Optimal Trading Strategies as Measures of Market Disequilibrium

Abstract

For classification of the high frequency trading quantities, waiting times, price increments within and between sessions are referred to as the a-, b-, and c-increments. Statistics of the a-b-c-increments are computed for the Time & Sales records posted by the Chicago Mercantile Exchange Group for the futures traded on Globex. The Weibull, Kumaraswamy, Riemann and Hurwitz Zeta, parabolic, Zipf-Mandelbrot distributions are tested for the a- and b-increments. A discrete version of the Fisher-Tippett distribution is suggested for approximating the extreme b-increments. Kolmogorov and Uspenskii classification of stochastic, typical, and chaotic random sequences is reviewed with regard to the futures price limits. Non-parametric and log-likelihood tests are applied to check dependencies between the a- and b-increments. The maximum profit strategies and optimal trading elements are suggested as measures of frequency and magnitude of the market offers and disequilibrium. Empirical cumulative distribution functions of optimal profits are reported. A few classical papers are reviewed with more details in order to trace the origin and foundation of modern finance.

1 Introduction

In financial economy theories equilibrium plays an important role. William Sharpe defines: "…a financial economy is in equilibrium when no further trades can be made" [203, p. 9]. He adds: "But of course in the real world trading seldom stops, and when it does stop, it is typically because low-cost markets are temporary closed. The implication is that financial markets never really reach a state of equilibrium. … In actuality, people make trades to move toward an equilibrium target but the target is constantly changing. Despite this completely valid observation, we need to understand the properties of a condition of equilibrium in financial markets, because markets will usually be headed toward such a position." Solving the task, Sharpe deviates from the mean/variance approach associated with the Modern Portfolio Theory of Harry Markowitz [152] and his own Capital Asset Pricing Model [202] and applies the state/preference method originated in the works of Kenneth Arrow [10] and Gerard Debreu [35].

In contrast to the task "to understand the properties of a condition of equilibrium", this article concentrates on the "complement", the non-equilibrium market state, considering it as an essential condition of the speculative market existence. If the non-equilibrium state is "people making trades", then it can be expressed in terms of trading. How?

The market equilibrium associates with the perfect distribution of information about the "equilibrium target" between the market participants, although Sharpe suggests that the "target is constantly changing". This view on the equilibrium leads to another deep notion - the efficient market hypothesis, EMH, developed by Eugene Fama [50], [51], [52], [53]. The market is efficient but speculators continue trading. Why?

Many speculators hardly know about moving "toward an equilibrium". Their striving for making money is so strong that the assortment of means supporting their decisions stretches from science to astrology. The market must have an objective property "explaining" such an aspiration. Ideally, it should be measurable. There must exist something. What?

Twenty years ago the author had to stop the research in analytical and computational chemistry, molecular dynamics and Monte-Carlo simulation of liquid phases and plunged into the world of markets, trading futures, stochastic processes, and models for pricing derivative instruments. He has found markets not less challenging. Coming from a society, where speculation of American jeans could result in a jail term and exchange of substantial amounts of rubles to a foreign currency in a death penalty, the Rokotov-Faibishenko case, the author was pleasantly astonished at the "lower FOREX transaction costs". "Things Have Changed". The English "f-u-t-u-r-e-s" is a frequent word in Russian TV News. This article summarizes the journey and presents the author’s answers, prompted by the market, on the questions: How, Why, and What.

The speculative markets, "the front lines of capitalism" [167, p. 7], are the areas of "cooperation between human consciousness and technology governed by partly unknown laws of nature" [192, p. 34]. Ignoring that electronic markets involve people and programs created by people and programs "bred" by programs [113] created by people is a costly trading experiment. Daniel Kahneman and Amos Tversky [88] [220] show us that a person knowing about mathematical expectations still may act against this knowledge, demonstrating the "risk aversion" and "reflection effect". Comparing their research with notes written by Jesse Livermore, an outstanding speculator [135, pp. 11 - 13], the author has made a "small discovery". Livermore describes a $2 profit per share taken without a risk in a fear to lose it. He also illustrates holding a position already losing $2 per share in a hope of a price reversion. This is a foresight of the risk aversion and reflection effect. An intuition built during 40 years by large-scale speculation accompanied by making and losing fortunes caught an idea of a remarkable scientific achievement 39 years earlier. Human beings tend to set targets "unexpected mathematically". Can this make equilibrium an exception but non-equilibrium properties a norm? A measure is needed.

George Soros, a large market practitioner and philosopher, designs the Theory of Reflexivity [211]. It emphasizes essential interference of the cognitive function aiming to bring the knowledge about our world and the participating or manipulative or executive function changing it. He demonstrates that markets are full of reflexive situations and sees this as one of the reasons, why they deviate from equilibrium. This qualitative paradigm could also benefit employing a measure of the frequency and magnitude of the reflexive situations.

The electronic markets, "ultra-high-frequency" coined by Robert Engle [48], unknown proportion of computer programs making trading decisions and hidden principals embedded into them complicate matters but do not give signs that speculation will cease to exist. It seems that the means distributing information about the "targets" faster also change the latter more frequently.

2 Inalienable Property of a Speculative Market

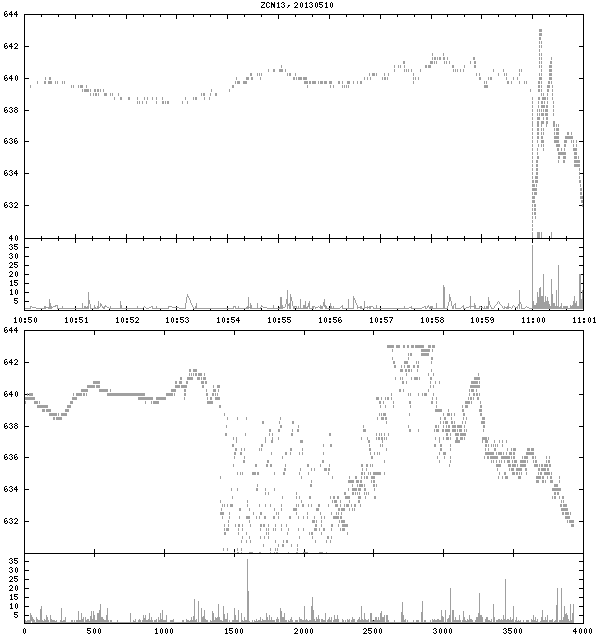

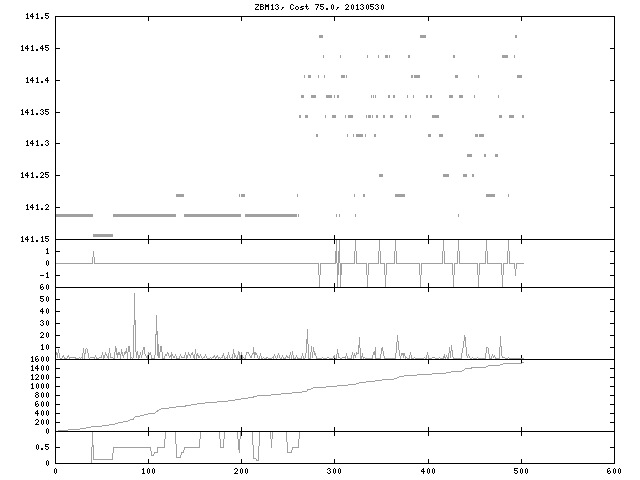

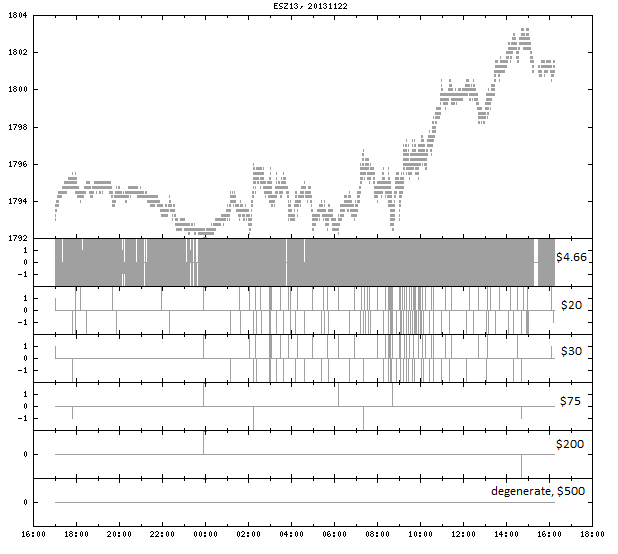

The market property to provide frequent opportunities to make large profits is discussed as an essential condition of its existence and the main law of the speculative market in the section "Why we speculate" of [193] and [194, p. 31]. If the term law will find a use, then it should be recognized as phenomenological: it is not deductively derived from other postulates, it is confirmed only by market data, it does not explain why the market posses such properties. A market is people and programs trading something. This activity is reflected by transactions occurred in time, at a certain price and number of contracts or shares. A market can "sleep" but not long. Sometimes it "explodes", Figure 1. Studying millions of transactions, the author did not find exceptions, contracts with horizontal lines of price vs. time, and started thinking towards the terms "regularity" or "law" instead of "hypothesis" in order to denote the phenomenon.

Such a regularity is in opposition to approaches intentionally or unintentionally dismissing these properties. Accounting the large number of market data supporting the regularity, the opposite approaches should be reviewed for correctness.

Even, being formulated as a law, this property does not provide a way to extract potential profits but supplies the maximum profit strategy framework, as we shall see, to search for such a way.

The qualitative formulation, "markets provide frequent opportunities to make large profits", is intuitively known to traders. Naming it the law intents to increase the confidence: these properties pass away only with a market. The law becomes quantitative after adding the measure - the maximum profit strategy, MPS. It answers on "how frequently" and "how large". For futures, a MPS can be constructed using the l- (left) and r-(right)algorithms [190], given chains of prices and transaction costs, margins, and accounting rules. This law is expressed not by an equation but algorithm. The latter circumstance is interesting with regard to the three modern definitions of randomness, each also based on the theory of algorithms [109].

The market offers profit opportunities in a view of the optimal trading elements, OTE. This term is coined in [193] and [194].

The law, based on MPS - an objective market property, relates to a human being activity. It has no status of physical laws: socialist revolutions or meteorites can delete the free markets from the face of the Earth and terminate trading, while the Newton’s laws will continue working.

3 A Comment on Equilibrium

A ping-pong ball hanging from a vertical thread is in equilibrium. The same ball balancing on a top of a vertical needle is in equilibrium too. The first equilibrium is stable. After displacement, the sum of gravitation, reaction (caused by tension), and friction forces decreases to zero and returns the ball to the initial state. The second equilibrium is unstable. After displacement, the sum of the same three types of forces increases up to a constant taking the ball away of the initial position. The same forces play an opposite role. Studying the two equilibrium states reveals the zero sum of the two vectors: the gravitation and reaction forces. If a reader feels uncomfortable comparing the thread tension with the needle reaction, then the author suggests to replace the first example with a tall wine glass and a pea on its bottom. To "understand the properties of a condition of equilibrium" is important, however, being identical in both cases they do not explains a very different behavior of the ball after displacement. The change and distribution of forces after displacement is crucial.

The word change was popular during the fall of 2008 in U.S. election TV News. The changes but not only absolute values are important for anticipation of a behavior involving human beings. In his Nobel Prize lecture [89, p. 460] Daniel Kahneman presents an example, where a person holds the left and right hands in two different buckets with cold and hot water and later places them in a bucket with tepid water. The judgment about the same temperature depends on the hand.

Two husbands talk about the third one. "His wife made him a millionaire." "A lucky man!" "No, before he was a billionaire." A trader left with $100,000 judges differently about the trade after $110,000 - $10,000 loss or $90,000 + $10,000 gain, although the final state, money, is the same.

These examples demonstrate unstable and stable equilibrium and importance of studying transitions together with the states. A market consisting of the stable equilibrium states only would not guarantee simplicity.

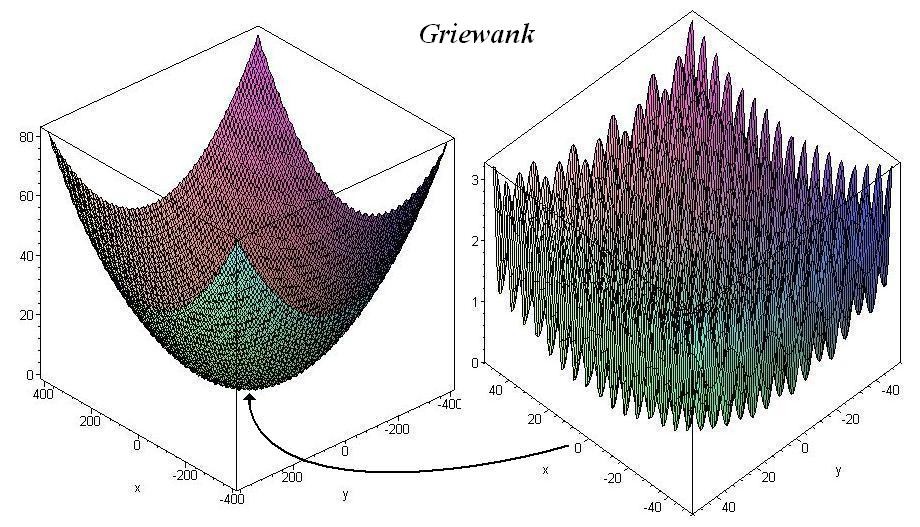

A steepest-descent solver [173, pp. 21, 22] starting from different points stably finds the minimum of the elliptic paraboloid . The mechanism resembles a pea rolling down to the bottom of a tall wine glass. However, the Griewank’s surface [74] traps the pea in one of the local minimums. The Mars Rover Curiosity’s mission would end after landing on the surface on Figure 2. A pea would need activation energy to overcome barriers, explore the surface, and reach the lowest point. The local minimums in smooth and convex areas mimic stable equilibrium states. Participants, trading on a market, consisting of such states only, would need enough activation energy in order to reach the most optimal equilibrium state, and analysts would need to find its source and mechanism. Let us notice that a differential evolution solver [214] combining directional moves with random selection, a kind of "diffusion tunneling" through the barriers, routinely finds the right answer.

4 A Comment on Surviving Systems

Nikita Moiseev, a mathematician widely known due to computer simulation of the "nuclear winter" - a consequence of a global nuclear war, applies the term homeostasis [165, p. 140]. It is a region of critical values of parameters that a system must not exceed in order not to be destroyed. A surviving system aims at the center of the region far from the dangerous boundary. This principal, combining monitoring of the distance from the boundary, a feedback, and adjustment of the parameters affecting the work of the system, leads to autopilots and missiles autonomously navigating to targets. A trading system enriched by money management rules and adopting its behavior to varying market and portfolio conditions would not be an exception.

At first glance, this principal contradicts to heroic life sacrifices on a battle field, when a solder closes an embrasure, dies, but his comrades using the moment win the battle. Surviving is ignored. A hierarchy seems save the principal. A higher level system, ideologically cultivating (in a good, patriotic sense) people, follows to the goal of surviving sacrificing its subsystems. The principal on the higher level overrides its violation on the lower one.

In the Immortal Game of chess played on June 21, 1851 in London, Adolf Anderssen sequentially sacrificed to Lionel Kieseritsky pawn (by definition in King’s Gambit), Bishop, second pawn, Rook, second Rook, Queen, and won on 23d move by Bd6-e7 (checkmate) [216, p. 291 - 293, game 227]. In chess, sacrifices impress. In life, they are tragedies suddenly supporting the principal.

A speculative market proposes prices, redistributes risk, intensifies cash flows. It does not create a treasure but redistributes it paying a part to the brokers, analysts, and information technologists. For traders, risking their and others’ capital, this is not a zero-sum game. In order to win, somebody must lose. Alexander Elder comments [47, p. 49]: "Trading means trying to rob other people while they are trying to rob you. It is a hard business." His provoking definition is [47, p. 44]: "Price is what the greater fool is ready to pay." The market needs frequent transactions offering attractive potential profits. Interest drives speculation more than a fear of losses. However, the latter are the only source of the real profits. The hierarchical principal seems justify partial financial disasters. What is death for a few hedge funds is life for the market, coming out as a steak house with exotic dish names such as Long-Term Capital Management, Tiger Management Corp., Basis Yield Alpha Fund, Sowood Capital, Lehman Brothers Holdings Inc., where the Nobel Prize does not guarantee a seat. The seat can be on a frying-pan. This creates enormous stress.

5 A Comment on Attractors and Fractals

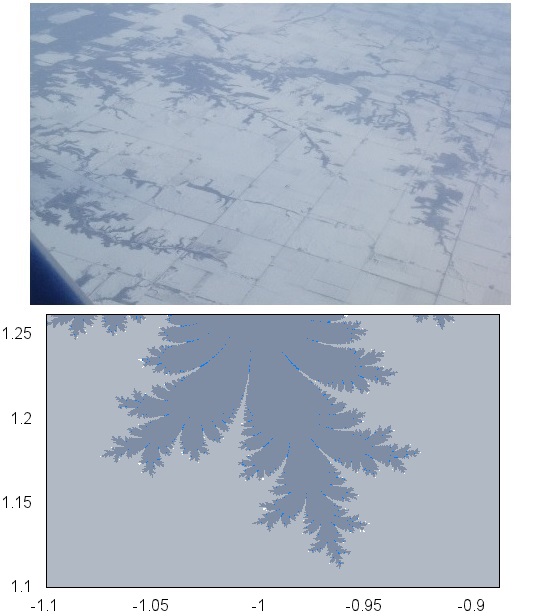

If we place the stable and unstable equilibrium of the ping-pong ball on the left side of a complexity axis and hypothetical equilibrium and non-equilibrium market states and transitions on the right side labeled by greater values, then the middle is ready for: the origin of the theory of chaos contained in celestial mechanics of Henri Poincare [179] [7, pp. 4 - 7], the theory of stability from Alexandr Lyapunov [140], the theory of rings of operators from John von Neumann [170] [171] [43, pp. 69 - 70] [207, pp. 2 - 3], the 1940th works of Andrey Kolmogorov on fluid dynamics [6, pp. 29 - 33] and his "first seeds in chaos theory" [102] [104] [207, p. 2], the entropy of dynamical systems from Yakov Sinai [206] [207], the Arnold diffusion [8, pp. 67 - 70] [207, p. 5] having its roots in the work of Alexandr Andronov, Lev Pontryagin, and Alexandr Vitt in 1930th [8, pp. 68], the contributions of Vladimir Arnold into unstable dynamical systems [4], the theorem of Olexander (Alexander) Sharkovsky [201] [164], the term chaos coined by Yorke [129] [159], the chain reactions from Nikolay Semenov [199] (coming to mind after examining Figure 1), the non-equilibrium processes from Ilya Prigogine [180] [181], the discovery of a strange attractor by Edvard Lorenz [136], the discovery of universality of period-doubling bifurcations by Mitchell Feigenbaum [55], the world of fractals presented by Benoit Mandelbrot [146, p. 402] [148] and surrounding us Figures 3, 4, the smooth ergodic theory from Yakov Pesin [178] providing strong links to the differential dynamical systems from Stephen Smale and Anosov systems from Dmitri Anosov, varieties of billiards [230], [219], the linear search problem [14]. The author was impressed how Grigory Galperin forces the billiard trajectories to count 50,000,000 of the decimal digits of [61] and to measure distances in the hyperbolic Lobachevsky’s space [62]. The human being consciousness shifts the markets to the right but inheritance from the middle is likely. Increasing complexity does not seem throw out but accumulates simple rules of the lower levels [70], [243]. It creates new regularities and laws on a higher level, otherwise, as it is wittily noticed by Nigel Goldenfeld and Leo Kadanoff: "In order to model a bulldozer, we would need to be careful to model its constituent quarks!" The author recognizes that "there are a number of glaring omissions in this" list [207, p. 5].

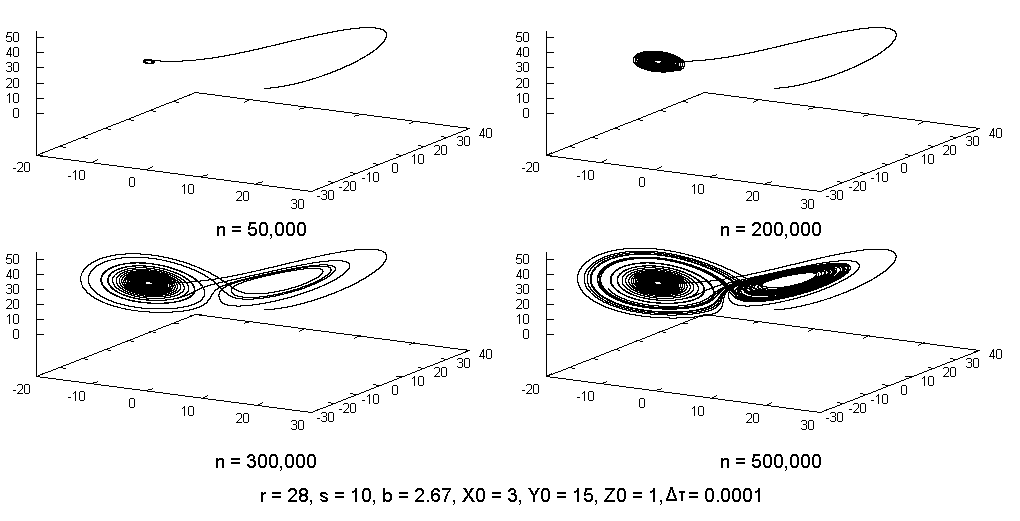

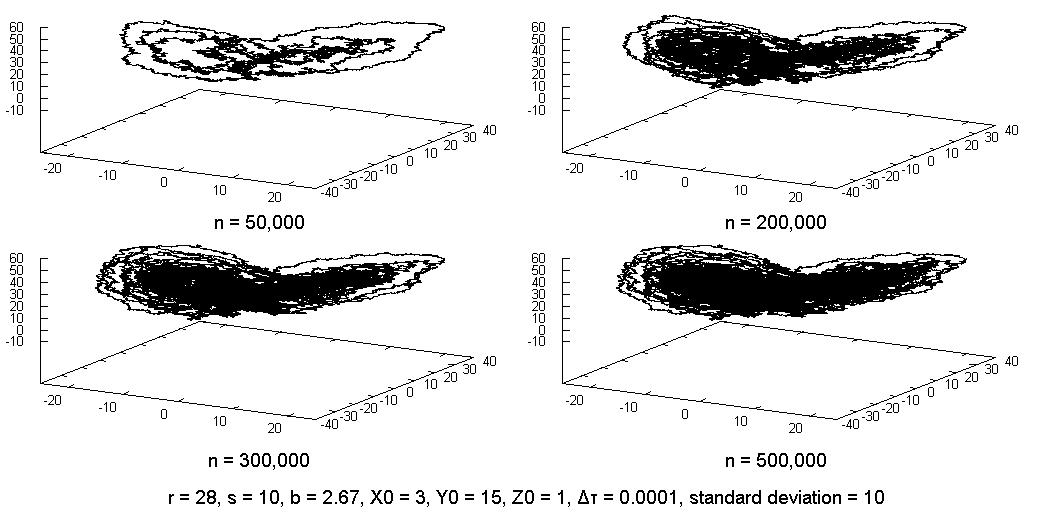

Let us check the influence of "diffusion of the phase coordinates" on a phase trajectory in a system with attractors. After modification of the model of Barry Saltzman [197], Lorenz [136] has come to the system of three ordinary differential equations named after him today

where and are positive constants, and is a dimensionless time. The solution is a phase trajectory , where and define a 3D phase space of a layer of fluid of uniform depth between two surfaces maintained at two different temperatures. Depending on the conditions and Rayleigh number the liquid remains steady or gets in motion, convection. is proportional to the intensity of the convection, is proportional to the temperature difference between the ascending and descending currents, and is proportional to distortion of the vertical temperature profile from linearity. These should not be mixed with a configuration space of liquid parts. The author has determined the iteral expression [195, p. 10] for the Lorenz’s double-approximation procedure [136, pp. 133 - 134] and written a C++ program outputting phase coordinates triplets to the graphics package Gnuplot [67]. Figure 5 applies instead of .

The Lorenz’s phase trajectory or orbit has no fixed points. It is non-periodic and does not intersect itself. Its future does not repeat its past. The bottom picture is obtained after adding to on each iteration the term . The number is drawn from the standard (mean 0, variance 1) Gaussian random generator reusing the Box-Muller algorithm [24]. Presence of diffusion speeds up filling of the phase space. Now, during the same 50,000 time steps the system has time to explore both attractors. This behavior, indeed, "correlates" with the qualitative picture predicted by Arnold in [8, p. 68], where he introduces the terms attractor force, attractor pull, and tunneling effect. We should also remember the robust differential evolution solver from a previous section, where random selection is crucial for finding the minimum of the Griewank function. This experiment shows that randomness from a continuous distribution theoretically can place an originally non-periodic chaotic system into a state, which it already had. From such a state and for a while the future trajectory could repeat the past one, especially, if randomness is suppressed after the impact.

6 The Data

The Chicago Mercantile Exchange, CME, Group publishes daily, after a market is closed, on the homepage http://www.cmegroup.com/ the Time & Sales tables for futures listed on CME, the Chicago Board of Trade, CBT, the New York Mercantile Exchange, NYMEX, and some other traded open outcry (pit) and electronically on Globex. A table is a chain of records containing date, time, price, indicator for pit and date, time, price, size, indicator for electronic sessions. The date is the same for all records belonging to one session, although the latter can last in two calendar dates. The time is accurate to one second. The price quotes follow to the contract specifications and may require conversion to decimal numbers. The size, available only for electronic sessions, is a positive number of traded contracts for transactions and zero for other types of prices. The indicator is a price type such as ’-’ used for transactions, indicative, open, close, ask, bid, settlement and other. Pit sessions omit size and majority of transactions occurred at the same price in a row. This creates snake tongue histograms of the price increments with almost "missed" zeros, the center.

A contract ticker consists of the product name, expiration month and year. The months are F - January, G - February, H - March, J - April, K - May, M - June, N - July, Q - August, U - September, V - October, X - November, and Z - December. For the same commodity, product names may differ for the Globex and pit like ZC and C for corn contracts. Some brokerage companies list such pairs under one ticker. Durations of electronic sessions typically overlap the pit and include nights. This supports people preferring trading to sleeping and not important for trading computer robots. This report is mainly based on Globex transactions, Table 6. Consult with brokers and review for details contracts specifications available on the CME Group homepage.

Some Properties of Futures Traded on Globex/Open Outcry Symbol Commodity Exchange Months Tick =$ ZB/US U.S. Treasury Bond CBT HMUZ 0.03125=$31.25 ZC/C Corn CBT HKNUZ 0.25=$12.50 ZS/S Soybean CBT FHKNQUX 0.25=$12.50 ZW/W Wheat CBT HKNUZ 0.25=$12.50 6A/AD AUD/USD CME HMUZ 0.0001=$10.00 6B/BP GBP/USD CME HMUZ 0.0001=$6.25 6C/CD CAD/USD CME HMUZ 0.0001=$10.00 6E/EC EUR/USD CME HMUZ 0.0001=$12.50 6J/JY JPY/USD CME HMUZ 0.0001=$12.50 ES E-mini S&P 500 CME HMUZ 0.25=$12.50 GE/ED Eurodollar CME All 0.0025=$6.25 LE/LC Live Cattle CME GJMQVZ 0.025=$10.00 HE/LH Lean Hogs CME GJKMQVZ 0.025=$10.00 CL Light Sweet Crude Oil NYMEX All 0.01=$10.00 GC Gold COMEX All 0.1=$10.00 HG Copper COMEX All 0.0005=$12.50 NG Natural Gas NYMEX All 0.001=$10.00 SI Silver COMEX FHKNUZ 0.005=$25.00

Due to the high frequency of transactions and limited accuracy of time, records may get one time, where only arriving order defines the chain. The lack of accuracy creates vertical zig-zags in plots of prices vs. time. Plotting the price against the index of a record assists but separates ticks by artificial constant waiting times. On Figure 1, one second at 11:00:00 AM CT is responsible for 806 transactions with accumulated volume of 1166 contracts and prices from the range [630.00, 638.75]. The , Table 1, gives the dollar equivalent of the range before fees and commissions, which could be $10.66 per contract per round trip.

While the words of Sir Maurice Kendall "the golden rule in publishing work on time-series is to give the original data" remain imperative, it is difficult to follow them in a paper on high frequency data 60 years later [93]. DVDs can accompany a book but not an article. Only the 57 sessions of ESM13 collected between March 1 and May 22, 2013 (Wednesday March 27, 2013 is missed) contain 21,364,635 records totaling 835,401,602 bytes in files like ESM13_20130522.txt:

... 2013-05-22 08:33:21.000-06 1669.25 6 T 2013-05-22 08:33:22.000-06 1669.25 1 T 2013-05-22 08:33:22.000-06 1669.25 1 T 2013-05-22 08:33:23.000-06 1669 34 T ...

This is 374,818 records per session. An ordinary ESM13 session lasts from 17:00:00 of one day until 15:15:00 of a next day, then 15 minutes pause, trading from 15:30:00 until 16:15:00, and the second pause until 17:00:00. With 23 hours, the mean number of records per second is . Transactions are distributed non-uniformly in time (compare the mean 4.5 with 806), Figure 1. There is some intraday seasonality of arrivals. The "time" will often mean the "date and time", where reserved milliseconds and time zone are marked as ".000-06" together with the 24 hours "HH:MM:SS" format.

7 The a-b-c-Process

The ultra-high-frequency futures transactions is a rich source of time-series. The Globex transactions are triplets of time, price, and volume. Such a triplet is called tick. This should not be mixed with the minimal absolute non-zero price fluctuation in Table 1. For classification, the author introduces a-b-c-increments, a-b-c-properties, and a-b-c-process.

7.1 Basic formulas

Each contract starts and expires at some date and time. No futures are traded 24/7. Time-series can be divided into sessions indexed by . The and a session date are in one-to-one correspondence. A th session contains transactions. The varies between sessions and contracts. Additional contract and date labels , can be helpful.

A th session may enclose several time ranges indexed by . During the contract life, their number, opening and closing times can change. The Globex ZCN13 was trading in one range 17:00:00 (previous date) - 14:00:00 (session date) CT before April 8, 2013 and in two ranges since April 8, 2013: 19:00:00 - 07:45:00 and 08:30:00 - 13:15:00 CT with the 45 minutes pause. The after Fourth of July 2013 holiday session, on July 5, 2013, had only one range 08:30:00 - 13:15:00 CT. If , then the range coincides with the enclosing session. The is the number of transactions within the th range of the th session and is the total per contract life number of transactions

| (1) |

The triplets are indexed by the intra-range . The and can be equal to zero. Contracts can be illiquid at the life beginning or expiration. The less liquid deferred months and years or expiring contracts coexist with the more liquid nearby or getting to become nearby contracts on the same commodity, supporting the Main Law. Futures can be delisted like the Frozen Pork Bellies on Monday July 18, 2011. The latter did not meet hedging needs and balance between hedgers and speculators. Contracts, which cannot frequently propose potential profits, die, confirming the Main Law - essential condition of the market existence. We shall deal mainly with cases .

The a- and b-increments are the differences between neighboring transaction times and prices within the -range of the -session

| (2) |

| (3) |

They are undefined for . Summing up the increments, the undefined quantities can be skipped. Replacing them by zeros would give the same sum but affect the sample statistics due to the increasing number of summands. A discretional approach may be needed for each indeterminate case.

The c-increments are the differences between the first price of a th session and the last price of a th session irrespectively on ranges

| (4) |

They are undefined for , , or . The c-increments over the pauses between regular sessions, weekends, and holidays are the cr-increments, cw-increments and ch-increments. The ci-increments (internal) are the differences between the first price of a th range and last price of a th range

| (5) |

They are undefined for , , or . If for all , then the second index can be dropped from Equations 1 - 3 and some other below. This is true for several futures. Thus, there is a family of c-increments.

The price b-increments and the family of c-increments are defined over different waiting times. The former associate with the a-increments. The latter correspond to the two a-like increments plus a known in advance, usually much longer than a-increments, time separating sessions and/or ranges.

The increments can be counted forward affecting initial and final index values

| (6) |

| (7) |

| (8) |

| (9) |

Forwarding does not change , determining whether the quantities are defined. The backward and forward b-increments have and c- have no lower index at . The c- and ci-increments have one and two upper indexes.

The time interval corresponding to a c-increment consists of a known interval between the current session opening and previous closing times plus two durations: between the current first tick time and and between and the previous last tick time, where

| (10) |

This can be written as the forward increment, where

| (11) |

The time intervals associated with the ci-increments for are

| (12) |

The corresponding forward time intervals for are

| (13) |

No names are introduced for the sums in Equations 10 - 13. The a1-increments are and . If and , then the a1-increment is included one time to a sample combining a1s from ranges and sessions. The a2-increments are and . If and , then the a2-increment is included one time to a sample combining a2s from ranges and sessions. The a1- and a2-increments are fractions of or . If but some , then a1- and/or a2-increments get ranges durations. The two a-like contributions remain intact. With 24/7 trading, the c-increments will become a history.

In contrast with classifications of time and price increments based on constant observation intervals, the a-b-c-increments associate with transactions and share the property: they are indecomposable - there are no ticks between neighbors. The a-b-c-increments measure the a-b-c-properties. The a-b-c-process evolves as following: a) the a-property determines the time fluctuation and, thus, the time of a next transaction within a range; b) the b-property determines the price fluctuation and the price of a next transaction within a range; and c) the c-property is responsible for the price change between the current range/session last and next range/session first prices and concatenates two neighboring ranges/sessions by price.

Any time or price within the th range of the th session is the algebraic sum of the a- or b-increments added to the first time or price

| (14) |

| (15) |

Conventionally, the sums vanish, when the iterating index is greater than the top value, for instance, if .

The time and price counted from the first contract transaction are

| (16) |

| (17) |

where, , , .

Equations 1 - 17 are exact, if each range has at least one tick. In Equation 17 the first price is added by the a) b-, ci-, and c-increments from all ranges and sessions prior the last requested th session, b) b- and ci-increments from all ranges prior the last requested th range from the last requested th session, and c) remaining b-increments up to the th one. The time Equation 16 is similar. The a-b-c-process, a strategy, liquidity, histograms of a-b-c-increments, price and volume distributions can be depicted, Figures 6, 7.

7.2 Two Shiryaev’s tasks

Describing financial ticks Albert Shiryaev [205, p. 379] formulates the two primary tasks (author’s translation from the Russian edition): (I) "What is the statistics of lengths of [VS: time] intervals between ticks; (II) What is the statistics of changes in prices [VS: between ticks] (in absolute … or … relative values)". The task (I) relates to the a-property and a-increments. The task (II) relates to the b-property and b-increments. Alfonso Dufour and Robert Engle [41, p. 2467] comment on the growing interest to such research: "The availability of large data sets on transaction data and powerful computational devices has generated a new wave of interest in market microstructure research and has opened new frontiers for the empirical investigation of its hypotheses", see the collection of articles [125].

8 The a-Increments

The a-increments are nonidentical stones building trading time. Globex transactions are caused by matching book orders. The a-b-c-process depends on the arriving orders, the book state, and the matching algorithms. If an order matches two others of smaller sizes in a queue, then two transactions are triggered with a CPU time between them. CPU instructions take nanoseconds. If the book is waiting an order, then the minimal time is determined by the order transfer. Latencies add. The 806 transactions during one second at 11:00:00 on Figure 1 being distributed uniformly would create the a-increment seconds. A non-uniformity shortens some. The sequential order processing implies non-zero a-increments. However, one second reporting inaccuracy creates an impression of discreteness and zeros.

8.1 One second inaccuracy

With the truncation [11:00:00, 11:00:01) 11:00:00, [11:00:01, 11:00:02) 11:00:01, for ticks with one time the a-increment seconds is set to zero. For 11:00:00, 11:00:01 it is set to one for seconds. For 11:00:00, 11:00:02 it is set to two for seconds. Ironically, 11:00.00.800, 11:00:01.100, 11:00.01.800 reported as 11:00:00, 11:00:01, 11:00:01 mismatch the a-increments 1 and 0 with differences 0.3 and 0.7 seconds. Rounding off time to a second has problems too: , , the a-increment 1 stays for 0.001 second. This "incorrectly reshapes" empirical distributions of a-increments at high liquidity and complicates their approximation by theoretical continuous distributions with zero probability density at zero. True zero a-increments require simultaneous transactions. Eventually, it can be implemented similar to parallel and multi-thread computer applications.

8.2 Irregular waiting times

Benoit Mandelbrot and Howard Taylor [144, p. 1057] write: "… the number of transactions in any time period is random …". Thus, durations between ticks are irregular. These authors, and Peter Clark [28] [29], are among the first researchers, who have emphasized the importance of this fact to finance. The random time comes out as a subordinator of the random price. The theory of subordinated processes is developed by Salomon Bochner [22]. High frequency trading presses on the tradition to collect prices at regular times. Charles Goodhart and Maureen O’Hara comment [68, pp. 80 - 81 and p. 74]:

Traditional studies of financial market behavior have relied on price observations drawn at fixed time intervals. This sampling pattern was perhaps dictated by the general view that, whatever drove security prices and returns, it probably did not vary significantly over short time intervals. Several developments in finance have changed this perception. … A fundamental property of high frequency data is that observations can occur at varying time intervals.

Transactions occur at irregular times independently on "observations". The observations at regular times would miss many ticks. Table LABEL:a-increments summarizes sample statistics of a-increments. Samples from time ranges within a session are treated separately and marked by 1 and 2 in the date column. They are also combined in one sample. The dates mark such aggregates and one range sessions.

8.3 The main regularities found

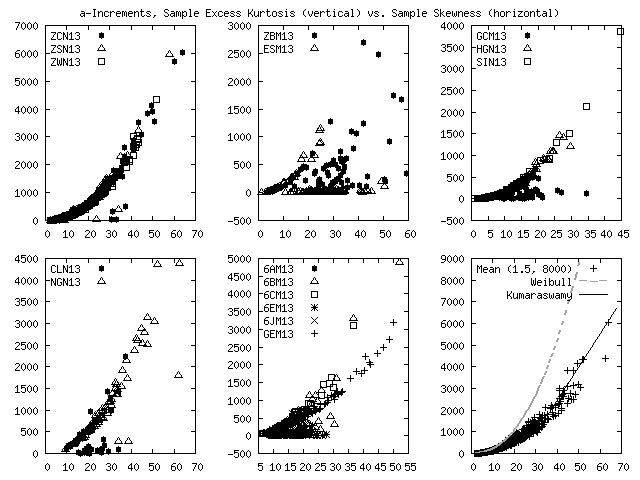

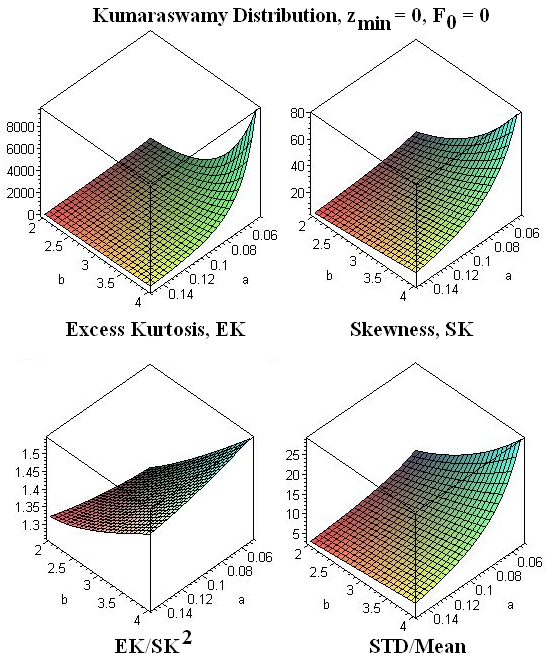

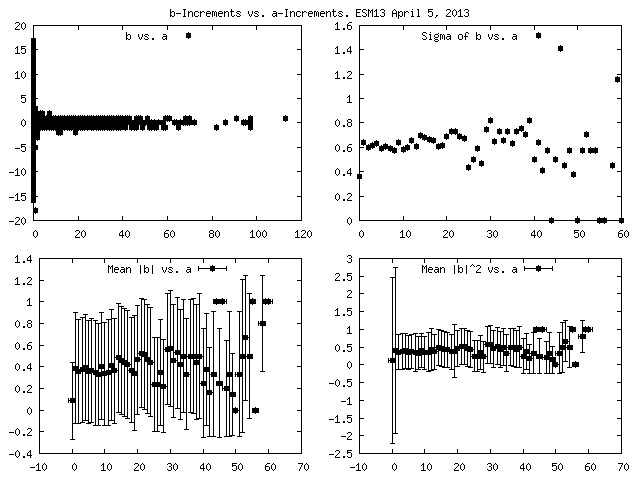

The author notices non-linear dependences between the sample excess kurtosis and skewness of the a-increments, Figure 8. The grains are the winners. It is interesting that points from ranges and aggregates belong to one curve. The four outliers for ZCN13 on April 29, 30 and May 13, 29, 2013 correspond to the mean . For liquid contracts, the time inaccuracy badly affects the statistics. The two outliers for ZSN13 on May 21 and 23, 2013 confirm it too. The mean a-increments of the ZBM13 and ESM13 are less than a second in many sessions, Table LABEL:a-increments. Conclusions about time differences would be suspicious for them. Other "clusters" sympathize with grains. The right bottom plot on Figure 8 combines 991 entries with the 1.5 < mean < 8000. It resembles a known dependence between the Weibull’s kurtosis and skewness [188]. The points from lines "ALL" deviate and are excluded.

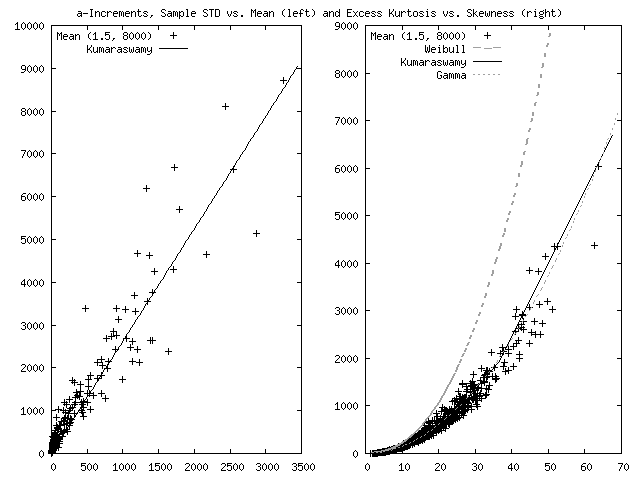

For the same 991 entires the standard deviations and means correlate with the coefficient of correlation 0.957, slope 2.65, and intercept 54.2, Figure 9.

The sum of all a-increments in a range is close to its duration promoting a hyperbolic curve: mean vs. . Short pre-holiday and last trading day ranges and sessions create outliers. Noise is larger for less liquid sessions, where the a1- and a2-increments become comparable with the range duration, Figure 10.

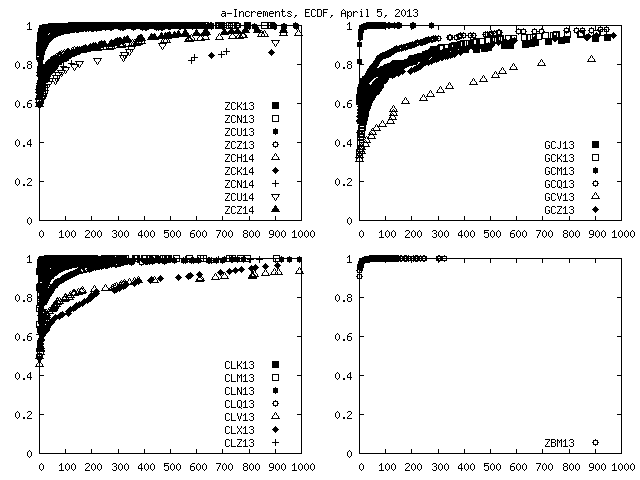

A histogram of a-increments, Figure 7, can be converted into the empirical cumulative distribution function, ECDF, Figure 11. A cumulative distribution function, CDF, is a full characteristic of a probability distribution. Kolmogorov [100] defines: "Let be mutually independent random variables following the same distribution law … Put where denotes the number of those ’s who’s observed values do not exceed ". is CDF. is ECDF. This definition implies counting repetitions. The one second inaccuracy is conductive to them. Thus, for the sorted chain the author builds ECDF as (value, probability): . Kolmogorov’s definition makes computing ECDF, the pairs, straight forward. But is the probability to get a value equal to 0.6 or 0.7? Boris Gnedenko [66, p. 201] clarifies: for a sample sorted in the ascending order the ECDF is

| (18) |

This does not assume repetitions but being applied to our example leads to the inequalities: . Thus, the ECDF used is left continuous. It is a consistent estimator uniformly converging over to a CDF with (the Glivenko-Cantelli main theorem of statistics [66, pp. 201 - 207]). Equation 18 adjusted for repetitions is applied for computing points on Figure 11.

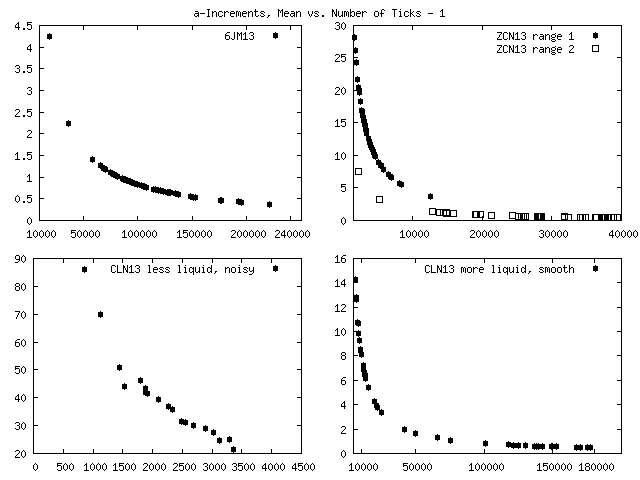

The means in A1-ALL and A2-ALL in Table LABEL:a-increments are often greater than in A-ALL, while individual a2s and especially a1s are frequently zeros in ranges and sessions: transactions arrive during the first and last second. Each studied session has one or two ranges giving one or two a1s and a2s found big for illiquid contracts. In contrast, the numbers of a-increments are usually greater than two. A single illiquid "outlier" affects stronger a1 and a2 than a-increments statistics. Let us consider two sessions with one range , , and uniform distributions of ticks: and . The mean a-increment is . The mean a1 and a2 are but . The 157 ZCN13’s a1s consist of 153 zeros, 13, 916, 60, and 30 seconds. In the range opened on July 7, 2013 at 19:00:00 CT, the first transaction had arrived at 19:15:16 creating a1 = 916. The mean 6.4904 is greater than the mean a-increment 2.1373.

9 A Comment on the Weibull Distribution

It is suggested [41, pp. 2475 - 2476] that the Weibull distribution is a "plausible assumption" for describing durations between transactions: "The Weibull distribution is to be preferred if the data show overdispersion with extreme values (very short and long durations) more likely than the exponential would predict." The exponential distribution with the constant skewness 2 and excess kurtosis 6 is unsound for the author due to Figure 8.

Waloddi Weibull proposed in 1939 a statistical distribution [235] named after him since 1951 [236]. Nancy Mann suggests [151] that it is similar to the Fisher-Tippett Type III distribution [59]. The Weibull’s three parameters CDF is

| (19) |

where, is the location or threshold, is the scale, and is the shape or modulus. Differentiating by gives the probability density function, PDF,

| (20) |

CDF and PDF are set to zero for . Setting gives the Rosin-Rammler equation [187] [236, discussion 1952]. The distribution mean can be derived using the substitutions , , and the properties of the Euler integral of the second kind, the Gamma function, for real [34] [111] , ,

| (21) |

With the , Equations 20, 21, and Newton’s binomial , where [111], we get the th central moment (about the mean)

| (22) |

These moments do not depend on . The variance, , is equal to

| (23) |

The ratio does not depend on . Thus,

| (24) |

| (25) |

depend on only and m-parametrically each on other. The Lanczos’s approximations [117] are sufficient for the Gamma function computation. Equations 24 and 25 are applied to plot the Weibull curve on Figure 8. It resembles the data but experiences a systematic shift up increasing with the skewness.

10 A Comment on the Kumaraswamy Distributions

Conducting hydrologic research, Ponnambolam Kumaraswamy has invented three probability distributions [114] - [116]. One [116] for is

| (26) |

where , . is cumulative probability of . Differentiating with respect to gives the PDF

| (27) |

This differs from the original [116, p. 81, Equation 3] by the factor . In fact, Kumaraswamy differentiates with respect to instead of the promised and . The should be taken care because but not one. The beginning th moment can be expressed as

where the last integral is zero but the first is accounting the probability mass (not density) at . With and the Kumaraswamy’s ,

The Newton’s binomial is applied. If , then

The right integral is the Euler integral of the first kind, the Beta-function, [111]

Finally,

| (28) |

Since [111], the and the mean, , is

| (29) |

With and the mass at , the th central moment is

Finally,

| (30) |

| (31) |

| (32) |

| (33) |

The skewness is . The excess kurtosis is . The holds.

On histograms of a-increments the highest bar is often at zero, Figure 7. A PDF can approximate it. For , Equation 27 gives at , where Equation 26 returns suitable for ECDFs on Figure 11. However, zero times between transactions is likely a consequence of the one second inaccuracy.

Alternative is to apply theoretically natural and fit the heights of the bars by the integrals of the PDF, Equation 27, on some intervals. We can use (a-increment, [integration interval]): or and the PDF

| (34) |

where can be greater than . If a simulated a-increment being added to the current time exceeds the range/session closing time, then no transaction is completed and trading terminates until a new range/session. Using as the Kumaraswamy’s bound would never stop trading because any a-increment will fit within the remaining time interval. This would lead to a-increments decreasing closer to the end but not observed.

The leave three degrees of freedom . The parametric curve of the excess kurtosis vs. skewness using , and arbitrary fits the data, Figure 8. The related equations are

| (35) |

| (36) |

| (37) |

| (38) |

Now, the skewness, excess kurtosis, and do not depend on . We can choose and to fit the sample skewness and excess kurtosis and to adjust the mean and variance depending linearly and quadratically on . This is useful, since the standard deviation and mean linearly correlate. The theoretical excess kurtosis and skewness within and support the experimental dependence , keeping the ratio within [1.30, 1.55], Figure 12. The theoretical ratio of the standard deviation to the mean [2, 25] is less supportive for the experimental slope 2.65, Figure 9. Fitting the excess kurtosis and skewness varying and and then reusing and to fit the mean and standard deviation changing works for many entries in Table LABEL:a-increments. Table 10 is an illustration, where rows with date are self-explanatory and rows "Theory" contain the ticker in column , the sum of relative errors taken by absolute value for skewness and excess kurtosis in column , and the sum of relative errors taken by absolute value for mean and standard deviation in column . These two sums of relative errors have been minimized in two steps using the Microsoft Excel Solver and the GAMMALN for expansion of the Beta function. With these cost functions the three parameters Kumaraswamy distribution describes better the skewness and excess kurtosis than mean and standard deviation. Reproduction of the four sample moments with relative errors from 0.3% to 37% is satisfactory for many purposes.

a-Increments. Sample and Computed Kumaraswamy Moments. Date 2013-03-01 7.3041 45.495 13.4 234.2 0.08021 2.565 1642.2 Theory 6.4605 45.495 13.4 234.2 ZCN13 0.35% 12% 2013-03-04 5.6324 58.506 41.1 2559 0.06680 3.807 10317.7 Theory 3.5658 58.506 41.4 2559 ZCN13 0.66% 37% 2013-04-05 3.4886 29.191 19.4 493.6 0.1179 4.016 2105.7 Theory 3.4886 26.754 18.3 493.6 ZCN13 5.6% 8.3% 2013-06-17 15.213 56.331 9.66 152.6 0.06680 3.807 10317.7 Theory 12.091 56.331 10.3 152.6 ZCN13 6.6% 21%

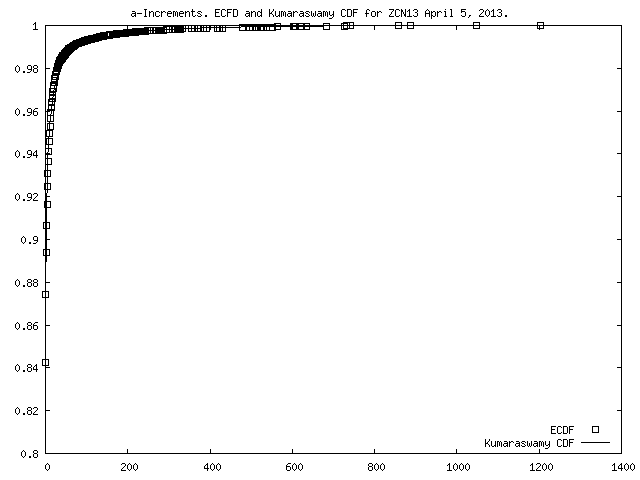

A general method for estimating distribution parameters based on fitting an ECDF by a CDF is suggested by Weibull [237]. The method of moments applied here can provide an initial guess for a solver. Figure 13 plots the CDF, Equation 26, together with ECDF, Equation 18.

a-Increments. The -Test. ZCN13, April 5, 2013, . Class 1 0 16 0.9639 20890 20886.6 0.0005438 2 16 135 0.03041 667 658.99 0.09727 3 135 260 0.003513 60 76.126 3.416 4 260 390 0.001199 22 25.976 0.6087 5 390 610 0.0006975 20 15.116 1.578 6 610 732 0.0001485 6 3.2185 2.404 7 732 1203 0.0001659 5 3.595 0.5492 Sum 21670 21669.7 8.653

Each class has at least five observations . With one second inaccuracy, it was difficult to follow to the Mann-Wald technique choosing classes [150], [239] and requiring to divide one second interval of the highest probability. With three parameters the number of degrees of freedom is . The probabilities are computed by Equation 26 using , , from Table 10 for 2013-04-05 and . The tabulated values for the levels 0.05, 0.02, 0.01, and 0.001 and are 7.815, 9.837, 11.341, and 16.268 [111]. The observed value is 8.653. The Kumaraswamy distribution hypothesis cannot be rejected. It is perspective for fitting the sample statistics of a-increments.

11 A Comment on the Gamma Distribution

12 The b-Increments

The b-increments are nonidentical stones building price, Table LABEL:b-increments.

12.1 Discreteness of prices and their increments

Futures prices are conventionally discrete. A ZBM13 price can be 140.00000 and 140.03125 but not between them. The dollar equivalent of 0.03125 is $31.25 - a lunch. Tom Baldwin, a trader, was known for trading 6,000 bond futures per day in 1980th [15, p. 321]. A 2,000 contracts position fluctuates $62,500 with each -tick. The large positions and high leverage do not allow ignoring price discreteness

| (39) |

The ratios of prices or b-increments are rational numbers common in accounting. To recollect it, try to withdraw exactly dollars from a bank. The asset return is the difference of the logarithms of integers. A theory is wrong, if it suggests that Probability. Discrete or lattice distributions are suitable for b-increments.

The words "God made the integers; all the rest is the work of man" are ascribed to Leopold Kronecker. Modern finance is carried away by using continuous price models and distributions starting from the Gaussian one. In contrast, the author is more impressed by the following Kolmogorov’s thought: "It is very likely, that with development of modern computational technology it will be understood that in many cases it is wise to study real phenomena avoiding intermediate stage of their stylization in the spirit of mathematical conceptions of infinite and continuous, moving directly to discrete models" [108].

12.2 Almost zero mean b-increments

Even, when the difference between the last and first price in a range is substantial, the number of ticks is so big, that the mean

| (40) |

is close to zero. The imbalance between negative and positive b-increments in a range or session exists on the background of their large total number including zeros. This keeps skewness small too. However, the distribution is not a Gaussian bell not only because it is essentially discrete but due to the non-zero sample excess kurtosis, Table LABEL:b-increments.

12.3 Futures limit prices

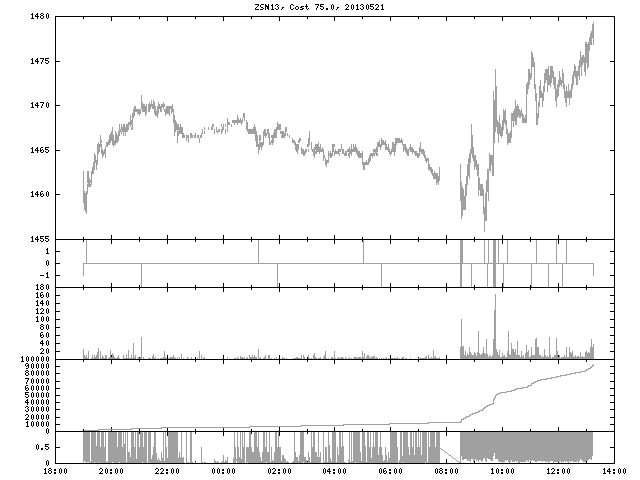

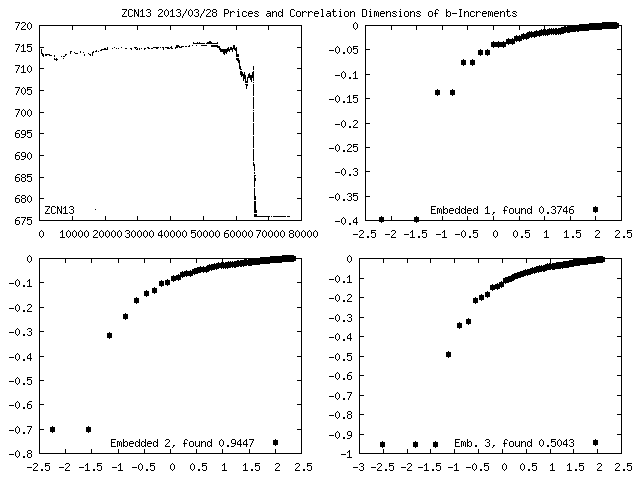

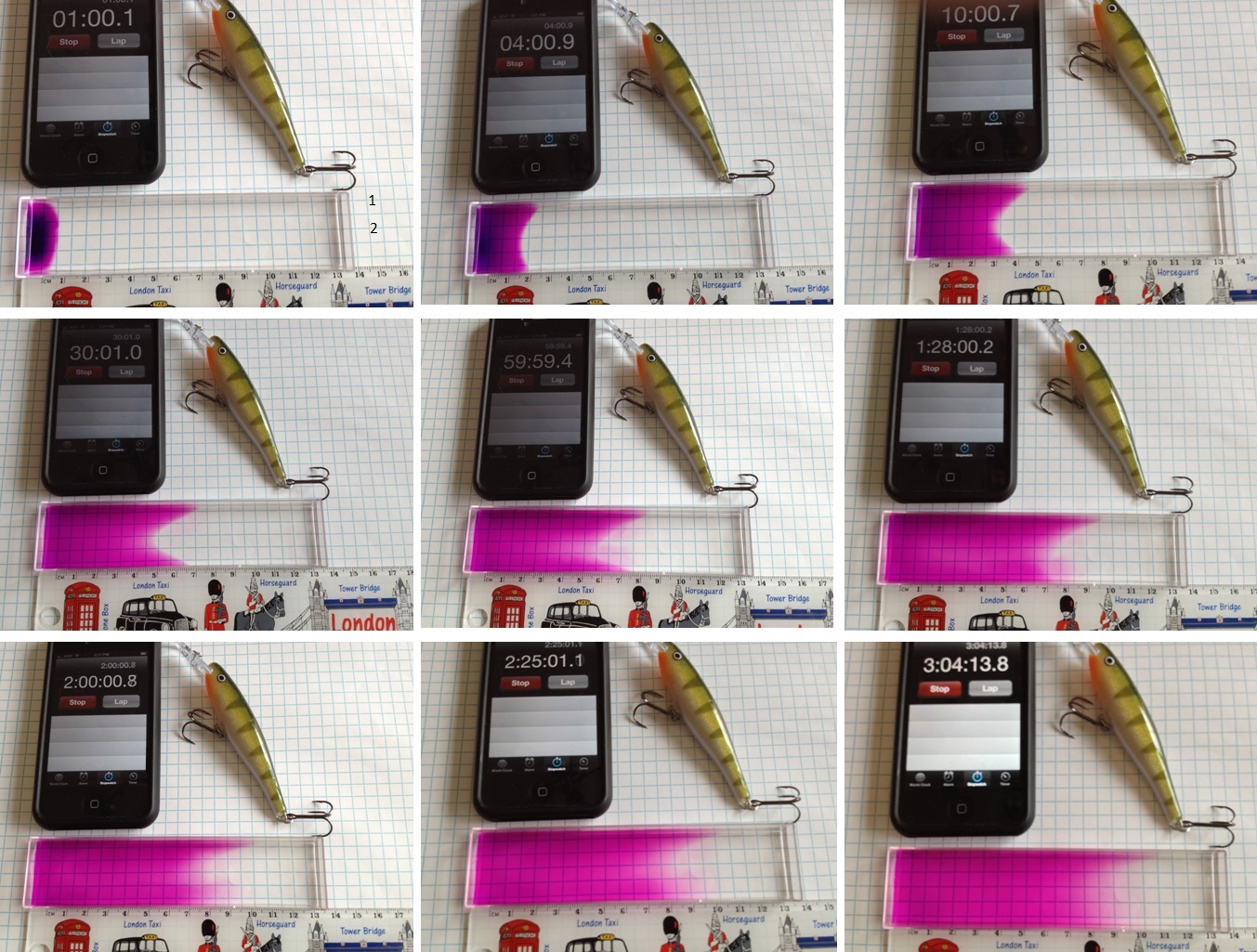

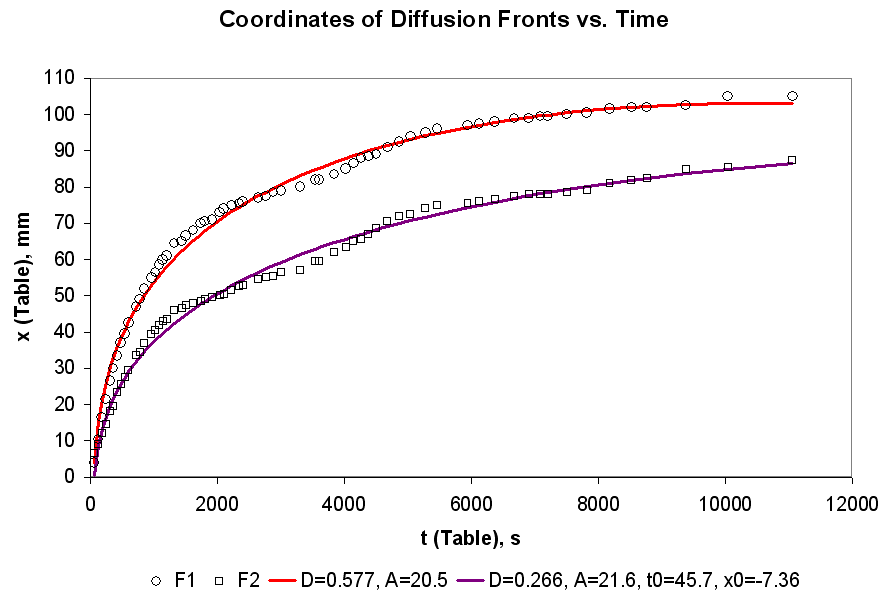

If a grain futures contract is traded prior its expiration month, then there is a limit price condition. Currently, the price of corn during the first limit session cannot move more than 40 points from the previous settlement price. On March 28, 2013 the bearish market news at 11:00:00 CT brought the price down to the limit 676 at 11:03:02 CT, Figure 14.

Trading does not stop. With the panic liquidation of long positions, a limit buy 676 order placed right after 11:00:00 would be filled. The price still may go up. That happened in the session prior Good Friday. Zooming to [11:03:02, 11:13:24] shows 1,835 transactions with the total volume 3,776 contracts at the price greater than 676, Figure 15. With the commission and fees $10.66 per trade per contract, a limit sell order for a few contracts placed two - three points above the limit would be very likely filled within the next 10 minutes resulting in a profit $89.36 - $139.36 per contract. The prices 686 indicate, even, bigger but less probable potential profit $489.36, Figure 15. The loss could not exceed $10.66. If the position could not be closed, then after the long weekend it would be a shocking > $1,000 loss after the open price gapped down, Figure 16. The price distribution on March 28, 2013 has a cut off tail known in advance. This can affect the b-increments.

12.4 The chicken and egg question

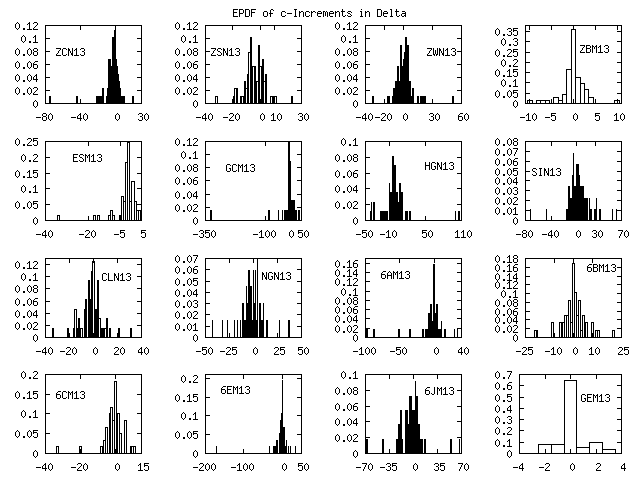

Sample moments are symmetric functions independent on the order of data. Holding the first price and changing the order of b-increments affects prices and their statistics but not b-increments. Reordering prices changes b-increments and their statistics but not prices. The relationship between the sample means and includes the prices order. From Equations 15 and 40 [192],

| (41) |

The product embeds dependence on the prices order, rising the chicken and egg question: which variables are fundamental prices or increments? The modern financial stochastic differential equations, SDE, taking the baton from Louis Bachelier’s Brownian motion [12] and Paul Samuelson’s geometric or economic Brownian motion [198] focus on absolute and relative price changes. Stochastic integration of increments creates prices leaving the latter a secondary role. This role is bigger in the geometric Brownian motion, where price denominators ensure the bigger risk and gain at higher prices. The Ornstein-Uhlenbeck process [221] extended to the mean reversion SDE [83] applied for simulation of interest and exchange rates has an embedded level coming out as an attractor. In contrast, often criticized in scientific literature technical analysis [166] puts significant accent to prices, their patterns, and trends. The author thinks that markets have many modes replacing each other in time, where prices or increments get varying accents.

13 A Comment on Science and Pseudoscience

Specialists on no-arbitrage pricing derivatives based on SDE and apologists of the technical analysis are two irreconcilable camps. The former exploit sophisticated mathematics. The latter draw lines and recognize patterns requiring more imagination than knowledge of geometry.

13.1 Sir Isaak Newton - a trader

Not every scientific worker trades and not every trader is a scientist. Sir Isaak Newton was such a "combination". His scientific authority is indisputable. His trading the South Sea Company stock since creation of the company in 1711 until the bubble in 1720 is an example, when an outstanding mind "can calculate the movements of the stars but not the madness of men" - the words attributed to Newton. This article is about the attractive market mean to withdraw specialists from professions - high frequency of big potential profits. The market keeps them in professions using losses. What kind of society would it be, if everybody would only speculate.

13.2 A common element of successful patterns

The source of income of a SDE, C++, software specialist in finance is profits made by traders. The traders watch the a-b-c-process. It, external, and internal events affect their minds and trading robots. They make decisions influencing on the process. The snake bites its tail. Its goal is survival. This is achieved by showing to the majority past frequent potential profits and hiding upcoming losses under the profit attire. If a market is efficient in something, then it is in this ability to fool. Larry Williams, a known trader and educator, writes: "The best patterns I have found have a common element tying them together: patterns that present extreme market emotions reliably set up trades for price swings in the opposite direction" [241, p. 95].

13.3 On technical analysis

Technical analysts appeal to Newton’s mechanics seeking a basis for price trends: "… a trend in motion is more likely to continue than to reverse. This corollary is … an adaptation of Newton’s first law of motion" [166, p. 4]. They criticize the theory of randomly walked prices. Ironically, the molecular-kinetic theory of heat served to Albert Einstein as an explanation of the Brownian particle displacement proportional to the square root of the time [46, Equation 11] employs statistics on a top of consideration of molecules as classical Newton’s particles. The system establishes the Laplace determinism. Quantum mechanics dismisses the latter paradigm axiomatically applying uncertainty on the micro level and making the classical mechanics a macro limit. This lack of causality seemed never satisfy Einstein.

Trend lines were drawn prior Bachelier. His ingenious mathematical model of Brownian motion coming five years prior the Einstein’s paper creates a parallel. Quantum mechanics has consumed the Newton’s one replacing the fully deterministic picture with uncertainty. Bachelier introduces uncertainty into price changes and presses determinism of trend lines. In both cases (physics and markets), applications continue using each paradigm depending on a situation. This parallel ends, if we recollect that the market, involving human beings, extends beyond the physical Brownian motion. Einstein derives his model for a physical phenomenon. His last equation for determination of the Avogadro number suggests experimental conditions for verification. Bachelier’s attempt to apply the same model to a phenomenon involving human consciousness and "the madness of men" requires serious confirmations. Its inadequacy leading to negative prices patched by Samuelson switching to a lognormal distribution and further attempts to eliminate inadequacy (volatility smile, volatility term, discrete dividend adjustments) of the advanced analog - the Black-Scholes-Merton option pricing formulas [83] - look important but minor details within the entire picture of complexity. Effects discovered by Kahneman and Tversky, masterly measuring human being behavior, is only the beginning of understanding of their influence on the a-b-c-process.

Since the market is "a result of cooperation of modern technology and human being consciousness governed by partly unknown laws of nature" [195], there is a danger to fall into pseudoscience. Indeed, some pay attention to moon phases. If they trade, should moon phases influence on prices? There are daily charts showing the days of full and new moon coinciding with significant local minimums and maximums of silver, corn, soybean, and wheat [240, pp. 94 - 96]. Are these events independent? Should we dismiss the dependence, if some minimums and maximums are one - three days apart from the full and new moon? Was it only in 1971 - 1973? The Karl Popper’s falsifiability - criterion of demarcation between science and pseudoscience implies that in this case we can formulate a hypothesis and prove or disprove it. In general, it is not easy to demarcate them [204] and a halo of scientist can play a terrible role. Serguei Kara-Murza, a philosopher of science, reminds about the Stanley Milgram’s experiments on obedience to authority figures conducted in the 1960th [90].

Sometimes technical analysis presents patterns without algorithmic definitions. Often it does not supply enough evidences of claims. Its representatives are seem busy with trading and have no time for a rigorous research: "technical analysis is a broad class of prediction rules with unknown statistical properties, developed by practitioners without reference to any formalism." [168]. Neftci is a constructive critic. His research is promising for technical analysis and cautiously gives a hope: "… if the processes under consideration were nonlinear, then the rules of technical analysis might capture some information ignored by Wiener-Kolmogorov prediction theory". Barton Malkiel is more skeptical: "In … simulated stock charts derived from student coin-tossings, there were head-and-shoulder formations, triple tops and bottoms, and other more esoteric chart patterns" [142, p. 131]. One formation was found very bullish by a chartist. However, Malkiel does not insist that market is a perfect random walk.

A technical analyst needs to turn his or her face to modern pattern recognition and machine learning techniques based on genetic programming [113], neural networks, support and relevance vector machines, probabilistic principal component analysis, Bayesian optimization (as a way to overcome overfitting) [17] with a solid theoretical foundation laid in works of Vladimir Vapnik and Alexey Chervonenkis [226]. The task here is to formalize algorithmic definitions of patterns and signals and automate their recognition with the purpose of objective statistical analysis.

13.4 Computer generated random walk vs. a-b-c-process

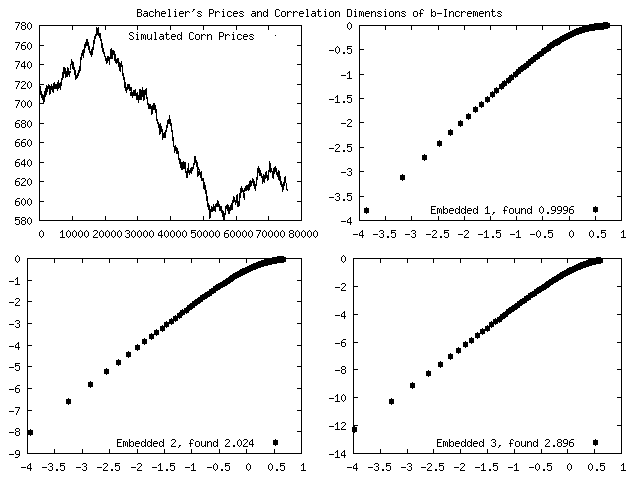

Visible similarity of a random walk with prices can be misleading. Techniques magnifying hidden differences of the two time series are valuable. A fair coin tossing, well studied Bernoulli trials, can be simulated with a uniform pseudo random numbers generator [121]. The normal generator [24] can be applied for simulation of the Bachelier’s normal and Samuelson’s lognormal time series. With the normal generator the variance must be set proportional to the time step of a Brownian motion, if time steps vary. For a constant step, it can be scaled to a single suitable value. The finite difference equations of the Bachelier’s model applied for generation of data on Figure 17 are

The chains of simulated b-increments and prices depend on a seed of the generator. It was 21325476. Presenting the seed makes sense, if a generating algorithm is given. The 19611 points are plotted, Figure 17 left top. While the price looks realistic for a chartist, the model cannot reproduce many important properties of the real a-b-c-process, Figure 18 left top: discreteness of prices and their increments, limit prices, distributions of b-increments changing in time within sessions, non-Gaussian properties of b-increments discussed later, volatility clusters. It ignores varying distributions of a-increments and implies independent normal b-increments distributed identically.

13.5 Computing the correlation integral

The author wants to attract attention to the correlation integral and dimension computed for both time-series. For time series the data is subdivided in chunks of size : , where small number of extra points not matching is neglected. The is embedded dimension. A norm, the distance between points, is computed for uniques pairs. Then, the fraction of pairs, where the distance is shorter than some , is computed

The indicator returns one, if the condition is true and zero otherwise. The is referred to as the correlation integral. For small dependence vs. is often a power law and the correlation dimension is

We are indebted for these notions and formulas to Peter Grassberger, Itamar Procaccia [71], [72], Floris Takens. Evaluation of distances is suitable for and . A ES session may get a half of million of ticks. This creates unmanageable 125 billions of unique pairs. James Theiler has invented the box-assisted algorithm [217] with the complexity reaching . The author’s C++ programs and implement both possibilities. Chains of pseudo random uniform and normal numbers are evaluated up to 1,000,000 points (). The slope well coincides with the embedded dimension. Changing variance shifts the curve in bi-logarithmic coordinates but does not change the slope. Real b-increments produce a lower correlation dimension than embedded one. The discreteness of b-increments creates horizontal plateaus of separated points complicating evaluation of . On charts, the found dimensions are given for the steepest slopes. Figures 17 and 18 emphasize additional property distinguishing pseudo random and real price increments.

14 A Comment on the Limit Theorems

Often, price changes are claimed to be sums of a number of hidden random factors. Consequently, if the number tends to infinity, they may obey a Gaussian or another stable law [128] [94] [95] [65, p. 76, p. 86], [143], [50]. The stable laws are a subclass of infinitely divisible probability distributions important for the limit theorems [58] [65, pp. 73 - 100] [141]. An example of infinitely divisible not stable laws is distributions given by the incomplete gamma function [65, p. 13].

14.1 "Non-Gaussian atoms"

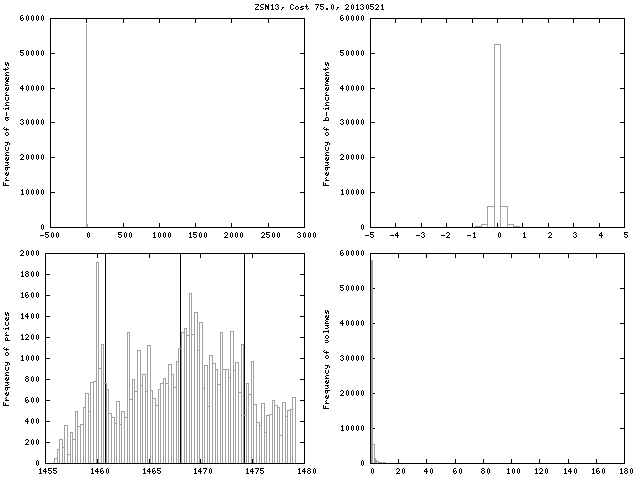

The a-b-c-classification implies that differences of two transaction prices are sums of the b- and c-increments, Equation 17. Times between transactions are sums of the a-increments and durations of the c-increments, Equation 16. For example, the difference of the last and first ZBM13 transaction prices on May 30, 2013 is the sum of the b-increments. Their sample has mean , standard deviation , skewness , and kurtosis . Table 14.1 presents the empirical probability mass distribution.

b-Increments of ZBM13, May 30, 2013 In In StdDev Gaussian, -7 -32.6 2 -6 -27.9 2 -5 -23.3 2 -4 -18.6 1 -3 -14.0 14 -2 -9.30 59 -1 -4.65 1808 0.0172 0.010 540 0 0 101598 0.964 0.98 26.2 1 4.65 1770 0.0168 0.010 487 2 9.30 65 3 14.0 18 4 18.6 7 5 23.3 1 6 27.9 2 7 32.6 0 0 8 37.2 1 105350 1 1

The hypothetic Gaussian probabilities are for the unit intervals, like , with the centers from the first column. The distribution is quite symmetrical. The kurtosis and astronomical summands in the last column evaluated for the test demonstrate absurdity of a Gaussian hypothesis for these b-increments, see also [192, p. 35].

The b-increments constituting intra-session price changes are not hidden. They are not mathematical abstractions but empirical indivisible "non-Gaussian atoms" limiting the range of self-similarity [148] and infinite divisibility.

14.2 Wisdom from the first source

A finite variance of i.i.d. variables guarantees approaching a Gaussian sum for non-Gaussian components. A varying number of summands compromises comparison of the sums. A violation of the i.i.d. property can be even a more serious obstacle for finding a limit distribution. The classics’ opinion is [65, p. 13] (author’s translation from the Russian Edition): "If the assumption about identity of the distribution laws of random variables in one series is refused, then the task to find possible limit law … becomes contentless: the limit law can be absolutely arbitrary. … The requirement has an illusive meaning: it does not prevent, for example, that a single summand could play a dominating role." Figure 19 exhibits two different behaviors answering on "I.I.D., or not I.I.D, that is the question." The sample statistics of b-increments, left|right, are size | , mean 0|0, standard deviation 0.196|1.75, skewness 0|-0.0984, kurtosis 26.3|8.34, ticks 262|241, elapsed seconds 82|1. In the "chain reaction" the standard deviation is nine times greater, kurtosis is three times less, duration getting almost the same number of transactions is 82 times shorter.

b-Increments of ZBM13, May 30, 2013, 07:28:39 - 07:30:00 and 07:30:01 In Gaussian, Gaussian, -7 0 2 176 -6 0 2 18.9 -5 0 2 0.955 -4 0 1 2.48 -3 0 8 1.87 -2 0 12 0.119 9.60 -1 5 17 0.00537 0.192 9.24 18.4 0 251 154 0.989 0.225 0.197 185 1 5 13 0.00537 0.192 9.24 23.7 2 0 11 0.119 10.8 3 0 10 0.657 4 0 5 0.133 5 0 0 1.02 6 0 2 18.9 7 0 0 0.0223 8 0 1 488 261 240 1 1 18.7 956

The value does not allow rejecting the Gaussian hypothesis for the left side and does not allow accepting it for the right side distribution. It is interesting that the sample kurtosis 26.3 for the left side deviates more from the Gaussian 3 than 8.34 for the right side.

Conclusions about the limit theorems cannot be made mechanically. It is needed to study the rate of convergence and pay attention to variation of distributions of b-increments within a range/session, dominating price fluctuations, presence of up and/or down limit prices, and possible price dependencies.

15 A Comment on Discrete Distributions

The multinomial distribution assumes fixed events with the probabilities , where . It generalizes the binomial distribution . For a th session, , where b-increments are expressed in , and empirical frequencies approximate . Since b-increments can be negative, zero, or positive, , where , if and . Prior opening a session with the limit and previous settlement price ,

| (42) |

Usually, . After the opening,

| (43) |

The limit implies the theoretical limits: and . These are equal to or for the current down or up limit price. The author has not seen prices gapping from the down to up limit or vice versa within a session. The open price gapping to the limit occasionally takes place. The Pork Bellies had been famous for making several limit sessions in a row.

For futures without the limit, theoretically the next and is unlimited. The minimum and maximum b-increments together with the numbers of occurrences in ranges and sessions are in Table LABEL:b-increments. By absolute values, all are less than the theoretical limits and varies from session to session. While the distributions are almost symmetrical, is rarely exactly equal to . The extreme value occurring just a few times with counted in thousands insignificantly influences on the skewness. They are more critical for the risk of triggering a stop loss order, because related frequencies are not negligible like in a Gaussian distribution. A multinomial distribution is not interesting unless the , , are allowed to be random variables governed by another distribution type and combined with a binary random variable selecting the negative or positive sign of the increment. An alternative to this is finding one distribution responsible for the absolute values of b-increments including their extreme values and combining it with a variable selecting the sign.

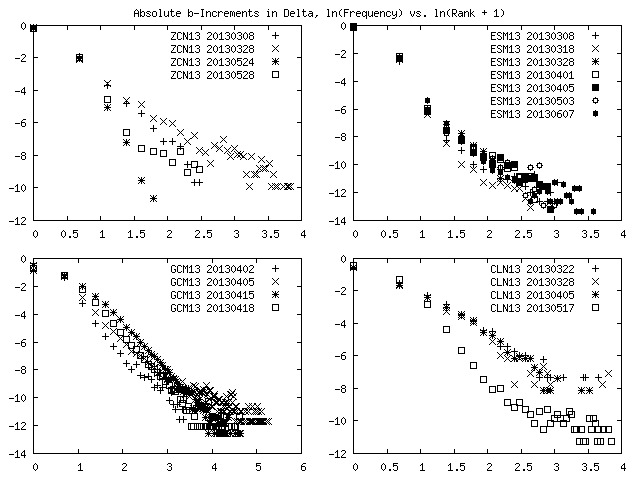

15.1 Zipf-Mandelbrot, Riemann and Hurwitz Zeta distributions

The author has reviewed the Zipf-Mandelbrot [147, pp. 198 - 218], where the Zipf case is ,

Riemann zeta [96, p. 35], [65, p. 82], [133, p. 821, Eq. 8], [16, related results]

Hurwitz zeta [42, related results], [82]

and power law [6, p. 29], [147, p. 30] distributions. It is interesting how simple words can trigger a research. The words of Chung Kai Lai [26, p. 259]: So far as known, this famous relationship between two "big names" has produced no important issue - initiated [133] and [82]. The author should recognize that his research on the maximum profit strategy has been triggered by the words of Robert Pardo [176, p. 125]: The measurement of the potential profit that a market offers is not a widely understood idea, [190, Preface].

The Zipf-Mandelbrot law assumes the maximum rank . While it can be set big, this is inconvenient because the upper bound of absolute b-increments can be unknown. The Riemann zeta distribution is less flexible than the Hurwitz zeta distribution. The latter is crafted so that it can start from rank zero, and there is plenty of zero b-increments. All equations imply

This is an equation of a straight line with the points , if or . The latter cannot be guaranteed for ZM, where . The H looks the most flexible from this group. Such lines express power laws . Vladimir Arnold recollects (the author’s traslation from Russian): From the stories of eye-witnesses, I know that Kolmogorov’s similarity laws in the theory of turbulences have been obtained by him not from consideration of dimensions (used for their explanation today) but due to covering the floors of the summer house in Komarovka by paper sheets with thousands of experimental data" and earlier "… my results are not proved (VS: mathematically) but correct, and this is more important" [6, p. 29]. Komarovka, a small Russian village outside Moscow, was in that time a Mecca for mathematicians from all over the world.

The points on Figure 20 accumulate large numbers of b-increments. For ES-mini it achieves 614991 on June 7, 2013. The lines for ZCN13 and CLN13 split between sessions. The points for ESM13 and GCM13 are closer to one approximating line. The "straight" lines have a tendency to bent at larger ranks meaning that frequencies are greater than predicted. The approximating lines underestimate risk but are better than the Gaussian distribution. An eye suggests that a parabola is more suitable than a straight line.

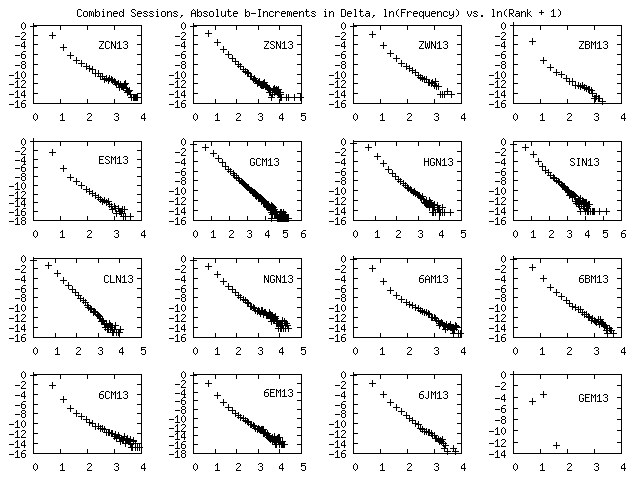

Combining b-increments from sessions prior computing EPDF creates smoother plots, Figure 21. The number of ticks used for the plot of ESM13 is equal to 27,438,059. This is greater than the number in Table LABEL:b-increments because the last extra session on June 21, 2013 is included. On these plots the initial artificial single zero increments are added. Their number is negligible and equal to the number of sessions. Also, ci-increments between ranges within a session are treated as b-increments. This cannot create a principal difference. The GEM13 significantly differs from other plots. The NGN13 b-increments expressed in are divided by 10 comparing with Table LABEL:b-increments. For this contract the minimal change in reported quotes is found equal to 0.01, while the official . Parabolas can better than straight lines approximate these data. While the plots indicate reasonable dependencies, the author could not find suitable and for b-increment frequencies combined from all sessions so that the result would satisfy the Pearson goodness of fit criterion. For b-increments obtained from a single session this is possible. Particularly, the one second ZBM13 May 20, 2013 data from Table 14.2 are well fitted by the Hurwitz Zeta distribution Table 15.1. The symmetric negative and positive are combined in one class. The number of degrees of freedom . The corresponding , , [111] are greater than the experimental 13.215.

b-Increments, ZBM13, May 30, 2013, Hurwitz Zeta Distribution with 1.510384234. 0 154 0.641666667 0.584630058 140.3112139 1.335480326 1 30 0.125 0.173952889 41.74869328 3.306254231 2 23 0.095833333 0.078165303 18.7596727 0.958458917 3 18 0.075 0.042982386 10.31577261 5.723987218 4 6 0.025 0.026656006 6.397441496 0.024691081 5 2 0.008333333 0.017906011 4.297442571 1.228228715 6 4 0.016666667 0.012733336 3.056000653 0.291601628 7 2 0.008333333 0.009449749 2.267939762 0.031655037 8 1 0.004166667 0.007249441 1.739865873 0.314622821 240 1 0.953725178 228.8940428 13.21497997

In our case the Riemann and Hurwitz zeta functions should be evaluated for real arguments and . This task is simpler than evaluation of the Riemann Zeta function of a complex argument . For this has become a competition. Finding 1,500,000,001 values of [139], where , cannot prove the Riemann Hypothesis [23] but contributes into computer science. The author has written the C++ functions RiemannZeta and HurwitzZeta and exported them from an XLL, a form of dynamically linked library DLL applied as Add-In for Microsoft Excel [161]. This helps to use the Microsoft Solver and Goal Seek in order to optimize the parameters and under the constraints and . The cost function for Table 15.1 is the experimental with the nine classes.

15.2 Euler-Maclaurin formula for Hurwitz Zeta

The chosen computational methods are based on the Euler-Maclaurin summation [44, pp. 114 - 117]. The Bernoulli numbers are taken from [1, p. 810]. The derivations are lengthy and the author presents the final formula only for the Hurwitz zeta function, which he could not find in literature. However, the idea is the same as in [44] for the Riemann zeta. Since convergence is slow for the direct sum, the Euler-Maclaurin summation is applied to the difference

where are the Bernoulli numbers and is the error term. Using the estimates of Harold Edwards [44] and Linas Vepštas [227], the and are selected to ensure 16 decimal digits of accuracy supported by the C++ built-in type double for the values of hinted by Figure 21. The Hurwitz Zeta distribution is perspective for describing distributions of b-increments without an attempt to combine multiple sessions or in smaller ranges. Generalization is likely prevented by the fact that the distribution changes in time, even, within a range/session.

16 A Comment on Parabolic Fractals

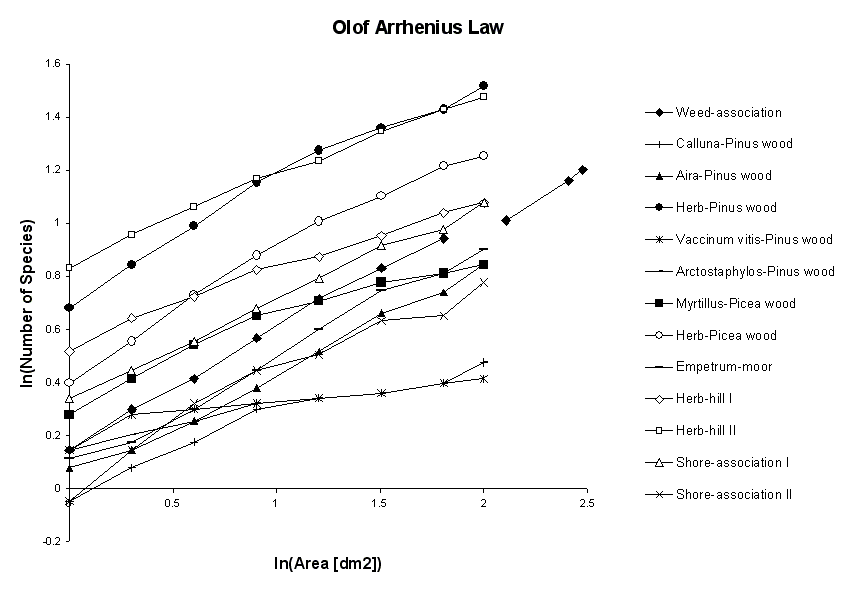

Arnold mentions that in many cases power laws remain experimental facts [6, pp. 36 - 41] and searching for asymptotic behavior and logarithmic corrections can provide theoretical explanations. He applies the Kolmogorov’s technique to smoothed mean minimal periods of remainders obtained after division of powers of two by odd numbers and finds an interesting bi-logarithmic dependence [6, p. 39, Figure 1]. His seven examples from botanics, literature, medicine, volcano activity, genetics, number of scientific publications, graph theory related to compact arrangement of elements in space important for computer science include the Olof Arrhenius Law: the number of species in a district is proportional to a power of its area. The author adds the first name to distinguish the son and his father - Svante Arrhenius (Nobel Prize in Chemistry 1903 for "… electrolytic theory of dissociation"), who’s equation for the temperature dependence of the constant of the chemical reaction rate is also known under the name "Arrhenius Law". It can be added to the Arnold’s list due to good straight lines on plots of logarithm of the constant vs. the reciprocal temperature in Kelvin degrees.

16.1 Plotting Olof Arrhenius’s data

The author has reviewed the article [9] and entered 106 pairs (area in decimeter2, number of species) [9, p. 96, Table] into the Microsoft Excel. For the first time we see the Olof’s results on Figure 22. My eye sees: 1) pieces of parabolas would be better for Calluna-Pinus wood, Herb-Pinus wood, Myrtillus-Picea wood, Herb-Picea wod, Herb-hill II, and Shore-association II; 2) Vaccinum vitis-Pinus wood has a big outlier. In the original Table, the 13 associations are accompanied by 10 - 30 percents deviations between experimental and computed data for greater areas: upper two - three from eight - ten observations. Arrhenius explains: "It is easily seen that the values calculated and observed agree very well. Generally there is an increase in the deviation corresponding to increasing area. This depends on the fact that the values of the smaller areas are the average of a greater number of observations than those of the larger".

16.2 Parabola’s shortcomings

Deviations from a straight line in log-log coordinates on frequencies vs. ranks plots got a collective name parabolic fractal. The so-called King Effect relates to the highest frequency rank outlier. A common example is the town-size relationship, where in France Paris deviates from the curve. Several phenomena are claimed to follow to the parabolic fractal: galactic intensities, the distribution of town-sizes, spoken languages, species, and hydrocarbons accumulations by petroleum system http://www.hubbertpeak.com/laherrere/fractal.htm. They extend the Arnold’s list. The cited reference [36] proves that "the set of points where exceptional oscillations of empirical and related processes occur infinitely often is a random fractal" and suggests how to evaluate its Hausdorff dimension. Figures 20, 21, and 22 demonstrate that parts of parabolas can be a better choice than a straight line. However, a parabola has a drawback: in many cases it cannot extrapolate far outside of the observed interval without violation of a natural monotonicity. More data is needed to confirm or reject the parabolic fractal effects in economics. The market ticks are valuable to clarify it for financial time-series.

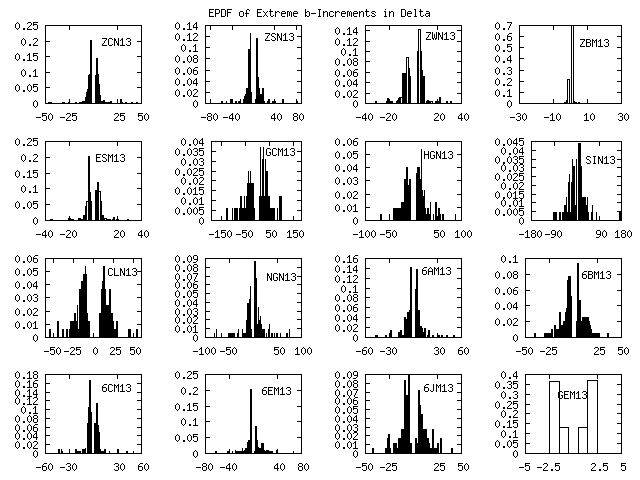

17 Extreme b-Increments

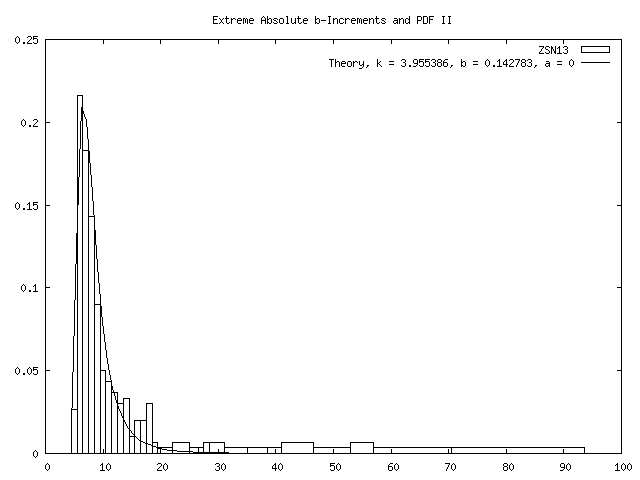

In Table LABEL:b-increments, columns Min, , Max, and present extreme b-increments and numbers of their occurrences within ranges and sessions. For each contract, the values are combined in a sample, where and are taken and times. The values are extracted from the session rows with dates. EPDFs are evaluated, Figure 23. Again, the ranks for NGN13 are divided by 10 prior plotting. The same extreme b-increments taken by absolute value are plotted in bi-logarithmic coordinates, Figure 24.

While the chances to get and b-increments are the highest, Figures 20, 21, a chance to get them as extremes in a session is negligible, Figure 23. Even, if we draw straight lines above the clouds of points on Figure 24, it would be wrong to extrapolate them to the left. The ZSN13, ZWN13, GCM13, SIN13, CLN13, NGN13, 6BM13, 6CM13, 6EM13, and 6JM13 on Figure 24 confirm that frequencies of absolute extreme b-increments have a maximum. Others confirm it indirectly: there were no sessions of ZCN13, ZBM13, ESM13, HGN13, and 6AM13 in March - July, 2013, with the extreme and b-increments.

17.1 Fréchet, Fisher, Tippett, von Mises, Gnedenko, Gumbel, Haan

The modern theory of extreme values is influenced by [59], [163], [64], [13]. Fisher and Tippett have presented three extreme limit distributions based on the functional relation which they must satisfy. Mises has proved a sufficient condition for the weak convergence of the largest order statistics to each of the three types. Gnedenko has given a rigorous proof of the necessary and sufficient conditions for the weak convergence of the extreme order statistics. Haan has improved exposition of the Gnedenko’s results. Differentiation of the CDFs of Gnedenko’s, G, [64, p. 423] with respect to gives the PDFs of Fisher and Tippett, FT, [59, pp. 211 - 212]

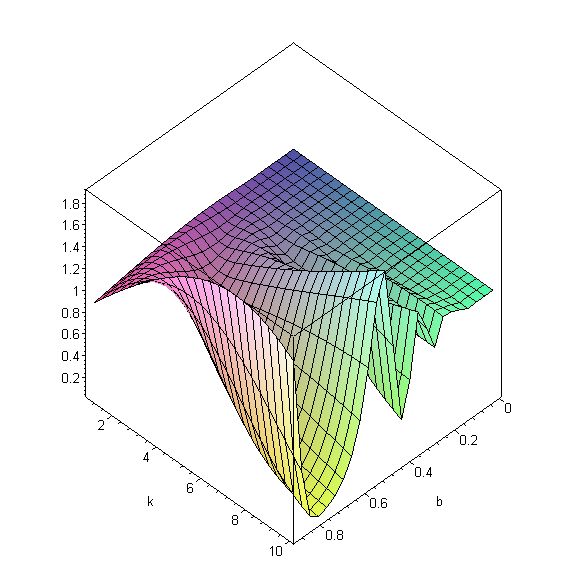

For a sample of combined absolute extreme b-increments the II might be useful. Maurice Fréchet wrote about II in 1927 [60]. It is used under his name too. By definition [65, p. 45], the distribution functions and are of one type, if for and , . It is easy to see that and are valid CDFs, belonging to one type for . While changing the scale and origin of the coordinate system does not create a new type, we get a better fitting instrument

| (44) |

Minimization of gives the solution , Figure 25. With the Microsoft Solver’s constraint , the optimal is stably obtained for guesses . If , then the PDF is the Type-2 Gumbel distribution marking the contribution of Emil Gumbel [75]. The optimal excludes the Frétchet’s case. It is inconvenient to use a continuous PDF like Equation 44 for minimization of the Pearson’s goodness of fit quantity: the fractional boundaries of classes would be far-fetched. Extreme and ordinary b-increments are discrete.

17.2 We need a discrete distribution