Do Bitcoins make the world go round?

On the dynamics of competing crypto-currencies

Abstract

Bitcoins have emerged as a possible competitor to usual currencies, but other crypto-currencies have likewise appeared as competitors to the Bitcoin currency. The expanding market of crypto-currencies now involves capital equivalent to US Dollars, providing academia with an unusual opportunity to study the emergence of value. Here we show that the Bitcoin currency in itself is not special, but may rather be understood as the contemporary dominating crypto-currency that may well be replaced by other currencies. We suggest that perception of value in a social system is generated by a voter-like dynamics, where fashions form and disperse even in the case where information is only exchanged on a pairwise basis between agents.

pacs:

89.65.-s, 05.50.+q, 05.65.+b, 64.60.DeI Introduction

The recent surge in interest and value of Bitcoins is fuelled by lack of confidence in the usual banking system and its lack of transparency. Currencies issued by central banks are not conserved and printing money has been a frequent response to various fiscal problems, abundantly spanning, both, nations and centuries. In recent years, the financial crisis led to bank bailouts and financial rescuing of whole nations, all at the expense of the big central currencies. Even private assets in banks were considered to be devaluated for the purpose of rescuing a national financial system. In this context, the prospects of a peer-to-peer currency without the need for a central bank meets the desire of many people. The crypto-currency Bitcoin, within only 5 years, has reached a market capitalization equivalent to ten billion US Dollars and therefore proves to be a popular new medium.

A major property of Bitcoins is its built-in limitation to a finite number of currency units, called coins. 21,000,000 coins in total can be generated, not more. This is in contrast to common currencies that can be printed in secret by central banks or can be devaluated by excessive issuing of loans. Cryptrographic methods ensure full transparency of the absolute conservation of Bitcoins and are therefore a considerable source of trust into this new medium.

The large volatility of the Bitcoin currency, as well as its low number of daily transactions and low trading volume, support arguments that Bitcoins do not yet share the characteristics of a mature currency. And, furthermore, a major caveat has become clear in recent months: While the number of coins in the new currency is conserved, the overall number of crypto-currencies is not. As the underlying software is open source, cloning a crypto-currency is an easy matter, as is the release of a modified version of a crypto-currency. Today, hundreds of crypto-currencies can be found on the World Wide Web, and an unknown large number may be waiting for acceptance online.

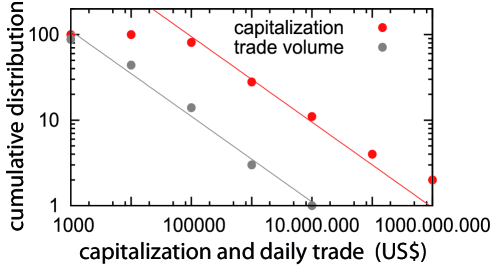

As a result, the constant volume of Bitcoins faces an unlimited number of alternative crypto-currencies and, therefore, an unlimited number of alternative coins. It is an interesting question whether this neutralizes the advantage of the finite inventory in Bitcoins. Clearly, an investor may move his assets from Bitcoins to a competing currency, thereby freely moving in a space with an unlimited number of coins. A quick look at a current crypto-currency exchange shows that so far Bitcoin capitalization dominates.

Fig. 1 shows that the relative strength of the 100 most valued crypto-currencies in fact does not distinguish Bitcoin as special. Rather, both the total market capitalization and the number of trades vary as a power law, with the number of currencies exceeding decrease as . Thus the major advantage of the Bitcoin is its historical position, but it could in principle as well be replaced with any of its competitors.

Here we propose to view the value of any crypto-currency from a popularity standpoint, where coins gain foothold in a market because people communicate about the currencies and thereby act according to the currencies’ popularity. The simplest process that takes such dynamics into account is the Moran process from evolutionary biology Moran58 , often rephrased as the Voter Model in Sociophysics Clifford73 ; Liggett75 ; Liggett97 .

II Model and Results

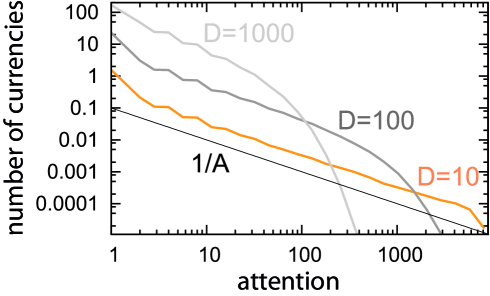

In terms of multiple currencies, a fashion process may be modeled as a number of sites, each representing memory slots in one person’s mind. Naturally, there may be more than one memory slots per person, representing the possibility that this person knows about several crypto-currencies, and also that this person perhaps allocates more memory to Bitcoins than for example to Litecoins. The update of this “fashion model” mimicks communication between two people, allowing one person to swap the state of one memory slot with the state of another memory slot from the other person. When a particular coin is not present in any memory slot of any person, it is considered to be eliminated. To generate a steady state process we here allow invention of a new coin by introducing it into one memory slot. The process is simulated for a system with a number of crypto-currencies , giving a time averaged distribution of popularity , see Fig. 2.

The above copying process is a classical model from sociology, implicitly suggested by Spencer in 1855 by his famous statement of proportionality between importance and how often people hear about a given subject Spencer1855 . From comparing the probability density Fig. 2 with the cumulative plot in Fig. 1 we see qualitative agreement, although the capitalization of real crypto-currencies is decreasing faster with size than the model expectation.

Based on the Moran process above, we now want to model a more complete market where agents also trade currencies and where crypto-currencies are mined at a constant rate. The latter mining aspect will be implemented to mimic the long period of Bitcoins where a constant amount of about 50.000 coins has been mined per week. Our agent based model will remain simplified in the sense that it only considers market fluctuations related to peer to peer exchange, and further by considering only steady state properties.

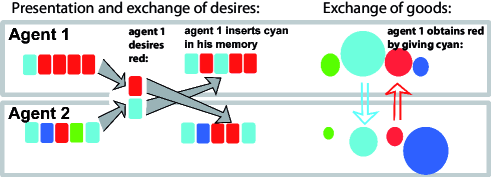

The model describes a market of agents that invest, mine, and trade in different crypto-currencies. The trades will occur between agents on a one-on-one basis, always involving information exchange and occasionally also exchange of coins. Each agent has two types of internal variables. First a repository for assets, implemented as a vector containing the respective assets of currencies . A second vector , contains the preferences of the agent in future acquisitions, with index number containing a memory referring to one of the currencies. Below we also use the derived quantity that counts the number of times currencies appear in the memory list of agent . The model is defined in discrete trade steps:

-

•

Communication: Select two different agents and and one memory slot from each ones’ memory, subsequently referred to as currency and currency . Let agents communicate by replacing a random one of their own interest slots with the selected interest slot from the other agent. If one currency is not any more present in the memory of any agent, it is eliminated from the system and a new currency is introduced in its place with one coin unit and one memory slot of a randomly selected agent.

-

•

Trades: If agent has coin in his inventory list and agent has coin , then the two agents may perform a trade, provided that both believe to gain. Agent evaluates the value of one unit to be , thereby also setting a lower threshold for value of the currency. Similarly, agent evaluates the value of as , whereas agent estimates the value of and respectively to and . A transfer of numbers of coins from and number of coins can take place if with exchange rate . At the exchange, the maximal possible exchange is taking place: If then and . If then and .

-

•

Mining: With a small probability all currencies are mined, and each agent increases its amount of currency at a rate proportional to the fraction that this currency fills the memory of , divided by the total memory of all agents allocated to this currency. Thereby, each currency is mined at a constant rate, whereas individual agents will find it much harder to mine popular currencies.

Notice that trading deals with any fractions of coins, and accordingly the overall behavior, is independent of absolute numbers of coins in the game, including the mining rates in step 3. Also note that there is no feedback from the trade step to the updating dynamics of the memories, leaving the underlying fluctuation in popularity to be very close to the multi-species Moran process simulated in Fig. 2, implying that the overall dynamics of global memory of a particular currency will be close to a Moran process.

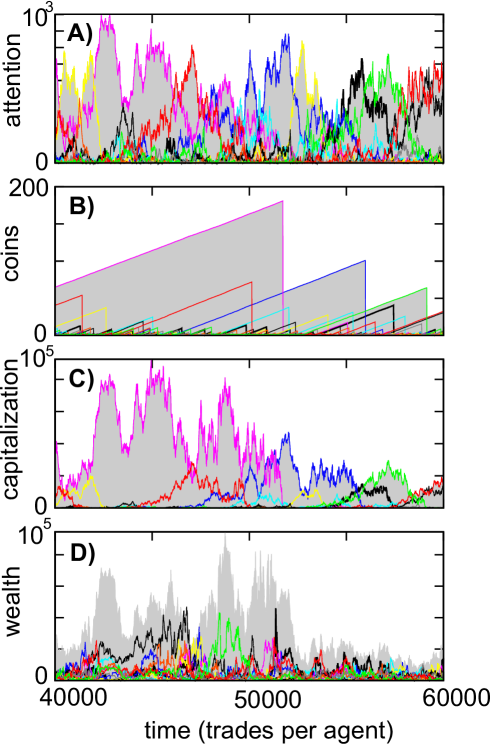

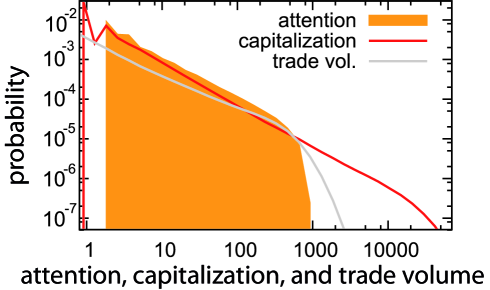

Fig. 5 illustrates the typical behavior of the model, with emphasis on the basic processes: attention, mining, capitalization and trading. All time courses are shown in units of exchange between pairs of agents, each with memory slots, trading different crypto-currencies. In A) we see that dominance is not secured. Due to the ongoing introduction of new currencies the memory allocated to also dominating currencies will be under constant challenge, and ultimately the dominance is predicted to shift. At the same time, some currencies get forgotten, to allow for new currencies with mining allowing their coin count to increase linearly, as seen in panel B). Panel C) shows the total capitalization of currencies, a quantity that for each currency is equal to its total attention multiplied with its total coin count. Panel D) finally shifts the focus to the agents’ trading and mining the currencies, a plot that illustrates that fluctuating currencies indeed open for a market where people may get rich, but as well may get poor. The overall steady state wealth distribution is found to be close to log-normal (not shown), as the individual agents’ fortune is the result of a partly multiplicative process of success and failures.

Fig. 5 shows that the distributions of both attention (memory) and total capitalization remain close to the overall expectation of an iterated Moran process, i.e. . Also the figure shows that trading volumes indeed follow a similar scaling, with large trades being associated to an exchange of popular currencies. Overall, the scale free distributions of real crypto-currencies are recapitulated, with the caveat that our model shows a substantially broader distribution than the observed distributions.

III Discussion

This paper proposes to study the emergent crypto-currencies as a model system of emerging and competing values. Emergence of value and money is an old and classical problem in economic literature, starting with Mengen Menger94 and later modelled through an interplay between need and fashion by Yasutomi95 ; Donangelo02 . In fact the above trading model shares the communication step with Donangelo02 , but does not couple the distribution of goods among agents to their value assessment, a coupling that would expect to be more strategic than a need for diversification. Crypto-currencies provide us with a fresh model system, presenting a real world phenomena of value that has emerged without any need or fundamental value at all. The apparent rise of Bitcoins to the status of a currency which already now can be used to buy real products on the World Wide Web, thus indeed emphasizes that money is a social concept that can self-organize from simple contacts between people.

Our model is at its core simplistic, re-iterating the basic fact that all crypto-currencies are inherently interchangeable and well may be reshuffled by future contingencies. Our model fails to give the same exponent as observed for the power law scaling of real crypto-currencies, and instead predicts systematically broader distributions. Said differently, the contemporary dominance of Bitcoin is in fact less than one would typically expect of a voter- or Moran-like underlying social dynamics.

Possible limitations of our model may be in particular the possibility to obtain more dramatically fluctuating fashion dynamics, caused by an interplay between global information spreading, marketing, or including propagation of potentially catastrophic news. Thus other types of preferential growth of attention may be considered, for example the rich-gets-richer dynamics by Simon Simon55 with an overall prediction of a wealth distribution with scaling exponent steeper than -2, which would be systematically steeper than the observed distribution. Also we here have abstained from modeling the transient aspect of real crypto-currencies. This allowed us to model a distribution that does depend on the functional form of the abundance of new currencies. An introduction that indeed should be expected to give an abundance of yet small currencies, and reduce the relative abundance of bigger currencies. Finally, the social network aspect of emergent crypto-currencies may contribute to the exponent, as information and trust about small currencies may be localized in certain regions of the human social network Rosvall09 , which is potentially quantifiable by following transactions of crypto-currencies, as well as information flows about the currencies Kristoufek2013 ; Kondor2014 .

Overall, our consideration serves to emphasize the crypto-currency as a good model-system for the study of human folly, including the history-dependent randomness in assigning what is valuable and what has no value. A consideration that should be at the heart of multiple aspects of social activity, social hierarchies, and thereby also be part of maintaining overall social order.

References

- (1) P.A.P. Moran, Random processes in genetics. Proceedings of the Cambridge Philosophical Society 54 (1958) 60-71.

- (2) P. Clifford and A. Sudbury, A model for spatial conflict. Biometrika 60 (1973) 581–588.

- (3) R.A. Holley and T.M. Liggett, Ergodic Theorems for Weakly Interacting Infinite Systems and the Voter Model, The Annals of Probability 3 (1975) 643-663.

- (4) T.M. Liggett, Stochastic models of interacting systems, The Annals of Probability 25 (1997) 1-29.

- (5) H. Spencer, The principles of psychology (Longmans, London, 1855).

- (6) C. Menger, Principles of Economics (Libertarian Press, Grove City, 1994).

- (7) A. Yasutomi, The emergence and collapse of money. Physica D 82 (1995) 180-194.

- (8) R. Donangelo and K. Sneppen, Self-organization of value and demand. Physica A 276 (2000) 572-580; R. Donangelo and K. Sneppen, Cooperativity in a trading model with memory and production. Physica A 316 (2002) 581-591.

- (9) H. Simon, On a Class of Skew Distribution Functions. Biometrika 42 (1955) 425-440.

- (10) M. Rosvall and K. Sneppen, Reinforced communication and social navigation generate groups in model networks. Phys. Rev. E 79 (2009) 026111.

- (11) L. Kristoufek, BitCoin meets Google Trends and Wikipedia: Quantifying the relationship between phenomena of the Internet era. Sci. Rep. 3 (2013) 3415.

- (12) D. Kondor, M. Posfai, I. Csabai, G. Vattay, Do the Rich Get Richer? An Empirical Analysis of the Bitcoin Transaction Network. PLoS ONE 9(2): e86197 (2014); doi:10.1371/journal.pone.0086197.