Varadhan’s formula, conditioned diffusions, and local volatilities

††thanks:

Corresponding author: Stefano De Marco, Ecole Polytechnique-CMAP, Route de Saclay, 91128 Palaiseau Cedex, France. demarco@cmap.polytechnique.fr

Key words and phrases: conditional density asymptotics, local volatility, stochastic volatility, large deviations.

2010 Mathematics Subject Classification: AMS 91G20, 91G80, 60H30, 65C30.

Abstract

Motivated by marginals-mimicking results for Itô processes [14, 24] via SDEs and by their applications to volatility modeling in finance, we discuss the weak convergence of the law of a hypoelliptic diffusions conditioned to belong to a target affine subspace at final time, namely if . To do so, we revisit Varadhan-type estimates in a small-noise (as opposed to small-time) regime, studying the density of the lower-dimensional component . The application to stochastic volatility models include the small-time and, for certain models, the large-strike asymptotics of the Gyöngy–Dupire local volatility function. The final product are asymptotic formulae that can (i) motivate parameterizations of the local volatility surface and (ii) be used to extrapolate local volatilities in a given model.

1 Introduction

Consider an -dimensional diffusion process given by the solution of

| (1.1) |

Applications to finance suggest a splitting of the state space, say , where is the main process of interest (for instance: price or log-price of an asset) and some auxiliary process (for instance: stochastic volatility, possibly multi-dimensional). There is a massive amount of literature concerning , the probability distribution function of at small times . In the elliptic case, that is when such investigations go back to Varadhan (“”) and then Molchanov [37] for full expansions of . The hypoelliptic situation (assuming the strong Hörmander condition ) was then studied by Azencott, Bismut, Leandre, Ben Arous,… (the function is then be interpreted as control distance associated to the diffusion vector fields.)

Similar results were recently obtained for , the density of (that is, a marginal density of ) by Deuschel et al. see [12, 13], improving on earlier works of Takanobu–Watanabe [41]. We postpone a detailed comparison of [41] and our results to Section 1.2 below.

Our main results are: (i) a Varadhan formula for in the short time limit, which is seen to be valid in great generality (without the need to check for the non-degeneracy conditions that appear as assumptions in [41, 12, 13]111As was seen in [13], checking non-focality requires a non–trivial analysis of certain Hamiltonian systems. We also note that focality actually happens in reasonably simple situations, e.g. in the context of a 2-dimensional Black–Scholes basket, as was seen in [15].) and then (ii) a limit theorem for conditioned on the value of . As far as we know, even in the elliptic case our results, concerning the marginals of , are new. The limit here may again be short time or, more generally, small noise. In fact, the small noise situations poses new difficulties (for instance, in a strictly hypoelliptic setting Varadhan’s formula may fail!) but then offers new applications: indeed, contribution (iii) of this paper is concerned with a class of stochastic volatility models introduced by Stein–Stein: we exploit scaling in a way that the small noise asymptotics for the conditioned diffusions gives us a (computable) expression for the asymptotic slope of local variance (the square of Dupire’s local volatility as induced from option prices). Postponing precise assumptions to Section 2, our first main result is stated as follows

Theorem 1.1.

(i) Let as above. Under a strong Hörmander condition, admits a density for and the following Varadhan type formula holds: for every

where is the squared control distance associated to and .

(ii) Under a further technical assumption (always satisfied in the elliptic case - see Thm 2.10 for a precise statement)

| (1.2) |

in the sense of weak convergence of probability measures, provided there exists a unique minimizer for the problem .

While the above theorem is clearly useful (it implies, for instance, short time asymptotics for local volatility; on a technical level, we remove the ellipticity requirement from [7]), it does not lend itself to understand spatial asymptotics. To this end, we generalize the setup and discuss small noise problems of the form

| (1.3) |

with and (in the precise sense of condition (1.13) below). By Brownian scaling, the short time setting falls into this setting by taking , and .

Theorem 1.2.

(i) Write . Under a strong Hörmander condition, and a further technical assumption (which is always satisfied in the elliptic case, or also when - see Thm 3.1 for precise assumptions), the following Varadhan type formula holds for the density of : for every and

where, as before . (Although the action is still given in terms of a variational problem, cf. (1.10) below, it has no more the interpretation as point-to-subspace distance.)

(ii) Under the same assumptions as above we have, for fixed and ,

| (1.4) |

provided there exists a unique minimizer for the problem .

The case in Theorem 1.1(ii) (“from to ”) is covered by the result of Molchanov [37] for elliptic diffusions, and more recently by Bailleul [2] in the hypoelliptic setting. Besides the more general framework of small noise asymptotics that we consider in Theorem 1.2, in (ii) the final target set for the process is an affine subspace instead of a single point (“from to ”, restoring the point-to-point situation when ). Also, the results of [37, 2] are given on compact manifolds, while we work here with -valued processes, and need to rely on some non-trivial tail bounds.

Following the well-known projection results [24, 14] for Itô SDEs, we then have the following corollaries of Theorem 1.2 for the local volatility:

Theorem 1.3.

(i) [Local volatility, short time behavior] In a generic stochastic volatility model (where denotes log-price and stochastic volatility)

| (1.5) |

Here is the “most likely” arrival point, computed as of where is the action associated to the stochastic volatility model. (Eventually, explicit computations depend on the specific model considered.)

(ii) [Local volatility ‘wings’ in the Stein–Stein model] In the Stein–Stein model (where follows an Ornstein–Uhlenbeck process, see equation (4.15)) 222When the correlation parameter between the log-price and the instantaneous volatility is not null, the Stein–Stein model is also known as Schöbel and Zhu model, see [39]., small noise asymptotics lead to

| (1.6) |

where the constants are given explicitly in terms of the model parameters.

As we will show in Section 4, under some special parameter configuration of the Stein–Stein model, the explicit expression of the constants appearing in (1.6) turns out to be consistent with known results from moment explosion for affine models [30].

As a particular consequence of Theorem 1.3(i), we see that the local volatility surface generated by a fairly general stochastic volatility model (see Theorem 4.4 below for detailed assumptions) does not explode in small time. Conversely, realistic local volatility surfaces typically do exhibit an explosive behavior out of the money when time goes to zero (namely as , for all ). This is the case for the parametric local volatility surface calibrated to SPX option data in [21, Section 4], and for the local volatilities obtained via Dupire’s formula from realistic SSVI parameterisations [20] of the implied volatility (and finally, the same behavior also appears when applying Dupire’s formula to option prices generated by models with jumps - see a related discussion in [17]). Apart from providing a tool for computing the limit, Theorem 1.3(i) tells precisely that the local volatilities generated by a standard homogeneous stoch vol model based on Brownian diffusions are not able to capture this phenomenon – thus providing a negative result for this class of models, in the same spirit as [18, Theorem 2], which focuses on the behavior of the at-the-money implied volatility skew.

On the other side, in analogy with the large-strike behavior of implied volatility [36, 22], the linear asymptotic behavior of the local variance in Theorem 1.3(ii) is likely to hold in even wider classes of stochastic volatility models (the same result is indeed known to hold for the Heston model, see [11], based on affine principles). On the one hand, the knowledge of an explicit spatial asymptotics for the local volatility can motivate the choice of functional forms used to smooth out and/or extrapolate a local volatility surface calibrated to market data. Already in use among practitioners, SVI-type parameterizations of the local variance, cf. again [21, Section 4], are compatible with the asymptotic result in (1.6). On the other hand, a robust implementation of the local volatility surface isof course the basis for a Monte-Carlo evaluation of exotic options under local volatility. Once this step is achieved, the comparison of the prices of volatility-sensitive products (cliquets, barriers,…) under a stochastic volatility model and the corresponding ‘projected’ loc vol model is often used by option trading desks in order to quantify the impact related to different volatility dynamics. This procedure often enters as an important step in the assessment of volatility model risk by model validation teams. Theorem 1.3 allows to extrapolate the local volatility function with explicit formulae in extreme regions, where the implementation of Dupire’s formula typically suffers from numerical instabilities.

Acknowledgment. SDM thanks Davide Barilari and Luca Rizzi for interesting discussions and insights on affine control systems. PKF acknowledges support from European Research Council under the European Unions Seventh Framework Programme (FP7/2007-2013) / ERC Grant Agreement #258237 and DFG grant FR2943/2. SDM acknowledges funding from the research programs ‘Chaire Risques Financiers’, ‘Chaire Marchés en mutation’ and ‘Chaire Finance et développement durable’.

1.1 Small noise systems

Standing assumption throughout this paper is that the vector fields and the functions of the one parameter family are smooth () functions: postponing any precise set of assumptions to the following sections, let us say here that our main results are stated under a boundedness assumption on the and the together with their derivatives of all orders, and then extended to a class of 2-dimensional diffusions (stochastic volatility models) with unbounded coefficients. We assume that

| (1.7) |

and that converges to some limit vector field

| (1.8) |

uniformly on compact sets of .

Under assumptions (1.7) and (1.8), it is known that the process satisfies a Large Deviation Principle (LDP) on the path space as (for a nice recent summary about large deviation principles for small-noise diffusions, see Baldi and Caramellino [4], and references therein). The deviations of are driven by the solutions of the limiting controlled differential system

| (1.9) |

where , and for any , denotes the Cameron-Martin (Hilbert) space of absolutely continuous functions with derivative in , equipped with the norm333We commit a slight abuse of notation writing , instead of , for : the time variable, kept fixed in our results, will always be clear from the context. . Following the typical terminology in large deviations theory, for every we define the action function by

| (1.10) |

with the convention , where

is the set of controls steering the trajectories of the system (1.9) from the point to the point in time . Following standard terminology, we call minimizing control any control realizing the infimum in (1.10), namely such that . Some properties of are presented in Lemma 2.7 below. For every fixed , the LDP for the family of finite dimensional random variables reads

| (1.11) |

for every closed set and open set in . Following a common convention in large deviations theory, we denote .

The large deviations principle (1.11) is very general, and depends only on some mild Lipschitz conditions on the coefficients of the SDE. We will be concerned with the situation where the fixed-time distribution of possesses a density: as it is common in the field of hypoelliptic heat kernel asymptotics [34, 35, 5], we assume that strong Hörmander condition holds at all points:

| (1.12) | ||||

that is, the linear span of the and all their Lie brackets444By definition, , . is the full tangent space to at for all . It is a classical result (due to Hörmander , Malliavin) that the law of admits a smooth density with respect to the Lebesgue measure on for every .555As is well known, weak Hörmander condition at the starting point is a sufficient condition to have a smooth density. Some of our technical results are actually proved under this assumption (weaker than (1.12)), see Lemma A.2 in Appendix A.2.

In order to study the asymptotic behavior of the density of , we impose the convergence of the partial derivatives of the drift vector field : in addition to (1.8), for every multi-index

| (1.13) |

uniformly on compact sets of , where . Furthermore, we assume that the families of norms and are uniformly bounded in , for every .

The deterministic Malliavin matrix . For every , the map is differentiable (indeed, ) from into , see Bismut [8, Theorem 1.1]. Let us denote its Fréchet derivative at . On the other hand, for fixed , is a diffeomorphism as a function of : we denote its differential at . The method of variation of constants allows to express , the image of through the linear map , via the representation formula

Following Bismut [8], and in analogy with the stochastic Malliavin matrix, we introduce the deterministic Malliavin covariance matrix , whose entries are given by

| (1.14) |

It is a fundamental remark due to Bismut [8, Theorem 1.3] that has full rank if and only if the matrix is invertible. The invertibility of is related to the non-degeneracy of the vector fields ; in the presence of a locally elliptic diffusion coefficient - which is the case for several financial applications - the following invertibility condition is useful, and easy to check:

Lemma 1.4.

Let . If there exists such that

then is invertible.

The proof of Lemma 1.4 is an easy linear-algebra exercise, see [8, Theorem 1.10] or [12, Proposition 2.1]. A sufficient condition for to be invertible for every , stronger than Hörmander ’s condition, is given as condition (H2) in [8, Chap.1].

Notation for densities. We denote

the density of and

the density of the -valued projection

It is clear that

| (1.15) |

where . Note that the (limiting) initial condition is fixed in the present discussion and, in contrast with the usual convention in heat kernel analysis, we do not write - including the initial condition in the symbol for the density - in order to avoid any confusion between initial and terminal points when writing for .

Finally, we denote the infinity norm in , and (resp. ) the associated closed ball of radius around (resp. the complementary of the ball).

1.2 Relation to the works of Takanobu–Watanabe

As is well known, conditional expectation of Wiener-functionals can be analyzed using Watanabe’s pullbacks of delta functions [27, Ch.V, Sec.9]. More specifically, for smooth functions one has

| (1.16) |

where denotes the Dirac delta function at . When is the solution to a stochastic differential equation, assuming small noise dynamics of the form

| (1.17) |

(cf. [41, equation (2.1)]), writing to indicate dependence on , asymptotic expansions of the form

| (1.18) |

were obtained in [41, Thm. 5.1], with given in [41, Equ. (3.2)]. It is then tempting to combine (1.16) and (1.18) such as to obtain an asymptotic expansion of

in terms of . There are, however, some (serious) obstacles in proceeding this way, a detailed discussion of which may also help to put this paper’s contribution into context. Before going into details, recall validity of [41, Thm. 5.1] hings on the following conditions: (A) strong Hörmander, (B) non-degeracy of the deterministic Malliavin matrix (essentially a control-theoretic condition, trivially satisfied in elliptic situations), (C) finite dimension, say , of the space of minimizing controls, where means finitely many minimizers, (D) a certain non-degeneracy of the action functional .666For : each minimizer must be a non-degenerate minimizer of the action; , the null-space of the Hessian is assumed to be compatible with the tangent space of the space of minimizers.

-

•

Takanobu–Watanabe conditions are difficult to check. Condition (D) in [41, Thm. 5.1] was left in a “raw” infinite-dimensional form which the authors can just about manage in explicit and simple situations [41, Sec.7] related to Lévy’s area.777On a related note, and with focus on 0, providing a finite-dimension criterion (checkable in terms of Hamiltonian ODEs, we called this condition “non-focality”) was a key contribution of [12, 13].

-

•

Takanobu–Watanabe conditions may not be satisfied. An example related to Lévy’s area, with single minimizer () but where condition (D) fails, is given in [41, Sec. 7, (III)4]; see also [12] (where this example is shown to be focal). However, an analysis “by hand” reveals [41, (7.7)] a density expansion which implies the correction large deviation behaviour

This provides an examples where [41, Thm. 5.1] fails to apply, whereas our Theorem 1.2 works.

-

•

The Takanobu–Watanabe setup does not cover our applications. The small noise dynamics (1.17) used in Takanobu–Watanabe do not allow for general -dependence in the drift vector field and initial data (with regard to our notation, only the case is covered by [41]). This generality, however, is crucial in our discussion of local volatility wings, part (ii) of Theorem 1.3, and introduces some non-trivial complications even at the large-deviation level, as seen in part (i) of Theorem 2.1 below.

-

•

Possible gap in Takanobu–Watanabe. According to the recent preprint [28], there was no proof available for Theorem 2.1. in [41], a large deviation result for pinned diffusions measures, on which [41, Thm 5.1.] relies. (A complete proof, based on rough paths, has then been offered by the author of [28].)

2 Theoretical main estimates

Ben Arous and Léandre [6, Section 3], showed that the asymptotics of the logarithm of the density for the small-noise problem (1.3) as might be governed by a different action function (what they call the “regular” action) defined by

| (2.1) |

with the convention .

Theorem 2.1 (Ben Arous and Léandre [6] revisited).

Consider

with as , and according to (1.13). Assume strong Hörmander condition (sH) at all points, and write for the density of . Then

-

(i)

the following estimates hold:

(2.2) and

(2.3) for every . In particular, if is non-empty for some and there exists a minimizing control such that is invertible, then , so that

(2.4) -

(ii)

Assume there exists a minimizing control with invertible Malliavin matrix . Then, there exists an open neighborhood of such that

(2.5) holds uniformly over in compact sets contained in .

Proof. The proof is given in Appendix A.2. The statement with and , and without the uniform convergence in (2.5), is given in Theorem III.1 in [6].

Remark 2.2.

If one assumes existence of a minimizing sequence for (1.10) such that is invertible for every , then immediately follows from the definition of the two actions. Under this assumption, (2.4) holds. In the end, the condition of invertibility of for all in (for some point ) will be satisfied in our applications.

Some additional comments are in order.

The following tail bound will be useful in the proof of our main result in the next section.

Proposition 2.4.

Let and be fixed. Under the assumption of Theorem 2.1, we have, for every , every and every

where with the usual convention, .

Proof. Given in Appendix A.2.

Crucial for the applications, the optimal control problem (1.10) defining the action function can be rephrased in terms of the Hamiltonian formalism. The following proposition provides necessary optimality conditions for the controls in when is fixed, in the spirit of Pontryagin’s maximum principle: as such, it appears as a generalization of the corresponding result in Bismut [8], from a point-to-point setting ( to ) to a point-to-subspace ( to , ) setting. Let us introduce the Hamiltonian

Proposition 2.5 (see Proposition 2 in [12]).

Fix , and assume is an optimal control for the problem

Moreover, assume the deterministic Malliavin matrix is invertible. Then, there exists a unique such that for all , where solves the Hamiltonian ODEs

| (2.6) |

subject to the (initial-, terminal- and transversality-) boundary conditions

| (2.7) |

Furthermore, the control is restored as

and .

Remark 2.6.

If is the terminal value of the -component of a solution to (2.6), then is a minimizer of the map .

Finally, the following lemma summarizes some properties of the control system (1.9) and of the action that will be extensively used throughout the paper.

Lemma 2.7.

Assume the vector fields and are Lipschitz continuous, with Lipschitz constant . Denote the solution of the ODE (1.9) on the interval , and the action of the system as in (1.10). Then

-

(i)

For every , the map is weakly continuous from into . Moreover, there exists a positive constant , increasing in , such that

(2.8) for every .

-

(ii)

is a good rate function of large deviations theory: that is, for every the level sets are compact. In particular, is lower semi-continuous.

-

(iii)

if , the infimum in (1.10) is attained: that is, there exists a minimizing control such that .

Assume moreover that the vector fields are (bounded with bounded derivatives). Then

-

(iv)

If the satisfy the strong Hörmander condition (sH) at all , then for every , and is finite on .

-

(v)

If there exists a minimizing control , , with invertible Malliavin matrix , then there exists a neighborhood of such that is continuous on .

Proof. . Weak continuity with respect to the control parameter is classical. See Bismut [8, Theorem 1.1] for the case of smooth vector fields: the case of Lipschitz continuous coefficients is handled analogously: in essence, the continuity property and estimate (2.8) follow from an application of Gronwall’s lemma. See also [4, proof of Lemma 2.5] for estimate (2.8). is a direct consequence of : use , and the latter set is compact since (weakly) continuous image of a (weakly) compact set. is a direct consequence of : indeed, assume . Then the infimum in (1.10) is in fact taken over the set , which is weakly compact; since the norm is weakly lower semi continuous, attains its minimum on this set. . The non-emptiness of (therefore, finiteness of ) under strong Hörmander condition is a classical result of controllability: see e.g. [29, Theorem 2, p. 106] for the affine control system with drift that we consider here. . In light of , it is sufficient to prove that is upper semi-continuous. Under the assumption of existence of a minimizing control with invertible Malliavin matrix, upper semi-continuity is proven as in the second part of [9, Proposition 3.2]: as it is typical in the geometrical control setting, the key point is the implementation of the Implicit Function Theorem locally around , which is made possible by the fact that the linear map has full rank.

Remark 2.8 (On point of Lemma 2.7).

When in (1.9) and strong Hörmander condition (sH) holds, it is classical that is finite and continuous on , without any further assumption about the existence of minimizers with invertible Malliavin matrix. This statement is equivalent to well-known continuity of the Carnot-Carathéodory distance on a sub-Riemannian manifold (here: equipped with the control distance induced by (1.9) with ). A standard proof, based on the small-time local controllability of driftless control systems, is provided for example in Bismut [8, Theorem 1.14]. For affine control systems with non-zero drift as (1.9), the continuity of is not, in general, a consequence of Hörmander condition. In [1, Section 2] an example is provided, where strong Hörmander condition holds at all points, and the function fails to be continuous.

Remark 2.9.

2.1 The conditioned diffusion

Denote the projection of over the last components, so that

We write

for the law of conditional on being at level at time . If , this is well-defined via

for all , where

| (2.9) |

is the density of conditional on .

Theorem 2.10.

Consider given by

| (2.10) |

with and according to (1.13), and assume strong Hörmander condition (sH) at all points. Fix and , and set . Assume that there exists a unique minimizer for the problem888The existence of a minimizer follows from the lower semi-continuity and compactness of the level sets of the map .

| (2.11) |

and assume that for every in a neighbourhood of there exists a minimizing control with invertible deterministic Malliavin matrix , as defined in (1.14). Then, and

in the sense of weak convergence of probability measures on , i.e. for all ,

| (2.12) |

Corollary 2.11 (Test functions with polynomial growth).

Under the assumption of Theorem 2.10, assume is continuous and has polynomial growth, that is for some and , for all . Then

holds.

Remark 2.12 (Extension to finitely many argmin’s).

If there exist finitely many global minimizer , , for the problem (2.11), assuming that is invertible for some minimizing control for every in a neighborhood of each , a modification of the arguments used in the proof of Theorem 2.10 allows to show that converges to a law supported by the , i.e.

for some with and , which means as , for every .

Remark 2.13 (Extension to the finite dimensional law).

Under the hypotheses of Theorem 2.10, assume in addition that there exist a unique minimizing control in , that is

| (2.13) |

(in particular, is the unique minimizer of on the set ). Then, for every ,

where , , is the trajectory associated to the control . The case of finitely many minimizing controls in gives rise to a limiting law supported by the , with . Subject to a tightness estimate, the convergence of the finite dimensional law yields the convergence at the path level, namely in the case of a unique minimizing path . In the point-to-point case , this result is proved in Molchanov [37] for elliptic diffusions and in Bailleul [2] in the hypoelliptic setting (see also Bailleul, Mesnager and Norris [3]).

Remark 2.14 (Relation with Takanobu–Watanabe [41]).

As discussed in section 1.2, the asymptotic expansion is given in [41] under suitable assumptions on and , allowing to study

| (2.14) |

The constant in the expansion depends on both and , see [41, Theorem 5.1]. Let us apply Takanobu–Watanabe’s expansion to both the numerator and the denominator at the RHS of (2.14), under the assumption of Theorem 2.10 that the minimizer is unique. An inspection of the expression of in [41, Theorem 5.1] reveals that the constant at the numerator is given by for some , while the constant at the denominator is . This means that overall

in agreement with Theorem 2.10.

As pointed out in section 1.2, the validity of Takanobu–Watanabe’s expansion relies on some conditions that are cumbersome to check (notably their infinite-dimensional assumption (D)), or may fail be satisfied in situations where Theorem 2.10 is instead applicable.

Moreover, we stress once again that only the case with zero limiting drift is considered in [41] - while it is crucial for our applications to space asymptotics of local volatilities in Section 4.3 to overcome this limitation.

Of course, using the full expansion in [41], higher order expansions in (2.14) (of the form ) are a priori accessible. However, in order to compute the correction , one needs to know the precise value of the constant for which there is no explicit expression, and significant additional analysis would be be necessary, e.g. in the spirit of [31].

In order to prove Theorem 2.10, we need a preliminary estimate on the marginal density .

Proposition 2.15.

Under the hypotheses of Theorem 2.10,

| (2.15) |

where with the usual convention, . In particular, for small enough.999The strict positivity of is not, in general, a consequence of Hörmander condition. According to Ben Arous and Léandre’s support theorem [6, Theorem II.1], the density of the full process is strictly positive at if and only if there exists some such that is invertible. While Hörmander condition ensures that is non-empty for every , the lack of controls with invertible Malliavin matrix can not be excluded a priori.

Proof. For simplicity, let us drop the explicit dependence on the (fixed) , and write for , for , etc. Also write for . We note that by definition, . Using Ben Arous and Léandre’s support theorem [6, Theorem II.1], the invertibility of for some implies for small enough: it follows that , therefore the conditional density in (2.9) is well-defined.

Let be a neighborhood of in such that, for every , is invertible for some minimizing control (with no loss of generality, we may assume to be compact). It follows from Theorem 2.1 that

| (2.16) |

From point in Lemma 2.7, is continuous on a neighborhood of : possibly making smaller, we can assume

for some fixed . It follows from estimate (2.2) in Theorem 2.1 that there exists such that

for every . Analogously, for every there exists such that

for all . It follows from these last two estimates that for every ,

| (2.17) |

for all . Now write

| (2.18) | ||||

where is the Lebesgue measure on . First applying Jensen’s inequality, then Fatou’s lemma, one has

| (2.19) | ||||

where we have used (2.17) in the last inequality. Finally using the lower bound (2.3) for and (2.19), it follows from (2.18) that

Since was arbitrary, (2.15) is proved.

Remark 2.16.

Note that we have nowhere used, in the proof of Proposition 2.15, the fact that the minimizer is unique, neither that there exist finitely many. Proposition 2.15 then holds under the weaker assumption that is invertible on at least one minimizing control , for every in a neighborhood of some global minimizer of the map .

Proof of Theorem 2.10. Let us drop the fixed from the notation, and write for , etc.

Step 1. We want to show that for all , one has as , with . Consider such that the map is continuous on (by Lemma 2.7, such a exists) and such that estimate (2.5) of Theorem 2.1 holds on . Let , and consider such that and , where . We have

and our aim is to show that the last integral converges to as .

We have

Step 2 (). Set

By the lower semi-continuity of and the uniqueness of the minimizer , one has . Let now be such that : on the one hand, since estimate (2.5) in Theorem 2.1 is uniform over a compact neighborhood of , we know there exists such that

for all and . On the other hand, it follows from estimate (2.15) in Proposition 2.15 that

for all . Putting these two estimates together and using the definition of , it follows

| (2.20) |

for all such that and . Therefore, we have

for all , where is the Lebesgue measure on . For every choice of and , the right hand side can be made arbitrarily small taking small enough.

Step 3 (). As done in Step 2, notice that . Since

it follows from 2.15 and Proposition 2.4 that

The last inequality clearly implies that vanishes as .

Proof of Corollary 2.11. Let , , be a bounded continuous function that coincides with on . Assume is fixed, but large enough so that contains and the compact set . We have (dropping the fixed index from the notation),

By Theorem 2.10, the first term tends to as . The second term can be bounded as in Step 3 of the proof of Theorem 2.10, that is

where we have used Proposition 2.4 and estimate (2.15) in the second step, and the choice of to conclude. The last inequality implies that the left hand side vanishes as .

3 Varadhan’s formula for marginal densities

As a by-product of the estimates presented so far (Theorem 2.1, Proposition 2.4 and Proposition 2.15), it is possible to show that a Varadhan-type formula holds for the density of the projected diffusion . Proposition 2.15 already provides a lower bound; we are left with the proof of the corresponding upper bound. In the following theorem, the case recovers the classical Varadhan’s formula [42], or rather Léandre’s extension [34, 35] to the hypoelliptic setting.

Theorem 3.1.

Consider the strong solution to

with , and assume strong Hörmander condition (sH) at all points. Fix and . Then

- (i)

-

(ii)

If , assume that is invertible for at least a minimizing control , for every in a neighborhood of , where is some (not necessarily strict, nor unique) global minimizer of the map . Then, estimate (3.1) holds.

Consider a financial model , where models the log-price of an asset, and its (possibly multi-dimensional) stochastic volatility. The small-noise behavior of the logarithm of the density of translates into the leading order asymptotic term of the implied volatility of European options (see for example Gatheral et al. [19] for an implementation of this approach in the small-maturity limit for 1D local volatility models).

Remark 3.2.

Comparison with the marginal density expansions of Deuschel et al. [12]. A sufficient condition for (3.1) to hold is given as condition (ND) in Deuschel et al. [12], see their Definition 2.7. This condition - the finite dimensional analogue of the infinite dimensional condition (D) in Takanobu–Watanabe - appears as a generalized “not in cut-locus” condition from Riemannian geometry, and actually allows to derive a full expansion for the marginal density as , of the form

| (3.2) |

expansion of which formula (3.1) captures only the leading-order exponential term (we refer to [12, Theorem 2.8] for an account of the additional term ). In addition to the first order condition of invertibility of the deterministic Malliavin matrix along the minimizing controls in , the condition (ND) in [12] requires to check a second-order condition corresponding to the non-degeneracy of the action along the minimizers. The geometric interpretation is the non-focality of for the arrival subspace . Theorem 3.1 precisely tells that this non degeneracy condition is not necessary in order to establish the asymptotic behaviour of the density on the log-scale as in (3.1).

Proof of Theorem 3.1. Let us establish the upper bound

From the hypotheses in and Theorem 2.1, we know that there exists such that estimate (2.5) holds uniformly on . Write (omitting the fixed index )

| (3.3) |

It follows from estimate (2.5) that for every we can find such that

| (3.4) |

for all and . For such values of , one has

where the last inequality trivially follows from . Therefore,

| (3.5) |

Now, using Proposition 2.4, one has

| (3.6) |

Therefore, taking in (3.3) and using estimates (3.5) and (3.6), one gets

Since was arbitrary, the right hand side can be improved to , as claimed.

The lower bound was already obtained in Proposition 2.15 (see Remark 2.16 for the case where the minimizer is not

unique).

Under strong Hörmander condition, together with , the function is continuous on (see Remark 2.8), and the two functions and coincide everywhere (see Comment 2.3). On the one hand, thanks to the continuity of , estimate (2.5) in Theorem 2.1 holds uniformly over in compact sets of (and not only locally around ). In the proof above, the upper bounds only relies on estimate (2.5) and Proposition 2.4, and can be proven exactly as done above. On the other hand, identity (2.16) in Proposition 2.15 holds, and the proof of Proposition 2.15 can be rerun with no modifications, leading to the lower bound , which proves (3.1).

4 Applications: asymptotics of local volatilities

In this section we focus on the stochastic volatility model

| (4.1) | |||||

where the process models the log-value of a financial asset, and its stochastic volatility.

Setting leads to the familiar “Black-Scholes with stochastic volatility” dynamics .

Here is a two-dimensional Brownian motion with correlated components, in short for some .

can be obtained from a two-dimensional standard Brownian motion by setting , where is a (any) choice of the square root101010A typical choice in this setting is provided by the Cholesky decomposition , with . of the correlation matrix .

Let us note straight away that the diffusion vector fields in (4.1) read

| (4.2) |

While it is clear that the couple spans at every such that (recall is invertible under the assumption ), this condition fails on the set , whatever value the function takes there. The model (4.1) then naturally fits into the non-elliptic framework.

Example 4.1.

A relevant parametric choice of the drift term in (4.1) is given by the affine function , which has the typical mean-reverting form when .

4.1 Extension of main results to Stochastic Volatility models

Postponing for a moment the precise assumptions on the coefficients , let us first describe the different types of asymptotic problems that can arise in the applications. The following class of small-noise equations embeds both small-time and (in some cases) space-asymptotic problems:

| (4.3) | |||||

Here, is a parameter that depends on the asymptotic regime under consideration (we will have in our applications),

and, analogously to (1.13),

| (4.4) |

for some limiting function , in the sense of uniform convergence on compact sets of together with the derivatives of any order. We also assume that the sequence of norms is uniformly bounded in , for every . The associated limiting controlled system reads

| (4.5) | ||||

where is a two-dimensional control and the correlation matrix in (4.1). Let us denote

| (4.6) |

the action of the system (4.5), where .

We assume that the coefficients and satisfy:

-

(SV)

are smooth and Lipschitz functions, with .

The application of Theorem 2.10 to the system (4.3) is a priori not justified, because of the lack of global boundedness for the coefficients of the SDE (and their derivatives). In this respect, let us note that, even if a boundedness assumption were in force for and , the two-dimensional system (4.3) would still not have bounded coefficients (because of the terms and in the equation for the component ). Nevertheless, one can exploit the Lipschitz condition in (SV) (which is rather mild in this setting) in order to extend our main result on the asymptotics of conditional expectations.

Theorem 4.2 (Small noise asymptotics of local volatility: the general case).

Assume condition (SV) on the coefficients and , and denote the unique strong solution to (4.3) with . Fix and , and assume there exist a unique minimizing the action in (4.6) on the set , and that there are finitely many minimizing controls in the set . If one of the following conditions is satisfied:

-

(i)

and ;

-

(ii)

and ;

then, for all functions with polynomial growth,

| (4.7) |

In particular,

| (4.8) |

Finally, if there exist finitely many minimizers for on (each one associated with finitely many minimizing controls ), and one of conditions or is satisfied, then the limits in (4.7) and (4.8) are replaced with , respectively , for some weights such that .

Remark 4.3.

Proof. Let , , and , , be smooth and bounded extensions of , , and respectively (see the Appendix A.1 for a precise definition of such extensions), and denote the unique strong solution to (4.3) when and are replaced with and . Also denote the action function associated to the limiting deterministic system (4.5) with coefficients . Set

On the event , by the pathwise uniqueness for the second equation in (4.3), is indistiguishable from . In addition,

Note that the assumption guarantees that strong Hörmander condition is satisfied at all points for the SDE (4.3): indeed, simple calculations show that

therefore the vectors

span the full (when the assumption is in force).

Denoting , one has

| (4.9) | ||||

where we have used Hölder’s inequality in the last step. We will now show that taking large enough, but fixed, the right hand side tends to zero as .

: Lemma A.1 in Appendix A.1 establishes that can be chosen such that is also the unique minimum point of the function . Assume that Condition is satisfied. The vector fields defined in (4.2) span the whole at the starting point : this is enough to establish, see Lemma 1.4, that the covariance matrix is invertible for all . Otherwise, assume that Condition is satisfied. From the continuity of and the condition in (SV), is bounded away from zero in a neighbourhood of . A simple inspection of the limiting (truncated) controlled system

shows that for all implies . Therefore, the second coordinate of the controlled path must cross the set , where the diffusion vector fields are elliptic, in order to have . Lemma 1.4 then allows to conclude that is invertible for every . In both cases, the hypotheses of Theorem 2.10 are satisfied, yielding as .

: Any optimal control satisfies . Estimate (2.8) in Lemma 2.7 then implies

where is the constant defined in Lemma 2.7, and is a common Lipschitz constant for and . It follows from Theorem 2.10 and the subsequent Remark 2.13 that the law of conditional on converges weakly to a law supported by the finitely many paths . Taking , it is clear that

therefore as well.

: The integral term in also appears in the proof of Corollary 2.11, and can be bounded exactly as done there.

The proof in the case of finitely many minimizers goes through the same steps, using in (4.9) the fact that is also the set of global minimizers of when is large enough (see Lemma A.1 in the Appendix).

4.2 Small-time behavior and Berestycki, Busca and Florent [7] asymptotics of efficient volatility revisited

The short time behavior of the local volatility function obtained as a projection of stochastic volatility was addressed by Berestycki, Busca and Florent [7, section 5], who use local volatility as an intermediate step in the computation of the implied volatility of European options. Using Theorem 4.2, one can give a generalization of their result, stated for stochastic volatility models with bounded and uniformly elliptic coefficients, to hypoelliptic models with unbounded coefficients.

Theorem 4.4.

Assume that the coefficients in (4.1) are smooth and Lipschitz functions with and , and consider the unique strong solution to (4.1). Let be the action function of the system (4.5) when , and , that is

Fix and assume there exists a unique minimizing the function on the line , and that there are finitely many minimizing controls in . Then

| (4.10) |

In the presence of finitely many minimizers , (each one associated with finitely many minimizing controls in ), convergence holds towards a convex combination of the :

| (4.11) |

Proof. For every , the process has the same law as the solution of the SDE (4.3) with

The functions , and clearly satisfy assumption (SV). Therefore, the hypotheses of Theorem 4.2, case , are satisfied, and Theorem 4.4 follows.

Once (4.10) is at hand, proceeding along the lines of [7], one could retrieve the well-known short-time limit for the implied volatility, namely (see [7, Theorem 1.2])

| (4.12) |

where is the Black-Scholes implied volatility of a Call option with maturity and log-moneyness . In this sense, Theorem 4.4 does not yield a refinement of the asymptotics of implied volatility in [7], but rather allows to weaken the hypotheses on the model coefficients. As addressed in Section 3, a more direct way to prove (4.12) would be to use the short-time version of Varadhan’s formula 3.1 for the marginal density of the projection , see Remark 3.2.

Comments on heat kernel expansions and the Laplace method. We compare our approach to Theorem 4.4 to the route followed in Henry-Labordère [25, Chap. 6]. Starting from a small-time heat kernel expansion

| (4.13) |

and assuming that for some , the map has a unique minimizer such that , an heuristic application of the Laplace method yields:

| (4.14) | ||||

in agreement with (4.10). Of course, here we have plugged the expansion (4.13), which is know to hold uniformly on compact sets (that do not intersect the cut-locus), and then integrated on the whole line, neglecting the tail contributions to the integrals in (4.14). The condition , typical from Laplace asymptotics, plays the role of the second-order ‘non-focality’ condition in Deuschel et al. [12, Definition 2.7]. As pointed out in our discussion after Remark 3.2, we do not rely here on such a non-degeneracy assumption. Moreover, the main message of Theorems 4.2 and 4.4 is that the asymptotic behaviour of the logarithm of the density is enough to establish the leading order term of the local volatility function. On the other hand, when a full heat kernel expansion is available as in (4.13), the Laplace method allows to provide higher-order terms in (4.14); see [25, Chap. 6] (where an ellipticity assumption is considered).

4.3 Asymptotic slopes of local volatility in the Stein-Stein model

In the Stein–Stein model [40] (see Schöbel and Zhu [39] for the correlated case ), the volatility process follows an Ornstein-Uhlenbeck process:

| (4.15) | ||||

with , and with .

The typical mean-reverting form of the drift coefficient is obtained when and .

In the following, we consider and (the typical configuration in Equity markets) in order to streamline the computations, but this restriction is not essential.

Setting , the rescaled variables are seen to satisfy the small-noise problem

| (4.16) | ||||

which belongs to the general class (4.3) with , , . Note that as , that is, we are in a situation where the limiting starting point belongs to the sub-elliptic set .

The Hamiltonian system associated to the Stein–Stein model was solved in [13]. For every , the solution of the ODEs (2.6) subject to the boundary conditions

reveal the existence of two minimizing controls , yielding the two (symmetric) arrival points . Full details about explicit computations are found in [13, Section 5.2]; the two minimizers are given by

| (4.17) |

where

| (4.18) |

with and , where

| (4.19) |

and is the smallest strictly positive solution to

| (4.20) |

The equation (4.20) appears when imposing the transversality condition from (2.7).

Remark 4.5.

It is not difficult to show that is the unique solution of equation (4.20) in a bounded interval , which is independent of the model parameters. In practice, can be found using some simple root-finding procedure (such as bisection or Newton method).

Applying Theorem 4.2 and the scaling leading to (4.16), we are able to show that the local variance in the Stein-Stein model is asymptotically linear for large values of , in a similar spirit to Lee’s moment formula [36] for the implied volatility (see also the subsequent refinements in [22]).

Theorem 4.6 (Local volatility ‘wings’ in the Stein–Stein model).

Note that the value of the limit in (4.21) does not depend on the initial volatility , nor on the parameter .

Comment 4.7.

The asymptotic formula (4.21) can be used to patch the numerical evaluation of the local volatility from Dupire’s formula [14], typically affected by numerical instabilities in the region . The use of (4.21), together with the evaluation of in a region where numerics can be trusted (say a fixed, or adaptive, bounded domain in the -plane) leads to a robust and globally defined local volatility surface, that can then serve as the basis for a Monte-Carlo evaluation of exotic option prices, with important consequences for model risk management. An analogous result for the asymptotic slopes of the local variance in the Heston model [26] was given in [11] (where the result (4.21) for the Stein-Stein model was announced), basing on previous work in [16]. Note that the analysis in [11] is based on an implementation of the saddle-point method, and is hence tied to the manipulation of characteristic functions and to the affine structure enjoyed by the Heston model [30]. Our main Theorem 4.2 does not rely on any particular structural assumption on the coefficients of the SDE, and is potentially applicable to families of models larger than the affine class.

Proof of Theorem 4.6. Setting and using the change of variables that leads to (4.16), we have the identity

The last limit above exists, and is equal to the right hand side of (4.21), if the application of Theorem 4.2 is justified. The functions and clearly satisfy assumption (SV). Since the starting point is and the arrival subspaces are , we are in case of Theorem 4.2, and the claim follows.

4.4 Consistency with the Heston model and moment explosion

Some basic Itô calculus shows that when , the Stein–Stein model (4.15) can be obtained as an instance of the Heston model . More precisely, consider a Heston model for the couple log-price/instantaneous variance :

| (4.22) | ||||

where ; and are two Brownian motions with correlation . When the parameters of the Heston model are given by

| (4.23) |

then the couple has same law as , for every (the identity in law actually holds for the entire processes; see [23, Section 2.4] for details). It follows that under the particular parameter configuration (4.23).

As pointed out in Comment 4.7 above, the local variance is know to be asymptotically linear also in the Heston model (with general parameters); from [11, Theorem 1]:

| (4.24) |

where and are the upper resp. the lower critical exponents of , and

| (4.25) | ||||

| (4.26) |

Under the parameter configuration (4.23), the asymptotic behavior (4.24) should be consistent with Theorem 4.6; that is, the two limits should have the same value. Since the two expressions on the right hand sides of (4.21) and (4.24) are hardly assessed at a glance, we carefully check below - as a ‘sanity check’ for our Theorem 4.6 - that the two constants obtained by different methods are indeed equal. Let us choose the sign in (4.24) and (4.21) in what follows; the case with the sign is handled analogously.

Under the condition and in (4.22), the critical exponents for the Heston model is the positive solution of the equation

| (4.27) |

where is the explosion time of the (exponential) moment of order , with

The explosion time can be computed explicitly exploiting the fact that the Heston couple is an affine process; see [30]. Under the condition , is positive for larger than its positive root . It is not difficult to see, then, that (4.27) admits a unique positive solution for any value of .111111 In its turn, the negative exponent is the unique solution of equation (4.27) on , where is the negative root of .

Lemma 4.8.

Define the function for , where is the positive root of . Denote

| (4.28) |

the inverse of the map . Then, is the unique positive solution of equation (4.27) if and only if is the smallest positive solution of the equation

| (4.29) |

Proof. For every , the equation

| (4.30) |

has a unique root . Applying the tangent function to both sides, it is seen that coincides with the set of (infinitely many) solutions to the equation , which is equation (4.29). Using , and , it is easy to see that the smallest positive solution to (4.29) is contained in the interval . On the other hand, using , it is clear that while for ; it then follows that the smallest positive root of (4.29) coincides with the unique root of (4.30) with . Setting , i.e. , it then holds that is the unique positive solution to

which is equation (4.27), therefore . Conversely, if denotes the unique root of (4.27), then , and the claim is proved.

Now consider the particular Heston parameterization in (4.23). Plugging and into (4.28) shows that the function in Lemma 4.8 coincides with the function , with defined in (4.19). Then comparing equations (4.20) and (4.29), it follows from Lemma 4.8 that

| (4.31) |

or yet .

The two constants obtained by different methods are the same. Denote

the asymptotic slopes of local variance as defined in (4.24) and (4.21), where and . Plugging and into , after some simplifications one obtains

with . Substituting inside the expression for in (4.18), reads

| (4.32) | ||||

Repeatedly applying (4.20), one has

| (4.33) | ||||

where we have used the identity (4.31) in the last step. Using (4.33) and again from (4.31), after some straightforward simplifications it follows from (4.32) that

and the proof that is complete.

We stress that our proof of consistency of the two local variance slopes and is valid for negative, non-zero correlation. In the context of implied volatility expansions, a similar consistency result was obtained by [23, p. 187-192], in the zero-correlation case.

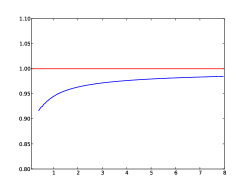

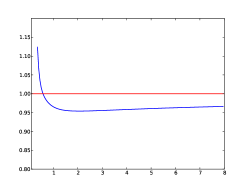

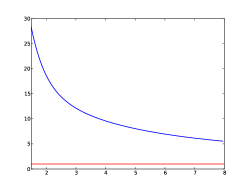

4.5 Numerical tests

In the Heston model, the local volatility can be evaluated using the classical inversion of characteristic functions within the computation of Call price derivatives in the Dupire’s formula .

This gives a way of computing the local volatility in the Stein–Stein model with , simply coinciding with a Heston local volatility, when the Heston parameters are given by (4.23).

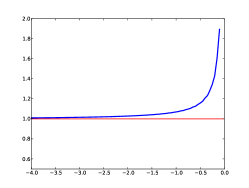

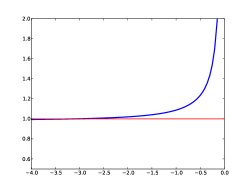

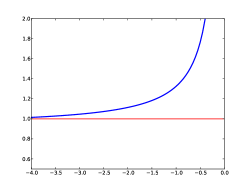

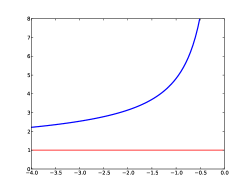

In Figures 1 and 2, we invert the Heston characteristic functions after a shift of the integration contour in the complex plane into an appropriate saddle-point, following the procedure described in [11], in order to obtain a stable implementation of the local volatility function for large values of .

The two figures illustrate the convergence result in Theorem 4.6, for the two regions and : the blue line represents the ratio , which must tend to as .

The empirical asymptotic behavior is in good agreement with formula (4.21), for both the wings: as one expects for a space-asymptotic result, the speed of convergence worsens with increasing maturity (i.e. as the density of the process gradually spreads out).

Note that the adaptive shift of the integration contour into the saddle-point allows to efficiently evaluate for large values of , but while this procedure is (i) relatively time consuming in comparison to any explicit formula, in particular if used on-the-fly inside a Monte-Carlo simulation and (ii) limited to models allowing for an explicit evaluation of Fourier transforms, the analysis behind Theorem 4.6 can be extended to other models.

Appendix A Technical proofs

A.1 Localization

Here we define the precise localization procedure for the SDE (4.3) that is used in Theorem 4.2, and state the lemma about the localization of the action that is used therein. Consider a family of truncation functions , , such that

and set

| (A.1) |

so that for every , the truncated vector fields and coincide with the original ones on the ball , but they remain bounded on (uniformly in in the case of , thanks to assumption (4.4)). If is a common Lipschitz constant for and , then

| (A.2) |

and it is clear that under assumption (SV). It follows that strong Hörmander condition (sH) holds at all points also for the controlled system with truncated coefficients

| (A.3) | ||||

where . Denote , , the action of the system (A.3), with .

Lemma A.1.

Assume and are Lipschitz continuous on . Denote the solution to the ODE (4.5), and the related action as in (4.6). For every , define and according to (A.1), the corresponding ODE solution as in (A.3), and the related action . Let and be fixed as in Theorem 4.2. Then, if at least one of Conditions and of Theorem 4.2 is satisfied:

-

(a)

for every , there exists such that

-

(b)

There exists such that the maps and attain their (common) global minimum at the same points:

Proof. Arguing as in the proof of Theorem 4.2, if at least one of Conditions or is satisfied, the deterministic Malliavin matrix is invertible for all ; it then follows from Lemma 2.7 that is continuous on an open set of containing the line .

Let us prove . Fix , and define . Since is finite and continuous around , is finite and is bounded in . Denote the set of minimizing controls in . It is clear that, for every , , hence , and . Setting

where is the constant defined in Lemma 2.7 and is a Lipschitz constant for and , it follows from estimate (2.8) that for every . Therefore, for such the trajectory , , remains in the region where the vector fields and coincide: from the uniqueness of solutions for the second ODE in (4.5), it follows that for all . Since only depends on , one also has for all , hence for all . In particular, for , and this establishes

| (A.4) |

On the other hand, for some : from (A.4), , therefore by the uniqueness argument above. This implies and , and is proved.

Let us now prove : note that estimate (2.8) in Lemma 2.7, together with the bound (A.2) on the Lipschitz constants of and , implies

| (A.5) |

where again . Set . Estimate (A.5) yields the inclusion , because for every on the left hand side there exists with such that . In particular, all the points are contained in , where is a global minimizer of the map . Now setting , point of the current lemma entails that and coincide on , therefore they - trivially - attain their common minimum on at the same points. One has to make sure that is strictly above the level outside : but (A.5) ensures that can be reached only along controls such that , hence for , and this allows to conclude.

A.2 Proofs of Theorem 2.1 and Proposition 2.4

The following lemma plays a key role. The proof is given under weak Hörmander condition at the starting point :

| (A.6) | ||||

that is, the linear span of and all the Lie brackets of is the whole at . Notice that under assumptions (1.7) and (1.13), one has

hence (wH) also holds when and are replaced with and , when is small enough. It is then classical that admits a smooth density for all under condition (wH).

Lemma A.2.

Let be the solution to (1.3). Assume weak Hörmander condition (wH) at . Then, for any , any and there exist a constant and positive integers and such that

| (A.7) |

for every . The constant also depends on and on the bounds on the derivatives of and the .

Proof. Given in section A.3.

Proof of Theorem 2.1. Let us write for the action function throughout this proof (dropping the fixed index from the notation). The following estimate is obtained with standard uniform large deviations arguments (see also Léandre [34, section 2]): for every , one has

| (A.8) |

uniformly over in compact sets.

Let first prove (2.2). is fixed; taking in estimate (A.7) and applying (A.8), one has

Now taking the limit , by the lower semi-continuity of . Since was arbitrary, (2.2) follows.

Let us now prove (2.5). Under the assumption in Theorem 2.1, it follows from Lemma 2.7 that is continuous on an open neighborhood of , hence uniformly continuous on compact sets contained in . Fix a compact ball and . We can find such that the closed -neighborhood of , , is contained in and moreover for all . In particular,

| (A.9) |

for all . Now taking in estimate (A.7), and applying (A.8) and (A.9), it follows that for any

where the limit holds uniformly over . Since and were arbitrary, the right hand side can be improved to , and (2.5) follows.

The lower bound (2.3) is actually estimate (3.5) in Ben Arous and Léandre [6, Theorem III.1]. Their proof can be adapted to the case where and depend on , under the convergence conditions (1.7) et (1.13). The statement about in Theorem 2.1 is obvious from the definitions of the two actions, and (2.4) is a direct consequence of (2.2) and (2.3).

Proof of Proposition 2.4. It follows from Lemma A.2 that, for every and small enough,

Since

one has

| (A.10) |

The integral on the right hand side of (A.10) can be bounded as follows

| (A.11) |

Note that the random variable has moment of all orders uniformly bounded in (for so does ): precisely, for any and there exists a constant such that for all . Then, from Markov’s inequality

| (A.12) |

for all such that and all . The exponent can be chosen sucht that

for all larger than, say, , for some positive constant . It follows that for any choice of , the integral on the right hand side of (A.11) is convergent, and uniformly bounded in .

Finally taking , multiplying by and taking in (A.10), we have

As , the right hand side tends to : since were arbitrary, we obtain the claim.

A.3 Proof of Lemma A.2

Throughout this section, we denote the strong solution of the SDE

| (A.13) |

where for all . For any multi-index , we denote and . Setting

for smooth real valued functions , we denote and .

Some elements of Malliavin calculus. Following the standard notation in [38], we denote the domain of the -th order Malliavin derivative, and . It is classical, see [38], that is a smooth random variable in Malliavin’s sense for every , that is . Denoting , the (-dimensional) Malliavin derivative of , the -th order derivative is obtained by iterating the operator: , for every . It is well-known that the random variables have finite moments of any order: the following lemma gives an explicit estimate on the norms, in terms of the bounds on and and their derivatives, and will be useful in what follows.

Lemma A.3 (Lemma 2.1 and Corollary 1 in [10]).

For every and there exist positive integers and a positive constant , all depending on but not on the bounds on and and their derivatives, such that, for any

for all and . Moreover,

for any .

The notion of non-degeneracy for (Malliavin-)differentiable random variables is understood in the sense of the (stochastic) Malliavin covariance matrix

A fundamental tool to study density of random variables with invertible covariance matrix is the integration by parts formula:

Proposition A.4 (Integration by parts formula of the Malliavin calculus; [38]).

Let . Assume that is invertible a.s. and moreover for all . Let and . Then, for any and any multi-index there exists a random variable such that

| (A.14) |

where the are recursively defined by

where denotes the adjoint operator of .

The key ingredient required to apply the integration by parts is an estimate of the norms of the Malliavin weights . The following theorem, proved in [10], provides explicit bounds in terms of the bounds on and and their derivatives.

Theorem A.5 (Theorem 2.3 in [10]).

For every , there exist a positive constant and positive integers and , all possibly depending also on and , such that for any multi-index , any and any ,

Let us go back to equation (A.13). If the stochastic integral in (A.13) is intended in Stratonovich sense, the drift coefficient is replaced by . If we assume that the vector field satisfy the weak Hörmander condition at

| (A.15) | ||||

then, denoting the vector space spanned by the Lie brackets of length smaller or equal to in (A.15), and setting121212The sum in (A.16) is in fact taken over a finite number of generating brackets, and it can alternatively be written using the notation introduced in the Appendix of [32].

| (A.16) |

it follows from (A.15) that there exists some such that . In other words,

for some . Under condition (wH) at , the Malliavin covariance matrix satisfies the fundamental estimate of Kusuoka and Stroock [32, Corollary 3.25]: for every and , there exist a constant and an integer such that

| (A.17) |

for all .

We are now ready to give the following

Proof of Lemma A.2. Let be a function. We can construct so that for some constant (eventually depending on the dimension ). Define and consider the Fourier transform of , that is (up to a constant factor)

Since the function is and compactly supported, is integrable and we can use Fourier inversion in order to write

| (A.18) |

On the one hand, it is clear that

| (A.19) |

On the other hand, using , and applying Theorem A.5, we have

| (A.20) | ||||

where . Using Lemma A.3 and the fact that the norms are bounded in , it follows that there exist some such that

| (A.21) |

for every , for some constant .

When the SDE (1.3) is written in Stratonovich form, the drift is replaced by . Noting that contains terms propositional to (coming from the brackets ) and terms proportional to (coming from the brackets ), for small enough one has

Therefore, . Under condition (wH), there exist some such that . Then, it follows from estimate (A.17) that for every and there exist , a function of time and an integer such that

| (A.22) |

for every , where is the Malliavin covariance matrix of .

Now, it follows from (A.21), (A.22) and Theorem A.5 that

| (A.23) |

for every , for some constant also depending on , where and is given in Theorem A.5. Plugging (A.23) into (A.20), one obtains a polynomial estimate for , precisely

| (A.24) |

Finally, using (A.23) and applying (A.19) and (A.24), for every we can write

Choosing large enough (but only dependent on and ), the last integral is convergent. Then, the final claim is proved, once we have set and .

References

- [1] A. Agrachev and P. W. Lee, Continuity of optimal control costs and its application to weak KAM theory, Calc. Var. Partial Differ. Equ., 39 (2010), pp. 213–232.

- [2] I. Bailleul, Large deviation principle for bridges of degenerate diffusion processes. Preprint arXiv, available at http://arxiv.org/pdf/1303.2854.pdf, 2013.

- [3] I. Bailleul, L. Mesnager, and J. Norris, Small time fluctuations for Riemannian and sub-Riemannian diffusions. Preprint, 2013.

- [4] P. Baldi and L. Caramellino, General Freidlin-Wentzell large deviations and positive diffusions, Statistics and Probability Letters, 81 (2011), pp. 1218–1229.

- [5] G. Ben Arous, Développement asymptotique du noyau de la chaleur hypoelliptique hors du cut-locus, Annales scientifiques de l’Ecole Normale Supérieure, 4 (1988), pp. 307–331.

- [6] G. Ben Arous and R. Léandre, Décroissance exponentielle du noyau de la chaleur sur la diagonale (II), Probab. Theory Relat. Fields, 90 (1991), pp. 377–402.

- [7] H. Berestycki, J. Busca, and I. Florent, Computing the implied volatility in stochastic volatility models, Communications on Pure and Applied Mathematics, LVII (2004), pp. 1352–1373.

- [8] J.-M. Bismut, Large deviations and the Malliavin calculus, Birkhäuser, Boston, 1984.

- [9] P. Cannarsa and L. Rifford, Semiconcavity results for optimal control problems admitting no singular minimizing controls, Ann. Inst. H. Poincaré (C) Anal. Non linéaire, 25 (2008), pp. 773–802.

- [10] S. De Marco, Smoothness and Asymptotic Estimates of densities for SDEs with locally smooth coefficients and applications to square root-type diffusions, Annals of Applied Probability, 4 (2011), pp. 1282–1321.

- [11] S. De Marco, P. Friz, and S. Gerhold, Rational Shapes of local volatility, Risk, (February 2013), pp. 82–87.

- [12] J.-D. Deuschel, P. Friz, A. Jacquier, and S. Violante, Marginal density expansions for diffusions and stochastic volatility I: Theoretical foundations, Communications in Pure and Applied Mathematics, (2014), pp. 40–82.

- [13] , Marginal density expansions for diffusions and stochastic volatility II: Applications, Communications in Pure and Applied Mathematics, (2014), pp. 321–350.

- [14] B. Dupire, Pricing with a smile, Risk, (January 1994).

- [15] P. Friz, C. Bayer, and P. Laurence, On the probability density function of baskets, in Large Deviations and Asymptotic Methods in Finance, Springer Proceedings in Mathematics & Statistics, vol. 110, Springer, 2015.

- [16] P. Friz and S. Gerhold, Don’t stay local - extrapolation analytics for Dupire’s local volatility, in Large Deviations and Asymptotic Methods in Finance, Springer Proceedings in Mathematics & Statistics, vol. 110, Springer, 2015.

- [17] P. Friz, S. Gerhold, and M. Yor, How to make Dupire’s local volatility work with jumps, Quantitative Finance, Special Issue: Themed Issue on Financial Models with Jumps, 14 (2014), pp. 1327–1331.

- [18] M. Fukasawa, Short-time at-the-money skew and rough fractional volatility. Preprint ArXiv http://arxiv.org/abs/1501.06980, 2015.

- [19] J. Gatheral, E. Hsu, P. Laurence, C. Ouyang, and T. Wang, Asymptotics of implied volatility in local volatility models, Mathematical Finance, 22 (2012), pp. 591–620.

- [20] J. Gatheral and A. Jacquier, Arbitrage-free svi volatility surfaces, Quantitative Finance, 14 (2014), pp. 59–71.

- [21] J. Gatheral and T.-H. Wang, The heat-kernel most-likely-path approximation, International Journal of Theoretical and Applied Finance, 15 (2012), p. 1250001.

- [22] A. Gulisashvili, Asymptotic formulas with error estimates for call pricing functions and the implied volatility at extreme strikes, SIAM Journal on Financial Mathematics, 1 (2010), pp. 609–641.

- [23] A. Gulisashvili, Analytically Tractable Stochastic Stock Price Models, Springer-Verlag, Berlin-Heidelberg, 2012.

- [24] I. Gyöngy, Mimicking the one-dimensional marginal distributions of processes having an Itô differential, Probab. Th. Rel. Fields, 71 (1986), pp. 501–516.

- [25] P. Henry-Labordère, Analysis, geometry, and modeling in finance: Advanced methods in option pricing. Chapman & Hall/CRC, Financial Mathematics Series, 2008.

- [26] S. Heston, A closed-form solution for options with stochastic volatility with applications to bond and currency options, The Review of Financial Studies, 6 (1993), pp. 327–343.

- [27] N. Ikeda and S. Watanabe, Stochastic Differential Equations and Diffusion Processes, North-Holland Publishing Co., second ed., 1989.

- [28] Y. Inahama, Large deviations for rough path lifts of Watanabe’s pullbacks of delta functions, Int. Math. Res. Notices, (2015).

- [29] V. Jurdjevic, Geometric control theory, Cambridge University Press, Cambridge ; New York, NY, USA, 1997.

- [30] M. Keller-Ressel, Moment explosions and long-term behavior of affine stochastic volatility models, Mathematical Finance, 21 (2011), pp. 73–98.

- [31] S. Kusuoka and Y. Osajima, A remark on the asymptotic expansion of density function of Wiener functionals, Journal of Functional Analysis, special issue dedicated to Paul Malliavin, 255 (2008), pp. 2545–2562.

- [32] S. Kusuoka and D. Stroock, Application of the Malliavin calculus, Part II, Journal of the Faculty of Science of the Univ. of Tokyo Sect IA Math, 32 (1985), pp. 1–76.

- [33] R. Léandre, Intégration dans la fibre associée à une diffusion dégénérée, Probab. Th. Rel. Fields, 76 (1987), pp. 341–358.

- [34] , Majoration en temps petit de la densité d’une diffusion dégénérée, Probability Theory and Related Fields, 74 (1987), pp. 289–294.

- [35] , Minoration en temps petit de la densité d’une diffusion dégénérée, Journal of functional analysis, 74 (1987), pp. 399–414.

- [36] R. W. Lee, The moment formula for implied volatility at extreme strikes, Mathematical Finance, 14 (2004), pp. 469–480.

- [37] S. Molchanov, Diffusion processes and Riemannian geometry, Russian Mathematical Surveys, 30 (1975), pp. 1–63.

- [38] D. Nualart, The Malliavin Calculus and Related Topics, Springer-Verlag, 2006.

- [39] R. Schöbel and J. Zhu, Stochastic volatility with an Ornstein–Uhlenbeck process: An Extension, European Finance Review, 3 (1999), pp. 23–46.

- [40] E. M. Stein and J. C. Stein, Stock price distribution with stochastic volatility: an analytic approach, Review of Financial Studies, 4 (1991), pp. 727–752.

- [41] S. Takanobu and S. Watanabe, Asymptotic expansion formulas of the Schilder type for a class of conditional Wiener functional expectations, in Asymptotic Problems in Probability Theory: Wiener Functionals and Asymptotics, K. D. Elworthy and N. Ikeda, eds., Longman, New York, 1992, pp. 194–241.

- [42] S. Varadhan, Diffusion processes over a small time interval, Comm. Pure Appl. Math., 20 (1967), pp. 659–685.

Comment 2.3.

In light of Lemma 1.4, if span the whole at either or , is invertible at every .

Even when strong Hörmander condition is satisfied at all points, might fail to be invertible on some . But if on a neighborhood of , the two actions and coincide (see the discussion in [6, Section 3], using results from [35, 33]). In this case, (2.4) holds.

In general, the two actions can be different. In [6, Section 1] an example on is given, where strong Hörmander condition is satisfied at all points, but the two actions and do not coincide. As a consequence, the classical Varadhan formula (2.4) does not hold at all points.