Temporal homogenization of linear ODEs, with applications to parametric super-resonance and energy harvest

Abstract

We consider the temporal homogenization of linear ODEs of the form , where is periodic and is small. Using a 2-scale expansion approach, we obtain the long-time approximation , where solves the cell problem with an effective matrix and an explicitly-known . We provide necessary and sufficient condition for the accuracy of the approximation (over a time-scale), and show how can be computed (at a cost independent of ). As a direct application, we investigate the possibility of using RLC circuits to harvest the energy contained in small scale oscillations of ambient electromagnetic fields (such as Schumann resonances). Although a RLC circuit parametrically coupled to the field may achieve such energy extraction via parametric resonance, its resistance needs to be smaller than a threshold proportional to the fluctuations of the field, thereby limiting practical applications. We show that if RLC circuits are appropriately coupled via mutual capacitances or inductances, then energy extraction can be achieved when the resistance of each circuit is smaller than . Hence, if the resistance of each circuit has a non-zero fixed value, energy extraction can be made possible through the coupling of a sufficiently large number of circuits ( for the first mode of Schumann resonances and contemporary values of capacitances, inductances and resistances). The theory is also applied to the control of the oscillation amplitude of a (damped) oscillator.

1 Introduction

1.1 Main mathematical results

Consider time-dependent non-homogeneous linear ODE

| (1) |

on , where is a constant real matrix, is a square-integrable -periodic function taking real matrix values, is a vector-valued function satisfying that is integrable on for some , and .

Our main purpose is to approximate the solution of (1) over a timescale, without resolving oscillations of over that (long) interval of time. Our first result is as follows:

Theorem 1.

Let be the solution of the non-autonomous ODE system (1). If is uniformly bounded in , then there exists a constant matrix , independent of , such that

| (2) |

with

| (3) |

where and, noting the Euclidean 2-norm of , the error ( in (2)) satisfies, for ,

| (4) |

for some constant independent of and . Moreover, can be identified by either

| (5) |

where is defined in Definition 5, or

| (6) |

where the limit exists if and only if is uniformly bounded in .

Theorem 1 shows that if remains uniformly bounded, then up to time , the solution of (1) can be approximated by

| (7) |

The analytical expression in the right side of (7) can be explicitly computed for a large class of ’s (e.g., for polynomial ). acts as an effective matrix characterizing the time-homogenized action of fast periodic oscillations. We provide two methods for the identification of : the first one (5) is algebraic and described in Proposition 9; the second one (6) is computational and described in Proposition 24.

Uniform boundedness of is not only sufficient for the accuracy of the approximation, but also necessary as shown by the following theorem.

Theorem 2.

Consider system (1). Given a constant matrix , define the approximation error

where satisfies (3). If is not uniformly bounded in time, then for any constant matrix independent of , there exists at least one initial condition and a constant (independent of ), such that there is no constant (independent of ) that satisfies

for .

1.2 Mathieu’s equation

Mathieu’s equation is an example that can be expressed as (1), with

It is a prototype for the study of parametric resonance (see Section 3.1). [60], for instance, used averaging and perturbation analysis to capture -time dynamics of the system, and the technique was extended to multi-dimensional oscillators in [22] (see also [18]) and applied in structural engineering for stablization purposes [21]. We also refer to [46, 10, 8, 3, 40, 64, 42] for examples of applications of parametric resonance in science and engineering. Parametric resonance can lead to not only exponential growths of oscillation amplitudes (a well known phenomenon used by children to make a playground swing go higher by pumping their legs) but also exponential decays (see Corollary 15 and its remarks; this aspect appears to have received less attention in the literature).

1.3 Relation with Floquet theory and perturbation analysis

It is in general difficult to obtain a closed-form solution of a non-autonomous system of the form

| (8) |

where is a periodic matrix-valued function.

Floquet theory [24] (known as Bloch’s theorem [6] in physics) shows that the fundamental matrix associated with (8), i.e., the matrix-valued solution of with , satisfies

| (9) |

where is a periodic matrix and is a constant matrix. Although Floquet theory provides important information on the solution structure, it does not, in general, help identify or .

If in our system of interest (1), then is the sum of a constant matrix and a small periodic perturbation, and perturbation analysis [41, 56, 47, 52] can be combined with Floquet theory to obtain a long-time approximation of the fundamental matrix. More precisely, using an asymptotic expansion Ansatz and matching orders yields

| (10) |

At the same time, (9) leads to

where is an integer, and is the period. Let

When , , and a standard local-to-global error analysis leads to

Therefore, when , Floquet theory provides an alternative to Theorem 1.

Now consider the case. It is natural to consider the approximation:

| (11) |

However, there are two issues with this approach:

(i)

(ii)

The error in may (depending on the choice of ) result in an error after integration to in (11). This issue could be addressed by further including a 2nd order term in the approximation , but this comes with the price of more complex calculations.

Note our method approximates the fundamental matrix by, up to ,

| (12) |

whereas the aforementioned perturbative Floquet approach uses (when ),

| (13) |

Since the integral of is small (Lemma 13), (13) could be seen as a 1st-order approximation of (12). Including 2nd-order terms in (13) would improve its accuracy at a price of increased computational complexity, whereas (12) provides a simple high order approximation.

1.4 Relation with averaging

Averaging methods (e.g., [41, 56, 47, 52]) approximate the solution of

| (14) |

by the solution of . These methods can be divided into two categories: (i) when is -periodic in , the effective dynamics can be obtained using

with a upper-error-bound for ; (ii) when is not periodic, the effective dynamics can be obtained using

| (15) |

with a upper-error-bound for under certain additional assumptions (see Definition 4.2.4 and Theorem 4.3.6 of [52]).

When , our approximation can be reproduced by averaging: introduce a change of variables (when has only imaginary eigenvalues, this is a common trick used in perturbation analysis [57]); then system (1) transforms into

| (16) |

Since may be non-periodic in , general averaging theory is required, and it approximates (16) by (when the limit exists)

| (17) |

This limit is identical to (6), and can be shown to be equivalent to our algebraic approach (5) (see Proposition 9 and Section 2.3).

Therefore, in the homogeneous case, the contribution of this paper is not to provide a new approximation but to (i) prove a sharper error bound, (ii) prove that the assumption that remains uniformly bounded in time is both necessary and sufficient for the accuracy of the approximation (17), and (iii) illustrate an algebraic alternative for computing the effect matrix (see Propositions 8 and 9), which could be used as a guiding tool for designing systems with distinct effective dynamics (see Sections 3 and 4).

When , approximation (2) is new. One can still introduce slow variables and show

However, might be exponentially large and this prohibits the application of classical averaging. For example, if and (both scalars), when .

1.5 Relation with classical homogenization

As in classical homogenization theory (e.g., [7, 43, 28, 5]), the constant matrix in Theorem 1 can be seen as an effective matrix capturing the homogenized effect of the periodic perturbation on the dynamics.

Our results are built on a two-scale expansion technique analogous to the one used in classical homogenization theory (see also [29]). One major difference is the lack of ellipticity in (1). See also [25, 16, 20] for homogenization problems involving time (with different systems of interest).

In the special case of , another analogy with classical homogenization is as follows: let , then after rescaling time our system becomes

| (18) |

Let be the matrix-valued solution of

| (19) |

and be the solution of the 1D problem

| (20) |

then it can be shown that . Here (20) is akin to the divergence form PDE used as a prototypical example in classical homogenization theory [7, 43]. Unfortunately, obtaining via (19) is as difficult as solving the original problem (18).

1.6 Other related work

Magnus expansion [34] allows for a representation of the solution of (8) (note has to be 0) as an infinite series of integrals of increasingly many matrix commutators. For practical applications (see [11] for a review), the infinite series has to be truncated to a finite number of terms. In many cases convergence after truncation is not guaranteed or slow (e.g., [12]), and one often faces such problem when studying long time behavior of our system of interest (1).

Alternative strategies become available when additional restrictions are placed on the system (8) or only coarse estimates are needed. For instance, stability theory exists for Lappo-Danilevskii systems (which is a small subclass of (8), characterized by the commutation of with its integrals [2]), or when is almost constant and the constant part is asymptotically stable [2]. There are also loose bounds of the characteristic matrix in (9) (e.g., [62, 63] and IV.6 of [2]). There is also a rich literature on the resolution and analysis of periodic time-dependent Schrödinger equation (e.g., [53, 49, 51]) and, in particular, on the steady state Schrödinger operator with multi-dimensional periodic potentials (e.g., [54, 17, 13]). [61, 14] are examples of reviews. We also refer to [4, 26, 38] for an incomplete list of additional methods.

This article is restricted to linear systems. Only partial results are available for nonlinear systems. For instance, [56, 33] provide nonlinear generalizations of Floquet theory. Nonlinear analogies to parametric resonance (e.g., autoparametric resonance) have been studied using averaging and perturbation analysis [58, 23, 59]; see also [36, 67, 66, 1] for more references. We also refer to [30] for the control of a nonlinear model of double-strand DNA via parametric resonance.

2 Theory

2.1 Algebraic structure

Condition 3.

Let , and be a real-matrix-valued periodic function in . Assume that is a real matrix (not necessarily diagonalizable and, possibly, with complex eigenvalues). Assume without loss of generality that is in Jordan canonical form.

Remark.

Lemma 4.

Under Condition 3, can be uniquely expressed (in sense, which will no longer be stated in the rest of the paper unless confusion arises) as a linear combination (with coefficients being constant real matrices) of and , where for some countable set , in which , and components respectively take values in a finite subset of , a countable subset of , and .

Proof.

As a well-known corollary of Jordan canonical form theory (see for instance [48]), both and can be uniquely expressed as linear combinations of and , where for each triplet , and correspond to the real and imaginary parts of one of eigenvalues, and is less or equal to the number of off-diagonal 1’s in the associated Jordan block.

Also, represent in Fourier series. Since products of and can be uniquely represented as sums of and , the lemma is proved. , and depend on , , , and Fourier coefficients of . ∎

Definition 5 (Growth operator).

Proposition 6.

remains bounded for all , if and only if is time-independent, i.e., when described in the form given by (22), it does not contain or terms.

Proof.

This directly follows from Definition 5. ∎

Remark.

When is diagonalizable and real parts of all its eigenvalues are the same, remains bounded for all . In general, however, whether it is bounded depends not only on but also on entries of .

Proposition 7 (Growth operator is equivalent to time-averaging).

| (23) |

exists if and only if remains bounded for all , and in this case

| (24) |

Proof.

If bounded, can be written as

| (25) |

where and ’s are constant matrices, ’s are constant quasi-periods that not necessarily have a finite least common multiple, and may take finitely-many or countably-many values (depending on whether Fourier series of terminates at finite terms). In this case,

| (26) |

Since and for or , we have

| (27) |

where in the case of infinite summation swapping the limit and infinite sum is justified by dominated convergence.

Proposition 8 (Algebraic calculation of growth operator).

Let . Denote ’s eigenvalues by (assuming ). Let and be the Fourier coefficients of . Let be the set of all nonnegative integers such that (recall is the largest frequency of ). For all , let be the identity matrix of the size of , and

be the canonical symplectic matrix when , and 0 if , also of the size of .

Then, for all pairs. Moreover, under Condition 3 and boundedness of , is of finite size, and , where if ; if ,

| (28) |

Proof.

It is not difficult to see from its definition that is a linear operator and .

Since is bounded, each term in that possibly persists after the application of is a product of at most 3 trigonometric functions (decaying components will be removed). Let their frequencies be respectively , , and . This product yields a non-zero constant term if and only if . Since only the constant terms will persist after the application of , it is sufficient to consider only -modes in the Fourier expansion of with , i.e.,

where

When , by the definition of , . When , boundedness of ensures , and therefore too.

Now consider only the case of . Since boundedness of rules out presence of ,

where ’s are matrices in canonical Jordan form with eigenvalues without ’s off-diagonal blocks, i.e.,

Therefore,

It can be computed by basic trigonometric identities that (for arbitrary parameters )

and hence we have (28). ∎

Proposition 9 (Algebraic calculation of effective matrix).

Under Condition 3, denote ’s Jordan blocks by . Let be the eigenvalue(s) associated to . Let be the set of all nonnegative integers such that . Then is a finite set, and expressing in the same block division as , we have that

-

•

, if .

-

•

, if and .

-

•

, if and .

-

•

, if and the representation of obtained from Lemma 4 contains terms in with .

- •

Observe that the presence of terms in with in the representation of obtained from Lemma 4 can be checked analytically. If this representation does not contain such elements, the case is characterized by only a finite number of Fourier coefficients of . Therefore, whether exists can be checked and its exact expression can be obtained, both in a number of computational steps independent from .

2.2 Preparatory analysis

Lemma 10.

For fixed or , if , the following integrals have asymptotic behavior

in the sense that if and only if

Proof.

(i) When , recall that the upper incomplete gamma function is defined as

Therefore,

Note that , when fixed, large and , has asymptotic behavior (e.g., [19])

Therefore,

(ii) When , integration by parts gives

when is large. That is, the same expression in (i) works.

(iii) A procedure similar to (i) and (ii) shows

∎

Definition 11.

Lemma 12.

Given constant vectors and , the solution of ODE

| (30) |

remains bounded if and only if

| (31) |

Proof.

By Lemma 4, we can assume that

| (32) |

for some sets and , and nonzero vectors , . We adopt the convention that so that this decomposition is unique.

Consider the solutions and to

Naturally, when , the solutions will not remain bounded. When and (recall ), they will not be bounded either. When and , remains bounded if and only if , and is bounded for and undefined for .

Note is the unique solution to (30). If all and remain bounded, so do ; on the other hand, if some and/or are unbounded, will be unbounded too, because cancelation will not happen due to different growth rates of and .

Hence, the necessary and sufficient condition for bounded is and being subsets of (note is meaningless for ), which by Definition 11 is equivalent to

| (33) |

∎

Lemma 13.

Let . Then there exists a constant such that for all . Furthermore, it has an antiderivative (i.e., ) such that for all too.

Proof.

By the definition of growth operator

| (34) |

Since is bounded for and , and and are bounded for real and , for some constant for all .

Moreover, when , antiderivatives of and are bounded. As for terms, we note the indefinite integral of converges because (i) the integrand is positive, and (ii) as . Therefore, the antiderivative of remains bounded as , because it is bounded by the indefinite integral of .

Therefore, for all too. ∎

2.3 Temporal homogenization

Heuristic derivation.

The intuition behind Theorem 1 lies in the introduction of the 2-scale asymptotic expansion ansatz, popular in perturbation analysis and classical homogenization (see, for instance, [41] or [7]):

| (35) |

where and correspond to slow and fast timescales, and are treated as independent variables as ; ’s are such that for at least as .

Due to the separation of timescales, formally differential operator . Consequently, (1) can be written as

| (36) |

Plot the expansion of (Eq. 35) into the above PDE. Matching terms leads to

| (37) |

and matching terms leads to

| (38) |

Let , then we have

| (41) |

where .

To satisfy , we require to be bounded by a constant independent of . Formally, let

| (42) |

Make a decomposition , where

Since and are independent variables as , , and are viewed as constant vectors at the fast timescale of . By definition of , is bounded as ; at the same time, Lemma 31 suggests is bounded if and only if , which leads to (see Definition 5):

| (43) |

When is bounded, is a constant (denoted by ), and is a function of only, consistent with the ansatz of scale separation. Going back to original time variable , the above equation is

| (44) |

However, one problem remains: does the right side of (42) have a limit as ? Rather than imposing extra restrictions on (such as it is fast/slow), we prefer a general result, and heuristically replace the cell problem (44) by

| (45) |

We then prove the effective solution (39) generated by this still has small error.

Rigorous justification.

Proof of Theorem 1.

Let , then

Since is bounded, is a constant. Let it be . Consider

Let and . Then

Let , then

| (46) |

where

Treat as fixed for now and let . Then

where prime means derivative with respect to .

Let be the antiderivative of defined in Lemma 13. Then

Note , , and hence all remain bounded till . Also, remains bounded for all time by Lemma 13. Therefore,

for and some constants . Since

and is bounded by assumption, there is some such that

Similarly, we have

| (47) |

Let . It can be analogously shown that

for some . Rearranging terms in (47), we obtain

Let . Since remains bounded till at least , we have

Gronwall’s inequality gives

∎

Remark.

The relative error is quantified in (4) by comparing the absolute error with the approximated solution after an appropriate scaling.

Remark.

The inhomogeneous term may not be small nor periodic. When it is, it can be homogenized. This can be done in our framework by concatenating with an extra dummy variable , with , , and replaced by .

The following corollary shows that, in the homogeneous case, one can drop the term in (1) without loss of accuracy if does not oscillate at a resonant frequency (defined as the difference between the imaginary parts of two eigenvalues of ). Unlike Theorems 1 and 2, this is only a sufficient condition.

Corollary 14.

Consider system (1). Assume without loss of generality that the Fourier expansion of does not contain constant terms (such terms can be absorbed into ), and denote by the smallest period of . Suppose . Assume that is diagonalizable and that all its eigenvalues (indicated by ) have the same real part (i.e., for all )111An example is a mechanical system subject to isotropic dissipation and with bounded trajectory.. If there is no integer such that

| (48) |

for some , then

with

| (49) |

for some constant independent from and when .

Proof of Theorem 2.

Let . Since is unbounded in , when written in canonical form (Lemma 4), it contains at least one or term with either or . Choose that correspond to the fastest growing term. The proof is by contradiction:

Suppose there exists a constant matrix , independent of the choice of , such that for all initial condition and all for some ,

for some . Then the above should hold for a particular choice of . In this case,

and therefore as long as ,

As before, we have

| (50) |

where satisfies and .

Variation of constants leads to

Rearranging terms, we have

| (51) |

Assume without loss of generality and choose , then right hand side (RHS) of (51) satisfies

Lemma 10 leads to

On the other hand, the left hand side (LHS) of (51) is

Write in Jordan canonical form , where

’s are eigenvalues, superdiagonal elements ’s are either 0 or 1, and is orthonormal. Then

Let . Since the conjugate transform preserves the matrix norm, , when written in canonical form, still has at least one element that contains an or term. Because LHS of (51) is a linear functional of , assume without loss of generality that

for some (the case is completely analogous). Also, let , then

For notational convenience, let

Suppose and are respectively located in in -by- and -by- Jordan diagonal blocks

Isolate the corresponding -by- blocks in and and call them and . Then

Let be the new location of in submatrix . Consider

then

Either is still at the order of (in ) as is, or some later term cancels this leading order.

If the latter case (cancellation), because , must be at this leading order too. In this case, choose a new to be , and repeat the above procedure.

Because is always true, this procedure will terminate eventually. In the end, there will be some such that is at the order of .

Now, pick -dimensional vector , where the only nonzero element is in column . Pick by padding with 0 elements, such that the location of in corresponds to the location of in . If we introduce notation

then .

Using the upper triangular matrix structure again, an analogous argument shows

also contains an element at the leading order of . Lemma 10 implies also contains an element at this leading order (up to a constant prefactor due to the factor involved in time integral), and therefore so does .

Since is orthonormal and hence vector-norm preserving,

and it is at least at the order of . Since

when is small enough, (51) cannot be an equality. This is a contradiction, and hence does not exist. ∎

3 Application 1: Control via parametric resonance

3.1 Parametric resonance in a variant of Mathieu’s equation

Consider the system

| (52) |

Without the additional phase , this is Mathieu’s equation, which is known to correspond to parametric resonance (PR for short; see [39, 27, 24] for seminal discussions on Mathieu’s equation and its generalization known as Hill’s equation, with motivations in celestial mechanics; see also [63, 32, 35] for some more modern reviews).

This system corresponds to the canonical form (1) with

A direct computation gives

This matrix has trace and determinant, and therefore

Hence, we have, till at least ,

| (53) |

Corollary 15 (Exponential decay).

When ,

till at least .

Proof.

Since and for all , it suffices to show the equivalency of , and .

This is immediate upon using basic trigonometric identities , and . ∎

Remark.

Although parametric resonance oftentimes leads to exponentially growing oscillations, it may, as observed in [32], also lead to exponentially decaying solutions. For a 2-dimensional periodic linear ODE system (52) with trace-free time-averaged coefficient matrix, Floquet theory (see for instance [57]) guarantees that exponentially growing and decaying solutions always come in pairs. Corollary 15 shows how to obtain this decaying solution. Note that the decay can either be achieved by a careful choice of initial condition (such that ), or by adding a phase in the perturbation to adjust to arbitrary initial condition.

Remark.

For such that , when is large will be dominated by exponentially growth. However, when , it can be shown that decays when is not too large; this is why the proposed method of control (see Section 3.2) is robust to small perturbations in caused by implementation errors.

3.2 Control of oscillations

Given a smooth enough, positive-valued function , our purpose is to control the amplitude of the oscillations of the solution of

| (54) |

so that it follows approximately . We will achieve this control by changing the values of and over a finite number of time intervals.

Assumption:

We will assume that is slowly varying when compared to the time scale , i.e., that and

| (55) |

and

| (56) |

for all , where is the end time of the control.

The following algorithm describes how the solution of (54) can be controlled by changing values of and on time intervals of length .

Algorithm 16 (Control of oscillations by parametric resonance).

-

•

Let , where is a pre-set constant ( in this paper).

-

•

At each time step, i.e., for , compute ; Let and .

-

•

If , let and for .

-

•

If , let and for .

-

•

and iterate until .

This algorithm works in the sense that it leads to a solution such that for all . The idea is to approximate by a piecewise-exponential function with piece-width .

The condition given by (56) ensures that changes very little within a step of length , so that it is well approximated by a piecewise-linear function with piece-width .

The condition given by (55) leads to

That is, if , then . Therefore, as Corollary 15 shows, the choice of in the algorithm enables a decrease of oscillation amplitude from at step to at step (or increase by an analogous reason). Furthermore, since , the envelope of is close to a piecewise-linear approximation of .

In addition, since we use but not , the approximation error from the previous step will not affect the current step.

Remark.

Numerical illustration:

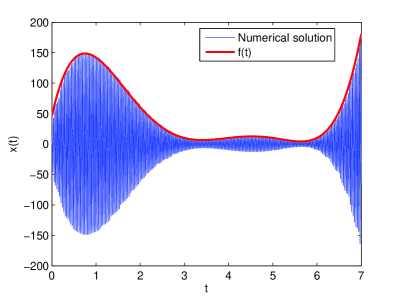

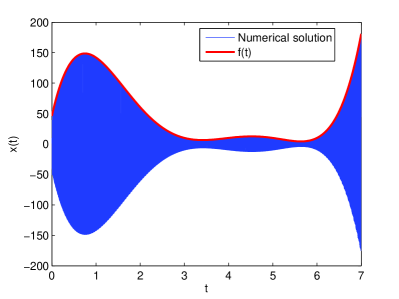

We arbitrarily chose a function to demonstrate Algorithm 16. is chosen to be a high degree polynomial so that its graph is nontrivial, and the constant is chosen such that for all .

As can be seen from Figure 1, control is achieved in the sense that the oscillation amplitude of approximates when is big enough. The initial condition is and . Even though significantly differs from , the amplitude rapidly converges to (at rate , and therefore barely observable in Figure 1(a)). Naturally, larger (and hence smaller ) leads to more accurate match. Longer simulation times do not degrade the quality of the approximation; however they obscure important details of the results (because is large and rapidly increasing when is large), hence we have truncated the plot at .

3.3 The initialization problem

One drawback of PR is if initially the oscillator contains no initial energy ( in (52)) then parametric excitation has no effect. A remedy is to also add a nonparametric perturbation (). For instance, if

an growth in the solution can be demonstrated by Theorem 1. This growth is due to the interaction between the small periodic and the nonparametric perturbations, because if either or is zero then the solution will not grow.

4 Application 2: Energy harvest via parametric super-resonance and coupled RLC circuits

Consider the effect of time-periodic oscillations in inductance or capacitance on the dynamic of RLC circuits. For example, suppose that the capacitance fluctuates according to , where . It is known that the dynamic of such circuits is characterized by parametric resonance if , where is the intrinsic frequency of the oscillator. It can also be shown that, if and then the energy injected into the circuit by parametric resonance overcomes the dissipation induced by , and the energy stored in circuit grows exponentially (see [37] for early experiments).

This phenomenon could, in principle, be used for energy harvesting. For instance, the earth-ionosphere behaves like a dielectric cavity with specific resonant frequencies. This leads to small oscillatory fluctuations in the ambient electromagnetic field at these frequencies [50]. Since these oscillations can result (through nonlinear effects) in oscillations of circuit parameters, one natural question is the possibility of extracting the energy of these oscillations by tuning the intrinsic frequency of the circuit to hit parametric resonance (such questions can be traced back to Tesla’s investigations on energy harvesting [55]).

The main limitation on the implementation of single parametrically-resonant circuit for harvesting energy is that the amplitude of induced parametrical fluctuations is usually too small to compensate the dissipative effect of the resistance ( is needed for the compensation). We will use the temporal homogenization framework developed here to show that a large number of such circuits can, under the right coupling, overcome the dissipation.

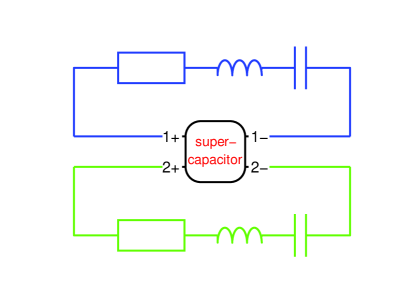

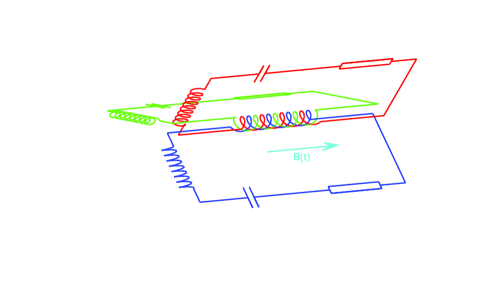

Coupled RLC circuits.

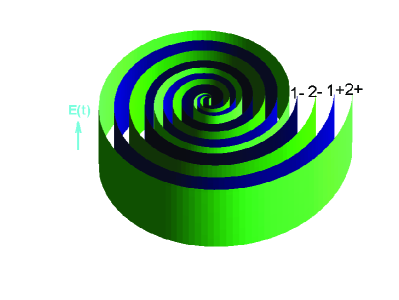

Consider RLC circuits as illustrated in Figure 2(a), coupled through the supercapacitor illustrated in Figure 2(b). This supercapacitor is analogous to a wound film capacitor (e.g., [9]), where alternating conductive layers and dielectric layers are wound together, and it generates an electromotive force according to the sum of currents in all circuits, yet keeping these circuits insulated from each other.

Due to the electrostriction property of dielectrics (e.g., [65]), the ambient electric field introduces a small periodic variation in the capacitance of this supercapacitor. This variation could be further enhanced, for instance, by attaching positive and negative charges respectively to two edges of electrodes via stiff nonconducting materials, which will stretch/compress the conducting plates according to the ambient electric field, and consequently change the capacitance (recall that parallel-plate conductor has a capacitance proportional to the plate area).

Denote by the current in the circuit. Assume the supercapacitor is symmetric with respect to permutations of electrodes (this is approximately true if sufficiently many turns are wound), such that the voltage difference across the public supercapacitor satisfies

| (57) |

where for some . Meanwhile, the voltage differences across the capacitor, inductor, and resistor of sub-circuit respectively satisfy

Kirchoff law of leads to the following dynamics:

Remark.

The model described here is conceptual. For example, the choice of constant and is based on the assumption that the ambient electromagnetic fluctuations are sustained by an infinite energy reservoir. Also, when is large, it is an engineering challenge to pack all layers into a supercapacitor.

Parametric super-resonance.

For simplicity, consider identical circuits, i.e., , , . Let , then . Let , then

We will show that, provided , the solution grows exponentially if

| (58) |

which is satisfied when (the number of coupled circuits) is large enough.

Lemma 17.

Proof.

Once the form of is obtained, the rest can be checked by simple algebra. ∎

Lemma 18.

Let . If , then

| (59) |

Proof.

Corollary 19.

Given for some dimensional linear subspace , is unbounded if and only if .

Proof.

Substitution of Lemma 59 in Theorem 1 leads to (as seen in the proof of Theorem 1, ignoring the term in the equation does not affect the leading term in the solution):

Since eigenvalues of are , real parts of eigenvalues of the above approximate solution operator are and . The solution will be dominated by exponential growth if and only if , unless projects to zero in the direction of the eigenvector associated with its eigenvalue. ∎

Remark.

As initial conditions that do not lead to unbounded growth are of measure zero, in practice it is unlikely that they will hamper energy harvest. To entirely avoid this possibility, one can add to the system an ‘ignition’, which is a short period forcing term (see section 3.3).

On the constitutive variable capacitor equation.

Using the equation instead of (57) to model the shared supercapacitor leads to similar results, i.e. an exponential growth of the solution is achieved when and is large enough. To sketch this calculation, note the system can be shown to be governed by

which can be written in canonical form (up to ) by letting ,

The following and lead to block-diagonal (with block sizes of ):

| where | |||

Once and are explicitly identified, it can be computed that

whose eigenvalue of resonates with the parametric perturbation, and that

Then parametric super-resonance can again be demonstrated by temporal homogenization.

A preliminary analysis of practical feasibility.

The first mode of ambient electromagnetic fluctuations has its peak around 8Hz, with an electric field amplitude at the order of (c.f., static fair-weather electric field is about ) [50]. This means is fixed and , and it is reasonable to assume to be at the order of or . We look for circuit parameters that satisfy

| (60) |

Contemporary technologies can provide compact (super)capacitors [15] and inductors with values ranging from F to F and H to H. Writing , it is also reasonable to assume and constraints for some positive parameter . Since , (60) can be satisfied if leading order terms (in ) match, i.e.,

This linear programming problem is feasible when . We choose to minimize in order to maximize the circuit gain, and then one solution is , , , . When , this corresponds to parameters:

When , this design requires the coupling of circuits to achieve energy gain.

Although this preliminary analysis gives some indications on the workability of energy harvesting via super-resonance, it is by far incomplete, and a comprehensive feasibility analysis would require addressing possibly difficult engineering challenges such as (1) identifying workable physical configurations for packing a large number of layers into a supercapacitor and a large number of circuits around that supercapacitor (2) keeping the financial cost of the system limited. These investigations are beyond the scope of this article.

Alternative design.

We also note that similar scaling effects can also be achieved by coupling inductors. See Figure 3 for an illustrative design. Inductance can be coupled to ambient magnetic fluctuations if, for instance, the inductors have a ferromagnetic core.

Acknowledgments

This work was supported by NSF grant CMMI-092600, a generous gift from UTRC, and Courant Instructorship from New York University. We thank Wei Mao for knowledge in engineering aspects of Amplitude Modulation, Gérard Ben Arous, Emmanuel Frenod, Jonathan Goodman, Robert Kohn for stimulating mathematical discussions, and anonymous referees for helpful comments.

References

- [1] G. Abraham and A. Chatterjee, Approximate asymptotics for a nonlinear mathieu equation using harmonic balance based averaging, Nonlinear Dynamics, 31 (2003), pp. 347–365.

- [2] L. Y. Adrianova, Introduction to Linear Systems of Differential Equations, American Mathematical Society, 1995.

- [3] E. Akhmedov, A. Dighe, P. Lipari, and A. Smirnov, Atmospheric neutrinos at super-kamiokande and parametric resonance in neutrino oscillations, Nuclear Physics B, 542 (1999), pp. 3 – 30.

- [4] M. S. Alam, Unified Krylov-Bogoliubov-Mitropolskii method for solving nth order non-linear systems with slowly varying coefficients, Journal of Sound and Vibration, 265 (2003), pp. 987–1002.

- [5] G. Allaire, Homogenization and two-scale convergence, SIAM J. Math. Anal., 23 (1992), pp. 1482–1518.

- [6] N. W. Ashcroft and N. D. Mermin, Solid State Physics, Harcourt, 1976.

- [7] A. Bensoussan, J. L. Lions, and G. Papanicolaou, Asymptotic analysis for periodic structure, North Holland, Amsterdam, 1978.

- [8] J. Berges and J. Serreau, Parametric resonance in quantum field theory, Phys. Rev. Lett., 91 (2003), p. 111601.

- [9] A. Bhattacharyya, W. Chu, J. Howard, and F. Wiedman, Method for manufacture of ultra-thin film capacitor, June 8 1982. US Patent 4,333,808.

- [10] J. P. Blanchard and C. F. Blackman, Clarification and application of an ion parametric resonance model for magnetic field interactions with biological systems, Bioelectromagnetics, 15 (1994), pp. 217–238.

- [11] S. Blanes, F. Casas, J. Oteo, and J. Ros, The Magnus expansion and some of its applications, Physics Reports, 470 (2009), pp. 151 – 238.

- [12] S. Blanes, F. Casas, J. A. Oteo, and J. Ros, Magnus and Fer expansions for matrix differential equations: the convergence problem, Journal of Physics A: Mathematical and General, 31 (1998), p. 259.

- [13] R. Carlson, Compactness of Floquet isospectral sets for the matrix Hill’s equation, Proc. Amer. Math. Soc., 128 (2000), pp. 2933–2941.

- [14] S.-I. Chu and D. A. Telnov, Beyond the Floquet theorem: generalized Floquet formalisms and quasienergy methods for atomic and molecular multiphoton processes in intense laser fields, Physics Reports, 390 (2004), pp. 1 – 131.

- [15] B. E. Conway, Electrochemical Supercapacitors: Scientific Fundamentals and Technological Applications, Springer US, 1999.

- [16] J. Cooper, Parametric resonance in wave equations with a time-periodic potential, SIAM Journal on Mathematical Analysis, 31 (2000), pp. 821–835.

- [17] B. Despres, The Borg theorem for the vectorial Hill’s equation, Inverse Problems, 11 (1995), p. 97.

- [18] M. Devaud, V. Leroy, J.-C. Bacri, and T. Hocquet, The adiabatic invariant of the n -degree-of-freedom harmonic oscillator, European Journal of Physics, 29 (2008), p. 831.

- [19] NIST Digital Library of Mathematical Functions. http://dlmf.nist.gov/, Release 1.0.8 of 2014-04-25. Online companion to [44].

- [20] M. Dobson, C. Le Bris, and F. Legoll, Symplectic schemes for highly oscillatory Hamiltonian systems: the homogenization approach beyond the constant frequency case, IMA J. Numer. Anal., 33 (2013), pp. 30–56.

- [21] F. Dohnal, Optimal dynamic stabilisation of a linear system by periodic stiffness excitation, Journal of Sound and Vibration, 320 (2009), pp. 777–792.

- [22] F. Dohnal and F. Verhulst, Averaging in vibration suppression by parametric stiffness excitation, Nonlinear Dynamics, 54 (2008), pp. 231–248.

- [23] S. Fatimah and M. Ruijgrok, Bifurcations in an autoparametric system in 1: 1 internal resonance with parametric excitation, International journal of non-linear mechanics, 37 (2002), pp. 297–308.

- [24] G. Floquet, Sur les équations différentielles linéaires à coefficients périodiques, Ann. École Norm. Sup., 12 (1883), pp. 47–88.

- [25] J. Garnier, Homogenization in a periodic and time-dependent potential, SIAM Journal on Applied Mathematics, 57 (1997), pp. 95–111.

- [26] T. Grozdanov and M. Raković, Quantum system driven by rapidly varying periodic perturbation, Phys. Rev. A, 38 (1988), p. 1739.

- [27] G. W. Hill, On the part of the motion of lunar perigee which is a function of the mean motions of the sun and moon, Acta Math., 8 (1886), pp. 1–36.

- [28] V. V. Jikov, S. M. Kozlov, and O. A. Oleinik, Homogenization of Differential Operators and Integral Functionals, Springer-Verlag, Berlin, 1994.

- [29] J. Kevorkian and J. D. Cole, Multiple scale and singular perturbation methods, vol. 114 of Applied Mathematical Sciences, Springer-Verlag, New York, 1996.

- [30] W.-S. Koon, H. Owhadi, M. Tao, and T. Yanao, Control of a model of dna division via parametric resonance, Chaos, 23 (2013).

- [31] S. M. Kozlov, The averaging of random operators, Mat. Sb. (N.S.), 109(151) (1979), pp. 188–202, 327.

- [32] L. Landau and E. Lifshitz, Mechanics, Elsevier, 3rd ed., 1976.

- [33] W. Li, J. Llibre, and X. Zhang, Extension of Floquet’s theory to nonlinear periodic differential systems and embedding diffeomorphisms in differential flows, American Journal of Mathematics, 124 (2002), pp. 107–127.

- [34] W. Magnus, On the exponential solution of differential equations for a linear operator, Comm. Pure Appl. Math., 7 (1954), pp. 649–673.

- [35] W. Magnus and S. Winkler, Hill’s equation, Dover, 2004.

- [36] G. Mahmoud and S. Aly, On periodic solutions of parametrically excited complex non-linear dynamical systems, Physica A: Statistical Mechanics and its Applications, 278 (2000), pp. 390–404.

- [37] L. Mandelstam, N. Papalexi, A. Andronov, S. Chaikin, and A. Witt, Exposé des recherches récentes sur les oscillations non linéaires, Technical Physics of the USSR, Leningrad, 2 (1935), pp. 81–134. Report on Recent Research on Nonlinear Oscillations, NASA Translation Doc. TTF-12,678, Nov. 1969.

- [38] M. Maricq, Application of average Hamiltonian theory to the NMR of solids, Phys. Rev. B, 25 (1982), pp. 6622–6632.

- [39] E. Mathieu, Mémoire sur le mouvement vibratoire d’une membrane de forme elliptique, J. Math. Pures Appl., 13 (1868), pp. 137–203.

- [40] C. C. Mei and X. Zhou, Parametric resonance of a spherical bubble, Journal of Fluid Mechanics, 229 (1991), pp. 29–50.

- [41] A. H. Nayfeh, Perturbation methods, Wiley, 1973.

- [42] T. Ng, K. Lam, and K. Liew, Effects of fgm materials on the parametric resonance of plate structures, Computer Methods in Applied Mechanics and Engineering, 190 (2000), pp. 953 – 962.

- [43] G. Nguetseng, A general convergence result for a functional related to the theory of homogenization, SIAM J. Math. Anal., 20 (1989), pp. 608–623.

- [44] F. W. J. Olver, D. W. Lozier, R. F. Boisvert, and C. W. Clark, eds., NIST Handbook of Mathematical Functions, Cambridge University Press, New York, NY, 2010. Print companion to [19].

- [45] G. C. Papanicolaou and S. R. S. Varadhan, Diffusions with random coefficients, in Statistics and probability: essays in honor of C. R. Rao, North-Holland, Amsterdam, 1982, pp. 547–552.

- [46] W. Paul and H. Steinwedel, Ein neues massenspektrometer ohne magnetfeld, Zeitschrift Naturforschung Teil A, 8 (1953), p. 448.

- [47] G. A. Pavliotis and A. M. Stuart, Multiscale methods, vol. 53 of Texts in Applied Mathematics, Springer, New York, 2008. Averaging and homogenization.

- [48] L. Perko, Differential equations and dynamical systems, Springer, 2001.

- [49] U. Peskin and N. Moiseyev, The solution of the time-dependent Schrödinger equation by the (t,t’) method: Theory, computational algorithm and applications, J. Chem. Phys., 99 (1993), p. 4590.

- [50] C. Price, O. Pechony, and E. Greenberg, Schumann resonances in lightning research, J. of Lightning Res, 1 (2007), pp. 1–15.

- [51] S. Rahav, I. Gilary, and S. Fishman, Time independent description of rapidly oscillating potentials, Phys. Rev. Lett., 91 (2003), p. 110404.

- [52] J. A. Sanders, F. Verhulst, and J. Murdock, Averaging Methods in Nonlinear Dynamical Systems, Springer, 2010.

- [53] J. H. Shirley, Solution of the Schrödinger equation with a Hamiltonian periodic in time, Phys. Rev., 138 (1965), pp. B979–B987.

- [54] M. Skriganov, The spectrum band structure of the three-dimensional Schrödinger operator with periodic potential, Inventiones mathematicae, 80 (1985), pp. 107–121.

- [55] N. Tesla, Experiments with alternate currents of high potential and high frequency, Cosimo, Inc., 2007. Originally in 1892. Page 58.

- [56] P. A. Vela, Averaging and Control of Nonlinear Systems, PhD thesis, California Institute of Technology, 2003.

- [57] F. Verhulst, Nonlinear Differential Equations and Dynamical Systems, Springer, Berlin-Heidelberg Germany, second ed., 1996.

- [58] F. Verhulst, Parametric and autoparametric resonance, Acta Applicandae Mathematicae, 70 (2002), pp. 231–264.

- [59] , Autoparametric resonance of relaxation oscillations, ZAMM-Journal of Applied Mathematics and Mechanics/Zeitschrift für Angewandte Mathematik und Mechanik, 85 (2005), pp. 122–131.

- [60] , Perturbation analysis of parametric resonance, Encyclopedia of Complexity and Systems Science. Springer-Verlag, (2009).

- [61] R. M. Wilcox, Exponential operators and parameter differentiation in quantum physics, J. Math. Phys., 8 (1967), p. 962.

- [62] V. A. Yakubovich and V. M. Starzhinskii, Linear differential equations with periodic coefficients (volume 1), Wiley, New York, 1975.

- [63] , Linear differential equations with periodic coefficients (volume 2), Wiley, New York, 1975.

- [64] J. Yang and H.-S. Shen, Free vibration and parametric resonance of shear deformable functionally graded cylindrical panels, Journal of Sound and Vibration, 261 (2003), pp. 871 – 893.

- [65] Q. Zhang, V. Bharti, and X. Zhao, Giant electrostriction and relaxor ferroelectric behavior in electron-irradiated poly (vinylidene fluoride-trifluoroethylene) copolymer, Science, 280 (1998), pp. 2101–2104.

- [66] W. Zhang, R. Baskaran, and K. Turner, Effect of cubic nonlinearity on auto-parametrically amplified resonant mems mass sensor, Sensors and Actuators A: Physical, 102 (2002), pp. 139–150.

- [67] R. Zounes and R. Rand, Subharmonic resonance in the non-linear mathieu equation, International journal of non-linear mechanics, 37 (2002), pp. 43–73.