On singular value distribution of large-dimensional autocovariance matrices

Abstract

Let be a sequence of independent dimensional random vectors and a given integer. From a sample of the sequence, the so-called lag auto-covariance matrix is . When the dimension is large compared to the sample size , this paper establishes the limit of the singular value distribution of assuming that and grow to infinity proportionally and the sequence satisfies a Lindeberg condition. Compared to existing asymptotic results on sample covariance matrices developed in random matrix theory, the case of an auto-covariance matrix is much more involved due to the fact that the summands are dependent and the matrix is not symmetric. Several new techniques are introduced for the derivation of the main theorem.

keywords:

[class=MSC]keywords:

, and t1Corresponding author.

1 Introduction

Let be a sample from a stationary process with values in . The matrix

| (1.1) |

is the so-called lag sample auto-covariance matrix of the process (here denotes the transpose of a vector or matrix ). In a classical low-dimensional situation where the dimension is assumed much smaller than the sample size , is very close to so that its asymptotic behavior when (so is considered as fixed) is well known. In the high-dimensional context where typically the dimension is of same order as , will not converge to and its asymptotic properties have not been well investigated. In this paper, we study the empirical spectral distribution (ESD) of , namely, the distribution generated by its singular values. The main result of the paper is the establishment of the limit of this ESD when is an independent sequence with elements having a finite fourth moments while and grow to infinity proportionally.

In order to understand the importance of limiting spectral distribution (LSD) of singular values of the auto-covariance matrix , we describe a statistical problem where these distributions are of central interest. In a recent stimulating paper, Lam and Yao [6] considers the following dynamic factor model

| (1.2) |

where is an observed -dimensional sequence, a sequence of -dimensional “latent factor” () uncorrelated with the error process and is the general mean. A particularly important question here is the determination of the number of factors. For any stationary process , let be its (population) lag- auto-covariance matrix, we have

It turns out that has exactly non-null singular values so that based on a sample it seems natural to infer from the singular values of the sample lag-1 auto-covariance matrix

Because has rank , the first three terms all have rank bounded by and appears as a finite-rank perturbation of the lag-1 auto-covariance matrix which in general has rank . Therefore, understanding the properties of the singular values of will be of primary importance for the understanding of the largest singular values of the matrix of which are, as said above, fundamental for the determination of the number of factors . Notice however that this statistical problem is given here to describe a potential application of the theory established in this paper, but this theory on singular value distribution is general and can be applied to fields other than statistics.

If we take in (1.1), the matrix is the sample covariance matrix from the observations. The theory for eigenvalue distributions of has been extensively studied in the random matrix literature dating back to the seminal paper [7]. In this paper, the famous Marenko-Pastur law as limit of eigenvalue distributions has been found for a wide class of sample covariance matrices. Further development includes the almost sure convergence of these distributions ([9]) and conditions for convergence of the largest and the smallest eigenvalues, see [4]. Meanwhile book-length analysis of sample covariance matrices can be found in [3], [1], [8]. The situation of an auto-covariance matrix is completely different. To author’s best knowledge, none of the existing literature in random matrix theory treats the sample auto-covariance matrix and the limit for its eigenvalue distribution found in this paper is new.

There are basically two major differences between and . First, while is a non-negative symmetric random matrix, is even not symmetric and we must rely on singular value distributions which are in general much more involved than eigenvalue distributions. Secondly, because of the positive lag , the summands in are no more independent as it is the case for the sample covariance matrix . This again makes the analysis of more difficult. As a consequence of these major differences, several new techniques are introduced in the paper in order to complete the proofs, although the general strategy is common in the random matrix theory (see Bai and Silverstein [3], Pastur and Shcherbina [8]). For example, the characterization of the Stieltjes transform of the limiting distribution is obtained via a system of equations due to the time delay where for the case of sample covariance matrix, the characterization is given by a single equation([7], [9]).

The rest of the paper is organized as follows. The main theorem of the paper is introduced in Section 2. Section 3 details the proof of the main theorem when time lag . Section 4 generalizes the proof from time lag to any given positive number. Meanwhile, in contrast to other aspects discussed above, the preliminary steps of truncation, centralization and standardization of the matrix entries are similar to the case of a sample covariance matrix. They are given in Appendix A. To ease the reading of the proof, technical lemmas are grouped in Section 5.

2 Main Results

In this paper, we intend to derive the limiting singular value distribution of the lag auto-covariance matrix defined in (1.1). It will be done in two steps. We derive the main result first for the lag-1 sample auto-covariance matrix . It turns out that the general case is essentially the same and the extension is easily obtained. The details of the extension are given in Section 4.

Therefore, we consider the lag-1 sample auto-covariance matrix . By definition, it is equivalent to study the limiting spectral distribution(LSD) of the matrix

Alternatively,

where , . Here we define a modified version of the A matrix,

where is the j-th row of , and the j-th row of . As and have same nonzero eigenvalues, the LSD of can be derived from the LSD of .

The main result of the paper is

Theorem 2.1.

Let the following assumptions hold:

-

(a)

are independent p-dimensional real-valued random vectors with independent entries satisfying condition:

for some constant and for any ,

-

(b)

As , the sample size and .

Then,

-

(1)

as , almost surely, the empirical spectral distribution of , converges to a non-random probability distribution whose Stieltjes transform , , satisfies the equation

(2.1) -

(2)

Moreover, for , equation (2.1) admits an unique solution with positive imaginary part and the density function of the LSD is:

where . Moreover, the support of f(u) is for , and for , where

It’s easy to check that when , the LSD of has a point mass at the origin since for large and , and at the same time we have

Since the matrix we are interested in has the same non-zero eigenvalues with , the following proposition holds.

Proposition 2.1.

Under the conditions of Theorem 2.1, the ESD of converges a.s. to a non-random limit distribution

whose Stieltjes transform , , satisfies the equation

In particular, has the density function

where in the later case , has an additional mass at the origin.

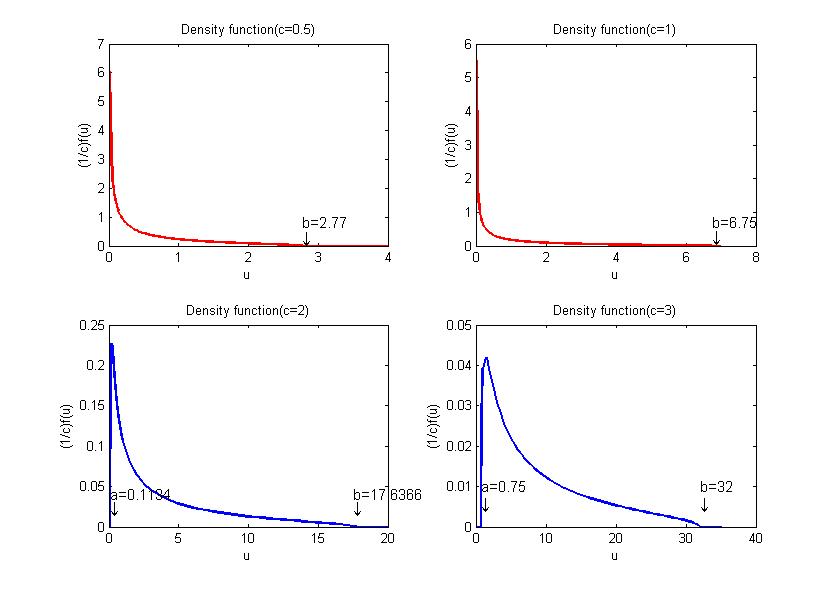

The following details the density function of LSD of for different values of c.

-

•

When , the support is and the density function is

where . It’s easy to see that as , .

-

•

If , it can be seen from the explicit form of that when , because the in the denominator of the density function cannot be completely canceled out.

-

•

If , the shape of the density function turns out to be a little different from the case . Nevertheless it’s quite intuitive because the lower bound of the support is positive and the density function is bounded.

The density functions of LSD of A for are displayed on Figure 1.

3 Proofs

3.1 Proof of Theorem 2.1

The proof of the theorem follows the general strategy based on the Stieltjes transform as presented in Silverstein [9], Bai and Silverstein [3] and Pastur and Shcherbina [8]. However, the random matrix B here is no more a covariance matrix as considered in these references. Almost all the steps of the proof need new arguments and ideas compared to the case of sample covariance matrices considered so far in the literature. Following this method, the first step is to truncate the entries at a convenient rate using Assumption (a). After truncation and the follow-up steps of centralization and standardization, we may assume that

The details of these technical steps are given in Appendix A.

By the rank inequality(Theorem A.44 of [3]), it is enough to consider

where

At this stage, the important observation is that here we have replaced by without altering the LSD of B since when , the effect of this substitution will vanish. For the sake of convenience, we still use to denote .

For , define

Let

The method consists in finding a system of two asymptotic equations satisfied by and . Solving the system yields an asymptotic equivalent for and finally leads to the equation (2.1) satisfied by the limit of . Nonetheless, is the Stieltjes transform of the matrix B which can be recovered from the inversion formula.

Let

then

We have

Taking trace and dividing both sides by , we get

| (3.1) |

Note that is the Stieltjes transform of the ESD of the matrix B, and its limit will be found by letting on both sides of the equation.

Consider , using the identities

and

we have

where and are explicitly defined.

For , we have

Therefore, by equation , we have

| (3.2) | |||

Here, we have used the following equivalents, uniformly in , as ,

Similar to equation (3.1), we have

| (3.3) |

Considering , we have

where and are explicitly defined.

For , we have

For , we have

Therefore, by equation , we have

| (3.4) | |||

By Lemma 5.2, the second term is since both and are non-negative and bounded as .

Finally, by equation , we find

| (3.5) |

This leads to

| (3.6) |

In conclusion, satisfy the system

Notice that for any is bounded, and by equation (3.6), is also bounded as , otherwise (3.6) may not hold. Therefore, both and are bounded sequences. Let be two subsequences so that and as . It can be concluded that the limiting functions satisfy the system of equations:

By eliminating , we finally find the equation (2.1) satisfied by the limiting function . Denote by all the analytical functions . Because according to the following proof we have one unique solution on that satisfies equation (2.1), the whole bounded sequence has one unique limit in .

As for the second statement of Theorem 2.1, in order to find the density function of the LSD of , we use the inversion formula:

where is the Stieltjes transform of . Write

both and are real-valued functions of . By substituting , into equation (2.1) and letting , both the real part and the imaginary part of the LHS of equation (2.1) should equal to 0, i.e.

By plugging in (4) into (3), we get

Solving this equation and substituting for in (4), we get

where

| (3.7) |

It can be checked that only the first solution is compatible with the fact that both and are real-valued functions of , i.e.

From the explicit form of we see that, necessarily,

since . Solving this quadratic inequality, we get two roots,

| (3.8) |

It’s very easy to see that is an increasing function of and when .

In other words, if , , then the support of the density function should be . If , , then the support of the density function is .

Then the density function of the limiting spectral distribution of the dimensional multiplied lag-1 sample auto-covariance matrix is

where , for and , for , with given in equation (3.7) and given in equation (3.8). Therefore, equation (2.1) admits at least one solution that corresponds to this density function of the LSD . As for the uniqueness, suppose there exists another solution that satisfies equation (2.1), then there should be another density that corresponds to while . However, it can be seen from the previous deductions that the density function is unique. Therefore, , . Equation (2.1) admits one unique solution.

3.2 Proof of Proposition 2.1

Under the same conditions in Theorem 2.1, the ESD of converges to a non-random limit distribution with Stieltjes transform . On the other hand, the ESD of converges to with Stieltjes transform satisfying

Since it’s known that

conclusively we have

Substituting into the equation of we can get the equation of , which is

4 Extension to lag- sample auto-covariance matrix

So far in previous sections, we have focused on the singular value distribution of the lag-1 sample auto-covariance matrix , while in this section, for any given positive integer , we discuss the singular value distribution of the lag- sample auto-covariance matrix .

Here we follow exactly the same strategy used in the derivation of the LSD of the lag-1 sample auto-covariance matrix. It’s easy to see that the difference between and lies in that we have now for ,

Meanwhile, the other matrices and notations remain the same using however the new definition of the above. Consequently, equation (3.2) becomes

| (4.1) | |||

Equation (3.4) becomes

| (4.2) | |||

Thus, according to equation (4.1) and (4.2), we still have

Meanwhile, by Lemma 5.3, we still have

| (4.3) |

then by equation (4.1), we have

| (4.4) |

Similarly, as for the second equation satisfied by and , equation (3.6) persists.

| (4.5) |

Therefore, the system of equations satisfied by and remains the same when the time lag changes from 1 to . In other words, for a given positive time lag , the singular value distribution of is the same with that of established in Theorem 2.1.

5 TECHNICAL LEMMAS

Lemma 5.1.

Under the same assumptions in Theorem 2.1, we have, , almost surely,

| (5.1) |

| (5.2) |

| (5.3) |

| (5.4) |

where the terms are uniform in .

Proof.

We detail the proof of (5.1) and the proofs of (5.2), (5.3) and (5.4) are very similar, thus omitted.

Denote by , , then we have

where is the image part of .

Following the scheme of Lemma 9.1 of [3] it’s easy to see that

where

What’s more,

Consider a graph G with edges that link to and to , . It’s easy to see that for any nonzero term, the vertex degrees of the graph are not less than 2. Write the non-coincident vertices as with degrees greater than 1, then, similarly in Lemma 9.1 of Bai and Silverstein [3], we have,

Therefore, by the Borel-Cantelli lemma, we have, ,

where the terms are uniform in . ∎

Lemma 5.2.

Under the same assumptions in Theorem 2.1, we have, , , almost surely,

where the terms are uniform in .

Proof.

Notice that, for ,

Here represents the power of the matrix , we use to denote the transpose of matrix . Denote, for ,

It’s easy to see that

In addition, for any ,

Now we can derive the recursion equations between and .

Firstly, for , , since

taking trace and dividing on both sides of the equation, we get

i.e.

| (5.5) |

Particularly, for , we have

| (5.6) |

Similarly, for , ,

i.e.

| (5.7) |

Particularly, for , we have

| (5.8) |

Note that

then we have either or .

If , according to equation (5.5), we have , then according to equation (5.7), we have , recursively, we have for all ,

Otherwise, if , according to equation (5.6), we have , then according to equation (5.7), we have , then according to equation (5.5), we have , recursively, we still have for all ,

Therefore we have, , , almost surely,

where the terms are uniform in . ∎

Lemma 5.3.

Extension of Lemma 5.2 to time lag :

we have, , , almost surely,

where the terms are uniform in .

Proof.

Denote, for ,

It’s easy to see that

In addition, for any ,

Now we can derive the recursion equations between and .

Firstly, for , ,

i.e.

| (5.9) |

Similarly, for , ,

i.e.

| (5.10) |

Particularly, for , we have

| (5.11) |

Note that

following the same arguments in Lemma 5.2, we have, , , almost surely,

where the terms are uniform in .

∎

Appendix A Justification of truncation, centralization and standardization

Recall that , are independent real-valued random variables with , and we are interested in is the LSD of time-lagged covariance matrix

The assumed moment conditions are: for some constant ,

and for any ,

The aim of the truncation, centralization and standardization procedure is that after these treatment, we may assume that

Since the whole procedure is the same with respect to different time lag , we focus on the case of lag-1 sample auto-covariance matrix.

A.1 Truncation

Let , , can be seen as a constant.

we have

Applying Bernstein’s inequality

where , , are i.i.d bounded by b, we can get that, for any small ,

which is summable, then by Borel-Cantelli lemma,

A.2 Centralization

Let , , .

With Theorem A.46 of [3],

we have

For ,

| (A.1) |

Consider the second term, we have

Notice that , we have

Moreover,

Therefore, .

For the term , we have

Therefore, a.s. , as .

Consequently, Similarly, we can prove that the last term in equation (A.2) tends to zero almost surely. As for the first term, we have

Therefore

Now, we consider ,

Firstly, for , since ,

Moreover,

Therefore , a.s. Next for ,

Therefore, . All in all,

A.3 Rescaling

Define , we can see that as , since , .

According to Theorem A.46 of [3], we have

Consider ,

Moreover,

Therefore

References

- Anderson, Guionnet and Zeitouni [2010] Anderson, G. W., Guionnet, A., and Zeitouni, O. (2010). An introduction to random matrices(No. 118). Cambridge University Press.

- Bai Silverstein [1998] Bai, Z.D. and Silverstein, J.W. (1998). No eigenvalues outside the support of the limiting spectral distribution of large-dimensional sample covariance matrices. The Annals of Probability, Vol. 26, NO. 1, 316-345.

- Bai and Silverstein [2004] Bai, Z. and Silverstein, J. W. (2010). Spectral Analysis of Large Dimensional Random Matrices (2nd ed.) Springer.

- Bai and Yin [1993] Bai, Z.D. and Yin, Y.Q.(1993). Limit of the smallest eigenvalues of large dimensional covariance matrix. Ann. Probab. 21(3), 1275-1294.

- Lam et al. [2011] Lam, C., Yao, Q. and Bathia, N. (2011). Estimation of latent factors for high-dimensional time series. Biometrika 98(4), 901-918.

- Lam and Yao [2012] Lam, C. and Yao, Q. (2012). Factor modeling for high-dimensional time series: inference for the number of factors. Ann. Statist. 40(2), 694-726.

- Marenko and Pastur [1967] Marenko, V.A. and Pastur, L.A.(1967), Distribution of eigenvalues in certain sets of random matrices. Math. USSR-Sb. 1, 457-483.

- Pastur and Shcherbina [2010] Pastur, L. A. and Shcherbina, M. (2010). Eigenvalue distribution of large random matrices. American Mathematical Society, Providence, Rhode Island

- Silverstein [1995] Silverstein, J.W. (1995) Strong convergence of the empirical distribution of eigenvalues of large dimensional random matrices. J. Multivariate Anal. 5, 331-339