A Proximal Stochastic Gradient Method with Progressive Variance Reduction

Lin Xiao

Machine Learning Group, Microsoft Research, Redmond, WA 98052.

Email: lin.xiao@microsoft.com. Tong Zhang

Department of Statistics, Rutgers University, Piscataway, NJ 08854;

and Baidu Inc., Beijing 100085.

Email: tzhang@stat.rutgers.edu.

(March 18, 2014)

Abstract

We consider the problem of minimizing the sum of two convex functions:

one is the average of a large number of smooth component functions, and

the other is a general convex function that admits a simple proximal mapping.

We assume the whole objective function is strongly convex.

Such problems often arise in machine learning, known as regularized empirical

risk minimization. We propose and analyze a new proximal stochastic gradient

method, which uses a multi-stage scheme to progressively reduce the variance

of the stochastic gradient.

While each iteration of this algorithm has similar cost as the classical

stochastic gradient method (or incremental gradient method),

we show that the expected objective value converges to the optimum

at a geometric rate.

The overall complexity of this method is much lower than both the

proximal full gradient method and the standard

proximal stochastic gradient method.

1 Introduction

We consider the problem of minimizing the sum of two convex functions:

(1)

where is the average of many smooth component functions , i.e.,

(2)

and is relative simple but can be non-differentiable.

We are especially interested in the case where the number of components

is very large, and it can be advantageous to use incremental methods

(such as stochastic gradient method)

that operate on a single component at each iteration, rather than

on the entire cost function.

Problems of this form often arise in machine learning and statistics,

known as regularized empirical risk minimization;

see, e.g., [HTF09].

In such problems, we are given a collection of training examples

, where each is a

feature vector and is the desired response.

For least-squares regression, the component loss functions are

,

and popular choices of the regularization term include

(the Lasso),

(ridge regression), or

(elastic net),

where and are nonnegative regularization parameters.

For binary classification problems, each is the desired

class label, and a popular loss function is the logistic loss

,

which can be combined with any of the regularization terms mentioned above.

The function can also be used to model convex constraints.

Given a closed convex set , the constrained problem

can be formulated as (1) by setting to be

the indicator function of , i.e., if and

otherwise.

Mixtures of the “soft” regularizations (such as or

penalties) and “hard” constraints are also possible.

The results presented in this paper are based on the following

assumptions.

Assumption 1.

The function is lower semi-continuous and convex,

and its effective domain, ,

is closed.

Each , for , is differentiable

on an open set that contains , and their gradients are

Lipschitz continuous.

That is, there exist such that for all ,

(3)

Assumption 1 implies that the gradient

of the average function is also Lipschitz continuous, i.e.,

there is an such that for all ,

Moreover, we have .

Assumption 2.

The overall cost function is strongly convex, i.e.,

there exist such that for all and ,

(4)

The convexity parameter of a function is the largest

such that the above condition holds.

The strong convexity of may come from either or or both.

More precisely, let and have convexity parameters

and respectively, then .

We note that it is possible to have

although we must have .

1.1 Proximal gradient and stochastic gradient methods

A standard method for solving problem (1) is

the proximal gradient method.

Given an initial point , the proximal gradient method uses

the following update rule for

where is the step size at the -th iteration.

Throughout this paper, we use to denote the usual Euclidean norm,

i.e., , unless otherwise specified.

With the definition of proximal mapping

the proximal gradient method can be written more compactly as

(5)

This method can be viewed as a special case of splitting algorithms

[LM79, CR97, Tse00], and its accelerated variants have been proposed

and analyzed in [BT09, Nes13].

When the number of components is very large, each iteration

of (5) can be very expensive

since it requires computing the gradients for all the

component functions , and also their average.

For this reason, we refer to (5)

as the proximal full gradient (Prox-FG) method.

An effective alternative is the proximal stochastic gradient

(Prox-SG) method:

at each iteration , we draw randomly from

and take the update

(6)

Clearly we have .

The advantage of the Prox-SG method is that at each iteration,

it only evaluates gradient of a single component function,

thus the computational cost per iteration is only that of

the Prox-FG method.

However, due to the variance introduced by random sampling,

the Prox-SG method converges much more slowly than the Prox-FG method.

To have a fair comparison of their overall computational cost,

we need to combine their cost per iteration and iteration complexity.

Let .

Under the Assumptions 1 and 2,

the Prox-FG method with a constant step size generates

iterates that satisfy

(7)

(See Appendix B for a proof of this result.)

The most interesting case for large-scale applications is when ,

and the ratio is often called the condition number of the

problem (1).

In this case, the Prox-FG method needs

iterations to ensure

.

Thus the overall complexity of Prox-FG,

in terms of the total number of component gradients evaluated to find an

-accurate solution, is .

The accelerated Prox-FG methods in [BT09, Nes13]

reduce the complexity to .

On the other hand, with a diminishing step size ,

the Prox-SG method converges at a sublinear rate

([DS09, LLZ09]):

(8)

Consequently, the total number of component gradient evaluations required by

the Prox-SG method to find an -accurate solution (in expectation)

is .

This complexity scales poorly in compared with

, but it is independent of .

Therefore, when is very large, the Prox-SG method can be more efficient,

especially to obtain low-precision solutions.

There is also a vast literature on incremental gradient methods for

minimizing the sum of a large number of component functions.

The Prox-SG method can be viewed as a variant of the randomized

incremental proximal algorithms proposed in [Ber11].

Asymptotic convergence of such methods typically requires diminishing

step sizes and only have sublinear convergence rates.

A comprehensive survey on this topic can be found in [Ber10].

1.2 Recent progresses and our contributions

Both the Prox-FG and Prox-SG methods do not fully exploit the problem structure

defined by (1) and (2).

In particular, Prox-FG ignores the fact that the smooth part

is the average of component functions. On the other hand,

Prox-SG can be applied for more general stochastic optimization problems,

and it does not exploit the fact that the objective function

in (1) is actually a deterministic function.

Such inefficiencies in exploiting problem structure

leave much room for further improvements.

Several recent work considered various special cases

of (1) and (2),

and developed algorithms that enjoy the complexity

(total number of component gradient evaluations)

(9)

where .

If is not significantly larger than , this complexity

is far superior than that of both the Prox-FG and Prox-SG methods.

In particular, Shalev-Shwartz and Zhang

[SSZ13, SSZ12]

considered the case where the component functions have the form

and the Fenchel conjugate functions

of and can be computed efficiently.

With the additional assumption that itself is -strongly convex,

they showed that a proximal stochastic dual coordinate ascent (Prox-SDCA)

method achieves the complexity in (9).

Le Roux et al. [RSB12] considered the case where

,

and proposed a stochastic average gradient (SAG) method which

has complexity .

Apparently this is on the same order as (9).

The SAG method is a randomized variant of the

incremental aggregated gradient method of

Blatt et al. [BHG07], and needs to store

the most recent gradient for each component function , which is .

While this storage requirement can be prohibitive for large-scale problems,

it can be reduced to for problems with more favorable structure,

such as linear prediction problems in machine learning.

More recently, Johnson and Zhang [JZ13] developed

another algorithm for the case , called

stochastic variance-reduced gradient (SVRG).

The SVRG method employs a multi-stage scheme to progressively reduce the

variance of the stochastic gradient, and achieves the same low complexity

in (9).

Moreover, it avoids storage of past gradients for the component functions,

and its convergence analysis is considerably simpler than that of SAG.

A very similar algorithm was proposed

by Zhang et al. [ZMJ13], but with a

worse convergence rate analysis.

Another recent effort to extend the SVRG method is

[KR13].

In this paper, we extend the variance reduction technique of SVRG to

develop a proximal SVRG (Prox-SVRG) method for solving the more general

class of problems defined in (1) and (2).

We show that with uniform sampling of the component functions,

the Prox-SVRG method achieves the same complexity in (9).

Moreover, our method incorporates a weighted sampling strategy.

When the sampling probabilities for are proportional to their Lipschitz

constants , the Prox-SVRG method has complexity

(10)

where .

This bound improves upon the one in (9),

especially for applications where the component functions vary

substantially in smoothness.

2 The Prox-SVRG method

Recall that in the Prox-SG method (6),

with uniform sampling of , we have unbiased estimate

of the full gradient at each iteration.

In order to ensure asymptotic convergence,

the step size has to decay to zero to mitigate the effect of variance

introduced by random sampling, which leads to slow convergence.

However, if we can gradually reduce the variance in estimating the full

gradient, then it is possible to use much larger (even constant)

step sizes and obtain much faster convergence rate.

Several recent work

(e.g., [FS12, BCNW12, FG13])

have explored this idea by using mini-batches with exponentially growing sizes,

but their overall computational cost

is still on the same order as full gradient methods.

Instead of increasing the batch size gradually,

we use the variance reduction technique of SVRG [JZ13],

which computes the full batch periodically.

More specifically, we maintain an estimate of the optimal

point , which is updated periodically,

say after every Prox-SG iterations.

Whenever is updated, we also computes the full gradient

and use it to modify the next stochastic gradient directions.

Suppose the next iterations are initialized with

and indexed by .

For each , we first randomly pick and compute

then we replace in the Prox-SG

method (6) with , i.e.,

(11)

Conditioned on , we can take expectation with respect to and

obtain

Hence, just like , the modified direction

is also a stochastic gradient of at .

However, the variance can be much smaller

than .

In fact we will show in Section 3.1

that the following inequality holds:

(12)

Therefore, when both and converge to ,

the variance of also converges to zero.

As a result, we can use a constant step size and obtain much faster convergence.

Algorithm: Prox-SVRGiterate: for probability on iterate: for pick randomly according to endset end

Figure 1: The Prox-SVRG method.

Figure 1 gives the full description of the

Prox-SVRG method with a constant step size .

It allows random sampling from a general distribution ,

thus is more flexible than the uniform sampling scheme described above.

It is not hard to verify that the modified stochastic gradient,

(13)

still satisfies .

In addition, its variance can be bounded similarly as in (12)

(see Corollary 3 in Section 3.1).

The Prox-SVRG method uses a multi-stage scheme to progressively reduce

the variance of the modified stochastic gradient

as both and converges to .

Each stage requires component gradient evaluations:

for the full gradient at the beginning of each stage, and two for

each of the proximal stochastic gradient steps.

For some problems such as linear prediction in machine learning,

the cost per stage can be further reduced to only

gradient evaluations.

In practical implementations, we can also set to be the last

iterate , instead of , of the previous stage.

This simplifies the computation and we did not observe much difference in

the convergence speed.

3 Convergence analysis

Theorem 1.

Suppose Assumptions 1 and 2

hold, and let and .

In addition, assume that

and is sufficiently large so that

(14)

Then the Prox-SVRG method in Figure 1

has geometric convergence in expectation:

We have the following remarks regarding the above result:

•

The ratio can be viewed as a “weighted” condition number of .

Theorem 1 implies that setting to be on the same

order as is sufficient to have geometric convergence.

To see this, let with .

When , we have

As a result, choosing and results in

.

•

In order to satisfy ,

the number of stages needs to satisfy

Since each stage requires component gradient evaluations,

and it is sufficient to set ,

the overall complexity is

•

For uniform sampling, for all , so we have

and the above complexity bound

becomes (9).

The smallest possible value for is ,

achieved at , i.e., when the sampling probabilities

for the component functions are proportional to their Lipschitz constants.

In this case, the above complexity bound becomes (10).

Since , Markov’s

inequality and Theorem 1 imply

that for any ,

Thus we have the following high-probability bound.

Corollary 1.

Suppose the assumptions in Theorem 1 hold.

Then for any and , we have

provided that the number of stages satisfies

If is convex but not strongly convex, then for any , we can define

It follows that is -strongly convex.

We can apply the Prox-SVRG method in Figure 1

to , which replaces the update formula for by the following update rule:

Suppose Assumption 1 holds and let .

In addition, assume that and is sufficiently large so that

Then the Prox-SVRG method in Figure 1, applied to , achieves

If has a minimum and it is achieved by some , then

Corollary 2 implies

This result means that if we take

and , then

The overall complexity

(in terms of the number of component gradient evaluations) is

Similar results for the case of

have been obtained in

[RSB12, MZJ13, KR13].

We can also derive a high-probability bound based on

Corollary 1, but omit the details here.

3.1 Bounding the variance

Our bound on the variance of the modified stochastic gradient

is a corollary of the following lemma.

Lemma 1.

Consider as defined in (1)

and (2).

Suppose Assumption 1 holds,

and let and .

Then

Proof.

Given any , consider the function

It is straightforward to check that ,

hence .

Since is Lipschitz continuous with constant , we have

(see, e.g., [Nes04, Theorem 2.1.5])

This implies

By dividing the above inequality by ,

and summing over , we obtain

By the optimality of , i.e.,

there exist such that

.

Therefore

where in the last inequality, we used convexity of .

This proves the desired result.

∎

Corollary 3.

Consider defined in (13).

Conditioned on , we have and

Proof.

Conditioned on , we take expectation with respect to to obtain

Similarly we have

,

and therefore

To bound the variance, we have

In the second equality above, we used the fact that for any random

vector , it holds that

.

In the second inequality, we used .

In the last inequality, we applied Lemma 1 twice.

∎

For convenience, we define the stochastic gradient mapping

so that the proximal gradient step (11) can be

written as

(15)

We need the following lemmas in the convergence analysis.

The first one is on the non-expansiveness of proximal mapping,

which is well known (see, e.g., [Roc70, Section 31]).

Lemma 2.

Let be a closed convex function on and .

Then

The next lemma provides a lower bound of the function using

stochastic gradient mapping.

It is a slight generalization of [HKP09, Lemma 3], and we give

the proof in Appendix A for completeness.

Lemma 3.

Let , where is Lipschitz continuous with

parameter , and and has strong convexity parameters

and respectively.

For any and arbitrary , define

where is a step size satisfying .

Then we have for any ,

Now we proceed to prove Theorem 1.

We start by analyzing how the distance between and changes

in each iteration.

Using the update rule (15), we have

where .

Note that the assumption in Theorem 1 implies

because .

Therefore,

(16)

Next we upper bound the quantity .

Although not used in the Prox-SVRG algorithm,

we can still define the proximal full gradient update as

which is independent of the random variable .

Then,

where in the first inequality we used the Cauchy-Schwarz inequality,

and in the second inequality we used Lemma 2.

Combining with (16), we get

Now we take expectation on both sides of the above inequality with respect

to to obtain

We note that both and are independent of the

random variable and , so

In addition, we can bound the term using

Corollary 3 to obtain

We consider a fixed stage , so that

and .

By summing the previous inequality over and taking expectation

with respect to the history of random variables , we obtain

Notice that and , so we have

By convexity of and definition of , we have

.

Moreover, strong convexity of implies

.

Therefore, we have

Divide both sides of the above inequality by ,

we arrive at

Finally using the definition of in (14),

and applying the above inequality recursively, we obtain

which is the desired result.

4 Numerical experiments

In this section we present results of several numerical experiments to

illustrate the properties of the Prox-SVRG method,

and compare its performance with several related algorithms.

We focus on the regularized logistic regression problem for

binary classification: given a set of training examples

where and ,

we find the optimal predictor by solving

where and are two regularization parameters.

The regularization is added to promote sparse solutions.

In terms of the model (1) and (2),

we can have either

(17)

or

(18)

depending on the algorithm used.

We used three publicly available data sets.

Their sizes , dimensions as well as sources as listed in

Table 1.

For rcv1 and covertype, we used the processed data

for binary classification from [FL11].

The table also listed the values of and

that were used in our experiments.

These choices are typical in machine learning benchmarks to obtain

good classification performance.

Table 1: Summary of data sets

and regularization parameters used in our experiments.

4.1 Properties of Prox-SVRG

We first illustrate the numerical characteristics of Prox-SVRG on

the rcv1 dataset.

Each example in this dataset has been normalized so that for

all , which leads to the same upper bound on the Lipschitz

constants .

In our implementation, we used the splitting in (17)

and uniform sampling of the component functions.

We choose the number of stochastic gradient steps between full

gradient evaluations as a small multiple of .

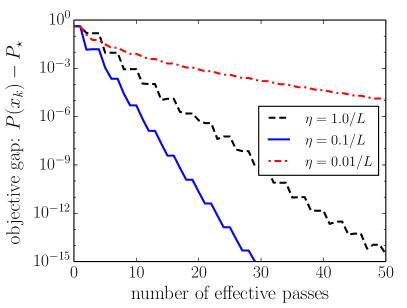

Figure 2 shows the behavior of Prox-SVRG with

when we used three different step sizes.

The horizontal axis is the number of effective passes over the data, where

each effective pass evaluates component gradients.

Each full gradient evaluation counts as one effective pass, and appears as

a small flat segment of length 1 on the curves.

It can be seen that the convergence of Prox-SVRG

becomes slow if the step size is either too big or too small.

The best choice of matches our theoretical analysis

(see the first remark after Theorem 1).

The number of non-zeros (NNZs) in the iterates converges

quickly to after about passes over the data.

Figure 2: Prox-SVRG on the rcv1 dataset: varying the step size with .

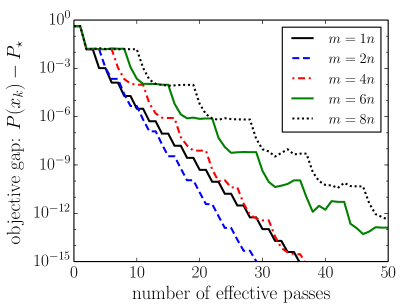

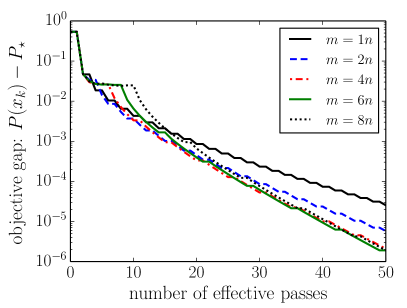

Figure 3: Prox-SVRG on the rcv1 dataset with step size

: varying the period between full gradient evaluations,

with on the left and on the right.

Figure 3 shows how the objective gap

decreases when we vary the period of evaluating

full gradients.

For , the fastest convergence per stage is achieved

by , but the frequent evaluation of full gradients makes its overall

performance slightly worse than .

Longer periods leads to slower convergence,

due to the lack of effective variance reduction.

For , the condition number is much larger, thus longer

period is required to have sufficient reduction during each stage.

4.2 Comparison with related algorithms

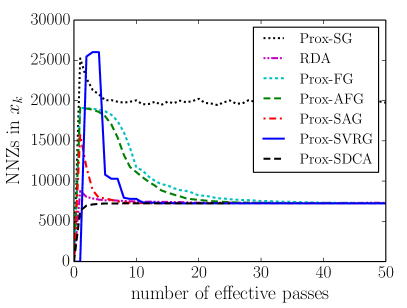

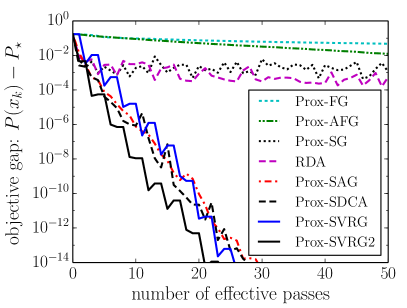

Figure 4: Comparison of different methods on the rcv1 dataset.

We implemented the following algorithms to compare with Prox-SVRG:

•

Prox-SG: the proximal stochastic gradient method given

in (6).

We used a constant step size that gave the best performance among

all powers of .

•

RDA: the regularized dual averaging method in [Xia10].

The step size parameter in RDA is also chosen as the one

that gave best performance among all powers of .

•

Prox-FG: the proximal full gradient method given

in (5), with an adaptive line search scheme

proposed in [Nes13].

•

Prox-AFG: an accelerated version of the Prox-FG method that is

very similar to FISTA [BT09], also with an

adaptive line search scheme.

•

Prox-SAG: a proximal version of the stochastic average gradient (SAG)

method [SRB13, Section 6].

We note that the convergence of this Prox-SAG method has not

been established for the general model considered in this paper.

Nevertheless it demonstrates good performance in practice.

•

Prox-SDCA: the proximal stochastic dual coordinate ascent method

[SSZ12].

In order to obtain the complexity

, it needs to use the

splitting (18).

Figure 4 shows the comparison of Prox-SVRG

( and ) with different methods described above

on the rcv1 dataset.

For the Prox-SAG method, we used the same step size

as for Prox-SVRG.

We can see that the three methods that performed best are

Prox-SAG, Prox-SVRG and Prox-SDCA.

The superior performance of Prox-SVRG and Prox-SDCA are predicted by their

low complexity analysis.

While the complexity of Prox-SAG has not been formally established,

its performance is among the best.

In terms of obtaining sparse iterates under the -regularization,

RDA, Prox-SDCA and Prox-SAG converged to the correct NNZs quickly,

followed by Prox-SVRG and the two full gradient methods.

The Prox-SG method didn’t converge to the correct NNZs.

Figure 5 shows the comparison of different methods

on two other data sets listed in Table 1.

Here we also included comparison with Prox-SVRG2,

which is a hybrid method by performing Prox-SG for one pass over the data

and then switch to Prox-SVRG.

This hybrid scheme was suggested in [JZ13],

and it often improves the performance of Prox-SVRG substantially.

Similar hybrid schemes also exist for SDCA [SSZ12]

and SAG [SRB13].

The behaviors of the stochastic gradient type of algorithms on

covertype (Figure 5, left)

are similar to those on rcv1, but

the two full gradient methods Prox-FG and Prox-AFG perform worse

because of the smaller regularization parameter and hence

worse condition number.

The sido0 data set turns out to be more difficult to optimize,

and much slower convergence are observed in Figure 5 (right).

The Prox-SAG method performs best on this data set, followed by

Prox-SVRG2 and Prox-SVRG.

Figure 5: Comparison of different methods on covertype (left)

and sido0 (right).

5 Conclusions

We developed a new proximal stochastic gradient method, called Prox-SVRG,

for minimizing the sum of two convex functions: one is the average of a large

number of smooth component functions, and the other is a general convex

function that admits a simple proximal mapping.

This method exploits the finite average structure of the smooth part by

extending the variance reduction technique of SVRG [JZ13],

which computes the full gradient periodically to modify the stochastic

gradients in order to reduce their variance.

The Prox-SVRG method enjoys the same low complexity as that of

SDCA [SSZ13, SSZ12] and

SAG [RSB12, SRB13],

but applies to a more general class of problems,

and does not require the storage of

the most recent gradient for each component function.

In addition, our method incorporates a weighted sampling scheme,

which achieves an improved complexity result for problems where

the component functions vary substantially in smoothness.

Dropping the nonnegative term on the

left-hand side results in

which leads to

Dropping the nonnegative term on the left-hand

side of (19) yields

Setting , the above inequality is equivalent to (7).

References

[BCNW12]

R. H. Byrd, G. M. Chin, J. Nocedal, and Y. Wu.

Sample size selection in optimization methods for machine learning.

Mathematical Programming, Ser. B, 134:127–155, 2012.

[BDA13]

J. A. Blackard, D. J. Dean, and C. W. Anderson.

Covertype data set.

In K. Bache and M. Lichman, editors, UCI Machine Learning

Repository, URL: http://archive.ics.uci.edu/ml, 2013. University of

California, Irvine, School of Information and Computer Sciences.

[Ber10]

D. P. Bertsekas.

Incremental gradient, subgradient, and proximal methods for convex

optimization: a survey.

Report LIDS-P-2848, Laboratory for Information and Decision Systems,

MIT, Cambridge, MA, 2010.

[Ber11]

D. P. Bertsekas.

Incremental proximal methods for large scale convex optimization.

Mathematical Programming, Ser. B, 129:163–195, 2011.

[BHG07]

D. Blatt, A. O. Hero, and H. Gauchman.

A convergent incremental gradient method with a constant step size.

SIAM Journal on Optimization, 18(1):29–51, 2007.

[BT09]

A. Beck and M. Teboulle.

A fast iterative shrinkage-threshold algorithm for linear inverse

problems.

SIAM Journal on Imaging Sciences, 2(1):183–202, 2009.

[CR97]

G. H.-G. Chen and R. T. Rockafellar.

Convergence rates in forward-backward splitting.

SIAM Journal on Optimization, 7(2):421–444, 1997.

[DS09]

J. Duchi and Y. Singer.

Efficient online and batch learning using forward backward splitting.

Journal of Machine Learning Research, 10:2873–2898, 2009.

[FG13]

M. P. Friedlander and G. Goh.

Tail bounds for stochastic approximation.

arXiv:1304.5586, April 2013.

[FL11]

R.-E. Fan and C.-J. Lin.

LIBSVM data: Classification, regression and multi-label.

URL: http://www.csie.ntu.edu.tw/~cjlin/libsvmtools/datasets, 2011.

[FS12]

M. P. Friedlander and M. Schmidt.

Hybrid deterministic-stochastic methods for data fitting.

SIAM Journal on Scientific Computing, 34(3):1380 1405, 2012.

[Guy08]

I. Guyon.

Sido: A phamacology dataset.

URL: http://www.causality.inf.ethz.ch/data/SIDO.html, 2008.

[HKP09]

C. Hu, J. T. Kwok, and W. Pan.

Accelerated gradient methods for stochastic optimization and online

learning.

In Advances in Neural Information Processing Systems 22, pages

781–789. 2009.

[HTF09]

T. Hastie, R. Tibshirani, and J. Friedman.

The Elements of Statistical Learning: Data Mining, Inference,

and Prediction.

Springer, New York, 2nd edition, 2009.

[JZ13]

R. Johnson and T. Zhang.

Accelerating stochastic gradient descent using predictive variance

reduction.

In Advances in Neural Information Processing Systems 26, pages

315–323. 2013.

[KR13]

J. Konečný and P. Richtárik.

Semi-stochastic gradient descent methods.

arXiv:1312.1666, 2013.

[LLZ09]

J. Langford, L. Li, and T. Zhang.

Sparse online learning via truncated gradient.

Journal of Machine Learning Research, 10:777–801, 2009.

[LM79]

P.-L. Lions and B. Mercier.

Splitting algorithms for the sum of two nonlinear operators.

SIAM Journal on Numerical Analysis, 16:964–979, 1979.

[LYRL04]

D. D. Lewis, Y. Yang, T. Rose, and F. Li.

RCV1: A new benchmark collection for text categorization research.

Journal of Machine Learning Research, 5:361–397, 2004.

[MZJ13]

M. Mahdavi, L. Zhang, and R. Jin.

Mixed optimization for smooth functions.

In Advances in Neural Information Processing Systems 26, pages

674–682. 2013.

[Nes04]

Yu. Nesterov.

Introductory Lectures on Convex Optimization: A Basic Course.

Kluwer, Boston, 2004.

[Roc70]

R. T. Rockafellar.

Convex Analysis.

Princeton University Press, 1970.

[RSB12]

N. Le Roux, M. Schmidt, and F. Bach.

A stochastic gradient method with an exponential convergence rate for

finite training sets.

In Advances in Neural Information Processing Systems 25, pages

2672–2680. 2012.

[SRB13]

M. Schmidt, N. Le Roux, and F. Bach.

Minimizing finite sums with the stochastic average gradient.

Technical Report HAL 00860051, INRIA, Paris, France, 2013.

[SSZ12]

S. Shalev-Shwartz and T. Zhang.

Proximal stochatic dual coordinate ascent.

arXiv:1211.2772, November 2012.

[SSZ13]

S. Shalev-Shwartz and T. Zhang.

Stochastic dual coordinate ascent methods for regularized loss

minimization.

Journal of Machine Learning Research, 14:567–599, 2013.

[Tse00]

P. Tseng.

A modified forward-backward splitting method for maximal monotone

mappings.

SIAM Journal on Control and Optimization, 38(2):431–446, 2000.

[Xia10]

L. Xiao.

Dual averaging methods for regularized stochastic learning and online

optimization.

Journal of Machine Learning Research, 11:2534–2596, 2010.

[ZMJ13]

L. Zhang, M. Mahdavi, and R. Jin.

Linear convergence with condition number independent access of full

gradients.

In Advances in Neural Information Processing Systems 26, pages

980–988. 2013.