The Log-Shift Penalty for Adaptive Estimation of Multiple Gaussian Graphical Models

Abstract

Sparse Gaussian graphical models characterize sparse dependence relationships between random variables in a network. To estimate multiple related Gaussian graphical models on the same set of variables, we formulate a hierarchical model, which leads to an optimization problem with a nonconvex log-shift penalty function. We show that under mild conditions the optimization problem is convex despite the inclusion of a nonconvex penalty, and derive an efficient optimization algorithm. Experiments on both synthetic and real data show that the proposed method is able to achieve good selection and estimation performance simultaneously, because the nonconvexity of the log-shift penalty allows for weak signals to be thresholded to zero without excessive shrinkage on the strong signals.

1 Introduction and background

For a set of variables , a graphical model is commonly used to reflect sparse dependence structure among the variables. The presence of an edge reflects that variables and are dependent even after controlling for the effects of the remaining variables. If , the resulting model is known as a Gaussian graphical model (GGM), and in this case the edges (i.e. conditional dependencies) correspond to nonzero entries in the precision matrix, . The log-likelihood for after observing iid draws of is given by

where is the sample covariance of the iid observations. These types of models arise in a wide range of applications, including genetics (modeling interactions among gene expression levels), finance (finding interactions between different stock prices), and social networks (modeling relationships among people, spread of information or disease, etc).

In a high-dimensional setting, where we observe iid realizations of for a sample size , the sparsity of the precision matrix allows us to accurately estimate the distribution of even though is in general not identifiable from samples. A well-studied convex approach to finding is the graphical Lasso [5], which calculates111 In some works in the literature, is penalized, i.e. the diagonal elements are not excluded from the penalty, but we exclude them to facilitate comparison with our work.

| (1) |

The penalty term promotes sparsity—due to the shrinkage on the off-diagonal entries of , many of the ’s (for ) will be zero when is sufficiently large. Under some conditions, the graphical Lasso is consistent for edge selection in sparse models, even at sample size [13].

Multiple graphs

In some applications, we may have multiple sets of observations with related (but not necessarily identical) covariance structures, for instance when the same variables are measured across different settings (such as gene expression levels in healthy vs in cancerous tissues [3] or across different phases of an organism’s life cycle [9]). Suppose that we observe data from different GGMs with similar sparsity structures, and would like to estimate the precision matrices jointly. Let be the log-likelihood for the th data set given by

for th sample size and th sample covariance matrix . Danaher et al. [3] propose the group graphical Lasso:

| (2) |

where is the feasible set of positive semidefinite matrix sequences,

and is the vector of coefficients at position across the settings. If , the solution reduces to performing a graphical Lasso on each data set ; no information is shared across the tasks. At the other extreme, for , the penalty ensures identical sparsity patterns across the estimated precision matrices.

A nonconvex approach

For the single graph setting (), recent work by Wong et al. [15] proposes an adaptive, nonconvex approach, defined by a hierarchical model for each :

| (3) | ||||

This hierarchical model can be viewed as a graphical model version of the Bayesian Lasso introduced by Park and Casella [11]. Marginalizing over , this induces a marginal (improper) density , leading to the MAP estimation problem

| (4) |

This procedure is adaptive because, due to the concavity of the log penalty, large entries suffer less shrinkage when estimated, as compared to an -norm penalty like the graphical Lasso. Empirically, Wong et al. [15] find that the adaptive nonconvex penalty leads to improvements relative to the graphical Lasso (1) in terms of accurate estimation and support recovery. However, the optimization problem (4) is in general nonconvex and may have local minima.

Contributions

In the work presented here, we formulate a hierarchical model for multiple graphs, and derive an optimization problem corresponding to finding the maximum a posteriori (MAP) estimate for . The resulting optimization problem combines a likelihood term with a nonconvex penalty, leading to reduced shrinkage on edges with strong signals (thus improving over convex-penalty methods).

Crucially, even with the nonconvex penalty, our optimization problem is convex under some mild conditions, thus avoiding issues with local minima. Furthermore, we find that the optimization speedup results of Danaher et al. [3] extend to our method. Empirically, our method is able to simultaneously identify the nonzero edges in a graph (model selection) and estimate the parameters on these edges—this is a strong advantage of our nonconvex penalty, which is able to produce a sparse solution while not imposing strong shrinkage on large nonzero estimated values, while convex-penalty methods generally cannot achieve both at the same tuning parameter value.

1.1 Outline

The remainder of this paper is organized as follows. We introduce our method in Section 2, which gives a hierarchical model for the linked GGMs, and derives an objective function to find the maximum a posteriori (MAP) estimate for . We discuss the sparsity and shrinkage properties of our method, in particular as compared to the group graphical Lasso, in Section 2.2. In Section 3 we discuss optimization for the objective function defined by our method, and in particular find conditions that lead to a convex optimization problem that can be split into smaller subproblems (connected components of the graphs); proofs for the results in this section can be found in Appendix A. We present experiments on simulated data and on stock price data in Section 4. Finally, we conclude with a brief discussion of our work and of future directions in Section 5.

2 Methodology

2.1 A hierarchical model for multiple GGMs

Consider the following hierarchical models for Gaussian graphical models with nodes each:

| (5) | ||||

We place a flat prior on and on the diagonal entries . Of course, we must require for each . We may also choose to allow improper priors for by allowing and/or to be zero.

This hierarchical model characterizes our prior belief regarding shared structure across the graphs. The common structure across the graphs is governed by the shared parameter for the weights on the same edge in different graphs. The hyperparameters and control the magnitude and the variation of the ’s and thus the sparsity pattern of the graphs.

Marginal distribution of given

We now calculate the marginal prior density of :

| (6) |

where the last step is obtained by marginalizing over and dividing by the constant . When , even though our hierarchical model takes a different form than the model (3) proposed by [15], we obtain the same marginal distribution of when we set and . However, we will show later on that choosing nonzero will allow for a convex optimization problem.

The posterior MAP

Combining the marginal prior on (6) with the log-likelihoods from the data sets, we would like to calculate the maximum a posteriori (MAP) estimate:

| (7) |

where (we introduce this reparametrization for later convenience). This penalized likelihood function combines a convex negative-log-likelihood term with a nonconvex “log-shift” penalty. While the underlying hierarchical model requires by construction, we relax this to .

A generalization

We can also consider replacing in (7) with any convex regularizer , which leads to the optimization problem

| (8) |

As an important example, we can consider a (sparse) group Lasso penalty on each :

In fact, the penalized likelihood optimization problem in (8) can be motivated by a generalization of our hierarchical model from Section 2.1. If for some norm , take

| (9) | ||||

Next, marginalizing over (following similar steps as in (6) earlier),

Combining this with the likelihood terms yields the penalized optimization problem (8).

2.2 Sparsity and shrinkage of

We next examine the effects of the parameters and in the log-shift objective function (8), which arise from and in the hierarchical model (9). To understand their role in inducing sparsity and shrinkage in , we first consider the function

In a sparse regression setting, this type of penalty function has been studied by Candes et al. [1] and others in the context of reweighted minimization, and was found to preserve the desirable sparsity properties of regularization while reducing the amount of shrinkage on large coefficients.

The penalty function behaves like a penalty when , which we can see by taking a local linear approximation to the log function:

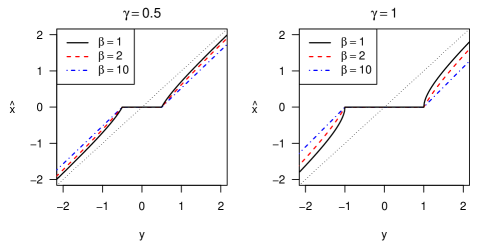

On the other hand, as grows large, the concavity of the log function becomes apparent, and therefore there is less shrinkage on large values of . See Figure 1 for an illustration.

Next, we return to our prior distribution on . Comparing the penalized likelihood function (8) with our calculations with above, we can interpret the parameters and in (8) as follows:

-

•

controls the amount of penalization on , and thus the sparsity level of the solution.

-

•

controls the nonconvexity of the penalty, with small yielding reduced shrinkage in the estimate of (but possible nonconvexity of the objective function), while causes the penalty term to approach .

2.3 Other related work

The graphical Lasso [5] and group graphical Lasso [3] methods, discussed above in (1) and (2), both propose estimation of via a convex penalty. Our method may be viewed as a generalization of the group graphical Lasso, which is obtained by setting in our log-shift penalty.

Turning to nonconvex methods, in addition to Wong et al. [15]’s model described in (3) above, we are aware of several other methods using nonconvex regularization, all of which allow for reduced shrinkage on large entries, but may potentially lead to nonconvex optimization problems. First, for estimation of a single graph, Fan et al. [4] apply an adaptive Lasso (reweighted ) penalty to the GGM setting, optimizing

where is some initial estimate of . In fact, for , this reweighted penalty is can be viewed as a single iteration towards solving Wong et al. [15]’s MAP estimation problem (4), although this is not the approach taken in [15] (see [1] for the sparse regression setting). Fan et al. [4] also examine a SCAD penalty on each , which behaves similarly.

Finally, in the multiple graph setting, Guo et al. [7] propose the optimization problem

| (10) |

This nonconvex penalty encourages similar sparsity patterns in the graphs, but does not allow for tuning the amount of nonconvexity or the balance between shared support vs different support.

3 Convexity and optimization

In this section, we derive a simple condition on the parameters and in our log-shift method (8) that guarantees the convexity of the objective function over a bounded set. We then develop a majorization-minimization algorithm for finding the global minimum, and a preprocessing step where the graphs are split into connected components, allowing for smaller optimization problems that can be solved in parallel. While we are primarily interested in regularizers of the form , our results apply more generally to any convex regularizer .

3.1 Convexity

To ensure that is convex, we will place a bound on to obtain strong convexity of the likelihood term, while placing a lower bound on to control the nonconvexity of the penalty term. The result below may be viewed as an application of Loh and Wainwright [10]’s results on nonconvex regularizers.

The condition that we require on is mild. For any , define

where is the matrix operator norm (largest singular value). This is a reasonable nondegeneracy condition on the graphical models underlying the data.

Theorem 1.

If is convex, nonnegative, and -Lipschitz, and if

| (11) |

then is convex over . If (11) is satisfied with a strict inequality, then we obtain strict convexity.

We note that this allows for a value of that is very small if the sample sizes are large, that is, even if the penalty is highly nonconvex, as desired to avoid excessive shrinkage on strong signals. The proof of this theorem, given in Appendix A, simply shows that the strong convexity of the likelihood term in is sufficient to counterbalance the concavity of the log penalty.

3.2 Optimization via majorization-minimization

To minimize we use majorization-minimization [8]. Let be our current estimate of . Since is concave, we bound by the linear approximation centered at :

Then the objective function is bounded as

with equality at . Note that is a convex function of . Therefore, to find ,

-

1.

Initialize (or any other initial value).

-

2.

For , solve the convex optimization problem

(12) -

3.

Stop when some convergence criterion has been reached.

For optimizing (12), if is chosen to be the sparse group Lasso regularizer

then the step (12) is equivalent to a weighted group graphical Lasso problem [3], but with an additional constraint that ; this constraint can be added to the ADMM algorithm for group graphical Lasso given in [3] with no additional computational cost.

If the objective function is convex over —that is, if our choices of , , and satisfy the condition (11) of Theorem 1—then majorization-minimization is guaranteed to converge to a globally optimal solution [16]. In practice, we may choose to remove the bound on the spectral norms, or equivalently, explore concavity of the penalty beyond what is allowed in the convexity condition (11), since lower values of may perform better empirically.

3.3 Separation into connected components

For the graphical Lasso (1), Witten et al. [14] proved that the connected components of the solution can be identified in a preprocessing step that simply requires screening for sample correlations that exceed the penalty parameter value . This allows for significantly faster optimization of the graphical Lasso. Theorem 2 of Danaher et al. [3] extends this result to the group graphical Lasso setting, by screening for any such that

| (13) |

and then solving separate optimization problems for each resulting connected component. Their results prove that the combined solution is a global minimizer of the group graphical Lasso (2).

This type of block-wise optimization can be extended to the nonconvex log-shift penalty:

Theorem 2.

Consider any partition of into disjoint sets. Suppose that

| (14) |

where . If the conditions of Theorem 1 are satisfied, then there exists some such that for all and all .

In particular, if , then condition (14) is equivalent to Danaher et al. [3]’s condition (13) for the group graphical Lasso. Although our penalty is nonconvex, near zero it is approximately equal to the group graphical Lasso penalty (or, more generally, when ). This allows us to extend the proof techniques of [3] to this nonconvex penalty setting. Theorem 2 is proved in Appendix A.

Based on this result, we now propose a faster algorithm for minimizing .

-

1.

Partition into sets , the connected components of the adjacency matrix :

- 2.

-

3.

concatenates the blocks: for all , and for all .

If the convexity condition (11) is satisfied, then Theorems 1 and 2 guarantee that the resulting solution is a global minimizer of over the set .

4 Experiments

4.1 Simulations

Data and methods

We simulate tridiagonal precision matrices of dimension , following the autoregressive (AR) process example in Fan et al. [4]. The precision matrices have identical tridiagonal support, but have different nonzero values (see example 4.1 in [4] for details). For each , we draw iid samples from the distribution .

To implement our proposed method, we take and minimize the objective function (8) for different values of tuning parameters . We also test the group graphical Lasso [3], the graphical Lasso [5], and Guo et al. [7]’s square-root method, for comparison. 222Computations for simulations and for the real data experiment were performed in R [12] and used the glasso [6] and JGL [2] packages. Code for Guo et al. [7]’s method was obtained from the online supplementary material for [3], available at http://onlinelibrary.wiley.com/journal/10.1111/(ISSN)1467-9868/homepage/76_2.htm.

Results

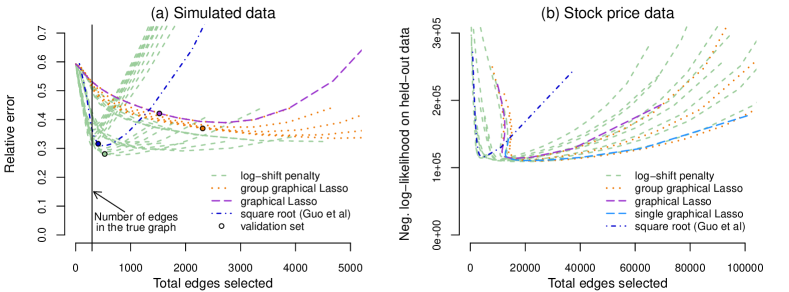

Figure 2(a) displays results from 10 trials. Among the methods considered, the log-shift method attains the lowest error in recovering and simultaneously selects an appropriately low number of edges, when tuning parameters are chosen judiciously (typically with a lower value of , i.e. with high nonconvexity in the penalty). As increases, the performance of our method approaches that of the group graphical Lasso. In order to select appropriate tuning parameters for each method in a data-driven way, we generate a validation data set of same size and compute the log likelihoods of the validation data using the estimated precision matrices. For our model, the estimate selected by the validation score achieves the minimum error measure, and yields a total number of selected edges that is close to the number of true edges.

4.2 Stock price data

Data and methods

We next test our method on stock price data from Yahoo! Finance.333Data available at finance.yahoo.com We collected the daily closing prices for stocks that were consistently in the S&P 500 index from January 1, 2003 to December 31, 2012. Let be the closing price for stock on day , and be the log return. We marginally transform the log returns of each stock to a normal distribution. Denoting the transformed data still as , we treat as independent observations, although they in fact form a time series. We divide the data into two time periods, one for before (2003–2007) and one for after (2009-2012) the 2008 financial crisis, and remove the data from 2008. The two sample sizes are and . In the belief that the relationship between stocks might have changed during the financial crisis, we model the data as two GGMs with similar but non-identical precision matrices. We select 20% of the data in each time period as training data, and hold out the remaining 80% to evaluate the performances. We implement our log-shift method with , and compare to the same existing methods as before. For an additional comparison, we also fit a single graphical Lasso to the combined data set.

Results

To evaluate the results, we calculate the likelihood of the held-out data under the fitted models for each method. Results are displayed in Figure 2(b). While the various methods’ best scores are similar for the log-shift, group graphical Lasso, and single graphical Lasso, the log-shift method is able to attain this best validation score with a substantially smaller number of selected edges relative to the convex methods, demonstrating the benefit of the nonconvex penalty.

5 Discussion

In this paper, we introduce a family of nonconvex penalty functions, called the log-shift function, for estimating multiple related GGMs. It arises from a simple hierarchical model and generalizes existing methods for learning multiple GGMs, such as the group graphical Lasso [3]. Compared with methods that use a convex penalty function, the nonconvexity of the penalty function leads to less bias on strong signals and thus makes it possible to obtain good selection and estimation result at the same time. The log-shift penalty can also be applied to estimating other models, such as undirected graphical models with non-Gaussian distributions, time-varying GGMs, etc., which we leave to future work.

References

- Candes et al. [2008] Emmanuel J Candes, Michael B Wakin, and Stephen P Boyd. Enhancing sparsity by reweighted minimization. Journal of Fourier analysis and applications, 14(5-6):877–905, 2008.

- Danaher [2013] Patrick Danaher. JGL: Performs the Joint Graphical Lasso for sparse inverse covariance estimation on multiple classes, 2013. URL http://CRAN.R-project.org/package=JGL. R package version 2.3.

- Danaher et al. [2013] Patrick Danaher, Pei Wang, and Daniela M Witten. The joint graphical Lasso for inverse covariance estimation across multiple classes. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 2013.

- Fan et al. [2009] Jianqing Fan, Yang Feng, and Yichao Wu. Network exploration via the adaptive Lasso and SCAD penalties. The annals of applied statistics, 3(2):521, 2009.

- Friedman et al. [2008] Jerome Friedman, Trevor Hastie, and Robert Tibshirani. Sparse inverse covariance estimation with the graphical Lasso. Biostatistics, 9(3):432–441, 2008.

- Friedman et al. [2011] Jerome Friedman, Trevor Hastie, and Rob Tibshirani. glasso: Graphical Lasso- estimation of Gaussian graphical models, 2011. URL http://CRAN.R-project.org/package=glasso. R package version 1.7.

- Guo et al. [2011] Jian Guo, Elizaveta Levina, George Michailidis, and Ji Zhu. Joint estimation of multiple graphical models. Biometrika, 98(1):1–15, 2011.

- Hunter and Lange [2004] David R Hunter and Kenneth Lange. A tutorial on MM algorithms. The American Statistician, 58(1):30–37, 2004.

- Kolar et al. [2010] Mladen Kolar, Le Song, Amr Ahmed, Eric P Xing, et al. Estimating time-varying networks. The Annals of Applied Statistics, 4(1):94–123, 2010.

- Loh and Wainwright [2013] Po-Ling Loh and Martin J Wainwright. Regularized M-estimators with nonconvexity: Statistical and algorithmic theory for local optima. In Advances in Neural Information Processing Systems, pages 476–484, 2013.

- Park and Casella [2008] Trevor Park and George Casella. The Bayesian Lasso. Journal of the American Statistical Association, 103(482):681–686, 2008.

- R Core Team [2013] R Core Team. R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria, 2013. URL http://www.R-project.org/.

- Ravikumar et al. [2011] Pradeep Ravikumar, Martin J Wainwright, Garvesh Raskutti, Bin Yu, et al. High-dimensional covariance estimation by minimizing -penalized log-determinant divergence. Electronic Journal of Statistics, 5:935–980, 2011.

- Witten et al. [2011] Daniela M Witten, Jerome H Friedman, and Noah Simon. New insights and faster computations for the graphical Lasso. Journal of Computational and Graphical Statistics, 20(4):892–900, 2011.

- Wong et al. [2013] Eleanor Wong, Suyash Awate, and P Thomas Fletcher. Adaptive sparsity in Gaussian graphical models. In Proceedings of The 30th International Conference on Machine Learning, pages 311–319, 2013.

- Wu [1983] CF Jeff Wu. On the convergence properties of the EM algorithm. The Annals of statistics, pages 95–103, 1983.

Appendix A Proofs

Proof of Theorem 1.

For any with ,

Then

is a convex function over . Applying Lemma 1 given below, the function

is convex, and so the following is a convex function over :

where the switch from a to a in the last step comes from the fact that is penalized for but not .

This proves that is convex over as long as for all , which is equivalent to the condition in the theorem. If this inequality is strictly satisfied, then this implies strict convexity of . ∎

Lemma 1.

Let be a -Lipschitz convex nonnegative function and fix any . Then

is a convex function.

Proof.

Take any , and any . Then, using the convexity of ,

| Since for all , | ||||

Then

proving convexity of the function as desired. ∎

Proof of Theorem 2.

Define

and let

We will show that is a minimizer of over the larger set .

Take any with for each . Let and be the block-diagonal and off-block-diagonal parts of ; that is,

Suppose that . Then

and so

proving that . Then by optimality of over the set ,

Then

| Since and are nonzero only when are in the same block, and is nonzero only if are in different blocks, | ||||

| Letting , | ||||

| By optimality of over , | ||||

| Since and is bounded for near , we can apply a Taylor expansion to the difference of terms: | ||||

| Since is block-diagonal and therefore so is , while is supported off of the diagonal blocks, | ||||

| Applying Taylor expansion to the terms , for sufficiently close to , | ||||

| Since is -Lipschitz, | ||||

| Simplifying, | ||||

| If we assume that for all , | ||||

| Cancelling out the terms that are linear in , | ||||

Since is convex over which is itself a convex set, this is sufficient to prove that is a minimizer of over . ∎