A note on error estimation for hypothesis testing problems

for some linear SPDEs

This version: July 15, 2014

Forthcoming in Stochastic Partial Differential Equations: Analysis and Computations)

Abstract

The aim of the present paper is to estimate and control the Type I and Type II errors of a simple hypothesis testing problem of the drift/viscosity coefficient for stochastic fractional heat equation driven by additive noise. Assuming that one path of the first Fourier modes of the solution is observed continuously over a finite time interval , we propose a new class of rejection regions and provide computable thresholds for , and , that guarantee that the statistical errors are smaller than a given upper bound. The considered tests are of likelihood ratio type. The main ideas, and the proofs, are based on sharp large deviation bounds. Finally, we illustrate the theoretical results by numerical simulations.

Keywords: Hypothesis testing for SPDE; Likelihood Ratio; Maximum Likelihood Estimator; error estimates; sharp large deviation; fractional heat equation; additive space-time white noise.

MSC2010: 60H15, 35Q30, 65L09

1 Introduction

Under assumption that one path of the first Fourier modes of the solution of a Stochastic Partial Differential Equation (SPDE) is observed continuously over a finite time interval, the parameter estimation problem for the drift coefficient has been studied by several authors, starting with the seminal paper [HKR93]. Consistency and asymptotic normality of the MLE type estimators are well understood, at least for equations driven by additive noise; see for instance the survey paper [Lot09] for linear SPDEs, and [CGH11] for nonlinear equations, and references therein. Generally speaking, the statistical inference theory for SPDEs did not go far beyond the fundamental properties of MLE estimators, although important and interesting classes of SPDEs driven by various noises were studied. The first attempt to study hypothesis testing problem for SPDEs is due to [CX13], where we investigated the simple hypothesis for the drift/viscosity coefficient for stochastic fractional heat equation driven by additive noise, white in time and colored in space. Therein, the authors established ‘the proper asymptotic classes’ of tests for which we can find ‘asymptotically the most powerful tests’ – tests with fastest speed of error convergence. Moreover, we provided explicit forms of such tests in two asymptotic regimes: large time asymptotics , and increasing number of Fourier modes . By its very nature, the theory developed in [CX13] is based on asymptotic behavior, , and a follow-up question is how large or should we take, such that the Type I and Type II errors of these tests are smaller than a given threshold. The main goal of this paper is to develop feasible methods to estimate and control the Type I and Type II errors when and are finite. Similar to [CX13], we are interested in Likelihood Ratio type rejection regions and , where is the projected solution on the space generated by the first Fourier modes, is the Likelihood Ratio, is a constant that depends on the first eigenvalues of the Laplacian, and are some constants that depend on and . We will derive explicit expression for and , and thresholds for , and respectively for , that will guarantee that the corresponding statistical errors are smaller than a given upper bound. However, this comes at the cost that these tests are no longer the most powerful in the class of tests proposed in [CX13]. The key ideas, and the proofs of main results, are based on sharp large deviation principles (both in time and spectral spatial component) developed in [CX13]. On top of the theoretical part, we also present some numerical experiments as a coarse verification of the main theorems. We find some bounds for the numerical approximation errors, that will also serve as a preliminary effort in studying the statistical inferences problems for SPDEs under discrete observations. Finally, we want to mention that the case of large and corresponds to classical one dimensional Ornstein-Uhlenbeck process, and even in this case, to our best knowledge, the obtained results are novel.

The paper is organized as follows. In Section 1.1 we set up the problem, introduce some necessary notations, and discuss why for the tests proposed in [CX13] it is hard to find explicit expressions for and in order to control the statistical errors. Since sharp large deviation principles from [CX13] play fundamental role in the derivation of main results, in Section 1.2 we briefly present them here too. Section 2 is devoted to the case of large time asymptotics, with number of observable Fourier modes being fixed. We show how to choose and such that both Type I and Type II errors, associated with rejection region , are bounded by a given threshold. Similarly, in Section 3 we study the case of large while keeping the time horizon fixed. In Section 4 we illustrate the theoretical results by means of numerical simulations. We start, with the description of the numerical methods, and derive some error bounds of the numerical approximations. Consequently, we show that while the thresholds for derived in Sections 2 and 3 are conservative, as one may expect, they still provide a robust practical framework for controlling the statistical errors. Finally, in Section 5 we discuss the advantages and drawbacks of the current results and briefly elaborate on possible theoretical and practical methods of solving some of the open problems.

1.1 Setup of the problem and some auxiliary results

In this section we will set up the main equation, briefly recall the problem settings of hypothesis testing for the drift coefficient, and present some needed results from [CX13]. Also here we give the motivations that lead to the proposed problems.

Similar to [CX13], on a filtered probability space we considered the following stochastic evolution equation

| (1.1) |

where , , , for some , ’s are independent standard Brownian motions, is a bounded and smooth domain in , is the Laplace operator on with zero boundary conditions, ’s are eigenfunctions of . It is well known that form a complete orthonormal system in . We denote by the eigenvalue corresponding to , and put . Under some fairly general assumptions, equation (1.1) admits a unique solution in the appropriate Sobolev spaces (see for instance [CX13]).

We assume that all parameters are known, except the drift/viscosity coefficient which is the parameter of interest, and we use the spectral approach (for more details see the survey paper [Lot09]) to derive MLE type estimators for . In what follows, we denote by the Fourier coefficient of the solution of (1.1) with respect to , i.e. . Let be the finite dimensional subspace of generated by , and denote by the projection operator of into , and put , or equivalently . Note that each Fourier mode , is an Ornstein–Uhlenbeck process with dynamics given by

| (1.2) |

We denote by the probability measure on generated by . The measures , are equivalent to each other, with the Radon-Nikodym derivative, or the Likelihood Ratio, of the form

| (1.3) |

where denotes the trajectory of over the time interval . Maximizing the Log of the Likelihood Ratio with respect to , we get the Maximum Likelihood Estimator (MLE)

| (1.4) |

In [CX13], we established the strong consistency and asymptotic normality of the MLE, when or goes to infinity.

In this work we consider a simple hypothesis testing problem for , assuming that the parameter can take only two values , with the null and the alternative hypothesis as follows

Without loss of generality, we will assume that , and . Throughout, we fix a significant level . Suppose that is a rejection region for the test, i.e. if we reject the null and accept the alternative. The quantity is called the Type I error of the test , and respectively is called the Type II error. Naturally, we seek rejection regions with Type I error smaller than the significance level :

Let us denote by the rejection region (likelihood ratio test) of the form

where , such that . In [CX13] we proved that is the most powerful test (has the smallest Type II error) in the class ,

While this gives a complete theoretical answer to the simple hypothesis testing problem, generally speaking there is no explicit formula for the constant . The main contribution of [CX13] was to find computable rejection regions, and the appropriate class of tests, by so called asymptotic approach. The authors study two asymptotic regimes: large time asymptotics, while fixing the number of Fourier modes , and large number of Fourier modes, while time horizon is fixed. We will outline here the case of large time asymptotics. Let and be defined as follows:

where is -quantile of standard Gaussian distribution, and is a constant that depends on . The class essentially consists of tests with Type I errors converging to from above with rate at least . It was proved that

| (1.5) |

In other words, has the fastest rate of convergence of the Type II error, as , in the class . We proved analogous results for , and being fixed, by taking

where is a constant depending on and only, and is a constant that depends on . We refer the reader to [CX13] for further details.

However, by their very nature of being asymptotic type results, one cannot assess how large (or ) shall be taken to guarantee that the error is smaller than a desired tolerance. The main goal of this manuscript is to investigate the corresponding error estimates for fixed values of and .

Let us start with some heuristic discussion on why for the tests and one cannot easily find computable expressions for or that will guarantee certain bounds on statistical errors. As it was shown in [CX13, Lemma 3.13], for sufficiently large , we have the following asymptotic expansion under the null hypothesis :

Hence, for large enough, we will have the estimate

where is a constant independent of . Similarly (cf. [CX13, Lemma 3.21]), we have the asymptotic expansions

Since , for , we get

where is a constant independent of .

Due to lack of knowledge of the behavior of higher order terms in the above asymptotics, practically speaking, the above constants and cannot be easily determined. The case of large Fourier modes is especially intricate, since the asymptotic expansion of Type I error is done in terms of rather than . To overcome this technical problem, we propose a new test, which may not be asymptotically the most powerful, but which is convenient for the errors’ estimation. Moreover, we validate the obtained results by numerical simulations.

1.2 Sharp Large Deviation Principle

The main results presented in this paper, and the ideas behind them, rely on some results on sharp large deviation bounds obtained in [CX13]. While the sharp deviations results for large time asymptotics are comparable in certain respects with those from Stochastic ODEs (cf. [BR01, Kut04, Lin99]), the results for large number of Fourier modes are new, and by analogy we refer to them also as sharp large deviation principle. For convenience, we will briefly present some of needed results here too.

Generally speaking, we seek asymptotics expansion of the form

for or , and where are some explicit function of , and is a residual term. Similarly, we are looking for asymptotic expansion of , while is fixed. With these at hand, we find a convenient representation of probabilities

where has the form or for some constant . Below we will present the explicit expressions for functions . Albeit the formulas are somehow cumbersome, their particular form is less important at this stage.

Along these lines, we adapt the notations

for . The following expansions hold true

| (1.6) | ||||

| (1.7) |

where , and where

Using these results, one can show that the following identities are satisfied,

| (1.8) | ||||

| (1.9) |

with

| (1.10) |

where is a number which may depend on and , and are numbers which depend on , and are the expectations under and respectively with

| (1.11) | ||||

| (1.12) |

By taking or such that or , we got

| (1.13) | ||||

| (1.14) |

and then by direct computations we found that

| (1.15) | ||||

| (1.16) |

where

| (1.17) |

Finally, also in [CX13] we derived the large deviation principles for considered SPDEs

| (1.18) | |||||

| (1.19) |

It should be mentioned that in [CX13] the relations (1.6)–(1.19) were derived only under the alternative hypothesis, , however, the corresponding results for are obtained in a very similar manner. The main difference is that in the PDE obtained by Feynman-Kac Formula is replaced by , but the method of solving it remains of course the same. We admit that some parts of these derivations may appear technically challenging, but nevertheless we felt unnecessary to mimic them here.

2 The case of large times

Throughout this section, we assume that the number of Fourier modes is fixed. Recall that without loss of generality we assume that (the obtained results are symmetric otherwise). We still consider tests of the form , but for the sake of convenience we write them equivalently as

| (2.1) |

where, unless specified, is an arbitrary number which may depend on and . Our goal is to find a proper expression for such that for larger than a certain number, the Type I and II errors are always smaller than a chosen threshold. Clearly, we are looking for that is a bounded function of . Using the results on large deviations from Section 1.2, we will first give an argument how to derive a proper expression of , followed by main results and their detailed proofs.

Following the large deviation principle (1.18), let us assume that is such that

| (2.2) |

Then, we have that , and hence Consequently, in view of (1.8), to get an upper bound for the Type I error, it is enough to estimate . By (1.15), combined with (1.18), we note that is the dominant term of asymptotic expansion of Type I error. Since we have an explicit expression of the residual part , this suggest that if we simply let the dominant part to be equal to the significance level , that is

| (2.3) |

we may be able to control the Type I error by a much simpler function. In fact, by solving equation (2.3), that has two solutions, and since has to satisfy (2.2), we choose

| (2.4) |

Clearly is a bounded function of . Moreover, indeed satisfies (2.2), a point made clear by (2) below.

Next we present the first main result of this paper that shows how large has to be so that the Type I error is smaller than a given tolerance level.

Theorem 2.1.

Assume that the test statistics has the form

where is given by (2.4). If

| (2.5) |

then the Type I error has the following bound estimate

where denotes a given threshold of error tolerance111Generally expected to be small, say less than 10%. Smaller will yield larger , and the final choice is left to the observer..

Proof.

Let us consider

| (2.6) |

Note that , which implies that . Moreover, since , as , we also have that , for sufficiently large , and hence (2.2) is satisfied.

Substituting (2.4) into (1.13), by direct evaluations, we deduce

| (2.7) |

By (2) and (2.7), we conclude that, if

| (2.8) |

then have the following estimate

| (2.9) |

A straightforward inspection of the derivative of implies that decreases for , and goes to 1, as . Thus, using (2.9), if

| (2.10) |

then we can guarantee that . From here, under assumption that (2.8) and (2.10) hold true, we have

| (2.11) |

Due to the fact that , we get

Therefore, under (2.8) and (2.10), we obtain

From the above, and by means of Bernoulli inequality, we continue

| (2.12) |

Note that the above inequalities hold true if all the terms in the parenthesis are positive, for which is enough to assume that

| (2.13) |

Recall that , and hence . Using (1.8) and (2.3), combined with (2.11) and (2), we conclude that

Thus, in order to make the Type I error to satisfy the desire upper bound , it is sufficient to require that

| (2.14) |

under assumption that (2.8), (2.10) and (2.13) hold true, which is satisfied due to original assumption (2.5). This concludes the proof.

∎

Next we will study the estimation of Type II error, as time goes to infinity.

Theorem 2.2.

Assume that the test is given as in Theorem 2.1. If

| (2.15) |

then the Type II error admits the following upper bound estimate

| (2.16) |

Proof.

Let be as in (2.4). By direct evaluations, one can show that

Recall that, from the previous theorem, assuming that (2.5) holds true, we have that

| (2.17) |

In view of (2) and (1.17), if we further require that

| (2.18) |

it can be easily deduced that

| (2.19) |

By (2.9), assuming that (2.10) holds true, we also have that

and hence

| (2.20) |

Note that (1.8)-(1.15) imply that

Therefore, (2.16) follows from (2.17), (2.19) and (2.20), under assumption that (2.5) and (2.18) are satisfied, which is guaranteed by (2.15). This finishes the proof. ∎

3 The case of large number of Fourier modes

In this section we study the error estimates for the case of large number of Fourier modes , while the time horizon is fixed. The key ideas and the method itself are similar to those developed in the previous section. We consider tests of the form

| (3.1) |

where is some number depending on and , and where as before . The goal is to find , as a bounded function of , that will allow to controll the statistical errors when the number of Fourier modes is large.

Similarly to -part, for , we have that , and hence . Thus, it is enough to estimate , and by the same reasons as in Section 2, we let , and derive that the natural candidate for has the following form

| (3.2) |

Next we provide the result on how large should be (for a fixed ) to guarantee that Type I and Type II errors are smaller than a given tolerance level.

Theorem 3.1.

Consider the test

where is given by (3.2).

-

(i)

If

(3.3) then the Type I error has the following upper bound estimate

(3.4) where denotes a given threshold of error tolerance.

-

(ii)

If

(3.5) we have the following estimate for Type II error

(3.6)

The proof is similar222For most of the derivations one just needs to ‘exchange with .’ The results are, in a sense, symmetric with respect to and . In (3.3) and (3.5) we separate the conditions for into two inequalities, since we want to place all the terms related to on the left side of the inequalities. to the proofs of Theorem 2.1 and Theorem 2.2, and we omit it here333We need to point out that sometimes we may not be able to find such that the conditions (3.3) and (3.5) are satisfied. For example, if then is bounded for all , and if its bound is smaller than the right hand side of the second inequality in (3.3) and (3.5), then the conditions (3.3) and (3.5) fail for all . However, for we might still be able to control the Type I and Type II errors by finite , which requires a more technical proof and is deferred to future study..

4 Numerical Experiments

In this section we give a simple illustration of theoretical results from previous sections by means of numerical simulations. Besides showing the behavior of Type I and Type II errors for the test proposed in this paper, we will also display the simulation results for test mentioned in Section 1.1 and discussed in [CX13]. We start with description of the numerical scheme used for simulation of trajectories of the solution (more precisely of the Fourier modes), and provide a brief argument on the error estimates of the corresponding Monte Carlo experiments associated with this scheme. In the second part of the section, we focus on numerical interpretation of the theoretical results obtained in Sections 2 and 3.

We use the standard Euler-Maruyama scheme444Of course many other discretizations of equation (1.1) can be chosen, such as implicit Euler scheme, or exponential Euler scheme, that can be computationally more efficient; cf. the monograph [JK11]. to numerically approximate the trajectories of the Fourier modes given by equation (1.2), and we apply Monte Carlo method to estimate the Type I and Type II errors. We partition the time interval into equality spaced time intervals , with , for . Let denote the number of trials in the Monte Carlo experiment of each Fourier mode. Assume that is the true value of the -th Fourier mode at time of the -th trial in Monte Carlo simulation. Then, for every , , we approximate according to the following recursion formula

| (4.1) |

where are i.i.d. Gaussian random variables with zero mean and variance . In what follows, we will investigate how to approximate the Type I and Type II errors of test using ’s, and how the numerical errors are related to , , and .

Throughout this section we consider equation (1.1), and consequently (4.1), with , in one dimensional space , with the random forcing term being the space-time white noise . We also assume that the spacial domain and the initial value . In this case . We fix the parameter of interest to be and . The general case is treated analogously, the authors feel that a complete and detailed analysis of the numerical results are beyond the scope of the current publication. The numerical simulations presented here are intended to show a simple analysis of the proposed methods. We performed simulations for other sets of parameters, and the numerical results were in concordance with the theoretical ones. For example, for the case of large times, if one increases , then the statistical errors are reaching the threshold for smaller values of - more information improves the rate of convergence. Similarly, increasing for the case of asymptotics in , one needs to take fewer Fourier modes to bypass the threshold of the statistical errors. Different ranges and magnitudes of the parameter of interest were considered, and the outcomes are similar to those presented below. All simulations and computations are done in MATLAB and the source code is available from the authors upon request.

4.1 Description and analysis of the numerical experiments

Throughout denotes a constant, whose value may vary from line to line, and whenever the formulas or results are indexed by , we mean that they hold true for all . Using (1.1), and by Itō’s formula, we get

| (4.2) |

where and are given by (2.4) and (2) respectively, and

We approximate and as follows

Define

Then, naturally, the approximation of is given by

| (4.3) |

Following [Bis08, Chapter 8], one can prove that

| (4.4) |

Consequently, for any , we have

According to [CX13, Lemma 3.13], for large enough , the following estimate holds true

By the above results, and Chebyshev inequality, we conclude that

Similarly, we have that

Combining the above two inequalities, we obtain that, for any ,

This implies that

| (4.5) |

where is a constant, which is small as long as is small. It is straightforward to check that for large

where is a constant independent of . From here and using (4.4), one can also show that

This implies that the error of Monte Carlo simulations can be controlled by uniformly with respect to and . Therefore, we have the following error estimate

| (4.6) |

which holds true with high probability (confidence interval of the Monte Carlo experiment). Here is a constant which depends on (usually small), and is a constant which only depends on the confidence level of Monte Carlo simulations. Thus, the estimator can be made arbitrarily close to the true value of with arbitrarily high probability, as long as we take small enough time step and large enough number of trials of Monte Carlo simulations.

To approximate the value of , similarly to (4.1), we obtain

and we define

Then, the approximation of is given by

| (4.7) |

Following the same proof we obtain error estimates similar to (4.6) for .

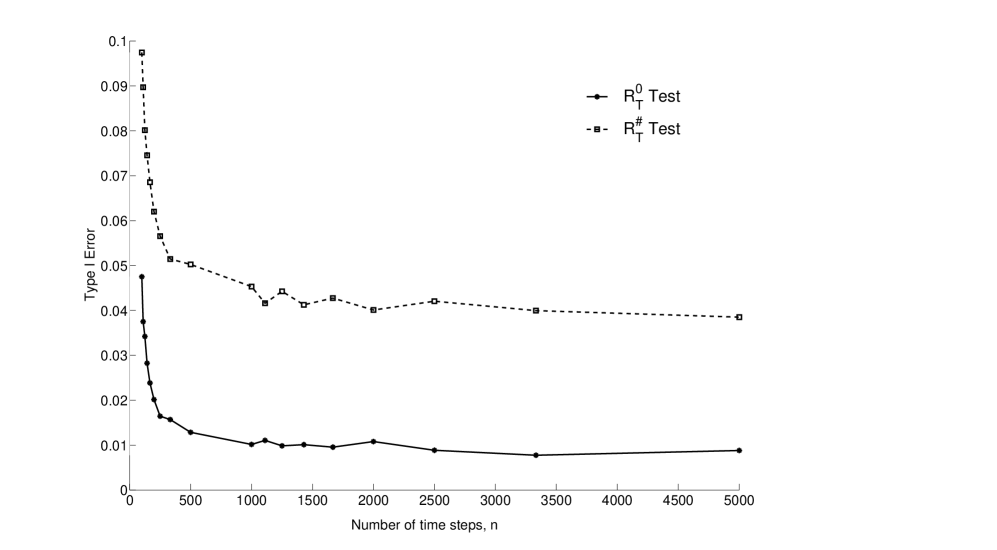

Next we will present some numerical results that validate relationship (4.6). In Table 1, we list simulation results of (4.3) for various value of the time step (or number of time steps ), while keeping fixed time horizon , number of Monte Carlo simulations , and number of Fourier modes . For convenience, we present same results in graphical form, Figure 1.

| 0.0475 | 0.0375 | 0.0342 | 0.0283 | 0.0239 | 0.0202 | 0.0165 | 0.0157 | 0.0129 | |

| 0.0975 | 0.0897 | 0.0802 | 0.0746 | 0.0686 | 0.0620 | 0.0566 | 0.0515 | 0.0503 | |

| 0.0102 | 0.0111 | 0.0099 | 0.0101 | 0.0096 | 0.0108 | 0.0089 | 0.0078 | 0.0088 | |

| 0.0453 | 0.0416 | 0.0443 | 0.0413 | 0.0428 | 0.0401 | 0.0421 | 0.0400 | 0.0385 |

Other parameters: , , , , ,

, , .

Graphical interpretation of Table 1.

As shown in Figure 1 the value of , and respectively , rapidly decays (approximatively up to the point when or ), and then it steadily approaches a certain ‘asymptotic level’, which, as suggested by (4.6), shall be the true value of (or ). This assumes a reasonable large value of , in our case . When gets smaller, we notice small fluctuations around that ‘asymptotic level’, which are errors induced by the Monte Carlo method, and one can increase the number of trials to locate more precisely that true value. In our case the fluctuations are negligible comparative to the order of .

Now we fix the time horizon , and vary the number of Fourier modes . Similarly to derivation of (4.1), we have

where

Next, we define

and approximate the probability by

| (4.8) |

One can prove555As usually, the case of large is more delicate and technically challenging, comparative to the case of large times. Apparently, (4.9) holds true for some positive . The sharpest value of is not relevant for this paper, and we defer the derivation of it to future study. that for some ,

| (4.9) |

Following the same procedure as for large time asymptotics, we get

| (4.10) |

where is a constant which depends on , and is a constant which depends on the confidence level of Monte Carlo experiment.

Similar results are obtained for the approximation of and the Type II errors , , and , and for brevity we will omit them here.

We conclude that the errors due to the numerical approximations considered above are negligible. Hence, the numerical methods we propose are suitable for our purposes of computing the statistical errors of , , and tests, and we will use them for derivation of all numerical results from the next sections.

4.2 Numerical tests for large times

We start with the case of large times and fixed , and the results discussed in Section 2. We take that , i.e. we observe one path of the first three Fourier modes of the solution over some time interval . For convenience, we denote by , and respectively , the lower bound thresholds for from Theorem 2.1, relation (2.5), and respectively Theorem 2.2, relation (2.15). In Table 2, we list the Type I error , along with corresponding values of , for various values of . Note that for all values of , the Type I error is smaller than the threshold , and as expected, being on conservative side.

| 0.1 | 0.05 | 0.01 | 0.005 | |

| 629 | 818 | 1258 | 1447 | |

| 0.021 | 0.010 | 0.0025 | 0.0015 |

Other parameters: , , ,

, .

In Table 3 we show that for , the error remains smaller than the chosen bound. In fact, the Type I error is decreasing as gets larger, with all other parameters fixed.

| 0.0100 | 0.0097 | 0.0105 | 0.0100 | 0.0105 | 0.0102 | |

| 0.0540 | 0.0525 | 0.0505 | 0.0526 | 0.0512 | 0.0505 |

Other parameters: , , , ,

, , .

As already mentioned, the statistical test derived in [CX13], while it is asymptotically the most powerful in , it will not guarantee that the statistical errors will be below the threshold for a fixed finite ; only asymptotically it will be smaller than . Indeed, as Table 3 shows, the Type I error for fluctuates around , with no pattern. That was the very reason we proposed the tests .

To illustrate the results from Theorem 2.2, and the behavior of Type II error , one needs to look at very large values of , which is beyond our technical possibilities and the goal of this paper. We will only give the results for some reasonable large values of ; see Table 4. Note that indeed the Type II error is decreasing as time gets larger. Also here, we show the corresponding results for the test .

| 0.7155 | 0.3329 | 0.1148 | 0.0293 | 0.0070 | 0.0012 | |

| 0.7946 | 0.2402 | 0.0457 | 0.0060 | 0.0006 | 0.0002 |

Other parameters: , , , , , .

4.3 Numerical tests for large number of Fourier modes

Now we do a similar analysis by varying number of Fourier coefficients , while the time horizon is fixed. As mentioned above, the case of large is much more delicate, and as it turns out, according to the numerical results presented below, the error bounds for the statistical errors from Theorem 3.1 are on conservative side. The decay of the errors obtained in our numerical simulations is much faster than suggested by theoretical results, which from practical point of view is a desired feature.

| 0.007 | 0.012 | 0.010 | 0.017 | 0.012 | 0.014 | 0.010 | 0.013 | |

| 0.006 | 0.037 | 0.039 | 0.053 | 0.040 | 0.039 | 0.054 | 0.046 |

Other parameters: , , , , , .

5 Concluding remarks

On discrete sampling. Eventually, in real life experiments, the random field would be measured/sampled on a discrete grid, both in time and spatial domain. It is true that the main results are based on continuous time sampling, and may appear as being mostly of theoretical interest. However, as argued in the Section 4, the main ideas of this paper and [CX13] have a good prospect to be applied to the case of discrete sampling too. The error bounds of the numerical results presented herein contributes to the preliminary effort of studying the statistical inference problems for SPDEs in the discrete sampling framework. At our best knowledge, there are no results on statistical inference for SPDEs with fully discretely observed data (both in time and space). We outline here how to apply our results to discrete sampling, with strict proofs differed to our future studies. If we assume that the first Fourier modes are observed at some discrete time points, then, to apply the theory presented here, one essentially has to approximate some integrals, including some stochastic integrals, convergence of each is well understood. Of course, the exact rates of convergence still need to be established. The connection between discrete observation in space and the approximation of Fourier coefficients is more intricate. Natural way is to use discrete Fourier transform for such approximations. While intuitively clear that increasing the number of observed spacial points will yield to the computation of larger number of Fourier coefficients, it is less obvious, in our opinion, how to prove consistency of the estimators, asymptotic normality, and corresponding properties from hypothesis testing problem.

On derivation of other tests. We want to mention that the (sharp) large deviations, appropriately used, can lead to other practically important family of tests. In fact, it is not difficult to observe that, if we take with

then both Type I and Type II errors will go to zero, as . Clearly, the motivation for doing this is to have both errors as small as possible. Moreover, for such the statistical errors will go exponentially fast to zero. Of course, this will not be the most powerful test in the sense of [CX13], since such chosen will reduce the exponential rate of convergence of Type II error. However, by shrinking the class of tests, one may preserve to be ‘asymptotically the most powerful’ in the new class. For example, once the asymptotical properties of errors are well understood, one can consider a new class of tests of the form

where () are some parameters to be determined. Then, employing the same methodology as in [CX13], one can show that is the most powerful in , with only slight modification of some technical results. Similar ideas can lead to corresponding results for .

On composite hypothesis. Despite of the fact simple hypothesis testing problems are rarely used in practice, the efforts of this work, as well as those from [CX13], should be seen as a starting point of a systematic study of general hypothesis testing problems and goodness of fit tests for stochastic evolution equation in infinite dimensional spaces. As pointed out in [CX13], the developments of ‘asymptotic theory’ for composite hypothesis testing problem will follow naturally, and consequently one can extend the results of this paper to the case of composite tests.

Acknowledgments

We would like to thank the anonymous referees, the associate editor and the editor for their helpful comments and suggestions which improved greatly the final manuscript. Igor Cialenco acknowledges support from the NSF grant DMS-1211256.

References

- [Bis08] J. P. N. Bishwal. Parameter estimation in stochastic differential equations, volume 1923 of Lecture Notes in Mathematics. Springer, Berlin, 2008.

- [BR01] B. Bercu and A. Rouault. Sharp large deviations for the Ornstein-Uhlenbeck process. Teor. Veroyatnost. i Primenen., 46(1):74–93, 2001.

- [CGH11] I. Cialenco and N. Glatt-Holtz. Parameter estimation for the stochastically perturbed Navier-Stokes equations. Stochastic Process. Appl., 121(4):701–724, 2011.

- [CX13] I. Cialenco and L. Xu. Hypothesis testing for stochastic PDEs driven by additive noise. Preprint http://arxiv.org/abs/1308.1900, 2013.

- [HKR93] M. Huebner, R. Khasminskii, and B. L. Rozovskii. Two examples of parameter estimation for stochastic partial differential equations. In Stochastic processes, pages 149–160. Springer, New York, 1993.

- [JK11] Arnulf Jentzen and Peter E. Kloeden. Taylor approximations for stochastic partial differential equations, volume 83 of CBMS-NSF Regional Conference Series in Applied Mathematics. Society for Industrial and Applied Mathematics (SIAM), Philadelphia, PA, 2011.

- [Kut04] Yu. A. Kutoyants. Statistical inference for ergodic diffusion processes. Springer Series in Statistics. Springer-Verlag London Ltd., London, 2004.

- [Lin99] Y. N. Lin′kov. Large deviation theorems for extended random variables and some applications. In Proceedings of the 18th Seminar on Stability Problems for Stochastic Models, Part III (Hajdúszoboszló, 1997), volume 93, pages 563–573, 1999.

- [Lot09] S. V. Lototsky. Statistical inference for stochastic parabolic equations: a spectral approach. Publ. Mat., 53(1):3–45, 2009.