounted cumulative cost for the policy learned by each of these algorithms. From left to right, the columns display the first two moments, the whole (distribution), and zoom on the right-tail of these distributions. The results indicate that the risk-sensitive algorithms yield a higher expected loss, but less variance, compared to the risk-neutral methods. More precisely, the loss distributions of the risk-sensitive algorithms have lower right-tail than their risk-neutral counterparts. Table 1 summarizes the performance of these algorithms. The numbers reiterate what we concluded from Fig. 1.

| PG | 0.8780 | 0.2647 | 2.0855 | 0.058 |

| PG-CVaR | 1.1128 | 0.1109 | 1.7620 | 0.012 |

| AC | 1.1963 | 0.6399 | 2.6479 | 0.029 |

| AC-CVaR-SPSA | 1.2031 | 0.2942 | 2.3865 | 0.031 |

| AC-CVaR-Semi-Traj. | 1.2169 | 0.3747 | 2.3889 | 0.026 |

7 Conclusions and Future Work

We proposed novel policy gradient and actor critic (AC) algorithms for CVaR optimization in MDPs. We provided proofs of convergence (in the appendix) to locally risk-sensitive optimal policies for the proposed algorithms. Further, using an optimal stopping problem, we observed that our algorithms resulted in policies whose loss distributions have lower right-tail compared to their risk-neutral counterparts. This is extremely important for a risk averse decision-maker, especially if the right-tail contains catastrophic losses. Future work includes: 1) Providing convergence proofs for our AC algorithms when the samples are generated by following the policy and not from its discounted visiting distribution (this can be wasteful in terms of samples), 2) Here we established asymptotic limits for our algorithms. To the best of our knowledge, there are no convergence rate results available for multi-timescale stochastic approximation schemes, and hence, for AC algorithms. This is true even for the AC algorithms that do not incorporate any risk criterion. It would be an interesting research direction to obtain finite-time bounds on the quality of the solution obtained by these algorithms, 3) Since interesting losses in the CVaR optimization problems are those that exceed the VaR, in order to compute more accurate estimates of the gradients, it is necessary to generate more samples in the right-tail of the loss distribution (events that are observed with a very low probability). Although importance sampling methods have been used to address this problem [3, 35], several issues, particularly related to the choice of the sampling distribution, have remained unsolved that are needed to be investigated, and finally, 4) Evaluating our algorithms in more challenging problems.

References

- Altman et al. [2004] Eitan Altman, Konstantin E Avrachenkov, and Rudesindo Núñez-Queija. Perturbation analysis for denumerable markov chains with application to queueing models. Advances in Applied Probability, pages 839–853, 2004.

- Artzner et al. [1999] P. Artzner, F. Delbaen, J. Eber, and D. Heath. Coherent measures of risk. Journal of Mathematical Finance, 9(3):203–228, 1999.

- Bardou et al. [2009] O. Bardou, N. Frikha, and G. Pagès. Computing VaR and CVaR using stochastic approximation and adaptive unconstrained importance sampling. Monte Carlo Methods and Applications, 15(3):173–210, 2009.

- Bäuerle and Ott [2011] N. Bäuerle and J. Ott. Markov decision processes with average-value-at-risk criteria. Mathematical Methods of Operations Research, 74(3):361–379, 2011.

- Bertsekas [1999] D. Bertsekas. Nonlinear programming. Athena Scientific, 1999.

- Bhatnagar [2010] S. Bhatnagar. An actor-critic algorithm with function approximation for discounted cost constrained Markov decision processes. Systems & Control Letters, 59(12):760–766, 2010.

- Bhatnagar and Lakshmanan [2012] S. Bhatnagar and K. Lakshmanan. An online actor-critic algorithm with function approximation for constrained Markov decision processes. Journal of Optimization Theory and Applications, pages 1–21, 2012.

- Bhatnagar et al. [2009] S. Bhatnagar, R. Sutton, M. Ghavamzadeh, and M. Lee. Natural actor-critic algorithms. Automatica, 45(11):2471–2482, 2009.

- Bhatnagar et al. [2013] S. Bhatnagar, H. Prasad, and L.A. Prashanth. Stochastic Recursive Algorithms for Optimization, volume 434. Springer, 2013.

- Boda and Filar [2006] K. Boda and J. Filar. Time consistent dynamic risk measures. Mathematical Methods of Operations Research, 63(1):169–186, 2006.

- Borkar [2001] V. Borkar. A sensitivity formula for the risk-sensitive cost and the actor-critic algorithm. Systems & Control Letters, 44:339–346, 2001.

- Borkar [2002] V. Borkar. Q-learning for risk-sensitive control. Mathematics of Operations Research, 27:294–311, 2002.

- Borkar [2005] V. Borkar. An actor-critic algorithm for constrained Markov decision processes. Systems & Control Letters, 54(3):207–213, 2005.

- Borkar [2008] V. Borkar. Stochastic approximation: a dynamical systems viewpoint. Cambridge University Press, 2008.

- Borkar and Jain [2014] V. Borkar and R. Jain. Risk-constrained Markov decision processes. IEEE Transaction on Automatic Control, 2014.

- Filar et al. [1989] J. Filar, L. Kallenberg, and H. Lee. Variance-penalized Markov decision processes. Mathematics of Operations Research, 14(1):147–161, 1989.

- Filar et al. [1995] J. Filar, D. Krass, and K. Ross. Percentile performance criteria for limiting average Markov decision processes. IEEE Transaction of Automatic Control, 40(1):2–10, 1995.

- Howard and Matheson [1972] R. Howard and J. Matheson. Risk sensitive Markov decision processes. Management Science, 18(7):356–369, 1972.

- Khalil and Grizzle [2002] Hassan K Khalil and JW Grizzle. Nonlinear systems, volume 3. Prentice hall Upper Saddle River, 2002.

- Kushner and Yin [1997] Harold J Kushner and G George Yin. Stochastic approximation algorithms and applications. Springer, 1997.

- L.A. and Ghavamzadeh [2013] Prashanth L.A. and M. Ghavamzadeh. Actor-critic algorithms for risk-sensitive MDPs. In Proceedings of Advances in Neural Information Processing Systems 26, pages 252–260, 2013.

- Markowitz [1959] H. Markowitz. Portfolio Selection: Efficient Diversification of Investment. John Wiley and Sons, 1959.

- Milgrom and Segal [2002] Paul Milgrom and Ilya Segal. Envelope theorems for arbitrary choice sets. Econometrica, 70(2):583–601, 2002.

- Morimura et al. [2010] T. Morimura, M. Sugiyama, M. Kashima, H. Hachiya, and T. Tanaka. Nonparametric return distribution approximation for reinforcement learning. In Proceedings of the 27th International Conference on Machine Learning, pages 799–806, 2010.

- Ott [2010] J. Ott. A Markov Decision Model for a Surveillance Application and Risk-Sensitive Markov Decision Processes. PhD thesis, Karlsruhe Institute of Technology, 2010.

- Peters et al. [2005] J. Peters, S. Vijayakumar, and S. Schaal. Natural actor-critic. In Proceedings of the Sixteenth European Conference on Machine Learning, pages 280–291, 2005.

- Petrik and Subramanian [2012] M. Petrik and D. Subramanian. An approximate solution method for large risk-averse Markov decision processes. In Proceedings of the 28th International Conference on Uncertainty in Artificial Intelligence, 2012.

- Rockafellar and Uryasev [2000] R. Rockafellar and S. Uryasev. Conditional value-at-risk for general loss distributions. Journal of Banking and Finance, 2:s1–41, 2000.

- Rockafellar and Uryasev [2002] R. Rockafellar and S. Uryasev. Optimization of conditional value-at-risk. Journal of Risk, 26:1443–1471, 2002.

- Ryan [1998] EP Ryan. An integral invariance principle for differential inclusions with applications in adaptive control. SIAM Journal on Control and Optimization, 36(3):960–980, 1998.

- Shardlow and Stuart [2000] Tony Shardlow and Andrew M Stuart. A perturbation theory for ergodic markov chains and application to numerical approximations. SIAM journal on numerical analysis, 37(4):1120–1137, 2000.

- Sobel [1982] M. Sobel. The variance of discounted Markov decision processes. Applied Probability, pages 794–802, 1982.

- Spall [1992] J. Spall. Multivariate stochastic approximation using a simultaneous perturbation gradient approximation. IEEE Transactions on Automatic Control, 37(3):332–341, 1992.

- Tamar et al. [2012] A. Tamar, D. Di Castro, and S. Mannor. Policy gradients with variance related risk criteria. In Proceedings of the Twenty-Ninth International Conference on Machine Learning, pages 387–396, 2012.

- Tamar et al. [2014] A. Tamar, Y. Glassner, and S. Mannor. Policy gradients beyond expectations: Conditional value-at-risk. arXiv:1404.3862v1, 2014.

- Thomas [2014] P. Thomas. Bias in natural actor-critic algorithms. In Proceedings of the Thirty-First International Conference on Machine Learning, 2014.

Appendix A Technical Details of the Trajectory-based Policy Gradient Algorithm

A.1 Assumptions

We make the following assumptions for the step-size schedules in our algorithms:

(A1) For any state-action pair , is continuously differentiable in and is a Lipschitz function in for every and .

(A2) The Markov chain induced by any policy is irreducible and aperiodic.

(A3) The step size schedules , , and satisfy

| (23) | ||||

| (24) | ||||

| (25) |

A.2 Computing the Gradients

i) : Gradient of w.r.t.

By expanding the expectations in the definition of the objective function in (4), we obtain

By taking gradient with respect to , we have

This gradient can rewritten as

| (26) |

where

ii) : Sub-differential of w.r.t.

From the definition of , we can easily see that is a convex function in for any fixed . Note that for every fixed and any , we have

where is any element in the set of sub-derivatives:

Since is finite-valued for any , by the additive rule of sub-derivatives, we have

| (27) |

In particular for , we may write the sub-gradient of w.r.t. as

iii) : Gradient of w.r.t.

Since is a linear function in , obviously one can express the gradient of w.r.t. as follows:

| (28) |

A.3 Proof of Convergence of the Policy Gradient Algorithm

In this section, we prove the convergence of our policy gradient algorithm (Algorithm 1).

Theorem 2

Suppose . Then the sequence of updates in Algorithm 1 converges to a (local) saddle point of our objective function almost surely, i.e., it satisfies for some and . Note that represents a hyper-dimensional ball centered at with radius .

Since converges on the faster timescale than and , the -update can be rewritten by assuming as invariant quantities, i.e.,

| (29) |

Consider the continuous time dynamics of defined using differential inclusion

| (30) |

where

and is the Euclidean projection operator of to , i.e., . In general is not necessarily differentiable. is the left directional derivative of the function in the direction of . By using the left directional derivative in the sub-gradient descent algorithm for , the gradient will point at the descent direction along the boundary of whenever the update hits its boundary.

Furthermore, since converges on the faster timescale than , and is on the slowest time-scale, the -update can be rewritten using the converged and assuming as an invariant quantity, i.e.,

Consider the continuous time dynamics of :

| (31) |

where

and is the Euclidean projection operator of to , i.e., . Similar to the analysis of , is the left directional derivative of the function in the direction of . By using the left directional derivative in the gradient descent algorithm for , the gradient will point at the descent direction along the boundary of whenever the update hits its boundary.

Finally, since -update converges in a slowest time-scale, the -update can be rewritten using the converged and , i.e.,

| (32) |

Consider the continuous time system

| (33) |

where

and is the Euclidean projection operator of to , i.e., . Similar to the analysis of , is the left directional derivative of the function in the direction of . By using the left directional derivative in the gradient ascent algorithm for , the gradient will point at the ascent direction along the boundary of whenever the update hits its boundary.

Define

for where is a local minimum of for fixed , i.e., for any for some .

Next, we want to show that the ODE (33) is actually a gradient ascent of the Lagrangian function using the envelope theorem in mathematical economics [23]. The envelope theorem describes sufficient conditions for the derivative of with respect to where it equals to the partial derivative of the objective function with respect to , holding at its local optimum . We will show that coincides with with as follows.

Theorem 3

The value function is absolutely continuous. Furthermore,

| (34) |

Proof. The proof follows from analogous arguments of Lemma 4.3 in [13]. From the definition of , observe that for any with ,

This implies that is absolutely continuous. Therefore, is continuous everywhere and differentiable almost everywhere.

By the Milgrom-Segal envelope theorem of mathematical economics (Theorem 1 of [23]), one can conclude that the derivative of coincides with the derivative of at the point of differentiability and , . Also since is absolutely continuous, the limit of at (or ) coincides with the lower/upper directional derivatives if is a point of non-differentiability. Thus, there is only a countable number of non-differentiable points in and each point of non-differentiability has the same directional derivatives as the point slightly beneath (in the case of ) or above (in the case of ) it. As the set of non-differentiable points of has measure zero, it can then be interpreted that coincides with , i.e., expression (34) holds.

Remark 1

It can be easily shown that is a concave function. Since for given and , is a linear function in . Therefore, for any , , i.e., is a concave function. Concavity of implies that it is continuous and directionally (both left hand and right hand) differentiable in . Furthermore at any such that the derivative of with respect of at exists, by Theorem 1 of [23], . Furthermore concavity of implies . Combining these arguments, one obtains .

In order to prove the main convergence result, we need the following standard assumptions and remarks.

Assumption 4

For any given and , the set is closed.

Remark 2

For any given , , and , we have

| (35) |

To see this, recall from definition that can be parameterized by as, for ,

It is obvious that . Thus, , and . Recalling , these arguments imply the claim of (35).

Before getting into the main result, we need the following technical proposition.

Proposition 5

is Lipschitz in .

Proof. Recall that

and whenever . Now Assumption (A1) implies that is a Lipschitz function in for any and and is differentiable in . Therefore, by recalling that and by combining these arguments and noting that the sum of products of Lipschitz functions is Lipschitz, one concludes that is Lipschitz in .

Remark 3

is Lipschitz in implies that which further implies that

for . Similarly, is Lipschitz implies that

for a positive random variable . Furthermore, since w.p. , and is Lipschitz for any , w.p. .

We are now in a position to prove the convergence analysis of Theorem 2.

Proof. [Proof of Theorem 2] We split the proof into the following four steps:

Step 1 (Convergence of update)

Since converges in a faster time scale than and , one can assume both and as fixed quantities in the -update, i.e.,

| (36) |

and

| (37) |

First, one can show that is square integrable, i.e.

where is the filtration of generated by different independent trajectories.

Second, since the history trajectories are generated based on the sampling probability mass function , expression (27) implies that . Therefore, the -update is a stochastic approximation of the ODE (30) with a Martingale difference error term, i.e.,

Then one can invoke Corollary 4 in Chapter 5 of [14] (stochastic approximation theory for non-differentiable systems) to show that the sequence converges almost surely to a fixed point of differential inclusion (31), where . To justify the assumptions of this theorem, 1) from Remark 2, the Lipschitz property is satisfied, i.e., , 2) is a convex compact set by definition, 3) Assumption 4 implies that is a closed set. This implies is an upper semi-continuous set valued mapping 4) the step-size rule follows from (A.1), 5) the Martingale difference assumption follows from (37), and 6) , implies that almost surely.

Consider the ODE of in (30), we define the set-valued derivative of as follows:

One may conclude that

We have the following cases:

Case 1: When .

For every , there exists a sufficiently small such that and

Therefore, the definition of implies

| (38) |

The maximum is attained because is a convex compact set and is a continuous function. At the same time, we have whenever .

Case 2: When and for any such that , for any and some .

The condition implies that

Then we obtain

| (39) |

Furthermore, we have whenever .

Case 3: When and there exists a non-empty set

.

First, consider any . For any , define . The above condition implies that when ,

is the projection of to the tangent space of . For any elements , since the following set

is compact, the projection of on exists. Furthermore, since is a strongly convex function and , by first order optimality condition, one obtains

where is an unique projection of (the projection is unique because is strongly convex and is a convex compact set). Since the projection (minimizer) is unique, the above equality holds if and only if .

Therefore, for any and ,

Second, for any , one obtains , for any and some . In this case, the arguments follow from case 2 and the following expression holds, .

Combining these arguments, one concludes that

| (40) |

This quantity is non-zero whenever (this is because, for any , one obtains ).

Thus, by similar arguments one may conclude that and it is non-zero if for every . Therefore, by Lasalle’s invariance principle for differential inclusion (see Theorem 2.11 [30]), the above arguments imply that with any initial condition , the state trajectory of (31) converges to a stable stationary point in the positive invariant set . Since , is a descent direction of for fixed and , i.e., for any .

Step 2 (Convergence of update)

Since converges in a faster time scale than and converges faster than , one can assume as a fixed quantity and as a converged quantity in the -update. The -update can be rewritten as a stochastic approximation, i.e.,

| (41) |

where

| (42) |

First, one can show that is square integrable, i.e., for some , where is the filtration of generated by different independent trajectories. To see this, notice that

The Lipschitz upper bounds are due to results in Remark 3. Since w.p. , there exists such that . Furthermore, w.p. implies . By combining these results, one concludes that where

Second, since the history trajectories are generated based on the sampling probability mass function , expression (26) implies that . Therefore, the -update is a stochastic approximation of the ODE (31) with a Martingale difference error term. In addition, from the convergence analysis of update, is an asymptotically stable equilibrium point of . From (27), is a Lipschitz set-valued mapping in (since is Lipschitz in ), it can be easily seen that is a Lipschitz continuous mapping of .

Case 1: When .

Since is the interior of the set and is a convex compact set, there exists a sufficiently small such that and

Therefore, the definition of implies

| (44) |

At the same time, we have whenever .

Case 2: When and for any and some .

The condition implies that

Then we obtain

| (45) |

Furthermore, when .

Case 3: When and for some and any .

For any , define . The above condition implies that when ,

is the projection of to the tangent space of . For any elements , since the following set

is compact, the projection of on exists. Furthermore, since is a strongly convex function and , by first order optimality condition, one obtains

where is an unique projection of (the projection is unique because is strongly convex and is a convex compact set). Since the projection (minimizer) is unique, the above equality holds if and only if .

Therefore, for any and ,

From these arguments, one concludes that and this quantity is non-zero whenever .

Therefore, by Lasalle’s invariance principle [19], the above arguments imply that with any initial condition , the state trajectory of (31) converges to a stable stationary point in the positive invariant set and for any .

Based on the above properties and noting that 1) from Proposition 5, is a Lipschitz function in , 2) the step-size rule follows from Section A.1, 3) expression (47) implies that is a square integrable Martingale difference, and 4) , implies that almost surely, one can invoke Theorem 2 in Chapter 6 of [14] (multi-time scale stochastic approximation theory) to show that the sequence converges almost surely to a fixed point of ODE (31), where . Also, it can be easily seen that is a closed subset of the compact set , which is a compact set as well.

Step 3 (Local Minimum)

Now, we want to show that converges to a local minimum of for fixed . Recall converges to . From previous arguments on convergence analysis imply that with any initial condition , the state trajectories and of (30) and (31) converge to the set of stationary points in the positive invariant set and for any .

By contradiction, suppose is not a local minimum. Then there exists such that . The minimum is attained by Weierstrass extreme value theorem. By putting , the above arguments imply that

which is clearly a contradiction. Therefore, the stationary point is a local minimum of as well.

Step 4 (Convergence of update)

Since -update converges in the slowest time scale, it can be rewritten using the converged and , i.e.,

| (46) |

where

| (47) |

From (28), it is obvious that is a constant function of . Similar to update, one can easily show that is square integrable, i.e.,

where is the filtration of generated by different independent trajectories. Furthermore, expression (28) implies that . Therefore, the -update is a stochastic approximation of the ODE (33) with a Martingale difference error term. In addition, from the convergence analysis of update, is an asymptotically stable equilibrium point of . From (26), is a linear mapping in , it can be easily seen that is a Lipschitz continuous mapping of .

Consider the ODE of in (33). Analogous to the arguments in the update, we may write

and show that , this quantity is non-zero whenever . Lasalle’s invariance principle implies that is a stable equilibrium point.

Based on the above properties and noting that the step size rule follows from Section A.1, one can apply the multi-time scale stochastic approximation theory (Theorem 2 in Chapter 6 of [14]) to show that the sequence converges almost surely to a fixed point of ODE (33), where . Since is a closed set of , it is a compact set as well. Following the same lines of arguments and recalling the envelope theorem (Theorem 3) for local optimum, one further concludes that is a local maximum of .

Step 5 (Saddle Point)

By letting and , we will show that is a (local) saddle point of the objective function if .

Now suppose the sequence generated from (46) converges to a stationary point . Since step 3 implies that is a local minimum of over feasible set , there exists a such that

In order to complete the proof, we must show

| (48) |

and

| (49) |

These two equations imply

which further implies that is a saddle point of . We now show that (48) and (49) hold.

Recall that . We show (48) by contradiction. Suppose . This then implies that for , we have

To show that (49) holds, we only need to show that if . Suppose , then there exists a sufficiently small such that

This again contradicts with the assumption from (70). Therefore (49) holds.

Combining the above arguments, we finally conclude that is a (local) saddle point of if .

Remark 4

When and ,

for any and

In this case one cannot guarantee feasibility using the above analysis, and is not a local saddle point. Such is referred as a spurious fixed point [20]. Practically, by incrementally increasing (see Algorithm 1 for more details), when becomes sufficiently large, one can ensure that the policy gradient algorithm will not get stuck at the spurious fixed point.

Appendix B Technical Details of the Actor-Critic Algorithms

B.1 Assumptions

We make the following assumptions for the proof of our actor-critic algorithms:

(B1) For any state-action pair in the augmented MDP , is continuously differentiable in and is a Lipschitz function in for every , and .

(B2) The augmented Markov chain induced by any policy , , is irreducible and aperiodic.

(B3) The basis functions are linearly independent. In particular, and is full rank.444We may write this as: In particular, the (row) infinite dimensional matrix has column rank . Moreover, for every , , where is the -dimensional vector with all entries equal to one.

(B4) For each , there is a positive probability of being visited, i.e., . Note that from the definition of the augmented MDP , and .

(B5) The step size schedules , , , and satisfy

| (50) | ||||

| (51) | ||||

| (52) |

This indicates that the updates correspond to is on the fastest time-scale, the update corresponds to , are on the intermediate time-scale, where converges faster than , and the update corresponds to is on the slowest time-scale.

(B6) The SPSA step size satisfies as and .

Technical assumptions for the convergence of the actor-critic algorithm will be given in the section for the proof of convergence.

B.2 Gradient with Respect to (Proof of Lemma 1)

Proof. By taking the gradient of w.r.t. (just a reminder that both and are related to through the dependence of the cost function of the augmented MDP on ), we obtain

| (53) | ||||

By unrolling the last equation using the definition of from (B.2), we obtain

B.3 Actor-Critic Algorithm with the Alternative Approach to Compute the Gradients

| TD Errors: | (54) | |||

| (55) | ||||

| Critic Updates: | (56) | |||

| (57) | ||||

| Actor Updates: | (58) | |||

| (59) | ||||

| (60) |

B.4 Convergence of the Actor Critic Algorithms

In this section we want to derive the following convergence results.

Theorem 6

Suppose , where

and is the projected Bellman fixed point of , i.e., . Also suppose the stationary distribution is used to generate samples of for any . Then the updates in the actor critic algorithms converge to almost surely.

Next define

as the residue of the value function approximation at step induced by policy . By triangular inequality and fixed point theorem , it can be easily seen that . The last inequality follows from the contraction mapping argument. Thus, one concludes that .

Theorem 7

Suppose , as goes to infinity and the stationary distribution is used to generate samples of for any . For SPSA based algorithm, also suppose the perturbation sequence satisfies . Then the sequence of -updates in Algorithm 2 converges to a (local) saddle point of our objective function almost surely, it satisfies for some and . Note that represents a hyper-dimensional ball centered at with radius .

Since the proof of the Multi-loop algorithm and the SPSA based algorithm is almost identical (except the update), we will focus on proving the SPSA based actor critic algorithm.

B.4.1 Proof of Theorem 6: TD(0) Critic Update (update)

By the step length conditions, one notices that converges in a faster time scale than , and , one can assume in the update as fixed quantities. The critic update can be re-written as follows:

| (61) |

where the scaler

is known as the temporal difference (TD). Define

| (62) |

and

| (63) |

Based on the definitions of matrices and , it is easy to see that the TD(0) critic update in (61) can be re-written as the following stochastic approximation scheme:

| (64) |

where the noise term is a square integrable Martingale difference, i.e, if the stationary distribution used to generate samples of . is the filtration generated by different independent trajectories. By writing

and noting , one can easily check that the stochastic approximation scheme in (61) is equivalent to the TD(0) iterates in (61) and is a Martingale difference, i.e., . Let

Before getting into the convergence analysis, we have the following technical lemma.

Lemma 8

Every eigenvalues of matrix has positive real part.

Proof. To complete this proof, we need to show that for any vector , . Now, for any fixed , define . It can be easily seen from the definition of that

By convexity of quadratic functions and Jensen’s inequality, one can derive the following expressions:

where and

The first inequality is due to the fact that and convexity of quadratic function, the second equality is based on the stationarity property of a visiting distribution: , and

As the above argument holds for any and , one shows that for any . This further implies and for any . Therefore, is a symmetric positive definite matrix, i.e. there exists a such that . To complete the proof, suppose by contradiction that there exists an eigenvalue of which has a non-positive real-part. Let be the corresponding eigenvector of . Then, by pre- and post-multiplying and to and noting that the hermitian of a real matrix is , one obtains . This implies , i.e., a contradiction. By combining all previous arguments, one concludes that every eigenvalues has positive real part.

We now turn to the analysis of the TD(0) iteration. Note that the following properties hold for the TD(0) update scheme in (61):

-

1.

is Lipschitz.

-

2.

The step size satisfies the following properties in Appendix B.1.

-

3.

The noise term is a square integrable Martingale difference.

-

4.

The function

converges uniformly to a continuous function for any in a compact set, i.e., as .

-

5.

The ordinary differential equation (ODE)

has the origin as its unique globally asymptotically stable equilibrium.

The fourth property can be easily verified from the fact that the magnitude of is finite and . The fifth property follows directly from the facts that and all eigenvalues of have positive real parts. Therefore, by Theorem 3.1 in [14], these five properties imply the following condition:

Finally, from the standard stochastic approximation result, from the above conditions, the convergence of the TD(0) iterates in (61) can be related to the asymptotic behavior of the ODE

| (65) |

By Theorem 2 in Chapter 2 of [14], when property (1) to (3) in (65) hold, then with probability where the limit depends on and is the unique solution satisfying , i.e., . Therefore, the TD(0) iterates converges to the unique fixed point almost surely, at .

B.4.2 Proof of Theorem 7

Step 1 (Convergence of update)

The proof of the critic parameter convergence follows directly from Theorem 6.

Step 2 (Convergence of SPSA based update)

In this section, we present the update for the incremental actor critic method. This update is based on the SPSA perturbation method. The idea of this method is to estimate the sub-gradient using two simulated value functions corresponding to and . Here is a positive random perturbation that vanishes asymptotically.

The SPSA-based estimate for a sub-gradient is given by:

where is a “small” random perturbation of the finite difference sub-gradient approximation.

Now, we turn to the convergence analysis of sub-gradient estimation and update. Since converges faster than , and converges faster then and , the update in (18) can be rewritten using the converged critic-parameter and ) in this expression is viewed as constant quantities, i.e.,

| (66) |

First, we have the following assumption on the feature functions in order to prove the SPSA approximation is asymptotically unbiased.

Assumption 9

For any , the feature function satisfies the following conditions

Furthermore, the Lipschitz constants are uniformly bounded, i.e., .

This assumption is mild because the expected utility objective function implies that is Lipschitz in , and is just a linear function approximation of . Then, we establish the bias and convergence of stochastic sub-gradient estimates. Let

and

where

Note that (66) is equivalent to

| (67) |

First, it is obvious that is a Martingale difference as , which implies

is a Martingale with respect to filtration . By Martingale convergence theorem, we can show that if , when , converges almost surely and almost surely. To show that , for any one observes that,

Now based on Assumption 9, the above expression implies

Combining the above results with the step length conditions, there exists such that

Second, by the “Min Common/Max Crossing” theorem, one can show is a non-empty, convex and compact set. Therefore, by duality of directional directives and sub-differentials, i.e.,

one concludes that for (converges in a slower time scale),

This further implies that

Third, since , from definition of it is obvious that . When goes to infinity, by assumption and . Finally, as we have just showed that , and almost surely, the update in (67) is a stochastic approximations of an element in the differential inclusion

Now we turn to the convergence analysis of . It can be easily seen that the update in (18) is a noisy sub-gradient descent update with vanishing disturbance bias. This update can be viewed as an Euler discretization of the following differential inclusion

| (68) |

Thus, the convergence analysis follows from analogous convergence analysis in step 1 of Theorem 2’s proof.

Step 3 (Convergence of update)

We first analyze the actor update (update). Since converges in a faster time scale than , one can assume in the update as a fixed quantity. Furthermore, since and converge in a faster scale than , one can also replace and with their limits and in the convergence analysis. In the following analysis, we assume that the initial state is given. Then the update in (19) can be re-written as follows:

| (69) |

Similar to the trajectory based algorithm, we need to show that the approximation of is Lipschitz in in order to show the convergence of the parameter. This result is generalized in the following proposition.

Proposition 10

The following function is a Lipschitz function in :

Proof. First consider the feature vector . Recall that the feature vector satisfies the linear equation where and are functions of found from the Hilbert space projection of Bellman operator. It has been shown in Lemma 1 of [7] that, by exploiting the inverse of using Cramer’s rule, one can show that is continuously differentiable of . Next, consider the visiting distribution . From an application of Theorem 2 of [1] (or Theorem 3.1 of [31]), it can be seen that the stationary distribution of the process is continuously differentiable in . Recall from Assumption (B1) that is a Lipschitz function in for any and and is differentiable in . Therefore, by combining these arguments and noting that the sum of products of Lipschitz functions is Lipschitz, one concludes that is Lipschitz in .

Consider the case in which the value function for a fixed policy is approximated by a learned function approximator, . If the approximation is sufficiently good, we might hope to use it in place of and still point roughly in the direction of the true gradient. Recall the temporal difference error (random variable) for given

Define the dependent approximated advantage function

where

The following Lemma first shows that is an unbiased estimator of .

Lemma 11

For any given policy and , we have

Proof. Note that for any ,

where

By recalling the definition of , the proof is completed.

Now, we turn to the convergence proof of .

Theorem 12

Suppose is the equilibrium point of the continuous system satisfying

| (70) |

Then the sequence of updates in (19) converges to almost surely.

Proof. First, the update from (69) can be re-written as follows:

where

| (71) |

is a square integrable stochastic term of the update and

where is the “compatible feature”. The last inequality is due to the fact that for being a probability measure, convexity of quadratic functions implies

Then by Lemma 11, if the stationary distribution is used to generate samples of , one obtains , where is the filtration generated by different independent trajectories. On the other hand, as . Therefore, the update in (69) is a stochastic approximation of the ODE

with an error term that is a sum of a vanishing bias and a Martingale difference. Thus, the convergence analysis of follows analogously from the step 2 of Theorem 2’s proof.

Step 4 (Local Minimum)

The proof of local minimum of follows directly from the arguments in Step 3 of Theorem 2’s proof.

Step 5 (The update and Convergence to Saddle Point)

Notice that update converges in a slowest time scale, (18) can be rewritten using the converged , and , i.e.,

| (72) |

where

| (73) |

is a square integrable stochastic term of the update. Similar to the update, by using the stationary distribution , one obtains where is the filtration of generated by different independent trajectories. As above, the update is a stochastic approximation of the ODE

with an error term that is a Martingale difference. Then the convergence and the (local) saddle point analysis follows from analogous arguments in step 4 and 5 of Theorem 2’s proof.

Step (Convergence of Multi-loop update)

Since converges on a faster timescale than and , the update in (21) can be rewritten using the fixed , i.e.,

| (74) |

and

| (75) |

is a square integrable stochastic term of the update. It is obvious that , where is the corresponding filtration of , the update in (21) is a stochastic approximations of an element in the differential inclusion for any with an error term that is a Martingale difference, i.e.,

Thus, the update in (74) can be viewed as an Euler discretization of the differential inclusion in (68), and the convergence analysis follows from analogous convergence analysis in step 1 of Theorem 2’s proof.

Appendix C Experimental Results

C.1 Problem Setup and Parameters

The house purchasing problem can be reformulated as follows

| (76) |

where . We will set the parameters of the MDP as follows: , , , , , and . For the risk constrained policy gradient algorithm, the step-length sequence is given as follows,

The CVaR parameter and constraint threshold are given by and . The number of sample trajectories is set to .

For the risk constrained actor critic algorithm, the step-length sequence is given as follows,

The CVaR parameter and constraint threshold are given by and . One can later see that the difference in risk thresholds is due to the different family of parametrized Boltzmann policies.

The parameter bounds are given as follows: , and .

C.2 Trajectory Based Algorithms

In this section, we have implemented the following trajectory based algorithms.

-

1.

PG: This is a policy gradient algorithm that minimizes the expected discounted cost function, without considering any risk criteria.

-

2.

PG-CVaR: This is the CVaR constrained simulated trajectory based policy gradient algorithm that is given in Section 4.

It is well known that a near-optimal policy was obtained using the LSPI algorithm with 2-dimensional radial basis function (RBF) features. We will also implement the 2-dimensional RBF feature function and consider the family Boltzmann policies for policy parametrization

The experiments for each algorithm comprised of the following two phases:

-

1.

Tuning phase: Here each iteration involved the simulation run with the nominal policy parameter where the run length for a particular policy parameter is at most steps. We run the algorithm for 1000 iterations and stop when the parameter converges.

-

2.

Converged run: Followed by the tuning phase, we obtained the converged policy parameter . In the converged run phase, we perform simulation with this policy parameter for runs where each simulation generates a trajectory of at most steps. The results reported are averages over these iterations.

C.3 Incremental Based Algorithm

On the other hand, we have also implemented the following incremental based algorithms.

-

1.

AC: This is an actor critic algorithm that minimizes the expected discounted cost function, without considering any risk criteria. This is similar to Algorithm 1 in [6].

-

2.

AC-CVaR-Semi-Traj.: This is the CVaR constrained multi-loop actor critic algorithm that is given in Section 5.

-

3.

AC-CVaR-SPSA: This is the CVaR constrained SPSA actor critic algorithm that is given in Section 5.

Similar to the trajectory based algorithms, we will implement the RBFs as feature functions for and consider the family of augmented state Boltzmann policies,

Similarly, the experiments also comprise of two phases: 1) the tuning phase where the set of parameters is obtained after the algorithm converges, and 2) the converged run where the policy parameter is simulated for runs.

Appendix D Bellman Equation and Projected Bellman Equation for Expected Utility Function

D.1 Bellman Operator for Expected Utility Functions

First, we want find the Bellman equation for the objective function

| (77) |

where and are given.

For any function , recall the following Bellman operator on the augmented space :

First, it is easy to show that this Bellman operator satisfies the following properties.

Proposition 13

The Bellman operator has the following properties:

-

•

(Monotonicity) If , for any , , then .

-

•

(Constant shift) For , .

-

•

(Contraction)

where .

Proof. The proof of monotonicity and constant shift properties follow directly from the definitions of the Bellman operator. Furthermore, denote . Since

by monotonicity and constant shift property,

This further implies that

and the contraction property follows.

The following theorems show there exists a unique fixed point solution to , where the solution equals to the value function expected utility.

Theorem 14 (Equivalence Condition)

For any bounded function , there exists a limit function such that . Furthermore,

Proof. The first part of the proof is to show that for any and ,

| (78) |

by induction. For , . By induction hypothesis, assume (78) holds at . For ,

Thus, the equality in (78) is proved by induction.

The second part of the proof is to show that and

From the assumption of transient policies, one note that for any there exists a sufficiently large such that for . This implies . Since is bounded for any and , the above arguments imply

The first inequality is due to the fact for , ,

the second inequality is due to 1) is bounded, when and 2) for sufficiently large and any ,

The first equality follows from the definition of transient policies and the second equality follows from the definition of stage-wise cost in the augmented MDP.

By similar arguments, one can also show that

Therefore, by taking , we have just shown that for any , .

Apart from the analysis in [4] where a fixed point result is defined based on the following specific set of functions , we are going to provide the fixed point theorem for general spaces of augmented value functions.

Theorem 15 (Fixed Point Theorem)

There exists a unique solution to the fixed point equation: , and . Let be such unique fixed point solution. Then,

Proof. For starting at one obtains by contraction that . By the recursive property, this implies

It follows that for every and ,

Therefore, is a Cauchy sequence and must converge to since is a complete space. Thus, we have for ,

Since converges to , the above expression implies for any . Therefore, is a fixed point. Suppose there exists another fixed point . Then,

for . This implies that . Furthermore, since with being an arbitrary initial value function. By the following convergence rate bound inequality

one concludes that for any .

D.2 The Projected Bellman Operator

Consider the dependent linear value function approximation of , in the form of , where represents the state-dependent feature. The feature vectors can also be dependent on as well. But for notational convenience, we drop the indices corresponding to . The low dimensional subspace is therefore where is a function mapping such that . We also make the following standard assumption on the rank of matrix . More information relating to the feature mappings and function approximation can be found in Appendix. Let be the best approximation parameter vector. Then is the best linear approximation of .

Our goal is to estimate from simulated trajectories of the MDP. Thus, it is reasonable to consider the projections from onto with respect to a norm that is weighted according to the occupation measure , where is the initial condition of the augmented MDP. For a function , we introduce the weighted norm: where is the occupation measure (with non-negative elements). We also denote by the projection from to . We are now ready to describe the approximation scheme. Consider the following projected fixed point equation

where is the Bellman operator with respect to policy and let denote the solution of the above equation. We will show the existence of this unique fixed point by the following contraction property of the projected Bellman operator: .

Lemma 16

There exists such that

Proof. Note that the projection operator is non-expansive:

One further obtains the following expression:

The first inequality is due to the fact that and convexity of quadratic function, the second equality is based on the property of visiting distribution. Thus, we have just shown that is contractive with .

Therefore, by Banach fixed point theorem, a unique fixed point solution exists for equation: for any , . Denote by the fixed point solution and be the corresponding weight, which is unique by the full rank assumption. From Lemma 16, one obtains a unique value function estimates from the following projected Bellman equation:

| (79) |

Also we have the following error bound of the value function approximation.

Lemma 17

Let be the fixed point solution of and be the unique solution for . Then, for some ,

Proof. Note that by the Pythagorean theorem of projection,

Therefore, by recalling , the proof is completed by rearranging the above inequality.

This implies that if , for any .

Note that we can re-write the projected Bellman equation in explicit form as follows:

By the definition of projection, the unique solution satisfies

By the projection theorem on Hilbert space, the orthogonality condition for becomes:

This condition can be written as where

| (80) |

is a finite dimensional matrix in and

| (81) |

is a finite dimensional vector in . The matrix is invertible since Lemma 16 guarantees that (79) has a unique solution . Note that the projected equation can be re-written as

for any positive scaler . Specifically, since

one obtains

where the occupation measure is a valid probability measure. Recall from the definitions of that

where is the expectation induced by the occupation measure (which is a valid probability measure).

Appendix E Supplementary: Gradient with Respect to

By taking gradient of with respect to , one obtains

where

Since the above expression is a recursion, one further obtains

By the definition of occupation measures, the above expression becomes

| (82) |

where

is the advantage function. The last equality is due to the fact that

Thus, the gradient of the Lagrangian function is