On The Longest Chain Rule and

Programmed Self-Destruction

of Crypto Currencies

Abstract

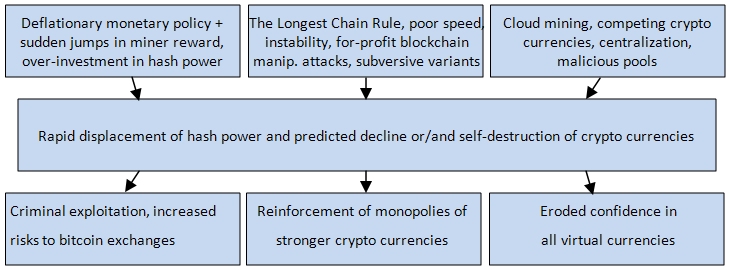

In this paper we revisit some major orthodoxies which lie at the heart of the bitcoin crypto currency and its numerous clones. In particular we look at The Longest Chain Rule, the monetary supply policies and the exact mechanisms which implement them. We claim that these built-in properties are not as brilliant as they are sometimes claimed. A closer examination reveals that they are closer to being… engineering mistakes which other crypto currencies have copied rather blindly. More precisely we show that the capacity of current crypto currencies to resist double spending attacks is poor and most current crypto currencies are highly vulnerable. Satoshi did not implement a timestamp for bitcoin transactions and the bitcoin software does not attempt to monitor double spending events. As a result major attacks involving hundreds of millions of dollars can occur and would not even be recorded, cf. [32]. Hundreds of millions have been invested to pay for ASIC hashing infrastructure yet insufficient attention was paid to ensure network neutrality and that the protection layer it promises is effective and cannot be abused.

In this paper we develop a theory of Programmed Self-Destruction of crypto currencies. We observe that most crypto currencies have mandated abrupt and sudden transitions. These affect their hash rate and therefore their protection against double spending attacks which we do not limit the to the notion of 51 attacks which is highly misleading. Moreover we show that smaller bitcoin competitors are substantially more vulnerable. In addition to lower hash rates, many bitcoin competitors mandate incredibly important adjustments in miner reward. We exhibit examples of ‘alt-coins’ which validate our theory and for which the process of programmed decline and rapid self-destruction has clearly already started.

Note: The author’s blog is blog.bettercrypto.com.

Keywords: electronic payment, crypto currencies, bitcoin, alt-coins, Litecoin, Dogecoin, Unobtanium, double-spending, monetary policy, mining profitability

1 Bitcoin and Bitcoin Clones

Bitcoin is a collaborative virtual currency and payment system. It was launched in 2009 [56] based on earlier crypto currency ideas [4, 27]. Bitcoin implements a certain type of peer-to-peer financial cooperative without trusted entities such as traditional financial institutions. Initially bitcoin was a sort of social experiment, however bitcoins have been traded for real money for several years now and their price have known a spectacular growth [26].

Bitcoin challenges our traditional ideas about money and payment. Ever since Bitcoin was launched [56, 57] in 2009 it has been clear that it is an experimental rather than mature electronic currency ecosystem . A paper at the Financial Cryptography 2012 conference explains that Bitcoin is a system which uses no fancy cryptography, and is by no means perfect [7]. In one sense it is still a play currency in early stages of development. The situation is even worse for bitcoin competitors. Their creators and promoters typically just copy features of bitcoin without any deeper insight into their consequences.

In this paper we are going to see that the exact same rules which might after all work relatively well (at least for some time) for a large dominating crypto currency such as bitcoin, are rather disastrous for smaller crypto currencies.

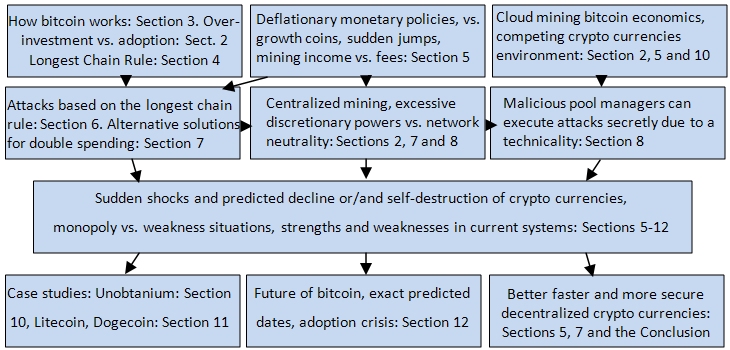

On the picture below we explain the organization of this paper.

2 Bitcoin As A Distributed Business: Its Key Infrastructure and Investor Economics

Bitcoin digital currency [56] is an electronic payment system based on cryptography and a self-governing open-source financial co-operative. Initially it was just a social experiment and concerned only some enthusiasts. However eventually a number of companies have started trading bitcoins for real money. One year ago, in April 2013, the leading financial magazine The Economist recognized bitcoin as a major disruptive technology for finance and famously called bitcoin “digital gold”. We can consider that the history of bitcoin as a mainstream financial instrument started at this moment.

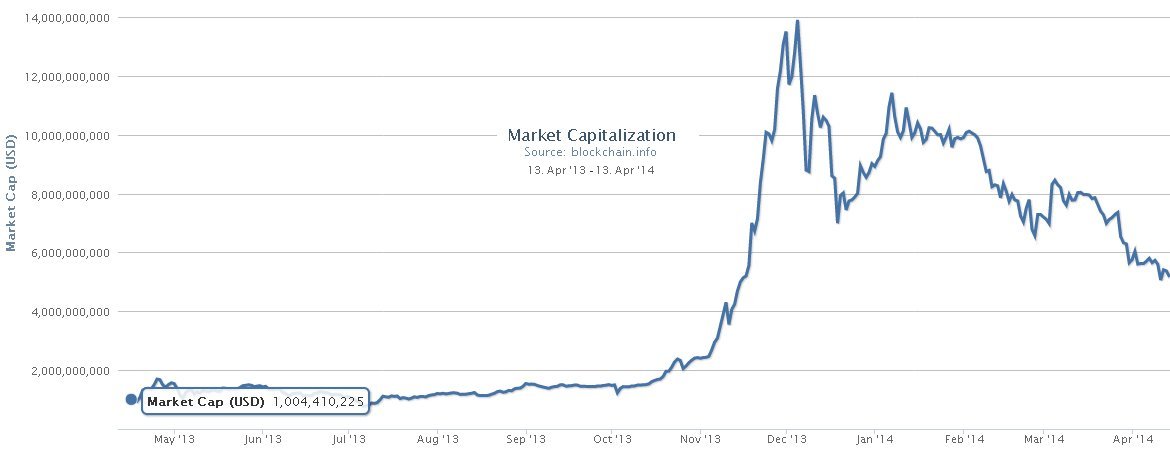

Our starting point of April 2013 coincides more or less with bitcoin achieving prices of 50 USD (and above), the market capitalization exceeding 1 billion dollars, and an important shift in the nature of the ownership of the bitcoin infrastructure. In a great simplification, before April 2013, one bitcoin was rarely worth more than 5-50 dollars, and new bitcoins were produced by amateurs on their PCs. Then a new sort of high-tech industry emerged. Specialized equipment (ASIC machines) whose only purpose is to produce new bitcoins. Such machines are called miners and are increasingly sophisticated [23]. Bitcoin then rapidly switched to the phase where new bitcoins are produced by a restricted111 The inventor of bitcoin has postulated that each peer-to-peer network node should be mining cf. Section 5 of [56]. In practice a strange paradox is that miners mine in very large pools cf. [70] and Table 2 in [25] and the number of ordinary peer-to-peer network nodes is in comparison incredibly low, falling below 8,000 recently cf. [16] . group of some 100,000 for-profit ‘bitcoin miners’ which people have invested money to purchase specialized equipment.

These last 12 months of bitcoin history, April 2013-April 2014, have seen an uninterrupted explosion of investment in bitcoin infrastructure. Surprisingly large sums of money have been spent on purchasing new mining equipment. All this investment has been subject to excessively rapidly decreasing returns. Bitcoin mining is a race against other miners to earn a fairly limited fraction of newly created bitcoins. We examine these questions in detail.

2.1 Investment in Hashing Power and Incredible 1000x Increase

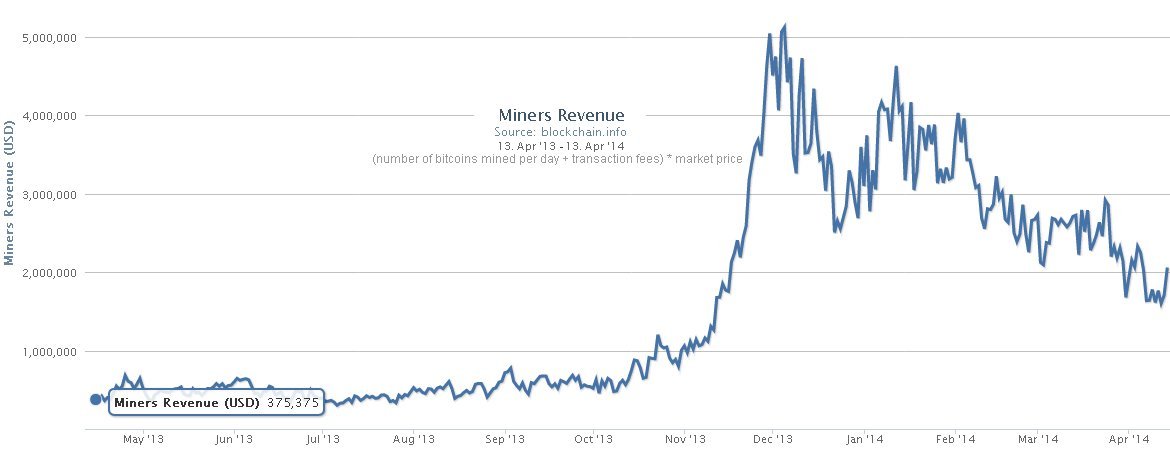

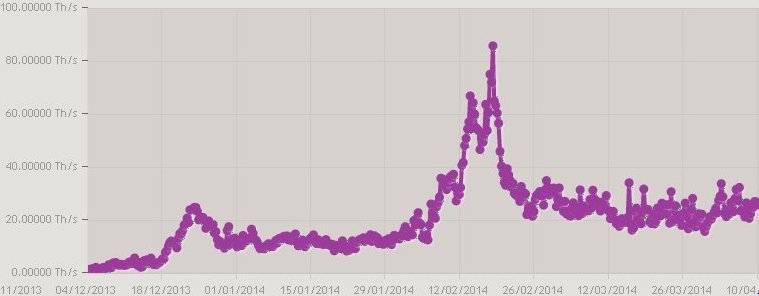

The combined power of bitcoin mining machines has been multiplied by 1000 in the last 12 months cf. Fig. 3. However due to built-in excessively conservative monetary policy cf. [23], during the last 12 months, miners have been competing for a modest fraction of bitcoins yet to be generated. The number of bitcoins in circulation has increased only by 15 , from 11 million to 12.6 million.

A 1000-fold increase in hash power is a very disturbing fact. We lack precise data in order to investigate how much of this increase was due to improved technology (important increase in the speed of bitcoin mining machines, cf. [23]), and how much was due to a surge in investment: more people bought bitcoin miner machines. However it is certain that a monumental amount of money has been invested in these ASIC miner machines. It is not easy to estimate it accurately. If we consider that the current hash rate is composed primarily of KNC Neptune 28 nm miners shipped in December 2013 which for the unit price of 6000 USD can deliver some 0.5 TH/s, we obtain that miners have spent in the last four months maybe 600 millions of dollars on approximately 120,000 ASIC machines which are already in operation222 Similar estimations can be found in [68]. If we consider that more recent miners with capacities between 1-3TH/s were already available for the same price to some privileged buyers many months before officially sold on the retail market, the total cost could be less than our 600M USD estimation.. In addition knowing that more miners were ordered and not yet delivered, it is quite plausible to assume that miners have spent already more than 1 billion dollars on ASIC miners.

As we have already explained, we don’t know exactly how this investment has evolved with time. However the near-doubling of the hash rate every month does certainly mean one thing: excessively rapid decline in mining revenue for every existing ASIC machine.

2.2 Investors Facing Incredibly Fast Erosion of Profitability

This is due to the fact all miners are in competition for a fixed number of bitcoins which can be mined in one month. The rule of thumb is that exactly 25 bitcoins are produced every 10 minutes. Doubling the aggregate hash rate for all bitcoin miners means dividing each individual miner’s income by 2 each month333 Assuming that the cost of electricity is low compared to the income generated and that the price of bitcoin is relatively stable. . It means that investors can only hope for fast short-term gains, and that their income tends to zero very quickly.

Let us develop this argument further. Imagine that a miner invests 5,000 USD and that the income from mining in the first month was 2,000 USD. Is this investment going to be profitable? Most investors will instinctively believe it will be. However in actual bitcoin it isn’t. In the recent 12 months the hash power has been decreasing approximately twice each month. We need to look at the following sum:

We see that the total income is only twice the income for the first month. This is not a lot. In our example the investor will earn only 4,000 USD and has spent 5,000 USD. The investor does not make money, he makes a loss.

2.3 Dividend From Hashing

It is easy to calculate exactly how much money has already been earned by miners in freshly minted bitcoins multiplied by their present market price.

If we estimate the area under Fig. 4 we see that currently all miners combined make some 60 millions of dollars only per month and have been paid roughly some 400 million dollars in mining dividend most of which was earned in the last 4 months. In this paper we neglect the cost of the electricity. Contrary to what was suggested in some press reports [42], this cost has so far remained relatively low for bitcoin mining in comparison to the high cost of ASIC miners which cost needs to be amortized over surprisingly short periods of time of no more than a few months as shown in Section 2.2.

2.4 Investors’ Nightmare

The market for ASIC miner machines is very far from being fair and transparent. There is only a handful of ASIC companies [58] and from their web pages it seems that they might have manufactured and sold only a few thousands units each. In fact most manufacturers have omitted to tell their customers the actual size of their production. It has been much higher than expected, as shown by the hash rate, cf. Fig. 3. Most manufacturers worked with pre-orders. Customers were never able to know when machines were going to be delivered and how much the hash rate would increase in the meantime. Many manufacturers had important delays in delivery, frequently 3, 6, 8, 12 months [58]. Such delays decrease the expected income from mining by an incredibly large factor. We give some realistic examples which based on personal experiences of ourselves and our friends:

-

1.

If for example a miner have ordered his device from ButterflyLabs and the device is delivered 12 months later. He earns roughly 1000 times less than expected (cf. Fig. 3), and even if the price of bitcoin rises 10 times during this period, cf. [26], he still earns maybe 100 times less than expected (!).

-

2.

ButterflyLabs are not the worst. Many miners ordered devices from suppliers which do NOT even exist, and were pure criminal scams, even though they advertise on the Internet and their machines are frequently compared to legitimate ASIC manufacturers on web sites such as https://en.bitcoin.it/wiki/Mining_hardware_comparison which have NOT attempted to distinguish between criminal scams and genuine manufacturers. See Appendix of [25] and http://bitcoinscammers.com for specific examples.

-

3.

A San Francisco-based startup HashFast currently embroiled in many federal fraud lawsuits related to production delays (3 months or longer) and the fact that they promised to refund their customers in bitcoins. However the market price of bitcoins went up significantly. In May 2014 they denied bankruptcy rumors and announced that they will lay off 50 of its staff [60, 58].

-

4.

Another miner ordered his device from BITMINE.CH (also near bankruptcy) and the device was delivered with 6 months delay, he earns roughly 64 times less than expected. Even if the price of bitcoin rises 4 times during this period, and even if BITMINE.CH compensates customers by increasing hash rate by 50 , he still earns maybe 10 times less than expected (!).

-

5.

In another example a miner ordered his device from KNC miner or Cointerra, and the device was delivered with just a one month delay compared to the predicted delivery date. Here the miner earns just half of what was expected, which is already problematic but might be OK.

Overall it is possible to see that most miners were mislead when they ordered the ASIC machines. Miners were probably confused and expected mining profitability to be much higher than what they actually experienced when machines were finally delivered. Accordingly many people lost money in the bitcoin mining business (see also Section 2.3). In addition, many of those who made profits have seen their bitcoins disappear in large-scale thefts, cf. [32].

2.5 Bitcoin Popularity and Bitcoin as Medium of Exchange

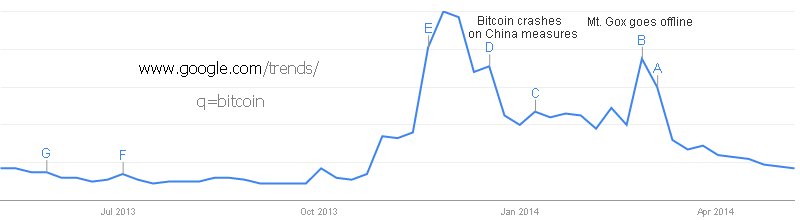

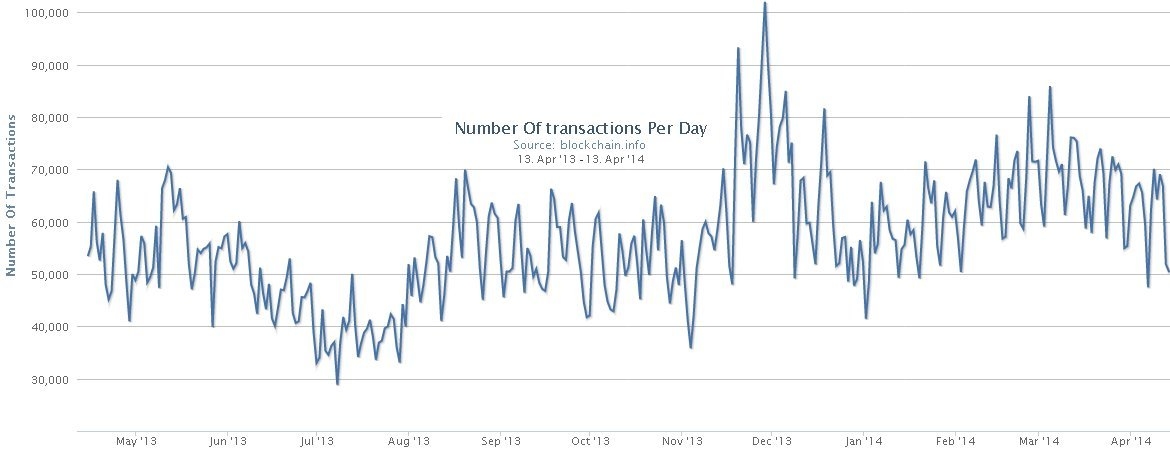

Bitcoin has certainly been very popular among investors in the last 12 months. Has it been popular among the general public? Are they adopting bitcoin as a currency in order to carry ordinary transactions? In Fig. 5 we show the Google trends for the keyword bitcoin. We see that the interest in bitcoin444It has been observed for a very long time that the bitcoin market price cf. Fig. 2 and the popularity of bitcoin in Google search cf. Fig. 5 are strongly correlated. is not growing. In May 2014 there were alarming reports about the total number of full bitcoin network nodes dropping to dangerously low levels of less than 8,000 nodes, cf. [16].

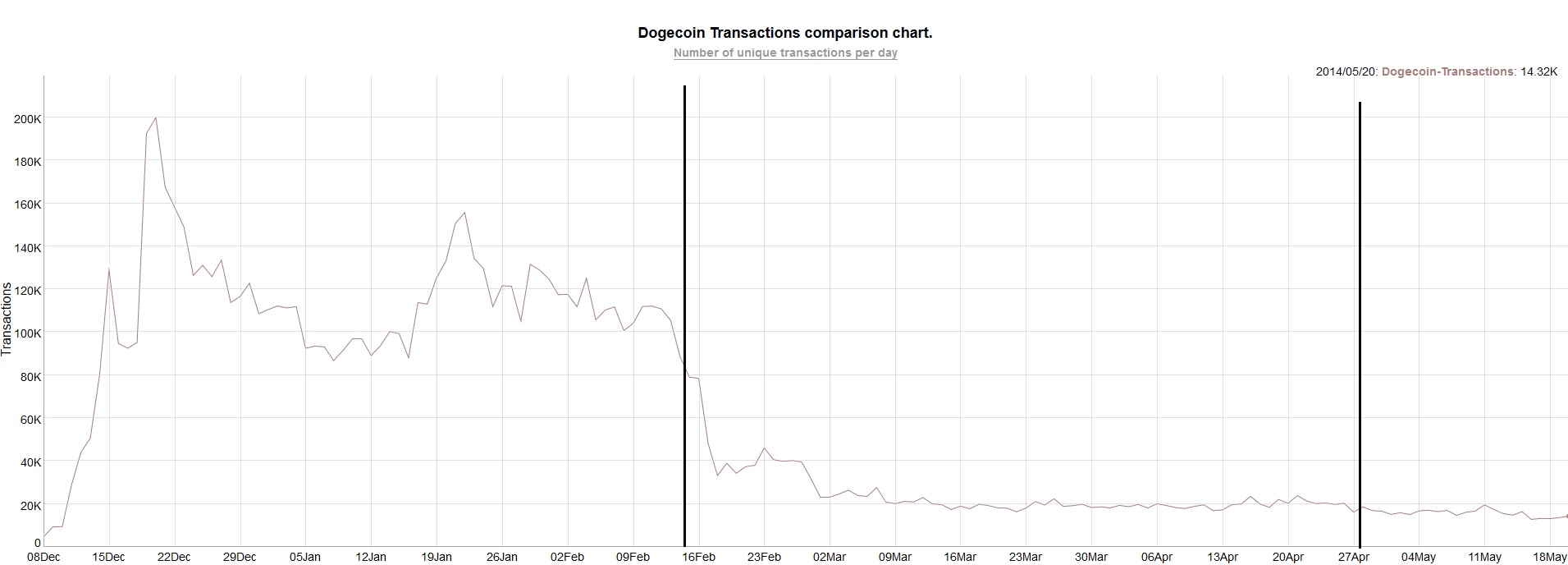

It appears that bitcoin is not used a lot as a currency or payment instrument. The number of transactions in the bitcoin network is NOT growing, cf. Fig. 6 and it can sometimes decrease. The number of merchants accepting bitcoin has been growing recently cf. [67] however the number of transactions wasn’t.

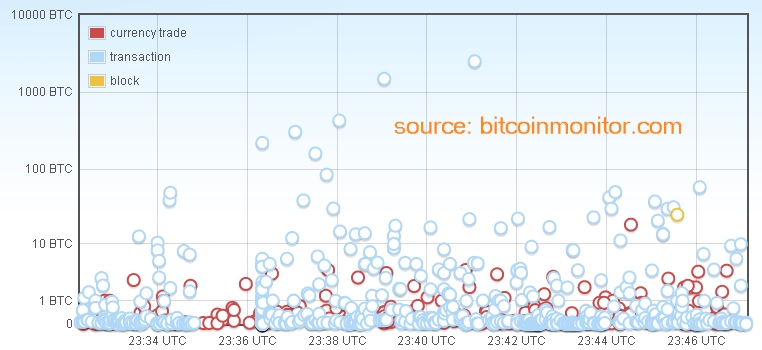

Things get more complicated if we want to look at the transactions in volume. An interesting tool which allows to distinguish between small and large transactions and to visualise their distribution are the real-time graphs produced by http://www.bitcoinmonitor.com/ cf. Fig. 7, cf. also [67]. However these graphs and much of the other data on transaction volume remain very seriously biased by the amounts which bitcoin users return to themselves. This is mandatory in all bitcoin transactions and makes analysis difficult.

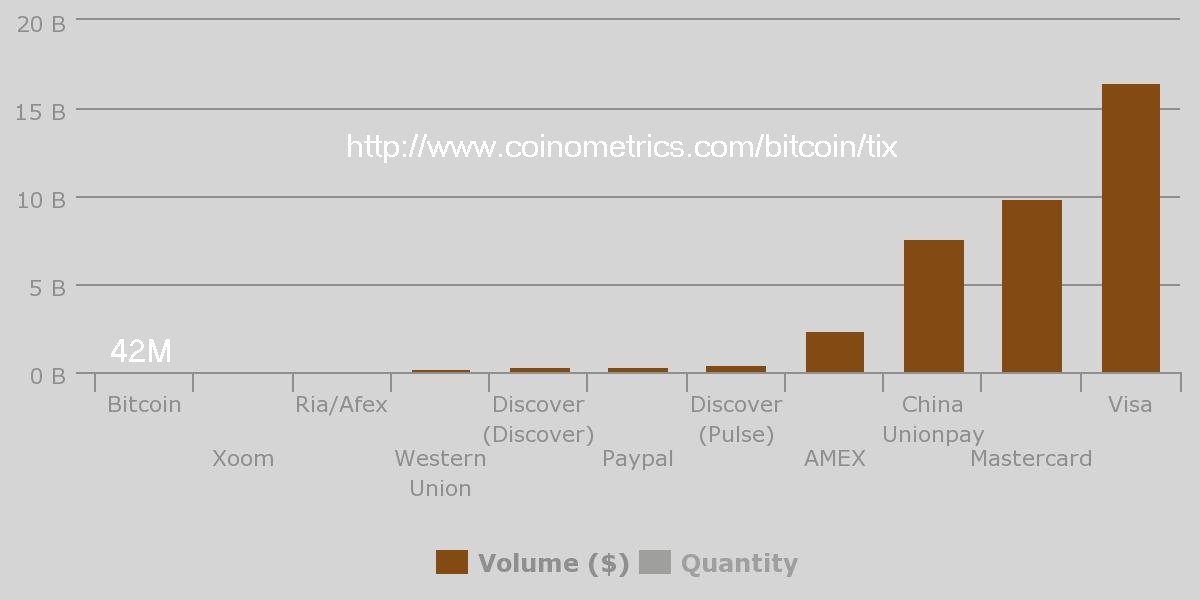

Several press reports have WRONGLY claimed that bitcoin has surpassed Western Union and is catching up with PayPal [76, 53]. These reports are based on bitcoin transaction volume figures which are artificially inflated. They do NOT reflect the actual bitcoin economy. It is easy to see that there is NO easy to way to reliably estimate the transaction volume from the blockchain data555 It is very difficult to reliably estimate the transaction volume from the blockchain data alone. Truly accurate estimations are impossible to obtain. A particular problem are the actions of some bitcoin addresses which hold very large balances and return change to themselves at new freshly created addresses. Another problem are outliers cf. [67]. . The Fitch rating agency has attempted to obtain more accurate data [39]. We learn that bitcoin transaction volume is 68 M per day [2 April 2014] and it remains “small relative to […] traditional payment processors”. A recent press report claims that the transaction volume was at the lowest level in 2 years [33] based on one imperfect method666 Blockhain.info provides both the misleading artificially inflated figures at http://blockchain.info/charts/output-volume and their estimation of the actual transaction volume by their own (imperfect) proprietary method cf. http://blockchain.info/charts/estimated-transaction-volume, cf. also [33, 39, 67]. to eliminate the amounts people return to themselves. The nature of bitcoin makes that we do NOT have a truly reliable source of data on actual bitcoin transactions. However it is possible to see that bitcoin is still about 400 times smaller than VISA, cf. Fig. 8.

Another method to measure the success of bitcoin is to count the unique users of bitcoin wallet applications. Their number has reached 1 million in January 2014 1.5 million was attained in April 2014, and the were 1.6 million in May 2014 777 Cf. http://www.coindesk.com/blockchain-info-reaches-one-million-wallets/ then https://blog.blockchain.com/2014/04/14/blockchain-15m-users/ and https://coinreport.net/blockchain-passes-1-6-million-users-mark/ . This growth is quite positive even though the number of bitcoin transactions is not increasing, as seen in Fig. 6.

We propose an alternative measure of the success of bitcoin as a currency: it will be the transaction fees. The more people are willing to pay in order to transfer money from one person to another using the bitcoin technology, the more successful it is. However we should NOT report fees in bitcoins (as in earlier version of this paper), but in US dollars.

We don’t have great news in this space, the income from fees has been stable or declining. cf. Fig. 9.

2.6 Analysis of Bitcoin From The Point of View of Investors

In the previous sections we have seen that the bitcoin ‘investment economy’ (mining or holding bitcoins for profit) has been thriving in the recent 12 months, while it is very hard to claim that we have seen any growth in adoption of bitcoin in ordinary e-commerce cf. Fig. 9. Moreover we were surprised to discover that the number of active miners seems was much larger than the number of ordinary bitcoin users see see Section 2 and [16].

Consequently we consider that until now the bitcoin business was primarily about some investors (A) spending some 1000 million dollars on mining hardware, and other investors (B) which preferred to buy or use these newly created bitcoins for 400 million dollars and holding them.

We can now argue that the second group (B) has potentially spent MUCH more than 400 million dollars. This is due to the fact that only a small fraction of bitcoins was manufactured in the last 12 months. Investors who in the last 12 months have purchased newly created bitcoins for 400 million dollars (due to Fig. 4) have also purchased a lot more bitcoins from previous owner of bitcoins who are free riders: people who have paid/invested very little mining or purchasing some bitcoins earlier. We lack any precise data but in order to be able to pay some 400 M in to miners (A) 888which has paid for some of their 600+ millions of dollars in hardware expenses, investors (B) must have injected into the bitcoin economy a possibly much larger sum of cash money (dollars). Let us assume that this was 2 billion dollars. This amount is hard to estimate from available data but it is probably a small multiple of 600 M and it cannot be higher than 5 billion dollars, the peak value at Fig. 2.

We can observe that the reason why so much money was made by owners of older coins was the monopoly rent: miners (A) were convinced to mine for this particular crypto currency which has influenced further investors (B) to provide additional funds also for this market. It is probably correct to assume that this is substantially more than the total amount of money invested in mining Litecoin and other crypto currencies, based on the fact that the total Market capitalization of all alternative currencies combined remains small compared to bitcoin, cf. http://www.cryptocoincharts.info/v2/coins/info.

Both investment decisions (A,B) have been made on expectation that the bitcoin market price will rise. In fact during the last 12 months the price has been increasing999This spectacular increase is now suspected to be an effect of a monumental market manipulation. An anonymously published report claims that up to 650,000 bitcoins were bought by two algorithms with money which is suspected to be paid from the customer money held as outstanding balances at the infamous MtGox exchange, cf. [26]. (a lot) just during just one month at the end of 2013 after which we have seen a long painful correction cf. Fig. 2.

The idea that bitcoin market price in dollars will appreciate in the future is based on several premises which in our opinion are more irrational than rational:

-

1.

Bitcoin is expected to imitate the scarcity of rare natural resources such as Gold [34] and for this purpose bitcoin has a fixed monetary supply.

-

2.

However the scarcity of bitcoins is not natural. It is NOT a hard reality. It is really totally artificial. It is mandated by the bitcoin specification and software [56, 57]. This property is not written in stone. It is frequently criticized [23, 77] and it CAN be changed if a majority of miners agree, cf. [23, 40].

-

3.

Investors might be overestimating the importance of bitcoin in the economy in the future: the adoption of bitcoin as a currency or payment instrument cf. Section 2.5.

-

4.

This expectation does not take into account the ‘alt-coins’ (competitors to bitcoin). Alt-coins clearly break the rule of fixed monetary supply of coins and can be created at will, cf. Section 5.6. It cannot be guaranteed that the current monopoly situation of bitcoin is going to last.

Various surveys show that about 50 of people involved with bitcoin do very naively believe that bitcoin will be worth 10,000 USD at the end of 2014, see [66]. Extremely few people have predicted that bitcoin would collapse: one university professor have claimed that bitcoin will go down to 10 USD by June 2014 [51]. This prediction was already largely proven wrong.

2.7 What Does This Monumental Investment Pay For?

We have estimated that for-profit bitcoin miners (A) have invested some 1,000 M dollars in bitcoin infrastructure, while at the same time other investors (B) have invested a yet larger sum of cash money, maybe 2,000 M on buying bitcoins probably driven by a naive101010 The bitcoin market price is rather going down ever since December 2013 cf. Fig. 2 and [26]. expectation that they will rise in the future.

Now the interesting question is, what these monumental investments pay for? Knowing that the bitcoin adoption as a medium of exchange is not expanding as suggested by Fig. 3 these investments went mostly into building an excessive quantity of hashing power (1000x increase). In [61] Sams writes:

”The amount of capital collectively burned hashing fixes the capital outlay required of an attacker to obtain enough hashing power to have a meaningful chance of orchestrating a successful double-spend attack on the system […] The mitigation of this risk is valuable, […]”

We have this expensive and powerful hashing infrastructure. We could call it (ironically) the Great Wall of Bitcoin which name is justified by the fact that bitcoin miners have invested roughly about 1 billion dollars to build it and it is expected to protect bitcoin against attacks. This leads to the following working hypothesis which is really about economics of information security and which we will later dispute. Maybe one must spend a lot of money on the bitcoin hashing infrastructure in order to achieve good security. Maybe there is a large cost associated with building a global distributed financial infrastructure totally independent from governments, large banks, the NSA, etc. Maybe one can hardly hope to spend less and security against double spending attacks has some inherent price which needs to be paid.

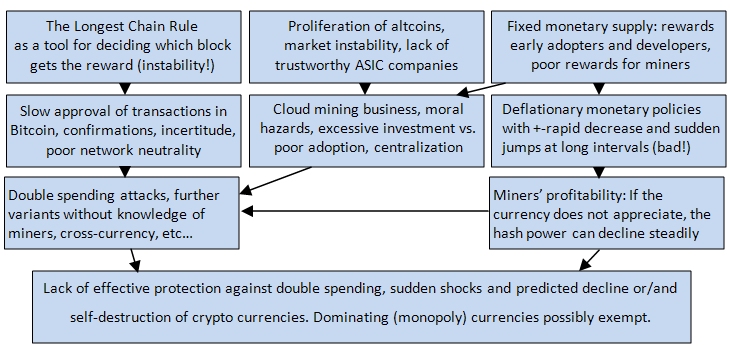

We claim that this sort of conclusion is MISTAKEN and the devil is in the details. In this paper we are going to show that the amount of money needed to commit for-profit double spending attacks remains moderate, it has nothing to do with the 600 M dollars spent on ASIC miners in activity. It is a fallacy to consider that money burnt in hashing could or should serve as effective protection against attacks. This is because money at risk, for example in large transactions, can be substantially larger than the cost of producing a fork in the block chain. We claim that nearly anybody can commit double spending attacks, or it will become so in the future. We claim that the current 1 billion dollar investment in bitcoin infrastructure is neither necessary nor sufficient to build a secure digital currency. It simply does NOT serve as effective protection and does not deliver the security benefits claimed. This is due to misplaced ideology such as the so called The Longest Chain Rule, important technicalities, dangerous centralization and insufficient network neutrality, and lack of the most basic features in Satoshi bitcoin specification. We intend to show that it is possible to fix the double spending problem in bitcoin with cryptography and timestamping, and the cost of doing so is in general much lower than expected.

3 Short Description of How Bitcoin Works

We have essentially one dominant form of bitcoin software [57] and the primary “official” bitcoin protocol specification is available at [71]. However bitcoin belongs to no one and the specification is subject to change. As soon as a majority of people run a different version of it, and it is compatible with the older software, it becomes the main (dominating) version.

Bitcoin is a sort of distributed electronic notary system which works by consensus. We have a decentralized network of nodes with peer-to-peer connections. The main functionality of bitcoin is to allow transfer of money from one account to another. At the same time network participants create new coins and perform necessary checks on previous transactions which are meant to enforce “honest” behavior. Integrity of bitcoin transactions is guaranteed by cryptographic hash functions, digital signatures and a consensus about what is the official history of bitcoin. Below we provide a short, concise description of how bitcoin works.

-

1.

We have a decentralized network of full bitcoin nodes which resembles a random graph. Network nodes can join and leave the network at any moment.

-

2.

Initially, when bitcoins are created, they are attributed to any network node willing and able to spend sufficient computing power on solving a difficult cryptographic puzzle. We call these people “miners”.

-

3.

It is a sort of lottery in which currently 25 bitcoins are attributed to one and unique “winner” every 10 minutes.

-

4.

With time this quantity decreases which has been decided by the creator(s) of bitcoin in order to limit the monetary supply of bitcoins in the future.

-

5.

The legitimate owner of these 25 bitcoins is simply identified by a certain public key (or several public keys).

-

6.

A public ledger of all transactions is maintained and it is used to record all transfers of bitcoins from one account (one public key) to another.

-

7.

Bitcoins are divisible and what is stored on the computers of the network participants are just the private keys.

-

8.

The amount of bitcoins which belongs to a given key at a given moment is stored in the public ledger, a copy of which is stored at every full network node application and constantly kept up to date.

- 9.

-

10.

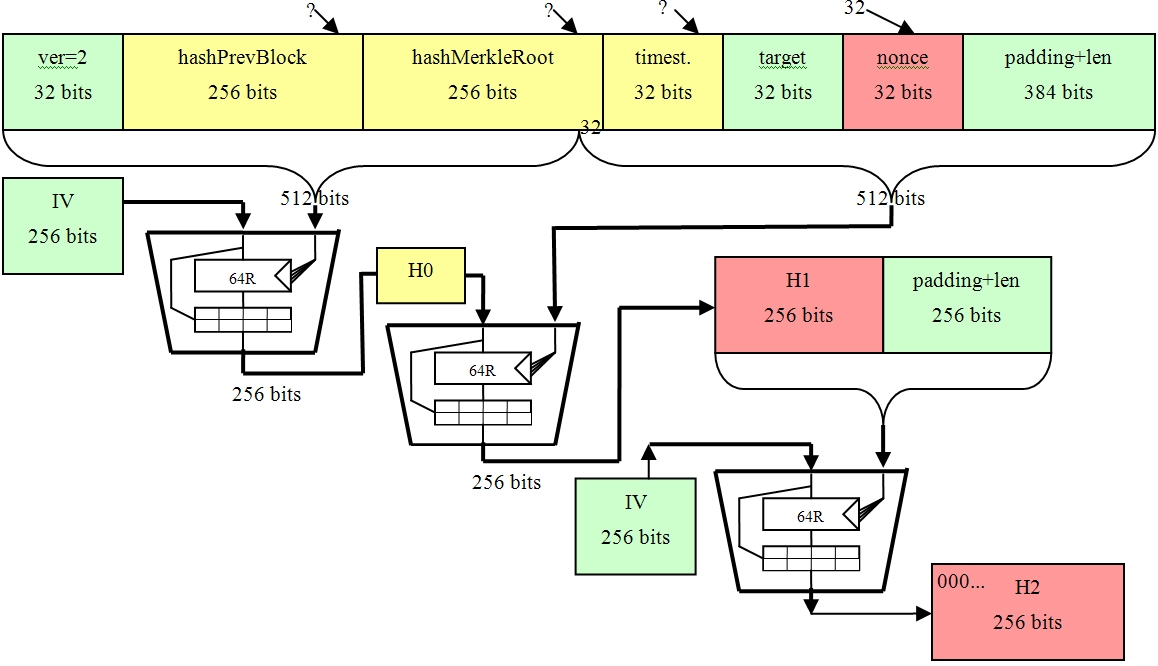

This H2 must be such that when written as an integer in binary it will have some 64 leading zeros which corresponds to the difficulty level in the bitcoin network at a given moment (cf. [23]).

-

11.

The difficulty level can go up and down depending on how many people participate in mining at a given moment. It tends increase and it does rarely decrease 111111In bitcoin it has increased at truly unbelievable speed, cf. Fig. 3. In other crypto currencies it is more likely to decrease in a substantial way as we will see in this paper.

-

12.

More precisely, in order to produce a winning block, the miner has to generate a block header such that its double SHA-256 hash H2 is smaller than a certain number called target.

-

13.

This can be seen as essentially a repeated experiment where H2 is chosen at random. The chances of winning in the lottery are very small and proportional to one’s computing power multiplied by . This probability decreases with time as more miners join the network. The bitcoin network combined hash rate increases rapidly, see Fig. 3.

-

14.

If several miners complete the winning computation only one of them will be a winner which is decided later by a consensus.

-

15.

Existing portions of the currency are defined either as outputs of a block mining event (creation) or as outputs of past transactions (redistribution of bitcoins).

-

16.

The ownership of any portion of the currency is achieved through chains of digital signatures.

-

17.

Each existing quantity of bitcoin identifies its owner by specifying his public key or its hash.

-

18.

Only the owner of the corresponding private key has the power to transfer this given quantity of bitcoins to other participants.

-

19.

Coins are divisible and transactions are multi-input and multi-output.

-

20.

Each transaction mixes several existing quantities of bitcoins and re-distributes the sum of these quantities of bitcoin to several recipients in an arbitrary way.

-

21.

The difference between the sum of inputs and the sum of all outputs is the transaction fee.

-

22.

Each transaction is approved by all the owners of each input quantity of bitcoins with a separate digital signature approving the transfer of these moneys to the new owners.

-

23.

The correctness of these digital signatures is checked by miners.

-

24.

Exactly one miner approves each transaction which is included in one block. However blocks form a chain and other miners will later approve this block. At this moment they should also check the past signatures, in order to prevent the miner of the current block from cheating. With time transactions are confirmed many times and it becomes increasingly hard to reverse them.

-

25.

All this is effective only for blocks which are in the dominating branch of bitcoin history (a.k.a. the Main Chain). Until now great majority of events in the bitcoin history made it to become the part of this official history.

-

26.

In theory every bitcoin transaction could later be invalidated. A common solution to this problem is to wait for a small multiple of 10 minutes and hope that nobody will spend additional effort just in order to invalidate one transaction. These questions are studied in more detail in Section 6.

-

27.

Overall the network is expected to police itself. Miners not following the protocol risk that their blocks will be later rejected by the majority of other miners. Such miners would simply not get the reward for which they work.

-

28.

There is no mechanism to ensure that all transactions would be included by miners other than the financial incentive in the form of transaction fees.

-

29.

There is no mechanism to store a complete history of events in the network other than the official (dominating) branch of the block chain. Memory about past transactions and other events in the network may be lost, cf. [32].

4 Asynchronous Operation And The Longest Chain Rule

According to the initial design by Satoshi Nakamoto [56] the initial bitcoin system is truly decentralized and can be to a large extent asynchronous. Messages are broadcast on the basis of best effort. Interestingly the system can support important network latency and imperfect diffusion of information. Information does not have to reach all nodes in the network in the real time and they could be synchronized later and can agree on a common history at any later moment.

The key underlying principle which allows to achieve this objective is the Longest Chain Rule of Satoshi Nakamoto [56]. It can be stated as follows:

-

1.

Sometimes we can have what is called a fork: there are two equivalent solutions to the cryptographic puzzle.

- 2.

-

3.

Different nodes in the network have received one of the versions first and different miners are trying to extend one or the other branch. Both branches are legitimate and the winning branch will be decided later by a certain type of consensus mechanism, automatically without human intervention.

-

4.

The Longest Chain Rule of [56] says that if at any later moment in history one chain becomes longer, all participants should switch to it automatically.

With this rule, it is possible to argue that due to the probabilistic nature of the mining process, sooner or later one branch will automatically win over the other. For example we expect that a fork of depth 2 happens with the frequency which is the square of previous frequency, i.e. about 0.01 of the time. This is what was predicted and claimed by Satoshi Nakamoto [56]. This is precisely what makes bitcoin quite stable in practice. Forks are quite rare, and wasted branches of depth greater than one are even much less frequent, see Table 1 in [25]. All this is however theory or how the things have worked so far in recent bitcoin history. In practice it is more complicated as we will see in this paper.

4.1 Why Do We Have This Rule?

This Satoshi rule can be seen as an early and imperfect attempt to solve the problem of double spending. More generally in some way it also is a yet another attempt to solve some version of the long-standing so called ”Byzantine Generals” problem [49], which is also solved by voting and has been studied by computer scientists since 1982. This sort of problems are known to be very difficult to solve in practice. In contrast in current bitcoin literature the Longest Chain Rule is somewhat taken for granted without any criticism. For example in the very highly cited recent paper [35] we read: ”To resolve forks, the protocol prescribes miners to adopt and mine on the longest chain.”. In this paper we are going to show that this rule is highly problematic and it leads to very serious hazards.

4.2 Genius or Engineering Mistake?

It is possible to see that this consensus mechanism in bitcoin has two distinct purposes:

-

1.

It is needed in order to decide which blocks obtain a monetary reward. It allows to resolve potentially arbitrarily complex fork situations in a simple, elegant and convincing way.

-

2.

It is also used to decide which transactions are accepted and are part of official history, while some other transactions are rejected (and will not even be recorded, some attacks could go on without being noticed, cf. [32]).

Here is the crux of the problem. The creator of bitcoin software Satoshi Nakamoto has opted for a solution of extreme elegance and simplicity, one single (longest chain) rule which regulates both things. This is neat.

However in fact it is possible to see that this is rather a mistake. In principle there is NO REASON why the same mechanism should be used to solve both problems. On the contrary. This violates one of the most fundamental principles of security engineering: the principle of Least Common Mechanism [Saltzer and Schroeder 1975], cf. also [20]. One single solution rarely serves well two distinct problems equally well without any problems.

We need to observe that the transactions are generated at every second. Blocks are generated every 10 minutes. In bitcoin the receiver of money is kept in the state of incertitude121212 This period of incertitude is even much longer for large transactions: for example we wish to withdraw some 1 million dollars which is currently about 2200 bitcoins, we should probably wait for some 100 blocks or 10 hours. Otherwise it may be profitable to run the double spending attack which we study later in Fig. 10, page 10. for far too long and this with no apparent reason. The current bitcoin currency produces a situation of discomfort and dependency or peculiar sort. Miners who represent some wealthy people in the bitcoin network, are in a privileged position. Their business of making new bitcoins has negative consequences on the smooth processing of transactions. It is a source of instability which makes people wait for their transactions to be approved for far too long time. This violates also another very widely accepted principle of security engineering: the principle of Network Neutrality. We claim that it should be possible to design a better mechanism in bitcoin, which question we will study later in Section 7.

4.3 Consensus Building

The common history in bitcoin is agreed by a certain type of democratic consensus. In the initial period of bitcoin history people mined with CPUs and the consensus was essentially of type one CPU one vote. However nowadays people mine bitcoins with ASICs which are roughly ten thousand times more powerful than CPUs (more precisely they consume ten thousand times less energy, cf. [23]). Bitcoin miners need now to invest thousands of dollars to buy specialized devices and be at the mercy of the very few suppliers of such devices which tend NOT to deliver them to customers who paid them for extended periods of time, see Appendix of [25]. It appears that the democratic base of bitcoin has shrunk and the number of active miners has decreased.

Nevertheless in spite of these entry barriers the income from mining remains essentially proportional to the hashing power contributed to the network (in fact not always, see [25, 35]). This is good news: malicious network participants which do not represent a majority of the hash power are expected to have difficult time trying to influence the decisions of the whole bitcoin network.

In a first approximation it appears that the Longest Chain Rule works well and solves the problem of producing consensus in a very elegant way. Moreover it allows asynchronous operation: the consensus can propagate slowly in the network. In practice it is a bit different. In this paper we are going to challenge this traditional wisdom of bitcoin. In Section 6 and in later Sections 10 and 11 we are going to argument that more or less anyone can manipulate virtual currencies for profit.

In fact we are not even sure if the Longest Chain Rule is likely to be applied by miners as claimed. This is what we are going to examine first.

4.4 The Longest Chain Rule - Reality or Fiction

This rule is taken for granted and it seems to work. However. We can easily imagine that it will be otherwise. There are several reasons why the reality could be different:

-

1.

We already have a heterogenous base of software which runs bitcoin and the protocols are on occasions updated or refined with new rules. On occasions there will be some bugs or ambiguities. This has already happened in March 2013. There were two major versions of the block chain. For 6 hours nobody was quite sure which version should be considered as correct, both were correct. The problem was solved because the majority of miners could be convinced to support one version. Apparently the only thing which could solve this crisis was human intervention and influence of a number of key people in the community, see [11].

-

2.

Open communities tend to aggregate into clusters. These clusters could produce distinct major software distributions of bitcoin, similar to major distributions of Linux which will make some conflicting choices and will not necessarily agree on how decisions can be made. For example because they promote their brand name and some additional business interests. We already observe a tendency to set up authoritative bitcoin authorities on the Internet such as blockchain.info. Software developers are tempted to rely on these web services rather than work in a more “chaotic” fully distributed asynchronous way. People can decide to trust a well-established web service rather than network broadcasts which could be manipulated by an attacker.

-

3.

This is facilitated by the fact that bitcoin community produces a lot of open source software and free community web services.

-

4.

It is also facilitated by the fact that the great majority of miners mine in pools. Moreover they tend to “flock to the biggest pools” [25, 70]. Just one pool reportedly based in Ukraine was recently controlling some 45 of the whole bitcoin network, see Table 2 in [25].

The pool managers and not individual miners are those who can decide which blocks are mined and which transactions will be accepted. The software run by pools is not open source and not the same as run by ordinary bitcoin users. In particular they can adopt various versions or exceptions from The Longest Chain Rule. In Section 8 we will propose further new ways for pool managers to attack the bitcoin network.

-

5.

More importantly participants could suspect or resist an attack by a powerful entity (which thing allows effectively to cancel past transactions and double spend) and they will prefer to stick to what their trusted authority says.

-

6.

Even more importantly these sub-communities of bitcoin enthusiasts will also contain professional for-profit bitcoin miners who can be very influential because for example they will be sponsoring the community. Their interest will be that their chain wins because they simply need to pay the electricity bill for it. If another chain wins, they have lost some money.

We see that sooner or later we could have a situation in the bitcoin community such that people could agree to disagree. If one group have spent some money on electricity on one version of the chain, their interest will be to over-invest now in order to win the race. Over-investment is possible because there is always spare capacity in bitcoin mining which has been switched off because it is no longer very profitable. However the possibility to earn money also for previous blocks which money would otherwise been lost can make some operations profitable again. Such mechanisms could also be used to cancel large volumes of transactions and commit large scale financial fraud, possibly in combination with cyber attacks. This can be done in such a way that nobody is to blame and everything seems normal following the Longest Chain Rule. Losses will be blamed on users not being careful enough or patient enough to confirm their transactions.

4.5 Summary: Operation in Normal Networks

We have seen that bitcoin has been designed to operate in extreme network conditions. Most probably bitcoin could operate in North Korea or in Syria torn by war operations, or in countries in which the government is trying to ban bitcoin or is very heavily limiting the access of the citizens to fast computer networks such as the Internet.

In contrast in the real life, the propagation in the global network of bitcoin client applications is quite fast: the median time until a node receives a block is 6.5 seconds whereas the average time is 12.6 seconds, see [30, 31]. The main claim in this paper is that in normal (fast) networks the Longest Chain Rule is not only not very useful, but in fact it is sort of toxic. It leads to increased risks of attacks or just unnecessary instability and overall slower financial transactions [38, 21].

Before we consider how to reform or replace the Longest Chain Rule, we look at the questions of monetary policy in bitcoin. Later we will discover that both questions are related, because deflationary policies erode the income of honest miners which in turn increases the risk of for-profit block chain manipulation attacks, cf. Sections 10, 11 and 12.

5 Deflationary Coins vs. Growth Coins

It is possible to classify crypto currencies in two families:

-

1.

Deflationary Currencies in which the monetary supply is fixed131313These are also called Log Coins in [77] which is not quite correct because the monetary supply in bitcoin does not grow logarithmically.. For example in bitcoin and Litecoin.

-

2.

Growth Currencies in which the monetary supply is allowed to grow at a steady pace, for example in Dogecoin.

Bitcoin belongs to the first family. This is quite unfortunate. In [77] we read:

”This limited-supply issue is the most common argument against the viability of the new currency. You read it so often on the web. It comes up time and again”.

In the following three subsections we look at the main arguments why a fixed monetary supply in bitcoin is heavily criticized. We need to examine the following four questions:

-

1.

comparison to gold, other currencies and commodities

-

2.

volatility

-

3.

miner reward vs. fees

-

4.

competition with other cryptocurrencies.

5.1 Comparison to Gold Other Currencies and Commodities

Bitcoin is frequently compared to gold and The Economist called it “Digital Gold” in April 2013, cf. [34]. However actually gold belongs to the second category: the worldwide supply of gold grows every year due to gold mining and other factors, with a yearly increase of the quantity of gold by some 0.5 - 1 . In fact when bitcoin mandates a fixed monetary supply, ignoring the growth of the bitcoin economy, arguably we enter an area of misplaced ideology and monetary non-sense. If the economy grows substantially, the monetary supply should probably follow or the currency is not going to be able to make a correct connection between the past and the future. It is widely believed that business does not like instability. It is well known in traditional economics that deflation discourages spending, creates an expectation that prices would further decrease with no apparent limit.

To the best of our knowledge, no currency and no commodity has ever had in the human history a totally fixed quantity in circulation. This is clearly an artificial property which makes that bitcoin is like no other currency and like no other commodity. This is expected to have very serious consequences and could be potentially fatal to bitcoin in the long run.

5.2 The Question of Volatility

Here the argument is that basically deflationary currencies are expected to have higher volatility due to the existence of people holding large balances for speculation. In [61] Robert Sams claims that deflationary currencies lead to a “toxic amount of exchange rate volatility” providing yet another reason for users to “run away” from using these currencies as a medium of exchange.

This is actually not so obvious and requires some explanation. We see one good reason for that. In a recent report published by Bank of England [1], we read that one of the key problems of bitcoin is that the supply of money does NOT respond to variations in demand. As a consequence they predict ”welfare-destroying volatility in economic activity”. They point out that ”growth rate of the currency supply could be adjusted to respond to transaction volumes in (close to) real time”, cf. [1].

5.3 Miner Reward

We need to recognize the role of miners in digital currencies. In [77] Sams writes:

”The amount of capital collectively burned hashing fixes the capital outlay required of an attacker to obtain enough hashing power to have a meaningful chance of orchestrating a successful double-spend attack on the system […] The mitigation of this risk is valuable, […]”

Now the deflationary currencies do with time decrease the reward for miners. This is highly problematic. In [77] citing J. Kroll from Princeton university we read: ”If you take this away, there will be no incentive for people to keep contributing processing power to the system […] ”If the miner reward goes to zero, people will stop investing in miners,”. Then the hash rate is likely to decrease and bitcoin will no longer benefit from a protection against double spending attacks, cf. Section 6.

Moreover Kroll explicitly says that the problem is NOT solved by transaction fees and says: […] You have to enforce some sort of standard payment to the miners, […] change the system so that it keeps creating bitcoins. In a paper presented at WEIS 2013 and co-authored by Kroll [48]. this is presented as a clear dilemma, either break the monetary policy or increase the fees:

The only way to preserve the system’s health will be to change the rules, most likely either by maintaining mining rewards at a level higher than originally envisioned, or making transaction fees mandatory.

5.4 Problems With Increasing The Fees

The question of whether higher fees could be effectively mandated in the current bitcoin is discussed by Kroll in Sections 4.2 and 6.2 of [48].

Now it is possible to see that it would be a very bad idea to increase the fees. This is brilliantly explained by Robert Sams in [61]. The argument is that basically sooner or later “deflationary currencies” and “growth currencies” will be in competition. Then all the other things being more or less in equilibrium, in deflationary currencies most of the profit from appreciation will be received by holders of current coins through their appreciation. Therefore less profit will be made by miners in these currencies. However miners control the network and they will impose higher fees. In contrast in growth coins, there will be comparatively more seignorage profit and it will be spent on hashing. Miners will make good profits and transaction fees will be lower. Thus year after year people will prefer growth currencies due to lower transaction fees.

Overall we see that this is crucial question of how the cost of the infrastructure necessary for the maintain a digital currency is split between new adopters (which pay for it through appreciation) and users (which pay through transaction fees). It is obvious that there exists an optimal equilibrium between these two sources of income, and that there is no reason why the creator of bitcoin would get it right, some adjustments will be necessary in the future.

5.5 The Appreciation Argument

There is yet another argument: it is possible to believe that bitcoin will appreciate so much that halving the reward every 4 years will be absorbed by an increase in bitcoin price. This means an extreme amount of deflation (double every 4 years) making it tempting to hoard bitcoins, which further decreases the amount of bitcoins in actual usage and makes people hoard bitcoins even more.

We claim that this is very unlikely. This is mainly because the digital economy is not expected to double every 4 years and even less it ie expected to grow by sudden jumps at the boundaries of the intervals arbitrarily decided by the creator of bitcoin. We refer to Part 3 of [23], Sections 10, 11 and 12 for further discussion and concrete examples of predicted and actual devastating effects of sudden jumps in the miner reward.

5.6 On Self-Defeating Monetary Policies and Alt-Coins

The bitcoin monetary policy is challenged by the very existence of alternative crypto currencies. In [10] we read:

[…] the constant volume of Bitcoins faces an unlimited number of alternative crypto-currencies and, therefore, an unlimited number of alternative coins. […] Clearly, an investor may move his assets from Bitcoins to a competing currency, thereby freely moving in a space with an unlimited number of coins.

It is easy to see that the bitcoin restricted monetary supply is a self-defeating property: if bitcoin is limiting the monetary supply beyond what is ‘reasonable’, and if as a result of this bitcoin economy suffers from excessive deflation, bitcoin adopters are likely to circumvent this limitation by using alternative coins. This can erode the dominant position of bitcoin.

5.7 The Future

Can Bitcoin change its reward rules and the monetary policy given that fixed monetary supply is problematic as shown above? User DeathAndTaxes, a highly respected frequent contributor in bitcointalk.org forum wrote on 10 May 2014:

”The bitcoin protocol reward is not going to be changed. Period.”

Source:

https://bitcointalk.org/index.php?topic=600436.msg6657579#msg6657579

5.8 Who Can Change The Bitcoin Monetary Policy?

There is an interesting additional question who has the power to change the bitcoin monetary policy, is it the majority of miners, ordinary bitcoin users, bitcoin developers, or is it that all must agree? This is a very complex and highly controversial question on which opinions differ rally a lot, see Sections 13.7 through 13.11 and [62, 40].

6 Is The Longest Chain Rule Helping The Criminals?

This section is the central section in this paper. We are going to show a simple attack which allows double spending. The attack is not very complicated and we do not claim it is entirely new.

Our attack could be called a 51 attack however we avoid this name because it is very highly misleading. There are many different things which can be done with 51 of computing power, (for example to run a mining cartel [25] or/and cancel/undo any chosen subset of past transactions) and many very different attacks have historically been called a 51 attack.

We are in general under the impression that a 51 attack is about holding more than 50 of the hash power kind of permanently or for a longer period of time, while our attacks are rapid short-term attacks cf. Fig. 10 page 10.

6.1 Common Misconceptions About 51 Attacks

There many reasons why such attacks has not been properly understood and studied before in bitcoin community and in the bitcoin literature.

-

1.

There is a large variety of attacks which could be or have been called a 51 attack. Opinions or statement which might be true for some of these attacks are simply not true for other attacks. This creates a lot of confusion in the bitcoin community.

-

2.

Great majority of people who discuss bitcoin make an implicit wrong assumption about a static nature of threats and attacks about bitcoin.

-

3.

We hear about 51 attack etc, entities who own or control 51 of hash power and it seems that only incredibly powerful or very wealthy entities [17, 3] could execute such attacks and that they are ”so amazingly cost-prohibitive to perform that we re basically talking about a government focusing the full power of every top-secret ridiculously expensive supercomputer”, cf. [59]

-

4.

Many commentators stress that 51 attack are only theoretical attacks, cf. [19, 3], try to convince us to “stop worrying” e.g. [59]. The official bitcoin wiki, does even consider that there are any real problems in bitcoin. The section about 51 attacks does NOT even get into the part entitled ”Might be a problem”. It appears in the following part entitled ”Probably not a problem”, cf. [13] which many people would maybe not read, why bother if it probably is not a problem?

-

5.

In the original paper Satoshi have portrayed ”a greedy attacker” being ”able to assemble more CPU power than all the honest nodes”, see Section 6 of Satoshi paper [56]. The attacker is also portrayed as having considerable ”wealth” which he would endanger by engaging in the attack. It is clearly suggested that the attack would have little to gain and a lot to lose from being dishonest.

-

6.

Satoshi has invented a term ”CPU power” and always explicitly states the principle of ”one-CPU-one-vote”. In reality nowadays it is rather ”one-ASIC-one-vote” and in the future it could be something yet different. A reasonable term is ”hash power”141414 It can be measured in GH/s (Giga Hashes per second) which notion is almost never properly defined in a non-ambiguous way: one hash per second is capacity to hash one block header, which is two applications of SHA256 and which in turn is three applications of the underlying block cipher. In repeated hashing some of these computations do not have to be done, this is why we speak about ”capacity to hash” rather than hashing, see [23] for a detailed analysis of this problem.

-

7.

In general a very common but also one of the most serious mistakes is to claim that 51 attacks occur when the attacker owns or is in possession of 51 of all the hash power.

This mistake is committed again and again by major Bitcoin experts and evangelists, cf. for example [56, 17, 59] to cite just a few. The official bitcoin wiki [13] has a subsection with this super highly misleading title: ”Attacker has a lot of computing power”. Quite happily just below they correct it and say it is rather about temporary control not ownership151515 They explain that the exact scenario is when he ”controls more than of the network’s computing power” and they make it clear it can be temporary: ”for the time that he is in control”. However almost to make things worse again, this official wiki at numerous places refers to another article about Bitcoin attacks written for more general audience [59] in which we see the repetition of the basic mistake to consider that attacks are ”so amazingly cost-prohibitive to perform”.

Nevertheless, the same confusion was made more recently by Cornell researchers in [36] which clearly very badly confuse between A) having 51 of the mining power and B) launching a 51 attack trying to convince the reader that A does not have to imply B while the real problem is that B can be executed without A.

Again attacks are presented as being exclusively about powerful entities who ”can turn dishonest” all of the sudden, [36]. They fail to see that the key problem is the control (not ownership) of hash power for the purpose of mining blocks, and this can be a lot easier and cheaper.

-

8.

Less people admit that the attacker could indeed be one single malicious pool which gathers more than 51 of hash power under his sole control (controlling but not owning hash power).

-

9.

Another serious mistake is to consider that ”control” is exclusive. For example in the Abstract of his paper Satoshi writes: ”As long as a majority of CPU power is controlled by nodes that are not cooperating to attack the network they’ll […] outpace attackers”. This is not correct in general. The key point is that control is NOT exclusive, both the miners and the attacker can have some control on the mining process. So ”a majority of CPU power is controlled by nodes” as Satoshi says and also at the same time it could be controlled by the attacker in a more or less subtle and more or less invasive ways, cf. Section 8.3.

-

10.

Many people stress that that 51 attacks, and for example double spending events would be visible to anyone to see on the public blockchain [17]. This is simply not true, the blockchains does NOT record double spending events, it rather hides them and would show only on transaction our of two, cf. also [32].

-

11.

In reality the notion of a 51 attack takes a very different meaning in a cloud computing world: the attacker does not need to own a lot of computing power, he can rent it for a short time, and then 51 attack can have a surprisingly low cost.

-

12.

Alternatively an attacker could also trick miners to help him to execute the attack without their knowledge and consent (man in the middle attacks).

This is particularly easy with mining pools: the attacker just needs to compromise extremely few web servers used by tens of thousands of individual miners and he can command very substantial hash power without owning any of it. At this moment less than 10 pools control over two-thirds of all the hash power, cf. [73, 25].

-

13.

It is important to remember that not only Satoshi did not predict ASIC mining and mining pools, but also he did NOT specify bitcoin fully in the sense that the mining pools typically use the Stratum protocol [65]. which was specified in 2012 and which at some moment took an important strategic decision which is clearly stated in documented in [65] in order to move the choice and the control of which transactions are included in a block from miners to the pool managers, see [65].

This decision broke the bitcoin peer network because miners do no longer have any incentive whatsoever 161616This decision also has definitely infringed on the initial intentions of Satoshi explicitly stated in Section 6 of his paper [56] where he explains that the fact that a block provides a monetary reward for the ”creator of the block” is something which ”adds an incentive for nodes to support the network”. This incentive is now broken. to support this network by running peer nodes, and the bitcoin network is now very seriously declining cf. [16].

-

14.

In fact, even if large pools had only 10 of hash power each, we should see reasons to worry: it would be sufficient to hack just 5 pool manager servers in order to be able to execute double spending attacks.

-

15.

Nobody has yet stated under which exact assumption bitcoin is expected to be secure and there is a lot of ambiguity in this space. Knowing the assumption is crucial because if we have stated our assumption and bitcoin is later shown to be broken insecure, we can blame either the real world which does not satisfy our assumption, or the designers and engineers of bitcoin which have not been able to design a secure system based on this assumption. In other worlds we could determine without ambiguity who is to blame. In this respect Satoshi shows a bad example of not being clear about what his assumption is and yet explicitly several times claiming that his system is secure:

-

A.

For example in the abstract of his paper [56] Satoshi says that he assumes that ”majority […] are not cooperating to attack the network”. Here Satoshi claims the system is secure under this assumption, which security claim is not true as people can easily be part of an attack without cooperating (as already explained above).

-

B.

Now in the conclusion of his paper Satoshi again claims that the system is secure if ”honest nodes control a majority of CPU power”. which is a very different and STRONGER assumption than A. above: nodes could be not honest and deviate from the protocol for fun or for profit in a variety of creative ways without ”cooperating” with any attacker.

Does this stronger assumption make that bitcoin becomes secure? Of course not, the security result claimed by Satoshi is wrong again if you take it literally: even if honest nodes control a majority of hash power, because the control is not exclusive, bitcoin can still be attacked.

-

A.

-

16.

It is nonsensical to claim that the attacker would prefer to behave honestly, and that it is ”more profitable to play by the rules” [56].

This is claimed by Satoshi on the grounds that the attacker should be able to ”generate new coins” which would be an honest way to use his hash power, see Section 6 of [56]. Many other authors repeat this mistake, for example in [36] we read about ”miners which may ”hold 49 of the [mining] revenue”.

-

17.

In reality, in almost all171717 With exception of attacks described in [43]. bitcoin mining scenarios known to us, the attacker does NOT control the money from mining: he does NOT have the private keys used for mining. This is because the whole process of mining requires exclusively the public keys.

It would simply be an unnecessary mistake for any miner or for any mining pool to have the private keys around to be stolen by the attacker which targets the mining process. Therefore the attacker typically does NOT have an honest option at all181818 In contrast Satoshi have claimed that he always has such an option, in Section 6 of [56] we read: ”he would have to choose between using it to defraud people by stealing back his payments, or using it to generate new coins.”.

-

18.

The notion of 51 attacks is also very highly misleading because presenting the hash power as a percentage figure does NOT make sense because the hash rate is measured at two different moments. Therefore the proportion of hash power used in attack is NOT a number between 0 and 100 . It can easily be larger than 100 .

-

19.

It was also wrongly assumed that the bitcoin adopters are more or less the same as miners, they own the devices and the computing power cannot change hands very quickly.

-

20.

It is in general not sufficient to trust the pools not to be malicious.

Attacks could be executed without the knowledge and consent of these companies by a single rogue developer.

-

21.

Many bitcoin adopters did not anticipate that in the future bitcoin will have to compete with other crypto currencies and that hash power could instantly be moved from one crypto currency to another.

- 22.

-

23.

People have wrongly assumed that bitcoin achieves very substantial computing power which no one can match, which is still the case today however it is highly problematic to see if this will hold in the future.

-

24.

Many people did not predict that an increasing fraction of all available computing power is going to exist in the form of rented cloud miners which further facilitates the attacks.

This is due to several factors. Investing in wholly owned mining equipment has been excessively risky. this is both due to the impossibility to know if and when miners will effectively be delivered (cf. Appendix of [25] and Section 2.4) and due to the price volatility. In contrast investing in rented capacity could be nearly risk-free.

Another reason is that some large investors may have over-invested in large bitcoin mining farms consuming many Megawatts of electricity (we know from the press that such facilities have been built in Sweden, Hong Kong, USA, etc..) and now they want to rent some parts of it in order to get immediate cashflow and return on their investment.

-

25.

Furthermore rented cloud miners can be seen as a method to absolve owners of hash power from any legal responsibility.

This does in addition lead to the possibility of running for-profit attacks with cooperating peers who may or not be aware of participating in an attack, see Section 7.9.

-

26.

There is some sort of intuitive understanding in the bitcoin community that the Longest Chain Rule solves all problems in this space, and there is simply no problem of this sort, and if there is, people naively believe that it is not very serious. In other terms nobody wants to admit that the brilliant creator(s) of bitcoin could have created a system which has serious security problems.

-

27.

For example many authors claim that the problem has already been fixed: and that the fix is to wait for 6 confirmations, cf. [59]. More generally it is frequently claimed that the probability of reverting a transaction in a block decreases exponentially with the number of blocks mined on the top of the current block cf. [56]. In fact if a lot of money is at stake in a large transaction (or in many small transactions) it is possible to see that a larger attack could be mounted. According to [50] core developers require 120 blocks (about 1 day191919 So it is in fact faster to take a plane to Switzerland, withdraw money from a bank, and travel back, than to use bitcoins to withdraw larger sums of money, cf. [38, 21].) before they consider the network sufficiently protected from the potential of a longer attack-chain. In general as the money at stake involved in each block is likely to grow in the future, the risk will also increase202020 Later we are going to see that 51 attacks will get worse with time due to the build-in monetary policy in bitcoin (money at risk grows in comparison to the cost of attack) and moreover there will be sudden transitions because the monetary policy mandates sudden jumps in the miner reward (cf. also Part 3 in [23]). and we believe that ”no amount of confirmations” can fix such problems, citing [14]. See also [6] and Section 6.

Overall we see that 51 attacks are a huge problem and cannot be easily dismissed.

6.2 The Basic Attack

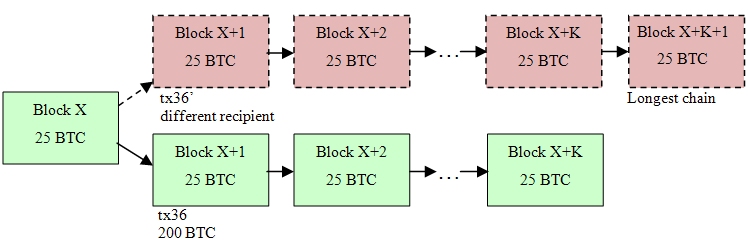

Our basic attack is self-explanatory, some attacker produces a fork in order to cancel some transaction[s] by producing a longer chain in a fixed interval of time, see Fig. 10 below.

The attack clearly can be profitable. The question of actual feasibility of this attack is a complex one, it depends on many factors and we will amply study this and related questions later throughout in this paper.

In the following sections we are going to analyse the risks which result form this and similar attacks.

6.3 Large vs. Smaller Transactions

Our attack does NOT limit to defraud people who would accept a single large payment in exchange of goods or another quantity of a virtual currency (mixing services, exchanges, some sorts of shares). The attacker (for example a bitcoin exchange or a bitcoin lottery) can in the same way issue a large number of smaller transactions and cancel all of them simultaneously in the same way and at exactly the same cost.

6.4 Feasibility Discussion

The attacker does NOT need to be very powerful, on the contrary. The most shocking discovery is that anyone can commit such fraud and steal money. They just need to rent some hashing power from a cloud hashing provider. Bitcoin software does not know a notion of a double spending attack and if it occurs possibly nobody would notice: only transactions in the official dominating branch of the blockchain are recorded in the current bitcoin network, cf. [32]. It may also be difficult to claim that something wrong happened: one may consider that this is how bitcoin works and the attacker has not done anything wrong.

In a competitive market they do not need to pay a lot for this. Not much more than 25 BTC per block (this is because miners do not mine at a loss, the inherent cost of mining per block should be less than 25 BTC). The attacker just needs to temporarily displace the hashing power from other crypto currencies for a very short period of time which is easy to achieve by paying a small premium over the market price.

There is another very serious possibility, that the spare hash power could also be obtained from older miner devices which have been switched off because they are no longer profitable (or a combination of old and new devices). However they may be profitable for criminals able to generate an additional income from attacks. Given the fact that the hash rate increases steadily, cf. Fig. 3, it is quite possible to imagine that the hash power which has been switched off is very substantial and comparable in size to the active hash power.

How to Achieve 500 or More

There is yet another way to execute such attacks: to offer a large number of miners a small incentive (as a premium over the market price) to go mine for another crypto currency, before the attack begins. This can lead to massive displacement of hash power before the attack starts. Then at the moment when block X+1 is mined following the notations of Fig. 10, the double spending attack costs less. The hash rate goes down dramatically at the very beginning of the attack, and raises back again. In this way it is possible also to achieve 500 hash power or more. More precisely the attacker can for example re-do this block , and potentially few more blocks with hash power which could be literally 500 compared to the (reduced) hash power with which first block was initially mined. Now the attacker is going to modify the recipients of one or many transactions included in this block to cancel his own transactions212121 He can also cancel transactions of many other people with double spending as a service bitundo.com, see Section 7.9.

Further advanced attacks scenarios with malicious pool managers and which can easily be combined with this preliminary displacement of hash power are proposed and studied in Section 8.2.

6.5 The Question of Dominance

It is important to understand that what we present in Fig. 10 is already feasible to execute today for nearly anyone, not only for rich and powerful attackers. Then as we advance in time, such attacks are expected to become easier.

At this moment bitcoin is a dominating crypto currency: its hash power is substantially larger than for other crypto currencies combined. It appears that bitcoin could claim to be a sort of natural monopoly: it is able to monopolize the market and its competitors find it hard to compete.

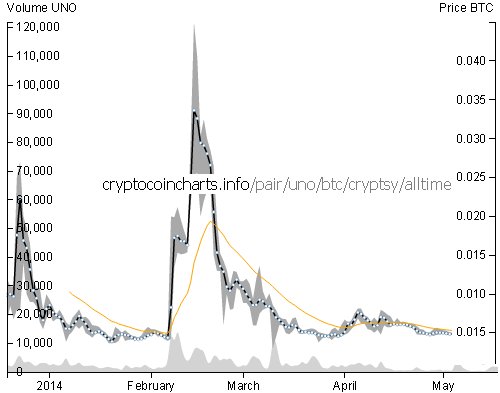

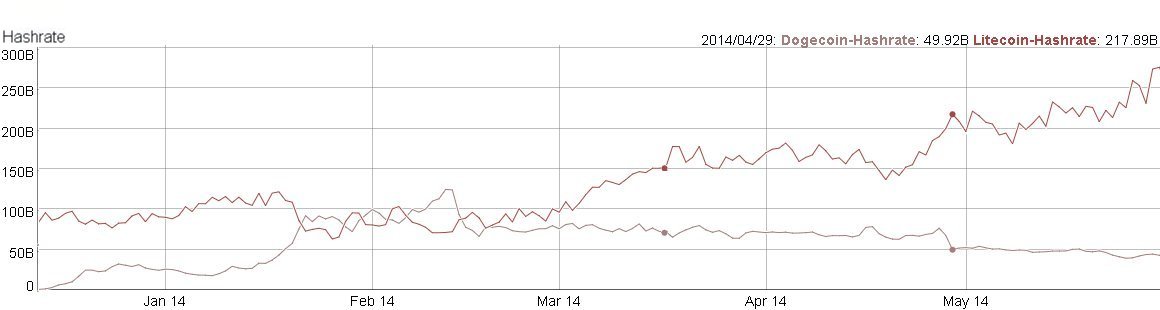

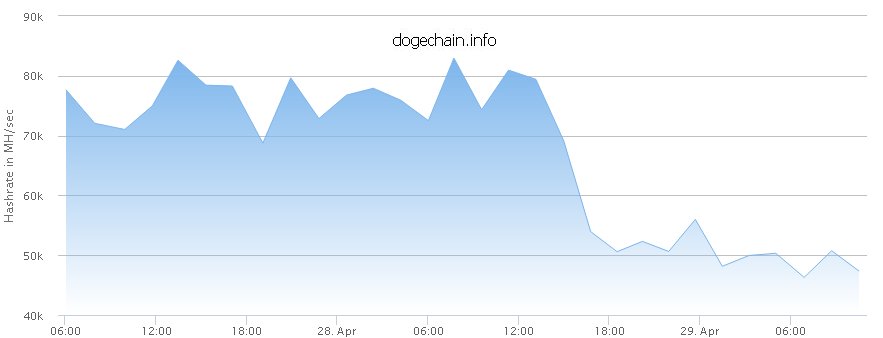

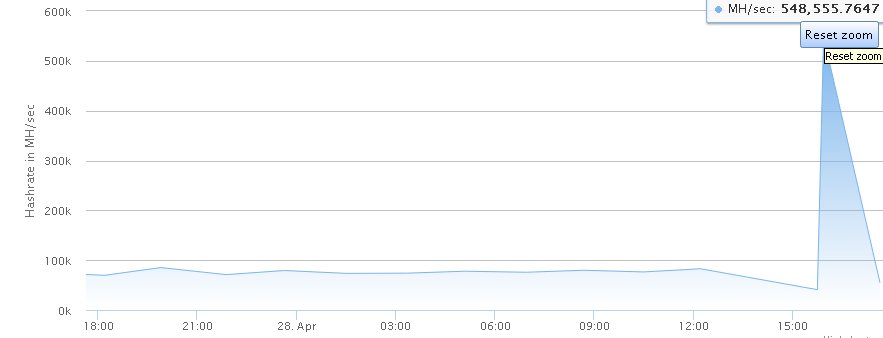

Now the attack will become particularly easy when bitcoin ceases to be a dominant crypto currency. At this moment the attacker needs for example to hack some (very few) pool manager servers in order to execute the attack. But when there is plenty of hash power available to rent outside of bitcoin, the attacker will be able to execute the attack without doing anything illegal (except possible legal consequences of canceling some bitcoin transactions). At this moment it is quite easy to execute double spending attacks on many existing crypto currencies cf. for example Section 10 and 11. For example in April 2014 one single miner owned 51 of the hash rate of Dogecoin.

In this respect things are expected to considerably change in the future for bitcoin. We do not expect bitcoin to remain dominant forever. Here is why! Unhappily due to the cost of adopting bitcoin as a currency (the necessity to purchase bitcoins which have already been mined at a high price) one cannot prevent users from creating their own crypto currency (cf. Section 5.6 and [10]). Gold does not give people and major countries any choice: some countries have gold mines or gold reserves, others don’t. Digital currencies put all the countries and all the people at an equal footing. There will be always a large percentage of the population which will not be happy about the distribution of wealth and will try to promote a new crypto currency which gives (new) investors a better chance than having to buy coins already mined by other people.

The fact that bitcoin is expected to lose its dominant position is also due to another factor, built-in decreasing returns for miners and the predicted consequences of this fact, see Section 5. At the same as miner rewards decreases substantially with time, the money at risk increases (compared to the cost of mining a new block).

Phase Transitions. All these factor combined, we expect that most crypto currencies will undergo “destructive” transitions from a secure state to an insecure state. For many crypto currencies all these things are already happening, see Section 10 and 11. The question whether it can also happen to bitcoin and what might be further consequences of it is further studied in Section 12.

7 Alternative Solutions For Double Spending

Note: this section is work in progress. Not everything can be covered inside this paper and many questions are really not obvious. We thank all the authors of very valuable comments on early versions of this paper posted at bitcointalk.org. We plan to develop these questions further and publish another paper on this topic.

In this paper we heavily criticize the longest chain rule of Satoshi Nakamoto. A single rule which offers apparent elegance and simplicity and regulates two things at one time. It is responsible for deciding which freshly mined blocks are “accepted” and obtain monetary reward and at the same for deciding which transactions are finally accepted and are part of the official common history of bitcoin. However as we have already explained in Section 4.2, it is problematic to solve both problems with one single “blunt” rule, there is NO REASON why the same mechanism should govern both areas. It should be possible to design better mechanisms in bitcoin and other digital currencies, this NOT in order to replace the blockchain by another solution, but as a complement, in order to improve the security and the speed of transactions.

7.1 Our Objectives

Our primary goal is to design and build Fast Consensus Mechanisms for bitcoin transactions. We approach the problem from a conservative angle: we do not think it is realistic un bitcoin to try to change the speed at which blocks are mined. We want to improve bitcoin in such a way that payments can be accepted much faster than the speed of mining the next block.

Desired Characteristics

Let us examine what kind of solutions would be desirable.

-

1.

Order and timing of transactions should matter and should be hard to modify (protection against malicious manipulation in the timing and network propagation of transactions).

-

2.

The solutions should be incremental and should NOT destroy the existing order in the bitcoin network. They should offer some benefits even if not every network participant adopts them initially. They should not require a permission of everybody in the bitcoin network.

-

3.

Earlier transactions should be preferred and as time goes by it should be increasingly difficult to emit a second (double spending) transaction.

-

4.

Instead of instability and all or nothing behavior where large number of transactions could be put into question, we should get stability and convergence.

-

5.

Relying parties should get increasing probabilistic certitude that the transaction is final as times goes by, second after second.

They should also be able to get obtain some tangible evidence in form of network events which are difficult to forge, which allows them to evaluate their risks.

-

6.

Unique transactions which spend some quantity[ies] of money in bitcoin should be always accepted with very large probability.

-

7.

Double spending transactions should simply be resolved on the (objective) basis of earlier transaction, if one transaction is much earlier than the other.

-

8.

Only in rare cases where competing transactions are emitted within a certain time frame there could be an ambiguity about which transaction will be accepted. We should also ask the question that maybe no transaction should be accepted in this case, as it would show that either the payer is trying to cheat or his private key has been compromised.

-

9.

In particular though it is possible and does not cost a lot to rewrite bitcoin history in terms of which blocks get the reward, it should be somewhat STRICTLY HARDER and/or cost more (the exact criteria to be determined) to rewrite bitcoin history in terms of who is the recipient of moneys.

-

10.