Regularized Portfolio Optimization

Abstract

Investors who optimize their portfolios under any of the coherent risk measures are naturally led to regularized portfolio optimization when they take into account the impact their trades make on the market. We show here that the impact function determines which regularizer is used. We also show that any regularizer based on the norm with makes the sensitivity of coherent risk measures to estimation error disappear, while regularizers with do not. The norm represents a border case: its “soft” implementation does not remove the instability, but rather shifts its locus, whereas its “hard” implementation (equivalent to a ban on short selling) eliminates it. We demonstrate these effects on the important special case of Expected Shortfall (ES) that is on its way to becoming the next global regulatory market risk measure.

1 Introduction

Risk minimization for large institutional portfolios suffers from the curse of dimensionality: the number of different assets (the dimension of the measured return vector), , is often comparable to, or even larger than the sample size (the length of the available time series), . As such, portfolio optimization belongs to the realm of high dimensional statistics [1]. Empirical estimates of returns, covariances, etc. are unstable under sample fluctuations.

The instability has been identified by [2, 3] as an algorithmic phase transition [4], occurring at a critical value of the ratio (depending on the risk measure in question). At this critical point the estimation error diverges with a universal exponent, independent of the risk measure, the nature of the underlying fluctuations, or even whether these fluctuations are stationary or GARCH-like [5].

Expected Shortfall (ES) [6, 7] is on its way to becoming the next global regulatory market risk measure [8, 9]. The sensitivity of ES to estimation error was studied in [2, 3, 10], where the critical value of the ratio was determined, at which the estimation error diverges and the risk function becomes unbounded from below. This instability is a common weakness [11] of all coherent risk measures [12].

Various methods have been proposed to address this problem [13, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23, 24, 25, 26, 27, 28, 29, 30, 31, 32, 33, 34]. In [35] we advocated the systematic use of regularization in portfolio selection to eliminate the instability. We illustrated the idea of regularized portfolio optimization (RPO) using the Expected Shortfall as risk measure and the norm as regularizer [35]. The optimization problem thus obtained was shown [36, 37, 35]111This relationship was first recognized in [37], but the budget constraint was omitted there, which is an important element of the portfolio problem, missing from support vector regression. to be closely related to support vector regression[36].

The financial content of regularization is revealed by realizing that regularized portfolio optimization arises naturally when investors take into account the impact their trades make on the market [38]. We demonstrated (again using the specific example of ES) that the norm regularizer corresponds to linear market impact, and that the resulting optimization problem is identical to RPO, eliminating the instability [38].

In this paper we show that considering market impact in the investment strategy results in a regularized portfolio optimization for all coherent risk measures. We identify the various regularizers corresponding to the different impact functions. We furthermore prove that the instability of all coherent measures can be removed by regularizers based on the norm with , but not by regularizers with .

The norm sits on the borderline: it may or may not remove the instability, depending on the sample, which means that on average it does not remove, but only shifts it. In order to prevent the instability, the norm regularizer has to be implemented as a ban on short selling, which corresponds to a hard constraint, i.e. imposing infinite penalty on solutions wandering outside a finite domain.

We illustrate the effect of various regularizers on the estimation error of Expected Shortfall, as it has acquired special significance recently since the Basel Committee proposed it as the next global regulatory market risk measure [8, 9]. The calculations can be carried through analytically in the limit of large Gaussian portfolios (, with their ratio fixed) by methods borrowed from the statistical physics of disordered systems.

The paper is organized as follows. In Section 2 we show how market impact considerations lead to regularization for all coherent risk measures, and display the correspondence between the various impact functions and regularizers. Section 3 analyzes the effect of various regularizers on estimation error, with particular focus on the norm. We start by analyzing a simple toy example: the Maximal Loss risk function (the limiting case of ES) with only two assets and two data points. This serves to provide intuition. We move on to show that the regularizer cannot remove the instability of any of the coherent risk measures, while an with can. Section 4 illustrates the above ideas using the example of a large random portfolio optimized under historical ES, and demonstrates the shift of the instability as a result of -regularization. The effect of , , regularizers is also discussed, with special emphasis on the case corresponding to a square root-like market impact that is characteristic of the liquidation of large positions under normal market conditions. A combination of the and norms as a regularizer is also considered in this Section. The last Section is a short summary, followed by the Appendix, where the technical details of the calculations have been relegated to.

2 Risk measures, market impact and Regularized Portfolio Optimization

The problem we focus on is that of determining the optimal portfolio of assets that an investor should hold. We assume the investor has a fixed wealth to invest and can buy assets today at current prices . Therefore, the set of feasible portfolios satisfy the budget constraint

| (1) |

The optimal portfolio is the one that minimizes the risk of the portfolio at a future time, at prices . Here we assume that

| (2) |

where is a random vector of returns, denotes the market impact function, and is a proportionality factor.222Notation: we use uppercase letters for random variables. denotes the component of the vector . The term accounts for the finite liquidity of the market. One way to motivate it is to argue that, in order to derive a monetary value from the portfolio, it ought to be sold [38]. Then this term accounts for effects of finite liquidity, which are currently of great interest [39, 40]. The liquidation of the portfolio will generally move prices “against” the trading activity (i.e. ). Much recent work has been devoted to deriving quantitative estimates of the market impact function (see e.g. [39, 40]). Most of this literature has been concerned with the single asset setting (), suggesting that with taking values around .

The value of the portfolio can then be estimated by the cash flow that can be generated when the portfolio is liquidated:

| (3) | |||||

| (4) |

The optimal portfolio should be chosen in such a way as to minimize the risk attached to this cash flow [38].

We discuss in section 2.1 how risk is measured. For the moment, we remark that risk enters only in the term , because is known. Hence, without loss of generality and for the sake of simplifying mathematical expressions, we will omit this term in future discussion. Also, for the sake of simplicity, we normalize current prices to , , so that the budget constraint becomes

| (5) |

2.1 Coherent risk measures

A risk measure is a function of the random variable , denoted by 333 The squared parenthesis denotes that this is an operator that associates a real number with any random variable . representing a loss, i.e. it is a quantity that one would like to minimize. Here we focus on coherent risk measures, a broad class of quantitative measures for risk [12]. A risk measure is coherent if it satisfies the following axioms:

- Normalization

-

.

- Monotonicity

-

if a.s. then

- Sub-additivity

-

- Positive homogeneity

-

if then

- Translation invariance

-

if is a real constant then

The failure of the widely used risk measure Value at Risk to satisfy subadditivity was the prime motivation for the introduction of these axioms [12]. The translation invariance property implies that adding a certain amount (of cash) to a portfolio reduces risk by .

2.2 Market impact and regularization

Because of the translation invariance property, we have for any coherent risk measure, evaluated on the value, , of a portfolio (see Eq. 4)

| (6) |

The first term corresponds to the risk evaluated on the portfolio without market impact considerations. The second term, , is a monotonically increasing function of the weights, therefore it penalizes large positions, which means that it acts as a regularizer. It is very natural that anticipation of future liquidation should limit the sizes of one’s positions.

In summary, if the investor minimizes the risk of the cash flow that could be generated by the liquidation of the portfolio, then considering the impact of the investor’s own actions on the market naturally leads to Regularized Portfolio Optimization (RPO) for all coherent risk measures.

The correspondence between market impact functions and regularizers is as follows:

- The bid-ask spread impact

-

leads to the use of the -norm, which we can write as . This applies to single trades, as well as to sequential trades executed in a very short time.

- Square root impact

-

Large positions are usually liquidated by chopping the execution into many small child orders that are executed sequentially. Such meta-orders typically have an impact obeying a square root law [39]. This leads to a regularizing term: .

- Linear impact

-

On longer time scales, when the sales are repeated over a long time, we expect the impact to be linear: . This leads to the regularizing term , i.e. implies the use of the norm.

- In general

-

is equivalent to a regularizing term , and thus implies the use of the -norm in RPO:

3 Stability of regularized portfolio optimization

In this section we analyze the stability of norm based regularized portfolio optimization. We focus particularly on , as it plays a special role. In particular, we show that, for all coherent risk measures, if , then regularization based on the norm removes the divergence that plagues portfolio optimization in the undersampled regime, but this is not the case for .

Let us recall that the phenomenon of interest is the instability of the empirical estimate of the risk measure, when the sample size, , is of the same order as the number of assets, , in the portfolio, i.e. the dimensionality of the return vector. Assume that a sample, , consists of observations, , , drawn i.i.d. from a true (but unknown) underlying probability distribution, , and that there is a space of samples, , which come from the same underlying distribution. The empirical estimate of a risk measure can then be obtained by using the empirical distribution

| (7) |

The empirical risk, , computed on this distribution, depends on the specific sample . For some samples, the function is unbounded from below, which means that the portfolio optimization problem does not have a finite solution. This results in an instability of the risk measure.

To develop an intuition, we first consider the simple Maximal Loss (ML) risk measure, regularized by the norm, for stocks and observations (Section 3.1).

We show in Section 3.2 that any coherent risk measure can become unstable to estimation error for norm based regularization. The proof generalizes that given in [11] for unregularized portfolio optimization. The proof relies on the probability of the existence of dominating portfolios. Depending on the ratio , this probability can be either very close to zero – making the instability a rare event that can be neglected – or very close to one. Sharp results for the threshold value of that separates the two cases can be given in the limit with fixed ratio, using methods from statistical mechanics (see Section 4).

3.1 regularized ML – a toy example

To develop an intuition about the regularized portfolio optimization problem with an regularizer, we first consider a simple risk measure called Maximal Loss (ML), defined as [41]

| (8) |

Maximal Loss is the best combination of the worst losses. As such it is a min-max type risk measure, a special case of Expected Shortfall (ES). Expected Shortfall is the average loss beyond a high quantile. The threshold beyond which the average loss ES is calculated has typical values in the range (0.95 to 1.00). Maximal Loss corresponds to .

The regularized portfolio optimization problem then becomes

| (9) |

where is the norm. This can be re-written to incorporate the regularizer directly into the loss function, since the term does not depend on the individual returns, measured at times . We can write the Regularized Maximal Loss as

| (10) |

Now, we investigate stability resulting from use of the norm, . To that end, let us consider the simple case of two assets () and two data points taken at times and . The loss associated with each time can be expressed as

| (11) |

where we have taken the budget constraint into account by setting and Now we distinguish three different cases:

-

•

if , then

-

•

if , then

-

•

if , then

The instability may arise in the following situations:

-

•

if , and (the two straights lines, and , both have positive slope).

-

•

if , and (the two straights lines, and , both have negative slope).

This means that in the absence of regularization the Maximal Loss is unbounded from below whenever one of the assets dominates the other (i.e. its return is higher at both times). Since both the loss function and the regularizer are piecewise linear functions, there is a threshold value for any given realization of returns such that if the instability is removed (see Figure 1). However, the threshold is in general different for different instances of the problem, therefore if we consider the whole ensemble of possible instances, the regularizer with a fixed, finite value of will only prevent the instability with a certain probability.

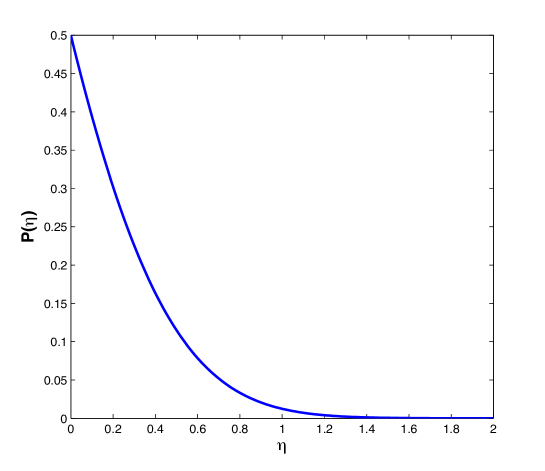

Let us calculate this probability by considering the ensemble of all possible realizations of returns. Assuming that are independent normal distributed random variables, the probability that the instability is not removed, is given by

| (12) |

Here the integration variable is distributed as the difference of two independent Gaussian variables.

The quantity is plotted in Figure 2.

This probability is positive for any finite , which means that a ”soft” implementation of the regularizer cannot prevent the instability. The instability disappears only for , when the regularizer imposes an infinite penalty on solutions with the weights outside the interval [0,1]. This ”hard” constraint is equivalent to a ban on short selling.

Whenever the original problem is unstable and the regularizer removes the instability, it does so by setting the weight of the dominant asset to 1, and that of the dominated asset to 0. The well-known property of – that it produces a sparse solution – means in the toy example considered here that it eliminates one of the assets.

The soft implementation of fails to eliminate the instability, because the original loss function and the regularizer are piecewise linear functions. In contrast, a nonlinear regularizer, such as the norm, removes the instability, as can be seen by considering the losses at times :

| (13) | |||||

| (14) |

The losses are now convex quadratic functions, therefore a finite and unique minimum for the Maximal Loss exists for all nonzero values of . The same holds true for any norm with , whereas a norm with can not remove the instability.

3.2 Instability of regularized coherent risk measures

We generalize the proof of the instability of coherent risk measures [11], which relies on the notion of dominant portfolios. The first step is to show that if such a dominant portfolio exists, then coherent risk measures are unbounded from below and the optimization problem is ill-defined. The second step is to show that the probability that dominant portfolios exist is bounded away from zero.

A vector is said to be a -dominant portfolio if i) and ii) for all , where is the norm.

Proposition: If a -dominant portfolio exists, then no finite -regularized portfolio can exist for .

Proof: The objective function that we wish to minimize is

| (15) |

For any normalized portfolio (i.e. ) consider the portfolio , where is a -dominant portfolio. This is a normalized portfolio, because of i) in the definition of . Now

To get to eq. (3.2), we used monotonicity with (constant) and .

For positive constant , which means that

| (17) |

For we can achieve portfolios with negative risk of arbitrarily large absolute value by letting : the solution of the optimization problem runs off to infinity.

Therefore, regularization is not a good choice if the probability that a -dominant portfolio exists is non-zero. The probability that a -dominant portfolio exists depends on the distribution of returns, and it is therefore hard to make any general statements without making assumptions about this distribution. Yet, if the support of the distribution of returns extends to the whole real axis, then the probability that a -dominant portfolio exists is non-zero. In the next section we assume Gaussian (random) portfolios, providing some intuition about this probability.

Notice that the proof breaks down when the norm is replaced by the norm with . Then the objective function

| (18) |

is dominated by the regularization term when the weights diverge.

Conversely, for it is the regularization term that becomes negligible compared to the risk measure. Hence regularization with is not able to cure the instability, as soon as a -dominant portfolio arises, for any .

4 Regularized Expected Shortfall for large random portfolios.

In this section we consider the problem of RPO for the risk measure Expected Shortfall in the particular case where both the number of assets and the number of observations are large (), but their ratio is a finite constant. In order to derive quantitative results, we consider, for the sake of simplicity, the case of i.i.d standard normal returns. We can extend the approach of [3] to include regularization (see also [38]). This provides us with typical results, i.e. results that occur with probability arbitrarily close to one in the limit .

For i.i.d. random returns, the true optimal solution is the one where all the weights are the same, . Individual solutions based on specific samples will likely deviate from the true optimum, especially when the sample size, , is not large enough. The optima for individual samples may deviate from symmetry, but averaging over the samples will necessarily restore it. Likewise, the regularizer that tends to produce sparse solutions will not be able to make a distinction between the equivalent assets, therefore it will set some weights to zero at random for each sample. Our goal here is merely to demonstrate the effect of on the instability of a portfolio optimized under ES. The real effect of should be studied using a heterogeneous (non-i.i.d.) portfolio, a problem we leave for future research.

The optimization of historical Expected Shortfall can be formulated as a linear programming problem [6]. Expected Shortfall is a piecewise linear loss function, just like the Maximal Loss. The optimization problem, including the regularizer, reads

| (19) | |||||

| (21) | |||||

where is a normalization parameter that is usually set to one. However, since market-impact depends on the size of the position that is liquidated, we explicitly keep track of in what follows. In addition, the sum of the weights was chosen to be of the order of , in order for the optimal weights to be of order one.

Assuming Gaussian returns, we can solve the above optimization problem analytically. Generalizing [3, 38] by including the regularizer, we follow lines familiar from the statistical physics of disordered systems: the loss function is regarded as the Hamiltonian (energy functional) of a fictitious statistical physics system, a fictitious temperature is introduced and the free energy of this system is calculated in the limit with fixed. Averaging over the different realizations of the returns corresponds to what is called quenched averaging in statistical physics. We report here only the final result, and refer the interested reader to the Appendix, where details of the calculation are given. After some effort, one ends up with a free energy functional, depending on six variables, the so-called order parameters:

where

| (23) |

The function is given in the Appendix. In Eq. (4) represents an average over the normal variable . The “true” free energy, i.e. the minimal risk per asset, is the stationary point of the above expression with respect to variations of the order parameters and . The original optimization problem involving variables has been reduced, in the limit of large and , to the simpler problem of finding the minimum of the functional that only depends on six variables.

4.1 regularization

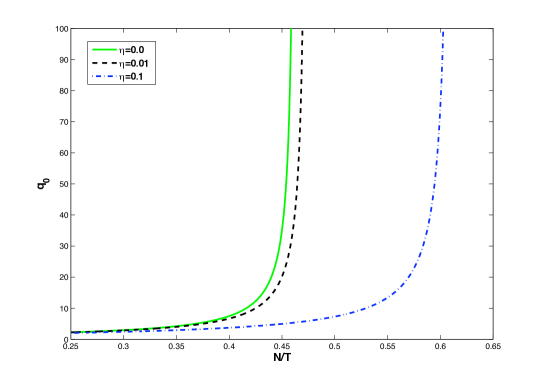

The origin of the instability for the Expected Shortfall under is the same as with Maximal Loss: Expected Shortfall diverges (becomes unbounded from below) when there is a dominating portfolio [11]. The divergence of ES is linear, therefore a piecewise linear regularizer like will not be able to eliminate the instability completely, it will do so only with a certain probability, depending on the sample. Thus we expect that after averaging over the ensemble of random returns the instability will persist. Yet, we know [3] that the probability to observe the instability is essentially zero for when is larger than a critical threshold whereas it is arbitrarily close to one if . We now illustrate how the instability arises by analyzing the extrema of Eq. (4), and show that regularization merely shifts the instability to a smaller threshold.

The fact that the solution for contains a nested optimization problem over in the first term on the second line of Eq. (4) is not accidental. Indeed, this arises from the optimization over the weights of the original problem. Therefore, the minimization of can be thought of as a “representative weight” problem, where the random variable over which the expectation is taken encodes the effect of the randomness in the sample.

The solution of the representative weight problem

| (24) |

has the typical shape induced by regularization. The Gaussian distribution of the then induces the weights to be distributed according to .

The first-order conditions for the free energy read

| (25) |

| (26) |

| (27) |

| (28) |

| (29) |

| (30) |

Notice in particular, that the first of these equations translates the budget constraint of the original problem into the properties of the representative weight problem above. The last equation, instead, relates the parameter to the fluctuation of the weights. This corresponds to the distance of the solution from the optimal one (given by the constant portfolio). In the present setting, this is also related to the estimation error, since different samples will deviate from the optimal solution in different ways.

The instability of portfolio optimization manifests itself in the divergence of the parameter . This, in turn, implies that the distribution of weights becomes degenerate, i.e. infinitely broad. Hence, some intuition about the origin of the instability can be gained from looking at the optimization problem for the representative weight. From the form of we see that the optimization problem for always has a finite solution as long as the order parameter . However, when , can be unbounded from below. In this case, the estimated expected shortfall runs to minus infinity, because the term in the free energy diverges. Note that, because of the budget constraint implemented in equation (25), the optimal portfolio will in this case dictate to go infinitely long in some of the assets and infinitely short in some of the others. In summary, the condition is what determines the critical point.

We numerically solved the system of equations (25)–(30), and we plot in Figure 3 the quantity as a function of the ratio for different values of the regularizer’s amplitude . The study of the stationarity conditions shows that, similarly to what we saw in the toy example, the regularization produces a shift towards higher values of of the feasible-infeasible transition, but does not eliminate it completely. The shift in the critical point where the estimation error blows up is clearly seen in Figure 3.

In the toy example discussed in section 3.1 we furthermore saw that the hard implementation of the constraint, obtained in the limit , was equivalent to a ban on short selling. This is true also here. Indeed, if goes to infinity, the regularizer imposes infinite penalty on any solution not on the ball (defined by the relation ). On the other hand, the solution also has to be on the plane corresponding to the budget constraint. This means the solution must be on the (+,+,+…+) face of the ball, where all the weights are positive. Conversely, if all the weights are positive and they also satisfy the budget constraint, then the solution is necessarily on the (+,+,+…+) face of the ball.

That imposing a ban on short positions helps taming the large sample fluctuations was noticed by [18] though the authors did not make the connection to regularization. It is clear that any constraint that reduces the domain over which the optimum is sought to a finite volume has a similar effect: there cannot be infinite fluctuations in a finite volume.

4.2 -norm

There is no qualitative difference between the effects of the soft (finite ) or hard () implementation of a non-linear regularizer that grows faster than linear, such as the -norm with ; the regularizer will eliminate the instability either way.

We can see this by noting that if , then the function always has a finite minimum for any value of , thus preventing the divergence of the estimation error. The solution of the representative weight problem, can be obtained by minimization of the function (Eq. 23). Let . To compute we must solve

| (31) |

Taking the limit , if the equation reduces to

| (32) |

which always has a finite solution for finite . More generally, we can say that any regularizer that grows faster than linear will prevent the solutions from running away to infinity.

4.3 Linear combination of the and regularizers.

In high-dimensional problems it is often expedient to use a combination of the and regularizers [1], sometimes called the elastic net [44]. This setting leads to the following optimization problem

| (33) | |||||

| (35) | |||||

The replica method readily extends also to this case. In this situation the free energy is again of the form (4), but with

| (36) |

The solution of the optimization problem for the representative weight reads:

| (37) |

From these expressions we see that the divergence of is prevented as long as , while a divergence may occur if when .

Using this form of to evaluate the averages over the variable that appear in equations (25), (29) and (30), we numerically solve the set of first-order conditions (25)–(30).

We show the behavior of as a function of the parameters and , for , in Figure 4 . The dependence on is naturally stronger than the dependence on .

A useful scheme may be to set to a value that ensures small estimation error given the value of in a particular application, and then to vary in order to achieve the desired level of sparseness. Although sparseness reduces diversification, there might be situations where limiting the dimension of a portfolio may be advantageous, for example by limiting transaction costs.

5 Conclusion

We have shown that market impact considerations will drive an investor to Regularized Portfolio Optimization (RPO) under any coherent risk measure. The impact function determines which regularizer should be used. Generalizing our previous result, that linear impact leads to the use of the norm regularizer [38], we have shown here how the impact function selects the regularizer in general.

We have also demonstrated that the instability of Expected Shortfall found in [3] will be removed by any nonlinear regularizer that grows faster than linear, but will only be shifted by the piecewise linear norm based regularizer that corresponds to a bid-ask spread impact. Although we wanted to mostly concentrate on Expected Shortfall in this paper, we would like to point out that due to the positive homogeneity and translational invariance axioms, regularizers will have the same effect on any coherent measure as they do on ES. (Moreover, as these properties are shared also by Value at Risk, this extends also to VaR.)

We find it appealing that the statistically motivated use of regularizers is intimately linked to market impact: consideration of finite liquidity should limit excessively large positions, which is exactly what regularizers do.

We also find it remarkable how powerful the method of replicas proves to be in producing analytic results for the estimation error in situations which would probably be very hard to approach by more conventional methods of probability theory.

Acknowledgement

I.K. has been supported by the European Union under grant agreement No. FP7-ICT-255987-FOC-II Project and by the Institute for New Economic Thinking under grant agreement ID: INO1200019. S.S. thanks the Abdus Salam International Center for Theoretical Physics for their hospitality and support of this collaboration. M.M. acknowledges support from the Marie Curie Training Network NETADIS (FP7 - Grant 290038).

Appendix

In this appendix we show how, in the limit where and go to infinity, the optimization problem defined by equations (19), (21) and (21) can be reduced to that of finding the minimum of the free energy functional given by (4).

We need to find the minimum of

under the constraints

and

The calculation proceeds as follows: Given a history of returns , we introduce the inverse temperature parameter and define the canonical partition function (or generating functional) as

| (38) |

where if and zero otherwise. The partition function is therefore an integral over all possible configurations of variables that are compatible with the constraints of the problem, where each configuration is weighted by the quantity (the Boltzmann weight). From the partition function, the minimum cost (per asset) can be computed in the limit of large as

| (39) |

To derive the typical properties of the ensemble we have to average over all possible realizations of returns and compute

| (40) |

where is the probability density function of returns. This calculation can be performed by help of the replica trick, using the identity

| (41) |

For integer , we can compute as the partition function of a system composed of replicas of the original systems. An analytical continuation to real values of will then allow us to perform the limit and obtain the sought quantity .

The replicated partition function can be computed as444In the calculation we will not keep track of constant multiplicative factors that do not affect the final result.

where we have assumed that

| (42) |

and we have enforced the constraints through the Lagrange multipliers , and . Averaging over the quenched variables and introducing the overlap matrix and its conjugate one obtains

We can now perform the Gaussian integral over the variables :

Introducing the variables and and integrating over the we obtain

where

In order to make further progress, let us consider the replica symmetric ansatz

| (43) |

| (44) |

and introduce the following rescaling relations

| (45) | |||||

| (46) | |||||

| (47) | |||||

| (48) |

The -dependent part of the partition function is

| (49) |

Exploiting the identity valid for , and after some manipulations, we arrive at the following contribution to the free energy

| (50) |

where the notation means averaging over the normal variable . After some further manipulations, we can write the partition function as

| (51) |

where

with ,

| (53) |

and

| (54) |

In the limit of large the integral in equation (51) is concentrated around the minimum of and can be computed through the saddle point method.

The minimum cost

| (55) |

corresponds then to the minimum of the free energy functional in the limit .

References

- [1] P. Bühlmann and S. van de Geer. Statistics for High-Dimensional Data: Methods, Theory and Applications. Springer Series in Statistics. Springer, Berlin, Heidelberg, 2011.

- [2] I. Kondor, S. Pafka, and G. Nagy. Noise sensitivity of portfolio selection under various risk measures. Journal of Banking and Finance, 31:1545–1573, 2007.

- [3] S. Ciliberti, I. Kondor, and M. Mezard. On the feasibility of portfolio optimization under expected shortfall. Quantitative Finance, 7:389–396, 2007.

- [4] M. Mézard and A. Montanari. Information, Physics, and Computation. Oxford Graduate Texts. OUP Oxford, 2009.

- [5] I. Varga-Haszonits and I. Kondor. Noise Sensitivity of Portfolio Selection in Constant Conditional Correlation GARCH models. Physica, A385:307–318, 2007.

- [6] R. T. Rockafellar and S. Uryasev. Optimization of conditional value-at-risk. Journal of Risk, 2(3):21–41, 2000.

- [7] C. Acerbi, C. Nordio, and C. Sirtori. Expected Shortfall as a Tool for Financial Risk Management, February 2001.

- [8] Basel Committee on Banking Supervision. Fundamental review of the trading book, 2012.

- [9] Basel Committee on Banking Supervision . Fundamental review of the trading book: A revised market risk framework., 2013.

- [10] I. Varga-Haszonits and I. Kondor. The instability of downside risk measures. J. Stat. Mech., P12007, 2008.

- [11] I. Kondor and I. Varga-Haszonits. Instability of portfolio optimization under coherent risk measures. Advances in Complex Systems, 13, 2010.

- [12] P. Artzner, F. Delbaen, J.-M. Eber, and D. Heath. Coherent Measures of Risk. Mathematical Finance, 9:203–228, 1999.

- [13] E. J. Elton and M. J. Gruber. Modern Portfolio Theory and Investment Analysis. Wiley, New York, 1995.

- [14] J.D. Jobson and B. Korkie. Improved Estimation for Markowitz Portfolios Using James-Stein Type Estimators. Proceedings of the American Statistical Association (Business and Economic Statistics), 1:279–284, 1979.

- [15] P. Jorion. Bayes-Stein Estimation for Portfolio Analysis. Journal of Financial and Quantitative Analysis, 21:279–292, 1986.

- [16] P.A. Frost and J.E. Savarino. An Empirical Bayes Approach to Efficient Portfolio Selection. Journal of Financial and Quantitative Analysis, 21:293–305, 1986.

- [17] R. Macrae and C. Watkins. Safe portfolio optimization. In H. Bacelar-Nicolau, F. C. Nicolau, and J. Janssen, editors, Proceedings of the IX International Symposium of AppliedStochastic Models and Data Analysis: Quantitative Methods in Business and Industry Society, ASMDA-99, 14-17 June 1999, Lisbon, Portugal, page 435. INE, Statistics National Institute, Portugal, 1999.

- [18] R. Jagannathan and T. Ma. Risk reduction in large portfolios: Why imposing the wrong constraints helps. Journal of Finance, 58:1651–1684, 2003.

- [19] O. Ledoit and M. Wolf. Improved Estimation of the Covariance Matrix of Stock Returns with an Application to Portfolio Selection. Journal of Empirical Finance, 10(5):603–621, 2003.

- [20] O. Ledoit and M. Wolf. A well-conditioned estimator for large-dimensional covariance matrices. J. Multivar. Anal., 88:365–411, 2004.

- [21] O. Ledoit and M. Wolf. Honey, I Shrunk the Sample Covariance Matrix. J. Portfolio Management, 31:110, 2004.

- [22] V. DeMiguel, L. Garlappi, and R. Uppal. Optimal versus Naive Diversification: How Efficient is the 1/N Portfolio Strategy? Review of Financial Studies, 2007.

- [23] L. Garlappi, R. Uppal, and T. Wang. Portfolio selection with parameter and model uncertainty: a multi-prior approach. Review of Financial Studies, 20:41–81, 2007.

- [24] V. Golosnoy and Y. Okhrin. Multivariate shrinkage for optimal portfolio weights. The European Journal of Finance, 13:441–458, 2007.

- [25] R. Kan and G. Zhou. Optimal portfolio choice with parameter uncertainty. Journal of Financial and Quantitative Analysis, 42:621–656, 2007.

- [26] G. Frahm and Ch. Memmel. Dominating estimators for the global minimum variance portfolio, 2009. Deutsche Bundesbank, Discussion Paper, Series 2: Banking and Financial Studies.

- [27] V. DeMiguel, L. Garlappi, F. J. Nogales, and R. Uppal. A generalized approach to portfolio optimization: Improving performance by constraining portfolio norms. Management Science, 55:798–812, 2009.

- [28] J. Brodie, I. Daubechies, C. De Mol, D. Giannone, and I. Loris. Sparse and stable markowitz portfolios. Proceedings of the National Academy of Sciences, 106(30):12267–12272, 2009.

- [29] L. Laloux, P. Cizeau, J.-P. Bouchaud, and M. Potters. Noise Dressing of Financial Correlation Matrices. Phys. Rev. Lett., 83:1467–1470, 1999.

- [30] V. Plerou, P. Gopikrishnan, B. Rosenow, L.A.N. Amaral, and H.E. Stanley. Universal and Non-Universal Properties of Cross-Correlations in Financial Time Series. Phys. Rev. Lett., 83:1471, 1999.

- [31] L. Laloux, P. Cizeau, J.-P. Bouchaud, and M. Potters. Random Matrix Theory and Financial Correlations. International Journal of Theoretical and Applied Finance, 3:391, 2000.

- [32] V. Plerou, P. Gopikrishnan, B. Rosenow, L. A. N. Amaral, and H. E. Stanley. Universal and nonuniversal properties of cross correlations in financial time series. Phys. Rev. Lett., 83:1471–1474, Aug 1999.

- [33] Z. Burda, A. Goerlich, and A. Jarosz. Signal and noise in correlation matrix. Physica, A343:295, 2004.

- [34] M. Potters and J.-Ph. Bouchaud. Financial applications of random matrix theory: Old laces and new pieces. Acta Phys. Pol., B36:2767, 2005.

- [35] S. Still and I. Kondor. Regularizing portfolio optimization. New Journal of Physics, 12(7):075034, 2010.

- [36] B. Schölkopf, A. J. Smola, R. C. Williamson, and P. L. Bartlett. New support vector algorithms. Neural Computation, 12(5):1207–1245, 05 2000.

- [37] A. Takeda and M. Sugiyama. -support vector machine as conditional value-at-risk minimization. In A. McCallum and S. Roweis, editors, Proceedings of the 25th international conference on Machine learning (ICML), volume 307, pages 1056–1063. Omnipress, 2008.

- [38] F. Caccioli, S. Still, M. Marsili, and I. Kondor. Optimal liquidation strategies regularize portfolio selection. The European Journal of Finance, 19(6):554–571, 2013.

- [39] B. Toth, Y. Lemperiere, C. Deremble, J. de Lataillade, J. Kockelkoren, and J-P. Bouchaud. Anomalous price impact and the critical nature of liquidity in financial markets. Physical Review X, 1(2):021006, 2011. http://arxiv.org/abs/1105.1694.

- [40] J. D. Farmer, A. Gerig, F. Lillo, and H. Waelbroeck. How efficiency shapes market impact. Quantitative Finance, 13(11):1743–1758, 2013.

- [41] M. R. Young. A minimax portfolio selection rule with linear programming solution. Management Science, 44:673–683, 1998.

- [42] E. Moro, L. G. Moyano, J. Vicente, A. Gerig, J. D. Farmer, G. Vaglica, F. Lillo, and R.N. Mantegna. Market impact and trading protocols of hidden orders in stock markets. Physical Review E., 80(6):066102, 2009.

- [43] F. Caccioli, J.-P. Bouchaud, and Farmer J. D. A proposal for impact-adjusted valuation: Critical leverage and execution risk. arXiv:1204.0922, 2012.

- [44] Hui Zou and Trevor Hastie. Regularization and variable selection via the elastic net. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 67(2):301–320, 2005.