Cluster analysis of weighted bipartite networks:

a new copula-based approach

Abstract

In this work we are interested in identifying clusters of “positional equivalent” actors, i.e. actors who play a similar role in a system. In particular, we analyze weighted bipartite networks that describes the relationships between actors on one side and features or traits on the other, together with the intensity level to which actors show their features. The main contribution of our work is twofold. First, we develop a methodological approach that takes into account the underlying multivariate dependence among groups of actors. The idea is that positions in a network could be defined on the basis of the similar intensity levels that the actors exhibit in expressing some features, instead of just considering relationships that actors hold with each others. Second, we propose a new clustering procedure that exploits the potentiality of copula functions, a mathematical instrument for the modelization of the stochastic dependence structure. Our clustering algorithm can be applied both to binary and real-valued matrices. We validate it with simulations and applications to real-world data.

Keywords: clustering, complex network, copula function, positional analysis, weighted bipartite network.

1 Introduction

In the last few years complex network theory has attracted the

interest of a widespread audience as a powerful tool to analyze

complex relational structures and to represent big data

[28].

Network analysis usually deals with a massive

amount of data that requires to be managed and organized efficiently

in order to extract as much information as possible, reducing the

dimensionality of the problem. One of the most important methodologies

to tackle this issue is the identification of network communities

[12], [19], [20],

[32]. Community detection allows us to extract

sub-networks which exhibit different properties from the aggregate

properties of the whole network and also to investigate information on

groups of nodes with similar characteristics which are more

likely to be connected to each other. Communities are usually defined

as subsets of nodes that are densely connected, i.e., they are more

connected among themselves than to the rest of the network. However,

in many network applications, there is a meaningful group structure

which does not coincide with the partition into dense communities:

indeed, the groups may be characterized by similar patterns of

interactions with other groups [8]. Within this context,

positional analysis is particularly interesting since it deals

with the identification of actors who occupy an equivalent position in

a system, i.e. play a similar role in the considered

organization. Differently to the community detection where the

clusters are represented by densely connected groups of actors,

positional analysis aims at studying relational data in order to

cluster the actors into some classes such that the elements of the

same class occupy equivalent positions in the system. In order to

illustrate the distinction between positional analysis and community

detection, let us consider the following example of the e-mails sent

among the employees of a company: it may be that we are able to

identify different communities of individuals among which e-mails are

more frequently exchanged. However, densely connected employees may

occupy different positions in the organization and we need to run a

positional analysis if we are interested in identifying groups of

actors with equivalent positions.

In this work we aim at

identifying clusters of “positional equivalent” actors in cases

where the available data are the relationships defined among actors on

one side and some features on the other one [5],

[6], [11], instead of interpersonal

relationships. Basically, the idea is that positions in a network

structure can be defined according to the characteristics or

behaviours that the actors exhibit, instead of the relationships that

actors hold with other actors. Individual to attribute relations can

be represented as a weighted bipartite network where the

edge-weights represent the level to which actors show a particular

feature. More precisely, a network is bipartite if its nodes can be

divided into two sets in such a way that every edge connects a node in

one set to a node in the other one [2]. Bipartite

networks are thus very useful for representing data in which the

elements under scrutiny belong to two categories (typically referred

to as actors, or agents, and features, respectively), and we want to

understand how the elements in one category are associated with those

in the other one. Notable examples that have been analyzed include

networks of company directors and the board of directors on which they

sit [14], [29], scientific collaboration

networks [3], [21], [32],

networks of documents and words [15], as well as network

of genes and genetic sequences [26].

The

widespread approach to partition bipartite networks consists of

applying standard community detection algorithms, such as the

Girvan-Newman modularity [20], to the one-mode projection

of the original network. Consider two types of nodes, say a and

b, in a one-mode projection of the bipartite network, nodes of

the same type, say a, are connected to each other if they share

a common node of the other type, say b. For instance, in the CEO

network, two CEOs are connected if they both sit in the same

board. Although the one-mode projection procedure can give some

insights on the topological properties of the network, at the same

time it can imply the lost of relevant information. In fact, different

bipartite networks may reduce to the same one-mode projection, and

thus a clustering based on the latter may produce unreliable or

incorrect results, as shown in [13] and [37].

Regardless of those critiques, in [18] the authors argue

that under some circumstances, using multiple projections, the

information extracted with this procedure is sound, and therefore the

simplicity of this approach can be still exploited. However, several

authors tried to solve this problem by defining measures and

algorithms that could be directly applied to the original matrix

associated to the bipartite network.

In the physics

community, two different definitions of bipartite modularity have been

proposed, [4], [22]. Both concepts extend the

Girvan-Newman modularity, but pose different assumptions on the null

model taken as the benchmark in the metric used for the module

identification. They return good results compared to the one-mode

projection, but their applicability is restricted to the case of

binary bipartite networks.

Some applications of bipartite

networks refer to affiliation networks [7], which

capture social relationships, such as membership or event

participation. Positional analysis is well established in social

network literature, where the usual approach consists of applying the

standard measures of structural or regular equivalence, and the

related algorithms, to the one mode-projection of the affiliation

network [36]. However, affiliation networks represent only

a very special case of bipartite networks since the associated

matrices are binary.

Other proposed methods for bipartite

network clustering, that are mostly used by sociologists, are based on

blockmodeling (e.g. [9], [10], [17]

and [38]). The key idea of this approach is that the rows and

the columns of the matrix associated to the bipartite network can be

partitioned simultaneously by means of a criterion function, which

measures the inconsistencies of the empirical blocks with the ideal

ones. Therefore, blockmodeling works directly on the matrix by trying

to permute rows and columns in order to fit, as closely as possible,

idealized pictures. The differences between the various types of

blockmodeling techniques concern the definition of the ideal blocks

and the criterion functions. Blockmodeling is mostly applied to binary

data, but it can also be exploited for weighted matrices (valued

blockmodeling and homogeneity blockmodeling [38]). However,

with the valued blockmodeling, information about the values above a

pre-specified parameter is lost and a problem is to determine

appropriately the value of this parameter. The homogeneity

blockmodeling does not require any additional parameters to be set in

advance and it uses all available information, but its main

disadvantage is that it can consider only a few possible ideal

blocks.

In [27], the authors proposed a

bipartite stochastic block model where a parametric

probabilistic structure is given, and the clusters are

identified by solving the inference problem of finding the parameters

that best fit the observed network. In particular, they model the

generating process of the number of edges between two nodes of

different types with a Poisson distribution with a certain intensity

parameter. The authors show that their method outperforms the one-mode

projection approach. Nevertheless, it does not deal with the case when

we have weights on the edges. In [1], the authors try to

go in this direction by proposing a stochastic block model for

edge-weighted networks, but their method requires to choose the number

of clusters (as in most stochastic block models).

The

algorithm we propose realizes a partition of “positional equivalent”

actors based on the entire information enclosed in the weighted

bipartite network that describes their characteristics or

behaviours. The main contribution of our work is twofold. First, we

develop a new methodological approach according to which actors are

grouped with respect to their intrinsic multivariate stochastic

dependence structure. In this framework, not only the magnitude of a

single weight matters but the whole pattern of the values the actors

show along all the features is relevant for the

classification. Second, we propose a new clustering procedure that

exploits the potentiality of copula functions, a mathematical

instrument for the modelization of the multivariate stochastic

dependence structure. In particular, copulas allow us to group actors

according to their underlying dependence structure, without any

assumption on their one-dimensional marginal distributions, and to

take into account various kinds of stochastic dependence structures

among actors. Moreover, there is no need to predefine the target

number of clusters.

The paper is structured as follows. In

Sections 2 and 3, we describe our approach,

together with the mathematical tool we employ, and then we illustrate

our clustering procedure. In Sections 4 and 5 we

show the performance of our clustering algorithm applying it to

simulated and real data. Finally, in Section 6 we conclude

with a discussion of the potentiality of our method and possible

future applications and extensions.

2 A copula-based approach

As explained in the previous section, we consider the general setting

where we have an real-valued matrix, that collects the

information on the connections that go from a set of actors to a

set of items, representing some features or behaviours. The

elements of such a matrix can be any real numbers, with zero

representing the absence of a relationship and a non-zero value

representing the presence of a relationships, together with its

intensity. As an example, this framework can be used to analyse

situations where we have actors on one side and personal qualities or

interests on the other side, and the weighted-edges between the two

sets can be used to represents the level to which an individual shows

a certain quality or interest. Another example may be a set of

individuals in a supermarket and the set of products they buy. In this

case, an edge represent whether an individual bought a particular

product or not, and its value gives the amount of product bought or

its cost.

Against this background, we want to emphasize that

actors may be classified into positions based on their patterns of

characteristics, interests or behaviours that they exhibit and on the

intensity wherewith the actors show them, instead of the kind of

relationships that they keep with other actors. In other words, we

move in the direction that the dependence (we mean positive

dependence, i.e. similarity) in the expression levels of the

considered features is related to the position that the actors occupy

in the system. Hence, we say that some actors are positional

equivalent if they show a significant dependence structure that

join them. In this framework, the use of the traditional one-mode

projection methods would be meaningless and misleading and also

blockmodeling or modularity approaches adapted to bipartite networks

could not give a clear answer to the problem because they are not well

tailor made for the analysis of weighted bipartite networks.

Our purpose is to identify clusters of actors by means of the

detection, from the original matrix, of some statistically significant

dependencies among groups of actors. Basically, our assumption is that

actors within a system have an underlying multivariate stochastic

dependence structure which generates the data. In order to identify

this intrinsic dependence structure, we propose to exploit the

mathematical copula theory.

The concept of copula was

introduced during the forties and the fifties with Hoeffding

[23] and Sklar [33], but the evidence of a

growing interest in this kind of functions in statistics started only

in the nineties [31]. Copulas are functions that join or

“couple” multivariate distribution functions to their

one-dimensional marginal distributions. More precisely, we have the

following definition and results444For more details, we refer

to the various excellent monographs existing in literature, such as

[25], [31] and [34]..

Definition 1.

A -dimensional copula is a function defined on with values in , which satisfies the following three properties:

-

1.

for every and ;

-

2.

if for at least one , then ;

-

3.

for every with for all ,

where, for each , and .

The advantage of the copula functions and the reason why they are used in the dependence modeling is related to the Sklar’s theorem [33]. It essentially states that every multivariate cumulative distribution function can be rewritten in terms of the margins, i.e. the marginal cumulative distribution functions, and a copula.

Theorem 1.

Let be a multivariate cumulative distribution function with margins . Then there exists a copula such that, for every , we have

| (1) |

If the margins are all continuous, then is

unique; otherwise is uniquely determined on

.

Conversely, if is a copula and

are cumulative distribution functions, then

defined by (1) is a multivariate cumulative distribution

function with margins .

In the case when and are the marginal probability density functions associated to and , respectively, the copula density satisfies

There are different families of copula functions that capture different aspects of the dependence structure: positive and negative dependence, symmetry, heaviness of tail dependence and so on. In our work, we limit ourselves to the principal copula functions of the Archimedean family (namely, Gumbel, Clayton and Frank copulas, see Appendix B for their definitions), which model, through a unique parameter , situations with different degrees of dependence. Nonetheless, it is worth to note that the application of our methodology is not restricted to those copula functions.

3 Methodology

In this section we present a copula-based technique that realizes a partition of actors into clusters so that the actors belonging to the same cluster show a significant dependence structure that allows us to classify them as being “positional equivalent”. Our approach is inspired by the work of Di Lascio and Giannerini [16], which introduced and studied a copula-based clustering algorithm, called CoClust, in the framework of microarray data in genetics. As they did, we use copula functions in order to model the multivariate stochastic dependence structure among groups of actors and we apply the maximized log-likelihood function criterion for the detection of the different clusters. Notwithstanding, our algorithm presents the following important differences with respect to the one proposed by Di Lascio and Giannerini:

-

1)

while they assume independence within clusters and dependence between clusters, we look for clusters of dependent actors;

-

2)

while they first find the optimal number of clusters and then perform sequential extractions of actors, where at each time one actor is added to each cluster in a certain way, we do not use a sequential extraction method but we directly look for the optimal partition of the actors into clusters;

-

3)

differently from them, we allow clusters to be of different sizes and we allocate all the actors into the clusters;

-

4)

whereas they assume identity in distribution for actors inside a certain cluster, i.e. each cluster identifies one margin, we do not make this assumption and we estimate for each actor his own cumulative distribution function.

Given actors and items, we can represent the data that describe the relationships between actors and items with a real-valued matrix of dimension ,

where represents the value of the item for the actor

. With the language of network theory, this matrix can be seen as

the matrix associated to a weighted bipartite network.

The procedure we propose takes as input this matrix and returns the optimal decomposition into clusters after the following four steps:

-

1.

First of all, we find the empirical cumulative distribution function

of every actor based on the corresponding -dimensional row of the items. For each actor , we are taking the values of the items as i.i.d. realizations drawn from the same univariate distribution.

-

2.

The second step consists in the estimation of the copula objective function for each possible group of actors, with , using pseudo-maximum likelihood estimation in order to estimate the dependence parameter. Thus, for each possible group, say , with , of actors, we maximize the log-likelihood function defined as

where denotes the parametric expression for the chosen copula density, and we find the value such that

Note that we are taking the vectors as i.i.d. realizations drawn from the same -variate distribution.

-

3.

In the third step, we consider the set of all possible partitions of the actors that do not contain clusters with a single actor. Hence, each in is formed by a certain number of clusters with . The set represents the set of all possible decompositions into clusters that the procedure can return555For example, if we have actors, numbered from to , the set is formed by the following partitions: , , and .. Namely, we find the maximum value of the map defined on by

-

4.

Finally, the procedure returns such that

More precisely, it returns the clusters that form in a decreasing order with respect to the value of each cluster in .

The R code for this procedure is available at http://riccaboni.weebly.com/code.html.

4 Simulations

In order to verify the accuracy of the proposed algorithm, we conducted some simulation experiments. We considered different scenarios and, for each of them, various values of (i.e. the number of items): or . For each scenario and each value of , we generated random samples of observations (actors), grouped into clusters. Specifically, we simulated the following scenarios:

-

1.

In the first three scenarios, clusters were generated using standard Gaussian margins and the same copula type: one scenario with Gumbel, another with Clayton and another one with Frank. Two of the clusters had observations (actors) and the dependence parameter . The last one had observations (actors) with dependence parameter .

-

2.

In the second three scenarios, we generate the clusters using discrete marginal distribution, namely the Poisson distribution with parameter , and the same copula type: one scenario with Gumbel, another with Clayton and another one with Frank. Two clusters had observations (actors) and dependence parameter , while the third one had observations (actors) with dependence parameter .

-

3.

In the last three scenarios, we decided to draw the observations from different margins and using the same copula type: one scenario with Gumbel, another with Clayton and another one with Frank. In particular, the first two clusters had dependence parameter and respectively, Pareto(1,2) and Lognormal(0,1) marginal distributions. Instead, in the third cluster the dependence parameter was with Exponential(0.5) marginal distribution.

For each considered scenario and each value of , we tested the

algorithm applying the same copula used for the simulation of the

data. Moreover, for the first three scenarios and each value of ,

we also applied the algorithm with the other two copula types than the

one used for simulations.

We observed that the choice of the

copula for the algorithm has no great effect on the performance of the

algorithm and the results seem quite good, especially in the case when

or . Some main remarks can be made:

-

•

First of all, under all the possible scenarios, for or , we always got a percentage of successes in recognizing the clusters correctly.

-

•

Second, when the observations are drawn from the Gumbel and the Clayton copulas, we got a percentage of successes equal to already for and between and for .

-

•

Finally, when the observations are drawn from the Frank copula, we notice some problems for . Indeed, for this copula type, realizations are too few to generate an evident dependence structure and so the algorithm does not work well in recognized it. However, we observed a fast improvement for getting larger and, starting from , we can say that the percentage of successes are good ().

5 Applications to real-world data

In this section, we describe two applications of our algorithm to real datasets. The first one deals with a real-valued bipartite network. The second one refers to a widely studied social network that is described by a signed network.

5.1 Trade data

The first application we show is based on the BACI666French acronym of “Base pour l’Analyse du Commerce International”: Database for International Trade Analysis.-COMTRADE777Commodities Trade Statistics Database. dataset, featuring the amounts of import-export trades among several countries in the world. We extracted a weighted bipartite network taking the export dollar values for the product categories of the HS2 888The Harmonized System (HS) is an international nomenclature for the classification of products. It allows participating countries to classify traded goods on a common basis for customs purposes. It is a six-digit code system but we exploit the first two-digit in the analysis. classification, for selected countries, in the year . More in details, we decided to select the countries according to their economies, in order to identify hypothetical categories:

-

•

a First world category composed by France, Germany, Canada and United states;

-

•

a Third world category represented by Burundi, Zimbabwe, Liberia and Somalia;

-

•

an OPEC representative category made by Kuwait, Saudi Arabia, Qatar and Iran.

We applied our procedure to the matrix, where the countries were in

rows, the products in columns, and each cell contained the gross

export value of a given country for a given product. Our aim was to

create clusters of countries which are similar (i.e. positional

equivalent in the International Trade Network) with respect to the

products they export. Much of the literature that focuses on

international trade looks for community detection, that is for

communities of countries with a high number of connections among them,

while being relatively less interconnected with countries outside the

community they are part of [35]. Differently from the

classical clustering analysis in international trade, we tried to

define “positional equivalent” countries based on the products they

trade and not on the basis of the countries wherewith they trade.

Indeed, we were not interested in finding dense communities of

countries for different commodities, but we wanted to identify

countries that cover the same position in the trade network since they

present a similarity in their exports.

The result we

obtained is reported in Table 1. As we can see, the

algorithm is able to perfectly recognize the above mentioned country

groups. However, since these groups were built according to a

subjective judgement, we decided to analyze the data in order to

provide a more robust explanation for the clusters we found. In table

4 we report for each country, the percentage on

the total amount of export999It is important to remark that,

while in this table we report the percentage amounts for some

selected product categories, we applied our algorithm directly on

the export values for the all categories. for a selection of

HS2 categories out of the available, in order to give some

hints on the trade joint patterns that our algorithm recognize.

Overall, we can agree on the fact that the result is coherent with the

observed data. Regarding the First world category, we can see

that at least a small amount of their total exports is allocated in

each selected categories and about the of their total export is

concentrated in the nine categories, corresponding to the following

commodities: 84 - Nuclear reactors, Boilers, Machinery and

mechanicals appliances; 87 - Vehicles; 88 - Aircraft and

Spacecraft; 85 - Electrical machinery, Telecommunications

equipment, Sound and Television recorders; 30 - Pharmaceutical

products; 90 - Optical, Photographic, Cinematographic,

Measuring, Checking, Precision, Medical instruments.

Conversely, for

the OPEC Representative group, it is clear that the nature of

the dependence arises from the fact that more than the of the

total export of these countries belongs to the following three

categories: 27 - Mineral, Fuels, Oils; 29 - Organic

chemicals; 39 - Plastic and Articles thereof. Nonetheless, we

underline that our algorithm did not recognize this cluster just

because of the large share of export these countries have in these few

products, but it captured the whole dependence between these countries

and so also the categories in which they do not trade, or trade a

little, play an important role. This is clear by looking at the

network structure for the Third world category in the last four

columns of table 4. As it can be seen, all these

countries present a huge amount of the total export in a few specific

commodities. For example, more than the of the somalian export

is in category 1 - Live animals, while the of the

burundian export is in category 9 - Coffee, Tea, Mate and

Spices. Thus, we can affirm that these countries present a highly

specific production and the dependence among them arise not as a

consequence of the products in which they trade but rather from the

products in which they do not trade. By looking carefully at table

4, it is possible to notice that for most of the

selected 21 HS2 categories, the share of export is almost zero in all

these Third World countries. In this sense, they are similar to

the OPEC representative countries but, as we already said, the

latter present a specific dependence deriving from the common

commodities they trade. Finally, Canada deserves some

comments. It has an high value in category 27 as the countries

in the Opec representative category, but its values for the

other categories are more similar to those of the First world

than the ones of the Opec representative group. Our algorithm is

able to capture this aspect.

An insight of all these distinguishing

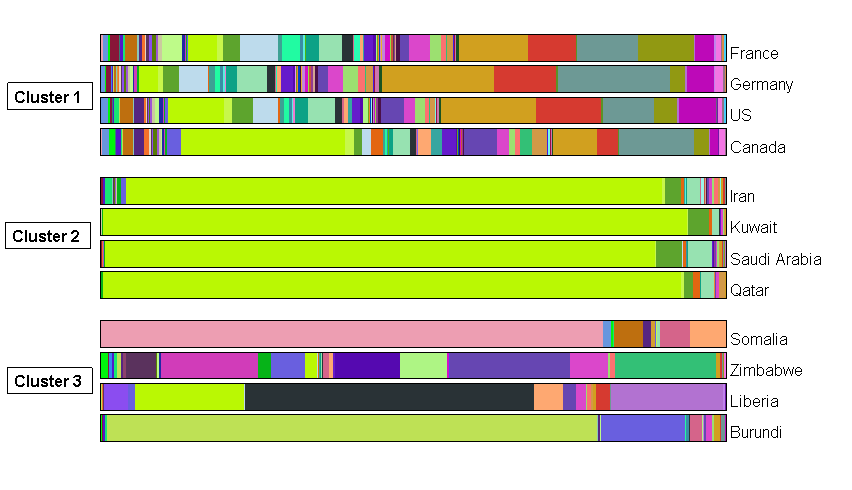

features between the clusters can also be grasped looking at figure

(1), where we report for each country a coloured bar

with the export shares for each of the 97 HS2 product categories over

the total amount of export, and figure (2), where

we depict the bipartite trade network between the countries and 15

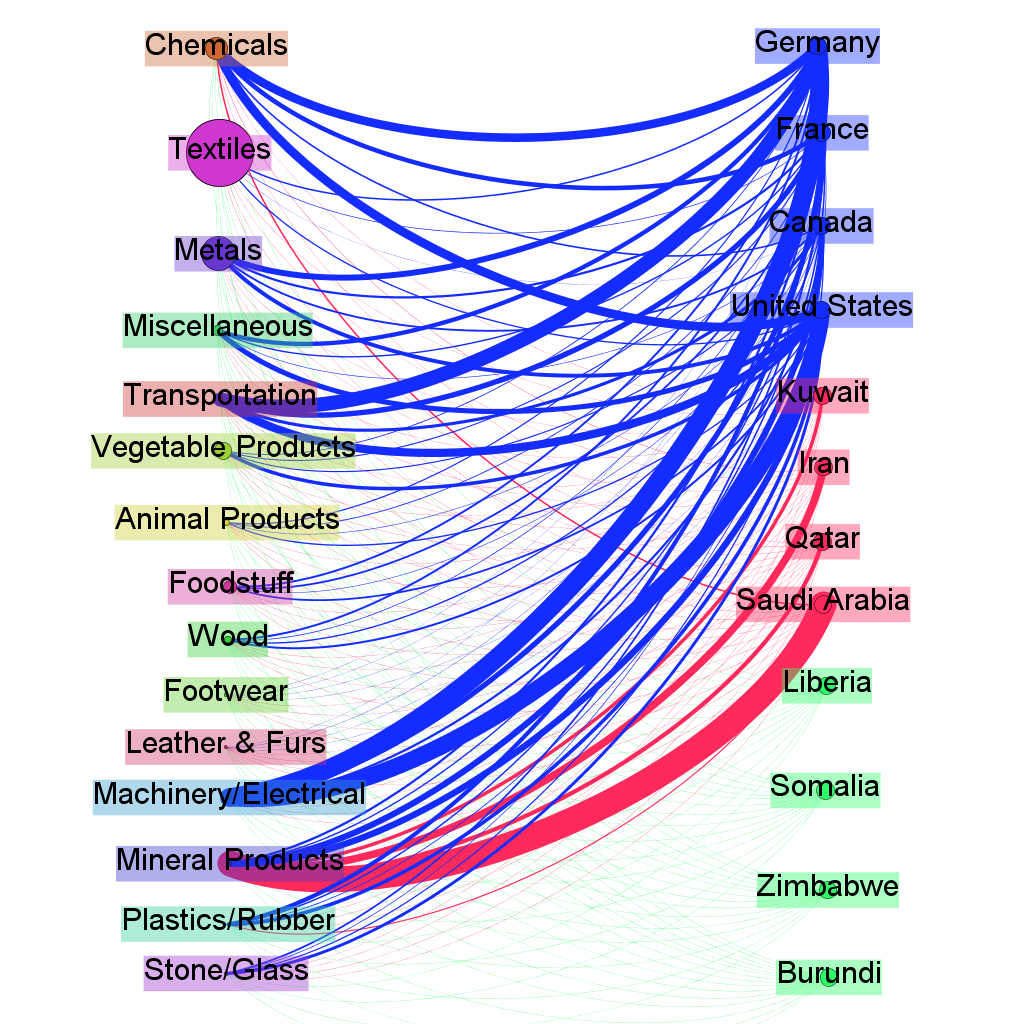

macro-categories of the HS2 products classification.

| Cluster 1 | France | Germany | United States | Canada |

|---|---|---|---|---|

| Cluster 2 | Iran | Kuwait | Saudi Arabia | Qatar |

| Cluster 3 | Burundi | Somalia | Zimbabwe | Liberia |

In this figure we report for each country, classified in the relative cluster, a coloured bar representing the share of export for each of the HS2 product categories over the total amount of export. Regarding Cluster 1, the high number of colours into the bar makes it clear that these countries use to trade in several product categories. Furthermore, an explicit dependence pattern arise from the proportion of the colours into the bars. In particular, the following product categories contributes to this strength relationship: 84 ( ) - Nuclear reactors, Boilers, Machinery and mechanicals appliances; 87 ( ) - Vehicles; 88 ( ) - Aircraft and Spacecraft; 85 ( ) - Electrical machinery, Telecommunications equipment, Sound and Television recorders; 30 ( ) - Pharmaceutical products; 90 ( ) - Optical, Photographic, Cinematographic, Measuring, Checking, Precision, Medical instruments. Regarding Cluster 2 the dependence relationship mainly arises from these three categories: 27 ( ) - Mineral, Fuels, Oils; 29 ( ) - Organic chemicals; 39 ( ) - Plastic and Articles thereof. However, it is important to remark that our clusering approach takes in consideration also the fact that these countries trade in a very small number of products, as can be seen from the few colours in the respective bars. The same reasoning apply for Cluster 3 where, although the countries are specialized in a unique product such as category 9 ( ) - Coffee, Tea, Mate and Spices for Burundi or category 1 ( ) - Live animals for Somalia, the common pattern that makes them similar is the fact that they do not trade in most of the HS2 categories.

In this figure we show the weighted bipartite Trade network. On the right the three groups of countries, detected by our algorithm, and on the left the products categories, grouped in homogeneus macro categories in order to highlight the relevant connections among the two different type of nodes. The size of the macro categories are in proportion to the number of categories grouped in them. It is clear from the links partition how our metodology is able to disentangle different country categories according to the trade patterns, even for the third world countries (green background) for which the link weights are much smaller than the others.

5.2 Supreme Court voting data

The second application is based on the dataset used in

[17] of the Supreme Court judges and their votes on a set

of issues. We have a signed bipartite network [30]

with justices, issues and the expressed

votes101010The table is filled with if the judge voted in the

majority for that issue and with if he was in the minority in

that decision. In case a is reported, it means that for that

particular case the judge refrain to vote..

In table

2, we present the result obtained with our algorithm

and the one obtained by Doreian [17]. At a first glance we

notice a remarkable similarity between the two results. However, it is

interesting to deepen the analysis by studying the data structure and

try to give a more detailed explanation for the differences. To this

end, we report in table (3) a permuted version

of the Supreme Court voting matrix, where the issues are blocked as in

[9] and the judges are partitioned according to the

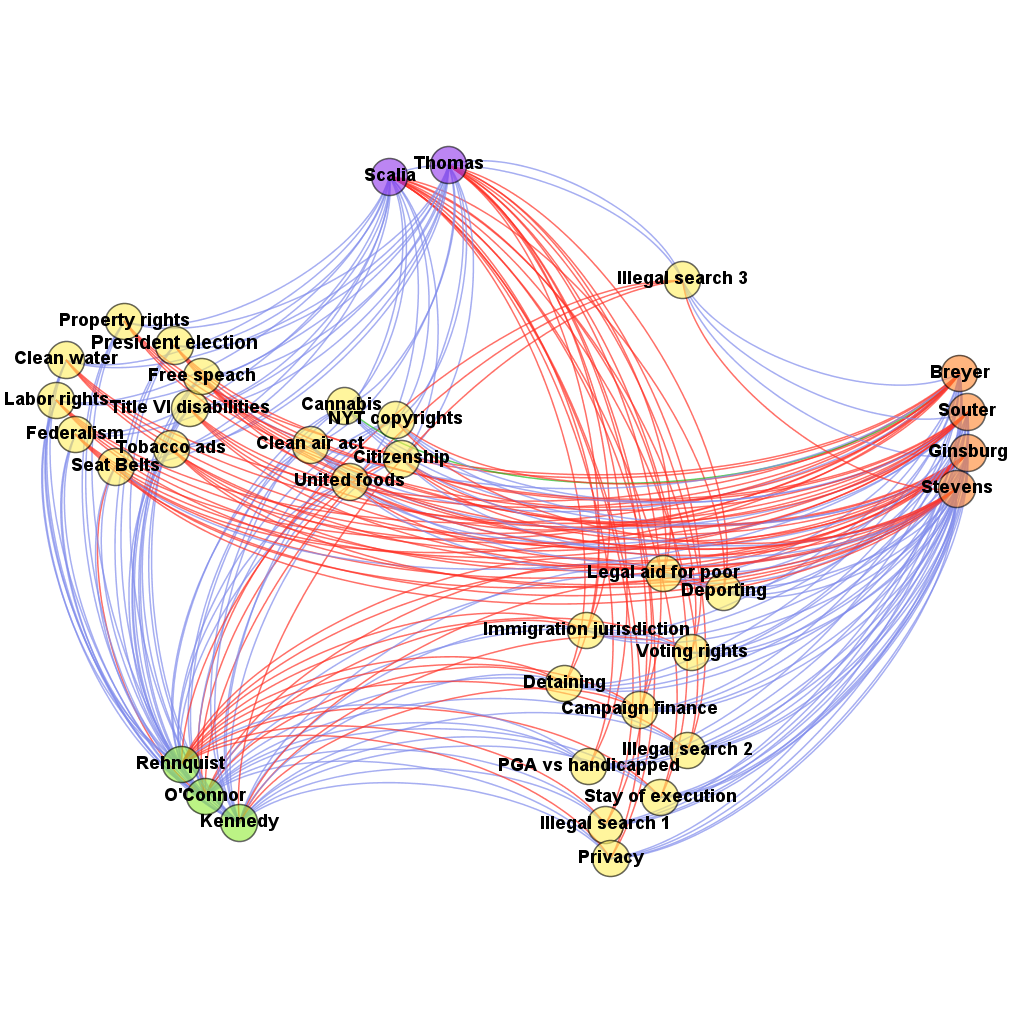

results from our algorithm, whereas in figure (3) we

depict the bipartite network structure. Looking at the first cluster,

containing Scalia and Thomas, and the second cluster,

composed by Breyer, Ginsburg, Souter, and Stevens, we can easily recognize a voting pattern remarkably

opposed one to each other and at the same time a coherent preference

expression within the groups.

The unique puzzling doubt

concerns the allocation of Rehnquist in the group of Kennedy and O’Connor rather than in the group of Scalia

and Thomas. In order to further investigate this issue, we

decided to check the global likelihood value in the case where we move

Rehnquist in the first group. What we found is that the addition

of him to the group of Scalia and Thomas considerably

decreases the global likelihood. This effect is a consequence of the

fact that our procedure recognizes the perfect dependence among these

last two actors, and therefore it prefers to allocate Scalia

and Thomas alone in one cluster in order to point out their

“positional equality”, and to group into the third cluster O’Connor, Kennedy and Rehnquist, which perfectly agree

over half of the issues. It is also worthwhile to remember that our

procedure is not allowed to give clusters of only one element.

| Our method | Doreian [17] | |||||

|---|---|---|---|---|---|---|

| Cluster 1 | Cluster 2 | Cluster 3 | Cluster 1 | Cluster 2 | Cluster 3 | Cluster 4 |

| Scalia | Breyer | Kennedy | Scalia | Breyer | Kennedy | O’Connor |

| Thomas | Ginsburg | O’Connor | Thomas | Ginsburg | ||

| Souter | Rehnquist | Rehnquist | Souter | |||

| Stevens | Stevens | |||||

This figure depicts the bipartite signed network of the US Supreme Court Justice votes upon different issues. The blue edges correspond to votes in the majority (), the red edges correspond to votes in the minority () and the unique green edge correspond to a case of abstention (). Furthermore, the nodes are classified as follow: yellow for the issues, violet for Cluster 1, orange for Cluster 2 and green for Cluster 3. The network has been built so as to capture the sharpness of the clusters partitioning. In particular, an higher cohesiveness among the judges within the first and second clusters with respect to those ones in the third cluster can be ascertained by the fact that a more coherent coloured pattern can be glimpsed from the beam of edges that originate from the first two clusters with respect to the last one, i.e. two different stacks can be distinguished, a red one and a blue one.

6 Conclusions

Clustering algorithms have increasingly assumed a central role for the

identification of communities in complex networks. In this paper, we

deal with a notion of community different from the classical

one: while the network clustering analysis, namely the

community detection, aims to identify clusters of densely connected

actors, we try to determine groups of actors that play a similar role

inside a certain organization basing on the characteristics or habits

that they exhibit. In the social network literature, this is known as

positional analysis.

To this end, we propose a new

clustering algorithm that can be applied to situations which are

suitably modelled through a weighted bipartite network.

Starting from the associated real-valued matrix, with the actors on

the rows, the features on the columns, and the weights as the

elements, we try to capture possible similarities among groups of

actors by analyzing the multivariate stochastic dependence among

them.

The contribution of this paper has to be found in the

novelty of the methodological approach we propose for positional

analysis that is based on the detection of the intrinsic multivariate

stochastic dependence among groups of actors and in the development of

a related algorithm that uses copula functions in order to model these

dependence structures. Furthermore, this algorithm directly operates

on the matrix describing the actor-feature relationships, differently

from many other algorithms that collapse the information of the

bipartite network to a unipartite one and then apply the classical

clustering procedure. In fact, this kind of operation can cause a lost

of information and a consequent erroneous cluster identification.

Another advantage of our technique is that it finds the optimal

partition, without fixing a priori the number of clusters and/or

the number of elements per cluster (as, on the contrary, for other

clustering algorithms). Furthermore, our algorithm is able to work

directly on any matrix, binary or weighted with real

numbers.

This is the first attempt of application of this

methodology to the network field and so it is not surprising that

there is still a issue to be addressed and that we leave for future

research. Indeed, the major drawback of our algorithm concerns the

high computational burden that it bears, as a consequence of the fact

that it explores all the possible combinations of groups of

actors. Since our first purpose was to understand the potentiality of

such a new approach, we have not tried to develop any optimized

version of our algorithm yet. However, we are convinced that a deeper

computational study of the behaviour of the algorithm will give some

insights on a possible criterion that could be exploited for a

reduction of the exploration procedure. From a first glance, our

suggestion to tackle this issue is to adopt an agglomerative or a

divisive approach as it is commonly used in the community detection

literature, based on some threshold on the log-likelihood function. In

such a case, the log-likelihood function could be computed only for

those groups of actors for which there is an interest with a

consequent reduction of the computational burden.

Acknowledgment

The authors acknowledge

support from CNR PNR Project “CRISIS Lab” and from the MIUR (FIRB

project RBFR12BA3Y). Moreover, Irene Crimaldi is a member of the

“Gruppo Nazionale per l’Analisi Matematica, la Probabilità

e le loro Applicazioni (GNAMPA)” of the “Istituto Nazionale di Alta

Matematica (INdAM)”.

The authors thank Daniel B. Larremore for an

useful remark on the first version of this work.

References

- [1] Aicher C, Jacobs AZ, Clauset A (2014) Learning Latent Block Structure in Weighted Networks. arXiv preprint arxiv:1404.0431v1.

- [2] Asratian AS, Denley T, Häggkvist R (1998) Bipartite Graphs and their Applications. Cambridge University Press.

- [3] Barabási AL, Jeong H, Néda Z, Ravasz E, Schubert A, Vicsek T (2002) Evolution of the social network of scientific collaboration. Physica A 311: 590-614.

- [4] Barber MJ (2007) Modularity and community detection in bipartite networks. Phys Rev E Stat Nonlin Soft Matter Phys 76: 066102.

- [5] Borgatti SP, Everett MG (1997) Network analysis of 2-mode data. Social Networks 19: 243-269.

- [6] Borgatti SP (2008) 2-Mode Concepts in Social Network Analysis. In Meyers RA. Encyclopedia of Complexity and System Science. Springer.

- [7] Borgatti SP, Halgin D (2011) Analyzing Affiliation Network. In Carrington P, Scott J (eds). The Sage Handbook of Social Network Analysis.

- [8] Brandes U, Lerner J (2007) Role equivalent Actors in Networks. In: Obiedkov S, Roth C. ICFCA Satellite Workshop on Social Network Analysis and Conceptual Structures: Exploring Opportunities.

- [9] Brusco M, Steinley D (2006) Inducing a blockmodel structure of two-mode binary data using seriation procedures. Journal of Mathematical Psychology 50: 468-477.

- [10] Brusco M, Steinley D (2007) A variable neighborhood search method for generalized blockmodeling of two-mode binary matrices. Journal of Mathematical Psychology 51: 325-338.

- [11] Brusco M (2011) Analysis of two-mode network data using nonnegative matrix factorization. Social Networks 33: 201-210.

- [12] Cerina F, Chessa A, Pammolli F, Riccaboni M (2014) Network communities within and across borders. Scientific Reports 4: 1-7.

- [13] Good BH, de Montjoye YA, Clauset A (2010) The performance of modularity maximization in practical contexts. Phys Rev E Stat Nonlin Soft Matter Phys 81: 046106.

- [14] Davis GF, Greve HR (1997) Corporate elite networks and governance changes in the 1980. American journal of sociology 103(1): 1-37. 1997.

- [15] Dhillon IS (2001) Co-clustering documents and works using bipartite spectral graph partitioning. Proceedings of the seventh international conference on knowledge discovery and data mining: 269-274.

- [16] Di Lascio FM, Giannerini S (2012) A copula-based Algorithm for Discovering Patterns of Dependent Observations. Journal of Classification 29(1): 50-75.

- [17] Doreian P, Batagelj V, Ferligoj A (2004) Generalized blockmodeling of two-mode network data. Social Networks 26: 29-53.

- [18] Everett MG, Borgatti SP (2013) The dual-projection approach for two-mode networks. Social Networks 35: 204-210.

- [19] Fortunato S (2010) Community detections in graphs. Physics Reports 486: 75-174.

- [20] Girvan M, Newman MEJ (2002) Community structure in social and biological networks. Proc Natl Acad Sci U S A 99(12): 7821-7826.

- [21] Guimerà R, Uzzi B, Spiro J, Amaral LAN (2005) Team assembly mechanisms determine collaboration network structure and team performance. Science 308: 697-702.

- [22] Guimerà R, Sales-Pardo M, Amaral LAN (2007) Module identification in bipartite and directed networks. Phys Rev E Stat Nonlin Soft Matter Phys 76: 036102.

- [23] Hoeffding W (1994) Scale invariant correlation theory. In Fisher NI, Sen PK (eds). The Collected Works of Wassily Hoeffding. Springer Series in Statistics. pp. 57-104.

- [24] Hoppner F, Klawonn F, Kruse R, Runkler (1999) Fuzzy cluster analysis. John Wiley and Sons, Ltd.

- [25] Joe H (1997) Multivariate Models and Dependence Concepts. Chapman and Hall.

- [26] Larremore DB, Clauset A, Buckee CO (2013) A Network Approach to Analyzing Highly Recombinant Malaria Parasite Genes. PLoS Comput Biol 9(10): e1003268. doi:10.1371/journal.pcbi.1003268

- [27] Larremore DB, Clauset A, Jacobs AZ (2014) Efficiently inferring community structure in bipartite networks. arXiv:1403.2933.

- [28] Lohr S (2012) The age of big data. New York Times [Internet]. Available from: http://wolfweb.unr.edu/homepage/ania/NYTFeb12.pdf.

- [29] Mariolis P (1975) Interlocking directorates and control of corporations. Social Science Quarterly 56(3): 425-439.

- [30] Mrvar A, Doreian P (2009) Partitioning Signed Two-Mode Networks. Journal of Mathematical Sociology 33: 196-221.

- [31] Nelsen RB (2006) An introduction to Copulas. Springer Series in Statistics.

- [32] Newman MEJ (2001) Scientific collaboration networks. Network construction and fundamental results. Phys Rev E Stat Nonlin Soft Matter Phys 64: 016131. 2001.

- [33] Sklar A (1959) Fonctions de la repartition a n dimensions et leurs marges. Publications de l’Institute de Statistique de l’Universite de Paris 8: 229-231.

- [34] Trivedi PK, Zimmer DM (2005) Copula modeling: an introduction for practitioners. Foundations and trends in Econometrics 1(1): 1-111.

- [35] Tzekina I, Danthi K, Rockmore DN (2008) Evolution of community structure in the world trade web. European Physics Journal B 63: 541-545.

- [36] Wasserman F, Faust K (1994) Social Network Analysis: Methods and Applications. Cambridge University Press.

- [37] Zhou T, Ren J, Medo M, Zhang Y (2007) Bipartite network projection and personal recommendation. Phys Rev E Stat Nonlin Soft Matter Phys 76: 046115.

- [38] Ziberna A (2007) Generalized blockmodeling of valued networks. Social Networks 29: 105–126.

Appendix

Appendix A Tables

| Issue () | Supreme Court justice () | ||||||||

| Br | Gi | St | So | OC | Ke | Re | Sc | Th | |

| President election | -1 | -1 | -1 | -1 | 1 | 1 | 1 | 1 | 1 |

| Federalism | -1 | -1 | -1 | -1 | 1 | 1 | 1 | 1 | 1 |

| Clean Water | -1 | -1 | -1 | -1 | 1 | 1 | 1 | 1 | 1 |

| Title VI Disabilities | -1 | -1 | -1 | -1 | 1 | 1 | 1 | 1 | 1 |

| Tobacco Ads | -1 | -1 | -1 | -1 | 1 | 1 | 1 | 1 | 1 |

| Labour rights | -1 | -1 | -1 | -1 | 1 | 1 | 1 | 1 | 1 |

| Property Rights | -1 | -1 | -1 | -1 | 1 | 1 | 1 | 1 | 1 |

| Citizenship | -1 | -1 | 1 | -1 | -1 | 1 | 1 | 1 | 1 |

| Free Speech | 1 | -1 | -1 | -1 | 1 | 1 | 1 | 1 | 1 |

| Seat Belts | -1 | -1 | -1 | 1 | -1 | 1 | 1 | 1 | 1 |

| United Foods | -1 | -1 | 1 | 1 | -1 | 1 | 1 | 1 | 1 |

| NYT Copyright | -1 | 1 | -1 | 1 | 1 | 1 | 1 | 1 | 1 |

| Cannabis for Health | 0 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 |

| Clean Air Act | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 |

| PGA vs. Handicapped | 1 | 1 | 1 | 1 | 1 | 1 | 1 | -1 | -1 |

| Illegal Search 3 | 1 | 1 | -1 | 1 | -1 | -1 | -1 | 1 | 1 |

| Illegal Search 1 | 1 | 1 | 1 | 1 | 1 | 1 | -1 | -1 | -1 |

| Illegal Search 2 | 1 | 1 | 1 | 1 | 1 | 1 | -1 | -1 | -1 |

| Stay of Execution | 1 | 1 | 1 | 1 | 1 | 1 | -1 | -1 | -1 |

| Privacy | 1 | 1 | 1 | 1 | 1 | 1 | -1 | -1 | -1 |

| Immigration Jurisdiction | 1 | 1 | 1 | 1 | -1 | 1 | -1 | -1 | -1 |

| Detaining Criminal Aliens | 1 | 1 | 1 | 1 | -1 | 1 | -1 | -1 | -1 |

| Legal Aid for the Poor | 1 | 1 | 1 | 1 | -1 | 1 | -1 | -1 | -1 |

| Voting Rights | 1 | 1 | 1 | 1 | 1 | -1 | -1 | -1 | -1 |

| Deporting Criminal Aliens | 1 | 1 | 1 | 1 | 1 | -1 | -1 | -1 | -1 |

| Campaign Finance | 1 | 1 | 1 | 1 | 1 | -1 | -1 | -1 | -1 |

| The data on the Supreme Court judges can be found in [17]. The blocks of the issues are based on [9]. | |||||||||

| HS2 | Countries | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| France | Germany | U.S.A | Canada | Iran | Kuwait | Saudi Arabia | Qatar | Somalia | Zimbabwe | Liberia | Burundi | |

| 84 | 11.14 | 17.83 | 15.20 | 7.05 | 0.41 | 0.09 | 0.29 | 0.11 | 0.04 | 0.57 | 0.54 | 0.86 |

| 87 | 9.74 | 17.86 | 8.22 | 12.07 | 0.21 | 0.06 | 0.17 | 0.01 | 0.00 | 0.15 | 0.06 | 0.69 |

| 88 | 8.86 | 2.41 | 3.63 | 2.34 | 0.02 | 0.04 | 0.08 | 0.00 | 0.00 | 0.12 | 0.00 | 0.00 |

| 85 | 7.60 | 9.85 | 10.38 | 3.34 | 0.22 | 0.05 | 0.21 | 0.03 | 0.02 | 0.36 | 2.27 | 0.21 |

| 30 | 6.06 | 4.62 | 4.01 | 1.44 | 0.10 | 0.03 | 0.05 | 0.01 | 0.00 | 0.13 | 0.04 | 0.02 |

| 90 | 2.97 | 4.34 | 5.96 | 1.29 | 0.05 | 0.01 | 0.03 | 0.01 | 0.00 | 0.02 | 0.04 | 0.10 |

| 27 | 4.64 | 3.08 | 9.02 | 26.22 | 85.69 | 93.33 | 87.79 | 92.33 | 0.00 | 1.87 | 17.29 | 0.00 |

| 39 | 3.70 | 4.84 | 4.36 | 2.82 | 2.02 | 1.19 | 3.84 | 2.09 | 0.52 | 0.20 | 0.09 | 0.03 |

| 29 | 2.65 | 2.47 | 3.38 | 1.32 | 2.53 | 3.38 | 4.19 | 1.50 | 0.00 | 0.02 | 0.10 | 0.00 |

| 31 | 0.09 | 0.27 | 0.39 | 1.96 | 0.50 | 0.43 | 0.45 | 1.03 | 0.00 | 0.21 | 0.00 | 0.00 |

| 1 | 0.43 | 0.12 | 0.08 | 0.33 | 0.03 | 0.01 | 0.03 | 0.01 | 80.23 | 0.04 | 0.00 | 0.05 |

| 9 | 0.06 | 0.19 | 0.07 | 0.11 | 0.14 | 0.00 | 0.01 | 0.00 | 0.00 | 0.58 | 0.15 | 78.11 |

| 71 | 1.38 | 1.56 | 3.68 | 5.31 | 0.34 | 0.03 | 0.20 | 0.15 | 0.01 | 19.09 | 2.10 | 0.29 |

| 40 | 1.66 | 1.31 | 1.14 | 0.93 | 0.05 | 0.09 | 0.01 | 0.00 | 0.00 | 0.23 | 46.07 | 0.04 |

| 97 | 0.45 | 0.07 | 0.36 | 0.05 | 0.01 | 0.00 | 0.00 | 0.02 | 0.00 | 0.11 | 0.07 | 0.00 |

| 96 | 0.24 | 0.17 | 0.10 | 0.02 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.03 | 0.00 | 0.02 |

| 95 | 0.26 | 0.39 | 0.34 | 0.23 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.03 | 0.00 | 0.00 |

| 93 | 0.07 | 0.06 | 0.22 | 0.05 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.20 | 0.00 |

| 92 | 0.04 | 0.05 | 0.05 | 0.02 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.02 |

| 91 | 0.28 | 0.11 | 0.06 | 0.01 | 0.00 | 0.01 | 0.00 | 0.02 | 0.00 | 0.00 | 0.22 | 0.00 |

| 86 | 0.20 | 0.36 | 0.23 | 0.10 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.02 | 0.01 | 0.00 |

| The table contains the percentage on the total amount of export for some product categories; while we applied the algorithm directly on the export values for all categories. | ||||||||||||

Appendix B Archimedean family of copulas

Here we recall just the principal copula functions belonging to the

Archimedean family that we employ in our simulations and real data

analysis.

The Archimedean family is defined using a

specific function , known as the generator, by means of

the formula

Different functional forms of the generator entail different dependence structures. The principal Archimedean copulas are the following.

-

•

Gumbel copula. The generator is given by and so the Gumbel copula is defined as

The parameter tunes the degree of the dependence. In particular, the value corresponds to independence (indeed, we get ).

-

•

Clayton copula. The generator is given by and so the Clayton copula is defined as

-

•

Frank copula. The generator is given by and so the Frank copula is defined as

Also for these two last copulas, the parameter controls the

degree of the dependence.